Chapter 4 Introduction to Practical Valuation

In this chapter we will take a first look on how different instruments can be priced using a relatively small set of tools. We present the most commonly used approaches and solutions, but do not enter into the pros and cons of each method. If you wish to follow market standards you can safely apply the presented toolbox. However, if you wish to overcome known shortcomings and “beat the market,” you are advised to study the related academic literature. Use Cochrane (2005) as a starting to that literature.

We start with pricing using discounted cash flows, which is arguably the most fundamental tool. We then move on to market interest rates and in particular how to use yield curves to obtain appropriate estimates for market interest rates for different horizons.

Next we take a brief look at “beta” calculation and the cost of equity before moving on to option pricing. Finally we introduce the most popular building blocks for financial instruments that should be in any valuation toolbox: a basic set of commonly used pricing models covering debt instruments, equity, and simple options.

Each tool description is accompanied by a hands-on exercise in our companion web site toolbox.

4.1 The Basic Tools for Valuation

The starting point for our journey will be some basic knowledge of the most fundamental and common tools for valuation. In the first part of the chapter we take a look at the pricing with discounted cash flows, which is arguably the most fundamental tool. Next we look at market interest rates and in particular how to use yield curves to obtain appropriate estimates for market interest rates for different horizons.

Next we will take a brief look at the calculation of beta and the cost of equity. The last tool we will look at in the first section is option pricing. This is second only to discounted cash flow valuation in its universal applicability and is completely indispensable for a very large number of valuation tasks.

4.1.1 Pricing with Discounted Cash Flows

Anybody who has cash available today and is willing and able to lend or invest normally would do so only if there was some reward. This reward might be a pre-agreed fixed percentage of the amount on loan or invested or some agreed share of rewards from a business or other asset. In the simpler cases we may know the actual amounts of the future rewards in monetary terms already, whereas in the more complex cases we may know the actual amounts only later.

In the simpler cases we can usually directly work out the price using the Discounted Cash Flow Valuation methods and an appropriate interest rate. In more complex cases, as long as no optionality is involved we can still use Discounted Cash Flow Valuation methods, albeit in some modified form.

The diagram in Figure 4.1 shows a simple loan or investment where both the time of repayment of the amount invested plus the pre-agreed reward and its actual amount are known. The cash payment at t0 is the price of the future cash flow at t1 in today’s (t0) money, and the cash flow at t1 is the original amount on loan plus some amount of interest. If the loan is for exactly one year then the ratio of the reward to the amount on loan is the annual interest rate.

If instead we know the interest rate to use and also the amount we will receive at the end of the loan we can similarly calculate the value of the cash flow in today’s money. This value in today’s money is usually called Present Value and in fact is the price of the future cash flow today. Formula 4-1 provides a general method for calculating the price or present value of a cash flow that an investor will receive at some arbitrary but pre-agreed time in the future given an appropriate market interest rate.

Formula 4-1 assumes that interest is calculated and added to the loan amount once a year and the resulting compound value is then used as the basis for the following year’s calculation for interest due. This is called annual compounding. If we have a nominal annual interest rate but actually compound the interest more frequently, for instance every month, we first have to translate the nominal annual interest rate into one that is adjusted for the effect of more frequent compounding. Formula 4-2 provides the method by which we can translate a nominal annual interest rate into one that is adjusted for the effects of compounding over a period other than a year.

For example, if the period is 6 months, representing a semi-annual frequency, n = 2. If the period is one week, n = 52, and so on.

Often it is better to use calculations that assume continuous compounding. Continuous compounding is the case in which the time period for compounding is infinitely small and thus continuous. If we have a nominal annual interest rate and any given period for compounding we can use Formula 4-3 to translate it into an equivalent interest rate for calculations assuming continuous compounding.

If the interest rate we have is a continuous compounding interest rate, then we need to use a modified form of the discounted cash flow formula given in Formula 4-1. This modified discounted cash flow valuation formula for continuous compounding interest rates is shown in Formula 4-4.

Formula 4-4: Valuing a cash flow using a continuous compounding interest rate

where:

- PVCashFlow: the present value or price of future cash flows in today’s money

- F: cash flow amount to be received at time t in the future

- T: the time to maturity, i.e. cash flow payment date, in number of years

- r: the continuously compounded annual interest rate for maturity T

- e: the exponential constant

We will later see that interest rates are normally not the same for different periods and thus we normally need to calculate the price of each cash flow and then add them all together if we want to get a price for an asset that has more than one cash flow (for instance, a bond paying coupon as well as returning the principal amount invested at maturity).

Sometimes, however, we might want to have a quick approximation for the price of such an instrument using just one average interest rate for all cash flows of the instrument. Formula 4-5 provides such an approximation for calculating the price for a fixed coupon bond as illustrated by the cash flow timeline diagram in Figure 4.2.

