Chapter 7

Market Participants

7.1 INTRODUCTION

This chapter explains the roles that various types of companies and individuals play in the investment industry, and describes how each of these organisations and individuals interact with one another in the processes of placing orders, executing them, confirming executions and settling the resulting trades. The different organisations may be divided into the following broad categories:

1. Investors, including:

- Institutional investors such as pension funds and insurance companies

- Private investors

- Hedge funds

2. Institutional fund managers

3. Private client stockbrokers and investment managers

4. Investment banks that accept and execute orders from investors

5. Investment exchanges

6. Settlement agents, including

- Central counterparties, also known as clearing houses

- Central securities depositaries and international central securities depositaries

- Commercial banks that provide payment and custodian services

7. Others, including:

- Information vendors

- Money brokers

- Stock lending intermediaries

- Registrars and transfer agents.

Note that some large organisations act in multiple roles – for example, a large bank may be an institutional fund manager, a private client stockbroker, an investment bank and a commercial custodian all at the same time.

7.2 INVESTORS

Institutional investors include pension funds, insurance companies and fund management companies that manage investment schemes such as mutual funds, unit trusts and investment trusts. In most countries, they are the largest investors in equities. Institutional investors usually delegate the actual investment decisions to institutional fund managers whose role is discussed in section 7.3. Traditional institutional investors usually only take long positions in securities, and avoid investment in complex derivatives. For this reason, they are sometimes known as “long only” investors.

Private investors include individuals and charities. Private investors place their orders through private client stockbrokers and investment managers, whose role is examined in section 7.4.

Hedge funds are pooled investment vehicles that are privately organised and administered by investment management professionals and not widely available to the public. Many hedge funds share a number of characteristics: they hold both long and short positions, use derivatives and leverage to enhance returns, pay a performance or incentive fee to their hedge fund managers, have high minimum investment requirements and target absolute (rather than relative) returns. Hedge funds usually deal direct with investment banks whose role is examined in section 7.5.

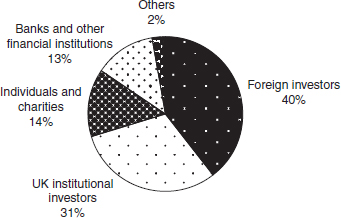

Figure 7.1 (taken from data produced by the UK Office of National Statistics) shows the breakdown of ownership of equities listed on the London Stock Exchange at the end of 2006. Note that foreign investors (mainly long only institutional investors and hedge funds) accounted for the 40% of the value of LSE listed shares.

Figure 7.1 UK share ownership at end of 2006

7.3 INSTITUTIONAL FUND MANAGERS

Institutional fund managers compete to win investment mandates from institutional investors. An investment mandate lists the types of investment (e.g. the geographical and industry sectors as well as the types of financial instruments) that the investor wishes the fund manager to invest in, sets performance targets for income and/or capital growth that the investor expects the fund manager to achieve, and describes how the fund manager will be remunerated. Within the guidelines of the mandate, the actual investment decisions are left to the fund manager.

A simplified example of an investment mandate might be as follows:

1. The Ethical Investment Pension Fund appoints XYZ Fund Managers to act on its behalf in investing in equities listed on exchanges in the United States of America and Canada.

2. Within the confines of (1), XYZ is not permitted to invest in the stocks of companies whose main business activities include the manufacture and/or distribution of alcohol, tobacco or armaments.

3. Within the confines of (1), XYZ is also authorised to lend securities provided that collateral is obtained from the borrower.

4. XYX may purchase or sell futures, and purchase put and call options on the equities that it has invested in, in order to hedge against falls in the market value of its portfolio, provided that such futures and options are listed on exchanges in the United States and Canada.

5. Ethical Investment Pension Fund expects XYZ to achieve capital growth of the portfolio equal to 100% of the growth of the Dow Jones US Large-Cap Index over the next three years.

