49 ASC 820 FAIR VALUE MEASUREMENTS

The Debate over the Use of Fair Value Measurements

ASC 820, Fair Value Measurement

Measurement Principles and Methodologies

Item identification and unit of account

Principal or most advantageous market and market participants

Selection of the valuation premise for asset measurements

Risk assumptions when valuing a liability

PERSPECTIVE AND ISSUES

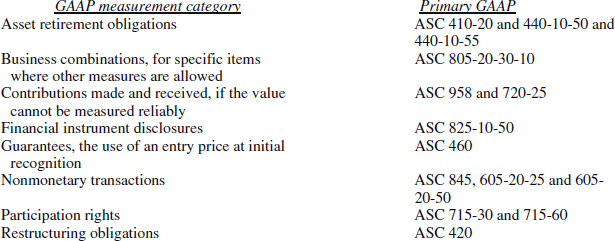

Subtopic

ASC 820 contains one subtopic:

- ASC 820-10, Overall, which defines fair value, describes a framework for measuring fair value and details required disclosures.

Scope and Scope Exceptions

ASC 820 does not require fair value measurement in addition to those required by other Topics in the Codification.

Scope. In pursuing an incremental approach, ASC 820 contained scope exceptions for certain, highly-complex specialized applications. It does not apply to:

- Share-based payments transactions, except for transaction covered in ASC 718-40 which are within the scope of ASC 820

- Measurement that are similar to fair value but that are not intended to measure fair value, including:

- Measurements models that are based on vendor-specific objective evidence of fair value, such as multiple-deliverable arrangements and software revenue recognition

- Inventory

- To accounting principles that address fair value measurements for purposes of lease classification or measurement. The exception does not apply to assets acquired and liabilities assumed in a business combination or an acquisition by a not-for-profit entity that are required to be measured at fair value regardless of whether those assets and liabilities are related to leases.

In addition to the scope exceptions listed above, ASC 820 retains the practicability exceptions included in GAAP that acknowledge that it is sometimes not reasonable to estimate fair value without “undue cost or effort.” When this is the case, however, management is required to inform the users of the financial statements that it has invoked this exception, as well as the reasons that it believes making fair value measurements would be impractical. (ASC 820-10-15-3) This exception applies to certain measurements made in connection with the following matters:

Overview

The Debate over the use of fair value measurements.

The communities of financial statement preparers, users, auditors, standard setters, and regulators have engaged in a longstanding debate regarding the relevance, transparency, and decision-usefulness of financial statements prepared under the current US GAAP “mixed attribute” model for measuring assets and liabilities.

Investors and creditors that use financial statements for decision-making purposes argue that reporting financial instruments at historical cost or amortized cost deprives them of important information about the economic impact on the reporting entity of real economic gains and losses associated with changes in the fair values of assets and liabilities that it owns or owes. They assert that, had they been provided this information, they might well have made different decisions regarding investing in, lending to, or entering into business transactions with the reporting entities.

ASC 820, Fair Value Measurement.

Accounting Standards Codification (ASC) 820 provides a unified definition of fair value, related guidance on measurement, and enhanced disclosure requirements to inform financial statement users about the fair value measurements included in the financial statements, the methods and assumptions used to estimate them, and the degree of observability of the inputs used in management's estimation process. The standard retains the longstanding exceptions that existed in GAAP that apply when, in management's judgment, it is not practical to estimate fair value. In such instances, management is required to inform the reader in an explanatory note to the financial statements that it is unable to estimate fair value and the reasons that such an estimate cannot be made.

This chapter provides the reader/researcher with

- An explanation of the fair value measurement model prescribed by ASC 820

- Illustrations of financial statement formats and comprehensive disclosures that integrate with the disclosures required by other provisions of the ASC regarding financial instruments and fair value.

Technical Alert

ASU 2011-04.

The Financial Accounting Standards Board (FASB) has been on record for more than a decade regarding its long-term goal of having all financial assets and liabilities reported at fair value. That said, it has taken a cautious, incremental approach towards attaining this goal. Its projects with respect to fair value have been conducted in multiple phases over long periods of time. In May 2011, the FASB issued, Accounting Standards Update (ASU) 2011-04, Amendments to Achieve Measurement and Disclosure Requirements in US GAAP and IFRSs. In addition to converging with International Accounting Standards Board (IASB) standards, the ASU clarified how a principal market is determined, addressed the fair value measurement of financial assets and financial liabilities with offsetting market or counterparty credit risks and the concepts of valuation premise and highest and best use, extended the prohibition on the use of blockage factors to all three levels of the valuation hierarchy, and required additional disclosures. The ASU is effective for public companies in interim and annual periods beginning after December 15, 2011, with early adoption prohibited. Nonpublic companies are required to apply the guidance in annual periods beginning after December 15, 2012, with early adoption permitted for any interim period beginning after December 15, 2011. Application is prospective. Any changes in fair values resulting from the new guidance are a change in estimate, recorded through the income statement in the first period of application.