Formula 4-5: Valuing a Coupon Bond using a continuous compounding interest rate

where:

- PVCashFlow: the present value or price of a future cash flow in today’s money

- FCoupon: coupon cash flows from the bond

- FPrincipal: cash flows from repayment of the principal of the bond

- T: the time to maturity in number of years

- n: number of coupon payments per year

- N = T × [1/n)

- r: the continuously compounded average annual interest

- e: the exponential constant

There are two common variations of the theme of valuing a coupon bond: First the valuation of an annuity, which is the same as valuing a coupon bond without including the value of the repayment of the principal at redemption. The cash flow timeline in Figure 4.3 illustrates this well since it is essentially the same as the cash flow time for a coupon bond as shown in Figure 4.2. A perpetuity, as illustrated by Figure 4.4, is an annuity with an infinite end date and thus again simply a special case of the valuation formula for a coupon bond.

Formula 4-6 shows how to value an annuity. You will note that this is the same as Formula 4-5 except that the final term for calculating the value of the principal repayment has been omitted. Formula 4-7 shows how to calculate the price of a perpetuity.

In this case the formula is similar to both Formulas 4-5 and 4-6, with the final and the penultimate terms missing. The final term is missing because there is no repayment of principal, and the penultimate because the value of the second term becomes 1 as the number of payments increases.

In order to improve your intuition about these formulas and their logic, it is helpful to take the time working through Lab Exercise 4.1 below.

Lab Exercise 4.1: Discounted Cash Flow Valuation

- 1. Open the file DCfValuation.R from the set of sample files from the companion web site for this book (http://modelbook.bancstreet.com/) and explore the R code illustrating the valuation calculation shown above.

- 2. Using the R application load the file DCfValuation.R and run the following examples at the command prompt in your R GUI:

R> InitialiseDCfValuation()

…

R> RunDCfValuation()

…

R> DCfValuation()

4.1.2 Interest Rates and Yield Curves

So far, we have taken the interest rates used in discounting for granted assuming that we can simply obtain an appropriate market interest rate for a given term from somewhere. In practice, however, obtaining such an appropriate interest rate is often one of the key challenges that must be overcome in the valuation process.

4.1.2.1 Zero Bond Rates and Interpolation

The simplest way to obtain an appropriate interest rate for discounting a given future cash flow would be to find a comparable zero coupon instrument with a redemption date that falls on the same date as the cash flow. In general it is unlikely that such an instrument would be available for an arbitrary date. Fortunately this can be easily overcome. If no zero coupon instruments with a fitting date exists we can use interpolation to arrive at an approximate rate from one zero coupon instrument that matures before the cash flow we want to price and one that matures after it. Formula 4-8 provides a method for Linear Interpolation that you can use to calculate an approximate rate for a given cash flow date that lies between the maturity dates of two zero coupon instruments such as either Zero Coupon Bonds or money market instruments that do not pay coupons (such as commercial paper).

Formula 4-8: Linear Interpolation

where:

- ri: interest rate for the cash flow for which we need an interest rate

- ti: time to the cash flow for which we need an interest rate in number of years

- t1: time to maturity in number of years for the zero coupon instrument maturing before the cash flow

- t2: time to maturity in number of years for the zero coupon instrument maturing after the cash flow

- r1: interest rate for the zero coupon instrument maturing before the cash flow; this is the yield to maturity for the instrument that is simply the Internal Rate of Return (IRR) of the instrument given its current market price and pre-agreed redemption value

- r2: interest rate for the zero coupon instrument maturing after the cash flow

In Example 4.1 you can see how Formula 4-8 can be used with some specific zero coupon bonds to obtain an interpolated interest rate for a point in time that lies between the maturity dates of the two chosen reference bonds.

Example 4.1: Linear Interpolation

Assume you have a cash flow in 4.25 years for which you need an interest rate. You have also already identified two zero coupon bonds, one with a maturity of three years and one with a maturity of six years from which you can interpolate the rate for 4.25 years. The bond with three years to maturity has a yield to maturity of 3.88% and the 6 year bond has a yield to maturity of 4.13%. Using Formula 4-8 you can then calculate

Thus, the interpolated interest rate for a cash flow in 4.25 years would be ri = 3.99%.

4.1.2.2 Bootstrapping and Interpolation

Although in some cases you may have two or more suitable Zero Coupon Bonds for which you may be able to obtain accurate market prices, in general there are not enough zero coupon instruments to be able to construct complete yield curves from the shortest maturities all the way to long-term maturities above 10 years and reaching 15, 20, or even 30 years.

One way to get around this problem is to recover zero coupon rates from the prices of coupon bearing bonds using a procedure called bootstrapping.

To illustrate what bootstrapping is, let’s consider the case where you have obtained a collection of coupon bonds each paying a six monthly coupon. The shortest maturity in this collection is a bond with only the last coupon and the redemption still outstanding, and thus six months or less from maturity. The next maturity in the collection should be a bond with two coupons still outstanding and thus a year or less from redemption. The remaining bonds in the collection in increasing order of time to maturity each should have one more additional coupon period remaining the one preceding it, starting with one that has three coupons outstanding.

