15

No Permission Required

The Permission Monster

The old saying goes that it's better to ask forgiveness than permission. The supposition here is that sometimes permission (for whatever it is that you are wanting to do) won't be granted and most things, even if they weren't going to be technically allowed, are forgivable. (Note, we are not talking about breaking the law. Don't break the law.) The concept of acting now and asking for forgiveness later has been used by schoolkids and business magnates, professors and politicians, dear friends and not‐so‐dear colleagues. It points to something common, however: that there is an authority who must allow whatever action you are taking.

Never was this truer than in the world of finance, where your bank is the ultimate authority on whether or not you can access your money. Your bank is a gatekeeper of funds – and that's for those who can get a bank account. Many cannot even get permission to open a bank account.

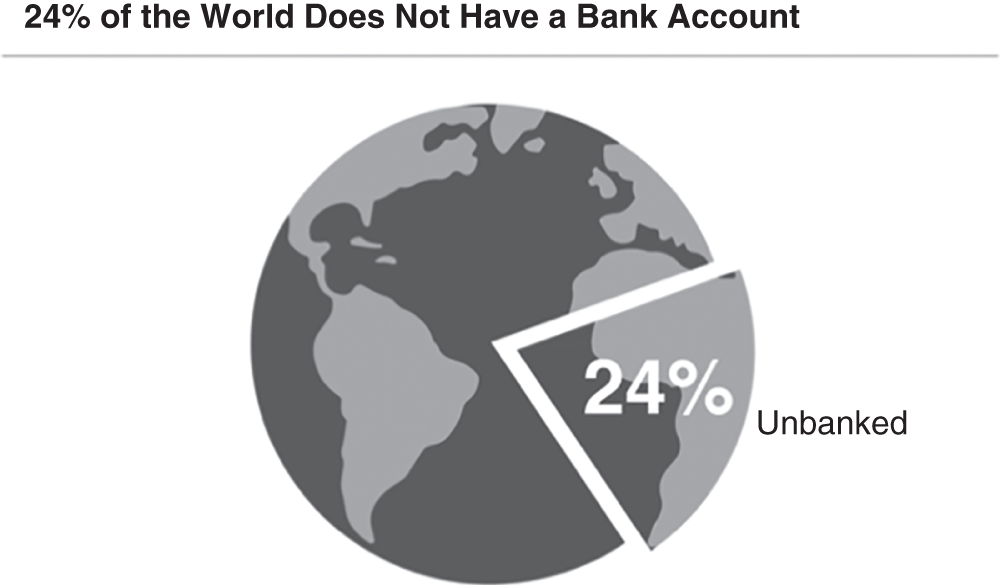

As noted in Chapter 4, as of 2021 24% of the world does not have a bank account (see Figure 15.1). That's approximately 1.9 billion humans; if we take out minors, that's 1.4 billion adults.1

The reasons for this are wide and varied but ultimately boil down to a lack of funds to meet bank minimums or fees, denying access and availability of financial institutions, especially in emerging markets. The common element here is that banks require you to meet certain requirements to use them. In some cases – whether it is your credit, past history, availability of funds, or just reporting errors on public (and private) databases – people can be denied access even if they do have funds. That's permission required.

Figure 15.1 Unbanked World Population

This problem is exacerbated as almost all unbanked people are in emerging markets, with India having the most unbanked in the world, followed by China, Pakistan, Indonesia, and Nigeria. Not to make this even more inflammatory, but the facts also reveal that the majority of the unbanked are women.2 Finally, lest one think that this is still an emerging market–only problem, approximately 4.5% of all U.S. adults are currently unbanked.3 Permission required.

Now, an essential corollary to this is that we need to consider that banks aren't interested in everyone having access to financial services. They are businesses run as businesses in order to make a profit and, if you can't help them do that, or if you are considered too high a risk, then, voilà, no bank for you. Permission required.

The Permission Monster can even step in when you are trying to use your own money. Lest you think that this is not a problem in the Western world, it happens here all the time. As a case in point, I have a colleague who was looking to invest in a business and the bank simply refused to wire his money at his direction. He had valid ID, proof of funds, and a working bank account at a global institution (that shall remain nameless), but they just wouldn't send the wire, for reasons known only to the bank. Ultimately, he withdrew all of his funds – which was a significant amount – walked across the street, and opened up an account with the bank's competitor, who then gladly wired the funds. What a pain for my friend, though. Permission required.

Please note that I'm talking about bank basics here – a place to store, access, and transfer money. The permission problem grows exponentially when one considers loans and credit, as anyone who has ever been declined a loan knows, or simply to have a way to have one's money work for them. Permission required.

