CHAPTER

TEN

AGENCY DEBT SECURITIES

Senior Trader/Analyst

Federal Reserve Bank of New York

FRANK J. FABOZZI, PH.D., CFA, CPA

Professor of Finance

EDHEC Business School

Agency debt securities are direct obligations of federal government agencies or government-sponsored enterprises. Federal agencies are entities of the U.S. government, such as the Tennessee Valley Authority (TVA). Government-sponsored enterprises (GSEs) were designed as publicly chartered but privately owned and operated entities, such as the Federal National Mortgage Association (Fannie Mae), the Federal Home Loan Mortgage Corporation (Freddie Mac), the Federal Home Loan Banks (FHLB), and the Farm Credit Banks. Technically, GSEs are instrumentalities of the government that exempt them from certain management laws and regulations that would be applicable to other direct government agencies. However, despite this difference, for the purposes of this chapter, GSEs will frequently be referred to as agencies.1

The agencies issue debt securities to finance activities supported by public policy, including home ownership and agriculture. Other government initiatives, such as the Temporary Liquidity Guarantee Program, have provided support for debt issued by other corporations and are considered by many market participants as having characteristics similar to those of agency direct obligations.

Agency debt securities typically are not backed by the full faith and credit of the U.S. government, as is the case with Treasury securities. Therefore, agency debt securities are not considered to be risk-free instruments and trade with some credit risk. Nevertheless, agency debt securities have traditionally been considered to be of strong credit quality due to the fundamentals of their underlying businesses and because of their government affiliation.

AGENCY DEBT MARKET OVERVIEW

The market for agency debt securities expanded rapidly during the 1990s, primarily due to increased issuance from housing-related agencies (including Fannie Mae, Freddie Mac, and the Federal Home Loan Bank) as they grew their retained portfolios and mortgage-related businesses. The agency debt market grew from $426 billion in 1990 to $2.7 trillion at the end of 2009. However, agency debt outstanding has declined in recent years, largely due to reductions in housing-related agency borrowing demand. This decline was largely driven by reduced Federal Home Loan Bank borrowings and could continue as Fannie Mae and Freddie Mac maximum retained portfolios shrink in coming years.2 In addition, future efforts to reform the government role in mortgage finance could affect the size of the agency debt market. At the end of 2010, there was approximately $2.6 trillion in outstanding agency debt.

Credit Quality of Agency Securities

There is a perception among some market participants that the government implicitly backs agency issues and would be reluctant to let an agency default on its obligations. However, there has been no explicit government guarantee for any agency security, and the extent of government backing for agency securities is a source of uncertainty for some investors.

Agency securities are perceived to have a government backing due to their legal characteristics and affiliation with the U.S. government. Agencies are granted authority to issue debt from Congress and many have directors that are appointed by the President of the United States. In addition, most agencies have the authority to borrow directly from the Treasury and some agencies have received direct Treasury financing. Furthermore, agency securities are eligible for Federal Reserve open market operations.

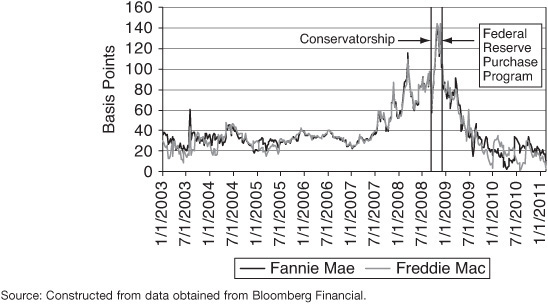

Despite their relation to the government, agency securities have historically traded at a slight discount to Treasury securities. The pricing difference between agency and Treasury securities has depended partially on the strength of each agency’s underlying business, the perceived strength of their government backing, and the liquidity difference between agencies and Treasuries. For example, Fannie Mae and Freddie Mac five-year debt traded at an average spread to comparable five-year Treasuries of 30 basis points during the mid 2000s. However, as the housing market deteriorated and losses on Fannie Mae and Freddie Mac retained MBS portfolios increased in 2007, their debt spreads to comparable Treasuries widened notably. This can be seen in Exhibit 10–1.