Bootstrapping works by solving first for the interest rate implied by the price for the bond with only one coupon remaining. The interest rate obtained in this way can then be substituted back into the calculation for the implied interest rate for the last coupon and redemption of the bond with two coupons outstanding, which now becomes solvable.

After solving for the implied one year zero coupon interest rate we can then substitute this together with the six month rate back into the calculation for the implied interest rate for the last coupon and redemption of the bond with three coupons outstanding. This will let us then solve for the zero coupon interest rate applicable to a term of 1.5 years.

If we now continue in the same way we will be able to obtain a zero coupon rate for each maturity in the set. Formula 4-9 provides a method for performing the bootstrap calculation in one step using matrix notation. Denote a discount factor d(t) as a function of a term t specific interest rates r(t) as

Formula 4-9 then shows that a vector of discount factors d multiplied by the matrix of coupon and redemption cash flows F results in the vector p of observed bond prices. This can be rearranged to solve for discount factors in d, which can be obtained by multiplying the transpose of Matrix F with the vector p. This method is implemented in the code for Lab Exercise 4.2 on page 89.

Formula 4-9: Calculating zero bond interest rates by bootstrapping

In matrix notation the problem is formulated as follows:

In full matrix notation the formulation looks as follows:

Solving for d we can rearrange as follows:

or in matrix notation:

where:

- p: vector of observed market prices P(t1) … P(tn)

- F: matrix of coupon and principal cash flows F(t1,1) … F(tn,1)

- FT: transpose of the matrix of coupon and principal cash flows

- d: vector of bootstrap zero coupon interest rates r(t1) … r(tn)

- p(t1) … p(tn): observed market prices of coupon bearing bonds with a range of maturities from, say, t1 = 6 months to tn = n × 6 months

- F(t1,1) … F(tn,1): coupon and principal cash flows of coupon bearing bonds with a range of maturities from, say, t1 = 6 months to tn = n × 6 months at times t1 = 6 months to tn = n × 6 months

- r(t1) … r(tn): calculated bootstrap zero coupon interest rates for a range of maturities from, say, t1 = 6 months to tn = n × 6 months

Nota Bene. The above method assumes that the series of cash flow dates coincide between the instruments used. This is a general shortcoming of the Bootstrapping Method. For the method to work, real cash flows have to be properly adjusted to fit the generic cash flow schedule used in the method.

Once we have obtained a set of zero coupon rates we can again interpolate rates between the maturities of the set of zero coupon instruments we used as input. We could again use linear interpolation. Alternatively we can use cubic interpolation, which will result in a smoother overall curve. Formula 4-10 provides a method for cubic interpolation that we can use for calculating intermediate points either in order to obtain rates for use in discounted cash flow valuation or to draw the full yield curve.

Formula 4-10: Cubic interpolation of interest rates

using

where:

- ri: interpolated interest rate we are looking to obtain to use for pricing given the cash flow

- ti: time to the cash flow for which we need an interest rate in number of years

- t1: time to maturity in number of years for the zero coupon instrument maturing before the cash flow and before t2

- t2: time to maturity in number of years for the zero coupon instrument maturing before the cash flow but after t1

- t3: time to maturity in number of years for the zero coupon instrument maturing after the cash flow but before t4

- t4: time to maturity in number of years for the zero coupon instrument maturing after the cash flow and after t3

- r1: interest rate for the zero coupon instrument maturing at t1

- r2: interest rate for the zero coupon instrument maturing at t2

- r3: interest rate for the zero coupon instrument maturing at t3

- r4: interest rate for the zero coupon instrument maturing at t4

- λ1: interpolation factor for R1

- λ2: interpolation factor for R2

- λ3: interpolation factor for R3

- λ4: interpolation factor for R4

Again, it is helpful to let the above logic sink in using the Lab Exercise below of the companion website.

Lab Exercise 4.2: Bootstrapping and Interpolating Zero Coupon Interest Rates

- 1. Open the file YCurveBootstrap.R from the set of sample files from the companion web site for this book (http://modelbook.bancstreet.com/) and explore the R code illustrating the yield curve calculation shown above.

- 2. Using the R application load the file YCurveBootstrap.R and run the following examples at the command prompt in your R GUI:

R> InitialiseYCurveBootstrap()

…

R> RunYCurveBootstrap()

…

R> YCurveBootstrapReports()

4.1.2.3 Parametric Yield Curve Estimation

Although the bootstrap method is easy to implement, it has one important drawback: Since it fits the resulting yield curve exactly to the data we have used as input it does not deal well with the errors that are unavoidable in the prices used. Bootstrapping will thus tend to be significantly influenced by any errors in individual bond prices. To alleviate this problem we can use a parametric yield curve estimation approach that fits a suitable parametric function to the observed data using a Nonlinear Least Squares estimation algorithm.

