CHAPTER 10

Growth, cycles and the econosystem

Getting in touch with the network of minds.

Previous chapters in part II explored the traps that are holding you back from being free. This chapter will give you a glimpse of life outside the Income Trap, free of short-term thinking. When you are free of the nine to five, when you don’t need to go to work tomorrow to put food on the table, what does that look like? Why is that so important, and what are you free to then do? You are free to grow, to look for opportunities instead of short-term fixes, to get in touch with the econo-system and to tap into the power of the network of minds. Live each season as it passes; breathe the air, drink the drink, taste the fruit, and resign yourself to the influences of each. Henry David Thoreau Whether it’s shares, property or business, in this chapter we’ll explore how wealth is created, and how being in touch with, and aware of, the seasons of money can make you rich. What is ‘wealth’? It takes two minds to create wealth. One free to create, the other free to value. Matthew Klan Seems like a pretty important question to ask if you want to get rich! But, too often, we spend years of our life aiming for something without really understanding what it is. Well, if you get right down to it, wealth is an emergent property of the network of minds. What does that mean? Simply, that wealth doesn’t exist without humans. Wealth is something we create in our minds. It can seem like wealth is ‘something out there’: assets, gold — tangible stuff. But if all the humans disappeared off the face of the earth tomorrow, all ‘wealth’ would evaporate too. Even though there would still be gold in the earth, it would have no ‘value’ without people to give it value. In the 20th century we saw some simple-looking formulas that have explained complex phenomena — such as E=mc², which describes the relationship between energy and mass. But more than that, the application of these simple formulas has unleashed tremendous energy. If you are a budding wealth creator or entrepreneur and you’d like to unleash the unlimited energy of your mind to create wealth, then the one formula you need to know is what I call the ‘Freedom First Wealth Creation Formula’. 1 mind free to produce, multiplied by 1 mind free to value = wealth creation Like E=mc² this formula looks pretty simple. But can it tell us anything useful? Let’s break it down and change some variables to see what we learn. You might remember from school that if you multiply something by zero, you get zero. So, if you have one mind that produces something but there are no other people to value what you’ve produced, you’ve created zero wealth. 1 mind to produce × zero minds to value = zero wealth Imagine you are Robinson Crusoe and you are stranded on an island. You may build yourself an awesome treehouse, but have you created any wealth? No. But you have created something of value to yourself. This teaches us an important lesson: Do what you love, that other people will value. Do what you love, that other people will value. Often, in this era of unlimited choices, we are told: Do what you love! While on the face of it, this sounds nice, I’m often reminded of our ancestors who lived in small villages, where every day was a struggle for survival. The choice of careers for most people throughout most of history was very limited, but they still managed to find meaning and purpose in what they did. I remember growing up, being told ‘You can’t make a living playing computer games.’ Well, the truth is, we are so fortunate today that you actually can make a living playing computer games! (In fact, the top two YouTubers of 2017 both ran video game channels, making $16.5 million and $15.5 million respectively.) It’s a great idea to do something you love: in part III I’ll show you how to turn a hobby or a skill you didn’t know you had, into a business that can set you free. But even the guys who play computer games for a living know that the other half of the Freedom First Wealth Creation Formula is important too: you need to do something that other people value. These YouTubers are not just doing what they love; they are filming, editing and narrating their gameplay so that other people can value it too. What if we play around with the formula some more? zero minds to produce × 1 mind to value = zero wealth Just like before, multiplying by zero gets us zero. Of course, there are not too many situations I can think of where there are zero producers in real life. But this does illustrate an interesting point: in the modern world we have the balance between producers and consumers completely out of whack. Everywhere you look, we are being encouraged to consume, consume, consume. In some cases we’ve become such sophisticated consumers, some people are afraid that what they produce could never meet their own high standards, so they never embark on a creative endeavour. On the production side of the equation, small producers are being gobbled up by bigger producers flush with cash in this easy money economy, which ultimately decreases the number of producers in total. Governments love consolidation of producers too — a few big businesses are easier to regulate, control and hand out favours to. That’s why you see so many big businesses down with whatever is the latest political trend. You didn’t really think your bank cared about the environment, did you? While we are all consumers by default, if we want to balance the wealth-creation equation and unleash prosperity, we need to encourage people to produce. A society with only a handful of producers who think in lockstep and aren’t really free to produce, plus a population reduced to being consumers, is not a winning formula. In the modern world we have the balance between producers and consumers completely out of whack. While people do technically produce at least as much as they consume (unless they are in debt or receiving welfare from state or family) their habits and thinking are defined overwhelmingly by consumption because it is as consumers that they are free to make the most choices. We have seemingly unlimited choices of things we can buy, see or do with our money. But, by and large, what people produce is decided by someone else: a boss, a teacher and so on. (This is where the ‘free to produce’ part of the formula is important.) When we consume, we get in touch with the network of minds. We form the yin to the yang of wealth creation: someone else creates a product or