15

SELLING ON LEASE/OPTIONS TO GENERATE LARGER PROFITS

To make a great buy, you typically have to sign a contract to buy the house today and then close within a few days. The reason people sell houses for far less than what they are worth is because they have to: they don’t have enough time to wait for a retail buyer.

When you sell a house, if you sell to a buyer who cannot close right away—who needs some time to pay you—you can sell for a significantly higher price. I often make an additional $10,000 per house when I sell on a short-term lease/option contract.

In the case of the “house of the rising water,” I sold the house using a lease/option contract. A lease/option is a form of owner financing, but a simpler, safer, and less costly way to sell to a buyer who may not be able to qualify for a loan.

Most buyers who want owner financing cannot qualify for a bank loan. There are always a substantial number of house buyers—or would-be buyers—who cannot qualify for a bank loan because of poor credit or low income. Some owner wannabes are eager to buy and are willing to pay a retail price and make regular payments if they are given the opportunity.

Using a lease/option, I sell many families their first home. They pay an option payment and then monthly lease payments for the term of the contract. If they want to buy the house, they must at some point qualify for a bank loan.

QUALIFIYING YOUR BUYERS

Before I sell to them, I get financial information and identify why they cannot qualify today for a loan. I help them to form a plan so that they can qualify within a period of time, often one or two years. If they have too many expenses, often the solution is to pay off a credit card debt or a car loan—and to avoid new debt. If they have poor credit because of overdue bills, I counsel them to form a plan to pay off those bills and then to begin making timely payments on their other credit accounts.

SETTING THE OPTION PAYMENT, THE RENT, AND THE PRICE

The option payment, the monthly rental amount, and the price you’ll sell the house for are directly related. You can charge a higher sales price if you will accept a lower option payment and rent. However, if no one ever buys because your price is too high, then you will never sell the house.

Which of the three—option payment, rent, or price—has the greatest impact on your total profit? If you increase the option payment from $3,000 to $5,000, how does that affect your profit? If the optionee doesn’t buy, you get to keep a larger option payment, but if the optionee does buy, you make the same amount of profit.

Raising the monthly rent will produce more income, but you must balance the amount of rent you charge with how long it will take you to rent the house. If you try to get an extra $100 a month, and the house sits empty for a month, you probably have lost more than you can recover. Using a lower rent and renting faster often will make you more money.

Of the three variables, the price is the one that will have the greatest impact on your profit. If you make someone a good deal on the rent and accept a relatively small option deposit, but set your price at the top of the retail range, you will collect several thousands of dollars more in profit when you close.

GETTING THE BEST PRICE WHEN YOU SELL

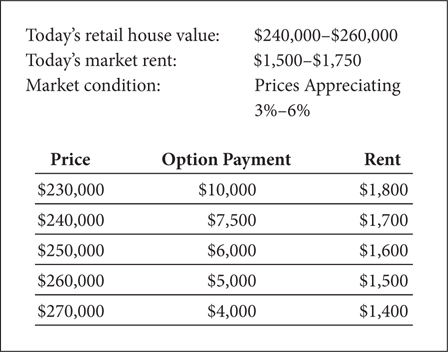

Table 15.1 presents an example of what you may be able to charge for a house in a typical market, one appreciating from 3 to 6 percent. Notice that both the price and rent are expressed in ranges. It is impossible to put an exact price or rent on a house. If you had four appraisers give you a price, you would get four different prices. You need to know your market well enough that you can establish these ranges. Establish a range for both price and rent that allows you to form a strategy for selling.

TABLE 15.1 A Bargain Rent and Option Payment Produce a Higher Price and Greater Profit

Selling on lease/options is an art, not a science. Every house will have a different market appeal: Some will need lots of work, and others will be ready to move into. The desirability of the neighborhood will determine how many people will want the house and how much they are willing to pay. Table 15.1 shows the relationship between what price you ask, what rent you ask, and the amount of option money you are able to command.

