Eight. Beta Blockers

Is your blood pressure rising?

The Center for Disease Control estimates that one in three American adults suffer from the “silent killer”—high blood pressure.107 Luckily, we have medications designed to help. Beta blockers work by reducing the effects of adrenaline, which can cause increased heart rate and higher blood pressure. Beta blockers can also help improve blood flow by opening blood vessels.108

107 Centers for Disease Control and Prevention, “High Blood Pressure,” May 2013 and Sung Sug Yoon, R.N., Ph. D.; Vicki Burt, R.N., Sc.M.; Tatiana Louis, M.S.; Margaret D. Carroll, M.S.P.H., U.S. Department of Health and Human Services, ODC, NCHS Data Brief, “Hypertension Among Adults in the United States, 2009–2010,” October 2012.

108 Mayo Clinic, “Beta Blockers,” December 2010.

In addition to its medical nomenclature, beta is also a financial term related to risk and volatility. After what could be called a global economic heart attack suffered in 2008, I feel that reducing beta serves as an appropriate metaphor for reducing the corresponding stress and angst associated with the market’s peaks, valleys, and wild swings. Understanding beta and its role in the portfolio can lead to better overall financial health.

We’ve looked at the problems caused by living longer with fewer sources of income and increasingly correlated markets. It’s now time to focus on a potential treatment by examining this important measurement of systematic risk.

The Prescription: Bringing Balance

“Past performance is no guarantee of future results.”

This well-known financial industry disclaimer has taken on added significance since 2008. It refers to the investment return of individual securities and portfolios and often reflects widespread market behavior. As volatility becomes more prevalent, strategies that performed well in the past cannot be expected to deliver the same returns. Diversification, which cannot assure a gain or a loss, can help stabilize your portfolio, so that when one stock goes down, the rest don’t necessarily follow.

Professor Israelsen, whom we discussed in the last chapter, has developed a multi-asset portfolio known as the 7Twelve® Portfolio. One of his business partners, Andy Martin, explains how our understanding of diversification in a portfolio has evolved over time.

Martin points to the first balanced fund, created by CPA Walter Morgan, as an example of a key transformation in how investment managers approached diversification. The fund was eventually renamed the Wellington Fund and is still in existence today.

“There could not have been a worse time to start a stock mutual fund, or perhaps a better time to start a balanced fund,” Martin writes. “The Dow Jones Industrial Average (DJIA) reaches a record peak of 381.17 on September 3, 1929, and loses 90% of its value over the next three years to a low of 41.22 on July 8, 1932. In contrast, the Wellington Fund loses ‘only’ 58.5%...The Wellington Fund earns a 5.9% annual return during this fateful 25 year period.”109 The fateful period that Martin is referring to is the first 25 years the Wellington Fund was in existence.

109 Andy Martin, 7Twelve, “The Right Number,” 2012.

The Wellington Fund used diversification strategies to help manage the volatility of the 1930s.110 By selecting stocks that had a low correlation to what turned out to be the Market Crash of 1929, the fund not only reduced losses but managed to achieve returns. In this case, the lower correlated stocks served as beta blockers.

