16

FINDING AND BUYING PREFORECLOSURES AND FORECLOSURES

Buying property from an owner in distress is exciting and can be very profitable. However, it is often complicated and requires specialized knowledge of the system and the law.

If you are a beginning investor, read this chapter, but know that you need some experience before you have success buying foreclosures. When you find an opportunity, use a competent real estate attorney who can guide you through the process of buying your first foreclosure. Another investor may be able to refer you to a knowledgeable attorney.

HOW AND WHY FORECLOSURES OCCUR

It is easy to borrow money against a home you own. Sometimes it is too easy, and homeowners borrow more than they can afford to repay. When this happens and the borrower stops making payments, both the lender and the homeowner have a problem.

Most lenders do not want to foreclose a loan and take title to a property. They are not property managers; they are lenders. Often, when they foreclose, they lose money on the loan. They cannot sell the property for enough to recover the loan balance and cost.

When a borrower loses a house in foreclosure, the event has a long-lasting effect on the borrower’s credit. When the borrower is able to borrow money again, it will be at a much higher interest rate. Banks will be reluctant to make another home loan to that borrower for many years.

Even more distressing is loss of the family home and the need to move abruptly into less of a house in a weaker neighborhood. This is traumatic to a family and can cause other family problems. If you can offer a solution to this serious financial problem, you can save the homeowner a lot of grief and money and personally make a substantial profit for your skill and efforts.

Foreclosures can result from misfortune, such as an accident, illness, or a job layoff. More often they are a result of a homeowner borrowing money on terms he cannot afford. Regardless of the reason for the foreclosure, the key to buying a property from an owner facing foreclosure is how you deal with the owner and the problem.

BEWARE OF THE FORECLOSURE SHARKS

Some people who buy properties in foreclosure are not tactful or even ethical. Buyers who use high-pressure tactics to get sellers who are behind in their payments to sign a contact may be breaking the law. Buyers who “steal” property, leaving nothing on the table for the sellers, don’t get many referrals or make many friends.

BUYING FORECLOSURES AND MAKING FRIENDS WHILE DOING IT

There is a different approach to buying properties in foreclosure. Much of my business comes from referrals. Previous sellers, borrowers, buyers, renters, and agents call me with repeat business and send me their friends. You can buy property from owners in distress and leave them with their honor intact and happy that they did business with you. The secret: deal with others as you would like to be treated if you were in their situation, and solve the problem.

NOT ALL FORECLOSURES ARE OPPORTUNITIES

Some property in foreclosure—as with property in general—is not worth buying because of its bad location or poor condition. Some owners are just too difficult to help or to make a deal with. Do not stray from your investment plan just to buy a property in foreclosure. Only look at houses in price ranges and in neighborhoods that you understand and that you know are profitable.

Often properties are in foreclosure because of a bad location, bad design, or bad concept. These problems may be expensive or even impossible to fix. If you buy these properties, even at a bargain price, you may become the next owner in distress. Frequently you will see the same house foreclosed on several times—there is a problem with that house, not just the owners.

FIVE SOURCES OF DELINQUENT HOMEOWNERS WHO NEED YOU

1. Homeowners who are in trouble and still trying to borrow more money

When a homeowner falls behind on her first mortgage, she often will try to borrow more against the house from a second mortgage lender to catch up on the payments on the first. These second mortgages are recorded in the public records and can be a source of leads.

Some lenders are much more aggressive than others and will make higherrisk loans. While most lenders want a certain level of credit and income, some lenders will loan to nearly anyone with income, even if that person is behind on his first loan and jobless.

Learn who the most aggressive lenders are in your area, and recognize that only the most desperate borrowers will borrow from them. Their interest rates and up-front fees will be high—and so will their default rate. If these borrowers were in financial trouble before, borrowing more money at a high interest rate will only compound their trouble. When you identify these borrowers, you are identifying people who may need to sell their house soon—and in a hurry.

You can identify these borrowers by searching the public records for loans recorded by these high-risk lenders and then contacting the borrowers. Simply tell them that you are looking for a house in their neighborhood, and ask them if they know anyone who wants to sell. This low-key approach opens the door to asking more questions if they admit that they want to sell.