service freely, from their mind, then as consumers we are free to choose to give value to their creation — we decide what we are prepared to pay, and whether we value the new creation enough to buy it at all. But that is only part of what creates wealth, and it really is the secondary part. So when it comes to creating wealth, thinking predominantly as consumers makes us run the risk that we will view ‘getting rich’ like we view everything else — as something to ‘get’. We want to consume our way to wealth! Think like a producer Wealth isn’t created by consumers. Consumers value the products that producers create. If they find no value in them, then no wealth is created, but if producers don’t produce something to value in the first place, there can be no wealth either! A consumer-minded investor ‘buys’ a property, for example, because they believe it is the best purchase they can make and it will be better than other purchases such as shares. A producer-minded investor, however, thinks about what they have the skills and experience to produce, and also what others will value. If the property market is in a downturn, the consumer-minded investor may be fleeing the market, while the producer-minded investor may see that while people are not paying up for the standard three bed/two bath property, they still need to live somewhere. Maybe people will choose to rent more, and smaller units will do better held for cashflow instead of capital gain. The producer-minded investor may extrapolate out and realise that more renting might lead to more need for storage between moves and invest in storage units instead. They might take the large house that has fallen in value and convert it into several dual key residences, for example. They will be aware of the changing needs of the market because they are in touch with the market. When you put on your producer hat you begin to think ‘What will other people value?’ The more you can tap into what other people will value, the more wealth you create and the richer you become. There are two ways to tweak the Freedom First Wealth Creation Formula to increase the wealth you create. The first way is to increase the multipliers by: The second way is to increase freedom, which is an important part of the formula. It takes two free minds to create wealth. As well as increasing the number of producers or consumers in the formula, we can increase the freedom each has to perform their roles. This can be done by: Finally, you’ll notice one thing that’s not in the Freedom First Wealth Creation Formula: cutting costs. Finding better, more effective ways to deliver your product or service may be boring, but it can be a legitimate part of ‘producing’ when it comes to creating wealth. If you create a better system for delivering the same product and level of service to your customers, then you are creating something new that’s of value, but if you just cut corners to cut costs, you may increase profits in the short term, but you’re not creating wealth. Finding ways to artificially drive down the costs of labour to keep unproductive businesses chugging along is not only as old as slavery, but it’s a sure sign that a company, or a country, is no longer able to create and thrive. Now that we’ve introduced the concept of the network of minds, we can pull back and look at the bigger picture: what happens when you take the small nodes and local connections we’ve looked at so far, and scale up to the entire world? The network of minds starts looking like an organic system, an ecosystem of wealth creation that I call the econo-system where billions of people make trillions of connections with each other, and just like nature, this econo-system has seasons and cycles to it, and being aware of the organic nature of wealth creation — being aware of these cycles — can make you money. Many people are aware of consumer cycles: we’ve all heard of winter sales (though how many people plan ahead based on such sales, as opposed to just using them as a pretext for buying something now, is up for debate). There are even weekly cycles you can track for things like the price of petrol. But cycles exist in more than just consumer products. Cycles exist in markets too: in stocks, property and business. Probably the biggest cycle that affects all markets, is what I call the lifetime cycle. The lifetime cycle can be understood broadly as the study of demographics. Seen as a group, people do similar things at similar times throughout their lives, on average. We all go to school at the same age; we start our first jobs at similar ages, get married, buy a home, earn more, have kids and save for retirement at roughly predictable stages throughout our lives. These consumer spending cycles allow us to predict what people will be doing and spending at different ages. Earlier, in chapter 8, I told you that it wasn’t debt so much as demographics that allowed me to predict that there would be a significant downturn at the end of the decade. The problem with credit default swaps and the debt bubble itself was just a proximate cause. It turns out that in the United States and other first-world countries we have an ageing population. What that means is that there are more older people than younger people. Now imagine the average older person: are they moving into bigger and bigger houses as their family grows? No, those years are behind them and they are instead likely looking to downsize their homes now that the kids have left and they’re getting older. Entering retirement, people not only earn less money, but they often spend less too — except in some areas, like healthcare. So it was relatively easy to predict that the baby boomer generation, which was the largest generation in history (especially compared to the preceding generation, which created a wave-like demand effect as it passed through each stage of life) upon reaching retirement, would have a big impact on many sectors of the economy. We saw not only the price of houses fall, but the cost of healthcare soar. People tend to look back on their life in terms of decades: their teens, twenties, thirties and so on. It seems natural for us to think and plan in decades and it turns out that businesses are no different. Businesses tend to plan aggressively for the decade ahead, expand, then once a new decade rolls over they tend to take stock and consolidate. Each decade has been marked by different trends in fashion, music and so on, but it takes time for everyone to decide what the next cool