10

USING A REAL ESTATE CONTRACT TO YOUR ADVANTAGE

“Those who don’t read have no advantage over those who can’t.”

—Mark Twain

Contracts to purchase real estate have evolved over the years, but one thing has not: few actually read the contracts they sign. When you are about to invest thousands of dollars and promise to pay much more, take the time to read a contract word for word before you sign it. Once you have read a few, you will recognize most of the standard clauses, terms, and conditions. More important, you will be able to identify and negotiate the parts of the contract that are most relevant to you.

Do you need a written contract to buy, sell, or lease real estate? You can answer no and be correct, but there is a catch. You do need a written contract if you ever want to enforce it in a courtroom. The statute of frauds requires that a contract regarding interest in real estate must be in writing and signed by the parties involved in order to be enforceable.

Another important reason to have a written agreement is unless both parties agree and understand the agreement or have a “meeting of the minds,” then the contract is not enforceable. A signed contract is evidence of this understanding.

A third reason to have a written agreement is to help everyone remember what they agreed to. All parties should understand the agreement the day they sign it, but that is no guarantee that they will remember it that way on the day of the closing. Relying on memories is a bad strategy in any business transaction. There is a good chance that the buyer and seller may remember things differently weeks, months, or years later. The written agreement is an essential memory aid.

A very practical reason to write down the important details is that the agent or attorney who will be closing the transaction will rely on the contract for the terms of the sale and of any financing involved. Another reason to have a clearly written agreement is to provide you with a way to get out of the contract if you decide not to buy (or sell). A way out is often called a loophole or contingency.

A written contract is also a checklist for items that are important for you to negotiate. The price, the down payment, the closing date, who will pay the expenses of closing, when you will close, and much more are all written into your purchase contract.

KEEPING IT SIMPLE

Real estate contracts can be confusing and even intimidating. Some agreements are dozens of pages long, and most have been prepared by attorneys and contain language that can be difficult to understand.

With preparation, you can understand any contract and use contracts to your advantage. The key is to take the time to read and understand any contract before you are under pressure to sign during a negotiation.

DON’T SIGN UNTIL YOU TAKE THE TIME TO READ IT

You may spend dozens of hours finding and researching a good deal, and if you buy it, you will spend hundreds of more hours managing and eventually selling it. Set aside the time you need to read any contract carefully before you sign it. Do this alone, without the pressure of others waiting on you to read it. You should never sign a document that you do not fully understand. You may discover later that you have made concessions worth thousands of dollars unknowingly because you signed a contract that you did not understand.

If you are presented with a contract that an attorney drafted, be cautious of any words or phrases that you do not understand. If an attorney prepared it, he or she was probably working for the other party, and the conditions in the contract may benefit the other party.

If you’re using your attorney, get him or her to send you a copy a day before you intend to sign it so that you can take your time and read it carefully. Attorneys occasionally use confusing or unclear wording. Make them use words that you understand. One attorney once prepared a document for me that was so convoluted that he could not even explain it to me. He had cut and pasted several paragraphs from another document that even he did not understand. It was back to the drawing board for him, without pay.

FORM CONTRACTS PROTECT THE SELLER, REALTOR, AND ATTORNEY

Remember that a Realtor almost always represents the seller and that a committee of agents and attorneys typically designs these contracts. These form contracts are designed to legally bind both parties but often have clauses that give the seller, Realtor, and the attorney more protection than the buyer.

As a buyer, you need to understand what you are signing and carefully read any form contract that you receive ahead of time. Get a copy of a contract (a Realtor with whom you might do business would be a good source), and practice by filling in all the blanks as if you actually were purchasing a house. Read all of the fine print to see what it requires you to do and what happens if you do not perform.

Beware: There is no “standard” contract. Even these form contracts are often modified to give one party an advantage. It is important to use a contract that is designed for the type of transaction you are making. A contract designed for residential sales would have inspection and financing clauses that you would not find in a contract used to buy and sell land. A contract to buy a commercial building or mobile home park would be significantly different.

USING THE SELLER’S CONTRACT

When you are buying, sometimes the seller will have a contract on hand, and it can be to your advantage to use her contract. Using an agreement that the seller will prepare or fill out, is evidence that she understands the agreement. It would be unlikely that she could raise misunderstanding the agreement as a successful defense.

