The sweetness of low price is soon forgotten; but the bitterness of poor quality is long remembered.

A value-based approach to investing such as the dividend-value strategy is a powerful arrow to have in your investment quiver. When properly implemented through high-quality companies that represent historically good value, an investor is well-armed to out-duel the competition.

The terms quality and value are repeated frequently throughout this book because they are the twin pillars on which the foundation of the dividend-value strategy rests. In previous chapters we have discussed the importance of value in a generic way; in later chapters the discussion will become much more specific.

Before we get into the finer aspects of value identification, however, it is important to introduce and understand the concept of quality and its underlying importance. As stated previously, the dividend-value strategy can be implemented with any company that has paid dividends long enough to establish a repetitive pattern. For optimum investment results, however, it is best implemented through high-quality, blue chip stocks.

More than 40 years of research shows that the dividend-value strategy, when implemented through high-quality stocks with long track records of excellence and performance, provides a powerful tool for building wealth. At the end of the day, it is the building of wealth, both of capital and income, to meet the present and future cash needs of the investor that is most important.

The extract that follows first appeared in The Dividend Connection, Geraldine's second book written with her son, Gregory Weiss. It is so well written there is simply no way to improve upon it.

In the real estate market, quality is determined by three measures: location, location, location. Three measures can also be applied to quality in the stock market: performance, performance, performance.

Financial performance is the first measure of quality. This includes the company's record of earnings, dividends, debt-to-equity ratio, dividend payout ratio, book value, and cash flow.

Production performance is the second measure of quality. We look for a company that manufactures useful products or services and actively pursues research and development of new products or services. The company must also demonstrate an ability to market its products or services successfully.

Investment performance, as reflected in long-term capital gains and dividend growth, is the third measure of quality. The most important objective of an investor is a rewarding total return. A well-managed company with a strong financial performance will generate a total return that will outperform any other investment vehicle.

These three measures of quality do not stand alone. They are intertwined in the fabric of the company and its shareholders' goals. All of our research has shown that there is as much or more profit potential in high-quality stocks than there is in stocks of inferior or unproven quality—and with far less risk.

Our method of investing in the stock market focuses exclusively on blue chip stock selection. It involves limiting investment selections to blue chip stocks and purchasing or selling those stocks based on their individual profiles of undervalue or overvalue.

As best as we can tell, there are at least 15,000 publicly traded companies in the U.S. financial markets alone. I doubt seriously that anyone would fault me for suggesting that not all of them represent blue chip stocks, let alone companies that are worthy of investment consideration.

There is a certain irony in the fact that, in a book in which we focus on value-based investing as a business as opposed to mere gambling or speculation, the objects of our affection, blue chip stocks, get their name from the highest denomination of betting chips in a poker game. Be that as it may, the term blue chip is nonetheless reserved for only the highest quality stocks. The reason for this is simple. Blue chip companies have a reputation for dependability as well as offering the best potential for increasing shareholder value through dividend growth and capital gains.

Although many blue chip companies are household names, an equal number, if not more, are not. There are also many stocks that are household names but are far from being blue chips. As you can see, it is important to have a mechanism or filter if you prefer to eliminate the pretenders from the contenders, so to speak.

Since 1966 we have used six criteria, which we call the Criteria for Select Blue Chips (our designation for the highest-quality blue chip stocks), as a starting place for our investment considerations. When a stock has passed this filter for its qualitative characteristics, we then analyze it further to determine its historically repetitive areas of undervalued and overvalued dividend yield.

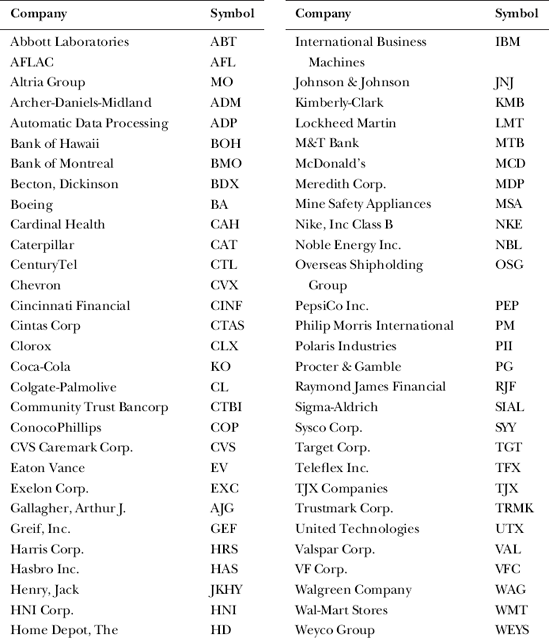

At first glance these six criteria appear relatively simple, which they are; no rocket science here. When combined into one fundamental filter however, it effectively eliminates approximately 98 percent of the domestic publicly traded universe of stocks. To put that into further perspective, of the roughly 15,000 publicly traded companies in the U.S. markets, only 350 companies meet this criteria, and of those 350 we can establish clear-cut dividend-yield profiles for only 273 companies as shown in Figure 4.1.