thing will be — what this decade is going to be about. Since it’s businesses that sell the fashion and the music, they tend to tread water at the beginning of the decade too. That’s why, in the stock market, another name for this cycle is the decade hangover cycle. From 1900 to now, only one half of every decade has been responsible for nearly all the gains in the stock market for that 10-year period. It’s usually the mid to later years of the decade (1995–99 and so on) that see most of the gains, while the first couple of years of the decade tend to be flat. In fact, almost 40 per cent of the entire gains for the decade tend to happen in the ‘5’ years, on average. You’ll also notice that the ‘7’ years also tends to have a negative return. If you’d simply stayed out of the market in the first two years of each decade, and also skipped the last part of each ‘7’ year, you could have avoided some of the worst corrections and bear markets in the past 100 years (1907, 1920–22, 1930–32, 1937, 1940–42, 1960–62, 1980–82, 1987, 2000–02). The GFC, of course, also had its start in late 2007. (If you’d stayed out of the market from 2000 to 2002 and then got back in, you would have caught one of the biggest booms in history from 2003 to 2007. When the market fell from late 2007 through 2008 it ‘only’ fell back to where it was at the end of 2002.) The decade following the GFC didn’t follow this cycle closely, but then it wasn’t exactly a ‘historically normal’ period of time following such a once-in-a-lifetime correction. Often it takes one such ‘substandard’ cycle to pass before the pattern re-asserts itself again. So we’ve looked at cycles that span years, but there are even predictable cycles within each year, with certain times of the year reliably performing better on average than others. Just as we saw that the vast majority of the gains each decade come from only half of the decade, it turns out the majority of the gains each year come from only a handful of months. The worst months each year tend to be February, June and October in Australia. (They tend to be February, May and September in the United States.) According to the Hirsch Organisation (www.stocktradersalmanac.com/Strategy.aspx), investing for just the half of the year that has the best months — 1 November to 30 April (February corrections tend to be mild compared to the other two negative periods) — and missing out the worst months, you could have turned US$10 000 invested in 1950 into US$467 103 today, instead of losing US$77 if you’d only invested in the other half of the year! Just as the decade cycle was based around businesses spending, the yearly cycle seems to be based around other predictable activity too. There is a saying in the market: sell in May and go away. May/June tends to be a negative time in Australia because individuals and fund managers tend to sell their losing stocks before the end of the financial year to lock in a tax deduction. Some mutual funds have their redemption dates or their fiscal years ending in autumn in the United States, which coincides with the yearly September/October period for corrections. However, this only explains a portion of why September and October tend to be historically bad months: some of the worst crashes in history have happened at this time and even stock markets can get superstitious sometimes! Not only do markets respond to when companies plan and spend money, they also react to when governments may spend money. In the United States there is a fixed election cycle of four years and another stock cycle can be observed in response to this. When a president is heading for re-election, starting in the third year of his term when the campaigning really kicks off, the markets expect and often receive a boost from all the promises of extra spending from both candidates. On average, 88 per cent of the time, the third year of a presidential term sees an average stock-market return of 16 per cent that year. The first two years of the next term often experience a ‘hangover’ as the reality of all the promises sets in. Civilisational cycles The last few cycles we’ve covered were stock specific, but of course there are many more cycles that affect all sorts of things — all the way up to civilisational cycles. We certainly are living through historically significant times! Alexander Tytler had a theory of civilisational cycles that says nations pass through predictable stages in their progress from growth to decline: ‘From bondage to spiritual faith; From spiritual faith to great courage; From courage to liberty; From liberty to abundance; From abundance to selfishness; From selfishness to apathy; From apathy to dependence; From dependence back again into bondage.’ This further supports the notion that there is a link between freedom (or liberty) and wealth (or abundance), while reminding us that valuing freedom or liberty takes courage and is something that has to be nourished or it will be forgotten. Now, using what we’ve just learned about cycles, you can see how I was able to predict two major events that many people felt were unpredictable well in advance. Using the decade cycle we can see that if there has been a correction at the end of the previous decade, the first two years of a new decade are likely to be flat. From 2000 through 2002 markets trended sideways as we recovered from the Tech Wreck. Knowing that the baby boomers had a few good years in them before the oldest would start to retire, it wasn’t hard to see that the next few years from 2002 onwards would see good growth — possibly great growth. Looking ahead with the decade cycle in mind I knew to be wary of late 2007 (the yearly cycle supported this too), but if the boom didn’t bust then, we might have had until as late as 2010, which would be closer to the boomers retiring. Therefore, to my mind, 2003–07 at least would be a fantastic five years to make hay while the sun was shining. After the GFC, a historic correction, the next 10 years would not be so easy to predict. My best guess at the time was that this would not be a correction we’d bounce straight back from; we could easily see a decade of flat growth following it. No amount of stimulus would make up for the decline in consumer spending, and in fact that stimulus would only increase the gap between the rich and the poor. And sure enough that was what we saw, a decade of stagnating wages and flat growth, while assets in the United States at least were eventually reinflated. But aside from the price of