Read the seller’s contract carefully and look for unusual provisions that favor the seller. Take your time, and, if possible, take a copy of the contract with you so that you can read it word for word before you sign it. If you are ready to make the offer immediately, go over the contract with the seller line by line, asking him questions about anything that is unclear to you.

USING AN INFORMAL AGREEMENT

Although you need to be careful in writing down your first few deals, professional buyers often use an informal agreement before actually filling out a binding contract. In Donald Trump’s The Art of the Deal, he explains how he typically negotiates all the important parts of a deal with the seller without using a contract and then gives his notes to his attorneys to incorporate in a binding agreement. These are $100-million deals.

The only contract I had for one of the largest transactions I was involved in was a large brown envelope on which the seller and I diagrammed a deal including thirteen properties and several financing transactions. It closed without a hitch because we both wanted to close and were able to work out the details that we had overlooked using the envelope.

When I am buying a house, I will often outline my offer one step at a time on a yellow pad or blank sheet of paper so that the sellers can both hear me and see in simple terms how I am willing to buy their house. Most sellers have little experience in buying or selling property. You cannot go too slowly or make it too simple when explaining an offer.

Sellers have two big questions they want answered:

1. How much will I be paid?

2. When will I be paid?

FILLING IN THE BLANKS

Most contracts you use will have blanks to fill in or, if a lawyer is preparing the contract, questions that need to be answered. You should practice filling out a form contract with real numbers. Fill in every blank and think about which ones are most important to you. The more comfortable you are filling out a contract, the more comfortable you will be presenting an offer. If you are nervous and do not understand the contract, the seller (or buyer if you are selling) will be nervous too and may be too nervous to sign.

NAMING THE BUYER

When buying, list the buyer’s name and use the language “and/or assigns.” Now you have the right to assign the contract if you find another buyer who will pay more before the closing. If you list an entity as the buyer, sign the contract as the representative of that entity. For example, “John Schaub, President” or “John Schaub, Managing Member” or “John Schaub, Trustee.”

THE AMOUNT OF EARNEST MONEY WITH THE CONTRACT

It is not in your best interest to make a large earnest money deposit. The only reason to make a large deposit is to convince the seller that you are a serious buyer. You can get the seller’s attention with less money by making an offer that closes in a week.

Offer a small amount of money as earnest money. The Realtor may ask for 5 percent or more of the selling price. Some contracts will say that this money is retained by the agents as a commission, even if there is a default and it does not close. One hundred dollars is enough earnest money if your offer calls for a quick closing. If the agent has another buyer, they can submit their offer as a backup, so it does not hurt their chances of collecting a commission. It’s an easy sell.

You may be able to get your deposit back, if you decide not to buy, depending on the conditions of the contract. However, it could take a while and it may be a hassle to get your deposit returned. If it’s only $100 instead of $10,000, it’s not as important to get it back so quickly.

THE TERMS AND CONDITIONS

ALL CASH. The simplest for the seller to understand. The cash is payable at the closing.

SUBJECT TO ACQUIRING A LOAN. This condition gives the buyer the opportunity to tie up the property while he looks for suitable financing. If the buyer cannot obtain financing that he likes, then he can cancel the agreement. Beware of clauses regarding financing that are too specific (a specific amount, loan term, or interest rate). Ask for as much time as possible.

CONTRACT TERMS WHEN THE SELLER AGREES TO FINANCE THE SALE. When the seller will agree to sell to you on terms acceptable to you both, include those details in your purchase contract.

CONDITION AND DELIVERY OF TITLE. To ensure that you acquire a good title, you will want to obtain a title search and title insurance policy. Both attorneys and title companies provide this service. Your contract should provide that you will receive title free and clear of all liens and encumbrances. Read your title insurance commitment carefully; it can list exceptions to a clear title and issue insurance that does not cover the exceptions. A common exception is unpaid property taxes, which will be prorated at the closing and the new buyer will be responsible for payment when they become due.

CLOSING DATE. A fast closing is often appealing to a seller who is in a hurry. The best buys are from sellers who have an almost immediate need for cash and are willing to sell at a bargain price to get it.

