Chapter 14

An Overview of Investment Accounting

14.1 ROLE OF THE FINANCIAL CONTROL DEPARTMENT

As its name implies, the core function of the financial control department of a business is to manage its financial resources. The department is usually headed by a main board director who may have the title of chief financial officer. CFO job descriptions vary, but are likely to include:

- Overseeing all company accounting practices, preparing budgets, financial reports, tax and audit functions

- Directing financial strategy, planning and forecasts; conferring with chief executive officer, executive directors and department heads

- Managing investment and raising of funds for the business

- Studying, analysing and reporting on trends, opportunities for expansion and future company growth.

Within the department there are likely to be the following sections specialising in different activities:

- Management accounting, also known as product control: This section prepares budgets and produces the profit and loss accounts and balance sheets for individual business units, working closely with the managers of the business units to ensure that the income and expenditure of the business units is correctly recorded, and any financial risks are measured and appropriately contained.

- Statutory reporting: This section produces the firm’s balance sheet and profit and loss account, which is then subject to both internal and external audit.

- Regulatory reporting: This section produces the financial and statistical returns demanded by the firm’s regulator. In the UK this will be the Financial Services Authority (FSA).

- Tax management: This section will be concerned with organising the firm’s activities so that its tax liabilities are (legally) minimised.

- Treasury: This section manages the company’s cash resources, and, if the company’s shares are listed on an exchange, it may be involved in decisions about raising additional capital in the form of equity or debt securities.

- Financial operations: This section makes payments to suppliers and payments of expenses to staff members, and in a non-financial company it would also control the sales ledger and credit control.

14.2 DEPARTMENTAL SYSTEMS

The department will have its own dedicated IT applications which include:

- A corporate general ledger system (section 14.3 examines the general ledger in more detail). This system will record all the assets, liabilities, income and expenditure of the firm, and is likely to include specialist modules which:

– Compare this year’s P&L to the previous years P&L, and also to budgeted P&Ls

– Allocate expenses across departments. For example:

If the firm occupies a single building and 25% of the space in that building is occupied by the settlements department, then the settlements department needs to be charged with 25% of the rent, electricity, gas, water and property taxes. The cost of the IT department itself needs to be recharged to those business units that benefit from it. There may be a number of bases for making this recharge. If, for example, there are five developers all working on an application used only by the settlements department, then the direct costs of these employees might be recharged directly to settlements. But other individuals in the IT department manage helpdesks, networks, desktop installations, etc. – from which all business units benefit – so the cost of these individuals may be recharged according to headcount – so if settlements employs 35% of all the firm’s staff, then it would be recharged 35% of all these “general” IT costs.

If the firm occupies a single building and 25% of the space in that building is occupied by the settlements department, then the settlements department needs to be charged with 25% of the rent, electricity, gas, water and property taxes. The cost of the IT department itself needs to be recharged to those business units that benefit from it. There may be a number of bases for making this recharge. If, for example, there are five developers all working on an application used only by the settlements department, then the direct costs of these employees might be recharged directly to settlements. But other individuals in the IT department manage helpdesks, networks, desktop installations, etc. – from which all business units benefit – so the cost of these individuals may be recharged according to headcount – so if settlements employs 35% of all the firm’s staff, then it would be recharged 35% of all these “general” IT costs.– Manage the firm’s purchase ledger and sales ledgers

– Translate profits and losses earned in foreign currencies into the firm’s base currency.

- A regulatory accounting system – this system will be used to calculate the financial and statistical information that the firm needs to send to its regulator.

14.3 THE GENERAL LEDGER

The general ledger, sometimes known as the nominal ledger, is the main accounting record of a business which uses the double-entry bookkeeping convention. It will usually include accounts for such items as current assets, fixed assets, liabilities, revenue and expense items, gains and losses.

The general ledger is a summary of all of the transactions that occur in the company. It is built up by posting transactions to general ledger accounts as and when the business events occur.

The general ledger is based on the principle of double-entry bookkeeping, where each transaction is recorded in at least two ledger accounts. Each transaction results in at least one account being debited and at least one account being credited, with the total debits of the transaction being equal to the total credits.