EXHIBIT 10–1

Fannie Mae and Freddie Mac Spreads on Five-Year Issues: January 1, 2003 to January 1, 2011

Fannie Mae and Freddie Mac were placed in a conservatorship run by the Federal Housing Finance Agency (FHFA) on September 8, 2008. At the time the conservatorship was established, then-U.S. Treasury Secretary Henry Paulson noted the action was taken to provide stability to financial markets; support the availability of mortgage finance; and protect taxpayers by minimizing the nearterm costs and by setting policymakers on a course to resolve the systemic risk created by the enterprises.3 Through the conservatorship, the U.S. Treasury Department and the FHFA established Preferred Stock Purchase Agreements (PSPA) in which Treasury ensured that each enterprise would maintain a positive net worth. Although the PSPAs were modified over time, the agreements effectively guaranteed the senior and subordinated debt of each enterprise by ensuring their solvency. Specifically, if either enterprise’s liabilities exceeded its assets under Generally Accepted Accounting Principles, the Treasury agreed to provide sufficient cash capital to eliminate the deficit in exchange for an increase in the liquidation preference on the Treasury’s $1 billion in senior preferred stock.4 As of January 1, 2011 Fannie Mae and Freddie Mac had drawn on a combined $150.8 billion of Treasury commitments and paid back to the Treasury a combined $20.2 billion through dividend payments.5

Even after Fannie Mae and Freddie Mac entered conservatorship in September 2008 the government did not provide an explicit guarantee covering their outstanding debentures, but rather increased direct support to each enterprise as explained in the previous paragraph. This step strengthened government backing for Fannie Mae and Freddie Mac but did not allay investor concerns sufficiently to stop their debt spreads from widening amid further disruptions in financial markets in late 2008.

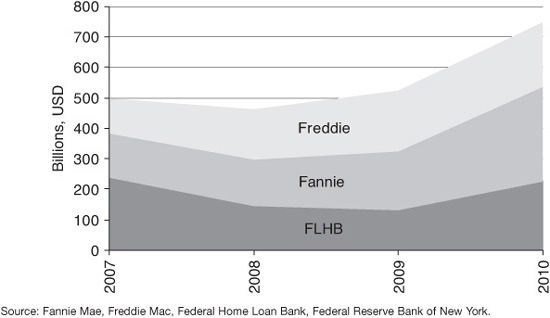

The sharp spread widening in Fannie Mae and Freddie Mac debt during 2008 was conclusively reversed only after the Federal Reserve announced it would purchase certain agency direct obligations on November 25, 2008.6 Through the program, the Federal Reserve purchased a total of $172 billion in direct obligations of Fannie Mae ($67.1 billion), Freddie Mac ($67.4 billion), and the Federal Home Loan Bank system ($37.2 billion). Although the Federal Reserve purchase program did not legally change the government commitment to the housing-related agencies, some investors interpreted the purchases as a further strengthening of official support for these institutions sufficient to reduce the large discount priced into their debt at that time.

Agency Debt Investors

A variety of market participants invest in agency debt. Many investors are attracted to the relatively high credit quality of agency debt, which offers a slightly higher return when compared with Treasury securities while offering the perception of only modestly more credit risk. In addition, agency issues are also attractive to investors because their interest income is exempt from state and local taxation for many of the issuers (albeit not for Fannie Mae or Freddie Mac issues). However, under current U.S. regulatory capital standards, most agency debt securities in U.S. banking book holdings require a 20% risk weight, as opposed to a zero risk weight for Treasury securities.

The composition of agency debt investors has changed over time. Using Freddie Mac debt statistics as an example, investment managers and North American investors were traditionally the largest buyers of such agency debt from the late 1990s through the mid 2000s. During the mid 2000s, central bank and Asian investors began purchasing Freddie Mac debt in larger quantities and the share of investment managers and North American investors declined. However, in the middle of 2008, this trend reversed and investment manager and North American investors again became the largest buyers of Freddie Mac debt. There is not adequate public data to know if similar investor trends hold true for other agencies.

TYPES OF AGENCY DEBT SECURITIES

Agency debt securities are issued in a variety of maturities and types to help manage their business financing needs, mitigate interest-rate risk, and expand their respective investor bases.