INSPECTION CLAUSE. Ideally, you want an inspection period that runs until the closing. If you are closing in a week or two, this should not be objectionable to the seller. You can make an offer to buy the property in “as is” condition, subject to an inspection. If you find defects that are too expensive to remedy, then you should be able to cancel the contract and receive a refund of your deposit. Of course, instead of canceling, you could renegotiate the contract to compensate you for the undisclosed defects.

The inspection clause could require the seller to fix items that cost up to a certain percentage of the purchase price. (If you’re selling, set a low limit.) Buyers and their inspectors will always find something wrong with the property. There are no perfect houses.

When you are the seller, you want the buyer to approve the property within a short period of time or to provide you a list of the deficiencies in the property in writing. As the seller, you may want the right to fix the deficiencies and close the deal or the right to cancel the contract. If problems are found, the seller may want to give the buyer a certain amount of credit to expedite the closing of the deal.

Regardless of what the contact says, with mutual agreement you can negotiate a settlement when a problem is found. If you are selling, it is better to simply give the buyer a credit and to let him make the repairs. This gets the house closed faster and puts the burden of making the repair on the buyer. If the seller makes the repair, it is common for the buyer to complain about the quality of the repair work. Don’t put yourself in this position.

When you are the buyer, you may want the seller to make the repairs, which gives you more time before you close. If you are borrowing money to buy the house, the lender may insist that the repairs are done before they will make a loan.

Just before closing (typically on the day of the closing, within hours of the time the papers are signed), the buyer inspects the house one more time. This is commonly called a walk-through inspection, and the purpose is to ensure that the house is in the condition promised in the contract and is vacant and empty.

Again, this inspection is better for the buyer than for the seller. If the seller has not made agreed-on repairs or has not left the house empty and clean, then the buyer has several choices. First, the buyer can refuse to close until the house is put in good condition. Second, he can insist on holding back part of the seller’s proceeds until the house is clean and in good repair. Or third, he can renegotiate the price of the house.

Often, the seller just wants to get the deal closed and is willing to renegotiate the price. If this situation comes up when you are buying, be prepared to ask for a lower price that reflects the cost of the needed repairs or cleaning.

CLOSING COSTS

By custom, and sometimes by law, buyers pay certain closing costs and sellers pay certain closing costs. Sometimes a lender, such as the Veterans Administration (VA) or the Federal Housing Administration (FHA), will require that a seller pay the buyer’s closing costs. Generally, with the exception of these government-insured or -funded loans you can negotiate who will pay these often substantial costs.

First, find out if your state requires a seller or buyer to pay a certain cost, for instance, the tax to record the deed or note. Next, determine which costs customarily are paid by the buyer and which costs are paid by the seller, such as title insurance, appraisals, loan closing fees, and so on. Although many of these fees are typically paid by the buyer, they still may be negotiable.

Just as a buyer can ask for a credit for repairs that need to be made, the buyer can also ask for a credit toward the closing costs of a new loan.

Paying a higher price and getting a credit for the closing costs may allow a buyer to borrow a higher percentage of the purchase price.

ASSUMING OR TAKING SUBJECT TO EXISTING LOANS AND LIENS

When you purchase a property that has an existing loan or existing liens recorded against it, you have three choices:

1. You can pay off those loans and liens.

2. You can assume the obligations and agree to pay them.

3. You can buy the house, paying the seller for his or her equity, and take title to the property subject to the loans or liens on the property.

If you agree to assume a loan, you are agreeing to become responsible for repaying the amount owed on the loan. If the lender is an institution, they will often require that you apply for a loan assumption and charge you for that privilege. There is often a fee, and when you assume the loan, it will show up on your credit report.

If there are liens to other creditors, you can agree to pay them off at closing or assume the responsibility to pay them. If you agree to pay them off, then the seller may hold you to that agreement, and if you do not pay them, the seller may sue you as a way to force you to pay the creditor. Be careful what you agree to when assuming a loan or a lien. Read the language in the contract carefully, and, if necessary, modify it to protect yourself.

When you take subject to rather than assuming a loan, you are not agreeing to pay these loans or liens; you are simply acknowledging that there is a loan or a lien against the property. Your contract should clearly state that you are buying subject to the loans, and the seller should understand what this means. The loan will still be in the seller’s name.