stocks, big corrections have other, more important effects. Sometimes stock corrections trigger recessions, even depressions. And these affect the average person more than the changes in the price of stocks, as most people are employees and not full-time investors. Stocks falling might hurt their future retirement funds, but losing their jobs affects the food they are putting on their tables now. In fact in the years that followed, it was these larger effects that to me became easier to predict than the market itself. After the bankers had seen their businesses saved, and Wall Street and rating agencies had gotten away without a single person held accountable, cracks had started appearing in the system. At the time of the GFC, the bank bailouts were opposed by 75 per cent of all voters, regardless of party. After the Great Depression in 1929 there were huge changes in geopolitics. Wasn’t it obvious that coming out of the GFC, a financial crash of historic proportions, as well as the decade after it, during which the average voter was still feeling the effects of the crash, would make political change more likely, rather than less? The 2016 US presidential election was regarded by many to be one of the most historic and unique elections in living memory — and also the one that the greatest number of people failed to predict. Looking back though, it surprises me that anyone was expecting things to continue along the same path. At the very least, people should have expected some change. The movement that came to be known as Occupy Wall Street, for example, should have alerted people that business as usual wasn’t going to be tolerated for long from either side of politics, especially when, for the 2016 election, it looked like the two major parties were planning to offer the electorate Clinton versus Bush Round 2 — the definition of politics as usual. Predicting elections While the smartest way to take advantage of a presidential election may be to hedge your stocks accordingly based on the four-year presidential cycle, what most people are interested in is can the elections themselves be predicted? Two of the most accurate predictors of presidential elections are independent models by Professors Allan Lichtman (30-year track record) and Helmut Norpoth (20-year record), which take into account things like: Has the same party held the office of president for two terms? Is the economy good or bad? These models ignore all the usual things you are supposed to think are important — such as polls and policies — and in fact just these two factors (incumbency and flat economy) by themselves heavily favour the challenger to win. But, larger political cycles aside, what also encouraged me to take a position on the 2016 election was what investors call a ‘market mispricing’. Stock markets and other markets rely on good, accurate information to help people judge what an asset should be worth. Sometimes, for various reasons, the markets get bad information. This bad information leads people to value something for less (or more) than what it should be worth. When this happens, it’s often not long before the correct information gets out and the asset moves back up in value to a price that more accurately reflects what the asset should be worth. Think of a property that everyone says is full of mould, is falling apart, and there’s a rumour that it’s about to be condemned: all this information would cause people to put a low value on it. But once people actually go and look at the house, maybe run it by a building inspector, and find out that there is actually nothing wrong with it, the price should shoot back up. So what I noticed occurring with the Trump candidacy was what I considered a market mispricing. News outlets had Trump’s chances at winning the primaries, and the election, at irrationally low odds. I planned to take advantage of that by placing a ‘trade’ prior to the conclusion of the primaries. I was sure that once Trump won the primary, people (the media) would finally realise his real chance of winning the election had to be close to 50 per cent — after all there are plenty of people on both sides who will vote for whoever the ‘official’ candidate is, as long as they have the R or D after their name — at which point, if I wanted to, I could have made a nice profit before the election was even held, by selling the contracts that had been mispriced early on, for closer to their ‘true’ value. But rather than reflect this, the polls and the markets stubbornly kept Trump’s odds low. Some had him at a 5 per cent chance of winning after he won the nomination. This was insane. But it was the kind of insanity I was familiar with leading up to the GFC. Rationality had been banished, emotions and wishful thinking took over and a bubble of disbelief was created from every news outlet, keeping his odds low and necessitating that I hold my position. In the end, I made $100 000 from predicting the ‘unpredictable’! The strangest thing about the whole experience for me wasn’t the worldwide media attention I received as a result of the trade, but the angry reaction of some people. These were people who knew that I had predicted the housing crash years before, and even profited from it, without for a second feeling like I caused it. We are living through revolutionary times and, looking forward, I predict that things are going to get crazier before they get calmer. Old political labels will become meaningless. This period of division will resolve, however, and a new equilibrium will eventually form. These political re-alignments happen quite regularly throughout history, but it can be hard to recognise it’s happening after a lifetime of familiarity with the same two major parties. Whatever your political views are right now, this message is for everyone: as the world changes around us everyone deserves a chance to be financially free, to live their best life and to make their own highest contribution. If liberty means anything at all, it means the right to tell people what they do not want to hear. George Orwell I suggest you don’t spend too much time at first worrying about multi-decade, political or civilisational cycles: in fact, getting lost in the big picture is a distraction if your mental horizon is consumed by the short term — if you are living pay cheque to pay cheque. Get started noticing trends You don’t need to be able to predict a once-in-a-lifetime correction to profit from an awareness that there are trends, cycles and seasons to the