Three. A Volatile Reality

Is it time to adjust your sails?

Back when commercial air travel was still in its infancy and largely relegated to those who could afford it, steamship was the only option for many travelers. Few things were more miserable than falling ill at sea, especially if it was day one of a seven day voyage. Relief came in 1949, when dimenhydrinate, now widely marketed as Dramamine®, was introduced to the market.29 For some travelers, this little pill (or patch) does wonders for helping to manage the nausea that accompanies high swells and angry seas. Just as a cruise ship unexpectedly encounters rough waters, the value of a portfolio can also experience sudden dips and dives that may leave investors queasy and ready for land. Yet, if you abandon ship at the first port you see, chances are you’ll never reach your final destination.

29 Encyclopedia Britannica, “Dimenhydrinate,” 2013.

While there is no known treatment to calm the nausea, anxiety, and other side effects involved with investing in a turbulent market, I believe alternatives can help, even though, as always, there are no assurances that they will. Let’s face it; no one can control the ups and downs of the market, but when used in tandem with traditional investments, alternatives can help manage the volatility inside your portfolio, thereby reducing the spinning and dizziness you might feel and providing the needed confidence to finish the journey.

Motion Sickness: Markets Are Increasingly Cyclical

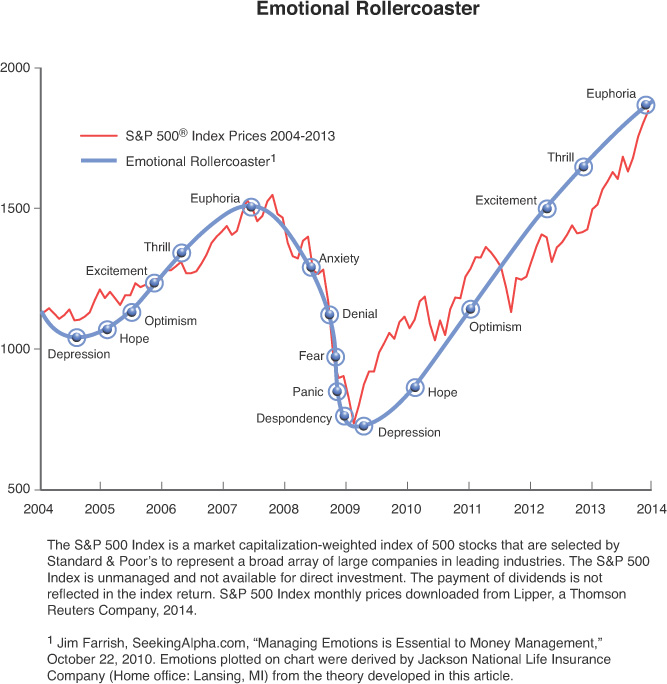

An office staple of many financial professionals during the nearly 20-year bull market from 1982 to 2000 was the S&P 500® chart detailing the rise of equities over the previous 70 years. Often prominently displayed as one would hang posters of fast cars and sports icons, it made for a colorful visual that framed nicely and illustrated that over time, despite fluctuations, markets trend up. That is, until one day they didn’t.

After the tech implosion at the beginning of the 2000, the S&P briefly wobbled and seemed to recover, only to find near catastrophic turbulence in 2008. From the perspective of a typical investor, experiencing the euphoria of a bull market and the despair of a bear market can feel like a ride on the proverbial emotional rollercoaster, as shown in Figure 3.1.

In the years since, the unpredictability of the market has continued. It used to behave in secular patterns (meaning over a long period of time) and could be fairly relied upon to allow for insight and planning. Today, it seems that cyclical volatility (or volatility occurring over a short period of time) is increasingly the norm. Since 2000, the adjective “rising” had been replaced by “sideways and volatile” when discussing market performance.