Most stock analysis is conducted through two central disciplines: fundamental and technical. Fundamental analysis has two main subsets: the quantitative and the qualitative. Quantitative generally refers to numbers, things that can be measured—earnings, dividends, cash flow, payout, debt, and so forth. Qualitative generally refers to intangibles—characteristics that can't necessarily be measured but nonetheless are important; for example, name recognition such as a company's brand, management expertise, commitment to research and development, industry cycles, and so forth.

Technical analysis is considered by many to be the polar opposite of fundamental analysis. Whereas fundamental analysis involves analyzing the economic characteristics of a company in order to estimate its value, technicians are primarily interested in price movements because the fundamentals, they believe, have been fully factored into the price. Another definition would be the study of supply and demand in a stock or market to determine what direction, or trend, will continue in the future.

Generally, but not always, analysts tend to favor one discipline over the other. For many practitioners, there is simply no way for the two disciplines to co-exist.

Our approach is based on a combination of the two disciplines, what we call a fundamental approach to technical analysis. The Criteria for Select Blue Chips is how we identify fundamental quality, or what stocks to buy. Our Profiles of Value, the study and identification of the historically repetitive patterns of undervalue and overvalue areas of dividend yield, is how we identify value, or when to buy, sell, or hold.

In later chapters we will discuss undervalue and overvalue in much greater detail. Before we can begin to focus on the when, however, we first have to identify the what. That is the primary purpose of the Criteria for Select Blue Chips—to identify corporate excellence, or quality.

Criteria 1 and 6 earlier both reference 12 years: dividend increases in five of the last 12 years, and earnings improvement in seven of the last 12 years. One of the most frequent questions I a masked is what is so special about 12 years?

The average business/economic cycle lasts approximately four years. Over the course of 12 years, then, the economy and markets will go through three complete cycles. During that period, a company will experience the inevitable economic surprise, be it on a macro level, which affects all companies, or on a micro level, which is specific to that company, industry, or sector. There is an equally high probability for major legislative and/or tax changes that will require a period of adjustment. In short, adversity is part of the cost of doing business. As such, a consistent track record for earnings growth is not only difficult to achieve, but also to sustain over significant periods of time.

For a company to meet both of these criteria, their earnings and dividends must show consistent improvement. Steady and improving earnings and dividend performance over the course of 12 years is not luck; it is evidence of strong and capable management.

The list of Select Blue Chips that have achieved consistent earnings and dividend growth is quite extensive. Only those from the Undervalued category in the mid-September, 2009, are listed below in Figure 4.2.

The most reliable measure of good management is long-term performance, a proven ability to grow the net earnings of its company and maintain a rising trend of increased dividends. You work hard to save the capital you put to work in the markets. Don't entrust it to just any company; put it to work with the best. The proof, once again, is in the pudding.

Standard & Poor's has provided Earnings and Dividend Rankings, commonly referred to as Quality Rankings, on common stocks since 1956.

The Standard & Poor's Earnings and Dividend Rankings for Common Stocks are as follows:

A+ Highest | B+ Average | C Lowest |

A High | B Below average | D In reorganization |

A− A Above average | C Lower | NR[a] |

[a] A ranking of NR signifies no ranking or insufficient data because the stock in not amenable to the ranking process. | ||

For inclusion in the universe of Select Blue Chips, a company must initially have at minimum an A_ Quality Ranking. The company may remain in the roster if its Quality Ranking declines to a B+, but will be removed from the listing if it is downgraded further.

There is an extensive body of research on the impact that market capitalization, or cap size, exerts on the returns of stocks. As a result of this research, the mutual fund complex has designed and offers a multitude of funds that invest solely in one capitalization segment of the market. These funds are easily identifiable as the term Cap will be part of the fund name. By example: Mega Cap, Large-Cap, Mid-Cap, Small-Cap, Micro-Cap, and so forth.

Also common today, particularly among financial consultants, is to provide their clients who invest in individual stocks the ever ubiquitous pie chart, to show what percentage of their holdings fall into the various capitalization segments.

For many, this type of analysis is sacrosanct. So be it; it is not within the purview of this book to engage in that debate. For our purposes of identifying quality, we aren't overly concerned with market capitalization. What we do care desperately about though is liquidity.

With enough common shares outstanding, a stock is assured of liquidity; we never want to be in the position of having to make an appointment to buy or sell a stock. Institutional investors, whose importance to our method is outlined in the next section, prefer to invest in companies that are liquid so they can establish large investment positions without disturbing the price of the stock. Equally important is that when the time comes to sell, they want to know that there will be sufficient numbers of buyers. Few experiences are as frustrating as trying to buy or sell a large position in a thinly traded stock. For institutional investors who frequently deal in large sums of capital, an orderly entrance and exit are extremely important. Lastly, liquidity helps to guard against share price manipulation.

When we use the term institutional investor, we are referring to the vast number of mutual funds, Exchange Traded Funds (ETFs), hedge funds, banks, insurance companies, pension fund and retirement companies, major brokerages, and money managers. On any given trading day, these groups account for the vast majority of trading activity. As such, their collective buying and selling decisions will exert an enormous impact on the trend of stock prices. In other words, institutions are the 800-pound gorillas of Wall Street.