One of the earliest such approaches is the method set out by Nelson & Siegel (1987). Formula 4-11 is implemented in Lab Exercise 4.3, Parametric Yield Curve Estimation, which uses a Nonlinear Least Squares estimation algorithm to fit this formula to a given data set of fixed income instruments.

Once the parameters α1, α2, α3, β have been estimated we can then use Formula 4-12 to calculate the interest rate at any point t in time as long as t > 0 and smaller than or equal to the value of t for the time of the cash flow with the longest time to maturity in the set of bonds that we used to estimate the parameters of α1, α2, α3, β.

Formula 4-12: Nelson & Siegel (1987) parametric yield curve calculation

where:

- y(t): interest rate for a cash flow at time t

- t: time from now to the cash flow at point t

- e: exponential constant

- α1, α2, α3, β: parameters obtained by estimation using Formula 4-11 and nonlinear least squares estimation

Lab Exercise 4.3 implements both the estimation of the parameters α1, α2, α3, β: for Formula 4-11 and the actual calculation of point on the estimated yield curve using estimated values for parameters α1, α2, α3, β as inputs to Formula 4-12 for a range of equally spaced values for t.

Lab Exercise 4.3: Parametric Yield Curve Estimation

- 1. Open the file YCurveParametric.R from the set of sample files from the companion web site for this book (http://modelbook.bancstreet.com/) and explore the R code illustrating the yield curve calculation shown above.

- 2. Using the R application load the file YCurveParametric.R and run the following examples at the command prompt in your R GUI:

R> InitialiseYCurveParametric()

…

R> RunYCurveParametric()

…

R> YCurveParametricReports()

4.1.2.4 Sources of Ready-made Yield Curve Data

After taking a look at the procedures for estimating yield curves and the resulting interest rates we need for valuation it should be clear that this is no trivial task, even in the very simplest of circumstances and taking the simplest possible method. It therefore often pays to obtain yield curve data ready from an external source such as either a commercial data vendor or a specialised calculation service.

4.1.3 Beta and the Cost of Equity

Being able to estimate yield curves will carry us a very long way in practical valuation tasks, but we need some more machinery before we can embark on valuing equity instruments and whole businesses. In order to be able to apply discounted cash flow pricing to equities we need a risk measure for equity analogous to the interest rate applicable in the discount rate for debt instruments.

The most commonly used pricing approach for equities is the Capital Asset Pricing Model (CAPM). The Capital Asset Pricing Model is based on the assumption that the variance of returns is the right measure of risk in the context of pricing, and the only risk that cannot be diversified will be rewarded.

In Formula 4-13 we can see the method for calculating the beta of an instrument relative to a market benchmark. Beta is the undiversifiable risk of an instrument or portfolio relative to the market as measured by a suitable market benchmark. A higher risk and thus higher rewards mean a higher beta, whereas a lower beta means less risk and thus lower expected returns.

where:

- βP,B: beta of instrument P with respect to benchmark B

- ŔP: time series of returns of the portfolio for periods 1 to n

- ŔB: time series of returns of the benchmark for periods 1 to n

- Cov(ŔP, ŔB): covariance between returns of the portfolio and the benchmark

- σ2B: benchmark variance

- n: total number of periods under consideration

Once we have calculated the beta for an instrument we can proceed to calculate its cost of equity. The cost of equity can be used to vale an equity instrument (stocks or investment fund shares) via the discounted cash flow method. The cost of equity is then used in an analogous manner as the time-dependent interest rate for debt instruments.1 Formula 4-14 shows how to obtain the cost of equity if we know the beta of an instrument, the risk free rest of interest applicable, as well as the long-term average return of the market index.

where:

- CEquity: cost of equity for equity instrument

- βP,B: beta of instrument P with respect to benchmark B

- RRf: risk free interest rate. Usually this is taken to be the interest rate for long-term government bonds at a suitable maturity such as 10, 15, 20, 25, or even 30 years. This we can read of or calculate from a suitable yield curve that represents such credit risk free government bonds.

- E(RB): expected return of the market benchmark. This is simply the long term average for equity returns that we can again estimate from a time series of returns for a market benchmark we plan to use.

In many valuations we will use the cost equity directly, but sometimes we need to use an average cost of capital instead, such as when we need to value an entire firm rather than just the equity issued by the firm. Formula 4-15 provides a method for calculating the weighted average cost of capital using the cost of equity and debt as well the total values for outstanding equity and debt capital.

Formula 4-15: Weighted average cost of capital (WACC)

where:

- CWACC: weighted average cost of capital

- CEquity: cost of equity

- CDebt: cost of debt

- E: total value of equity issued by the firm

- D: total value of debt issued by the firm

- [E/(E + D)]: proportion of equity issued by the firm to total of all capital

- [D/(E + D)]: proportion of debt issued by the firm to total of all capital

Lab Exercise 4.4 implements the calculations for beta, cost of equity, and the weighted average cost of capital using some hypothetical index and instrument return data.

