PAYROLL PROCESSES (STUDY OBJECTIVE 2)

The payroll process is initiated when employees are hired by the company. Different companies may have very diverse hiring processes. For example, some companies may have an employment office or placement department to handle their recruiting and hiring, while in others (especially smaller companies) personnel in the various departments that have job vacancies may conduct these activities. Regardless of the manner in which it is handled, the hiring of employees is typically considered a nonroutine process. Accordingly, members of management are required to specifically approve all employees hired by the company, even if they are initially screened by an employment office. A hiring decision usually happens as a result of an interview or interviews and is documented on a signed letter and/or signed employment contract.

Since companies need human resources in order to conduct business operations, the hiring process must occur before other business transactions can take place. Although this may be true initially, the payroll process is also an ongoing organizational process. A company may need to hire new employees at various times throughout its life cycle in order to accommodate growth and replace employees who have left the company, have retired, or have been relocated, reassigned, or terminated.

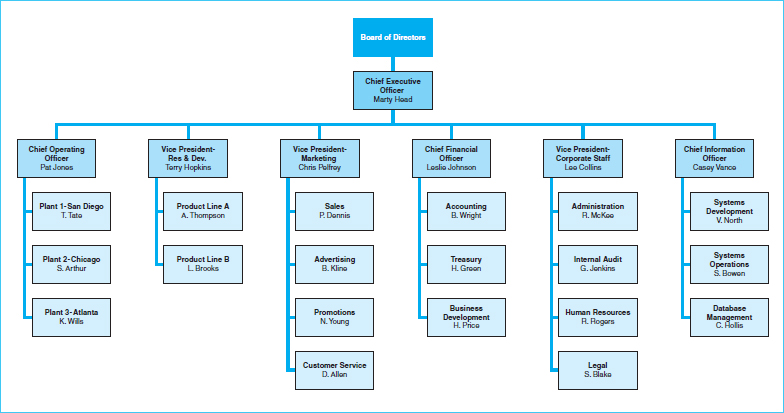

Information for all employees must be retained and updated regularly. The human resources department is responsible for maintaining records for each job and each employee within the organization, as well as tracking job vacancies and supporting the company's recruitment efforts. Most companies maintain an organization chart to map out the jobs and reporting relationships. Exhibit 10-2 presents an example of an organization chart for a generic business.

This organization chart presents only the top branches of the organization's structure. A complete organization chart would include a box or cell for each position within the company. The organization charts of different companies may look different, and the numbers of layers and boxes depend on the complexity of the organizational structure and the number of middle management positions. For example, the sales department may include several sales territories, and each territory may have a manager and several employees making up its sales force. The human resources department typically maintains job profiles or job descriptions that explain the qualifications and responsibilities of each position shown on the chart. These job profiles are further supported by policies and procedures manuals that outline specific activities performed by each position.

In addition to maintaining job records, the human resources department also keeps personnel files; thus, it is often referred to as the personnel department. Personnel files include the information that the company needs, relevant to the people who work there. Personnel records typically include documentation related to the initial hiring, such as an employment application and contract, resume, recommendation letters, interview reports, wage or salary authorization, and results from a background investigation. Personal information must also be maintained, such as the employee's address, Social Security number, employment history, and so forth. Important information related to payroll processing is also contained in each employee's personnel file, such as overtime and commission rates, applicable tax withholdings, and authorization for payroll deductions.

Exhibit 10-2 Generic Organization Chart

In addition to the necessary tax withholdings, most companies have employee payroll deductions for such things as contributions to employee benefits programs, unions, savings plans, retirement plans, and charities. Employees must authorize which of these options they choose to be deducted from their pay. In addition, employees may have wage attachments for items such as child support, loans, or bankruptcies. Written records authorizing each of these amounts must be included in the personnel file. Also included in a personnel file is documentation regarding vacation and sick time, as well as records of attendance, performance evaluations, work schedule, promotion, and termination. Although a detailed examination of these types of employee processes and records is beyond the scope of this chapter, they are mentioned here as examples of the diverse and specialized nature of these records. Each employee's personnel file is as individual as the person it represents, so there are significant differences in the processes required to keep the records up to date. The record-keeping responsibilities of employees in the human resources department must be thorough in order to take into consideration all the different possibilities for an employee's pay status.

