1

HOW BUYING ONE HOUSE AT A TIME CAN MAKE YOU WEALTHY

Everyone knows something about houses. Ask them, and they will tell you their opinion about what house prices are doing; they even may tell you about a good deal they just missed. Most people agree that a house can be a good investment, yet only a few actually make money investing in houses.

Houses are not complicated, and they’re not scary. Their performance is predictable. They produce income when rented, and house rents have a long history of increasing. Likewise, house prices have increased at an average annual rate of roughly 5 percent for about as long as we can measure. They don’t go up every year, and in recessions they can drop in price.

When houses are not going up in price, you will make your best buys. The old adage, “You make your money when you buy,” has a double meaning when buying houses.

First, you have to buy a house to make money. Just looking won’t make you rich. Second, you can make thousands of dollars in profits every time you buy if you buy a house that someone else does not want.

WHY HOUSES ARE YOUR BEST INVESTMENT

After years of investing, I still buy houses instead of apartments or shopping centers. Why? Houses make me more money with less work than any other investment.

There is a common conception that apartments or commercial buildings are less work. I’ve owned both, and I can tell you that this is not true. The tenants in apartments and commercial properties come and go often. Every time they leave, the property will need work. Every time they move, you need to find a new tenant. Tenants in both apartments and commercial buildings are very demanding. They want an immediate response when something breaks. In short, apartments and commercial property are not passive investments. They require hands-on management and an owner who is available 24/7 for problems.

House tenants are different. First, they tend to stay longer. This is a big deal, because a long-term tenant reduces both your maintenance and vacancy expense. My house tenants typically stay five years or longer. That gives me five years of no vacancy and five years of low maintenance expenses. You don’t have to repaint the inside or clean or replace the carpet until they leave.

You want to buy property that attracts long-term, low-maintenance tenants—tenants who will pay rent and take care of your property. You want to buy a property that you can rent to tenants who want your house more than you want them.

A side benefit of buying and managing houses is that you can help people sell houses they don’t want anymore. You can rent houses to people who need a place to live, and when you sell, you can help people buy their first home. You can solve big problems by buying a house that an owner can’t afford and that is ruining their credit. These are all profitable and rewarding experiences.

HOUSES ARE DIFFERENT FROM OTHER INVESTMENTS

Houses are unique investments. You can rent them to provide income, but their value does not depend on that income. Even an empty house can make you money, since it will appreciate as much as a full one. I know investors who buy houses in appreciating areas like San Francisco and never rent them. Many wealthy individuals own many expensive houses in places like Aspen or Palm Beach and never rent them. They are happy with the appreciation alone.

The value of other investment real estate, such as apartments or commercial property, depends on the amount of income it produces. If you rent an apartment or office space for below-market rent, it will be worth less money. An empty house is worth as much as a full one.

Houses Are Safer and More Liquid

Houses are safer investments for several reasons. First, you can buy a house with a smaller investment. You can buy a house with a small down payment, so you have less at risk. Lenders routinely will lend more against a house than any other type of property. And the loans that they make are safer, because they can be for a long term with a fixed interest rate and payment. This makes the payments smaller.

Loans on commercial properties are often shorter in term and some have variable interest rates. A shorter-term loan is riskier, because the payments may be higher and you may have to refinance or sell in a down market.

Next, there are more buyers for houses than for bigger properties. If you need to sell in a hurry, you can—if you offer a house at a good price. Third, houses rent faster and have fewer vacancies. Apartment vacancies often run 10 to 20 percent, whereas house vacancies rarely exceed 5 percent. Commercial properties sit empty for months and even years at a time between tenants. You need a lot of cash in the bank to survive a long-term vacancy in a large building.

WHEN YOU BUY, YOU ARE DEALING WITH AN ANXIOUS SELLER

When you buy a house, typically you are dealing directly with a homeowner who is in a hurry to sell. If the homeowner had plenty of time to sell, then she could wait for a retail price. When you decide to sell any real estate in a hurry, you will have to discount the price to sell it quickly. Learn this lesson: Never put yourself in a position where you have to sell in a hurry.