One index in particular is receiving an increase in scrutiny because of this increase in volatility. The Chicago Board Options Exchange (CBOE) Volatility Index®, or the VIX®, takes the average volatility for the Standard and Poor’s 100 Index, which deals with futures (a contract to buy an asset at a predetermined price and future date), and uses it to measure the volatility of the overall market. A low VIX indicates investor confidence, while a high VIX indicates investor concern (some would say fear). For this reason it is informally referred to as the “fear index.” Typically, a level of 30 or higher signals a great deal of volatility.30 The VIX has reached a low of just below 10, while it hit almost 90 during the peak of the financial crisis in 2008. The long-term VIX average has been somewhere between 20 and 22.31

30 Investopedia, “CBOE - VIX,” 2013.

31 Macroption.com, “VIX Chart,” 2013.

In the interest of examining history, I would argue that the roots of this volatility go back more than 30 years. There are several factors to consider in order to fully understand the unpredictability of a cyclical market. First, the secular decline of interest rates over the past three decades has had a significant influence on the U.S. economy and capital markets. If the economy dipped toward, or into, recession, the U.S. Federal Reserve, which controls short-term interest rates, would cut rates to spur a refinancing cycle and thus encourage economic activity.

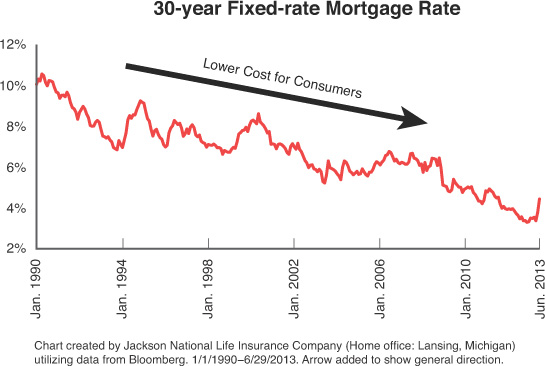

As interest rates moved lower, consumers gained access to cheaper capital. The ability to refinance mortgages at lower rates every few years, for example, allowed individuals to reduce one of their most significant costs—that of their home. With data going back to the early 1990s, the average 30-year mortgage rate (as measured by Freddie Mac’s Primary Mortgage Market Survey available on Freddie Mac’s website and on Bloomberg) has gone from over 10% in the early 1990s to just above 4% by the end of the second quarter of 201332 (see Figure 3.2). This provided consumers with more disposable income to spend on other wants and needs.

32 Bloomberg, “30-Year Fixed Rate Mortgage Index,” January 1990–June 2013.

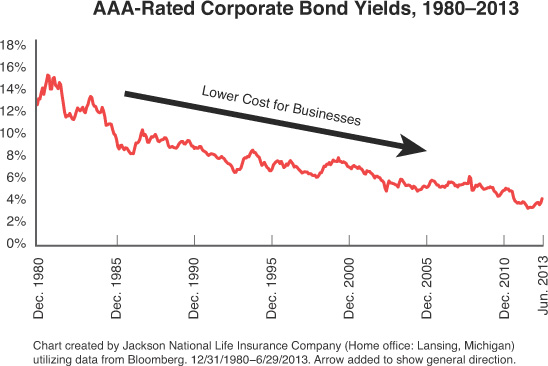

Business managers also enjoyed access to cheaper capital. Like homeowners, businesses were able to refinance their own debt or loan obligations at lower rates every few years, reducing their interest expense while increasing profits and helping to spur economic growth. Businesses have also been able to borrow at cheaper and cheaper costs, helping to expand their operations. The chart in Figure 3.3 shows the average yield of AAA-rated corporate bonds over the last 30 (plus) years. During this time period, their average yield for the highest-rated corporate bonds has dropped from a high of about 15.5% to around 4.3% at the end of the second quarter of 2013, using Moody’s Seasoned Aaa Corporate Bond Yield Index.33 Due in part to the lowering of interest rates during the 20-year period between 1980 and 2000, the U.S. real gross domestic product (GDP) grew around 2.83% on average per year.34

33 Bloomberg, “AAA-Rated Corporate Bond Yields,” December 1990–June 2013.

34 Bloomberg, “GDP Index,” February 1980–December 2001.

Conversely, lower interest rates meant lower income from bonds available from the government. During this period of stock market growth, the 10-year U.S. Treasury yield went from its peak near 16% in 1981 to around 5% by the end of 2000.35 In July 2012, the yield fell to a historic low of 1.47%. Now, however, lower interest rates seem to be losing their stimulus effect on the overall economy. In the years since 2001, the GDP has grown at a muted 1.75% average yearly rate.36 Interest rates hit bottom, largely remained there since the economic crisis, and are now beginning to turn. As a result, the Fed is much more limited in how, and how much, it can stimulate the economy through refinancing. I believe this could result in more pronounced economic cycles, which in turn could influence a continued cyclical stock market pattern.

