8

BORROWING WITHOUT GOING TO A BANK

When I started investing in houses, I was a self-employed real estate salesman with no steady income. Not one banker in my town would loan me money to buy property. As it turned out, that was a key to my success. It forced me to learn how to buy property without going to a bank to borrow money.

Many real estate investors who are millionaires today, started with only a little money. Some did not have a job with a W-2, or great credit. They bought their first property with a small down payment, and then they bought another property as soon as they could. They continued to buy, one property at a time, negotiating better terms and prices as they learned more.

The secret to being able to buy property that will make you large profits is to learn how to borrow on terms that your tenants can repay with their monthly rent. Buying a property with little or nothing down is a great strategy, as long as you can afford to make the payments. If you can’t afford to make the payments, you will never collect any profits.

Banks require investors who want to borrow to make a down payment, often 20 percent, and require good credit. They will only loan 80 percent of the purchase price or appraisal, whichever is lower. If you buy a house worth $200,000 for $150,000, they will only loan you 80 percent of the $150,000.

When you find a bargain, it is often because the sellers need to sell right away. If they could wait ninety days, they would and probably sell for more.

Unfortunately, banks will not make you a new loan in a few days. Borrowing from a bank takes longer and costs more than other sources. When you borrow from a bank you will pay high closing costs and they will charge you the current retail rate of interest. The paperwork you are required to sign will protect the bank, and if you read the fine print, you give them the right to take other assets that you own if you cannot repay the debt.

If you have a good job and good credit, banks will loan you money for a few house purchases. If you buy a lot of houses, you will find that lenders often have limits to the amount and number of loans that they will make you, and, eventually, the banks may refuse to make you more loans.

BORROWING A MILLION DOLLARS AND STILL SLEEPING WELL

How would you feel about owing a million dollars? If you buy more than five $200,000 houses, you could easily owe a million dollars. The key to sleeping well while you are in debt is knowing that you can repay the debt. When you buy rental houses, your tenants will repay your debt if you buy and finance wisely.

My friend Jack Miller said that the surest way to become a millionaire with real estate is to borrow a million dollars secured by property, and then pay it off. Even if the property is never appreciated, you would have your million dollars.

Jack is right. If you can learn how to borrow that million dollars safely so you can sleep well, then you are on your way to unlimited financial success. The safety comes from borrowing against property that generates enough income to repay the loan.

Most people can’t conceive the idea of borrowing that much money, because they are thinking about going to the bank and qualifying for a million-dollar loan. You can borrow from sources other than banks without qualifying for a loan based on your income and credit.

Bankers have a lot of rules to follow. The rules are both imposed by the government and self-imposed by the banking industry. Before a banker lends you money on real estate, he will want an appraisal, a credit report, proof of your income, and a list of your other debts and assets. If you start buying property aggressively, you will soon reach the point where the rules will limit the number of loans you can have with one lender. These rules make borrowing from banks both time consuming and agonizing.

THINGS YOUR BANKER WON’T DO

1. Your banker won’t make a decision fast enough to loan you the money to buy a really good deal.

A good deal is when a seller has decided to sell today (or in the next few days) and selling quickly is more important than the price. Often the seller is out of time and needs money today (or very soon) or something bad is going to happen.

I have purchased several homes from sellers a day or two before their house would be sold at a foreclosure auction. Although they may have had chances to sell before, they waited until the last minute to make a decision. At that point, there were few buyers willing to take the risk of buying on such short notice and able to close in one day.

Even though I have great credit and can qualify for a loan, there is not a banker in my town who can close a real estate loan the same day I call him. A home equity loan or line of credit could be used for quick purchases at bargain prices. However, these loans have variable interest rates and some are short-term loans. These terms make them dangerous loans for a long-term investor.

New federal consumer protection regulations (SAFE Act and Dodd-Frank Act) lengthen the time it takes a homeowner to get a bank loan and to close a real estate purchase. Some sellers just can’t wait that long. Look for sellers who can’t wait, and make them offers that allow them to finance either part of or all of the purchase price.

2. Your banker won’t loan you more than 80 percent of the purchase price of an investment property.

If you wait to buy a house until you save up a 20 percent down payment, it may take you years to buy your first house. And, by then, houses will probably be more expensive, so waiting can cost you a lot.

If your goal is to buy a property with a smaller down payment, then you will have to find a lender other than a bank. Some sellers will sell you a property and finance most of or all of the price. Often they are sick—either sick of managing or sick of making payments. Look for burned-out investors who have bought several properties but never learned to manage. They will often sell to you with a low down payment and carry all the financing to get out of management. Even a small payment is more money than they can get when they rent to a tenant.