6. Ethical Investment Pension Fund expects XYZ to achieve an annual income of 4% of the value of the fund over the next three years.

7. Ethical Investment Pension Fund will pay XYZ an annual fee of 1% of the fund value each year.

The fund manager will perform its own research into the United States and Canadian securities markets, and base its investment decisions on that research. When it makes a decision to purchase or sell a particular investment, it will place orders to buy or sell individual securities, futures and options with an investment bank – see section 7.5.

Institutional fund managers are often known as buy-side firms; and this term will be frequently used in the remainder of this book.

7.4 PRIVATE CLIENT STOCKBROKERS AND INVESTMENT MANAGERS

As their name implies, these organisations exist to serve the private individual. The services that such firms offer their clients may be divided into three categories. Some firms will only offer one or two of these services, while others will offer all three:

- Execution only: The investor takes sole responsibility for all investment decisions. When he is ready to buy or sell, he enters the order by telephone, letter or the firm’s website; and the firm executes the order on the investor’s behalf. The firm cannot be held responsible for the quality of the investment decision.

- Advisory dealing: When the investor is ready to buy or sell, he is able to talk it over with the firm, and he may or may not take the advice of the firm. The ultimate responsibility for the quality of the decision lies with the investor.

- Discretionary dealing: The investor signs an investment mandate with the firm, and the firm then manages the investor’s portfolio according to the terms of that mandate. The ultimate responsibility for the quality of the decision lies with the firm itself.

In addition, these firms also provide other services to investors that normally include safe custody services and also tax sheltered investments, estate and pension planning:

7.5 INVESTMENT BANKS THAT ACCEPT AND EXECUTE ORDERS FROM INVESTORS

This book uses the term “investment banks” to describe institutions that accept orders from investors and/or their agents and execute them. The book also uses, in the context of order flows, the term “sell-side firms” to describe them. Not all investment banks offer all the services described in this section, and not all the firms that offer these services would describe themselves as investment banks.

7.5.1 Investment banks’ business activities

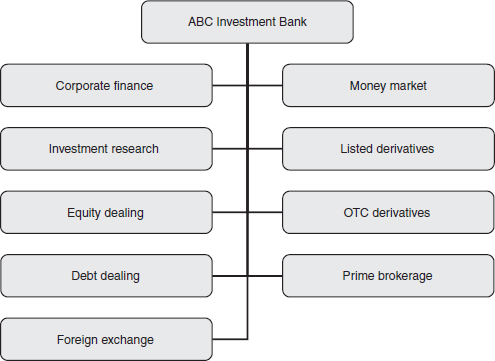

An investment bank that offers all the services described in this section might be organised along the business lines shown in Figure 7.2.

Figure 7.2 ABC investment bank organisation chart

- Corporate finance: The customers of this service are companies, central and local governments and supranational institutions. These customers use the bank’s corporate finance department to advise and possibly also to provide finance to them when they are, inter alia:

– Considering issuing new shares on the primary market, or making a primary market offering of debt securities

– Considering acquiring other companies

– Reacting to approaches from other companies to purchase some or all of their assets

– Considering other corporate actions such as share splits, rights issues, bonus issues, etc.

- Investment research: This department researches the likely economic outlook for individual countries, business sectors and individual companies. The results of its research are made available to all the other business departments of the bank as well as to the bank’s customers.

- Equity dealing: This department accepts orders to buy and sell equities from clients, as well as dealing on the bank’s own behalf using its own capital. These orders may be executed either as agency trades or principal trades.

- Debt dealing: This department accepts orders to buy and sell debt securities from clients, as well as dealing on the bank’s own behalf using its own capital. Debt trades are usually, but not exclusively, executed as principal.

- Foreign exchange: This department accepts orders to buy and sell currencies from clients, as well as dealing on the bank’s own behalf using its own capital. Debt trades are almost always executed as principal.

- Money market: This department attracts deposits and makes loans.