For example, if a business purchases a desk for £100 cash, then its cash balances will decrease by £100 and the value of its office equipment will increase by £100. The cash account will be credited and the office equipment account will be debited with £100. Use of the double entry convention means that the accuracy of the accounts can be checked quickly – when all the accounts that have debit balance are summed, they should equal the sum of all the accounts which have a credit balance. Without this facility there would be no quick means to check accuracy.

However, the idea that a reduction in a bank balance is a credit does confuse the layman, who is used to talking to his bank about payments being debited, not credited. This is because the bank is talking from its point of view, not its customers. The customers account is a liability to the bank, and liabilities are credit balances. When a customer withdraws cash, he is reducing the bank’s liabilities, and a reduction of a credit balance requires a debit.

14.3.1 Assets and liabilities, income and expenses, gains and losses

There are seven basic categories in which all accounts are grouped. Table 14.1 shows the seven groups together with some examples of each group in the finance industry.

Table 14.1 General ledger categories

| General ledger account category | Accounting convention | Finance industry examples |

| Assets | Debit | Market value of securities purchased interest receivableMoney due from counterparties and clientsCash in the bank accountPremises, furniture, fittings and equipment |

| Liabilities | Credit | Market value of securities sold Interest payableMoney due to counterparties and clients Overdrawn bank accounts |

| Revenue | Credit | Net interest income – i.e. interest received less interest paid Fees for client advice |

| Expense | Debit | Salaries and other employee benefits Rent, property taxes, heat, light, power, etc. All other expenses of running the business |

| Gains | Credit | Gains are profits (or increases in value) of an investment such as a stock or bondGain is calculated by fair market value or the proceeds from the sale of the investment minus the sum of the purchase price and all costs associated with it.If the investment is not converted into cash or another asset, the gain is then called an unrealised gain |

| Losses | Debit | The opposite of gains – losses arise when the investment is sold for less than the purchase price, or when the fair market value is less than the purchase price |

| Shareholders’ equity | Debit | The net value of the business to its shareholders. Based on the accounting equation: Shareholders, Equity = Assets – Liabilities |

Shareholder’s equity is the net value of the business to its owners, and is represented by the equation

![]()

Assets and liabilities are collectively known as balance sheet accounts, while income, expenses, gains and losses are collectively known as P&L accounts. Some items (such as the notional principal of swap transactions) are known as off-balance sheet items.

14.3.2 General ledger account types for securities and investment firms

Firms in the financial sector will have (at least) the following account types within their general ledger. The concept of account types is used by applications that calculate the value of transaction- and position-related entries and post them to the ledger. There will be many individual unique accounts of each type, as discussed in section 14.3.3. The account types that are referenced in this book are shown in Table 14.2.

Table 14.2 General ledger account types

| Account type | Category | Purpose of the account type |

| Security position | Balance sheet | To record the value of securities bought and sold in the firm’s trading books or portfolios |

| Security trading party | Balance sheet | To record amounts payable or receivable for security purchases and sales |

| FX position | Balance sheet | To record the value of foreign currencies bought and sold in their original currency |

| Base currency cost of FX position | Balance sheet | To record the value of foreign currencies bought and sold in the firm’s base currency |

| Money market deposits attracted | Balance sheet | To record the value of money market deposits attracted |

| Money market loans placed | Balance sheet | To record the value of money market loans placed |

| Swap notional principal | Off-balance sheet | To record the notional principal values of any swap transactions to which the firm is a party |

| Accrued interest on securities | Balance sheet | To record the value of interest due to the firm on its long security positions and payable by the firm on its short positions |

| Accrued interest on money market deposits attracted | Balance sheet | To record the value of interest payable by the firm on the money market deposits it has attracted |

| Accrued interest on money market loans placed | Balance sheet | To record the value of interest receivable by the firm on the money market loans it has placed |

| Accrued interest expense on swaps | Balance sheet | To record the value of interest payable by the firm on its outstanding swap transactions |

| Accrued interest income on swaps | Balance sheet | To record the value of interest receivable by the firm on its outstanding swap transactions |

| Collateral placed | Balance sheet | To record cash collateral placed by the firm |

| Collateral received | Balance sheet | To record cash collateral received by the firm |

| Accrued interest on collateral placed | Balance sheet | To record the interest receivable on collateral placed |