Some investors try to trick bankers into lending to them by using fake contracts or phony appraisals. This is called bank fraud, and you will go to jail if you get caught. Typically, the lender does not go to jail, just the borrower who provided false statements.

Beware of those who tell you to lie or use devious methods to buy or borrow. Understand that many lenders work on commission and that they are under pressure to lend money. If you are uncomfortable with what they are asking you to do, get a second opinion from another lender or an attorney.

3. Your banker won’t make you a loan when prices are at their lowest.

When real estate prices are going up, it’s typically easier to get a loan and bankers will make loans to investors. But when a recession comes and prices fall, banks stop making investor loans. You want to be able to buy when there is a recession. The prices are at their lowest during a down cycle.

4. Your banker won’t make you a loan without regular monthly payments or with the first payment due several months from now.

In fact, bankers typically insist on monthly payments starting right away. This is a problem if you are buying a house that will sit empty for a while.

Sellers will often accept financing with more flexible terms and lower payments in the beginning that would allow you to have cash flow immediately. I have negotiated payments with seller financing starting in six months or longer after the closing date.

5. A banker won’t loan money to someone who really needs it.

If you need it, then you must be in trouble or almost in trouble, and bankers hate trouble.

If you know you are going to need money one day, borrow before you need it. You may really need it because you are about to be temporarily unemployed, or divorced, or unable to pay your taxes. Whatever the reason, it will be hard to borrow once you are in trouble.

WHY A SELLER WILL DO WHAT YOUR BANKER WON’T DO

When a banker loans you money, he writes you a check. He is going to be very cautious and charge you a high rate of interest, because he has borrowed the money he is lending to you from his depositors. He has to pay them back, so he can’t take big chances with their money.

When you buy a house from a seller who wants to get rid of it, the seller is not lending you money, he is waiting for his equity or profit from his house. This may be equity or profit that he will not get if he does not sell to you.

A seller is not as cautious as the banker when it comes to lending money. He just needs to be comfortable that you will make his payments and eventually pay him.

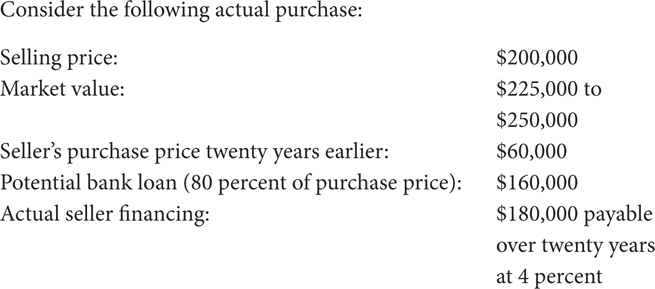

With this house, the seller had a large profit because he or she had owned the house for twenty years. When a seller has a large profit or large equity, he is often willing to finance the purchase and receive payments and his profit over several years.

With $20,000 down, the seller has received one-third of what he paid for the property as a down payment. In addition, over the next twenty years he will receive payments totaling $261,782 (240 payments of $1,090.76). Compared to what he originally paid, the seller has made a great investment.

A banker making a $160,000 loan has no profit until you begin making payments. What looks like a risky deal to a banker with a $40,000 down payment can look very safe to the seller of a property.

BORROWING ON TERMS THAT YOUR TENANTS CAN AFFORD TO REPAY

A wonderful feature of investing in property is that you can structure the financing on a property so that your tenants make all the payments. When you borrow on terms that have payments that your tenants can afford to make, they will buy the house for you.

Sometimes this requires a combination of financing. For example, suppose that you can buy a house worth $200,000 to $220,000 for $180,000. The gross rents are $1,600 a month, and the net income after taxes, insurance, and repairs is about $1,000 a month.

If you borrowed the entire $180,000, what interest rate and term would you need to have payments low enough that your tenants would repay the loan?

To answer this question, you need either an amortization schedule or a financial calculator. You can get a financial calculator app on your phone if you don’t want to buy the calculator. Learn how to calculate both payments for different loan amounts, terms and interest rates, and the rate of return on your investment. Then you will be able to compare two potential investments.

With a financial calculator, you can solve for one variable if you know the other three. With the preceding question in mind, what interest rate can I pay and how much time would it take to repay the $180,000 purchase price with $1,000 a month in net income?

I know the amount ($180,000) and the payment ($1,000). To find an answer to the interest rate or term, I need to plug in one of the variables. In this case, that is the loan term of thirty years.

Now suppose that you have to pay 7 percent today for the money you need to borrow. You could solve for the term you would need. If you know that you can borrow at 7 percent for thirty years, then you could solve for how much you can borrow:

What if you cannot borrow enough money at today’s rate to buy the house and repay it with the cash flow the tenants will produce? Then you need to borrow part of the purchase price at a lower rate, with lower payments or with deferred payments.