Another direct approach is to meet with the people making these loans. They are paid on commission when they make a loan. You can offer them a finder’s fee to refer homeowners to you who need to sell, not borrow more. Even the most aggressive lenders turn down some homeowners because they have too much debt already. These homeowners may have little equity, but the lenders they owe may be willing to renegotiate the terms of their loans, allowing you to buy for a profit.

2. A second source of owners in trouble is advertising, bandit signs, and mailing postcards

Cash for Your House

Fast Closing

Save Your Equity

Call John anytime at 222-222-2222

Another approach that gets calls is:

Private Investor Has Cash

for Notes and Mortgages

Call John anytime at 222-222-2222

Ads and signs will get calls from people looking to sell or needing a loan. Both will generate leads. Your challenge will be screening them and following up on the good leads. Use a phone number that you can answer often; many of these people will not leave a callback number. If your regional newspaper is too expensive to run an ad for a month, try one of your small papers or shoppers.

Mailing postcards can be effective, but targeting your mail to those who might be in trouble means compiling or buying a qualified list. It will take repeated mailings to the same owners to get a response. I have seen stacks of letters and postcards from foreclosure buyers in houses that I have purchased. It’s a competitive and expensive way to find opportunity.

3. A third source is other house buyers who will be your “bird dog”

If your town is like mine, you have bandit signs or ads that say “I will buy your house for cash.” If you own houses, you may be getting letters from these same people. The buyers with these signs have limited cash. I have found that every buyer seems to have a favorite type of house and a favorite neighborhood. The secret is to find another buyer who is short on cash or has an interest different from yours and offer to pay him for leads on the houses that you like. These “bird dogs” will find you opportunities for a small fee, typically a few thousand dollars.

4. A fourth source is referrals from bankers and other lenders whom you may know

Local lenders often refer troubled homeowners to other lenders; when such homeowners are in too much trouble to borrow more, they refer them to buyers.

Understand that lenders will not call you and tell you about their customer. They will call their customers and tell them about you. To get these referrals, the lender must first know that you buy houses and then trust that you will treat people fairly. Lenders do not want negative repercussions from referring business to you.

5. A fifth source is property in good neighborhoods that is being neglected

I frequently drive and walk through neighborhoods I like, looking for empty or physically distressed property. While not every property that needs work is an opportunity, it is a free phone call to the owners to find out if they want to sell. Even if you only buy one in a hundred and it takes you three months to find one that you can buy, this is highly profitable work.

There are more sources, but this is enough to get you started. The key is you. You need to do research, make contacts, run ads, and canvas neighborhoods to generate the leads that you need. There are always opportunities.

TALKING WITH OWNERS IN FORECLOSURE

Many owners in foreclosure are not willing to answer questions or even admit that they have a problem. Try to help them, but don’t spend too much time with them unless they admit to needing help and are willing to accept it.

Explain the consequences of a foreclosure:

1. Poor credit will cause them to pay higher interest rates.

2. They may have to move into a much less desirable house.

3. They may not have enough money to move into any house.

4. They will lose their equity.

5. A new job or a promotion may require a credit check. An applicant who is under severe financial stress may not be a desirable employee.

6. A foreclosure can be a long-term family disaster.

TESTING THE OWNER’S MOTIVATION

Most sellers want you to come to look at their house. As a test of their motivation and willingness to cooperate, ask a homeowner in distress to come to you. Ask her to bring all her paperwork on the house.

Specifically ask for loan documents, title insurance, closing documents from the purchase, and any refinancing and all correspondence from the lender or lenders. These documents will give you the information you need to assess the situation and consider if you are part of a solution. A solution would be to make the owner an offer if you can make a profit in a transaction that solves her problem.

GIVING SOUND ADVICE TO DELINQUENT BORROWERS

Borrowing more money is not a solution when you cannot make your current payments. Unless you can roll the back payments into a new loan with a lower payment, you are just getting deeper into trouble. Refinancing loans in default is expensive and often has high closing costs and high interest rates. It may buy a little time, but often at a high cost.

If the house has enough equity to refinance, it has enough equity to sell. Selling may net the owners some cash, avoid a foreclosure, and give the owners some options they would not have if they were foreclosed.

Never lend money to anyone behind on his payments. First, it is not good for them. If they cannot make their payments now, how could they make new, higher payments? Second, there are complex laws in many states that protect homeowners who are in default from unscrupulous lenders. You may violate one of those laws even when you are trying to help.