Lab Exercise 4.4: Cost of Equity

- 1. Open the file CostOfEquity.R from the set of sample files from the companion web site for this book (http://modelbook.bancstreet.com/) and explore the R code illustrating the valuation calculations shown above.

- 2. Using the R application load the file CostOfEquity.R and run the following examples at the command prompt in your R GUI:

R> InitialiseCostOfEquity()

…

R> RunCostOfEquity ()

…

R> CostOfEquityReports()

4.1.4 Option Pricing

So far we have looked at discounted cash flow valuation as well as related tools for the estimation of yield curves or the cost of equity, which will allow us to value already calculated prices for a large number of different assets covering both debt obligations and equity rights.

There is however another large set of assets that is derived from debt obligations and equity rights. These are option rights—the right, but not the obligation, to either sell or buy some other asset like a debt obligation or equity right. The most commonly used method in practice is the Black & Scholes option valuation formula, developed by Fischer Black, Myron Scholes and Robert Merton in the early 1970s.2 This method is set out in Formula 4-16 and illustrated in Lab Exercise 4.5.

Lab Exercise 4.5: Option Pricing

- 1. Open the file SimpleBSOptionVal.R from the set of sample files from the companion web site for this book (http://modelbook.bancstreet.com/) and explore the R code illustrating the option valuation calculation introduced above.

- 2. Using the R application load the file SimpleBSOptionVal.R and run the following examples at the command prompt in your R GUI:

R> InitialiseSimpleBSOPtionVal()

…

R> RunSimpleBSOPtionVal ()

…

R> SimpleBSOPtionValReports()

4.2 Valuing Financial Assets

Now that we have a basic set of valuation tools let us take a look at the features of some of the most common financial instruments and how our tools introduced so far might help in the valuation of such instruments in a building block manner.

Finally to we will round up the first part of the chapter by taking a look at the most popular building blocks for financial instruments that should be in any valuation toolbox.

4.2.1 Valuing Bonds and Other Debt

Debt instruments are contracts between the issuer and the investor(s) by whom the issuer receives a lump-sum payment from the investor(s) and obliges himself to repay that lump-sum plus a pre-set set of interest (fixed or by formula) according to a pre-defined payment schedule.

4.2.1.1 Zero Bonds and Equivalent Securities and Loans

The simplest kinds of debt instruments are zero coupon bonds and equivalent securities and loans. A zero coupon bond is issued at a deep discount to its par or redemption value and then redeemed in one single payment that constitutes both a return of capital and a component that represents the required interest income for the entire life of the bond for the money originally received by the issuer from the investor when the instrument was issued or the loan taken out.

The cash flows involved can be illustrated in a Cash Flow Timeline diagram. Figure 4.5a shows such a diagram for a zero coupon bond or equivalent security or loan.

Figure 4.5b shows the data model building blocks involved when capturing data in a Zero Coupon Bond.

To value a Zero Coupon Bond or equivalent security or loan you can use the basic formula for calculating the present value of future cash flows by applying an appropriate interest rate for discrete compounding periods such as an annual interest or an interest rate for compounding at six month intervals.

We reproduce the formula in Formula 4-1, introduced earlier.

Formula 4-1 also works for shorter or longer compounding periods. For instance if interest is supposed to be compounded every six months then the rate rsix month should be used instead of rannual. Likewise instead of Tin Years you need to use Tin Half-Years and for Tin Years the equivalent six months figures can be calculated as follows: Tin Half-Years = 2 * Tin Years and rsix month = (1/2) * rannual = 0.5 * rannual.

Formulas 4-17 and 4-18 show how r can be adapted to compounding periods other than a year in the general case. Use Formula 4-16 to translate annual rate into one for another period and Formula 4-18 to translate the time to maturity from a value measured in years into one measured in other types of periods like months or quarters. After converting both the rate of interest and the number of periods to maturity you can then again use Formula 4-1, but this time substitute rperiod for rannual and Tin Periods for Tin Years.

Often you may have the interest rate as a rate for continuous compounding rather than for a given compounding period like a year. In this case you will need to use a slightly different formula. We have already introduced this in Formula 4-4, which shows how to calculate the price of a zero bond or equivalent if you have the interest rate used for continuous compounding. For convenience we have repeated Formula 4-4 here again.

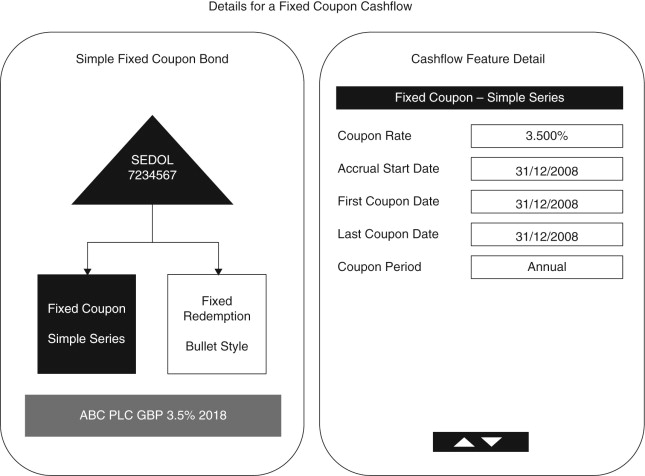

4.2.1.2 Fixed Coupon Bonds and Equivalent Securities and Loans

A large number of bonds and some equivalent instruments as coupon paying certificates of deposit have coupon or interest payments at regular intervals throughout the life of the instrument in addition to a redemption payment returning the capital at the end of the life of the instrument.