| Accrued interest on collateral received | Balance sheet | To record the interest payable on collateral received |

| Cash at bank | Balance sheet | To record the bank accounts used by the company |

| Coupon control | Balance sheet | To record any discrepancy in the value of coupons due to the company and the amount that it has actually received |

| Dividend control | Balance sheet | To record any discrepancy in the value of dividends due to the company and the amount that it has actually received |

| Corporate action control | Balance sheet | To record any discrepancy in the value of corporate action proceeds due to the company and the amount that it has actually received |

| Security fees and charges control | Balance sheet | To record the value of fees and charges (such as stamp duty and PM levy in the UK) that have been collected by the sell-side firm and need to be paid to the appropriate authorities |

| Swap gains and losses | Balance sheet | To record the mark-to-market gains and losses on swap trades |

| Security trading P&L | P&L | To record the income earned by the company from trading securities as principal |

| Security commission income | P&L | To record the commission that the firm has charged its clients for executing agency trades |

| Security interest P&L | P&L | To record the interest that the firm has earned from its inventory of bonds |

| Money market loan interest income | P&L | To record the income earned from the deposits that the company has placed |

| Money Market Deposit interest expense | P&L | To record the cost of the deposits that the firm has attracted |

| Swap interest income | P&L | To record the interest income from the firm’s swap transactions |

| Swap interest expense | P&L | To record the interest expense from the firm’s swap transactions |

| Swap P&L | P&L | To record the mark to market gains and losses on swap trades |

| Stock lending income | P&L | To record the fees earned from stock lending |

| Stock borrowing expense | P&L | To record the fees payable from stock borrowing |

| Collateral interest income | P&L | To record the interest earned on collateral placed |

| Collateral interest expense | P&L | To record the interest paid on collateral received |

| Exchange fees | P&L | To record fees charged by exchanges |

| Settlement fees | P&L | To record fees charged by settlement agents |

| Option premium expense | P&L | To record the cost of options purchased or sold |

| Option premium income | P&L | To record income from writing options |

| FX trading P&L | P&L | To record gains and losses from FX trading |

Examples of the use of account types in posting entries

Business applications use the concept of account types and trade amounts (refer to Chapter 6) to determine the money amounts that need to be posted to the general ledger.

Consider the following trade.

On 3 January 2008, ABC Investment Bank’s trading book number 1 sold 10 000 shares in Sony Corporation to Client A at £11.30 per share, for value 7 January 2008. The Bank did not charge the client commission on this trade, so the amount payable by Client A is also £113 000 – 10000 shares * £1130. As ABC purchased the shares for an average price of £11 each, it has made £3000 profit on this deal. ABC’s settlement agent is Euroclear.

The entries that will be required on trade date will be as shown in Table 14.3.

Table 14.3 Example accounting entries for a securities principal sale

The effects of these postings are that:

1. They have used the double-entry bookkeeping convention, the sum of the amounts debited less amounts credited is zero

2. They have recorded the profit as soon as it was made

3. They have recorded that a trading party – Client A – owes ABC £113 000.00

On the date that the trade settles the entries shown in Table 14.4 will be posted.

This entry reflects the fact that Client A no longer owes ABC the trade consideration, the trade has settled and the cash is now in the bank.

Table 14.4 Example accounting entries for securities settlement

14.3.3 A unique general ledger account

The list of the accounts used by an individual general ledger system is called its chart of accounts. General ledger systems used by financial firms are usually multicurrency ledgers; that is to say that each individual account exists in all the currencies that it is possible for the user firm to trade in.

Each account code in the chart of accounts is given a unique account code. Sometimes this is a number, or it may be a meaningful alphanumeric code such as “SECPOS Book1”.

In addition, user firms need to be able to see which entries apply to which individual securities, contracts or customer. Therefore, at account type level a decision needs to be made as to what further breakdown of the account postings and balances is required for each account code with this account type. The account types that were used in the example trade in section 14.3.2 of this chapter were:

- Security position: Accounts for this account type would normally be subdivided into an individual unique account for each individual security within each book, within each currency that the book trades.

- Security trading P&L: As for security position.

- Trading party: Each individual trading party would have at least one account in each currency that they have traded.