- Listed derivatives: This department accepts orders to buy and sell listed futures and options from clients, as well as dealing on the bank’s own behalf using its own capital. Listed derivative trades are always executed in an agency capacity.

- OTC derivatives: This department trades in instruments such as swaps, OTC options, forward rate agreements, etc. Investment banks risk their own capital in these transactions which are executed in the capacity of principal.

- Prime brokerage: This is a package of services offered to hedge funds. The business advantage to a hedge fund of using a prime broker is that the prime broker provides a centralised securities clearing facility for the hedge fund, and the hedge fund’s collateral requirements are netted across all deals handled by the prime broker. The prime broker benefits by earning fees (“spreads”) on financing the client’s long and short cash and security positions, and by charging, in some cases, fees for clearing and/or other services.

The following “core services” are typically bundled into the prime brokerage package:

- Global custody (including clearing, custody and asset servicing)

- Securities lending

- Financing (to facilitate leverage of client assets)

- Customised technology (provide hedge fund managers with portfolio reporting needed to effectively manage money)

- Operational support (prime brokers act as a hedge fund’s primary operations contact with all other broker/dealers).

7.5.2 A typical application systems configuration for an investment bank

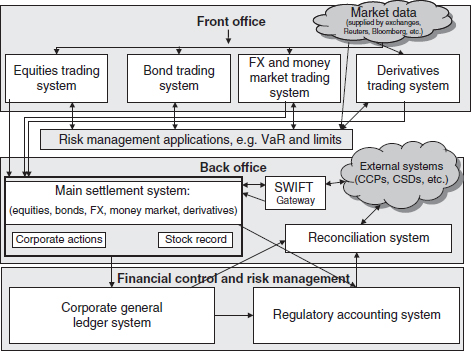

An investment bank that is active in all of the business areas described in section 7.5.1 will need a number of specialised business application systems to process the transactions and manage the positions in financial instruments that result from the transactions. Figure 7.3 shows a typical systems configuration diagram for such a bank. No two banks will have the same configuration, and the configuration of many large banks will be much more complex than the one in this example.

Figure 7.3 Simplified investment bank configuration

The bank uses the following systems to process its transactions and manage the positions that arise as a result of these transactions.

Front-office systems

There are four of these, one for each instrument type. Each one of them is linked to sources of market data that enable the dealer to “see the market” – in other words, to be able to see the current levels of market prices, interest rates and exchange rates, economic and political news stories that may affect these rates and prices, and corporate announcements such as company results and merger and acquisition activity that may affect the share price of a single company.

Some of this data will also be fed into the individual front-office systems where it will be used in either automated or manual trading decision support. Suppliers of market data include Reuters, Bloomberg and the major stock exchanges.

The front-office systems also hold details of client orders that are awaiting execution. When these orders are executed, details of the trade are forwarded to the main settlement system, which is classed as a “back-office system”.

Risk management applications

These applications are used to measure and control market risk and credit risk, and are described in Chapter 24.

Back-office systems

Main settlement system

The functions of the main settlement system usually include:

1. Receiving real-time trade details from the front-office systems and enriching those trade details with client/instrument-specific settlement instructions

2. Sending trade confirmations to clients and counterparties, and “matching” confirmations received from counterparties with its own records of those trades

3. Reporting trade details to regulators, in real time and within the maximum allowed period demanded by the regulators

4. Sending settlement instructions to settlement agents

5. Receiving reports from settlement agents about which trades have settled and which have not, and updating its records as a result of such reports

6. Forwarding details of trades, settlements and positions to the reconciliation system

7. Forwarding details of all the activities listed in items (1)–(8) that affect the general ledger to the corporate general ledger system and the regulatory accounting system.

8. Position management activity for bonds, equities and currencies, including the maintenance of the stock record which is described in Chapter 15

9. Processing of changes to positions as a result of corporate actions, dividends, etc. – these activities are described in Chapter 23.

