Live the questions now. Perhaps then someday far in the future, you will gradually, without even noticing it, live your way into the answer.

Having published an investment newsletter in excess of four decades, we have received and answered hundreds of questions from subscribers, not to mention an equal if not greater number from attendees at investment workshops and speaking engagements. In addition, there are two previous books and countless commentaries in Investment Quality Trends and other publications that have addressed the dividend-value strategy in every way imaginable.

Be that as it may, it seems there is no such thing as too much information, as the title of this chapter would suggest. To our delight, the readers of Investment Quality Trends have demonstrated a talent for looking at investment problems from a very interesting angle. All of the following questions were posed by those readers.

Q: How can I tell when a dividend is in danger?

A: As my grandfather told me many times, "you can't draw water from an empty well." Dividends are paid out of earnings. When a company's dividend payment equals or exceeds its earnings, the well is dry and there is nothing left to operate and expand the company. A company can pay the dividend for a time out of cash flow or savings, but this is a temporary solution to what could be a serious financial problem. It is akin to putting a Band-Aid on a deep laceration before a doctor can attend to it.

For this reason we look at a company's payout ratio. The payout ratio is calculated by dividing the dividend by the trailing 12-month earnings and then multiplying by 100. By example, if the dividend is $1.60 per share and the trailing 12 months earnings are $3.43 per share, the formula would look like this: $1.60/$3.43=0.466. We then multiply 0.466 by 100, which equals 46.6, and is expressed as a percentage, 46.6 percent. In this case the payout ratio is 46.6 percent.

As a general rule of thumb we prefer the payout ratio to be 50 percent or less for an industrial company, and because of its different capital structure, 75 percent for a utility company. When the payout ratio is too high, it can limit a company's ability to invest in future growth. This isn't such a great concern if a company maintains a high return on equity (ROE), but all things being equal, we prefer to see a company grow its dividend while maintaining a healthy balance between net profits and dividend payouts.

Q: How can I tell when a dividend is likely to be increased?

A: Companies that have a more rapid rate of growth will often maintain a lower payout ratio than a more mature company that has a slower rate of growth but a more developed earnings stream. In that case, the shareholder is typically rewarded with greater capital appreciation than dividend income.

What we look for are companies that can grow earnings and increase dividends at the same time. In Investment Quality Trends, these companies often are awarded our "G" designation, which reflects a record of average annual dividend increases of 10 percent per year over the last 12 years.

In our experience, when such a company has a payout ratio of 30 percent or less, it often is an indicator that the dividend will likely be increased.

Q: According to some reports, the preferential tax treatment afforded to dividends in the Tax Reform Act of 2003 may sunset in 2011. What impact would this have on the share prices for dividend-paying stocks?

A: Have you ever looked at the federal income tax code? If you have, you are either an accountant or an insomniac. The number of pages and regulatory changes is never ending. This is because the tax code is Congress's private little fiefdom and it changes constantly regardless of the party in power.

If you look throughout history, the federal tax rate on dividends has been raised and lowered many times. Initially the market reacts in a knee-jerk way to any changes, but eventually adjusts to the underlying reality of values.

The simple fact is that as an investor, you have a partner in Uncle Sam. The degree to which his hand is in your pocket will vary from time to time, but his hand will always be in your pocket. As my partner Mike often says, "It is what it is." The mistake many investors make is letting the tax-tail wag the investment-dog. If you try to adjust your investment program to the ever-changing tax code, you will lose; it can't have any long-term success.

Just stick with the principles of good investing as described in this book. The capital and dividend growth from blue chips will prove more than sufficient to grow your wealth and provide for your cash needs.

Q: Do you believe stock buybacks add value to a stock?

A: Technically, a stock buyback does increase the value of a stock. With fewer shares outstanding, earnings per share rise and P/E ratios shrink. As an enlightened investor, though, you know you should buy shares only when they are at historically repetitive areas of undervalue. The management of many companies has not yet learned that lesson.

Earlier in this decade, share buybacks were all the corporate rage. Unfortunately many of the buybacks occurred when the companies were deep into rising trends or, in the worst of cases, at overvalued levels. In these cases it was a needless waste of shareholder money. I would have preferred that the money spent on buybacks been paid to the shareholders directly to either spend or to invest in shares of another undervalued company.

Q: Do stocks ever move from Declining Trends into the Rising-Trends category?