- Cash at bank: Each individual bank with whom the firm deals would require an individual account in each currency that the firm deposits with the bank concerned.

Thus the individual identities of the four unique accounts that were used in the example might be as shown in Table 14.5.

Table 14.5 Examples of unique accounts

14.3.4 Selecting the correct account to which an entry should be posted

Applications that decide to which general ledger account entries should be posted need to provide those users concerned with chart of accounts design with access to an account selection parameters table where they are able to build business rules that define:

1. Which trade amounts are posted to which account type, and to which individual account of that type

2. What further breakdowns are required.

It is not usually the general ledger system itself that decides what amounts are to be posted to which accounts. The decision logic is usually a part of the main settlement system. The exact methodology used will vary from system to system, but it is normally based on the principles described in this section.

Table 14.6 shows an example of the types of data found in the user interface to an account selection parameters table.

Table 14.6 Account selection parameters data input

The explanation of the columns is:

1. Trade amount: The money amount connected with the trade, settlement or other event. A full list of these amounts needs to be defined in the system that is performing the account postings. The way that these objects are set up and defined in applications will vary. In older applications all of the definitions may be hard-coded; newer applications may make more use of metadata that provides users with more flexibility.

2. Action: The action that is being performed (e.g. buy, sell, profit, loss, receive, deliver). Once again, a full list of all possible actions needs to be defined in the system.

3. Sign: This tells the application whether a trade amount concerned with this action, which is a positive number, should be debited or credited to the account concerned. The converse will be true for negative numbers.

4. Account type: This tells the application to which account type data in this row should be posted.

5. Breakdown 1 and Breakdown 2: These columns tell the system how account types should be subdivided to create individual unique accounts. Subdivision is usually based on a defined list of suitable external objects such as trading books, currencies, securities and trading party IDs. Once again, a full list of available objects needs to be maintained, either in a hard-coded form or by the use of metadata.

The example used in this chapter shows only two further levels of breakdown below account type, but many applications in use provide further levels of analysis. Very often a further level is used to allocate funding costs to particular business units. In the example trade that is used in this chapter, “book 1” sold the securities, and needs to fund the position until actual settlement date. Therefore breakdown 2 could be used to allocate the costs of funds to book 1.

14.3.5 A typical view of a general ledger account

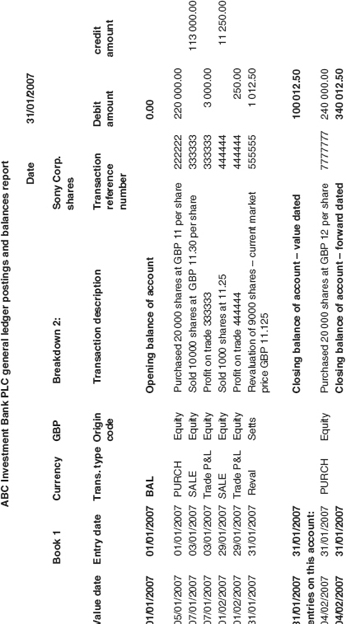

A typical enquiry or report on a unique general ledger account will look similar to the example in Figure 14.1. It will contain the following data.

Figure 14.1 A unique general ledger account

Static data items

1. The account type

2. The name of the account

3. The identity of the currency in which postings are made for this account.

Balance information items

1. The opening balance of the account

2. The date of the opening balance

3. The closing balance of the account on a value dated basis – this includes all postings where value date is equal to or earlier than the current date

4. The closing balance of the account on a forward basis – this includes all activity including those in (3) and also including those where value date is in the future

5. The date of the closing balances described in (3) and (4).

Transaction information items

1. The date that the transaction was carried out (business date)

2. The date that the transaction is expected to settle (value date)

3. The date that the transaction was entered into the general ledger system (entry date)

4. The money value of the transaction

5. A description of the transaction

6. A code to represent the type of the transaction (e.g. securities purchase, FX sale, etc.)

7. A “configuration origin code” – this tells the user of the general ledger which of the many systems in the configuration produced the transaction

8. A unique transaction reference number – ideally this reference number will be used by all the systems (front office, back office and FCD) that have recorded this transaction. This number should be meaningful in context. For example, if the user is looking at a general ledger account for a nostro account used for settlements, then the most useful transaction reference number for them to see is probably the unique instruction number that was described in section 12.2.7.