BUYING A HOUSE FROM AN OWNER IN DEFAULT

Buying homes from owners in foreclosure is not as simple as it seems on late-night TV. Your first challenge is finding owners (1) who are behind in their payments, (2) who own a house that you want, and (3) who will agree to sell. Finding them is not difficult; getting them to make a good decision (to sell to you) can be. They did not get into financial trouble by making good decisions.

Another challenge is dealing with the lenders. In this era of megabanks, it’s a challenge to find the right person to talk to. Many loans in default are owed to lenders who have made higher-risk second mortgage loans. These lenders often are eager to talk because they are in a risky position. Some of these lenders are private individuals who are just trying to recover their capital.

A third challenge is finding the money to fund these purchases. Foreclosure buying can require a lot of cash. Lenders often will want cash for their positions. Investors who will loan you money at decent rates and will co-invest in longer-term deals are a good source, along with home equity loans and lines of credit.

DEALING WITH THE LENDERS

When borrowers quit making their loan payments, the lender begins writing letters trying to inspire them to pay. Understand that lenders do not want the real estate. They want their money back. While some lenders do make a profit when they foreclose, many more lose money. Foreclosures are an expensive distraction from their main source of profits—lending money.

A junior lender, one who has made a second, third, or even fourth position (behind other loans), is taking a bigger risk and often will be more aggressive and more creative in collecting her money.

Many first mortgages are insured for nonpayment through the Federal Housing Administration (FHA) or Mortgage Guarantee Insurance Corporation (MGIC) or are guaranteed by the Veterans Administration (VA), so the lender’s risk is lower. Second mortgage lenders rarely have insurance, so they are more willing to accept a partial payment when a loan is in default.

SOLVING THE DELINQUENT OWNER’S BIGGEST PROBLEM

To homeowners facing foreclosure, ruined credit and loss of equity are both small problems compared with having to move their family out of their home. They are facing a move into a rental house in a neighborhood that probably is far less desirable than their current one. An owner who has to move because of a foreclosure is no catch as a tenant and may have to accept the dregs of the rental market. Obviously, if an owner did not pay the lender, he may not pay the rent either.

You can solve this one big problem, but you must solve it carefully or you can become the victim. If you buy a house in foreclosure and then rent it back to the owners, there are three requirements:

1. Make sure that the sellers understand what they are doing. Because they are not moving, they may think that they are borrowing money, not selling their home. Be clear in what you say and specific in what you write down. Document clearly that this is a sale, not a loan. In a separate document, agree to rent the former owners the house.

2. Something has to change before renting to the sellers makes sense (either the house they are in or another rental you have). Has their income increased or their expenses decreased? How much rent can they afford to pay? They proved that they cannot afford the current house payments. How much can they afford?

3. Always build in a financial incentive for the sellers to pay the rent on time and then at some point to move out of the house and leave it in good condition. You want them to be able to afford the rent and then to leave you a house in good condition when they leave. They will be more likely to do these things if they are paid to do them. Build into your offer a below market rent if they pay on time, and also more money in the form of a large security deposit when they move out, if they leave the house clean and in good repair.

Buying a House and Renting It Back to an Owner Who Is Behind on His Payments

Many homeowners who are behind on their payments like their house and don’t want to move. Moving is expensive and not a lot of fun. You can buy a house using this strategy, but you must use a great deal of caution and common sense. Remember: If the homeowner is not making payments to the lender, you have to structure a deal that she can afford, or she won’t make payments to you either.

Important Note: Some states have laws designed to protect sellers who are behind in their payments. These laws may address buying a house from a seller who is behind in his payments and then renting it back to him. Other states allow the seller to back out of the contract within a certain period of time. Understand your state laws that deal with foreclosures before entering into any agreement with sellers who are behind in their payments.

NEGOTIATING A PURCHASE AND LEASE

If the sellers have equity in their house, you can let them use that equity to pay rent on either their own house or another. For example, if their house is worth between $180,000 and $200,000 (always give yourself a range of prices) and their loan balance with back payments is $120,000, then they have enough equity that you can buy and give them bargain rent.

