Four. It’s a Smaller World After All

Can a New Yorker get sick if someone sneezes in China?

In our interconnected world, an epidemic can become a pandemic as the result of a simple sneeze.45 Witness the panic surrounding the Severe Acute Respiratory Syndrome (SARS) epidemic of 2003. More than 700 of the 8,000 people who became infected died.46 Even though actions by the Center for Disease Control likely prevented the disease from spreading to more parts of the world, global media perpetuated greater panic than was likely warranted. Concern over the disease disrupted international trade and travel, severely impacted tourism, and forced the cancellation of mass events. The Rolling Stones famously postponed a weekend set of stadium concerts in Hong Kong over fears of spreading the virus.

45 T. Déirdre Hollingsworth, Neil M. Ferguson, Roy M. Anderson, U.S. National Library of Medicine, “Frequent Travelers and Rate of Spread of Epidemics,” September 2007.

46 Center for Disease Control, “SARS—Basic Facts,” July 2012.

Such talk of contagions also applies to markets and investing. A ready metaphor involves the wave of bank failures and currency devaluations that swept across Asia just five years before the SARS outbreak. Aptly referred to as the Asian Flu, it began when Thailand, Indonesia, and South Korea fueled their country’s economic growth with capital borrowed in U.S. dollars. These currencies soon fell dramatically in value when their link with the dollar proved unsustainable. As a result, the debt of many Asian companies became so expensive that their governments came close to bankruptcy.47

47 BBC News, “Catching the ‘Asian Flu,’” June 1998.

BBC News reported at the time that “...world markets are now so interlinked that a recession in one part of the world quickly affects trade in all regions. And because financial markets are even more closely tied together by global electronic trading, a crisis in confidence in one market will quickly be transmitted to others.”48

48 Ibid.

As the Asian financial crisis was unfolding, an American investment firm experienced a contagion threat of its own. On September 23, 1998, the Federal Reserve of New York reached an agreement with 14 financial banks to recapitalize Long-Term Capital Management, a Greenwich, Connecticut based hedge fund, in which the banks would provide the firm with emergency funds. The announcement capped a trying year for Long-Term Capital, which employed sophisticated strategies for high-net-worth investors and counted two Nobel Laureates, Myron Scholes and Robert Merton, as principals. In the late 1990s, the firm made investments in derivatives. They bet wrong, the markets turned, and the firm teetered on the edge of collapse. Because of the large amount of money involved and the co-mingling of global markets, the president of the Federal Reserve Bank of New York feared a global pandemic if the firm was to go under and therefore began recapitalization efforts with the help of European and domestic banks.49 Of course, these events were just a hint of what was to come with other venerable Wall Street firms a decade later.

49 Roger Lowenstein, New York Times, “Long-Term Capital Management: It’s a Short-term Memory,” September 2008; Kimberly Amadeco, About.com, “What Was the Long-Term Capital Management Hedge Fund and the LTCM Crisis?” January 2012.

Booster Shot: Globalization Begins

This modern concept of globalization began with the Bretton Woods monetary system, named for the conference held by the Allied Nations in the New Hampshire wilderness in the waning days of the Second World War. It featured liberalization measures that set exchange rates between countries and oversaw creation of both the International Monetary Fund, as well as a precursor to what today is the World Bank.50 This new era of global economic cooperation is one reason world trade has grown by an average of 6% per year, every year since World War II reconstruction began (with a few exceptions).51

50 The Levin Institute, The State University of New York, “International Monetary Fund and World Bank,” 2013.

51 World Trade Organization, “Growth, Jobs, Development, and Better International Relations, How Trade and the Multilateral Trading System Help,” 2013.

One result of modern globalization is a corresponding acceleration of the wide availability of communication and information technology. This communication revolution has led to greater micro-level efficiencies. For instance, financial professionals can now instantly collect and evaluate data on everything from foreign markets to economic trends in other countries without having to travel overseas.