Because no two investment firms have the same configuration, it is often the case that the activities of dividend and corporate action processing, and the maintenance of the stock record, are carried out by separate applications to the main settlement system. In other firms, however, these activities will be an integral part of the main settlement system.

Reconciliation application

The purpose of this system is to take feeds from the main settlement system concerning transactions, balances and positions and compare them to data received from settlement agents so that the bank is able to prove that its records about transactions have settled today, and that the resulting position from such settlements agrees with the records of the external agents concerned.

SWIFT gateway

Most of the communications with the external systems will be in the form of SWIFT messages. The SWIFT Gateway system is the portal that validates, encrypts and transmits outgoing messages, and receives, de-encrypts and routes incoming messages to the appropriate applications or users. SWIFT is examined in Chapter 11.

Financial control systems

The corporate general ledger is the system that consists of the company’s legal records. The general ledger records all the assets, liabilities, income and expenditure of the company. See Chapter 14 for more detailed information about investment accounting.

The regulatory accounting system is the system that is used to calculate the financial and statistical information that the firm needs to send to its regulator. The requirements of the regulators are examined in Chapter 8.

7.6 INVESTMENT EXCHANGES

An investment exchange (also known as stock exchange, share market or bourse) is a corporation or mutual organisation that provides facilities for stockbrokers and traders, to trade company stocks and other securities including bonds, derivatives and physical commodities such as precious metals and agricultural products. There are three economic functions of an investment exchange:

1. To provide a means for companies to raise new capital in the form of equities and debt instruments

2. To provide facilities for investors to trade company stocks and other securities

3. To create standardised derivative instruments such as futures and options which are based on the underlying securities, and to provide facilities for investors to trade in these derivative instruments.

7.6.1 The world’s major investment exchanges

According to the World Federation of Exchanges, the 10 largest stock exchanges by market capitalisation as of 12 July 2007 (in trillions of US dollars, rounded to two significant figures) are as follows:

1. NYSE Euronext – $211

2. Tokyo Stock Exchange – $4.7

3. NASDAQ – $4.22

4. London Stock Exchange – $4.03

5. Hong Kong Stock Exchange – $2.1

6. Toronto Stock Exchange – $2.0

7. Frankfurt Stock Exchange (Deutsche börse) – $2.0

8. Shanghai Stock Exchange – $1.7

9. Madrid Stock Exchange (BME Spanish exchanges) – $1.5

10. Australian Securities Exchange – $1.3.

7.6.2 Connecting to stock exchange trading systems

Buy-side firms that wish to trade instruments listed on an investment exchange have to route their orders to a sell-side firm – a stock exchange member. That member firm’s IT department therefore needs to organise connectivity to a large number of stock exchange computer systems to facilitate trading.

Stock exchange trading systems may be classified in three ways.

Order-driven markets are designed to support markets in highly liquid, heavily traded securities, futures and options. They have no designated or official market makers. A member firm who wishes to buy a given stock at a given price submits a buy order to the relevant LSE market system, while at the same time other member firms who wish to sell the same stock submit sell orders to the relevant LSE system. When a buyer’s bid meets a seller’s offer (or vice versa) the stock exchange’s matching system will decide that a deal has been executed. The identity of the buyer is not known to the seller, and vice versa.

Example

In Table 7.1, three firms have entered orders to a stock exchange system to buy shares in Company A with price limits – i.e. the maximum price that they are prepared to buy at and one firm has entered an order to sell securities in the same company with a price limit – i.e. the minimum price at which it is prepared to sell. Before the stock exchange trading system executes the trade, the order book looks like that shown in the table.

Table 7.1 Orders placed on the stock exchange queue

The stock exchange system will therefore be able to fill part of Firm 4’s order to sell by matching it as follows:

- 4800 shares against the buy order issued by Firm 1

- 1500 shares against the buy order issued by Firm 2.

The remaining part of Firm 4’s sell order and the whole of Firm 3’s buy order cannot be filled immediately, so they will remain on the order book until such time as other firms place further orders. The state of the order book will now be as shown in Table 7.2.