When you buy commercial or apartment property, you are buying from another investor. You are often dealing with someone who is an experienced negotiator. He might be a better negotiator than you are and that reduces your chances of making a good buy.

When you buy from a homeowner, you have the negotiation advantage. They want to sell more than you want to buy, and you won’t buy unless you get the price or terms that you need.

WHEN YOU SELL, YOU WILL GET A RETAIL PRICE AND ALL CASH

More important, when you decide to sell a house, sell only to a user. You want to sell to someone who really likes the house, because if they really like your house, they will pay a retail price. I had a potential buyer looking at one of my houses and they called me on their cell phone to ask me a question. I overheard the wife say, “I love this house.” I knew then that they would pay full price for the house.

Now, for the really important part! When you sell a house to an owner occupant, that person usually can get a long-term, low-interest-rate loan for nearly the entire purchase price. This allows you as the seller to get a higher price. Plus, when they borrow from the bank to buy your house, you will receive all cash when you sell.

If you want to finance the sale of a house to generate interest income, you have that option. There are always buyers who need help with financing, and often you can sell at an even higher price if you will agree to finance the property for a buyer who cannot qualify for a bank loan. However, if you want the cash to reinvest in another house or just to spend, you can achieve that.

A disadvantage of selling an apartment building or commercial property is that the buyer will be another investor. This investor will not “love” your apartments. They will negotiate to get the best price and terms that they can.

LENDERS PREFER HOUSES

Unlike houses, apartments and commercial properties are not the banks’ favorite collateral. Because commercial loans have a higher risk of default and more management responsibility in the event of a foreclosure, banks often limit their commercial loans to 70 percent of value and the term of the loans is often shorter. Often the buyer will not have enough for the down payment, so the deal falls apart, or the seller must agree to finance part or all of the price.

Investment property prices can experience large swings as the economy changes. An empty office building or commercial building will sell for a small fraction of what it cost to build.

A well-located house will appreciate at a greater rate than an average property and will not suffer as dramatic a drop in value as commercial properties during business recessions.

DIVERSIFICATION BRINGS SAFETY AND HIGHER PROFITS

Not all houses perform the same. Higher-priced houses may jump more in price during a boom but can fall in price during a recession. Lower-priced houses are more stable and stay full. It costs a certain amount to buy a lot and build a starter house in your town, and that price is constantly increasing. This supports the lower-priced houses in the market.

A major advantage of investing in several houses rather than one big apartment or office building is that you can diversify by investing in different price ranges. By owning both less expensive and more expensive houses, you can have the safety of the lower-priced houses and the upside potential of the higher-priced ones. Plus, if you needed to raise just a little cash, you could sell just one of your houses. If you owned an apartment building it would be difficult to sell just a part of it to raise cash.

When Average Isn’t Average at All

Read reports of prices booming or busting with a little skepticism. Remember that the headline writer’s job is to sell newspapers or attract page views, and a spectacular headline is more likely to get him a bonus.

When the press reports that the average price of a house has risen or dropped, that report is often an exaggeration of what is really happening in the market. The average price of a house sold in your town will include the more expensive houses, which are more likely to stop selling when the market cools off.

There is no national house market or national trend for real estate. Although some factors, such as interest rates, the economy, and national security, have national implications, even these affect different housing markets differently. A hurricane in Texas has little effect on the markets in other states.

Housing markets are local in nature. The market in your state can be booming while the next state over is experiencing a recession. In your town, one neighborhood may be appreciating while another is declining in value.

Changes in interest rates will have a more profound effect on house sales in towns where there are a lot of first-time buyers than in a town where many buyers are retired and pay cash for their homes. A threat to national security may drive prices up in areas considered safer while depressing prices in areas perceived as higher risk.

HOW AVERAGES CAN MISLEAD

Suppose that last month four houses sold in your town, and they sold at these prices: $100,000, $150,000, $150,000, and $400,000. The average price of a house sold that month was $200,000. If the following month four other houses sold at $100,000, $150,000, $150,000, and $200,000, the average price of a house sold in your town that month would be $150,000.