Because the loan is in her name, it may affect the seller’s ability to borrow money. If she is facing foreclosure, she is far better off if you begin making the payments rather than letting the loan go further into default. When you begin making on-time payments on the loan, it will actually improve her credit. Most sellers who will sell to you subject to a loan are in financial distress and cannot make their payments. The lender is also in better shape when you begin making payments. The lender normally would rather have the payments than the property.

Of course, if you buy a property and take title subject to a loan and then are unable to make the payments, you will lose your down payment and any other money you invest in the property. But—and this is an important but—you have no legal responsibility to pay such a loan. If you decide to walk away from this property because you cannot make a profit, you can walk away with a clear conscience.

Don’t buy a property unless you are confident that you will make money from renting and/or selling it. In more than thirty years of buying properties and taking title subject to existing loans, I have made money on every deal, and in every case I made the payments.

One reason to take title subject to existing loans and liens is because the seller owes more on the property than you are willing to assume. You want to avoid the personal responsibility for repayment.

Some properties are burdened with high-risk debt, debt with a high interest rate, or a short-term loan that requires high payments. You do not want to guarantee to make payments on this high-risk debt. If you cannot make the payments, you want the option to give back the property to the seller or to the lender without any further responsibility.

In the last recession, several builders gave me the equity in their new houses, and I agreed to take them subject to their debt and began making payments to the lender. The builders were unable to make the payments and faced foreclosure and potential bankruptcy. While bankruptcy is more common now than in the past, many people are still proud of their good credit record. They will do all they can to avoid a foreclosure or a bankruptcy.

The lenders were delighted to begin receiving payments. I had to scramble to find good tenants during the recession, but they always appear when the rent is right.

THE RIGHT TO RENEGOTIATE OR DISCOUNT EXISTING LOANS AND LIENS

If you offer to buy a house subject to the existing loans and liens, you may be able to renegotiate the terms of these loans or negotiate a discount.

A young couple was trying to sell me their house, which had an existing loan with high payments. I agreed to buy the house, but only if they would allow me to negotiate with their lender to lower their payments. (They needed to be part of this process because the lender would not negotiate with me without their permission.)

The lender agreed to lower the payments by about $300 a month, I bought the house, and I was able to rent it for enough to make the payments.

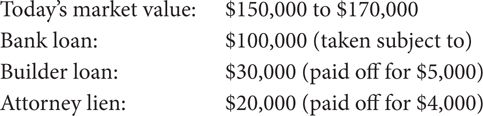

Another seller had a bank loan and another loan to the builder that he had bought the house from, and a third lien on the house owed to an attorney for an unpaid legal bill. In talking with the seller, I learned that the builder had promised to make repairs and had never made them and that the attorney had not been successful in suing the builder.

I agreed to buy the house and take “subject to” the bank loan but not formally assume it. I further agreed to close subject to being able to negotiate both the builder’s lien and the attorney’s lien to my satisfaction. The seller then gave me permission to negotiate with both the builder and the attorney. I contacted both the builder and the attorney and offered to pay them that week if they would accept less money. Both agreed to a substantial discount and were happy to receive the money. I was able to buy the house at a significant discount because of the discount the lien holders agreed to take.

SPECIFIC PERFORMANCE

A specific performance clause requires one party (or both parties) to fulfill the contract. It is more likely that the seller would be required to sell the property than a buyer would be forced to buy the house. But either or both parties can be held to the terms of the contract if there is a specific performance clause. When you are the buyer, you want to be able to walk away from a contract with the right to forfeit your deposit. Being able to walk away gives you a way out of a deal. You may find a better deal or discover something about this property that you really don’t like.

ONE GOOD LOOPHOLE

You don’t need a dozen ways out of a contract, just one good one. In all my years of buying, I have never used a loophole to get out of a deal. Make your offer good enough that you won’t want out.

Sometimes small problems arise, or you discover something unexpected and expensive that’s needed to fix the house. A loophole is not designed to protect you from little things, but major problems with that house or with you personally. It’s like a major medical policy. When it comes to small issues, though, you should remember that every house has little things wrong with it and those issues may be part of the reason you are buying at a good price.