econo-system. Realising that your industry might be changing, that the era of reliable retirement pensions is ending and that higher education does not guarantee the prosperity it once did are all trends to be aware of that can greatly impact the course of your life. In chapter 9 I shared with you the covered call strategy, which in some ways is the ‘perfect’ almost-passive income strategy. At least that’s how it’s often promoted. I prefer to think of it as an active income strategy, or better, an active dividend strategy. In certain situations, it pretty much is a risk-free way to actively generate some extra income from an asset with very little time — and far less money outlaid than for an investment property, for example. The way writing covered calls works is this: if you own 100 shares in a company, you may be able to write a covered call against them. We learned earlier that when someone buys a call option they are buying a contract that gives them the right (but doesn’t obligate them) to buy a parcel of shares, at a given price, for a set period of time. The reason they would do this is because they believe the shares are going to rise in value, and they’d like to ‘lock in’ a price they can buy them at in the future, if they go up. If they don’t rise, at least they haven’t forked out a lot of money to buy shares that then fall in value. You can buy these contracts through a broker in the same way as you buy shares. However, if you are someone who owns a parcel of shares, you might want to write or ‘sell’ these contracts to buyers, giving them the right to possibly buy your shares in the future, in exchange for some ‘rental’ income right now. Again, although this sounds tricky, it is something you can just get a broker to do for you. When you ‘write’ an option (you don’t have to actually write anything, you just choose one) you can choose how long the option will last for, what price it will allow someone to buy your shares for and how much you want to sell it for. If you own shares that are worth $10 today, that you’d be happy to sell if they ever go up in value, you might ‘option’ your shares for $11, and pocket perhaps a couple of hundred dollars of income for doing so. On some shares you can do this each month. Each month that your shares stay flat, you keep the income and the option expires. If your shares go down, well, at least earning some income helped offset that. If your shares do rise in value, say above $11 by the end of the month, you may be ‘forced’ to sell them. (You don’t have to sell your shares; you can always simply buy back the option contracts you sold, however this may cost you more than you got paid for the contracts initially.) After the month has finished you can write another option the next month, perhaps at a higher price if the shares have risen. Imagine being able to generate 0.5 per cent, even 1 per cent, of income per month. That would be an extra 12 per cent return per year — on top of the dividends you already receive! Some people go so far as to claim you can generate even more per month (you can, but there is a cost to this which no-one explains). The hidden risk with this strategy is that it could cost you some growth: markets move in cycles and most of the gains that occur even in good years tend to happen in the space of a few months. If you are forced to sell your shares (that were worth $10) when they rise in value, you might be selling shares for $11 that have actually risen higher than that in value. For some passive investors who are perhaps well into retirement, this doesn’t bother them: they are happy to receive the extra income from writing options, as well as the capital gain that results from selling their shares for a little higher than what they were worth. But everyone else who wants their money to grow over the long term should be aware of this. Because this ‘cost’ is invisible (while the income is visible) most people never notice it. What bugs me is that some people sell this covered call strategy as a passive income strategy, appealing perhaps to people stuck in the Income Trap, when with just a little awareness this can actually be a much more profitable active income or active dividend strategy. Pitfalls of being passive The worst part is when these people appeal to greed and advertise that you can make 1 per cent, 2 per cent even 3 per cent per month! You can make more money from writing covered calls, the more ‘in the money’ you write them. When you are giving people the right to buy your shares for $11 — as in our example (while your shares are currently worth $10) — you are writing what is called an ‘out of the money’ covered call. The share would have to rise above $11 for you to get exercised (and have to sell your shares). You can make higher rental returns, though, if you instead write an option that is ‘at the money’ or ‘in the money’, giving someone the right to buy your shares by the end of the month for $10 or even $9*. However, encouraging people to do this passively every month just means they will get exercised and forced to sell their shares all the time. Staying stuck in the ‘income’ frame and trying to increase your returns in this way will just end up costing you money. *If your brain is going ‘Hang on, who would want to sell the rights to buy their shares for less than what they are currently worth?’ stop right now — don’t panic, you don’t need to understand this. This is just an example of how we can apply principles we’re learning to even ‘sophisticated’ strategies. The truth is though, that this stuff is much easier to learn than you’d think, and I’ve successfully taught many people to get their heads around these concepts in a matter of days. We saw earlier that a share strategy that involved buying shares and holding them during the best half of the year, and selling everything and sitting out during the worst half of the year could be a very profitable use of an awareness of cycles. However, it would involve the transaction costs and tax costs of selling all your shares every year. By using options instead, you could write ‘in the money’ call options, ‘renting out’ your shares for much higher premiums only during the months that the market is likely to be flat or declining, and abstain from writing calls during the months the market is likely to rise — maximising your earnings, while minimising the chance you may have to sell your shares and miss out on growth. You could even add to this strategy by going the other way and writing puts