Notice which number has the greatest impact on your profit—it’s the price. By charging a lower rent and deposit, you can charge a higher price. The amount of the deposit you charge will have an impact on the number of buyers who actually close. The lower the deposit you charge, the fewer the number of buyers who will be able to close on the purchase.

A buyer with more money and better credit is likely to be a better negotiator and often will negotiate the sales price. If you can sell at a higher price and still collect a larger down payment, do it. It is probably a sign that the market is heating up and that prices will be moving up faster.

The time it takes you to sell the house will be determined by how you price it. If you ask for a high price, high rent, and a high deposit, it may take you months to sell. In an average market, you can sell a house on a lease/option in a month or less if you price it at retail and charge a fair rent and deposit.

If getting a higher price is more important to you than getting more rent or more money up front, then you should advertise the house with a lower down payment and rent to make it more attractive to more buyers.

If getting your money sooner is more important to you, then selling at a lower price and getting a larger deposit will increase the chance of the buyers actually closing. The more they have invested up front, the harder they will work to close on the house.

The option payment is part of the money you are asking for before you give a lease/option buyer possession of the house. You also will collect the first month’s rent—in cash. The total amount you collect needs to be low enough to attract buyers. The condition of the house and the desirability of the house will determine how much you can charge.

My student Bob Bruss advised to advertise the amount of money it takes to move you in:

Bob invested in the San Francisco area and sold houses in high price ranges on lease/options with relatively small down payments.

DON’T USE LEASE/OPTIONS AS A MANaGEMENT TOOL

Some lease/option sellers never actually sell a house. They sign a lease/option to renters who could never qualify for a loan. These sellers are just collecting additional money in the form of option payments every time they rent the property.

Use a lease/option to sell a house that you want to sell. Don’t use it as a technique to increase your cash flow from your long-term investments. There are risks to selling your investment houses on lease/options. First, if the market takes off and prices jump 15 to 20 percent in one year, many of your buyers will buy. This will take you out of the market just when you want to own property.

Suppose that you owned ten houses and instead of renting them, you sold them all on lease/options to increase your cash flow and reduce your maintenance costs. (Later, in Chapter 17, you will learn how to rent to tenants who will take care of your property.)

House prices jump 20 percent, and eight of ten of your tenants buy their houses, leaving you with a large tax bill to pay or the challenge of reinvesting your money in property in a market that’s going up 20 percent a year. If the houses were worth an average of $200,000, you have given up (20% × $200,000) or about $40,000 per house profit.

The lease/option is the best way to sell a property at a retail price, but don’t make the mistake of selling property that you want to keep. When you buy a house in a strong neighborhood with good long-term financing, don’t sell it just because someone wants to buy it. Your best houses will make you the most money. Others constantly will try to buy them from you.

SETTING THE TERM, MONTHLY CREDIT, AND EXTENSIONS

When you sell a house, use a one-year lease/option period. If house prices jump 10 percent during the year, you are giving less away when you use a short term. If the buyers are nervous (and they often are) that one year may not be enough time for them to solve the problem that keeps them from qualifying for a loan, then offer them a one-year extension—at a higher price. In an average market, use a 5 percent increase in both the price and the rent for the second year. If the market is increasing at a faster rate, ask for a larger increase. You can always give some of the increase back if you want to sell the house and it does not appraise at the higher price when the buyers apply for a loan.

Put in your lease/option agreement a monthly credit amount toward the purchase that the buyers will “receive” when they pay on time. Use $100 a month. If you use a higher amount, the lender who the buyers borrow from may disallow it unless they are paying a credit on top of the fair market rent. While a larger credit may make the buyers more interested in buying the house, it will not help them to get a loan. If they accumulate a large credit and then cannot buy the house, they may feel entitled to part of it if they cannot buy.

BEING A GOOD GUY IF THEY CANNOT BUY

Reporters have asked me what percentage of my lease/option buyers actually close. Overall, it’s about 50 percent, but it depends on the credit market. When interest rates are low and loans are easier to come by, the percentage of buyers who can qualify for a loan and close goes way up—to 100 percent in some years. When interest rates rise and loans are hard to get unless you have perfect credit, then the percentage of buyers drops.