Suppose that you need to borrow a total of $180,000, and you find a source that will lend you $150,000 at 6 percent for thirty years. A smaller loan will have a lower interest rate.

After making the $899 payment, you have $102.05 a month (this year, because your rent should increase with time) to use to pay the other $30,000. Each year your cash flow should increase as rents increase.

Here are four ways to repay $30,000 with $100 a month:

1. Pay the seller (or a friendly lender such as your parents) $100 a month without interest, with payments to increase as you raise the rent.

2. Pay the seller $100 a month beginning when you can raise the rent enough to start making that payment.

3. Pay the seller $100 a month now and agree to increase it as you increase the rents. You can take your best guess at rent increases and design a repayment schedule based on your projections: say, $100 a month for the first five years, $125 a month for the subsequent five years, and then $150 a month until it is paid in full.

4. Pay the seller the whole amount ($30,000) in one lump sum ten years from now. This may cause you to either refinance or sell at that time unless you have saved the money to make the payment.

BUYING EMPTY HOUSES WITH ZERO-INTEREST, SINGLE-PAYMENT NOTES

Owners with an empty house will finance the amount of their equity with no payments for a while if you begin making the payments on their existing bank loan instead. These sellers have a big problem; they own an empty house that may cost them $1,000 or more every month. Few people have an extra $1,000 a month in their budget that they can use to make payments on an empty house.

I have purchased many houses by agreeing to start making payments on an existing loan and agreeing to pay the sellers the amount of their equity, without payments or interest, when I sold their house. This could take years, but in the meantime, they don’t have anymore big payments to make.

You may be asking how you will be able to make the big payments that the seller can’t make. The answer is that you will rent the house to a tenant who will pay you enough to make the payments. Before you make an offer on any property, know how much it will rent for and what your operating expenses will be so that you know how large of a payment you can make.

Suppose that a seller owns this house:

Offer the seller a note for $50,000 with no interest and no payments until you sell the house. You can agree if the house does not sell in ten years you will pay the note. You agree to begin making the payment on the existing $150,000 loan. Secure the $50,000 note with a second-position mortgage or deed of trust on the house. In the event that you cannot make the payments, you can deed the house back to the seller.

The major benefit for the seller is that he or she gets immediate relief from both the payments and the responsibility of maintaining the house. If the seller wants to buy another house, he or she can show the new lender the agreement with you in which you took responsibility for making the payments on the first loan.

You get to buy a house with nothing down that will produce enough income when rented to make the payments on the first loan. When the house appreciates enough that you can refinance it or sell it at an acceptable profit, you will have the cash to pay off the second loan to the seller.

SHORT-TERM BANK LOANS FOR EMERGENCIES

A line of credit is an unsecured bank loan that you can obtain based on your credit and ability to repay it. You borrow only what you need when you need it and typically pay interest only on the balance until you repay the loan. These interest-only payments are lower than payments required on an amortizing loan.

The disadvantage in having lines of credit is that there may be a requirement to pay off the loan within a short period of time. Another disadvantage is that the interest rate typically is tied to the prime rate, or the rate set by the big banks. This rate can change with time, and your payments can increase.

A home equity line of credit (often called a HELOC) is a loan that is secured by your personal home. Some lenders will allow HELOCs on investment houses. Because it is secured, there is less risk to the lender, and the interest rate is often lower than you can negotiate on an unsecured line of credit. Again, you can typically arrange to pay interest on the outstanding balance only, although the interest rate will change with time.

These loans are useful for buying a house that you plan on selling for a short-term profit or selling to an investor to recover your investment and keeping half interest. They are not advisable for a house you want to hold for many years, because the rates and your payments could increase dramatically.

If you borrow using your home equity line at 5 percent and rates jump, you could soon be paying 10 percent interest, or twice your original payment. If you borrowed to buy a house and the rent just covered your payments, then with a higher interest rate, the rents would not cover the payments.

If you cannot repay a home equity loan, you could lose your home.

Use this money carefully. Only use it for emergencies, like an unexpected roof replacement or to buy a house that you know you can sell for a short-term profit. Know that when interest rates are rising rapidly, it may be harder to sell a property quickly for a profit.

WHY YOU SHOULD NOT REFINANCE ONE HOUSE TO BUY ANOTHER

If you are committed to buying several houses, your strategy for buying and financing them is important to your long-term success. Simply buying houses won’t make you rich.

New investors often assume that the best way to get the down payment for a second house is to refinance the first house. Logically, they would then refinance the second house for the down payment on the third house and continue to refinance to pull out cash for new investments.