Just because the average price of a house sold in your town dropped from $200,000 to $150,000 in one month does not necessarily mean that houses are decreasing in value. It simply means that fewer expensive houses sold that month.

Averages include houses that you don’t want to own. Track the prices of houses in neighborhoods that you do want to own. Research what a particular house sold for new and compare it with its resale price to get a real appreciation rate for a neighborhood that interests you.

HOW TO LEARN AND ANTICIPATE THE REAL TRENDS IN YOUR TOWN

To learn how houses have performed as investments in your town, identify several houses that have sold recently in neighborhoods that you think would be a good place to invest. Research what those houses sold for in previous years. You can find this information in your public records. In the past, this usually meant a trip to the courthouse, but now this information is often available online.

Now calculate how much these houses have increased in value per year on average. Continue to track these houses, and add others to your research as you discover other neighborhoods that you think have potential. This information will help you to identify neighborhoods with a strong history of growth, and you will begin to learn the values in your town.

Neighborhoods and towns are dynamic. They are changing constantly, and you need to become a student of that change. Neighborhoods and towns change like the seasons. If you are paying attention, you can feel, see, and recognize the signs of change early in the cycle. This will enable you to be among the first to buy in a market changing for the better and among the first to sell in a market changing for the worse.

FACTORS THAT AFFECT HOUSE PRICES IN YOUR TOWN

Changes in Population

A growing population will create an increasing demand for housing. If your town is growing in population, then your prices probably will outperform the national average. If your town is losing population, your prices may not increase without inflation and could decline if the loss in population is permanent. People make real estate valuable. Without people, land has little value except to hold the earth together.

Changes in population in nearby communities will also affect your market. If a nearby city is growing rapidly, then it will have a positive effect on your market.

Demographics

When populations change, it’s not just in number. As new people move into your town, they will have new needs and demands. If there are young working people moving to your town because of jobs, they will need houses appropriate for children and will want to be near schools and parks that cater to family activities.

If the newcomers are retired, then they may want to be near medical centers, entertainment facilities, and restaurants. The US Census Bureau is a valuable source of information about age, income, family size, and education levels (www.census.gov/housing).

Government Regulation of Developers and Builders

As populations boom and overwhelm roads, parks, schools, and other public facilities, it is typical for the existing population, through the local government, to react and take steps to slow growth. The result is often a steady increase in the cost and time required to develop land and build new houses. Because it costs more to produce a new house, the existing housing market becomes more valuable.

Inflation

Inflation is increasing prices as a result of an increased supply of money and credit. Picture fifty college students in a room. You show up with tickets to a popular sold-out concert that you will sell to the highest bidder, but only for cash. The sales price would be limited to the amount of money in everyone’s wallet at the time.

If before you held the auction you gave everyone in the room $100 in cash, then it’s pretty predictable that the amount that they would be willing to pay for the tickets would be higher because they had more money. If you would allow them to bid any amount they wanted and would agree to pay you in one year at 6 percent interest, the price bid would be higher still.

The federal government can stimulate economic activity by increasing the amount of money we all have. It does this by both increasing the amount of money in circulation and increasing the amount of money the government lends to banks at relatively low rates. The banks, in turn, can lend this money to consumers and businesses, thereby stimulating buying.

Inflation will drive up the prices of all commodities, including land and house prices. Buying houses protects you against inflation, because both your house prices and rents will keep up with inflation. A leveraged house will allow you to make a dramatic profit with inflation.

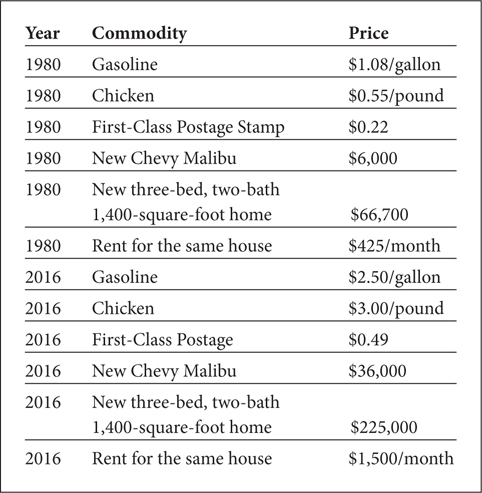

Compare prices of commodities that you buy every day with the prices of houses in your town and the rents that they produce. Table 1.1 shows some numbers from my town.