When that happens, I often renegotiate the agreement so that the buyers can stay in the house and continue to try to buy it. I adjust the rent and price to keep up with the market. Eventually, if the buyers clean up their credit, they can buy the house.

In the event that the buyers change their mind, get transferred, or get divorced, sick, or any of the real-world things that happen to people every day, then I offer some of their original deposit back if they have paid the rent and taken care of the property. In effect, I treat them like a good tenant and refund part of their original option money, treating it like a security deposit.

This is a nice thing to do, and it is also good business. If you have to go through the eviction process to move out a tenant who was buying under a lease/option, it will cost you both your time and money. It is better business to give the buyers some of their own money back as an incentive to move and give you back a house in good condition than to use the courts to force them out.

If you get a house back in good condition, then you can resell it quickly to another lease/option tenant.

GETTING YOUR CASH NOW WHEN YOU SELL ON LEASE/OPTIONS

When you buy a house that you intend to sell on a lease/option, you may need to recover part of the cash that you have tied up in the house before the buyers close on their lease/option contract. A bank line of credit and a private line of credit are good ways to obtain the cash you need before you receive your profit.

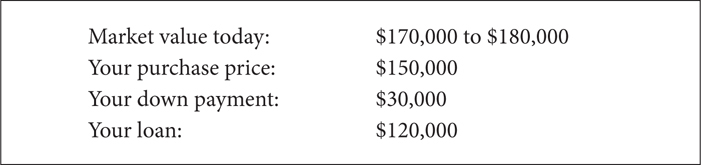

Suppose that you bought and sold this house:

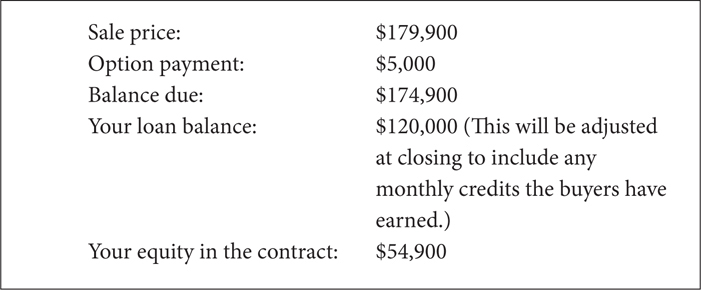

You resell on a lease/option:

You now have about $55,000 of equity in the contract and about $25,000 cash tied up in the house (your $30,000 down payment less the $5,000 down payment). You can use this contract to borrow $25,000 on a short-term loan either from a bank or from a private party. You can show the lender that she will be repaid from the proceeds at the closing. You could assign your contract as collateral for the loan if she insists, but often you can borrow unsecured. If the house does not close as planned, you will sell it again and pay off your loan when it does close.

If you are getting the money from a private investor, you could sell her a half interest in your equity in the house, subject to the lease/option sale, for $25,000. The investor would then own one-half the house and would receive one-half the rent as well as the proceeds ($54,900/2 = $27,450) when the sale closes. If the first sale does not close, then you would resell the house at hopefully a higher price, and the investor would then participate in half that sale.

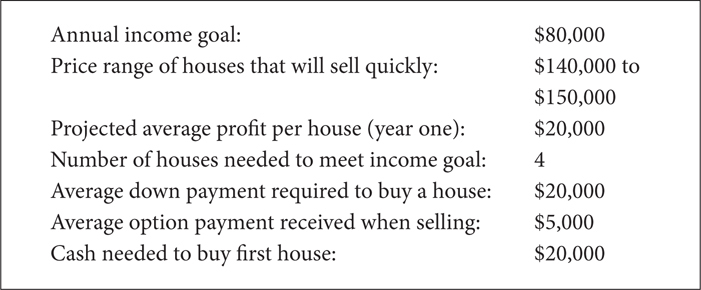

A BUSINESS PLAN FOR BUYING AND SELLING

If you want to make buying and selling a full-time business, you need a plan to produce a certain amount of income. Here is a simple plan that you can use as a format to form your own plan. Plug in real numbers in your town to see how it would work for you.