As this capability in communication has evolved, so has financial trading technology. For the first part of the 20th century, chalkboards, newspapers, and tickertape dominated financial communication. In 1960, the first Quotron system was developed, which employed magnetic tape and allowed brokers to retrieve stock prices from keyboards at their desks.52 The introduction of personal computers in the 1980s ushered in an era of on-demand information and real-time quotes, something that continues to evolve with the Internet and now mobile devices.53 I often say that one person with an iPad is probably more efficient than the output of an entire Wall Street office in the 1970s and 1980s. Tablet trading applications and online platforms provide real-time results, meaning that due to the increase in global dependency across time zones, trading never stops. However, it’s a double-edged sword. Technology may build efficiencies through interconnections and integration, but it also builds interdependencies—making it easier for a contagion to spread.

52 Roy S. Freedman, Elsevier Inc., “Introduction to Financial Technology,” 2006.

53 Moss Strohem, eHow, “Software for Technical Analysis of Stocks,” 2013.

For an illustration of how this interconnectedness increasingly fuels market growth and collapse, consider what happened with credit default swaps during the worldwide credit bubble of the last decade. Famously tagged as financial “weapons of mass destruction” 54 by legendary investor Warren Buffet, a credit default swap transfers the default risk from the security owner to swap seller.55

54 Cate Long, Reuters, “Column: Warren Buffett’s Municipal Weapons of Mass Destruction,” August 2012.

55 Investopedia, “Credit Default Swap—CDS,” 2013.

The underlying global credit default swap market size at the end of 2001 was $918 billion. By the end of 2007, investors had purchased swaps on underlying assets worth $62.3 trillion—a stratospheric 6,686% increase in just six years.56 But eventually the housing bubble and credit crisis grew too big, popped in 2007, and started to wind down in 2009.57 Credit default swaps are complex, and a detailed description of what they are and how they work could easily be the subject of another book entirely. Because they’re so complex, the vast majority of retail investors would not hold swaps within their portfolio. But they provide a good illustration of how quickly bubbles can inflate and deflate, and how conditions in seemingly unrelated financial markets and countries across the globe can wreak havoc in the average investor’s portfolio.

56 Reuters, “How the Credit Default Swaps Market Works,” October 15, 2008.

57 Investopedia, “Market Crashes: Housing Bubble and Credit Crisis (2007–2009),” 2013.

Immune System Breakdown: Volatility Reaches Fever Pitch

As a more recent example, on May 6, 2010, the Dow Jones Industrial Average lost almost 1,000 points in intraday trading in a period of 20 minutes, temporarily wiping out $1 trillion in market value.58 What became known as the “flash crash” had never been seen before and was attributed to the activity of high-frequency traders and the rapid, electronic execution of trades.

58 Reena Aggarwal, Center for Financial Markets and Policy, Georgetown University, “The Growth of Global ETFs and Regulatory Challenges,” January 2012.

If only this was an isolated incident. In August of 2012, the market experienced a “flash crash” when a software glitch caused the prices of 150 companies to suddenly spike. The hiccup occurred in the market-making unit of Knight Capital when a technical problem affected how trade orders were routed. The next day the company projected it would lose $440 million and within two days Knight Capital’s stock value plummeted by 75%.59 Barely a year later, in another incident, on August 22, 2013, trading on the NASDAQ, which includes companies such as Microsoft and Intel, shut down for three hours due to what officials at the exchange called a “technical glitch.”60

59 Maureen Farrell, CNN Money, “Knight Capital Surges 60% as Trades Return,” August, 2012.

60 Washington Post, “Nasdaq Resumes Trading After Technical Glitch,” August 22, 2013.

The reality is that the investment world today is heavily dependent on information and the rapid flow of data. Technology is making our financial world smaller, and when someone sneezes, more and more people are likely to catch colds. Before 2008, many investors thought they were well diversified by holding international stocks, emerging markets, high-yield bonds, and real estate in addition to more traditional equities. However, over time, correlation rose between these types of investments and the S&P 500, and investors were not as well diversified as they were before. The overall rise in correlation of traditional investments, something that made the 2008 economic crisis devastating to so many investors, can now quickly spread throughout the globe.

So why then would an investor even want to invest internationally?