Table 7.2 Orders remaining on the queue

Quote-driven markets are designed for less liquid, less heavily traded instruments. In these systems some of the exchange’s member firms take on the obligation of always making a two-way price in each of the stocks in which they make markets. These firms are therefore known as market makers. If another member firm wishes to buy or sell a stock then they approach the market maker direct, either by telephone, or more likely electronically by using the stock exchange market system concerned. This system will display the bid and offer prices quoted by each market maker for trades in normal market size, and the firm that wants to execute the order will be able to use the stock exchange system to select the market maker that will provide best execution. In a quote-driven market, unlike an order-driven market, the identity of the buyer and seller are known to each other.

Hybrid markets offer both facilities – most orders are fulfilled through the order queue, but market makers exist side by side to guarantee trade execution if there is not enough liquidity in the order queue. Firms that have to execute orders may choose to place the order on the queue, or to approach a market maker. Depending on how the order was placed, the identity of the buyer and seller may or may not be known to each other.

All the systems that investment exchanges use to facilitate trading in listed futures and options are order-driven systems. Equities, which are less liquid than listed derivatives, may be traded on any one of the three types of platform.

7.7 SETTLEMENT AGENTS

Once orders have been executed, then mechanisms need to be put in place to settle the resulting trade. Settlement is the process where the buyer pays the proceeds of the trade and receives legal title to the item it has purchased, while the seller receives the proceeds of the trade and has to deliver the item it has sold to the buyer.

Settlement date is the date on which settlement occurs. Settlement date should be the same date as value date. FX, money market and OTC derivatives deals usually do settle on value date unless there has been some kind of processing error by one of the parties. Securities trades are less likely to settle on value date, because of the affect of short selling.

Several different kinds of institution provide services whose end result is trade settlement. This book refers to them collectively as settlement agents, and there are four different types.

7.7.1 Clearing houses or central counterparties

In section 7.6 we learned that investment exchanges offer both order-driven markets and quote-driven markets, and that in an order-driven market the identity of the borrower is unknown to that of the seller, and vice versa. Clearly, then, the buyer and seller cannot settle the trade directly with each other in these circumstances. Therefore there is a role for a clearing house or central counterparty (CCP) in these markets.

In the example in section 7.6, the orders shown in Table 7.3 have been matched against each other.

Table 7.3 Matched trades

Because Firms 1, 2 and 3 are not aware of each other’s identity, as soon as the exchange has matched the orders, its systems inform a CCP that the trades have been executed. The CCP then takes over the obligations to make payments and/or deliver the instrument concerned – every other counterparty settles its obligations with the CCP, and not with each other.

This process – the substitution of one party to a contract by another party – is known as novation. The advantages to an exchange and its member firms in having a CCP include the following:

1. Post-trade anonymity: It is not necessary for the exchange to divulge the identity of Firm 1 to Firm 4 or vice versa; so there is no danger of one party learning the other party’s commercial secrets as a result of discovering their trading pattern.

2. Netting of positions: Firm 1 may have carried out many trades in an identical instrument. The CCP nets these into a single position.

Without netting, Exchange Member 1 would have had to make two deliveries of HSBC shares and three receipts of the same stock, make three payments and receive two. Because of netting there is a single payment and a single delivery.

3. A reduction in credit risk: Because the buyers and sellers are unaware of each other, they are by definition unaware of each other’s credit status. Once the CCP has novated the contract, sellers no longer have to worry about Firm 3’s ability to pay for the securities on settlement date, and buyers no longer have to worry about the other Firms’ ability to deliver. The CCP’s ability to meet its obligations is monitored by the regulator in the country where the CCP is located. However, the CCP has to monitor the ability of its member firms to meet their obligations. It does this by requiring them to place collateral with the CCP to meet margin requirements.