Borrowing against the first contract could raise the down payment for the second house. With $80,000 in initial capital, you could acquire all four houses without borrowing.

Compare this business with other small businesses that you could own and operate in your town. Most small businesses require far more than $80,000 in startup capital. They also require employees, and have overhead such as rent, advertising, utilities, and so on. Many businesses have inventory that can spoil (like food), go out of style (like shoes), or be stolen. Your inventory is appreciating, won’t go out of style, and it’s hard to steal.

The owner of a small business often works or is on call many hours, seven days a week; in addition to his own work, such an owner must supervise the work of his employees. You alone, working part-time, can generate more net income than most small businesses in your town.

DOING GOOD WORK AND GETTING PAID FOR IT

The business of buying and selling houses provides a service to your community. There are always sellers who need to sell quickly and buyers with credit problems who need help buying. By treating people fairly and by filling both these needs, you can make a good living and help people out of difficult situations. At the same time, you can hold on to the better properties for long-term investment, which will one day give you the ability to simply collect rent rather than continue to buy and sell.

When you sell on a lease/option, you can have the buyers pay your closing costs, and you sell the house in its “as is” condition.

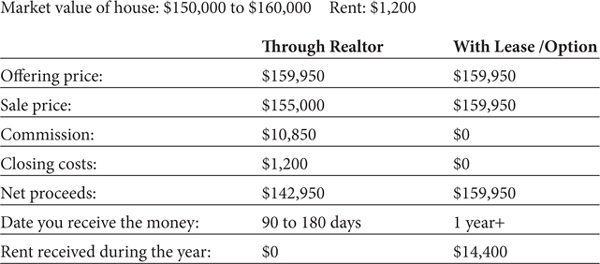

How Much Does Selling on Lease/Option Save You?

Here is a comparison of a lease/option sale and a sale through an agent:

The advantages of selling through a professional agent are that you are sometimes paid sooner and you do not have to talk and show to potential buyers, and then close the deal. Not all houses listed for sale sell during the first listing period. You might have to wait the best part of a year to be paid, even selling through a good agent.

Every day you wait you are supporting an empty house. This often puts so much pressure on a seller that they sell the house for far less than what it is worth. Agents will put pressure on you to reduce your price if the house does not sell quickly. No sale means no commission to them. A low price increases the chances of a sale. It’s good for them but costly to you.

With a lease/option, you collect rent while you wait for the house to close. If it takes a year, you collect the rent each month while you wait. This results in a higher net profit to you.

Selling to a Family Member Using a Lease/Option

You may have a family member who is interested in investing but who is short of funds. You could sell that person a house that you want to sell using a lease/option. You could make them a good deal on both the rent and the price to give that person a better than average chance of making a profit. You could even help the person manage the property and provide a little advice along the way.

When selling to a family member, you could use a longer-term lease/option to give the person more time to make a profit. You might plan for your relative to refinance and pay you off when the property increases 50 percent in value. If in your town that would take about five years, you could use that term and then renegotiate if the person needed more time.

Should it not work out, then you would still own the house. It is better to sell to a family member using a lease/option for a couple of reasons:

1. You don’t have to report the sale on your tax return until the relative exercises the option to buy. If he doesn’t buy, you still own it and have not had to report a sale.

2. You don’t have to foreclose to recover title to the property. You would not want to foreclose on a family member.

SELLING TO ANOTHER INVESTOR USING A LEASE/OPTION

If you have no one in your family who wants to invest, there are many young investors getting started today who would eagerly buy from you on a lease/option. You could sell at a retail price without a commission. The investor then would manage the property and pay you when she resold it or refinanced it.