Table 1.1 The Effect of Inflation on Your Purchasing Power

Compare the numbers in your town. The relative value of these items has not changed much. Inflation of the currency has changed the amount of money it takes to buy these items.

Some people are confused by the fact that the prices for some items seem to be cheaper, such as computers. When a new product or technology hits the market, it will be priced high in its early years until the demand increases. This increased demand allows manufacturers to increase production to levels where prices fall because of the economy of producing thousands or millions of the same product. Another factor that can drive down prices is competition. Nothing inspires competition like extraordinary profits.

In inflationary times, you want to invest in assets, such as houses, that protect you from the tremendous loss in purchasing power that inflation causes.

Inflation hurts the investor with cash in the bank. With $100,000 in 1970 in my town, I could have bought five brand-new homes. With the same $100,000 in 2004, I could buy one-half of a house. If you plan on being here twenty-five years from now, that same house may cost you $2 million.

Inflation also hurts those who invest in fixed-income investments. If you bought an annuity or held a mortgage with payments of $500 a month in 1970, you would have had enough income to buy a new car every four months. With the same income in 2004, it would take you forty months of income to buy the same car.

“Everyone can predict the future. Unfortunately, the future usually pays no attention.”

—Dr. Gary North

If the next twenty-five years are anything like the last twenty-five, the investor with cash in the bank or holding fixed-income securities or mortgages will be hurt, whereas investors in real estate will benefit.

HOW 5 PERCENT PER YEAR AVERAGE APPRECIATION CAN MAKE YOU RICH

Over the long run, the average house in the United States increases in price about 5 percent per year. How can an investment that goes up 5 percent per year make you rich?

If you buy a house that will produce income, your return will be much higher than 5 percent. If you borrow most of your purchase price, your rate of return could be 30 percent or more.

Suppose that you bought a house worth $200,000 and paid a retail price. If you borrowed 80 percent of your purchase, you would need a 20 percent, or a $40,000, down payment. If the rental income would just cover the monthly payments, and the house appreciated at 5 percent the following year, 5 percent of $200,000 is $10,000, a 25 percent return on your $40,000 investment.

If you learn how to buy a house at below-market prices and then finance even more of the purchase price, your rate of return increases considerably.

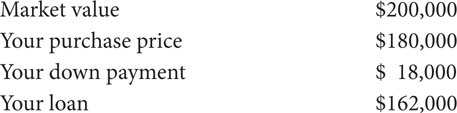

Suppose that you bought the same $200,000 house for $180,000 and were able to buy it with a $20,000 down payment. You still get 5 percent appreciation on the full $200,000, so you will earn $10,000 on a $20,000 investment—not accounting for the $20,000 profit you made when you bought the house.

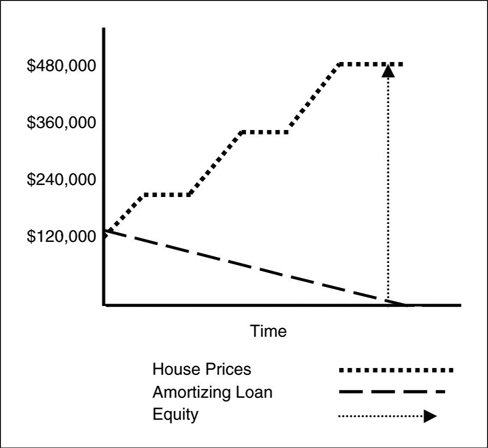

The power in buying real estate on leverage comes in the following years as your profits increase at a compounded rate. The next year your house would be worth $210,000 and go up another 5 percent, or $10,500. The amount the house value goes up increases each year; at the same time, you are paying off debt (see Figure 1.1).

FIGURE 1.1 Increasing Equity and Decreasing Debt

Real estate fortunes are made by buying houses and by then financing them so that you can afford to hold the house until it is free and clear of debt.