If you discover that the house you are buying has a problem that would be very expensive to correct, you will want to find a way to get out of the deal. Likewise, if you had a serious financial setback or personal disaster that would make closing problematic, you will want a way out of the deal.

A commonly accepted loophole is an inspection clause that allows you to unilaterally cancel the contract up to the closing date. Every house has something wrong with it. Most inspection clauses give the seller the right to correct the problem and close or to cancel the contract. You want a clause that obligates the seller to close but allows you to cancel the contract without giving a specific reason that could then be debated or corrected.

The clause could read, “The buyer has the right, at his expense, to inspect the house or to have the house inspected by a contractor or inspector; in the event that the buyer is not satisfied with the results, the buyer has the right to terminate this contract without further liability at any time before the closing.” Have your attorney review and approve this clause before you use it.

When you buy a house at a good price, the seller is typically in a hurry to sell, and the reason you were able to get the good price is that you have agreed to close quickly. Most of my closings take place soon after I sign a contract. A contingency clause that ties up a property for months and gives the buyer the right to cancel the contract right up to the closing would not be acceptable to many sellers. Be wary of these clauses when you are selling.

AFTER YOU SIGN THE CONTRACT

After you and the seller sign the contract, make a copy for each party. If you have no way to make a copy, make two originals. Have the other party fill out a duplicate original by hand, proofread it carefully, and everyone sign both copies. You keep the one the seller filled out. It would be hard for the seller to claim that she did not understand the contract if she actually filled it out.

CONTRACTS CAN BE MODIFIED

If you need to change any provision of a printed or typed contract, you can by striking through the part that you want to change and writing the change near the part you struck through.

Make any changes clearly, striking through the number or conflicting language in the printed contract. Have all parties to the contract initial any changes, and if you use an addendum, have all parties sign and date it. If the change requires lengthy language, then using a separate addendum would be advisable.

USING A REALTOR’S CONTRACT WHEN BUYING THROUGH AN AGENT

Typically, when you are buying a property through an agent, the agent will want to use his contract. It will protect the agent and generally offers the seller, whom the agent represents, more protection than the buyer.

You can modify this contract to please you or you can use a separate addendum if you need to make changes or additions that won’t fit on the contract. These Realtor contracts usually have a lot of fine print and little space to make additions or changes, so an addendum is a good way to add what you need to make the offer acceptable to you. Remember, both parties should strike through any words or phrases or complete sections that your addendum supersedes—and don’t forget to initial it.

ADDENDUMS

Use a separate written addendum when many or lengthy modifications are required. If you use an addendum, have all parties (including the Realtor) sign and date it. The addendum should refer to the contract it is modifying. For example, “This is an addendum to the contract between Joe and Sally Seller and Bob and Betty Buyer, dated January 5, 2016, regarding the property described as 123 Paradise Way, Sarasota, Florida.”

You could add a complete legal description, but the address is sufficient because you will then attach the addendum to the full contract, which has a legal description.

Your addendum could include your inspection clause. It also may contain a clause dealing with existing loans and liens that you may want to keep on the property rather than pay them off at the closing.

ALWAYS BE WILLING TO WALK AWAY

No matter how well written your contract is, if one party wants out and won’t close, it won’t close. No matter how simple (or defective) your contract is, if both parties want to close, they will.

Suppose I reach an agreement with a seller and he changes his mind before closing and refuses to close. Even if I have the right to take him to court and force him to sell to me, is it worth the expense and amount of time required to do that?

The answer is, sometimes it is. If you have invested a lot of time and money in a property before the closing and will experience a large loss of profit if the sellers won’t close, it may be worth suing them for specific performance. Recognize that this may cost you up-front attorney’s fees and months, if not years, of your time. However, courts will enforce a contract, even if one side is making a large profit.

With a typical house purchase, it’s not worth the time and money to sue to force the other side to close. It will be easier and faster to find another good deal than to force this one to close. Be confident that you can find another (and often better) deal and be willing to walk away with a smile.

If the seller has found another buyer who is willing to pay him more, ask the seller for part of the profit. It is better for the seller to pay you part of the profit than to go to court to resolve the problem.