Figure 4.6a shows the cash flows involved on a cash flow timeline diagram. Looking at this diagram you may come to the conclusion that in fact the instrument is very much like a series of zero bonds—one for each coupon and the redemption—all packaged into a single unit. This in fact is a very useful view since it lets us reuse the pricing formulas we used for zero bonds. The price of the coupon bond in this case is simply the sum of the prices of the individual coupon and the redemption cash flow all added together.

Figure 4.6b and Figure 4.6c show the data model building blocks involved in capturing data on a Fixed Coupon Bond or an equivalent instrument.

If we need a quick shorthand method for calculating the price of a coupon paying bond we can also use Formula 4-5, which we introduced at the beginning of the chapter.

However, as this formula does not allow us to use different interest rates for the cash flows that occur at different points it can only approximate the price. It can be very useful if we need a fast and easy way to calculate an approximate price. For higher accuracy, however, we need to determine the details of each cash flow of the bond, and treating each like a separate Zero Coupon Bond, by calculating a price for each using the appropriate interest rate from a suitable yield curve.

Formula 4-5: Valuing a Coupon Bond using a continuous compounding interest rate

where:

- N = T × [1/n)

- PVCashFlow: present value or price of future cash flows in today’s money

- FCoupon: coupon cash flows from the bond

- FPrincipal: cash flows from repayment of the principal of the bond

- T: time to maturity in number of years

- n: number of coupon payments per year

- r: continuously compounded annual interest rate

- e: exponential constant

4.2.1.3 Bonds with Floating Coupons and Other Features

Another common form of a bond are Floating Rate Notes. They pay floating or resettable interest rates. In that case instead of paying a given coupon of say X% over the life of the instrument it pays a coupon that is based on some market interest rate like the LIBOR. At periodic intervals the rate is reset using a formula such as LIBOR + Y% and the following coupon or coupons until the next rate reset are then based on this rate as fixed at the last reset date. In the next chapter we will show how the formulas used for pricing Zero Coupon Bonds can again be applied to Floating Rate Notes. In Figure 4.7 you can see an illustration of how a floating rate without a call feature can be represented using the building block method. Figure 4.8 shows a building block representation of a simple zero bond in comparison.

Floating Rate Notes also sometimes have a cap or a floor that defines the maximum or minimum to which the rate can be reset. Here, as we will show later our zero bond formulas are no longer sufficient on their own, and we need to make use of option pricing tools to price the added feature. Again we will look at how to price these features in the following chapter.

Both fixed and floating coupon instruments also often offer the issuer the ability to call; that is to redeem the instrument early; and some bonds allow the investor to put the bonds back to the issuer; that is, they can ask the issuer to redeem their bonds early. Redemption put features for investors and redemption call features for issuers represent options that again could be calculated separately from the value of the rest of the bond and just added to the total price for the instrument.

Other features that can be added to a bond can usually be dealt with in a similar way.

4.2.2 Valuing Equities

Equity shares represent ownership rights in the assets of a specific company. As such, the purchaser of equity shares is entitled to a proportion of the income and capital of the company. Fund units are either equity shares in a fund or entitlements in a fund established as a trust rather than a company. In either case the main difference from equity shares is that the underlying asset pool is not a business but rather a portfolio of financial instruments.

See Chapter 3 for a more detailed description of both types of Equity and the related Cash Flows.

4.2.2.1 Valuation Models for Dividend Paying Equities

All equities ultimately derive their value from some form of equitable share of the cash flows generated by one or more underlying assets. Usually, this is a business or in the case of fund units a portfolio of financial assets or real assets like real estate properties. Equities are claims on the residual cash flows from income and capital after all other obligations such as debt interest and repayment and taxation have been met. Equities can thus again be valued with tools derived from those we used for valuing debt.

In a very simple case we might find an equity that has a long track record, paying a steadily growing divided paid for by a business in a very stable industry and very stable economic environment with profits growing at a steady rate that could be maintained indefinitely. The steadily growing dividend cash flows of this scenario are illustrated in Figure 4.10. In this case we can use the simple dividend discount model for equity valuation shown in Formula 4-19.

Many times you will find that even for a very simple rough estimate the assumptions of the simple dividend discount equity valuation model are unrealistic.

