7

Always Have a Plan

When I say “always have a plan”, I am – initially – talking about having a business plan. But I think you should apply this principle to anything in life. Your plan can change; it's okay and necessary to adapt it as you continue along your path in business and in life, but you must have one to begin with or you'll be flailing around in the dark.

Business Plan or Bust

If you do want to start a business, the single most important piece of advice that I can give you is… have a business plan!

I am consistently dumbfounded by the number of people I meet who have started a business without writing a business plan. They come to me and ask me for help, but when I ask to look at their business plan, they say they haven't got one. Having a business plan is the bedrock of your business. Not having one would be like starting to build a house with no architect drawings. Where would you dig your foundations? How deep would you dig them? What materials do you need to use? You wouldn't dream of building a house without a plan; don't try to start a business without one.

You also need to put real numbers into your business plan or else it's worthless.

I remember someone who used to work for me came to me and asked for advice because he was setting up his own company as a mortgage broker. He had used the figures he saw my company getting paid by the banks. He had assumed that, as a one-day-old company, he would get the same fees as a ten-year-old business. I told him that this was completely unrealistic; he needed to go directly to the bank and get realistic figures unique to him and his position in the market as a start-up broker. I knew his figures would be very different once he found out how much banks would offer him (as opposed to a large, established company) as a fee for brokering a mortgage.

If you get your forecasting right, you are more likely to make money. You are only likely to make money if you make calculations based on real predictions, based on facts.

I mentioned in the last chapter on due diligence the mistakes that people make on Dragons' Den. I am sure many of those mistakes are made by people who do not have business plans. Think of how often the dragons ask people, “What's the size of your market?” and the entrepreneurs don't have an answer. If you don't even know the size of your potential market, how can you predict how much you could sell? If you're going to manufacture golf clubs for left-handed people, you must have some idea of how many left-handed golfers there are in the world, and whether they require a different type of golf club or not? It's a waste of time and money manufacturing a product if there is no market for it. And you must know what people would pay for that golf club – either from existing figures or predictions based on real market research, otherwise how can you predict your margins? Your margin is the difference between cost price and sale price, which is your profit. No one wants to invest in a business that does not have the potential to make profit.

Sadly, too many people make products that they would like, and then assume that everyone else will like them. They spend a fortune trying to bring that product to market with no real fact-based estimates of whether it will sell. Those people are not real entrepreneurs, they are product designers and need to find an entrepreneur to steer the way.

Of course, there are times when people get lucky; they were in the right place at the right time, and the rest is history. Did people make money in the “dotcom” boom, or in the “tech start-up” boom? Yes, they made a lot of money. But it was all based on speculation and overvaluations, and – like the property market or cryptocurrency market – the bubble eventually burst and no one else saw such profit levels in that market ever again. The people who made money were lucky because of the time they chose to invest. They got lucky because they got in as the bubble was about to blow up, and got out before it burst.

But you can't base a business plan purely on luck!

I also have a theory that a massive injection of equity investment is not always that conducive to building a successful business. When an owner has a lot of equity investment, they don't have the same motivation as they do when they own the whole business. Losing someone else's money is far less painful than losing your own money.

I suspect that there are many people who start a business because they are lured by the perceived luxurious lifestyle of a successful entrepreneur. Any real entrepreneur will tell you that it is not a glamorous life at all… it entails a lot of blood, sweat and tears to start up and run a business. Most people drop out of the game when they realize quite how much work it's going to take.

There is still value in trying. Even if you make mistakes – by not doing your due diligence – you at least still get experience. And every ounce of experience is worth something; it goes into your knowledge bank. There's no shame in making mistakes. Much of my knowledge comes from little mistakes I made along the way. When you make painful mistakes, you learn from them pretty quickly!

Always Begin With “Why”

Some people who approach me for advice when they want to start a business not only don't have a business plan, they also don't seem to know why they are setting up a business. Your “why” always has to come first, even before your plan. You have to know why you are setting up a business and what that business is for before you even start your business plan. Is it a lifestyle business… something that you enjoy doing and just want to earn enough from to keep it going? Is it a family business that you would never sell on? Or is it a business that you would want to exit from by a trade sale or an IPO? If you want to float your company on the stock exchange one day, you will have to be able to manage people; if you don't like managing people, this is probably not the right goal for you. I knew from very early on that I was good at managing people; I knew that I could build a company that I could potentially take public or sell to a third party.

You cannot move forward until you know your destination. Until you know where you want to go, you will tread water. When you know where you want to go, when your objective is clear, you can start taking the small, incremental steps that will take you to your destination; you can make your plan, do your research, reduce your risk and build your business.

Goal Setting

Goal setting is the most important part of your plan – in business and in life. If you don't know your intended destination, there's not much point trying to build a plan. How can you plan to get to a place if you don't know where you want to go? And of course, you have to want to go there. You need to set goals that motivate you – and keep you motivated.