Netting example

On 12 February Investor 1 placed an order to buy 5000 HSBC shares with Exchange Member 1 for £5 per share for value date 15 February. Exchange Member 1 placed this order on the London Stock Exchange SETS Queue and it was matched with a sell order from another member.

Exchange Member 1 also placed the four additional orders shown in Table 7.4 for HSBC shares on the SETS queue on 12 February, all for value date 15 February, and all the orders were matched by other member firms. The summary for all five additional orders is therefore as shown in the Table.

Table 7.4 Trade settlement netting by central counterparty

Margin and collateral – an introduction

The following is an example of how the CCP uses collateral and margin to manage its credit risk:

1. On 1 February 2007 Party A bought a futures contract that obliges them to take delivery of 1000 shares in ABC plc on 30 March 2007 in return for payment by Party A of £10 per share. So the total amount they have to pay to the CCP if they still hold the contract on 30 March would be £10 000.

2. However, by 7 February the price of ABC plc shares is only £8 per share. Party A stands to lose £2000 if it still holds the position on 30 March. The CCP therefore required Party A to make a margin payment of £2000 to cover the CCP’s risk.

3. If, at some time between 8 February and 30 March, the price of ABC shares rises to £9 per share, then the CCP will refund £1000 to Party A. If, however, it falls to £7 per share then the CCP will demand another £1000 from Party A.

To avoid frequent margin calls immediately after the trade is agreed, CCPs require their member firms to pay an amount of initial margin that allows them to take positions of a given number of lots of each instrument. They follow this up with further margin calls to pay maintenance margin (also known as variation margin) which is the payment to cover the mark-to-market losses shown in the example.

When a member firm has many positions, some of which are showing losses and some showing profits, the maintenance margin is calculated on the net figure. Most exchanges use a methodology known as SPAN (Standard Portfolio ANalysis of risk). This is a leading margin system, which has been adopted by most options and futures exchanges around the world. SPAN is based on a sophisticated set of algorithms that determine margin according to a global (total portfolio) assessment of the one-day risk for a trader’s account.

Instead of paying a margin call in cash, the CCP accepts the deposit of a wide variety of government bonds as collateral.

All investment exchanges that list contracts in futures and options use a central counterparty to handle the post-trade activities for these instruments. Some exchanges that list securities use a CCP to novate all securities trades, while some of them just use a CCP to settle those trades that are eligible to be executed on an order-driven market. Table 7.1 shows which CCPs are used in each of the world’s 10 largest securities markets.

It is not necessary for every sell-side firm to be a member of every clearing house associated with every exchange of which it is a member. Derivatives exchanges provide three types of membership:

- A clearing member is an exchange member that clears only its own trades with the CCP appointed by the exchange.

- A general clearing member is an exchange member that clears both its own trades and also trades executed by other firms, who are known as:

- A non-clearing member – a firm whose trades are cleared by a general clearing member.

General clearing members will receive margin calls from the CCP for both their own positions and also the positions held by their clearing clients, and they have to pass those margin calls on to their clearing clients.