One unique feature of the information contained in an individual personnel file is that it is accessed frequently, but changed relatively infrequently. After all the information is established in an employee's file, it needs to be accessed each time payroll is processed in order for net pay to be accurately computed. It is important that the supporting information be kept up to date. Although payroll information may change periodically due to such things as tax rate changes and pay raises, the frequency of these kinds of changes is slight in comparison with the number of times the information is accessed for payroll purposes.

Depending upon the amount of computerization of the company's system, personnel records may be retained in hard copy or they may be entered into the system and retained electronically. Given the varying extent of information collected from employees, most modern companies have implemented some level of automation of their personnel records and payroll applications. After we examine the basic features of a manual payroll system, the related IT processes will be discussed.

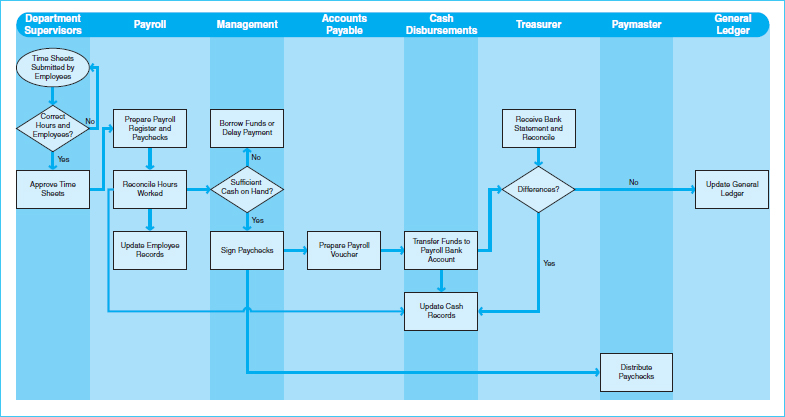

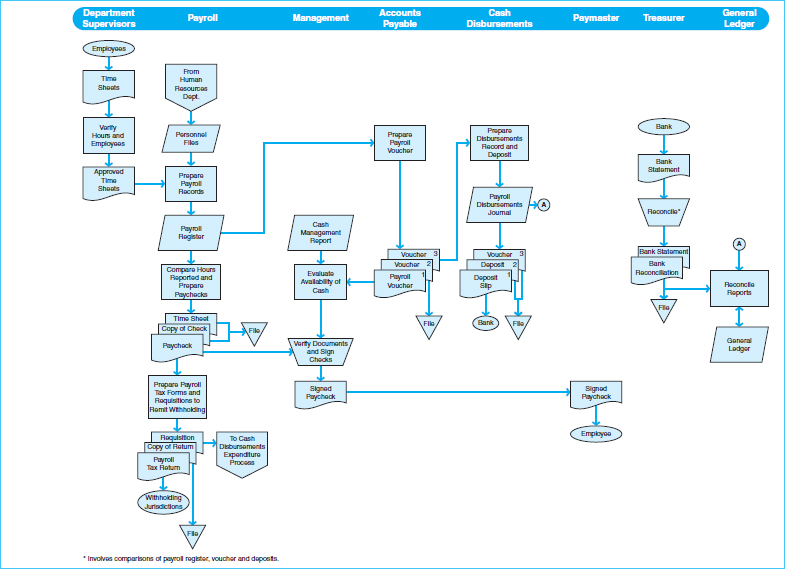

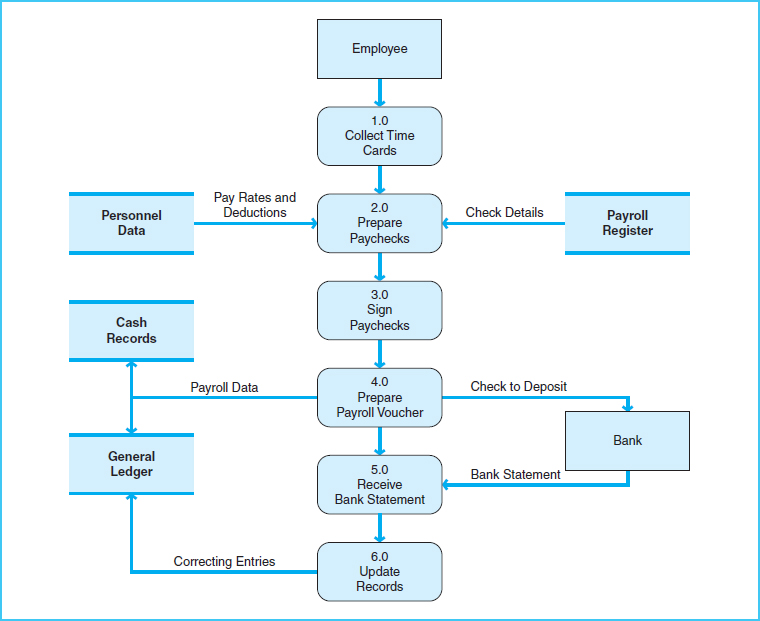

Once an employee's personnel file is complete and the term of employment has begun, routine activities take place regarding payroll processing. Exhibit 10-3 is a business process map depicting these activities. Exhibit 10-4 shows a document flowchart for payroll processing and Exhibit 10-5 presents a data flow diagram of these processes. This is undoubtedly the most important process from the perspective of the company's employees, because it is the source of employees' paychecks. The payroll process is also unique because of its widespread nature; it affects everyone within the company. It requires the involvement of each individual within each department or location. Accordingly, personnel-related expenses are usually among the largest expenses reported on the company's income statement. For these reasons, it is important that the company has a reliable system in place to handle its payroll activities. Without paychecks, few employees would remain with the company. And without human resources, few companies would be able to survive.

Exhibit 10-3 Payroll Process Map

Exhibit 10-4 Document Flowchart of the Payroll Processes

Exhibit 10-5 Payroll Processes Data Flow Diagram