You also need to be flexible. If you know your goal and you make a plan as to how you are going to get there, be prepared to change that plan. In other words, don't worry too much when things don't quite go as you were expecting. Every time you “fail” you find one path that doesn't work, which brings you one step closer to the path that will help you achieve your goal.

No one ever got successful by accident. Even those who got lucky usually started out with some goals.

Get SMART

I find the acronym SMART very useful for goals setting. The term first appeared in Management Review in a 1981 paper by George T. Doran.

This is what “SMART” stands for (and for specific examples, I've used my goal of writing this book!):

- S = SPECIFIC: you must be specific when you set goals… no generalizing. (I made a specific goal of writing a book and getting it published.)

- M = MEASURABLE: you have to be able to measure your achievements by certain criteria, such as time or money. (I aim to sell at least 500 books each month and make £5,000 in royalties from book sales in my first published year.)

- A = ACHIEVEABLE: meaning it must be within your grasp. (I did my research and knew I had the skills and knowledge to put together a decent book that would be of value to a wide audience.)

- R = RELEVANT: your goal must be relevant to your overall ambitions and associated with the direction you are going in. (I knew that writing a book would help to position me as a mentor and open up ways in which I could work – perhaps as a business coach or mentor – beyond my current business offering.) (NB: R is sometimes given as “REALISTIC”– but I think that is covered in “Achievable.”)

- T = TIME BOUND: you must have a deadline for your goal. (Voila!)

The Spidergram

I find it's essential that I have my goals written down, so at the beginning of every year I create a “spidergram.” I draw a circle on a piece of paper and write the year I'm setting goals for in the middle of the circle. Then I draw four “legs” on the left-hand side and four “legs” on the right-hand side, so that it looks like a spider – well, like a very bad drawing of a spider!

On one side of the spider, I write four professional goals along each of the legs; on the other side I write down four personal goals.

Before I write them down, I test the goals to make sure I can apply SMART to each one. In other words, they have to be specific, measureable, attainable, relevant and time bound. So, they can't just be things like, “I will do better this year” or “I want to make more money this year.”

The personal goals must also qualify; so, “I will win the lottery this year” doesn't count!

Once I have set my goals, I break them all up into small steps so that I know what I need to do in order to achieve them.

I look at my spidergram on a regular basis throughout the year, to check in with my progress. I keep mine in a folder that sits on my desk while I'm working. I also share my spidergram with the whole company to make me accountable to a large number of people.

My 2018 spidergram looked like this:

And this is how I got on with those goals.

Professional goals:

- Turn over £11 million+ in sales. (ACHIEVED!)

- Employ 160+ people. (ACHIEVED!)

- Make my Heads of Departments into Directors and develop them into great business leaders that are respected in the industry. (ACHIEVED – by giving them more exposure and sending them to corporate events from which I got very positive feedback).

- Digitization of our mortgage process. (About 25% achieved – this is an ongoing project and a huge one, so I was happy to get this far. We delivered about two stages of this.)

Personal goals:

- Buy a new “mid-life crisis” car. (ACHIEVED: I bought a BMW i8!)

- Complete the “Three Peaks Challenge.” (ACHIEVED!) This involves climbing Mount Snowdon (in Wales), Ben Nevis (in Scotland) and Scafell Pike (in England in the Lake District) within 24 hours, including the driving time between them.

- Holiday to Asia (including Hong Kong, Malaysia and Singapore) with the family. (ACHIEVED!)

- Invest more time and money in my family by making sure weekend time is family time only (no working), and by continuing to send the children to private schools. (ACHIEVED!)

Although I separate the professional and personal goals on the diagram, they are obviously all linked. For example, achieving my professional goals gives me the ability to finance my personal goals. I was able to continue to focus on the family at the weekends, and to send the kids to private school, because I achieved my goal of turning over £11 million in sales.

And it works both ways.

For me, doing the “Three Peaks Challenge” fed back into my professional performance because it gave me an extraordinary boost in mental strength and self-belief. Setting a challenge like that and meeting it, overcoming the obstacles that threatened my progress, and believing in myself, gave me new insight into where I set my own limits. It also brought the company together because they all supported me, many sponsored me, and 17 members of the team joined me in doing it – so it also ended up being a great team-building exercise.

The best thing of all was that my eldest son, Brandon, did it with me. He was only 13 at the time, I couldn't have been more proud of him!