during the best months of the year, when it’s most likely shares will rise! (I haven’t even touched on writing put options. We discussed how you might buy a put option to insure your shares, but did you know that you could write a put option and get paid money to buy shares? Once you start learning this stuff, the possibilities are endless.) By unplugging your mind from the Income Trap, becoming aware of seasons and taking a more active approach to generating income, the covered call strategy can be an excellent way for you to actively generate extra returns from your shares, without giving up the growth. Don’t worry if this section seems confusing at first: what I wanted to show with this example is that straight line thinking and the allure of passive income, can blind you to growth, while an awareness of cycles can see you generate higher active returns without giving up your growth at all. Why is this so important? Well, first we need to understand the power of growth, as well as take a glimpse into how billionaires think about growth, which those stuck in the Income Trap can learn from. The stories surrounding chess go back almost as far as the great game itself, which current estimates place at over 1400 years. From the earliest days of chess it was more than just a game; it was also a teaching tool that captured people’s imaginations, and was often used as a metaphor to help transmit complex ideas, such as the power of growth. One chess story from India involved a king and a travelling sage. As a gift to the king, the sage invented for him a novel new game called chaturanga, or what came to be known as chess. So impressed was the king with the new game that he offered the sage any reward he could name. The sage thanked the king profusely and said, ‘All I would ask of your majesty is a single grain of rice for the first square on the chess board, two grains for the second, four for the third and so on — doubling each square.’ At first the king thought this too modest a request, but the sage insisted and being a man of his word the king assented to the request. However, he quickly realised that he could never fulfil it. After doubling for several squares the amount quickly grew so large that all the rice in India, and indeed the world, would not be enough to repay the debt: the 20th square alone would require 1 000 000 grains of rice, and the 40th square 1 000 000 000 grains. By the 64th and final square the king would have to have given the sage over 18 quintillion grains of rice, more than enough to cover the entire surface of the earth several inches deep, or enough to create a pile of rice larger than Mount Everest! Just as the king was trying to think of how he could repay his debt (or have the impudent sage killed) the sage revealed himself to be Lord Krishna himself, who told the king he could repay his debt over time. And so the tradition of serving Paal Payasam to visiting pilgrims was said to have started, and the immensely powerful concept of exponential or compounding growth was also illustrated in a way people could understand. If anyone should understand the power of growth, it’s PayPal co-founder Peter Theil. Peter is not only famous for starting PayPal, he was also the first outside investor in Facebook, buying a 10.2 per cent share in the company for $500 000. He later cashed in the majority, but not all, of his holdings for over $1 billion. His success as a venture capitalist in Silicon Valley is legendary. A character called Peter Gregory in the hit TV series Silicon Valley was even based on him and his unique approach to investing. So, considering Peter’s skill at growing a small company into a giant, and spotting other seedling companies that were about to grow huge, I found his answers to the following questions quite revealing. Peter did an ‘AMA’ or Ask Me Anything session on the website Reddit where, for a few hours, he fielded questions from all over the internet. One user (called ‘papabearshoe’ — where do they get these names from?) asked him what was the worst investment he’d ever made and what lessons he learned from it. Now, if you are like most people you would expect Peter to answer with an example of an investment that lost him money. But here’s what he said: Biggest mistake ever was not to do the Series B round at Facebook. What Peter is saying here is so important if you want to understand the power of growth. The worst investment he ever made was not something he invested in that lost him money — or even an investment that he didn’t make. We all can look back at investments we should have gotten into. No, the biggest mistake he ever made in investing was not to take the opportunity to invest more money in Facebook when he had the chance to, in the second round of funding. Most people would be happy turning half a million into well over $1 billion dollars, which is what Peter did with his first-round investment in Facebook. But by not adding to his initial investment, he missed the chance to multiply his money more than 2000 times. How many failed investments could you do where you lost 100 per cent of the money you put out there, if one investment grew your money over 2000 times? That one missed opportunity was as costly as doing thousands of investments where he lost 100 per cent. But as humans we are prone to want to avoid losses at all costs, and we find it hard to wrap our straight line thinking brains around the power of growth. Another user called ‘byalik’ asked Peter what had been the most difficult mental barrier to his success. Peter answered: Even when one understands that exponential growth and exponential forces are incredibly important, it is still hard to internalise this. At the time of the launch, PayPal was growing at 7 per cent per day. Peter continued: We did not fully fathom the rocket we were riding. Growth is far more powerful than loss. What Peter understands is that if you plant a seed, and it doesn’t sprout, you’ve only lost a seed. But if you plant a seed and it grows, it can grow into a mighty oak, a million times the size of the little seed it came from. We referred to this, in chapter 8, as optionality: the ability to put a small investment — of your time, or your money — into something where what you have to lose is limited, but what you stand to gain is potentially unlimited. The heart of optionality, the secret to how it works, is the power of growth. If you’ve ever read a financial planning book, you might recognise this ‘power of growth’ as a concept