Modern Medicine: Combating Home Country Bias

If one studies the allocation of the average investor, their assets are overwhelmingly located within the country they reside. To put it plainly, Americans buy American stocks. Known as “home country bias,” American investors had over 70% of their equity investments in U.S. domestic stocks as of 2012.61 While growth in emerging and developing economies has recently slowed, they are still predicted to grow at a rate of 5.1% in 2014, compared to a growth of 2.0% in advanced economies, and 3.6% for the world overall.62 With the wide availability of domestic asset management companies (mutual fund and ETF managers, for instance) that offer international investment opportunities in various regions of the world, the practice of home country bias may be unsound. Just as it makes little sense to concentrate a portfolio in one company’s stock, it makes little sense to concentrate a portfolio in one industry, sector, and yes, country. Of course, international investing does not come without risks, such as exposure to potentially adverse local political and economic developments; nationalization and exchange controls; potentially lower liquidity and higher volatility; possible problems arising from accounting, disclosure, settlement, and regulatory practices that differ from U.S. standards; and the chance that fluctuations in foreign rates will decrease the investment’s value.

61 International Monetary Fund’s Coordinated Portfolio Investment Survey (2012), International Monetary Fund’s Coordinated Direct Investment Survey (2012). MSCI Data as of 12/31/2012. Notes: The IMF’s Coordinated Portfolio Investment Survey and Coordinated Direct Investment Survey were used in conjunction with market-cap information to determine domestic and foreign investment. The MSCI USA (IMI) was used to represent the United States equity market portfolio.

62 Rupa Duttagupta and Thomas Helbing, International Monetary Fund, “World Economic Outlook: Global Growth, Patterns Shifting, Says IMF WEO,” October 8, 2013.

Even with all of the above, international allocations can still act as a further diversification63 tool. A truly global investor learns to recognize there are segments within the global marketplace that are priced attractively at any given time. As such, they are not concerned about pulling back to American shores simply due to one crisis in one particular area of the world. A well-thought-out investment strategy takes into consideration opportunity at every point within an economic cycle and recognizes the importance of seeking opportunity globally in addition to the investor’s geographic base.

63 Diversification does not assure a profit or protect against loss in a declining market.

To put it more plainly, although globalization led to an increased risk of “catching a cold,” secluding oneself at home may not be the cure, especially if you live with others that act as carriers.

Second Opinion: The Best Advisors Seek the Counsel of Their Peers

A global investment strategy calls for a measured approach, one that is executed with the help of one, or a number, of investment professionals. The investing climate has become so crowded with different strategies and opportunities that, increasingly, even investment professionals are seeking the counsel of their peers in finding hidden potential. According to the old adage, “even the doctor needs to see a doctor,” and we all know that someone who represents themselves in a legal matter “has a fool for a client.” Consequently, financial and investment opportunities may exist where one may not have thought and may be uncovered with the help of those with a particular expertise in one sector or geographic area of the globe.

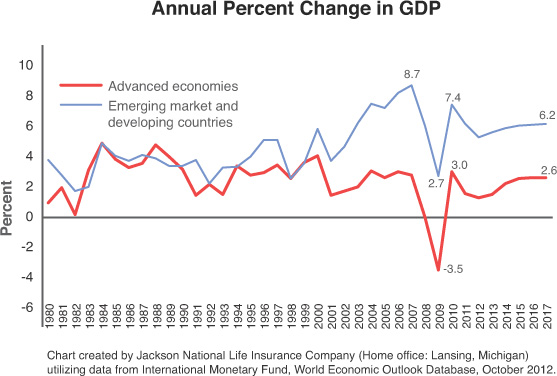

For instance, some emerging market countries were not as affected by the global financial meltdown of 2008 and had better fiscal balance sheets with their government debt than many developed nations.64 In fact, as evident from Figure 4.1, while the average GDP for emerging market and developing economies fell in 2008, it remained positive at 2.7 compared to negative GDP in advanced economies at -3.5. As a result, when the dust settled, investors realized emerging markets had differing growth rates.65 Yet the news comes fast and often; by mid-2013, emerging markets were back on their heels, hit hard by rising inflation, sliding currencies in many others, and a slowdown in Chinese economic growth.66

64 Maureen Nevin Duffy, Oxstone Investment Club, “ETFs Provide Exposure to Emerging Markets Growth and Risk,” April 2012.