A: The only time a Declining Trend stock can directly reenter the Rising-Trends category is if the stock scores a new high price and dividend increases have lifted the price at overvalue, boosting the upside potential and giving the stock additional upside potential. However, when this happens (especially if it happens early in the new cycle), the upside potential rarely justifies the downside risk, and the shareholder is best advised to sell into the Rising Trend.

Q: Do you advise buying stocks that are in the Rising-Trends category?

A: The trend is your friend until it isn't. If the upside potential to overvalue exceeds the downside risk back to undervalue, stocks in Rising Trends are attractive, in a bull market. However, stock trends are greatly influenced by major market trends. As such, in a bear market, stocks in Rising Trends are likely to fall back into the Undervalued category. Once a bear market has been identified, we suggest that you limit your investment considerations to stocks in the Undervalued category. Rising Trend stocks can be held if the downside risk back to undervalue is not large. If Rising Trend stocks fall back into the Undervalued category in a correction, they are often investment opportunities.

Q: Are stocks that fall into your Faded Blues category "bad companies" as it pertains to quality?

A: Terms like bad and good are subjective interpretations. This is why we use the Criteria for Select Blue Chips to eliminate emotion and subjectivity so we may view a stock solely on a qualitative basis. A major benefit of using the criteria is that it brings clarity to the universe of over 13,000 publicly traded stocks by eliminating approximately 96 percent of them from investment consideration.

This clarity is distilled even further by assigning each Select Blue Chip to its respective category of current value based on its historic dividend yield profile. This allows us to concentrate only on the undervalued stocks when we undertake investment considerations for your hard earned capital.

The result of this disciplined approach is that we invest in only the best of the best. This also supports our three primary investment objectives: protect your principal, earn an immediate return on investment from dividends and dividend increases, and harvest long-term capital gains at overvalued levels to realize real total return.

When a stock is moved to the faded-blues category, it is because it no longer meets our strict criteria. Although many of these companies continue to perform without incident, the loss of Select Blue Chip status is often a harbinger of trouble for others. In our opinion, the potential risks outweigh the potential returns in these situations.

Q: Should I sell a stock when it is moved to the Faded Blues category?

A: In general terms, a move to the Faded Blues category raises the yellow flag of caution. What is required at this point is some discernment about the cause of the downgrade. For some stocks, a downgrade to the Faded Blues is a transitory event, because the company quickly addresses the issue(s) that prompted the downgrade. For other stocks, the downgrade can be the first in a string of negative events.

We would suggest a review of recent history to assist in the discernment process. By example, if, prior to the downgrade, a stock is earmarked as a dividend in danger (the dividend exceeds the trailing 12-months earnings) for an extended period of time and its level of debt has been persistently elevated, it may be prudent to eliminate the position. Remember, there is no profitable substitute for quality.

Q: When analyzing the Undervalue category, can you discuss what weight you place on each of the table headings?

When considering the stocks in the Undervalue category, our analysis begins with the Standard & Poor's Earnings and Dividends Quality Ranking. This measurement by S&P is a very comprehensive assessment of a company's ability to consistently generate earnings, which allows them to fund and maintain their dividend. Optimally, we prefer a ranking of A+, which is not awarded lightly and suggests a superior company.

Time and space do not permit a thorough discussion of all the components that are considered by S&P in this assessment, but subscribers who are so inclined can obtain a white paper directly from S&P that discusses each component in detail.

Closely following the S&P ranking is the "G" designation, which denotes a remarkable 10 percent average annual dividend growth over the past 12 years. Stocks that maintain this record are excellent compounding vehicles and generally realize consistent price appreciation.

The "BC" number, which represents how many of the six criteria in our Criteria for Select Blue Chips the stock meets, is a number we look at closely. Obviously, we prefer that a stock maintain all six, but many outstanding companies vacillate between five and six.

A payout percentage at or below 50 percent (75 percent for utilities) suggests that a company can both maintain their dividend and still have room to raise the dividend as earnings increase. Debt is another measure we look at closely. It is important to note that, when used correctly, debt can be an important tool. When debt reaches an abnormally high level for a sustained amount of time, however, it can become a problem and an indicator of potential trouble. We generally prefer that companies keep their debt level below 50 percent (75 percent for utilities).

Q: When a takeover occurs, do the undervalued and overvalued yield lines change for the dominant company?

A: The acquiring company is typically larger than the acquired company in terms of capitalization and number of shares outstanding. Therefore, the dominant company has the most influence on the patterns of undervalue and overvalue, and the boundaries of dividend-yield will typically follow the pattern of the dominant partner.