As employees perform their jobs, they earn their pay and the company accrues a corresponding liability for the wages and salaries. Determining the correct amount of pay depends on the employees keeping adequate records of their hours and projects. A time sheet is the record of hours worked by an employee for a specific payroll period. A time sheet covers a specified time (ranging from one week to one month, depending on the frequency with which paychecks are prepared). In order to ensure that the time sheets include the most accurate and up-to-date information, they need to be updated by each employee on a daily basis. Salaried employees sometimes are not required to report their hours worked on a daily basis, but are often required to report the activities performed within the period. Employees in the production area are often required to prepare very detailed (to-the-minute) time reports, identifying the types of projects they worked on and the exact lengths of time spent, so that the company can determine the precise cost of its products. Additional information on the conversion processes is discussed in Chapter 11.

At the end of each pay period, employees submit completed time sheets to their departmental supervisors for approval. Supervisors should carefully review each time sheet, being certain that these documents accurately reflect the employees and hours worked in their departments. Because time sheets represent the hours for which employees expect to be paid, care should be exercised in determining the appropriateness of these reports, including any overtime hours. Likewise, any vacation and sick time should be properly reported by employees and verified by the supervisors.

Once time sheets have been approved, they are forwarded to the payroll department. The payroll department is responsible for figuring the amount of net pay to be included on each paycheck. Paycheck amounts are based on the hours reported on time sheets and pay rates and deductions authorized in the respective personnel files. The computations required to support the paychecks are as follows:

Gross Pay = Hours Reported × Authorized Pay Rate Net Pay, i.e., Paycheck Amount = Gross Pay – Authorized Deductions

Although these are relatively simple formulas that may be considered part of a routine process, it may actually be challenging to figure the amount of deductions applicable to an employee's pay. This is because each employee's deductions are likely to be different. In addition, the payroll formulas must be applied to every employee in the company, one at a time. The process is further complicated by the fact that the inputs tend to change constantly. Each payroll period will include some changes in the number of hours worked, pay rates or withholdings. An accounting software program is a very efficient tool to assist the payroll department in managing this abundance of information. On the other hand, when done manually, the process of extracting all these inputs from the records and performing the mathematical computations is extremely time-consuming.