110 John C. Bogle, Bogle Financial Markets Research Center, “Reflections on Wellington Fund’s 75th Birthday,” 2004.

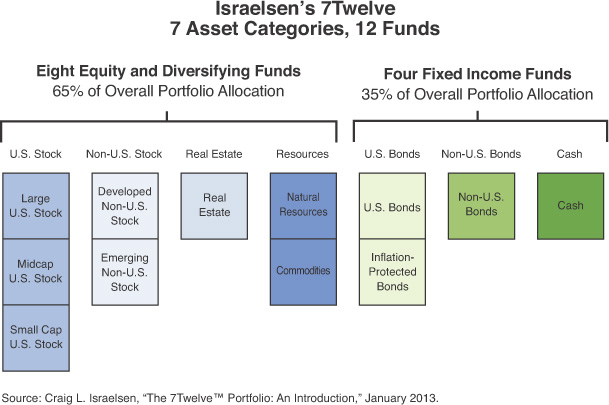

In the same way the Wellington Fund used diversification to reduce beta in the 1930s, modern examples of balanced portfolios utilize multiple asset classes to enhance diversification, potentially improve performance, and manage risk. An example is Israelsen’s 7Twelve strategy (shown in Figure 8.1), which allocates money across 12 funds that fall in seven different asset categories. Strategies such as 7Twelve recognize that we live in a multi-asset world, including domestic and foreign stocks, domestic and non-U.S. bonds, real estate, commodities, and cash.111

111 Craig L. Israelsen, “The 7Twelve Portfolio: An Introduction,” January 2013.

Martin says that the turbulence of 2008 taught “...us that the two-asset investment model of stocks and bonds may no longer be enough to diversify against the numerous threats to investors’ security.”112 This illustrates that the right asset mix from yesterday’s markets may not be the best mix for today’s or tomorrow’s markets, especially if one is looking to hedge against increasing correlation.

112 Andy Martin, 7Twelve, “The Right Number,” 2012.

Better Beta: Reduce Stress

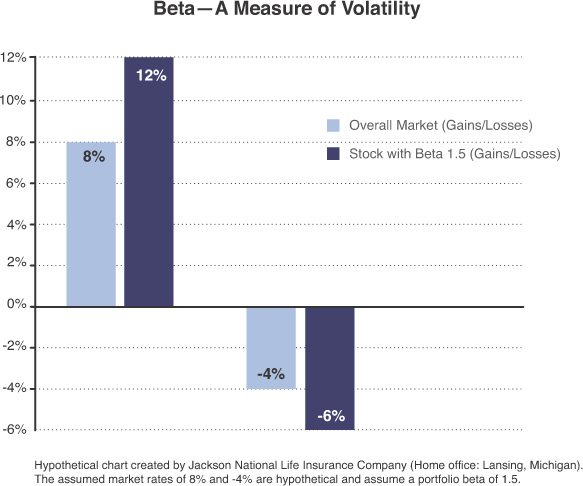

You may wonder if there’s a way to maintain your portfolio’s health by attempting to maximize the performance of the individual stocks that comprise the portfolio. One option is to understand and adjust for beta, which is a statistic that compares the overall volatility of a stock to that of the market. Volatility can negatively or positively affect the performance of the stock, depending on direction. Financial professionals and money managers use beta as one of many indicators to determine investment volatility, which is a component of risk. A beta of 1.0 means that a stock’s price will increase or decrease in the same direction and magnitude as the market as a whole, meaning they are closely correlated. A beta that is less than 1.0 generally means the asset has less volatility than the overall market. A beta that is greater than 1.0 means the asset has more volatility than the overall market. For example, a beta of 1.5 implies that an investor can anticipate 50% greater volatility in the movement of a stock or portfolio compared to the total market.

The chart in Figure 8.2 is a hypothetical example of how a highly correlated stock moves with the market and how volatility can have a positive or negative effect on return. When the market does well, the stock is expected to do even better. When the market does poorly, the stock is expected to do worse.

Specific to our discussion, the beta of a portfolio is a measure of market correlation and can act as a guide to better diversification. By adding together the beta of the individual securities within a given portfolio, and determining how far the portfolio is then removed from the base beta of 1.0, managers can add or remove securities to better target risk-adjusted returns.

When implementing alternative strategies, beta can be reduced through greater diversification, perhaps without sacrificing long-term, risk-adjusted returns. This can enhance risk-adjusted returns and may be possible by structuring a portfolio that is focused on achieving returns that are, for the most part, uncorrelated with those of the market.