Short-Dated Agency Securities

Agencies frequently issue securities with relatively short-term tenors of less than one year, often referred to as discount notes. Discount notes are issued at a discount from par with maturities ranging from one day to 365 days and are priced similar to Treasury bills. Some of the agencies offer regular and predictable discount note supply through established programs with standard announcement and offering dates, including Fannie Mae’s Benchmark Bill program, Freddie Mac’s Reference Bill program, and the Federal Home Loan Bank’s discount note auctions. Other discount notes issued by the agencies are offered through reverse inquiries from investors.

Longer-Dated Agency Securities

Agencies also offer a wide variety of longer-dated securities with maturities of between 1 and 30 years. Most agency debt is U.S. dollar denominated, although some agencies have issued debt denominated in foreign currencies. Some longer-dated issues are large in size with fixed-rate coupon offerings issued through established programs, such as Fannie Mae’s Benchmark Notes program, Freddie Mac’s Reference Notes program, and the Federal Home Loan Bank’s Global Debt program. These programs were established in the late 1990s to create more regular and standardized types of debt with greater liquidity. Debt issued through these programs increased from $118 billion in 2000 to $400 billion in 2010. The programs were also intended to produce a yield-curve for liquid agency securities and thereby appeal to investors that might otherwise purchase Treasury securities. These fixed-rate coupon offerings typically have semiannual coupon payments with principal redeemed only at the security’s stated final maturity date.

In addition to these programs, agencies also offer smaller longer-dated securities with a variety of characteristics that are frequently referred to as medium term notes. In the past, agencies have offered medium term notes with a variety of characteristics, including: senior and subordinated hierarchies; callable, putable, and fixed-tenor structures; fixed-rate, floating-rate, indexed, and zero coupons and, denominations in U.S. dollars or in other currencies. Some agencies also offer variations on fixed-rate callable securities called “step-up notes,” in which the issuer will generally have the choice to call a security on a specific date and if it is not called then the investor’s interest rate increases or “steps up.” In addition, the FHLB Office of Finance offers a TAP issue program, in which it issues fixed-rate securities at longer-dated maturities and has the option to continually reopen a security for a three-month period based upon investor demand. Some of these longer-dated security types are discussed in greater detail later in this chapter.

Most longer-dated agency securities generally make semiannual coupon payments and are priced similar to Treasury notes, depending on their various characteristics. Some longer-dated agency securities are also eligible for stripping into principal and interest components through the Federal Reserve Book Entry System.

Callable Securities and Other Tools to Mitigate Interest-Rate Risk

Agencies issue a wide variety of longer-dated securities to better manage the interest rate and cash flow risk inherent in their businesses, especially as some relate to securitizing mortgages and purchasing mortgage-backed securities. One of the most notable risks for housing-related GSEs is the unpredictable nature of mortgage prepayment speeds, given that mortgage prepayments tend to vary with the interest rate environment. Specifically, mortgage prepayment speeds tend to increase in a declining interest rate environment and decrease in a rising rate environment.

Housing-related agencies partially mitigate this risk by issuing callable debt securities, which have somewhat similar characteristics to mortgage-backed securities. Specifically, the duration of mortgage-backed and callable debt tends to shorten as interest rates decline due to the increased likelihood that the call options inherent in these structures will be exercised by the mortgage owner or callable debt issuer. By issuing a callable debt, GSEs effectively purchase a call option from an investor and compensate the investor by issuing the security at a slightly lower price or higher yield when compared to similar noncallable securities.

Callable securities generally have three main characteristics: the maturity date, the lockout period, and the type of call feature. The maturity date is somewhat similar to a noncallable security, which is the latest date on which the security will be retired and principal redeemed assuming the security is not called. The lockout period refers to the amount of time over which a callable security cannot be called by the issuer. For example, a “3 noncall 1-year security” cannot be called for the first year but may be callable at a specific time over the remainder of the security’s total 3-year life. The call feature is generally one of three types: European-style, in which the call option can only be exercised on a single day at the end of the initial lockout period; Bermudan-style, in which the call option can be exercised on coupon payment dates after the conclusion of the initial lockout period; and, American-style, in which the call option can be exercised at any point after the initial lockout period.7

Housing-related agencies frequently issue callable debt, as shown in Exhibit 10–2, and callable debt issuance has been between $460 and $745 billion in recent years. Callable debt has comprised at least 35% to 49% of total housing-related GSE issuance for maturities greater than 1 year since 2007.