A very common case in valuation are firms that grow at very fast rate for some years and then are expected to settle down at a rate of growth that is sustainable indefinitely. In this case you need to value the equity by valuing the expected divided for each of the first n years using the simple debt valuation model from Formula 4-1, then calculate a value for the dividends from the year after year n until forever using simple dividend discount equity valuation from Formula 4-19, but using the correct values for year n. Then add all these valuations to a single total value for the equity. This valuation model is shown in Formula 4-20. Figure 4.11 illustrates the cash flow pattern of the two stage growth model.

Formula 4-20: Two stage dividend discount equity valuation

where:

- VEquity: value of the equity share

- dt: dividend paid on the equity share in year t

- t: index of year in the first 1 to t years (i.e., 1 in first year, 2 in second year, etc., and n in the final year where t = n)

- CEquity: cost of equity for equity instrument, representing the appropriate “interest rate” to discount the dividend stream

- glongterm: estimated steady sustainable growth of dividend stream from year

- dn+1: expected dividend on the equity share in the year after year t

- Vlongterm: = dn+1/(r − glongterm)

If the dividend growth is the same for the first n year you can take a slight short-cut using the model shown in Formula 4-21.

Formula 4-21: Simplified two stage dividend discount equity valuation

where:

- VEquity: value of the equity share

- VInitialPeriod: equity valuation for the first n years

- VLongTerm: equity valuation for the period after year n

- dcurrent: expected dividend paid on the equity at the end of year 1

- ginitial: estimated growth for the first n years

- glongterm: estimated steady sustainable growth of dividend stream after year n

- n: number of years initial period: e.g., 3 or 5 years

- CEquity: cost of equity for equity instrument, representing the appropriate “interest rate” to discount the dividend stream

- dn+1: expected dividend on the equity share in the year after year n

The model in Formula 4-20 is the most common in practical use since more accurate valuations can often be obtained from detailed forecasts that can be made for a certain number of years, whereas the value of cash flows from years beyond the forecast period is estimated using the simple steady state growth equity valuation model.

4.2.2.2 Valuation Models for Equities Based on Free Cash Flows

Up to now we have taken the basis for equity valuation to be the dividend stream they pay. In practice, however, you will find many equities do not pay a regular dividend. This is often the case with younger companies experiencing strong growth. In this case we can still value the equity but need to use a replacement for the dividend cash flows. This replacement is a value called Free Cash Flow to Equity, which is the net cash flow for the company in each period after paying all other claims like operating and other cash-based expenses, interest, and principal repayments on debt due as well as taxes.

We will look at how to calculate and value free cash flows in more detail in the following chapter.

4.2.3 Valuing Forwards and Futures

Forwards are simply trades concluded in advance where the exchange of cash against delivery of the asset takes place at some time in the future. A Futures Contract is a highly standardised alternative form of a forward that can be traded on an exchange because of its standardisation.

4.2.3.1 Valuing Forwards and Futures of Financial Assets without Income

Prices for futures and forwards are not necessarily exactly equal because of the difference in actual cash flow patterns between the two. In practice, however, this difference is usually ignored and a single formula is used for both. The basis for valuing both forwards and futures is the fact that they are essentially debt instruments denominated in terms of a certain quantity of an asset. In Figure 4.7 you can see an illustration of how a floating rate not with a call feature can be represented using the building block method. Figure 4.8 shows a building block representation of a simple zero bond in comparison.

To illustrate this consider the following alternatives for both the buyer and the seller of the forward or future:

The buyer of a forward could borrow money and buy the asset in the spot market. If the seller did not want to offer a forward, he or she could just sell the asset in the spot market and invest the proceeds in the money market, earning the given market interest rate for deposits or short-term instruments. Figure 4.13 illustrates the building block structure of a simple forward contract without any income and cost features.

Formula 4-22, which is the model for valuing futures and forwards on assets not paying any income and not having any storage cost, thus is based on the value of the asset in the spot market and the interest that could be earned on the equivalent cash amount in the money market at the risk-free rate.

4.2.3.2 Valuing Forwards and Futures of Financial Assets with Income or Storage Costs

Some assets (e.g., certain equities) actually pay a known or expected income over the period of the forward or future. Other assets such as oil or other commodities will require storage at a known cost. In both cases we will need to extend our valuation model to account for the cost. If the asset receives some income between the start of the forward and the time delivery takes place then we need to subtract the appropriately discounted income from the plain forward price since the income reduces the funding costs for the provider of the forward. If the asset requires the holder to pay expenses for storage, the appropriately discounted expenses need to be added to the plain forward price since the expenses add to the funding costs for the provider of the forward. Formula 4-23 shows the extended forward valuation model that includes both an adjustment for income received and expenses paid. Figure 4.14 illustrates the building block structure of a forward contract with income and costs.