65 Thomas Kenny, About.com, “Investing in Emerging Market Corporate Bonds: The Next Frontier,” 2013.

66 Tom Lydon, ETFTrends.com, “Emerging Markets ‘Triple Threat’ Could Hurt These ETFs,” August 21, 2013.

Many markets in the developed world were just as volatile, yet despite the barrage of headlines in recent years, not all countries in Europe are the hopeless cases the press would have you believe. In fact, in 2012, European banks restructured and, in some cases, were forced to deleverage by selling distressed assets at reduced prices67 (similar to what happened with U.S. banks in 2008). Sophisticated investors and money managers took advantage of these deleveraging requirements by making strategic trades in those distressed assets. As an example, a number of hedge funds bought new, distressed asset offerings from the banking sector,68 believing their quick infusions of capital would be rewarded.

67 Anne-Sylvaine Chassany, Bloomberg, “Europe Banks Fail to Cut as Draghi Loans Defer Deleverage,” September 2012.

68 Bob Parker, Seeking Alpha, “Bank Deleveraging, Opportunities Expected But No Gold Rush,” August 2012.

Beyond Europe, many other countries appeared (and are still appearing) in global investment discussions. The Brazilian bond market that was once hot quickly cooled.69 Middle Eastern markets looked attractive in 2012 relative to their past performance.70

69 Rob Dwyer, Euromoney, “Debt Capital Markets: Brazil DCM is No Longer a Darling Abroad,” October 2012.

70 Rabah Arezki and Mustapha K. Nabli, IMF Working Paper, “Natural Resources, Volatility, and Inclusive Growth: Perspectives from the Middle East and North Africa,” April 2012.

Fatal Mistake: Do Nothing

Regardless of how investors feel about the issue of globalization, access to money managers with specialized investment expertise in sectors and geographic locations are now available, but most individuals have yet to take advantage. A “do-it-yourselfer” faces the task of gathering and understanding all of the information available to appropriately manage such a wide array of potential options. It was a difficult task with traditional, long-only investments—even more so now with the advent of non-correlated and counter-correlated investments.

For example, if someone was looking to invest in real estate in China, they could probably find someone in New York to help. But wouldn’t it be better to partner with someone on the ground, who knows the culture, people, and politics of the world’s largest developing market? These “partners” are now increasingly available to the average retail investor.

It’s tempting to throw up your hands in surrender and bury your head, but to do nothing can be harmful. The increasingly longer life spans discussed in the first chapter, and the issues they bring, mean investors who sit it out are sitting still. Investment professionals are available to help, but one must be prudent in their choice of whom to hire. How is this done? How does one go about allocating money and assets across investments? Questions we will now discuss.

From the Alt Vault: Valuable Takeaways from Chapter Four

Is the cure worse than the cold? Globalization has brought the world closer together, and investing in once-overlooked, far-off lands may help provide sought after diversification. However, faster communication means quicker real-time adjustments, and often more volatility. The key is acting on the former while managing the latter. Experienced financial professionals can help.

![]() Our globalized, hyper-connected world can affect the investor’s portfolio.

Our globalized, hyper-connected world can affect the investor’s portfolio.

![]() Advances in technology and increased availability of on-demand information may have contributed to the correlation of traditional investments—investors can now make instant adjustments to their portfolio in response to breaking news from around the globe.

Advances in technology and increased availability of on-demand information may have contributed to the correlation of traditional investments—investors can now make instant adjustments to their portfolio in response to breaking news from around the globe.

![]() Diversification is often hampered by “home country bias” or investing in what we know.

Diversification is often hampered by “home country bias” or investing in what we know.

![]() If your portfolio has problems, doing nothing won’t solve them.

If your portfolio has problems, doing nothing won’t solve them.

What’s next: Too often, investors have no one but themselves to blame. Bad behavior and a lack of proper investment “nutrition” conspire with global factors to negatively affect portfolio health. How can these bad behaviors be identified and overcome?