EXHIBIT 10–2

Callable Debt Issuance by Fannie Mae, Freddie Mac, and Federal Loan Home Bank: 2007–2010

In addition to callable securities, housing-related GSEs also utilize a variety of other tools to help mitigate interest rate risk, including interest rate derivatives such as swaps and swaptions. Callable debt and interest-rate derivatives are an important part of housing-related GSE risk management strategies, which have also allowed some GSEs to expand their investor base.

THE PRIMARY MARKET

The agencies use a variety of methods to distribute their securities, including competitive dealer bidding through auctions, issuance allocation to dealers, sales to investors through dealers, and direct sales to investors. The method may differ based on the issuer and the type of debt being offered.

Agencies have a variety of ways to issue short-dated securities, although most offerings are executed through regular discount note auctions or reverse inquiry sales. Housing-related agencies offer programs that provide a regular and predictable supply of short-dated securities to the market through weekly discount note announcements and auctions. Auctions are underwritten by a predetermined group of dealers who participate in the auctions through Internet platforms specific to each of the housing-related agencies. Depending on the agency, these discount note offerings may be conducted through single- or multiple-price auctions.

Agencies also provide discount notes through reverse inquiry offers. In this process, an agency will post rates daily to the public or investor community at which they are willing to issue discount securities. These rates are sometimes referred to as window rates. Dealers will then assist investors in making offers to the issuing agency for a specific amount and tenor near the applicable rate. This process is attractive for both the agency issuer and investor as it allows for a broader range of participants to finance the agencies at short-dated tenors which best meet their investment objectives. However, discount notes issued through the reverse inquiry or window offering process may have nonstandard maturity dates and limited sizes outstanding, which can hinder secondary market liquidity should they be sold by the original investor.

For longer-dated securities, agencies will also use a variety of methods, including syndicated offerings, reopening auctions, or reverse inquiry sales. A common distribution mechanism for agency debt securities is to allocate them among members of a selling group or syndicate of dealers. The syndicate provides market and trading information to the issuing agency before and during the allocation and may support secondary trading in the issue after allocation. In compensation for their services, the syndicate members are offered a concession in the offering or they are able to retain a percentage of the proceeds from the sold securities.

The syndication process is used by some agencies to issue callable and standard fixed-rate coupon offerings. Syndications are most frequently used to issue large fixed-rate coupon offerings such as those issues through Fannie Mae’s Benchmark Notes program, Freddie Mac’s Reference Notes program, and the Federal Home Loan Bank’s Global Debt program. To coordinate the issuance process among these programs, the U.S. Treasury Department in coordination with the FHFA and the housing-related agencies establish a monthly issuance calendar in which each agency has one predetermined day on which it can offer large fixed-rate coupon offerings to investors. The agencies can choose to offer securities on their respective date or pass and wait until their next scheduled issuance date. This monthly calendar coordination ensures that each housing-related agency has the potential to offer coupon securities in relatively large size without interfering with the issuance plans of any other agency. Of note, on these scheduled offering dates, the agencies can also choose to reopen previously issued securities through these established programs. The agencies generally manage the reopening auctions through their internal systems and do not require a dealer syndicate for this process.

Similar to discount notes, agencies also issue medium term notes through a reverse inquiry process. Some dealers will post or send daily rates for a variety of security types to underwriting dealers, who then assist investors in making offers to the issuing agency. Agencies frequently issue callable securities through the reverse inquiry process and are able to entertain a wide variety of callable structure reverse inquiries simultaneously, including those with European, American, and Bermudan call options. Agencies will also consider a wide variety of other debt structures through the reverse inquiry process. On any given day, agencies can issue longer-term securities with a variety of different maturities, coupon types, and call features through this process.

THE SECONDARY MARKET

Like Treasury securities, agency securities trade in a multiple-dealer over-the-counter secondary market. Also like Treasury securities, trading among dealers is screen-based, through interdealer brokers. Trading volume is significantly lower than that in the Treasury market, but it is still reasonably high relative to other fixed income markets. In fact, primary dealer trading volumes in agency debt securities averaged 11% of U.S. fixed income daily trading volumes from 2000 to 2010.

Secondary market trading activity is also concentrated in agency securities in discount notes. From 2002 to 2010, discount notes averaged 78% of daily primary dealer trading volumes, versus longer-term agency securities which averaged only 22% of such volume. During 2010, daily trading by primary dealers averaged $60 billion per day, with $47 billion in discount notes and $13 billion in longer-dated coupon securities.