Formula 4-23: Value of a Forward or Future of a security with income and/or costs

where:

- VForward: theoretical value of the forward or future contract

- VSpot: value of the same position in the instrument in the spot market

- T: time to maturity of the contract of years

- r: market interest rate assuming annual compounding

- rd: r * period_between_income_payments_in_year_fractions

- re: r * period_between_expense_payments_in_year_fractions

- dt: income from asset in period t for any t in between 1 … n

- et: income from asset in period t for any t in between 1 … m

- t: time index terms of no periods for either income (dt) or expenses (et)

- n: number of income payments from start to end of the contract

- m: number of expense payments from start to end of the contract

4.2.4 Valuing Options

If we wanted to value a call option, that is the right but not obligation to buy some given equity shares (e.g., shares for Marks & Spencer Plc, Daimler AG or General Motors) at a pre-agreed price at some future date we can use our Black & Scholes option valuation tool from Formula 4-16, introduced earlier in the chapter.

In order to get accustomed to the various valuation methods presented so far, please work through the following exercise on the companion web site of the book.

Lab Exercise 4.6: Financial Instrument Valuation Examples

- 1. Open the file FinInstValutions.R from the set of sample files from the companion web site for this book (http://modelbook.bancstreet.com/) and explore the R code illustrating the valuation calculations shown above.

- 2. Using the R application load the file FinInstValutions.R and run the following examples at the command prompt in your R GUI:

R> InitialiseFinInstValuations()

…

R> RunFinInstValuations ()

…

R> FinInstValuationsReports()

4.3 Valuing Real Assets

Not all assets that we may have in a portfolio will be financial instruments like tradable securities, derivatives or over-the-counter (OTC) derivatives contracts of account-based loan or deposit-based products. Sometimes we may well need to value such entities as an entire business, a real estate property, or some large project asset like a new power utility or a very large innovative new ship. Although each of those are clearly different from financial instruments we can again use our tools to price them.

4.3.1 Valuing a Business

To value a business we can again use our equity valuation tools introduced earlier. Formula 4-24 is an adaptation of the model from Formula 4-20. In this case however we will have to use the weighted average cost of capital.

Formula 4-24: Two-stage cash flow based business valuation

where:

- VBusiness: value of the business

- dt: cash flows for the business in year t

- t: index of year in the first 1 to t years (i.e., 1 in first year, 2 in second year, etc., and n in the final year where t = n)

- r: market interest rate appropriate for discounting the stream of expected cash flows from the business

- glongterm: estimated steady sustainable growth of the stream of cash flows

- dn+1: expected cash flows from the business in the year after year t

- Vlongterm: = dn+1/(r − glongterm)

Formula 4-15, introduced earlier, provides a method for calculating the weighted average cost of capital using the cost of equity and debt as well the total values for outstanding equity and debt capital. We need to use this formula to calculate the correct cost of capital to use for discounting, taking into account any debt funding the business may use in addition to the equity that may have been invested.

Formula 4-15: Weighted average cost of capital (WACC)

where:

- CWACC: weighted average cost of capital

- CEquity: cost of equity

- CDebt: cost of debt

- E: total value of equity issued by the firm

- D: total value of debt issued by the firm

- [E/(E + D)]: proportion of equity issued by the firm to total of all capital

- [D/(E + D)]: proportion of debt issued by the firm to total of all capital

4.3.2 Valuing Real Estate Property

In cases where we want to value some real estate property, we can again use the method we just introduced for the valuation of businesses. Some more complex properties may have additional complex features such as options to sell or to buy more units from a multiunit development. Instead of needing a completely new valuation approach though, we can again just value the additional features using other tools such as option valuation and then add the different partial valuations together.

4.3.3 Valuing Large Projects: Ships, Utilities, and More

Sometimes, such as in the case of certain utilities projects of new innovative large ships to be built, it may be better not to use a tool like the business valuation method introduced in Formula 4-24. Instead it may be better to use an alternative, more sophisticated option valuation approach that allows us to capture the value from the optionality such projects entail better than a business/equity valuation approach. In the case of an innovative large new ship, the building and commissioning process may take some years while the future revenues, which because of this time lag are still in the relatively distant future, will depend very heavily on the evolution of markets in the future. The ship building project can thus be seen as a call option on the future business that may result from owning such a ship. Such real options are a good illustration that selecting the right valuation model and thus an appropriate way of representing an instrument’s financial characteristics should be done with great care. In some cases you even have several such models in parallel for an instrument so that you can compare them.

Before concluding this chapter you may find it useful to work through Lab Exercise 4.7, which will allow you to explore some of the aspects of the implementation of the previous approaches for valuing real assets in more detail.

Lab Exercise 4.7: Real Asset Valuation Examples

- 1. Open the file RealAssetValutions.R from the set of sample files from the companion web site for this book (http://modelbook.bancstreet.com/) and explore the R code illustrating the valuation calculations shown above.

- 2. Using the R application load the file RealAssetValutions.R and run the following examples at the command prompt in your R GUI:

R> InitialiseRealAssetValuations()

…

R> RunRealAssetValuations ()

…

R> RealAssetReports()

1See Damodaran (2002) for a detailed discussion of equity valuation methods.

2See Black and Scholes (1973) as well as Merton (1973).