ASU 2013-09.

In July 2013, the FASB released Accounting Standards Update—Fair Value Measurement (Topic 820): Deferral of the Effective Date of Certain Disclosures for Nonpublic Employee Benefit Plans in Update No. 2011-04 to defer quantitative disclosures about investments held by a nonpublic employee benefit plan in the plan sponsor's own equity securities. Stakeholders expressed concerns that certain disclosure requirements would reveal sensitive proprietary information of private companies. The ASU is effective 7/8/2013 for financial statements not yet issued.

DEFINITIONS OF TERMS

Source: ASC 820-10-20

Active market. A market in which transactions for the asset or liability occur with sufficient frequency and volume to provide pricing information on an ongoing basis.

Brokered market. A market in which brokers attempt to match buyers with sellers, but do not stand ready to trade for their own account.

Cost approach. A valuation technique that reflects the amount that currently would be required to replace the service capacity of an asset, often called current replacement cost.

Credit risk. For purposes of a hedged item in a fair value hedge, credit risk is the risk of changes in the hedged item's fair value attributable to both of the following:

- Changes in the obligor's creditworthiness

- Changes in the spread over the benchmark interest rate with respect to the hedged item's credit sector at inception of the hedge.

For purposes of a hedged transaction in a cash flow hedge, credit risk is the risk of changes in the hedged transaction's cash flows attributable to all of the following:

- Default

- Changes in the obligor's creditworthiness

- Changes in the spread over the benchmark interest rate with respect to the related financial asset's or liability's credit sector at inception of the hedge.

Currency risk. The risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes in foreign exchange rates.

Dealer market. A market in which dealers stand ready to trade (either buy or sell for their own account), thereby providing liquidity by using their capital to hold an inventory of the items for which they make a market. Typically, bid and ask prices (representing the price at which the dealer is willing to buy and the price at which the dealer is willing to sell, respectively) are more readily available than closing prices. Over-the counter markets (for which prices are publicly reported by the National Association of Securities Dealers Automated Quotations systems or by Pink Sheets LLC) are dealer markets. For example, the market for US Treasury securities is a dealer market. Dealer markets also exist for some other assets and liabilities, including other financial instruments, commodities, and physical assets (for example, used equipment).

Discount rate adjustment technique. A present value technique that uses a risk-adjusted discount rate and contractual, promised, or most likely cash flows.

Entry price. The price paid to acquire an asset, or received to assume a liability in an exchange transaction.

Exchange market. A market in which closing prices are both readily available and generally representative of fair value (such as the New York Stock Exchange).

Exit price. The price that would be received to sell an asset or paid to transfer a liability.

Expected cash flow. The probability-weighted average (that is, mean of the distribution) of possible future cash flows.

Fair value. The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Financial asset. Cash, evidence of an ownership interest in an entity, or a contract that conveys to one entity a right

- to receive cash or another financial instrument from a second entity or

- to exchange other financial instruments on potentially favorable terms with the second entity.

Financial instrument. Cash, evidence of an ownership interest in an entity, or a contract that both:

- Imposes on one entity a contractual obligation either:

- To deliver cash or another financial instrument to a second entity

- To exchange other financial instruments on potentially unfavorable terms with the second entity.

- Conveys to that second entity a contractual right either:

- To receive cash or another financial instrument from the first entity

- To exchange other financial instruments on potentially favorable terms with the first entity.

The use of the term financial instrument in this definition is recursive (because the term financial instrument is included in it), though it is not circular. The definition requires a chain of contractual obligations that ends with the delivery of cash or an ownership interest in an entity. Any number of obligations to deliver financial instruments can be links in a chain that qualifies a particular contract as a financial instrument.

Contractual rights and contractual obligations encompass both those that are conditioned on the occurrence of a specified event and those that are not. All contractual rights (contractual obligations) that are financial instruments meet the definitions of asset (liability) set forth in FASB Concepts Statement No. 6, Elements of Financial Statements, although some may not be recognized as assets (liabilities) in financial statements—that is, they may be off-balance-sheet—because they fail to meet some other criterion for recognition.