AGENCY DEBT ISSUANCE

The quantity of agency debt securities sold in the primary market increased throughout the 1990s and 2000s. In 1990, agencies issued only $20 billion in securities with one year or more to maturity. At the end of 2000 agencies issued $483 billion in longer-term debt and by the end of 2009 agencies issued nearly $1.1 trillion in debt with maturities over one year. However, agency short-term issuance exceeds long-term issuance by nearly four times.

The housing-related agencies have also been the largest issuers of agency debt with maturities of over one year since the early 1990s. Since 1998, Fannie Mae, Freddie Mac, and the Federal Home Loan Bank have also issued more than 90% of total long-term agency debt securities in any year. At the end of 2009, issuance from these three entities comprised 92% of total long-term agency debt issuance.

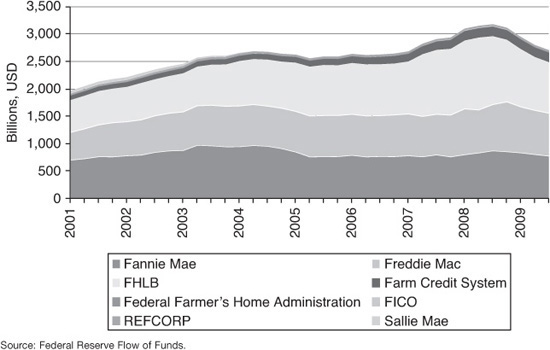

Despite the increased agency issuance since 2000, agency debt outstanding has increased only modestly over the same time horizon, as shown in Exhibit 10–3. The outstanding debt of the agencies stood at $1.8 trillion by the end of 2000 and increased $880 billion to $2.7 trillion by the end of 2009. Much of the new agency debt issuance has gone to service outstanding debt and resulted in limited net new issuance during the period.

EXHIBIT 10–3

Agency Debt Outstanding: 2001–2009

The vast majority of total agency debt outstanding is attributable to the three main housing-related agencies, Fannie Mae, Freddie Mac, and the Federal Home Loan Bank. Debt issued by these three entities accounted for as much as 95% of outstanding debt in 2005 and 92% percent of total outstanding debt at the end of 2009. As shown in Exhibit 10–3, at the end of 2009 outstanding Fannie Mae, Freddie Mac, and Federal Home Loan Bank debt totaled $2.5 trillion.

ISSUING AGENCIES

As mentioned previously, agency securities are direct obligations of federal agencies or government-sponsored enterprises. Federal agencies are entities of the federal government. They include the Export-Import Bank of the United States, the Federal Housing Administration, the Government National Mortgage Association (Ginnie Mae), the Tennessee Valley Authority (TVA), and the Small Business Administration. Historically, a number of federal agencies issued their own debt securities. In 1974, the Federal Financing Bank was set up to consolidate agency borrowing and thereby reduce borrowing costs. However, the TVA still issues its own debt securities and accounts for nearly all the outstanding debt issued directly by federal agencies.

Government-sponsored enterprises (GSEs) are privately owned and operated entities chartered by Congress to work toward public policy goals and decrease the cost of funding for certain sectors of the economy. The GSEs are granted certain privileges to help them achieve their public purposes and, in turn, are limited to certain activities. As mentioned, agency debt securities are thought to have an implicit government guarantee, and agency security interest income is exempt from state and local taxation for many issuers. The agencies themselves are exempt from state and local income taxes and are also exempt from Securities and Exchange Commission (SEC) registration fees.

The largest GSEs were chartered to provide credit to the housing sector. As previously noted, they include Fannie Mae, Freddie Mac, and the Federal Home Loan Banks. Another set of GSEs was established to provide credit to the agricultural sector, including the Farm Credit Banks, the Farm Credit System Financial Assistance Corporation, and the Federal Agricultural Mortgage Corporation (Farmer Mac).

There are also older GSEs with debt outstanding and other GSEs that have recently been privatized. The Financing Corporation and the Resolution Funding Corporation are GSEs that were established to recapitalize the savings and loan industry but have not issued new securities in years, although they both have some debt outstanding. Another older GSE, the Student Loan Marketing Association (Sallie Mae), was wholly privatized at the end of 2004.