Illustrations like the beta chart point to methods to reduce risk without necessarily having a corresponding reduction in returns or, as Yale’s David Swensen puts it, “by identifying high-return asset classes, not highly correlated with domestic marketable securities, investors achieve diversification without the opportunity costs of investing in fixed income. The most common high-return diversifying strategy for a U.S. investor involves adding foreign equities to the portfolio. Other possibilities for institutions include real estate, venture capital, leveraged buyouts, oil and gas participations, and absolute return strategies. If these asset classes provide high equity-like returns in a pattern that differs from the return pattern of the core asset (U.S. domestic equities), investors create portfolios that offer both high returns and diversification. Although on an asset-specific basis, higher expected returns come with the price of higher expected volatility, diversification provides investors with a mechanism to [manage] risk.”113

113 David F. Swensen, “Pioneering Portfolio Management,” 2000.

Now Swenson’s advice is a bit outdated as foreign equities have become increasingly correlated to domestic equities (discussed in Chapter Four). But the overall point is still valid—diversification can help manage risk. And of course, always remember that past performance is not indicative of future results.

Clinical Trial: Safe for Public Use?

Arbitrage is an alternative investment strategy that attempts to take advantage of the price discrepancy of one financial instrument available for sale or purchase in two different markets. This difference in prices means arbitrage is a “spread vehicle,” since it seeks to capitalize on the difference (or spread) of the given prices.

The textbook business started by Supap Kirtsaeng is an example of arbitrage. As a student at Cornell, Kirtsaeng was shocked at how much more expensive textbooks were compared to those found in his home country of Thailand. He asked his family to send over the less expensive textbooks and sold them to U.S. students. It is estimated that he eventually netted $1.2 million, enough to catch the attention of publishers.114 John Wiley & Sons filed a copyright infringement suit against Kirtsaeng, but ultimately lost (in March 2013 the U.S. Supreme Court overturned a lower court’s ruling that had gone in the publisher’s favor). Kirtsaeng’s story is an example of arbitrage, as he used the difference in pricing between two markets to his advantage.

114 Bill Hadley, UneMed, “Limitations on Copyright—The First-Sale Doctrine,” 2012.

In the investment world, arbitrage opportunities exist only momentarily, and if the strategy is incorrectly performed, can be especially devastating. Currency arbitrage trading, for instance, requires the availability of real-time price quotes and the ability to react quickly as opportunities present themselves. To determine the best arbitrage moment, some use “black boxes,” which rely on proprietary algorithms for speed and efficiency to calculate opportunities in the market. 115 Of course, Wall Street doesn’t rely entirely on artificial intelligence. Often a real, live human makes the final trading call.

115 Investopedia, “Definition of Black Box Model,” 2013.

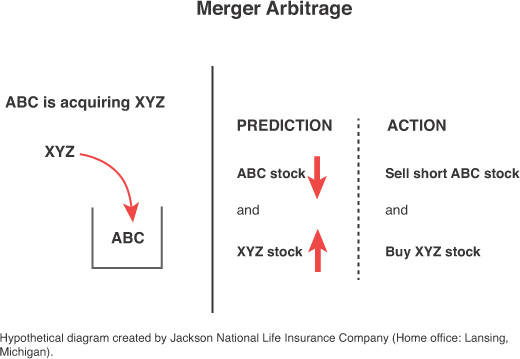

Another example of arbitrage is a merger arbitrage. Specific to our investment topic, suppose ABC company is acquiring XYZ company. An investor who believed XYZ stock will increase in value due to the merger, and that ABC stock would drop in value, would take advantage of a merger arbitrage opportunity by buying XYZ stock and selling short ABC stock (or bonds).

Company ABC is acquiring Company XYZ

Company ABC’s stock drops slightly

Company XYZ’s stock increases

Mergers and acquisitions occur regardless of market conditions (market neutral/low volatility/low correlation). Figure 8.3 is a graphical depiction to help you further understand the process of merger arbitrage.