For some financial instruments, the rights held by or the obligation is due from (or the obligation is used to or by) a group of entities rather than a single entity.

Financial liability. A contract that imposes on one entity an obligation

- to deliver cash or another financial instrument to a second entity or

- to exchange other financial instruments on potentially unfavorable terms with the second entity.

Highest and best use. The use of a nonfinancial asset by market participants that would maximize the value of the asset or the group of assets and liabilities (for example, a business) within which the asset would be used.

Income approach. Valuation techniques that convert future amounts (for example, cash flows or income and expenses) to a single current (that is, discounted) amount. The fair value measurement is determined on the basis of the value indicated by current market expectations about those future amounts.

Inputs. The assumptions that market participants would use when pricing the asset or liability, including assumptions about risk, such as the following:

- The risk inherent in a particular valuation technique used to measure fair value (such as a pricing model)

- The risk inherent in the inputs to the valuation technique.

Inputs may be observable or unobservable.

Interest rate risk. The risk of changes in a hedged item's fair value or cash flows attributable to changes in the designated benchmark interest rate.

Legal entity. Any legal structure used to conduct activities or to hold assets. Some examples of such structures are corporations, partnerships, limited liability companies, grantor trusts, and other trusts.

Level 1 inputs. Quoted prices (unadjusted) in active markets for identical assets or liabilities that the reporting entity can access at the measurement date.

Level 2 inputs. Inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly.

Level 3 inputs. Unobservable inputs for the asset or liability.

Liability issued with an inseparable third-party credit enhancement. A liability that is issued with a credit enhancement obtained from a third party, such as debt that is issued with a financial guarantee from a third party that guarantees the issuer's payment obligation.

Management. Persons who are responsible for achieving the objectives of the entity and who have the authority to establish policies and make decisions by which those objectives are to be pursued. Management normally includes members of the board of directors, the chief executive officer, chief operating officer, vice presidents in charge of principal business functions (such as sales, administration, or finance), and other persons who perform similar policy-making functions. Persons without formal titles also may be members of management.

Market approach. A valuation technique that uses prices and other relevant information generated by market transactions involving identical or comparable (that is, similar) assets, liabilities, or a group of assets and liabilities, such as a business.

Market participants. Buyers and sellers in the principal (or most advantageous) market for the asset or liability that have all of the following characteristics:

- They are independent of each other, that is, they are not related parties, although the price in the related-party transaction may be used as an input to a fair value measurement if the reporting entity has evidence that the transaction was entered into at market terms

- They are knowledgeable, having a reasonable understanding about the asset or liability and the transaction using all available information, including information that might be obtained through due diligence efforts that are usual and customary

- They are able to enter into a transaction for the asset or liability

- They are willing to enter into a transaction for the asset or liability, that is, they are motivated but not forced or otherwise compelled to do so.

Market risk. The risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes in market prices. Market risk comprises the following:

- Interest rate risk

- Currency risk

- Other price risk.

Market-corroborated inputs. Inputs that are derived principally from or corroborated by observable market data by correlation or other means.

Most advantageous market. The market that maximizes the amount that would be received to sell the asset or minimizes the amount that would be paid to transfer the liability, after taking into account transaction costs and transportation costs.

Net asset value per share. Net asset value per share is the amount of net assets attributable to each share of capital stock (other than senior equity securities; that is, preferred stock) outstanding at the close of the period. It excludes the effects of assuming conversion of outstanding convertible securities, whether or not their conversion would have a diluting effect.

Nonperformance risk. The risk that an entity will not fulfill an obligation. Nonperformance risk includes, but may not be limited to, the reporting entity's own credit risk.

Nonpublic entity. Any entity that does not meet any of the following conditions:

- Its debt or equity securities trade in a public market either on a stock exchange (domestic or foreign) or in an over-the counter market, including securities quoted only locally or regionally.

- It is a conduit bond obligor for conduit debt securities that are traded in a public market (a domestic or foreign stock exchange or an over-the-counter market, including local or regional markets).

- It files with a regulatory agency in preparation for the sale of any class of debt or equity securities in a public market.

- It is required to file or furnish financial statements with the Securities and Exchange Commission.

- It is controlled by an entity covered by criteria 1 through 4.

Not-for-profit-entity. An entity that possesses the following characteristics, in varying degrees, that distinguish it from a business entity:

- Contributions of significant amounts of resources from resources providers who do not expect commensurate or proportionate pecuniary return

- Operating purposes other than to provide goods or services at a profit

- Absence of ownership interest like those of business entities.