Whether they choose to acknowledge it or not, institutional investors can exhibit some fairly predictable behavior. This is due, in no small part, to the fact that it is a closely linked community. This is to say that they associate with, listen to, and behave like other institutional investors. As value investors, we can use this propensity for like-minded behavior to our advantage.

It is not uncommon when using the dividend-value strategy to be early to the table, which means that we often take positions in high-quality companies that offer excellent historic value long before other investors. Eventually one or two institutional analysts will stumble upon one of our companies, write up a buy recommendation, and distribute it to its traders or sales force.

Nothing in the institutional community remains secret very long, so when the word gets out, the full force that is institutional buying power kicks in. Strong institutional buying eventually hits the radar screens of our favorite investor type, the momentum investor. In simple terms, a momentum investor attempts to capture capital gains by buying a stock with a discernible uptrend in price, or to short a stock with a discernible downtrend in price. The underlying belief is that, once a trend has been established, it is likely to continue in that direction than to move against the trend.

There is nothing intrinsically wrong with this idea. In fact, we engage in some momentum investing ourselves. There is nothing more attractive than a high-quality company with an undervalue price, a high-yield and upward momentum in its dividend trend.

Okay, we're not really momentum investors, but I think you get the point.

To bring this point to conclusion, between institutional interest and momentum investing, stocks that we purchased at excellent historic value will often reach their historic upside potential, at which point we lock in our profits and search for another high-quality undervalued opportunity.

Of the six Criteria for Select Blue Chips, the number of institutional sponsors is the least rigid, which is to say there is nothing magical about the number 80. What is important is evidence of widespread interest in a stock, and that it has attracted a broad and diverse institutional following. In terms of price stability, we prefer to find that 80 or more institutions hold 50 percent of the common shares outstanding, rather than one or several institutions holding the same amount; with diversity comes an element of safety. Most full-service brokers and investor databases can provide information on the number of institutional investors and their percentage of holdings in any individual stock.

Of the six criteria that comprise the Criteria for Select Blue Chips, this is the one that separates the big dogs in the tall grass from the pups in the weeds. We are often asked if there is really a meaningful difference between a company that has paid uninterrupted dividends for 25 years and one with 10, 15, or 20. The short answer is absolutely.

In a sufficient number of instances, our research indicates there is a greater likelihood for price volatility and less reliability in the trends of earnings and dividends for companies with shorter track records of uninterrupted dividend payments.

Although we lack a single empirical measurement that explains this phenomenon, our best guess, based on our experience, is that the market, which posseses all the wisdom from its collective participants, has determined that companies that have achieved this milestone have earned elite status and investors simply treat them differently.

What we do know is that over a 25-year period a company will go through many business and economic cycles, will experience the exhilaration of bull markets and the despondence of bear markets, will see their products or services enjoy periods of wide popularity and periods of less; the list can go on and on.

In the final analysis I believe it all boils down to one factor, namely, competence. If a company can weather the myriad challenges it will inevitably face over such a period of time and maintain a strong record of earnings growth and maintain a rising dividend trend, that is competence. If a company can keep its products and services at the forefront of consumer interest, or reinvent itself if necessary, that is competence. If a company can consistently attract, train, and retain the next generation of management that will continue a tradition of excellence—that is competence.

You work hard to save the investment capital you put to work in the financial markets. All things being equal, who are you most comfortable associating with that capital? For us the answer is easy: the most competent companies we can find.

With the rare exception, the majority of the current 273 companies in the Investment Quality Trends roster of Select Blue Chips have paid uninterrupted dividends for 25 years.

At this juncture the importance of cash dividends should be crystal clear. When a dividend is increased, the stock price will inevitably rise to reflect the increase in value. Conversely, when a dividend is reduced, the stock price will inevitably decline to reflect the decrease in value.

Dividends are an indicator of value and a predictor of future growth, which attracts new investors to the company and provides a tangible reward for accepting investment risk. Value-conscious investors can depend on cash dividends to either provide a reliable stream of income to meet their current cash needs or as capital to reinvest to keep pace with inflation and improve their standard of living. A company that pays cash dividends year after year and increases those dividends regularly is well managed.

An ongoing dividend stream is the most reliable evidence a company is generating sufficient earnings to cover expenses, pay the interest on its debt, grow the company, and reward its owners. When a dividend is increased, the stock owner knows without reading a balance sheet or an annual report that their company is performing.

In this chapter we have explored the importance of quality as it pertains to the dividend-value strategy. Although the strategy can be implemented through any stock that has paid dividends long enough to establish a discernible pattern for repetitive areas of undervalue and overvalue, four-plus decades of research has proven that for the best investments results, investors should confine their investment considerations to only the highest-quality, blue chip stocks.

High quality, blue chip stocks are the first to rise in a bull market and the last stocks to fall when the market declines. In good times, blue chip companies outperform both their lesser competitors and the economy. In bad times, they resist adversity best. Time and time again, experience has shown, there is no profitable substitute for quality.

Although quality is one of the twin pillars of the dividend-value strategy, it isn't the final word; value is. In the following chapters, we discuss the importance of identifying value to build a winning portfolio.