Six. Exploring the Alternative Universe

Where does the rubber meet the road?

Goodyear Tire and Rubber Co. is best known for its brand of tires (as well as the dirigible blimp that bears its name). However, the company undertakes research and development in lesser known, but I think equally important, areas that intersect business and science. In 1971, Goodyear worked with NASA to develop a new tire that could withstand the treacherous conditions on Mars. The result was a new material that was stronger than steel. Recognizing the increased durability of the material, Goodyear engineers introduced the technology in its consumer-based business and went on to produce a new radial tire with a tread life expected to be 16,000 kilometers (approximately 10,000 miles) longer than conventional radial tires.81 More recently Goodyear again partnered with NASA to develop an energy efficient, airless “Spring Tire” for further exploration both in space and on Earth.82

81 Peter Nowak, MSN Tech & Gadgets, “10 Surprising NASA Inventions: Stronger Tires,” 2013.

82 AutoBlog, “Goodyear ‘Spring Tire’ Engineered to Withstand the Harshest Environments on the Moon and Possibly the Toughest Places on Earth,” March 2012.

Flight Plan: Collaborate to Win

NASA was involved in the design and development of something that Goodyear eventually marketed to consumers. Likewise, I’ve observed that many financial services companies have taken the portfolio model designs developed by institutional investors and used them to create similar products for their retail investors. Investment banks, brokerage firms, mutual fund companies, insurance companies, endowment funds, pension funds, and hedge funds are all examples of institutional investors.

For example, David Swensen, chief investment officer at Yale University, is famous in the investment world for his exploration of new strategies. It’s no simple task, but one that I would assume has been key to the well-being of the funds he’s charged with overseeing. After all, he is responsible for managing and investing Yale’s endowment, worth more than $18 billion as of October 2012.83

83 Yale University, About Yale, “Chief Investment Officer David Frederick Swensen,” 2012.

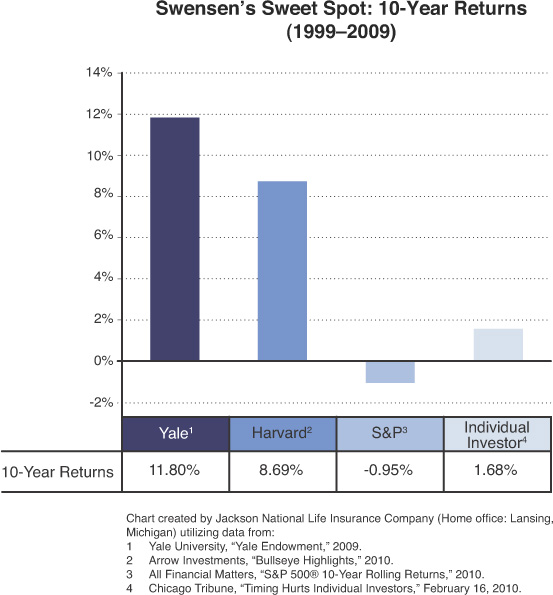

In Figure 6.1, “Swenson’s Sweet Spot: 10-Year Returns,” you see Swensen’s historical average annual return was 11.8% over the 10-year period from 1999 to 2009 on his investments.84 This historical period is significant because it encompasses a major portion of the economic downturn in 2008. During the same time, the broader S&P 500 Index returned less than 1%.85 Swensen’s consistent track record has the attention of top Wall Street money managers, all wondering how he does it. His consistency is one reason he’s held his position with Yale for almost three decades.86

84 Seeking Alpha, “Top Investor Swensen Has High Conviction in These 3 Companies,” March 22, 2012.

85 Lipper, a Thomson Reuters Company, May 2013.

86 Seeking Alpha, “Top Investor Swensen Has High Conviction in These 3 Companies,” March 22, 2012.

Swensen applies a variation of Modern Portfolio Theory (discussed in Chapter One) which attempts to increase returns for any given level of risk. He revised this theory in his groundbreaking book, Pioneering Portfolio Management.