35 Bloomberg, “10-year U.S, Treasury Yield,” December 1980–June 2013.

36 Bloomberg, “GDP Index,” March 2001–April 2013.

This means if the seismic trends experienced since 2008 continue, there could be more risk for a given level of return. And that, in turn, means a new approach may be needed to help manage that volatility. Unfortunately, too many people forget their Dramamine. Perhaps, they feel they can ride out whatever may come or, worse yet, they don’t even know they’re prone to seasickness. And so it is with their investments—they believe they can handle market volatility with traditional allocations, and may not even realize other options are available.

Investor Shock: When Fear Leads to Missed Opportunities

Undoubtedly, many investors were shell shocked when the stock market crashed in 2008; their investment portfolios took a significant hit and some thought it would be better to “cash out.” But increased volatility means markets can quickly turn. If you’re “on the sidelines” when that turn occurs, you could miss the eventual rally. For example, in 2009, despite many cyclical trends, the market appeared to generally move upwards. As a result, those who sold their investments missed an opportunity to regain some of what was lost.37 To compound the problem, those investors who reentered the market largely did so by investing in fixed income assets such as bonds.38

37 Rebecca Lipman, Kapitall Wire, “Rallying Stocks: Will Small Investors Miss Out on the Rally, Again?,” November 2011; Steven Reiff, Advisor Today, “Preparing Clients for New Market Realities,” July/August 2012.

38 Daniel Wagner, Yahoo Finance, “Bonds Retain Appeal, Despite Rock-Bottom Yields,” August, 2012.

I know of investors who relied on the standard 60/40 equities-to-fixed income split before the crisis who subsequently retreated to cash when the market crashed. These investors then flipped the ratio, significantly increasing their allocations to bonds, which in turn helped to drive bond yields (the potential returns generated) significantly lower. Money continued to pour into taxable bond funds until mid-2013, despite low interest rates and yields. The irony was that people were willing to invest in something that would earn them relatively lower returns while, maybe unknowingly, exposing themselves to the risk that inflation would outpace their growth. The possibility of rising interest rates means fixed income vehicles are no longer as popular as they once were. Yet even though investors have materially changed their view of investing post crisis, I think it’s the wrong view—especially if interest rates continue to rise.

Why? Many consumers might still retain the perception that their portfolios, allocated across a narrow spectrum of assets, will earn between 5% and 9% annually, something they might have experienced in earlier bull markets.39 However, traditional fixed-income investments are susceptible to the pressures of increasing interest rates and inflation (yields have been historically low for the last few years,40 which means investors are locking in low investment returns). And because the bond market has an inverse relationship with interest rates (low rates mean high prices, high rates mean low prices), the client’s portfolio, heavy with fixed income allocations, may grow too slowly or be subject to increased bond market volatility. This could therefore cause the portfolio to be worth less at a time when principal and purchasing power is needed most—like, say, retirement. The point is that portfolio values increase and decrease over the life of the accumulation phase, but might be worth less at the exact moment investors need to begin withdrawing assets.

39 Joseph Davis and Daniel Piquet, Vanguard Research, “Recessions and Balanced Portfolio Returns,” October 2011.

40 Federal Reserve, downloaded on 7/22/2013.

The goal of a retirement plan is to help investors accumulate enough assets during their working years to cover daily living expenses and any unexpected events that might arise in retirement, without severely depleting their savings. The importance of picking a broadly diversified investment allocation that fits with the investor’s long-term needs can, therefore, not be overemphasized.