The challenge took place in June, so the weather was relatively good. We left from the office at dawn one Friday, all of us together in a minibus, and drove all the way up to Scotland, which took about 12 hours. We had some dinner and got an early night because we were up at the crack of dawn on Saturday to climb Ben Nevis. At about midday we left for the Lake District and then climbed Scafell Pike. I think it was about 10 pm by the time we left for Snowdon. We had a few hours to sleep on the journey, but by 2 am we had to start climbing Snowdon so that we were finished by 6 am and had completed the challenge in 24 hours. The pace is absolutely relentless! Each hike took about 4–5 hours. If you hadn't reached the peak in a certain amount of time, you were made to turn around so that you didn't delay the bus leaving for the next location. That was a great motivator and made us all push that bit extra to reach the summit.

One of the most challenging moments, for me, was when I received a call to tell me that Mum had gone into hospital in Malaysia. It was so frustrating that I couldn't just pack a bag and go and get on a plane immediately; I had to wait until I returned. I remember FaceTiming with her when I was on the top of Mount Snowdon!

The whole experience was so worthwhile. We raised more than £7,867 for our chosen charity, “Reach Out.” It was definitely one of the hardest but most rewarding challenges of my life!

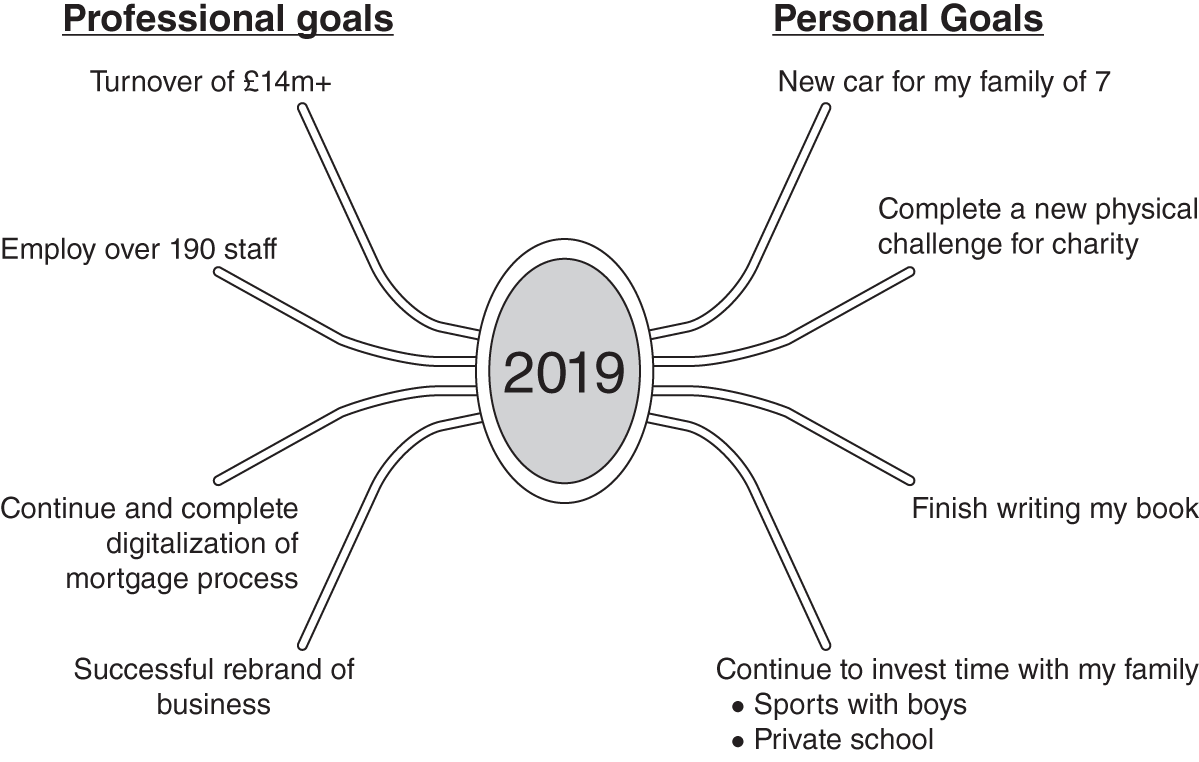

These are the goals I put on my 2019 Spidergram (so I am accountable to all of you readers!).

Professional goals:

- Turnover £14 million+.

- Get to 190 staff. (In May 2019, we were at 184.)

- Continue the digitization project. (That we had completed 25% of in 2018 – by May 2019 we were at about 50% delivered and expecting to finish by the end of 2019.)

- Successfully launch the rebranded company.

Personal goals:

- Buy new family car that can accommodate seven people.

- Complete a new physical challenge. (Either the Jurassic Coast walk or something similar to the “Three Peaks Challenge” – to be confirmed.)

- Finish my book. (If you're reading this… ACHIEVED!)

- Continue to invest in the family by playing sport with the boys on Sundays. (We recently got a table tennis table… anything to get them off the computer for a stretch of time!) And to continue to invest in my children's education by keeping them at their private schools.