Swensen developed this variation with Dean Takahashi. The method, once given the nickname “The Yale Model,” is now commonly known as “The Endowment Model” as many other funds have attempted to replicate Swensen’s success. This model is characterized by heavy allocations to different asset classes when compared with conventional portfolios. It consists broadly of dividing a portfolio into seven or eight parts and dividing the money amongst different investment categories, which roll up to five asset classes.87

87 Yale University, “2012: The Yale Endowment,” 2012.

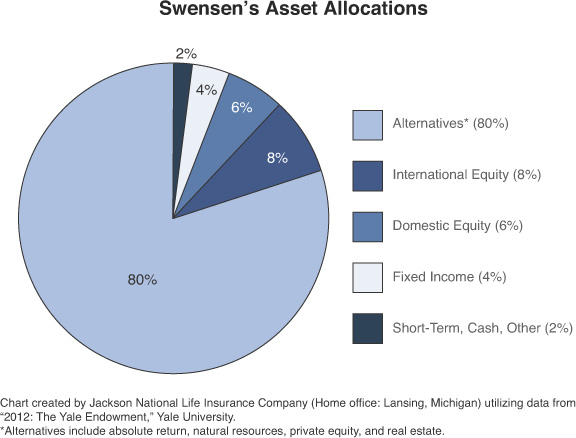

As shown in the “Swensen’s Asset Allocations” chart in Figure 6.2, the Yale Portfolio generally has smaller allocations to asset classes with low expected returns such as fixed income and money markets, in favor of non-correlated assets. Non-correlated assets could be investments such as private equity and other alternative investments.

Investing can be considered both an art and a science. As we’ve learned from the field of behavioral finance, many investors still cling to outdated prejudices, emotional responses, and superstitions not suited to successful strategies in the modern portfolio. I see the art of investing as adjusting and interpreting according to what investors anticipate will happen in the future. The science is based on math and a revised Modern Portfolio Theory. Revising MPT and updating it to reflect non-correlated inputs and variations likely not present at the time the original theory was developed is, in my opinion, much more desirable than rejecting it outright.

Down to Earth: What It Means for the Average Investor

As we saw in our Goodyear example, technology innovation driven by very smart people can eventually benefit the average consumer. This technology is now causing the financial industry to experience significant change. Or is it really a change at all? Some think alternatives are just a trend. I think alternative investments are a movement driven by the institutional market’s search for better risk-adjusted returns and increasing need for diversification.88

88 Virginia Munger Kahn, Financial Advisor, “Alternatives Becoming Mainstream,” July 2012.

Analysis by Eager, Davis, and Holmes found that from the beginning of 2011 to late 2012, investors added more money to alternative investments than to equity and fixed income combined—$94.6 billion in alternative investments (real estate included), versus a combined $79.6 billion to equities and fixed income that same year.

Consider that only $15.4 billion was committed to alternative investments and real estate just eight years earlier in 2003 by North American institutional investors. In that same year, investors made $65.9 billion of combined investments in equities and fixed income (excluding balanced and global tactical asset allocation mandates).89 What does this mean? As markets in this country and around the world have expanded, alternative strategies are receiving a disproportionate share of these assets.

89 Tracker Hiring Analytics, Database of Institutional Investment Manager Hires, Eager, Davis, and Holmes.

If the increasing speed with which alternatives are being adopted by institutional investors is any indication, I would say the trend towards alternatives is unlikely to end any time soon. After reaffirming that the “60% equities/40% fixed-income allocation that was standard decades ago is long gone,” Mr. Kloepfer told Pension & Investments that “the typical public pension plan’s fixed-income allocation, for example, could start heading toward 20%,” and “many plans already are in the 20% to 30% range for fixed income.”90 Much of it is fueled by the “danger in safety” that exists in bonds.

90 Arleen Jacobius, Pensions & Investments, “Institutional Investors Quicken Shift to Alternative Investments,” September 2012.