If you willingly agree to cancel the contract rather than fight to keep them in the deal, sellers will sometimes change their minds. One seller called me to cancel a deal. I told her I’d be glad to because I had found another house I liked better. She then reconsidered and wanted me to close on her property.

IS A LONGER CONTRACT BETTER?

Is it easier for a homeowner to understand and agree to a twelve-page contract with a five-page addendum or a one-page agreement? Obviously, a shorter contract with less fine print is easier to understand and sellers are more likely to understand and sign it.

Use the shortest contract that gets the job done, and you will buy more property.

Realtors use a “form” contract prepared by their attorneys. When you buy through an agent, she will insist on using her contract, but that does not prevent you from adding to it or modifying it. Realtor/lawyer contracts have grown in size from one page (front and back) to twelve pages or more (front and back) during my time in the business. In addition to a twelve-page purchase, a sale agreement may include a five-page disclosure and another dozen pages of addendums that cover items not discussed in the contract.

Know what a contract requires and when it puts you in harm’s way, then modify it so it protects you. Make your offers as clear and concise as possible and you will buy bargains that others miss.

SOME CONTRACT CLAUSES ARE ENFORCEABLE AFTER THE CLOSING

Parts of the contract may “survive” or be enforceable, even after the closing. A seller benefits by not having any continuing obligations or liabilities after the closing. When you are the seller, be aware of these potential ongoing obligations.

As a buyer, you would like the seller to be responsible if a problem, previously unknown to you, arises after the closing.

Common warranties and promises that a seller would make that would survive the closing are:

• Seller is conveying the property free of all mechanic’s liens and other claims

• Seller warrants that information in the listing agreement, or otherwise provided, is correct to the best of his knowledge

• Seller warrants that he has disclosed to the buyer all material latent defects that are known to him

• Seller warrants that he has disclosed any information in his possession that materially and adversely affects the consideration paid by the buyer

In addition, the right to require specific performance (to force the other party to close as agreed in the contract) survives to both the buyer and seller, unless modified in the contract.

Although buyers commonly rely on representations made by agents, note this paragraph from a Realtor’s contract:

BUYER AGREES TO RELY SOLELY ON SELLER, PROFESSIONAL INSPECTORS, AND GOVERNMENTAL AGENCIES FOR VERIFICATION OF PROPERTY CONDITION, SQUARE FOOTAGE, AND FACTS THAT MATERIALLY AFFECT PROPERTY VALUE AND NOT ON THE REPRESENTATIONS (ORAL, WRITTEN, OR OTHERWISE) OF BROKER.

This paragraph puts buyers on notice not to rely on the agent’s statements.

ASKING THE SELLER TO WRITE IT DOWN

When an offer is accepted by a seller in a hurry and he agreed to a price or terms favorable to you, have the seller write it down in its most basic form, to show that he understands the offer. “I, John Seller, accept Barb Buyer’s offer to purchase my house at 2357 Prime Street, for a price of $100,000, with $10,000 down and the balance payable at $500 a month including interest of 3% until paid in full, closing on May 1, 2016. The buyers agree to pay all closing costs.”

You can take a simple contract like this and fill in the blanks to reflect your understanding and all can sign it.

IN REVIEW

• A contract that will close will reflect a meeting of the minds. When both want to close they will do so and if either party does not want to close, it is better to look for another deal rather than try to force this deal to close.

• You never want to go to court; your contract does not have to be enforceable in a court. An agreement written on the back of an envelope will close if both parties want to close. Have a clear agreement that covers the important points and then close as soon as is practical. I often try to close in less than a week.

• Negotiate patiently and don’t worry about losing the deal, but once you have an agreement, close quickly. If the sellers have agreed to sell to you at a bargain price or on good terms, someone else may offer them more. Closing sooner reduces this possibility.

• Filling out the contract is part of the negotiation process. Go slowly, one point at a time, and see how the seller reacts. You will learn a lot about how a seller negotiates. You can negotiate the points most important to you last, when you have a feel for how the seller negotiates.

• Always have a way out. Just one good loophole is all you need.

• Always be willing to walk away. Never make it personal. If they won’t close, walking out of a closing sometimes brings them back to the table.