The Permissionless Solution

What if you could conduct a transaction and you didn't need to get Big Brother's blessing? What if you could make a trade or purchase simply because you and someone else wanted to, without asking a bank, a vendor, or the government (or your parents, for that matter)? Well, that's exactly what you can do with the blockchain breakthrough. We're going to call this the Permissionless Solution.

Blockchains are built to be permissionless, meaning that they are open to everyone. Anyone can create a wallet, which, as noted in Chapter 2, is simply a place on a phone or computer that has access to crypto assets. Anyone can store funds there. Anyone can then send them to anyone else. No one has to grant permission. Period. This breakthrough cannot be oversold.

Let's say Bob, who lives in America, wants to send Sally, who lives in Africa, $1,000. If we look at the traditional banking example, there are a few hoops to jump through, and the process would look something like this: First, Bob needs to apply for a bank account. Apply. Once the myriad paperwork is filed, someone allows Bob to use a bank by granting him a bank account (permission). Once the bank grants Bob an account, Bob needs to ensure that Sally has a bank account (permission). Then, through interbank transfer, generally wire and with the bank's consent, Bob can send money from his account to Sally's. We want to underscore the bank's permission point here. I have seen plenty of places where banks refused transactions for reasons that are – absurd. Mostly because they didn't want to. Finally, for the privilege of using your own money, the bank will generally charge one or even both of you a fee.

One of the breakthroughs that blockchain technology provides is the ability to get things done without any of these hoops. Technically, these permissionless transactions occur on public blockchains. That's a mouthful of words, so let's break it down. A public blockchain is a blockchain that anyone can use. It's available to you, me, our parents, our kids, the janitor, the president, and anyone else. Bitcoin is an example of a public blockchain. It is also permissionless, which means that anyone can use it. There is no approval to be granted. It's the opposite of big banks. All Bob needs to do is to create a wallet using any of hundreds of wallet apps. In general, as long as you have a phone or a computer with access to the Internet, you can get a free wallet. Crypto wallets are many and we're making no recommendations here, but they include soft wallets like Exodus and Electrum or hard wallets like Ledger and Trezor. Fortunately, most humans on the planet have a cell phone, including the unbanked.4 It costs no money to keep money in your Bitcoin wallet. There are no bank fees. You don't need approval to do anything with your money. And a whole new world of financial solutions are available. This changes everything.

Back to Bob. In our permissionless example, Bob has a wallet. Sally has a wallet. Bob sends Sally some bitcoin (BTC). It shows up in minutes and costs pennies. Notably, there were no gatekeepers. No fees. No approvals. No wonder it's taken the big banks a while to warm up to this – they lose control! Note that most crypto wallets are not just limited to BTC; they can also store NFTs (digital goods), governance tokens, utility tokens – any crypto asset. For this chapter, we're just going to focus on money, but this universe expands quickly.

The Game, Changed

Imagine, if you will, then, that you were unbanked. You had no way to easily store, save, and transfer money. How would life be different? Consider first that buying food would be a challenge. Buying clothes would be a challenge. Buying … anything … would be a challenge. A good portion of your day would be devoted to addressing basic human needs – and this is without even considering that more and more, we're moving to a worldwide society that favors cashless transactions. Without a place to safely store and accumulate money, it's virtually impossible not only to transact but to handle life's necessities. Your life would ostensibly be about … surviving life. This is how it is for approximately one‐quarter of the world.

There is an argument that the unbanked are generally poor and therefore don't have enough money to put into a bank account, but we argue that this is a case of the expense of poverty creating a vicious circle. Let's take a look at an example close to home. Say Mike earns minimum wage but has no bank account. The current federal minimum wage is $7.25 per hour, so working full‐time Mike would earn a gross income of $15,080 per year, which we think we can all agree is not livable, so let's double that to a basic minimum of $15 per hr. At that wage, Mike is now earning $31,200, or $1,200 every two weeks, as a gross number. After deductions, in Texas that comes to about $992 net (note that Texas is a state with no state income tax!). But how does Mike get access to his money? Well, with no bank account, that leaves cash. Check‐cashing services are most happy to provide a service and give you cash, but this privilege can cost anywhere from 1% to 12%. For purposes of our example, let's take a lower‐end number of 3%. This means that of that $992, Mike would have a check‐cashing payment of $29.72 per check, or almost $30 in fees per month. That's insane.

In this case, banks make it almost impossible for those who do not have a means to save because they are nickel‐and‐dimed (literally) with fees. No wonder Mike remains unbanked – it's expensive! Now, what happens if Mike wants to send money abroad? There's just no cost‐effective way to do it. Wires cost money, cashier's checks cost money, and services like Western Union certainly cost money; even if a transaction is not fee‐based, there are hidden costs baked into currency exchange rates. Sending cash in the mail is a fool's errand, so there are no good solutions. The bottom line is that operating without a bank account is simply expensive.