Rising interest rates expose investors to interest rate risk; low yield that has plagued the space in recent years now means investors are paying a premium to own bonds. This is a premium they’re unlikely to recover anytime soon due to the end of historically low interest rates imposed by the Federal Reserve’s quantitative easing policy. The volatility introduced by the end of the policy was acutely felt in the summer of 2013, when talk of a program commonly referred to as “tapering” by the Fed led to $61.7 billion in bond mutual fund and ETF redemptions in June of that year, which was a record amount. As ThinkAdvisor.com noted at the time, the outflow “far exceeds the previous record monthly outflow of $41.8 billion at the height of the financial crisis in October 2008.”91

91 John Sullivan, “Bond Mutual Funds, ETFs Post Record Outflow,” ThinkAdvisor.com, June 28, 2013.

So, where is that money going now? It may be going to alternative investments.

In addition to Pension & Investments and Callan’s findings, research firm Morningstar, along with Barron’s, reported that at the beginning of 2012, approximately 65% of financial advisors and 67% of institutions surveyed said that alternative investments “...are as important as or more important than traditional investments, down slightly from the last survey.”92 The survey included 264 institutional investors and 365 advisors.

92 Morningstar, “Annual Survey Finds Continued Strong Usage of Alternative Investments Among Institutions and Financial Advisors But Growth Slowing,” May 29, 2012.

Similarly, Russell Investments’ 2012 Global Survey on Alternative Investing found that institutions participating in the survey have made “significant allocations to alternatives”—on average 22% of total fund assets. The majority of respondents expect to keep their alternative allocations the same or increase them in the next one to three years, with expected increases to alternatives such as hedge funds and private real estate.93 The survey included 144 organizations totaling $1.1 trillion in assets.

93 Russell Investments, “Russell 2012 Global Survey on Alternative Investing Finds Institutional Investors Looking to Alternatives for Both Diversification and Alpha,” June 2012.

Institutional managers such as David Swensen have found success in the alternative investments market, which brought attention to these strategies from retail investors. Most likely the increasing correlation (discussed in Chapter Four) and disappearing diversification associated with traditional investments are driving sophisticated institutional investors to alternative investments as well.

Alternative Investments: No Longer So Alien

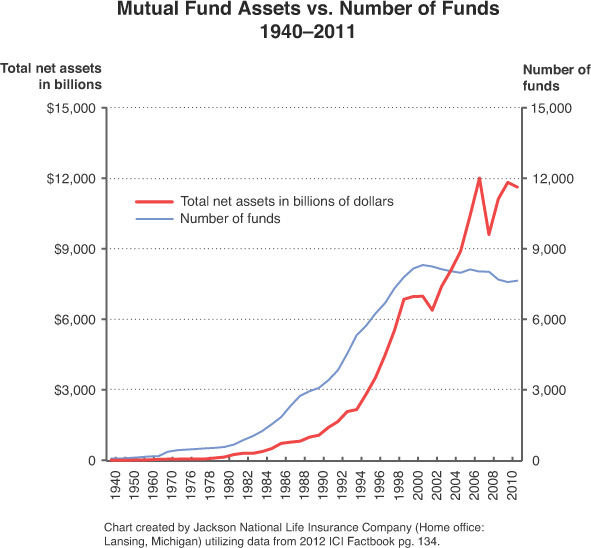

What it all means is that interest in alternative investments may be growing. Historically, many financial innovations were once likely considered alternative. Although Massachusetts Investors Trust, largely thought of as the first contemporary mutual fund, was created and deployed in the 1920s, it wasn’t until the bull market in the 1980s that mutual funds gained widespread adoption and acceptance.94 Today mutual funds are a common addition to portfolios and currently hold trillions of investable dollars. The chart in Figure 6.3 measures the growth of mutual funds, as well as their assets, since 1940.