Step by Step

Writing down the incremental steps that you need to take in order to achieve your goals is vitally important; as important as actually naming the goal in the first place. You have to know which small, practical steps you need to take to achieve your ultimate goal, and – again – you need those to be written down. I am a big fan of writing everything down.

You need to be able to see results, by achieving each step, or you will lose focus. If I say “my ambition is to be a millionaire” but I don't write down the numerous small steps that will help me get there, I will probably fail because I won't see the incremental rewards on a daily basis.

I see so many people fail to achieve their ultimate goal simply because they haven't written down all the incremental steps. They write down the goal, so they know their ultimate destination, but they don't write down the step-by-step plan to get there. So they soon give up, lost in confusion. You have to be able to do the work. There's no point in setting goals if you can't do the hard work. Most people fail because they don't break down their goals into incremental steps and do what it takes to achieve each step. They think that setting the goal is everything, that once they write that down, it will magically happen. They make goals, feel good about themselves for that, and then sit back and wait! People write, “I'm going to lose 5 kg (about 10 lb)” and then, a few months later, ask “Why aren't I thin yet?” The answer is: because you haven't done anything. You have to write down those steps. Join a gym. Go to three cardio classes a week. Cut out sugary snacks, etc.

I have people who join my team with the ambition of becoming a senior mortgage consultant. That's great. And the advantage for them is that the steps are already laid out for them (in terms of what they have to achieve to get there). But they still need to put in the work to achieve each step. Those incremental steps are set. If you want to become a senior mortgage consultant, first you have to do the induction course, then you have get your CeMAP (Certificate in Mortgage Advice and Practice) qualification, then you have to get your first deal (which you can break down further into goals for numbers of calls and numbers of quotes made). If you achieve all this, you will graduate from the academy. Then you need to do £10,000 of written business in one month and achieve this for three consecutive months. If you hit all those targets, you'll get promoted. That's how it works. The whole process takes around 12 months, so you need those small, incremental steps to keep you focused and motivated. You need to feel those little wins along the way, it enables you to track your progress.

To achieve your goals, you must persevere and consistently review your progress. You can't give up. When you get knocked back, you get up and go again. You see if there is possibly another way of doing it; you check that this step is genuinely relevant to your overall goal. You reassess everything and recalibrate.

The key is to create a journey. When you create a journey, and you hit milestones along that journey, there is a greater sense of achievement.

In the Long or Short Run

For me, running a marathon was a great example of how you set an overall goal and then break it down into incremental steps. I always offer people this advice when they tell me that they are planning to run a marathon: if you start your training focused on running 26.2 miles, you'll never even get out of bed; you have to increase your distances gradually, week by week, adding a mile or so each week, and then dropping down to a shorter distance and then building back up again slowly. Ideally, if you plan to run a marathon, you should get a proper running plan – there are loads available online.

For me, running a marathon was a huge achievement and 26.2 miles was quite enough, thank you very much! However, there are “ultra-marathoners” who literally run marathons back to back. All they do to achieve their goals is continue to build on their training, increasing their distances incrementally. Their perspective on running is completely different from mine. And mine is completely different from someone who has never run more than a mile before. Everything is relative! And relativity gives you perspective.

The same approach can be applied in business. I always look at how we can set a schedule for “quick wins.” For example, if we are implementing a new IT project (like a new customer relationship management system) that is going to take three years to complete, we have to break it up into bite-size chunks. If we only set that one goal, if we only focused on that one deliverable, we'd get overwhelmed and would quickly give up. We have to break it down into several different phases and set goals for each phase so that we can really feel that achievements are being made along the road to the big overall goal. Breaking it down keeps you motivated because you get to feel the small wins along the way. Every time you hit a target and complete a deliverable piece of the bigger picture, it feels good. You are then motivated to reach for another one. Eventually, all those little goals, those “quick wins”, will result in you completing the “big picture”, i.e. the overall project.

When you achieve a goal, no matter how small, you feel motivated. Always view your overall goal as a series of smaller, achievable tasks. Whether your overall goal is to get a new skill, or improve the quality of your life, or start your own company, it doesn't matter; everything can be broken down into smaller, digestible chunks that make it easier for us to stay on track.

Be Accountable

You must share your goals with someone; several people even – the more the better. I share mine with the whole team. Feeling accountable to many people, some of whom I know really look up to me, helps keep the pressure on me. And it works for my professional and personal goals. There is no way I would have achieved my goal of running a marathon in 2017 if I hadn't announced it to the team. The training schedule is brutal. I would have given up many times if it hadn't been for the fact that I'd made myself accountable to the whole team. I knew the shame of telling them I'd given up would have hurt more. Letting yourself down is bad, but letting others down is always worse.

But the most important part of any plan is to set the goals that are right for you. So, how do you find out the best path to suit your skills, your passion, your… “why”?