The owners’ payments today (that they cannot afford) with taxes and insurance are $1,250 a month.

During your initial conversation, ask the owners what their house would rent for. They often have a high opinion of what their house is worth and what it will rent for. If during your negotiation you determine that they want to stay in their house, you can then use their rent estimate as a starting point.

If they guessed low or you are uncertain of the market rent, then you need to gather comparable market rent information to establish a rent. In the preceding example of a house with a wholesale value of $140,000, the market rent may be between $1,200 and $1,400 a month.

Next, it is important to determine the amount of rent that the owners can comfortably afford to pay. Ask them what they can afford. Ask them how much income they have. They should pay around one-third of their income in rent. Do not rent them the house at a rent higher than one-third of their income.

Next, establish the amount of security deposit that gives them enough incentive to give you the house in good condition. The amount will depend on the value and condition of the house and the risk that you are taking by renting them the house.

Always make the deposit greater than a month’s rent. If the house is in good condition, use several months’ rent. Some states have laws that set a maximum security deposit. Learn your state law—it will be under the “Landlord-Tenant” heading in your state statutes.

By keeping the rent low and the deposit high, you give the owners a large financial incentive to stay in the house and to give it back in good condition. If they leave early, you can rent the house to another tenant for more rent.

Assume that the owners in this example had lost their jobs but have now found new, lower-paying, jobs. Their monthly income has dropped from $5,000 to $3,000. With this income, they can afford to pay about 33 percent, or about $1,000 a month in rent.

Their greatest problem is finding affordable housing until they can get back on their feet. Moving is expensive. If you let them rent back their own home, you have saved them a lot of hard work and expense, not to mention the trauma of moving from their nice home into a neighborhood that they can currently afford.

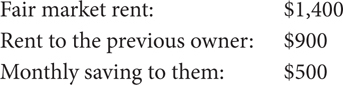

Offer to rent them the house for one year at the bargain price of $900 a month, a $500 monthly discount from the high end of the market rent of $1,400. Understand that $1,400 is retail rent. If you rented to another tenant today, you would be more likely to collect around $1,300 a month.

If you rent to them for twelve months at this $500 discount, they would save $6,000. In addition, you could give them a credit of $4,000 as the security deposit, which you would refund at the end of the twelve months if they turn over the house clean and in good condition. Giving this large a credit as a security deposit is important. You need to give them a significant incentive to keep the house in good condition, leave it clean, and leave on time.

Calculating the benefit of the lease to them is as follows:

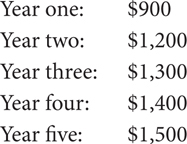

If they want to extend the lease and continue living in the house as tenants, then you can raise the rent to closer to a market rate. I have rented back to sellers for as long as five years at a reduced rate. You can build in an increase each year.

Using the preceding house with a market rent of between $1,200 and $1,400 today, a five-year monthly rent schedule could look like this:

By the time you reach the fifth year, you may be at market rent. Having a tenant stay in the house five years eliminates all vacancy costs, advertising costs, and a lot of maintenance expense. It can be a good deal for both you and the tenant. When you purchase a house using this technique, you often can make a deal that other buyers cannot make. You are offering a solution to the homeowners’ biggest problem: where to live. In addition, you are saving them from a foreclosure, helping their credit.

Before you make the offer, calculate your potential profit, and make sure that the profit you will make will be fair for the amount of money and risk you are taking. In the preceding example, you are buying a house worth at least $140,000 for a total price of $130,000 (the loan balance of $120,000, the rent loss of $6,000, and the security deposit of $4,000). You may be able to buy this house with little or no down payment, depending on your ability to negotiate with the lender. If so, your risk is relatively low, and your profit potential when the former owners move out in a year should be a minimum of $10,000 and hopefully more.

WHEN NEGOTIATING WITH LENDERS, ASK FOR MORE THAN YOU EXPECT

Before you take title to a property, contact the lender. You need to talk with a high-ranking employee who has the authority to renegotiate the terms of the loan. This may be the president of a small bank, the senior mortgage officer of a midsize bank, or the person in charge of the department in a large bank that handles delinquent loans. You often can get the name and number of the appropriate person from correspondence sent to the homeowners by the lender after they fall behind in their payments.

You often will begin with a lower-level employee and have to ask to speak with the supervisor. Keep asking until you get to a decision maker.