New Prescription: Rethink Buy-and-Hold

With so many factors now influencing a company’s stock performance—especially in our increasingly globalized world—the days of relying on buy-and-hold investing, quite simply, may be days gone by. We’ve seen many once seemingly invincible companies fold due to unexpected (and unprepared for) circumstances. It was never a good idea to remain invested in a company over time simply for the sake of buy and hold. Today such strategies are especially dangerous. Here’s an example of why:

Let’s assume an analytical person, one who enjoys studying the underlying financials of companies and in-depth sector research, decides to buy Apple based upon its strong consumer brand. It’s a traditional investment approach that relies completely on the financial fundamentals of a company, and one that until recently made sense. Today, however, it’s just one aspect of a complex overall investment construct. Economic conditions that affect large markets such as China and Europe would certainly affect Apple’s success. Apple employs many manufacturing workers through subsidiaries and sells many phones in China, so any increase or decrease in demand would affect the company’s financial performance and, consequently, share price. In Europe, the sovereign debt crisis that recently spread throughout the continent increased the likelihood that financial institutions could face widespread write-downs, which would negatively affect shareholder returns.41 This, in turn, increased the risk that the crisis would spread to markets in other parts of the world.42 With all there is of which to keep track, how could the average investor possibly expect to sift through such macroeconomic information to determine the right time to buy or sell their individual Apple stock?

41 Matthew Curtin, The Wall Street Journal, “Firms Brace for Write-Downs,” January 2013.

42 Katie Martin and Jonathan House, The Wall Street Journal, “Contagion Returns,” February 2013.

Is It Time to See a Specialist? The Role of Proper Diversification

The result is that in today’s world, it can be tough for individual investors to digest the incredible amount of information needed to make decisions about their portfolio. Institutions and endowments employ experts to strategically use alternative investments (among other types of investments) for the express purpose of capitalizing on, or managing, the effects of the types of scenarios described above. These strategies enable them to enjoy a broader range of diversification.43 As I mentioned in the first chapter, since the downturn, endowment returns have been mixed. For their fiscal year that ended June 2012, endowment returns lagged those found in a traditional 60% equity/40% fixed income portfolio. However, for their fiscal year that ended June 2013, while allocations to alternatives decreased to 47%, endowment returns were strong. As I mentioned, there was a reduction in alt exposure, from 54% to 47% on average, for endowments. However, there is no indication that this tactical tweak means that alts are losing favor with endowments.44

43 James B. Stewart, The Wall Street Journal, “University Endowments Face a Hard Landing,” October 2012.

44 Tim Sturrock, FundFire, “Endowment Returns Strong, Alts Allocations Drop,” November 7, 2013.

However, although an option to enhancing diversification, the alternative space is unknown to many investors, and diversification does not assure a profit or protect against a loss in a declining market. Portfolios that have a greater percentage of alternatives may have great risks, especially those including arbitrage, currency, leveraging, and commodities. This additional risk can offset the benefit of diversification. As such, one consideration might be to purchase investment products that are managed by high-level experts with specialized skill sets that employ components of both fundamental and technical analysis, as well as risk management vehicles and procedures.

Radical Idea: Do Something Different

Previous generations utilized newspapers as their primary information source, yet the increased transparency and on-demand availability of information are two more components I think play a critical role in cyclical volatility. With new technological advances (cable news, GoogleTM, financial blogs) facilitating the flow of information, investors now have the opportunity to react quickly to a given event, but not always in the most rational manner. This can, in turn, create even more volatility. As a result, the sheer volume of financial tools and information available today has greatly increased the speed with which high-volume trades can be executed. This is just one more catalyst for increasing volatility, and consequently, the increasing need for investors to do something different.

From the Alt Vault: Valuable Takeaways from Chapter Three

A new strategy is needed to help weather the highly volatile markets experienced in recent years. Alts may do this either by helping to reduce volatility in the individual portfolio or, where appropriate, attempting to use volatility as an advantage.

![]() Markets are increasingly cyclical.

Markets are increasingly cyclical.

![]() Too many investors missed the post-2008 rebound, unsure of how—or when—to get back in.

Too many investors missed the post-2008 rebound, unsure of how—or when—to get back in.

![]() The days of relying on buy-and-hold investing may be days gone by.

The days of relying on buy-and-hold investing may be days gone by.

![]() Proper diversification is important in a strategic plan.

Proper diversification is important in a strategic plan.

![]() With a smart strategy, investors (along with their financial professionals) can learn to use volatility to their advantage.

With a smart strategy, investors (along with their financial professionals) can learn to use volatility to their advantage.

What’s next: Globalization means markets are increasingly interconnected—and prone to volatility. A hiccup in a far-away land can cause major disruptions in the average investor’s portfolio. If you think you’re immune, think again. How can alternatives help?