In addition to the agencies and GSEs, there have been some government initiatives that explicitly back types of fixed income securities for public policy purposes. The Temporary Liquidity Guarantee Program (TLGP) was established during the 2008 financial crisis, through which the Federal Deposit Insurance Company (FDIC) guaranteed senior unsecured debt of insured depository institutions issued between October 14, 2008 and June 30, 2009 that matures before June 30, 2012.

The remainder of this section provides a brief overview of each of the agencies, GSEs, and government-backed initiatives that have debt securities outstanding or were recently wound-down. This information is also summarized in Exhibit 10–4.

EXHIBIT 10–4

Agency Descriptions

LARGE, ACTIVE ISSUERS

The three large, active issuers include Fannie Mae, Freddie Mac, and the Federal Home Loan Bank System.

Federal National Mortgage Association (Fannie Mae)

Fannie Mae was established in 1938 to develop a secondary market for residential mortgages and was chartered by Congress in 1968 as a private stockholder-owned corporation. Fannie Mae buys home loans from banks and other mortgage lenders in the primary market and holds the mortgages until they mature or issues securities backed by pools of the mortgages.

As previously noted, on September 6, 2008 the Director of the FHFA was appointed conservator of Fannie Mae, at which time the GSE also established the PSPA with the U.S. Treasury Department to ensure the enterprise will maintain a positive net worth. Through the end of 2010, Fannie Mae had drawn $87.6 billion from the U.S. Treasury. FHFA also regulates Fannie Mae.

To finance their businesses, Fannie Mae issues a variety of securities, including discount notes and medium-term notes. In January 1998, Fannie Mae initiated its Benchmark Notes debt issuance program, followed by the introduction of its Benchmark Bills program in November 1999. Both Benchmark programs are intended to provide for the regular and predictable issuance of large-sized securities and are meant to enhance their efficiency, liquidity, and tradability. Benchmark Bills are issued via Dutch-style auction, with three- and six-month bills offered weekly and one-year bills offered on a less frequent, ad hoc basis. Benchmark Notes are issued via an underwriting syndicate of dealers following a yearly issuance calendar.

In 2010, Fannie Mae issued $439 billion in securities with maturities less than one year and $463 billion in securities with maturities greater than one year. At the end of 2010, Fannie Mae had outstanding $152 billion in securities with maturities less than one year and $642 billion in securities with maturities greater than one year.

Federal Home Loan Mortgage Corporation (Freddie Mac)

Freddie Mac is a stockholder-owned corporation chartered in 1970 to expand opportunities for homeownership and improve the liquidity of the secondary mortgage market. Freddie Mac purchases mortgage loans from individual lenders and sells securities backed by the mortgages to investors or holds the mortgages until they mature.

Similar to Fannie Mae, Freddie Mac entered conservatorship overseen by the FHFA in September 2006 and has a PSPA with the U.S. Treasury Department. In order to remain in positive net worth, Freddie Mac drew $63.2 billion from the U.S. Treasury through the end of 2010. FHFA also regulates Freddie Mac.

Freddie Mac issues a variety of debt securities, including discount notes and medium-term notes. In April 1998, Freddie Mac established its own benchmark securities program called Reference Notes, followed by Reference Bills in November 1999. Reference Bills are issued via Dutch auction, with three- and six-month bills offered weekly and one- and 12-month bills auctions offered optionally every month. Reference Notes are issued via an underwriting syndicate of dealers following a yearly issuance calendar.

In 2010, Feddie Mac issued $482 billion in securities with maturities less than one year and $331 billion in securities with maturities greater than one year. At the end of 2010, Freddie Mac had outstanding $195 billion in securities with maturities less than one year and $534 billion in securities with maturities greater than one year.

Federal Home Loan Bank System

The Federal Home Loan Bank (FHLB) system was established as a GSE in 1932 to increase credit access for the housing sector by supporting residential mortgage lending and related community investment through its member financial institutions. It consists of 12 federally chartered, privately owned Federal Home Loan Banks that are charged with supporting residential mortgage, small business, rural, and agricultural lending by more than 8,000 member-stockholder institutions. The FHLB system is a cooperative structure in which each member bank is a shareholder in one of the 12 regional banks. The regional banks make loans to the member institutions, which in turn make loans to homebuyers, small businesses, and others.

