4

Belief Perseverance Bias #2: Conservatism Bias

To invest successfully over a lifetime does not require a stratospheric IQ, unusual business insight, or inside information. What's needed is a sound intellectual framework for decisions and the ability to keep emotions from corroding that framework.

—Warren Buffett

Bias Description

Bias Name: Conservatism

Bias Type: Cognitive

Subtype: Belief perseverance

General Description

Conservatism bias is a mental process in which people cling to their prior views or forecasts at the expense of acknowledging new information. For example, suppose that an investor receives some bad news regarding a company's earnings and that this news negatively contradicts another earnings estimate issued the previous month. Conservatism bias may cause the investor to underreact to the new information, maintaining impressions derived from the previous estimate rather than acting on the updated information investors persevere in a previously held belief rather than acknowledging new information; this is again a variation on the cognitive dissonance theme described in the last section.

Example of Conservatism Bias

James Montier is author of the book Behavioural Finance: Insights into Irrational Minds and Markets1 and an analyst for DKW in London. Montier has done some exceptional work in the behavioral finance field. Although Montier primarily studied the stock market in general, concentrating on the behavior of securities analysts in particular, the concepts presented here can and will be applied to individual investors later on.

Commenting on conservatism as it relates to the securities markets in general, Montier noted: “The stock market has a tendency to underreact to fundamental information—be it dividend omissions, initiations, or an earnings report. For instance, in the United States, in the 60 days following an earnings announcement, stocks with the biggest positive earnings surprise tend to outperform the market by 2 percent, even after a 4 to 5 percent outperformance in the 60 days prior to the announcement.”

In relating conservatism to securities analysts, Montier wrote:

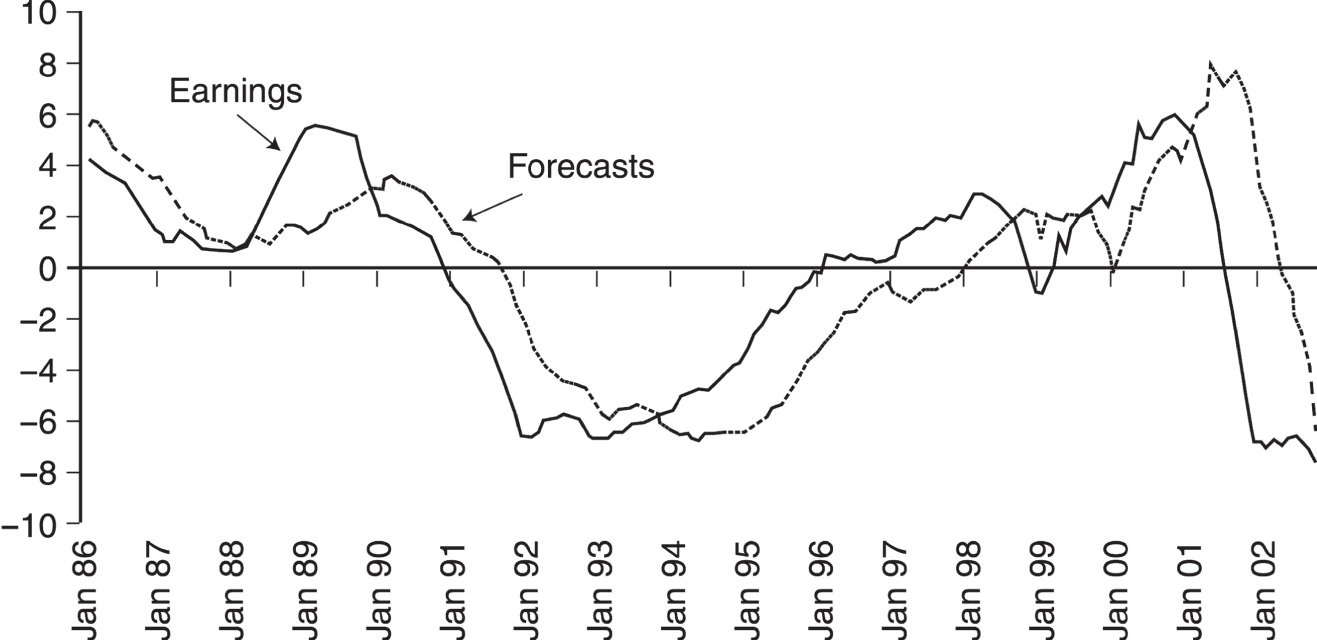

People tend to cling tenaciously to a view or a forecast. Once a position has been stated, most people find it very hard to move away from that view. When movement does occur, it does so only very slowly. Psychologists call this conservatism bias. The chart below [Figure 4.1] shows conservatism in analysts' forecasts. We have taken a linear time trend out of both the operating earnings numbers and the analysts' forecasts. A cursory glance at the chart reveals that analysts are exceptionally good at telling you what has just happened. They have invested too heavily in their view and hence will only change it when presented with indisputable evidence of its falsehood.2

This is clear evidence of conservatism bias in action. Montier's research documents the behavior of securities analysts, but the trends observed can easily be applied to individual investors, who also forecast securities prices, and will cling to these forecasts even when presented with new information.

Figure 4.1 Montier Observes That Analysts Cling to Their Forecasts

Source: Dresdner Kleinwort Wasserstein, 2012

Implications for Investors

Investors too often give more attention to forecast outcomes than to new data that actually describes emerging outcomes. Investors are sometimes unable to rationally act on updated information regarding their investments because they are “stuck” on prior beliefs. Box 4.1 lists three behaviors stemming from conservatism bias that can cause investment mistakes.

Am I Subject to Conservatism Bias?

The following diagnostic quiz can help to detect elements of conservatism bias.

Conservatism Bias Test

Question 1: Suppose that you live in Baltimore, Maryland, and you make a forecast such as, “I think it will be a snowy winter this year.” Furthermore, suppose that, by mid-February, you realize that no snow has fallen. What is your natural reaction to this information?

- There's still time to get a lot of snow, so my forecast is probably correct.

- There still may be time for some snow, but I may have erred in my forecast.

- My experience tells me that my forecast was probably incorrect. Most of the winter has elapsed; therefore, the cumulative amount of snow is not likely to be significant.

Question 2: When you recently hear news that has potentially negative implications for the price of an investment you own, what is your natural reaction to this information?

- I tend to ignore the information. Because I have already made the investment, I've already determined that the company will be successful.

- I will reevaluate my reasons for buying the stock, but I will probably stick with it because I usually stick with my original determination that a company will be successful.

- I will reevaluate my reasoning for buying the stock and will decide, based on an objective consideration of all the facts, what to do next.

Question 3: When news comes out that has potentially negative implications for the price of a security that you own, how quickly do you react to this information?

- I usually wait for the market to communicate the significance of the information and then I decide what to do.

- Sometimes, I wait for the market to communicate the significance of the information, but other times, I respond without delay.

- I respond without delay.

Test Results Analysis

People answering “a” or “b” to any of the preceding questions may indicate susceptibility to conservatism bias.

Investment Advice

Because conservatism is a cognitive bias, advice and information can often correct or lessen its effect. Specifically, investors must first avoid clinging to forecasts; they must also be sure to react, decisively, to new information. This does not mean that investors should respond to events without careful analysis. However, when the wisest course of action becomes clear, it should be implemented resolutely and without hesitation. Additionally, investors should seek professional advice when trying to interpret information that they have difficulty understanding. Otherwise, investors may not take action when they should.

When new information is presented, ask yourself: How does this impact my portfolio? Does it actually jeopardize my forecast about how my portfolio will perform? If investors can answer these questions honestly, then they have achieved a very good handle on conservatism bias. Recognizing conservatism can prevent bad decisions from being made, and investors need to remain mindful of any propensities they might exhibit that make them cling to old views and react slowly toward promising, emerging developments.