Now, let's change the game. Let's suppose Mike could receive payment directly into a crypto wallet with no fees regardless of the source, whether the deposit is from his work, his family, a friend, or whatever. In the case of work, it makes a huge difference, bringing an additional 3% in realized funds into his account. Now that the funds are in his control, he can safely store, save, and transmit funds at virtually no cost to anyone in the world who has a crypto wallet.

This now also opens the world to permissionless financial services. These are services that are not available to Mike if he is unbanked. Now we bring in DeFi protocols, introduced in Chapter 4, where you generally don't need permission to utilize a blockchain DeFi contract. You simply need a crypto wallet.

This changes the game. Mike can put the 3% he would have spent in fees into a DeFi protocol and make money on his money. If Mike opted for a DeFi contract that earned him 5%, the net difference to him at the end of the year is $832. At the end of five years it is $4,474. That's money the banks would have gobbled up in fees. Saving requires some discipline, but at least there is the opportunity available that simply was not available before.

Now let's take this global. With citizens worldwide now able to save a little more, to help their families a little bit more, to keep the money they earn, we can impact economies across the world. We can decrease poverty and make the world a better place for everyone. According to the Borgen Project:

Issues like hunger, illness, and poor sanitation are all causes and effects of poverty. That is to say, that not having food means being poor, but being poor also means being unable to afford food or clean water. The effects of poverty are often interrelated so that one problem rarely occurs alone. Bad sanitation makes one susceptible to diseases, and hunger and lack of clean water makes one even more vulnerable to diseases. Impoverished countries and communities often suffer from discrimination and end up caught in a cycle of poverty.5

Helping people not only keep their money but providing the ability for them to grow their money is powerful. We're not naïve here; we know that such a change is not going to happen overnight, but empowering people with money universally is something that is possible with blockchain‐based permissionless systems.

We saw this with the impact of cell phones and microloans, which are small loans (in some cases as little as $50–$100) made available to even the unbanked. Both are transformational tools for 24% of the world's population without access to banks. Cell phones allow the availability of information that was, to many, inaccessible. In addition to simply providing the ability to communicate, they allow access to global news, educational content, political information, economic tools, social networks, and so much more.6 With landlines generally almost impossible to get in many emerging markets such as Africa, the cell phone has allowed those traditionally excluded from society to engage. It has allowed them to have access to information that others simply take for granted. This has had a profound effect on learning and opportunity. Cell phones have provided the initial entry into the world of mobile payments with applications such as M‐Pesa (an African application that allows users to store and transfer money via their phones), which we would consider a proof of concept if you will for permissionless wallets.7

Cell phones also provide access to a variety of data, such as usage habits, which have been used in emerging markets to determine creditworthiness and lead to microloans. Microloans have significantly changed the shape of emerging markets by providing basic, working capital to individuals and small businesses. In the West, where just about everyone has a credit card, we take this for granted, where the ability to charge now and pay later for groceries, rent, supplies, and so on is a way of life. Getting credit is equivalent to traveling to the Moon in emerging markets where it's difficult to get a bank account. A few have done it, but it's pretty rare indeed. Enter microloans, which can ease the burden of everyday life and financial hardship. According to a research study conducted in Bangladesh, microfinance accounted for a 40% reduction of poverty. In addition, farmers across the African countries are adopting microlending to buy crops. People in rural areas are taking loans from microlenders to set their own business and raise their standard of living, which propels the growth of the market.8 Mobile phones and microloans are technological advancements that have changed emerging markets.

Permissionless blockchains serve as a transformative tool for people to access and leverage money, including people who haven't traditionally had that access. This is a game changer for those individuals and the communities and economies they live in. These tools not only will drive positive social and economic impact in emerging markets, but will help anyone looking to have a powerful relationship to their money because, frankly, it is theirs. Last I checked, you shouldn't need to get permission to use your own things. Game changed.

Notes

- 1. Global Findex Database, https://www.worldbank.org/en/publication/globalfindex/interactive-executive-summary-visualization#.

- 2. http://www.wsj.com/ad/article/mlf-women-around-the-world-face-hurdles-to-financial-inclusion.

- 3. https://www.fdic.gov/analysis/household-survey/index.html#:~:text=An%20estimated%204.5%20percent%20of,the%20survey%20began%20in%202009.

- 4. Global Findex Database, https://www.worldbank.org/en/publication/globalfindex/interactive-executive-summary-visualization#.

- 5. https://borgenproject.org/how-poverty-effects-society-children-and-violence/.

- 6. https://www.pewresearch.org/internet/2019/03/07/mobile-connectivity-in-emerging-economies/.

- 7. https://www.economist.com/special-report/2017/11/10/what-technology-can-do-for-africa.

- 8. https://www.alliedmarketresearch.com/micro-lending-market-A06003.