The FHFA regulates the FHLB system for mission, as well as safety and soundness issues. Unlike Fannie Mae and Freddie Mac, none of the 12 regional Federal Home Loan Banks are in conservatorship.

FHLB debt issuance is conducted through the system’s fiscal agent, the Office of Finance. The FHLB Office of Finance sells a variety of debt securities, including discount notes and medium-term notes. The FHLB Office of Finance issues discount notes twice weekly via multiple price auctions in four standard maturities: 4-, 9-, 13-, and 26-weeks. The Office of Finance also maintains a discount note reverse inquiry window. In July 1999, the Office of Finance launched a TAP Issue Program in which it offers longer-dated fixed-rate securities at common maturities that can be reopened daily over a three-month period. In July 1994, the FHLB Office of Finance established a Global Debt program in which it generally offers large-sized, fixed-rate securities, although it can offer smaller issues with different characteristics. FHLB globals are issued via a single dealer or an underwriting syndicate of dealers following a yearly issuance calendar.

In 2010, the FHLB Office of Finance issued $1.2 trillion in securities with maturities less than one year and $533 billion in securities with maturities greater than one year, including $31 billion in TAP issues. At the end of 2010, the FHLBs had outstanding $195 billion in securities with maturities less than one year and $602 billion in securities with maturities greater than one year, including $88 billion in TAP issues.

SMALLER, ACTIVE ISSUERS

The Farm Credit System, the Federal Agricultural Mortgage Corporation, and the Tennessee Valley Authority are three smaller, active issuers.

The Farm Credit System

The Farm Credit System (FCS) is a GSE established in 1916 to provide credit to the agricultural sector. The FCS consists of five Farm Credit Banks and approximately 88 Associations. Products and services offered by FCS institutions include real estate loans, operating loans, rural home mortgage loans, crop insurance, and various financial services. The FCS and the system’s fiscal entity are regulated by the Farm Credit Administration.

The Federal Farm Credit Banks Funding Corporation is the system’s fiscal entity, providing funds to system institutions through the issuance of debt securities. The FCS issues discount notes, fixed-rate callable and noncallable securities, and floating-rate notes. In addition, FCS also issues Designated Bonds, which are large, liquid callable and noncallable issues. These bonds are issued through a dealer syndicate and can have 2- to 10-year original maturities, with a minimum issue size of $1 billion for noncallable issues and $500 million for callable bonds. Near the end of 2010, FCS outstanding debt included $17 billion in maturities less than one year and $162 billion in long-term debt.

Federal Agricultural Mortgage Corporation (Farmer Mac)

Farmer Mac is a stockholder-owned corporation chartered in 1988 to promote a liquid secondary market for agricultural real estate and rural housing loans. It does this by buying qualified loans from lenders and grouping the loans into pools against which it issues securities. Farmer Mac thus performs a role for the agricultural mortgage market similar to that performed by Fannie Mae and Freddie Mac for the residential mortgage market. Farmer Mac issues discount notes and medium-term notes, including callable and noncallable securities. Near the end of 2010, Farmer Mac outstanding debt included $4 billion in maturities less than one year and $3 billion in long-term debt.

Tennessee Valley Authority

The Tennessee Valley Authority (TVA) is a government-owned corporation established in 1933 to promote development of the Tennessee River and adjacent areas. The TVA manages the river system for flood control, navigation, power generation, and other purposes and is the nation’s largest public power company.

The TVA issues discount notes as well as longer-term coupon securities, called Power Bonds. Interest and principal on Power Bonds are paid from the proceeds of TVA’s power program. Near the end of 2010, TVA outstanding debt included $219 million in discount notes and $23 billion in long-term debt.

NONACTIVE ISSUERS AND RECENTLY RETIRED GSEs

In addition to the issuers discussed above, there are issues outstanding and traded in the market from entities that were previously GSEs and those that are not currently active in the issuance market.

Financing Corporation

The Financing Corporation (FICO) was established in 1987 to finance the recapitalization of the Federal Savings and Loan Insurance Corporation (FSLIC). Between 1987 and 1989, FICO issued debt obligations with an aggregate principal value of $8.2 billion. Towards the end of 1991, FICO’s authority to issue new debt was terminated. The FHLB system provided FICO with initial capital to purchase zero-coupon Treasury securities in order to repay their principal. FICO interest payments are funded by an assessment on FDIC-insured institutions. Near the end of 2010, FICO debt outstanding totaled approximately $8 billion.