called compound interest. The best investment you can make is in yourself! But compound interest is simply one example of the deeper law of growth. In fact, applying the power of growth to savings, while you work a job your whole life and never touch the savings (you have to start early to really see a good effect from this) seems to me to be the least exciting way you can harness the power of growth, and the most boring way to tap into the power of savings too! Rather than rely on your money growing passively while you work to feed it, there are much more direct ways you can tap into the power of growth: out of all the possible assets you could have, the one that has the most potential to grow is you. The best investment you can make is in yourself! Dr Carol Dweck of Stanford University believes that most people adhere to either a fixed mindset (where they mistakenly believe that their abilities are fixed) or a growth mindset (where they believe they can grow their capabilities by way of effort, struggle and failure). While I don’t agree with Dr Dweck that we can sort people into either a fixed or growth mindset, I do think that there is tremendous power in opening your mind up to opportunities and possibilities for growth. In fact, if exposed to the right conditions, anyone, regardless of mindset, can and will begin to grow. For example, most people have experienced how much you can learn and how rapidly you grow the first year in a new job or business. If you want to unlock your potential to grow, it can be as simple as getting freer first. Get free of your comfortable rut, put yourself in a position to grow and connect yourself to the network of minds. … if exposed to the right conditions, anyone, regardless of mindset, can and will begin to grow. Why is it so important to have a growth mindset and be open to learning new things and growing? Because wealth isn’t earned, it isn’t found — it’s created, and grown. Plugging into the econo-system Being aware of cycles is one thing, being in touch with them is another. Matthew Klan The final trap that comes from not being free is the ‘lack of feedback trap’. You don’t get the same feedback from the network of minds when you are insulated from it by the boundaries of your job. You may work with customers, but the network of minds includes all the producers, suppliers, customers and clients that the business you work for deals with. As an employee, you may listen to what customers tell you, but it’s not until you can measure all the costs and see for yourself what customers are prepared to pay for that you will truly know what they value. Lack of feedback extends to the cycles and seasons of the econo-system too. Jobs, salaries and passive investing all shield us from direct and timely feedback from the market. While we are all aware of the seasons in nature, there is a reason why you should ask a farmer what the weather is going to do, and not an office worker. David had become freer to produce. His boss had put him on commission, because he was often sick and had missed so much work that he didn’t want to pay him a regular salary. But the freedom that came from being able to control how much he worked had unleashed the fire in David. Not only was he making more money than before, but his illness had stopped flaring up so often. However, this new productivity came with a cost. David’s boss started to get almost resentful of the money he was making (despite the fact that he was making the business more money too). Clients were coming to the shop and asking for him by name. His boss started to pay him later and later. Things were coming to a head. Would David retreat from his new freedom back to a salary, perhaps with another boss? Or would he double down and shoot for even more freedom now that he’d had a taste of it? One day the decision was taken out of his hands, and David lost his job. Realising that his security (or at least the illusion of it) was gone, initially created a panic — over the course of a weekend David got busy registering a business name, cleaning out an office under his house, and on Monday he picked up the phone with trepidation and made his first ‘sales call’: someone he’d done good work for repairing computers in the past. He later told me how terrifying that first call felt, but it was a success — he landed some work and his first client. David didn’t do everything perfectly at once. But what’s amazing was how something simple — getting free and getting in touch with the market — actually started to lead him in the right direction naturally. At first he had done what many people starting a small business do: he started out as a generalist. (When you are not used to living outside the Income Trap it’s tempting to want to try to be all things to all people to get as much work as possible early on. In part III we’ll look at why you want to specialise so you can systemise.) But then something interesting happened: the market told David what to specialise in if he wanted to prosper. In his old job, David had done the work that the boss had given him. But in his own business, David was in touch with the network of minds. He knew first-hand what it was that consumers were willing to pay for, and what he could produce with other suppliers at the lowest cost. More and more people came to him wanting to get their mobile phones fixed, and the computer repairs he was initially doing took a back seat. The market had led him to find a niche business. Maybe it was because of a downturn that more people were repairing rather than upgrading their phones; maybe it was because the constant increase in features that phones had had since smart phones first burst onto the market, was reaching diminishing returns. The point is, David didn’t sit at home while working a job, researching current trends in an attempt to predict what the next niche business would be before starting his business. He started his business first, and got connected to the network of minds. With a mind open to growth opportunities, he let the market tell him what to focus on, and it told him to specialise. And that’s when his business really took off. A Quick Recap There is a ‘nature’ to the economy that being stuck in the previous traps can isolate us from. Getting in touch with the network of minds, applying the Wealth Creation Formula, and observing and responding to the cycles and seasons of the econo-system can unlock our potential to grow and to find what we love doing that other people will value.