Investors will adjust these boundaries if the earnings and/or dividend patterns change once the acquisition has been completely digested.

Q: How should I adjust my portfolio once a bear market has been identified?

A: When the market is undervalued or early in a rising trend, up to 90 percent of the investment capital that is allocated to stocks should be invested. I never invest 100 percent of my capital because an unforeseen circumstance might arise in which I need to access some cash, or an unexpected investment opportunity may become available.

When the market reaches the overvalue area, however, the rules change dramatically. In general, I want to sell any overvalued positions that are in the portfolio. If an overvalued stock is still showing signs of strength, however, I may elect to use a rising stop loss order to milk the gains. If I have any rising trend stocks that are less than 50 percent from the overvalue area, I will use a stop loss for these positions as well. The important point to understand is that it is prudent to protect against a sudden reversal and decline.

My primary goal when the market reaches overvalue and shows signs of topping out is preservation of capital. When the market is overvalued or in a primary declining trend, preservation of capital is more important than appreciation of capital. That is, the return of capital is more important than the return on capital.

When the market is overvalued or in a primary declining trend, I don't want to have more than 25 percent of my capital invested. That 25 percent should also be limited strictly to undervalued blue chips. As the Dow declines from overvalue, it will typically find support in the 4 percent dividend-yield range and reverse into a counter-trend rally. At this point, another 25 percent can be invested in undervalued blue chips. Once the counter-trend rally has retraced 50 percent of the previous decline, it is time to place stop-loss orders once again.

As the second leg down gathers momentum, the stop losses will get hit and the second 25 percent tranche will most likely be liquidated, leaving you with 25 percent still invested. The second leg down should find support at the 5 percent yield area on the Dow, halt, and reverse into a second counter-trend rally. At this juncture I would place another 50 percent of my capital, for a total of 75 percent, into undervalued blue chips. Once the second counter-trend rally has retraced 50 percent of the previous decline, I would place very tight stop loss orders and prepare for the third leg down.

The third leg down is often the most severe, which means you should return to a 25/75 split again as the result of your stop loss orders. The third leg down will typically find support at the 6 percent yield area on the Dow. This is also typically the area that the bear market will end. At this juncture I want to move my 75 percent in cash into undervalued blue chip stocks in 25 percent increments until I am at 90 percent to 95 percent invested.

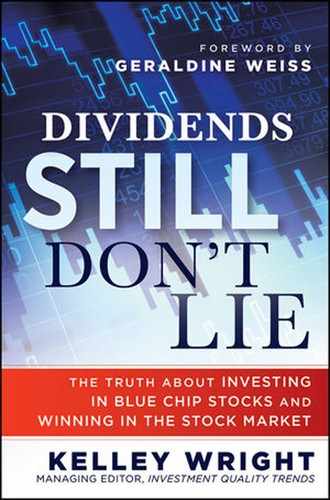

In Figure 12.1, you will find the DJIA from 1896-2008. Note that the periods in which the dividend yield was 6 percent or greater have been coincident with bear market bottoms.

Q: Regarding the Timely-Ten feature, if I bought a stock that made the list in the last issue but it isn't in the current issue, should I sell that stock and replace it with another stock that made the current list?

A: This is an excellent question that obviously needs to be addressed. In short, the answer is no. In accordance with our long-term policy, our buying considerations are generally made from the stocks listed in the Undervalued category. I know that some long-term subscribers are already preparing e-mails to remind us that, on occasion, we deviate from that policy, but those occasions are rare, are based on my discretion and intuition, and are generally accompanied by a well-worded caveat.

Also, a long-held policy is that it is always a good time to buy a good undervalued stock. We approach the Timely Ten then, as if the reader is looking at IQ Trends for the first time. The 10 stocks that make up the current list are the ones we would start a portfolio with as of this issue, make additions to a partially invested portfolio as of this issue, or, to compare to a fully invested portfolio when the investor may be looking to replace one or two of their least favorite positions as of this issue.

If a stock is dropped from one issue to the next, it is generally because the stock has entered its Rising Trend and is no longer appropriate for buying consideration. If a stock is dropped from one issue to the next but is still undervalued, we have determined that another selection is simply more attractive as of this issue, but it does not mean that you should liquidate the position.

Stocks that are purchased at undervalue are appropriate to hold until they complete their Rising Trend and reach overvalued levels.