Because it involves stock markets, investors might think the arbitrage strategy is highly correlated and presents the same level of risk as stocks, but this is not the case. By being long one stock (owning the stock you expect to increase) and short another (selling the stock you expect to decrease) in equal magnitudes, market risk may be reduced. In the diagram above, the investor would buy the XYZ stock because it is expected to go up, while simultaneously selling the ABC stock because it is expected to go down. As a result, arbitrage has a low beta connection with stock markets themselves, even though they may use stock spreads (or differences) as the underlying investments. For example, the data shows that arbitrage has mid-single-digit returns and low volatility when the HFRX Merger Arbitrage Index is used as a proxy for arbitrage.116

116 Lipper, a Thomson Reuters Company, 2013. Arbitrage returns measured by using the HFRX Merger Arbitrage Index from the index’s inception of 1/30/1998 to 12/31/2013.

It is important to keep in mind that this is an investment and may lose value. In a merger arbitrage transaction, an investor could lose value from both the long and short positions held. Holding a long position, or owning a security, is a traditional investing strategy and comes with the risks typically associated with investing. A short sale may be affected by selling a security that the fund does not own. If the price of the security sold short increases, the fund would incur a loss, as the investor was expecting the price to fall; conversely, if the price declines, the fund will realize a gain.

Like all sophisticated strategies, arbitrage requires education and expertise in order to successfully execute. While in theory arbitrage is often thought of as risk-free, in practice risks abound—some are minor, such as mistiming a trade that erodes the spread (and therefore the expected return) and some can be major.

Risk Parity

Another category that potentially manages risk is a concept known as risk parity. Risk parity is all about diversification. Rather than focusing on how specific dollar amounts are spread across a portfolio, it instead involves the allocation of risk across various components in a portfolio. Risk parity means that the balance is focused on the allocation of risk, not the allocation of capital. The strategy usually involves four main drivers: equity risk, credit risk, commodity risk, and interest rate risk. Balancing the portfolio’s risk across these four drivers is needed to achieve parity. Think of macro factors such as periods of rising and falling economic growth and the resulting effect on rising and falling interest rates. While it’s very difficult to predict when each will occur, risk parity seeks to balance risk across each factor, thereby increasing the potential likelihood risk parity strategies perform better than capital allocated traditional investments.

More simply, by focusing on risk allocation rather than asset allocation, risk parity attempts to provide a customized risk compared to the traditional portfolio allocation of 60% stocks and 40% bonds. Because of the complexity of predicting risk, risk parity strategies are not without potential for poor returns.

So, how do strategies like risk parity and merger arbitrage transfer to other markets and other strategies in the alternative space? Let’s take a look.

From the Alt Vault: Valuable Takeaways from Chapter Eight

Alternative strategies can be used as a strategy to help reduce beta. This is possible by structuring a portfolio uncorrelated to the broader market, as the premise behind this “smoother the better strategy” is that it potentially could result in less volatility.

![]() Beta is a risk measurement that compares the volatility of a stock or portfolio to the volatility of the market. Higher beta securities and portfolios tend to be more volatile and therefore riskier. Lower beta securities and portfolios tend to be less volatile and therefore less risky. Of course investing always involves risk.

Beta is a risk measurement that compares the volatility of a stock or portfolio to the volatility of the market. Higher beta securities and portfolios tend to be more volatile and therefore riskier. Lower beta securities and portfolios tend to be less volatile and therefore less risky. Of course investing always involves risk.

![]() The 60/40 mix does not always offer the optimal mix of growth and stability due in part to higher correlation and lower diversification.

The 60/40 mix does not always offer the optimal mix of growth and stability due in part to higher correlation and lower diversification.

![]() Alternatives could be an attractive consideration thanks to a history of low correlation to traditional markets, but it is always important to keep in mind that past performance does not guarantee future results, and when considering any of these strategies, it is prudent to understand how these types of securities fit into your personal risk profile.

Alternatives could be an attractive consideration thanks to a history of low correlation to traditional markets, but it is always important to keep in mind that past performance does not guarantee future results, and when considering any of these strategies, it is prudent to understand how these types of securities fit into your personal risk profile.

What’s next: Alternatives are receiving attention from the general public. Adding them to your asset allocation may help to navigate different market environments.