Refinancing can be a good strategy to reduce your interest costs when rates drop. If you can borrow at a lower rate and for a longer term, your payments will drop and your cash flow will increase.

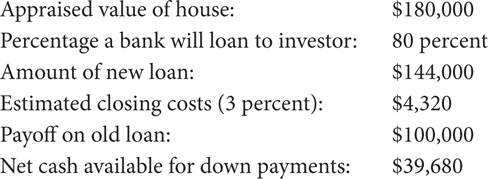

When you refinance and pull cash out of a property, you are increasing your debt, and if your payments increase, you are increasing your risk of losing that property. Consider the result of refinancing a house appraised at $180,000 to get the down payment to buy another one:

REFINANCING DOES NOT MAKE YOU RICHER

Note that before you refinanced the house in this example you had $80,000 in equity, the difference between the value of the property and the loan balance. After you refinance, you would have $36,000 in equity and $39,680 in cash for a total of $75,680. Your net worth has dropped by the amount of the refinancing cost.

Refinancing is not a profitable move unless you reduce your interest cost significantly so that the interest you save repays your cost of refinancing in five years or less. If you sell the house in less than five years, you will not even recover your refinancing costs. Lenders know that many loans are either paid off or refinanced in five years or less, so refinancing is a profitable business for them.

Temptation is another risk of refinancing. Despite your intentions to buy another investment property with the proceeds, those new cars and exotic vacations are very tempting. Either have the house you want to buy under contract so that you know where you will spend the refinancing proceeds, or put the funds in a separate account (not your personal checking account). If the money is in your personal account, you may yield to temptation and spend some or all of it on toys or good times.

An alternative strategy may be to put a second mortgage on this investment house and avoid paying the closing costs on the $100,000 balance on the old loan that you get no benefit from paying off. Second mortgages often have higher interest rates. Compare the increased interest cost to the closing costs you can save by not refinancing the whole amount.

Closing costs, when borrowing, typically include a credit report, an appraisal, title insurance on the new loan, recording fees, state taxes, sometimes points (interest paid in advance), and miscellaneous fees that the lender tacks on. These costs often equal about 3 percent of the new loan amount.

Whenever you borrow, recognize that some of these costs are the same regardless of how much you borrow. If you only borrowed $124,000 in the preceding example, netting you $20,000, but had to pay closing costs on the whole amount, your costs would be a much higher percentage of the money you borrowed (4,320/20,000 = 21.6%; 4,320/39,680 = 10.88%).

REFINANCING INCREASES YOUR RISK

Suppose that you owned a house today that is worth $200,000 with a $100,000, 6 percent loan with a payment of $700 and a net rent (after all operating expenses, maintenance, taxes, and insurance) of $900. You would have $200 cash flow each month. If you refinance to an 80 percent loan, you could raise $60,000, less your closing costs, and if the interest rate and the term stayed the same, your payment would be $1,146. Your cash flow on this house would change from a plus $200 to a negative $246.

Before refinancing:

Result: The risk of loss to foreclosure is very low.

After refinancing:

By refinancing, you put your remaining equity of $40,000 at a higher risk of loss.

Before you refinanced this house it was a safe investment; you had $200 a month in cash flow. If there was a recession in your town, you could lower your rent by $200 a month and still make the payments. After you refinance you have a $246 loss each month, and if you can’t make up the difference you could lose the house to foreclosure.

If you take the money you borrowed and bought two more houses, you could buy other $200,000 houses, hopefully for no more than $180,000. With your $30,000 down payment on each house you would owe $150,000. At 6 percent and on a thirty-year term, the payment would be $900 a month. Each house would break even. Your total portfolio of three houses would be a loss of $246 a month.

A BETTER STRATEGY

Rather than refinancing a loan, consider the difference in your risk if you used the cash flow from your first investment property to acquire another house. Suppose you find a house with an existing loan on it that will rent for $200 a month less than the loan payments. It might look like this:

The positive cash flow on the house you already own could be used to make up the difference each month. As a side note, the principal paydown on this loan would be about $180 a month. Even though it requires an additional investment of $180 a month, the loan is being reduced each month by about the same amount.

Consider the difference between refinancing and using the cash flow from your existing house to buy another house. You have not refinanced your first house, so it still has a safe loan. If you had to reduce your rent, you could still afford the payment on that house so you would not lose your equity.

Say you have bought a new house by taking over existing financing or by giving a seller a note payable at $1,080 a month. Because you did not borrow this money from a bank, or hard money lender, there would be no personal guarantee. If you could not make the payments, you could lose this house, but you would not be putting your first house at risk.