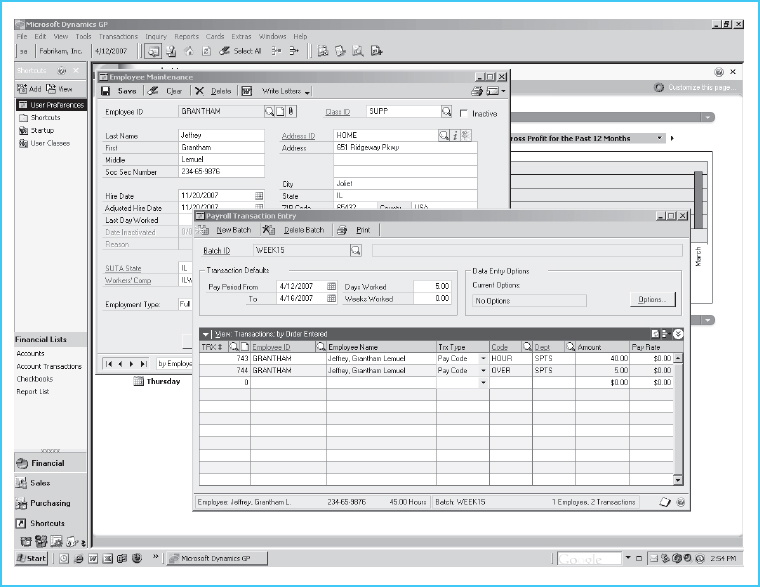

The payroll department prepares a payroll register to accumulate all paycheck data. A payroll register is a complete listing of salary or wage detail for all employees for a given time. Exhibit 10-6 shows a payroll register entry as it would be established in Microsoft Dynamics® accounting software. Note that this entry is for a single employee, but because this employee worked overtime hours, distinct entries are needed for the standard hours and overtime hours. Since overtime is paid at a higher rate (usually, one and one-half times the standard rate), it must be shown separately. Also note that inputs to this software application include the employee's identification number, hours worked, and applicable dates. All other information needed for the preparation of the payroll register and paycheck is retained in the system so that the payroll department personnel do not have to look it up each pay period.

The payroll department should compare the hours reported on time sheets with the hours accumulated in the payroll register before the paychecks are sent to management for authorization. Authorization is typically indicated by a manager's signature on the paychecks.

Before signed paychecks can be given to employees, the company must be sure that it has sufficient cash on hand to cover the total amount of the payroll. In addition, the cash must be deposited in the payroll cash account. Since employees usually do not hesitate to cash their paychecks, the timing of these activities is important. The accounts payable department determines the total amount of the net payroll from the payroll register and prepares a payroll voucher. A payroll voucher authorizes the transfer of cash from the company's main operating account into the payroll cash account. Most companies maintain a separate bank account to handle payroll transactions. This makes it easier to account for payroll transactions and to distinguish them from cash disbursements for other business purposes.

Exhibit 10-6 Preparing a Payroll Register in Microsoft Dynamics®

The cash disbursements department receives the payroll voucher, carries out the transfer of funds between bank accounts, and updates the related accounting records. A payroll disbursements journal is prepared to provide a listing of all paychecks written, in check-number sequence, with the total supporting the amount of payroll funds transferred to the payroll bank account.

On the designated pay day, signed paychecks are distributed to employees by an independent paymaster. Any unclaimed paychecks should be returned to the treasurer or other independent party for followup.

Another responsibility of the payroll department is the preparation of payroll deposits and the related tax forms. All withholdings from employees' pay must be paid as designated. For example, when employees elect deductions from their pay for union dues, the company must pay the amounts withheld for the union. Similarly, federal income taxes withheld from paychecks must be paid to the federal government in a timely manner and reported periodically. This may be a challenging task, depending on the number of employees and considering the fact that multiple jurisdictions may be represented by the company's work force, each with different withholding rates and payment requirements. In addition, the company often supplements employee withholdings by paying its share of contributions for such things as insurance premiums and other employee benefit programs, savings plans, and charitable donations.

Similar to the cash disbursements system described in Chapter 9, the payroll process should involve reconciliation of the payroll bank account with the payroll disbursements journal and payroll deposit slips. This practice is performed by someone independent of the accounting function.