14.3.6 Posting errors and their possible causes

Because both the trade amounts and the account selection decisions will normally have been calculated by systems other than the general ledger system itself, dealing with a support call from a user of the general ledger application that is querying the amount of a posting (or indeed the lack of a posting or duplication of a posting) to a particular account can be complex. For example, consider the nature of this support call:

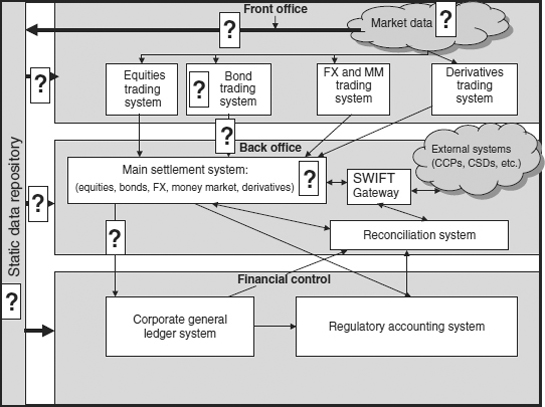

I am looking at the security interest P&L account for book 1. For the past 10 months we have had the same bond portfolio, and the interest income has always been in the region of $100 000 per month. This month it is only $20 000.

Now look at the configuration diagram in Figure 14.2. A number of applications, services and interfaces between applications play a role in generating posting entries concerned with bond interest, and the error – assume that it is a genuine error – could have occurred in any one of them. The applications, interfaces and services that are concerned with bond interest are highlighted by question marks.

Figure 14.2 Where did the error occur?

And the cause of the error could include any one or more of the following:

- Human (data entry) errors, such as entering:

– Buy instead of sell

– Wrong stock

– Wrong party

– Wrong SSI or other static data

– Etc.

- Technical errors including:

– Interfaces that don’t run/run twice/miss items out/duplicate data/run late

– Incorrect static data obtained from an external information source

– Systems that can not perform accurate trade computations/mark-to-market/interest accruals.

Because of the complexity of such a help desk call, it is recommended that general ledger reports and enquiries – such as the one illustrated in Figure 14.1 – always contain:

- The ID of the system that created the entry – the configuration origin code

- Meaningful – in context – transaction reference numbers

- Meaningful descriptions of entries

- The entry date of the entry – normally this will be the same as trade date, value date or settlement date – whichever date applies to entries of this type – but because of processing errors on earlier dates sometimes entries are passed late.

Effective, timely and comprehensive internal reconciliations between applications (as examined in section 23.11.2) can also be used proactively to detect problems of the sort that the user was reporting in this example.

14.3.7 Profits and losses in foreign currencies – translation into base currency

Any firm that invests in securities or other instruments that are denominated in foreign currencies will earn some of its profits, and incur some expenses in those currencies. As part of the accounting process, these P&L items need to be translated into its base currency at regular (usually monthly) intervals. If they are not translated, then their base currency value will fluctuate according to the exchange rate. This is known as translation risk, which is also covered in section 24.1.

The general ledger application usually contains specific functionality to automate the translation. At the end of the period defined by the user firm, accounting entries are passed that have the affect of reducing the balance of all the P&L accounts denominated in non-base currency to zero. The opposite entry debits or credits the sum of all the balances for that currency to a single balance sheet account.

Simultaneously, entries are passed that create the base currency equivalents of all the P&L accounts affected, using the exchange rate of the day. The opposite side of these entries is a single balance sheet account.

Consider the example in Table 14.7. ABC Investment Bank has a base currency of GBP and the following non-GBP balances in its P&L accounts.

![]()

Table 14.7 Non-base currency P&L balances

After the automated translation process has run, the balances for each currency will be as shown in Table 14.8.

Table 14.8 P&L accounts after the translation

The firm now needs to carry out FX deals for the FX translation account to sell USD 10000.00 and EUR 5000.00 and buy CAD 15 000.00 for GBP. The base currency cost of these deals will be in the region of GBP 1190.48. If there has been a movement in the FX rates between the time that the translation entries were passed and the time that the deal is executed then there will be a further profit or loss on these deals.