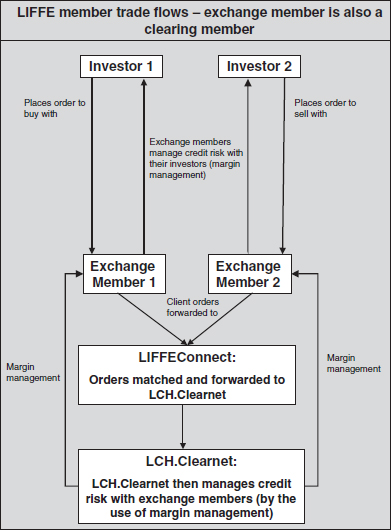

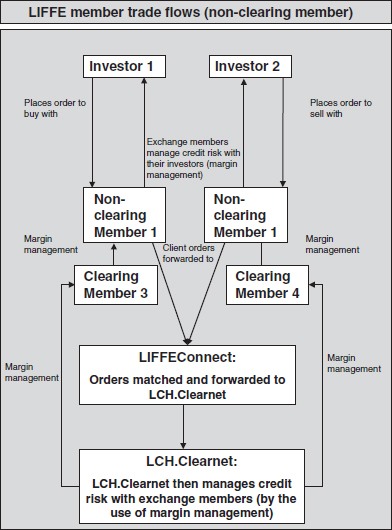

Diagrammatically, this is shown in Figures 7.4 and 7.5, which show the flow of a trade executed on the Euronext.LIFFE exchange in London; this is then cleared by LCH.Clearnet, the clearing house associated with the exchange.

Figure 7.4 shows the trade flow when the firm is clearing its own trades; Figure 7.5 shows the trade flows when the firm’s trades are cleared by a general clearing member:

Figure 7.4 LIFFE trade flows – self clearing

Figure 7.5 LIFFE trade flows – non-clearing member

Once the LIFFEConnect system (the order-driven market system used by Euronext.LIFFE) has matched the orders, the exchange reports the matched trades to LCH.Clearnet and the transactions are novated. The clearing house then manages its credit risk with the member firms by the use of margin management. If the member firm was not itself a clearing member, then two exchange members who are also clearing members would be involved, and the diagram now appears as shown in Figure 7.5.

The CLS Bank – netting for FX transactions

FX transactions are not executed through an investment exchange. Until 2001, each FX trade was settled separately, creating enormous volumes of individual payments and creating operational risk. CLS Bank was created to carry out transaction netting in this market. Firms who are CLS Bank participants advise the CLS Bank of the trades that they have to settle, and it nets all the movements in each of the currencies down to a single net payment or receipt for that currency. CLS Bank offers this service for 15 currencies. CLS Bank is headquartered in New York and regulated by the Federal Reserve Bank. An example of settlement netting using the CLS Bank is provided in section 18.1.5.

7.7.2 Central securities depositaries and international central securities depositaries

Sell-side firms use CSDs and ICSDs to settle their trades in securities. Each country has a single CSD. A CSD is an organisation that serves the investment exchanges of a particular country by holding securities either in certificated or uncertificated (dematerialised) form, to enable transfer of securities between buyer and seller. The functions of a CSD include, inter alia:

- Settlement: The buyer instructs the CSD to deliver the securities to the seller, and the seller instructs the CSD to make payment to the buyer on value date. Provided that:

– The seller’s instructions and the buyer’s instructions match

– The seller has the securities to deliver

– The buyer has either cash or credit to pay for the securities.

Then the CSD will settle the trade on value date.

- Safe custody: The CSD holds the securities on behalf of its members.

- Dividend and coupon processing as well as corporate action processing. Registrars as well as issuers are involved in these processes, depending on the level of services provided by the CSD and its relationship with these entities.

- Other services: CSDs offer additional services aside from those considered core services. These services include securities lending and borrowing, and repo settlement, which are examined in Chapter 21.

An international central securities depository (ICSD) is a central securities depository that settles trades in international securities and in various domestic securities, usually through direct or indirect (through local agents) links to local CSDs. ClearStream International (formerly Cedel), Euroclear and SegaInterSettle are considered ICSDs. While some view the New York-based Depository Trust Company (DTC) as the national CSD for the United States rather than an ICSD, in fact DTC – the largest depository in the world – holds over USD 2 trillion in non-US securities from over 100 nations.

Table 7.5 shows the relationship between exchanges, central counterparties and CSDs for the world’s 10 largest securities exchanges.

Table 7.5 Major stock exchanges and their clearing arrangements

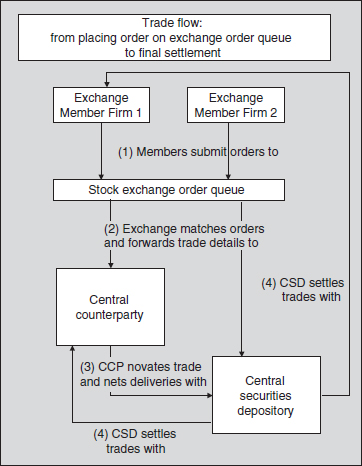

The flow of trades in securities between sell-side firms, exchanges, CCPs and CSDs can be represented by Figure 7.6.