Doubling Your Money—The Rule of 72

Do you know how long it takes an investment to double in value if it goes up 5 percent each year? The answer can be calculated by using the mathematical rule of 72, which states that you can calculate the time it will take to double your money by dividing the compounded rate of return (the interest you would earn on a savings account at a bank) into the number 72 (see Figure 1.2).

FIGURE 1.2 Number of Years to Double Your Money

Thus, 72 divided by 5 equals 14.4. It will take 14.4 years for a house that increases in value at the rate of 5 percent a year to double in value (72/5 = 14.4 years).

DOING BETTER THAN AVERAGE

You want to buy houses that will double your money sooner. You can shorten the time it takes significantly by doing two things:

1. Learn how to buy a house for less than its retail price. The 5 percent average appreciation is based on retail prices. When you learn to buy below retail, your rate of return will be significantly higher.

2. Buy a house in an area with better than average appreciation. Some of my houses have averaged 12 percent a year appreciation. At that rate, they double about every six years. If I can buy a house at a below-market price that will double in value in six years, I can shorten the amount of time it takes me to turn my 10 percent down payment into $300,000 to four years or less. Look at these results.

The house appreciates at 12 percent a year and doubles in value in six years.

This does not include cash flow produced by the rental income.

BUYING WITH NOTHING DOWN

Read the classic book Nothing Down, written by my former student Robert Allen. Robert was a young real estate agent when he took my seminar in the mid-1970s. He bought a number of properties and then wrote about his experience.

You can buy property with nothing down. If you doubt that, look for a property in your town that has been empty for six months or more. Make the owners an offer with nothing down and agree to take responsibility for the property and begin making them monthly payments. When you own an empty property for months and months, the prospect of someone else taking care of it and making monthly payments to you looks good. I know!

Some properties that you can buy with nothing down, you may end up selling for nothing down to the next adventurer. There is a lot of property that is only attractive to people with no money. As you acquire more money, you acquire better taste in property.

Sometimes great properties are available with nothing down. It’s not the property that has the problem; it’s the owner. Find an owner who has a big problem that he cannot solve, and you may have found an owner who will sell to you with nothing down.

A local lender foreclosed on a property that was occupied by several tenants and a pit bull. After the dog chased the bank representative off the property, the bank sold the property the next week at way below market and nothing down.

WHEN YOU BUY WITH NOTHING DOWN, YOU OWE IT ALL

When you buy a property with nothing down, you owe the full amount of your purchase price. The terms you get on the money you borrow are more important when you borrow the entire amount than when you buy with less leverage. If you can’t make the payments, you will not own the property long enough to make a profit.

You need a plan to generate enough income to repay the loan, or you will soon lose the property. Buying with high leverage is risky business. It is a great way to acquire property when you are starting, but it’s like driving a car at a high speed. You need to be totally focused on what you are doing, or there is a good possibility of a wreck.

Another student of mine purchased more than 100 houses—really—the year after he took my class. He bought many of them with nothing down because he was starting out with almost no money.

Unfortunately, he bought faster than he could find good tenants. Eventually, he sold most of these properties for little or no profit because he could not afford to make the payments on a lot of empty houses.

If you buy more than you can manage, nothing down can lead to nothing left.

Buying 100 Houses—One at a Time

Other investors have accumulated more than 100 houses following my advice to buy them one at a time.

Buy one, rent one, then—and only then—look for the next deal.

By using this strategy, you will learn management at the same time you learn to buy. Ask yourself this question: If I begin buying houses, will I make a better deal on my first five houses or the last five houses that I buy? If you are learning from the experience, you will make much better buys on the last five houses.

* Using the rule of 72, the compounded rate of return can be figured by asking how often $18,000 doubled in six years. The answer is 3.74 (18,000 × 2 = 36,000 × 2 = $72,000 × 2 = 144,000 × 1.74 = 250,000). It doubled then about once every 1.6 years (6/3.7). To calculate the compound annual rate of return, divide 72 by 1.6 and the answer is about 45 percent.