94 James E. McWhinney, Investopedia, “A Brief History of the Mutual Fund,” September 7, 2009.

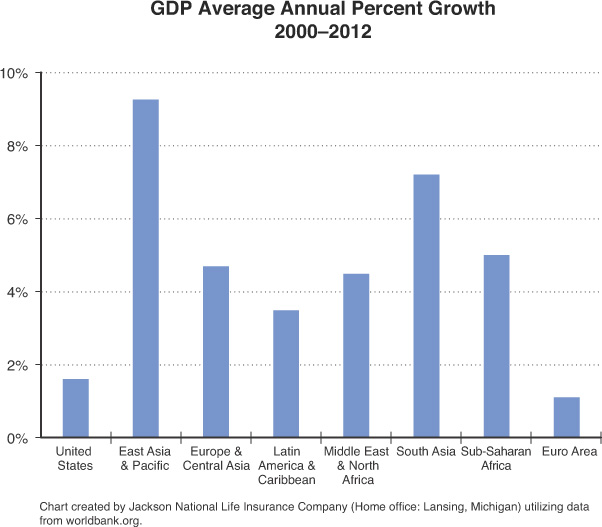

More recently (and as discussed in the Chapter Three), an increase in wealth and average standard of living in many emerging market countries is a direct result of globalization that began post-World War II. Through the advent of emerging market mutual funds and similar products, countries once considered exotic and far-flung, now offer many investing opportunities. In fact, the GDP growth of developing countries has outpaced that of developed since the global economic crisis of 2008.95 Who would have thought, even as recently as a few years ago, that South Africa, Laos, Vietnam, and many other so-called frontier markets would offer the potential that they have recently—so much so that many mutual fund companies now offer investment strategies that provide exposure to these regions?96 As you look at Figure 6.4, observe how the GDP growth of developing countries has outpaced that of the U.S.

95 The World Bank, “GDP Growth (Annual Percent),” 2013.

96 Conrad De Aenlle, New York Times, “Looking to Frontier Markets for the Next Big Thing in Investing,” April 2012.

Yet recent headlines haven’t made it easy to take advantage of these offerings. Scandals involving once-trusted financial titans have left some individuals understandably skeptical of anything new or perceived as untested.

I’ve seen that too few realize that alternative investments aren’t new and in many cases have a long track record in the institutional markets. However, alternatives just recently gained the attention of Main Street investors, thanks in large part to the success of strategies employed by endowment and other institutional investors, and their recent collaborations with financial services companies. Over the last six years, 1,012 alternative products have been introduced, in the form of public securities (mutual funds, ETFs, ETNs, and closed-end funds). Their popularity should continue to grow as asset managers have plans to create more alternative investment products than traditional investment products over the next 12 months. In fact, these same managers anticipate that, on average, alternative mutual fund assets will comprise 13.6% of total assets by the end of 2023.97

97 Cerulli Associates, The Cerulli Report, “Alternative Products and Strategies,” pages 68, 72, 76, 2013.

From the Alt Vault: Valuable Takeaways from Chapter Six

Although new ideas are often met with skepticism, good ideas are able to stick around and gain public approval. Just as important technology often starts with NASA engineers, important alternative investment concepts have been ignited by institutional investors—and mainstream investors are starting to take notice.

![]() Collaborative efforts can lead to cutting edge products and strategies, but not all ideas make smart investments.

Collaborative efforts can lead to cutting edge products and strategies, but not all ideas make smart investments.

![]() Investors should start thinking beyond the two-dimensional world of stocks and bonds.

Investors should start thinking beyond the two-dimensional world of stocks and bonds.

![]() Investing is both art and science.

Investing is both art and science.

![]() Investors can’t be the Magellan of their portfolios without a little exploring.

Investors can’t be the Magellan of their portfolios without a little exploring.

![]() Money is moving towards alternatives as part of some investors’ diversification strategy.

Money is moving towards alternatives as part of some investors’ diversification strategy.

What’s next: The improper understanding of risk results in the slow erosion of assets and purchasing power over time. What’s to be done? It might be as simple as a few more swings at bat.