Remember, you are dealing with employees in a big institution. It’s not their money, but a bad loan is their problem. You can be the solution to that problem.

If the lender is a community bank, go right to the president. She will be the decision maker and it is likely that some of what’s owed is her money.

Once you are speaking to the right person, you need to have a plan. You can ask for many things that would benefit you, for example, a lower interest rate, a lower monthly payment, and the forgiveness of the back payments and penalties. If they won’t forgive the back payments and penalties, ask them to add the amount of any delinquent payments to the loan. Often you can negotiate that the bank will let you sell the house to a new buyer who can assume the loan without qualifying.

Ask for a lot. It will work in your favor because the lender will see you as a professional buyer, not an amateur.

OFFER TO BANK WHEN BUYING A SECOND IN DEFAULT

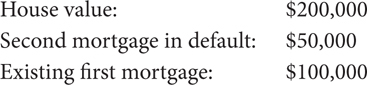

If an institution owns the second mortgage or trust deed in default, see if it would be willing to lend you enough to pay off the first loan and add it to the second mortgage. That lender then would have a first mortgage in the amount of both the first and second mortgages.

The bank with the second agrees to make a new first loan in the amount of $150,000 that would replace both existing loans.

Negotiate aggressively on the interest rate and terms so you will have cash flow immediately from the rents that you collect. You may agree to a shorter-term loan, say, ten years, to get a lower rate. If you need money to fix up or remodel the house, ask the lender to lend it to you and add it to the loan. If it’s a great deal for you, but the lender is unwilling, offer to pay down the existing loan by $10,000. You could also give the lender a second mortgage on another house that you own with more equity.

BUYING AT A FORECLOSURE AUCTION

This is the most dangerous, but potentially lucrative, time to buy a property. Both lenders auctions and municipal auctions to collect back taxes are opportunities to buy at steep discounts, but the terms are all cash, often due the day of the sale, and you might not have much information about the property.

A house sold at a tax or foreclosure auction may be occupied. If owners are losing their home, or a tenant losing his rental, whoever is about to be evicted will not be happy. I’ve seen houses significantly destroyed by owners losing them. Tenants are unlikely to clean and paint on their way out, since they will not be getting their deposit back. It can take more money to repair the house than it is worth.

If you ever bid on a house in foreclosure, meet the occupants and offer to pay them to leave the house in good condition if you buy it. If you can agree on a reasonable number and you are the winning bidder at the sale, then you might get the house in good condition.

If you are not the winning bidder, find out who is and go talk with them. They may be willing to sell to you for a quick profit and you might be able to buy the house at a price that you like.

An empty house is much safer to buy. Just because it is empty today, is no guarantee that someone won’t move in tonight. Empty houses in foreclosure often attract squatters, who will not improve the house.

BUYING FROM A LENDER THAT HAS FORECLOSED

A much safer time to buy is after the bank has foreclosed, evicted the occupants, and taken possession. The house may need a lot of work, but you have a good idea of how much. I have bought several bank-owned properties that were in good condition. That is the best house to buy, because you can rent it immediately.

Banks will often get multiple offers on REO (real estate owned) property. You increase your chances of buying by: (1) Offering all cash and a fast closing. Generally, ten days is acceptable. (2) Offer to accept the property in its “as is” condition, subject to your inspection. Your inspection period can run up to the date of closing if it’s only ten days.

Banks can and do finance the sale of their foreclosures, but if the price is more important make a cash offer. See Chapter 8 for ideas on financing.

BUYING FORECLOSURES TAKES KNOWLEDGE AND EXPERIENCE

There are a lot of highly skilled, professional foreclosure buyers. This group includes attorneys and others with knowledge of the system and the market. They are your competition. Buying foreclosures successfully requires experience, knowledge, and good legal advice.

In a rising interest-rate market, there are generally more foreclosures and a good deal of opportunity. Although tremendous opportunities are available, be careful not to buy beyond your ability to manage and handle the cash flow.

Let this be the beginning of your education, because there is much more to learn. If you are a beginning investor, get good legal advice before bidding at a foreclosure sale or entering into a contract to buy a property from owners who are behind on their payments. The laws that govern the sale of foreclosures change. Check them before you buy.