Figure 7.6 Trade flow between members, exchanges and clearing houses

Note that trades in futures and options do not require the involvement of the CSD. The reasons why are explained in Chapter 8.

7.7.3 Commercial custodians

Institutional investors use custodian banks to settle their security trades. The role of a custodian is very similar to that of a CSD, i.e. to hold in safekeeping assets such as equities and bonds, arrange settlement of any purchases and sales of such securities, collect information on and income from such assets (dividends in the case of equities and interest in the case of bonds), process corporate actions, securities lending and borrowing and repo settlement, provide information on the underlying companies and their annual general meetings, manage cash transactions, perform foreign exchange transactions where required and provide regular reporting on all their activities to their clients. This reporting often includes “value added” services that are not provided by a CSD, such as performance measurement and peer group comparison.

Custodian banks are often referred to as global custodians if they hold assets for their clients in multiple jurisdictions around the world, using their own local branches or other local custodian banks in each market to hold accounts for their underlying clients.

Note that although the order to trade is given to the sell-side firm by the fund manager that is acting for the institutional investor, it is the investor itself that appoints the custodian. This can lead to the situation where a sell-side firm receives an order from a fund manager to buy or sell the same security for a number of investors, and the sell side firm has to settle separately with many custodians – one for each of the investors.

7.8 OTHER MARKET PARTICIPANTS

7.8.1 Information vendors

Investment firms depend on high quality, fast and robust feeds of real-time information covering market prices, company announcements and corporate actions, and economic and political events in order to make investment decisions. The two market leading suppliers of real-time market data are Reuters and Bloomberg.

The original missions of both Reuters – starting in the 1970s – and Bloomberg in the early 1980s were to deliver market data to securities professionals. Since then both companies have expanded enormously and diversified widely, and they both offer a very wide range of information services, media content and packaged software that is far beyond their original scope.

Reuters offers both conversational and automated trading in FX markets. Conversational dealing is where two dealers make use of the Reuters messaging facility to type requests for prices, and if the price is acceptable they type in their agreement to that price. A record of the conversation is printed out at each company’s dealing room and is also written to the database, to act as an audit trail of the deal. A significant proportion of FX deals are originated in this way.

Reuters publishes APIs for software developers to enable them to integrate Reuters data with the firms’ own applications. Most of this information may be downloaded from www.reuters.com. Registration is required.

7.8.2 Money brokers

Wholesale money brokers arrange deals in FX, money market loans and deposits, OTC derivatives and debt instruments. Sell-side firms pay them a commission for putting them into contact with investors and buy-side firms. Money brokers arrange deals by telephone, and through a variety of electronic networks and internet/intranet portals.

7.8.3 Stock lending intermediaries

Stock lending and repos are discussed in detail in Chapter 21. There are a number of specialised firms that find firms that are prepared to lend stock to those firms that wish to borrow, and they normally act as principal in these transactions.

7.8.4 Registrars and transfer agents

Where shares or bonds are issued in registered form, the function of the registrar is to keep the register updated, process corporate actions, ensure that holders receive the correct correspondence from the securities issuers, and pay dividends and coupons.

1 NYSE Euronext comprises the following exchanges:

- The New York Stock Exchange

- Euronext Belgium

- Euronext France

- Euronext Netherlands

- Euronext Portugal

- Euronext.LIFFE – based in London, this division of NYSE Euronext handles all the group’s European futures and options contracts.

2 New York-based NASDAQ is currently in merger talks with the OMX exchange that services six Nordic countries.

3 The London Stock Exchange has since acquired Milan-based Borsa Italiana.