The Freedom First Wealth Creation Formula

Using the Freedom First Wealth Creation Formula

Cycles

Lifetime cycles

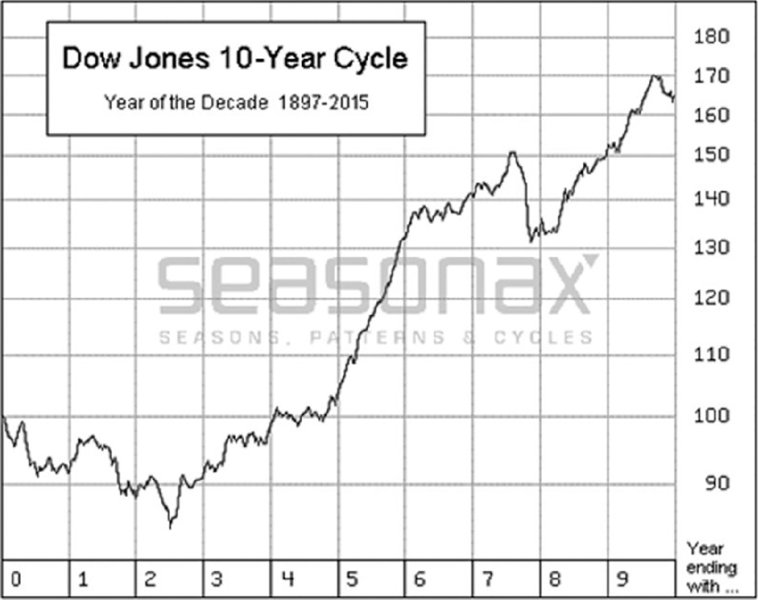

Decade cycles

Yearly cycles

Presidential cycles

Seeing cycles can make you rich

Trends helped me predict an end-of-decade bust in 2002

Cycles helped me predict the unpredictable election

Market mispricing

Beyond passive income: applying what you’ve learned

Making a good strategy great, with an awareness of cycles

![]()

Growth

Tech billionaires and growth

Beyond compound interest

Growth versus fixed mindset

![]()