Resolution Funding Corporation

The Resolution Funding Corporation (REFCorp) was established in 1989 as the funding arm of the Resolution Trust Corporation to finance the recapitalization of the savings and loan industry. REFCorp issued $30 billion in debt securities between 1989 and 1991. Interest payments on REFCorp bonds are guaranteed by the U.S. government, and the principal is protected by the purchase of zero-coupon bonds with a face value equal to those of REFCorp bonds. The full $30 billion in issued debt securities was outstanding near the end of 2010.

Farm Credit System Financial Assistance Corporation

The Farm Credit Financial Assistance Corporation was chartered in 1988 to finance the recapitalization of FCS institutions. Between 1988 and 1990, the corporation raised $1.3 billion through the issuance of debt securities, which it provided to system institutions in return for preferred stock. Unlike most GSEs, the debt securities of this corporation were fully guaranteed by the U.S. Treasury. All debt issuance by the corporation has been called or matured, with the last bond maturing in June 2005. The Financial Assistance Corporation’s charter was canceled by the FCA as of December 31, 2006.

Student Loan Marketing Association

Student Loan Marketing Association (Sallie Mae) was a stockholder-owned corporation established in 1972 to increase the availability of student loans. As a GSE, Sallie Mae purchased insured student loans from lenders and made loans to lenders secured by student loans. Sallie Mae was reorganized in 1997 in a step toward privatization and was fully privatized at the end of 2004. As a GSE, Sallie Mae issued discount notes, medium-term notes, and other debt securities, but no longer has any GSE-related debt outstanding. Sallie Mae was replaced by a publicly held, private sector financial services company named SLM Corporation, which specializes in financing education.

Treasury Liquidity Guarantee Program

The Treasury Liquidity Guarantee Program (TLGP) was announced on October 14, 2008, as an initiative to counter systemic risks in the financial sector by ensuring that financial institutions would be able to rollover maturing wholesale debt. Through the TLGP, the Federal Deposit Insurance Corporation (FDIC) provided guarantees for a limited amount of newly issued senior unsecured debt of insured depository institutions, most U.S. bank holding companies, and one large nonbank finance company. Debt issued through the TLGP is backed by the full faith and credit of the U.S. government.

Issuers in the TLGP were required to pay a fee to the FDIC that was based on the maturity of the debt and the type of institution that was issuing it. Each participating financial institution was limited to a maximum amount of guaranteed debt that it could issue based on the amount of senior unsecured debt scheduled to expire over a set time period. Guarantees for TLGP-backed senior unsecured debt originally applied to issuance by June 30, 2009 for maturities before June 30, 2012. However, this was extended to issuance by October 31, 2009 for maturities before December 31, 2012.

Issuance through the TLGP was elevated at the start of the program when other forms of corporate debt issuance were limited. During the first 6 months of the TLGP program $346 billion in term debt was issued from applicable institutions. However, as corporate credit markets improved, credit availability increased, and the FDIC encouraged firms to return to private funding markets, TLGP issuance and amounts outstanding declined. At the end of 2010, outstanding TLGP debt totaled $267 billion.

ACKNOWLEDGMENTS

Mark Cabana’s views expressed in this chapter are his and not necessarily those of the Federal Reserve Bank of New York or the Federal Reserve System.

KEY POINTS

• Agency securities are direct obligations of federal government agencies or government-sponsored enterprises. Agency securities have historically been viewed as having limited credit risk, although they are not risk free and have at times traded with a notable discount to Treasury securities.

• Agency security issuance and amount outstanding have grown in recent years owing to the growth of the housing GSEs—Fannie Mae, Freddie Mac, and the FHLB system. However, going forward, the supply of agency securities may decline as housing GSE retained portfolios shrink and as the government reforms its role in mortgage finance.

• Federal agencies and GSEs issue a wide variety of debt securities, including discount note securities at tenors less than one year and medium term notes with numerous structures at maturities greater than one year.

• Agencies use a variety of methods to distribute their securities, including competitive dealer bidding through auctions, issuance allocation to dealers, sales to investors through dealers, and direct sales to investors.

• The vast majority of agency debt issued (mostly concentrated in discount notes) and traded is from Fannie Mae, Freddie Mac, and the FHLB system.