Entities that clearly fall outside this definition include the following:

- All investor-owned entities

- Entities that provide dividends, lower costs, or other economic benefits directly and proportionately to their owners, members, or participants, such as mutual insurance entities, credit unions, farm and rural electric cooperatives, and employee benefit plans.

Observable inputs. Inputs that are developed using market data, such as publicly available information about actual events or transactions, and that reflect the assumptions that market participants would use when pricing the asset or liability.

Orderly transaction. A transaction that assumes exposure to the market for a period before the measurement date to allow for marketing activities that are usual and customary for transactions involving such assets or liabilities; it is not a forced transaction (for example, a forced liquidation or distress sale).

Other price risk. The risk that the fair value of future cash flows of a financial instrument will fluctuate because of changes in market prices (other than those arising from interest rate risk or currency risk), whether those changes are caused by factors specific to the individual financial instrument or its issuer or by factors affecting all similar financial instruments traded in the market.

Present value. A tool used to link future amounts (cash flows or values) to a present amount using a discount rate (an application of the income approach). Present value techniques differ in how they adjust for risk and in the type of cash flows they use.

Principal market. The market with the greatest volume and level of activity for the asset or liability.

Principal-to-principal market. A market in which transactions, both originations and resales, are negotiated independently with no intermediary. Little information about those transactions may be made available publicly.

Readily determinable fair value. An equity security has a readily determinable fair value if it meets any of the following conditions:

- The fair value of an equity security is readily determinable if sales prices or bid-and-asked quotations are currently available on a securities exchange registered with the US Securities and Exchange Commission (SEC) or in the over-the-counter market, provided that those prices or quotations for the over-the counter market are publicly reported by the National Association of Securities Dealers Automated Quotations systems or by Pink Sheets LLC. Restricted stock meets that definition if the restriction terminates within one year.

- The fair value of an equity security traded only in a foreign market is readily determinable if that foreign market is of a breadth and scope comparable to one of the US markets referred to above.

- The fair value of an investment in a mutual fund is readily determinable if the fair value per share (unit) is determined and published and is the basis for current transactions.

Related parties. Related parties include:

- Affiliates of the entity

- Entities for which investments in their equity securities would be required, absent the election of the fair value option under the Fair Value Option Subsection of Section 825-10-15, to be accounted for by the equity method by the investing entity

- Trusts for the benefit of employees, such as pension and profit-sharing trusts that are managed by or under that trusteeship of management

- Principal owners of the entity and members of their immediate families

- Management of the entity and members of their immediate families

- Other parties with which the entity may deal if one party controls or can significantly influence the management or operating policies of the other to an extent that one of the transacting parties might be prevented from fully pursuing its own separate interests

- Other parties that can significantly influence the management or operating policies of the transacting parties or that have an ownership interest in one of the transacting parties and can significantly influence the other to an extent that one or more of the transacting parties might be prevented from fully pursuing its own separate interests.

Risk premium. Compensation sought by risk-averse market participants for bearing the uncertainty inherent in the cash flows of an asset or a liability. Also referred to as a risk adjustment.

Systematic risk. The common risk shared by an asset or a liability with the other items in a diversified portfolio. Portfolio theory holds that in a market in equilibrium, market participants will be compensated only for bearing the systematic risk inherent in the cash flows. (In markets that are inefficient or out of equilibrium, other forms of return or compensation might be available.) Also referred to as nondiversifiable risk.

Transaction costs. The costs to sell an asset or transfer a liability in the principal (or most advantageous) market for the asset or liability that are directly attributable to the disposal of the asset or transfer of the liability and meet both of the following criteria:

- They result directly from and are essential to that transaction.

- They would not have been incurred by the entity had the decision to sell the asset or transfer the liability not been made (similar to costs to sell, as defined in ASC 360-10-35-38).

Transportation costs. The costs that would be incurred to transport an asset from its current location to its principal (or most advantageous) market.

Unit of account. The level at which an asset or a liability is aggregated or disaggregated in a Topic for recognition purposes.

Unobservable inputs. Inputs for which market data are not available and that are developed using the best information available about the assumptions that market participants would use when pricing the asset or liability.

Unsystematic risk. The risk specific to a particular asset or liability. Also referred to as diversifiable risk.

Variable interest entity. A legal entity subject to consolidation according to the provisions of the Variable Interest Entities Subsections of ASC 810-10.

CONCEPTS, RULES, AND EXAMPLES

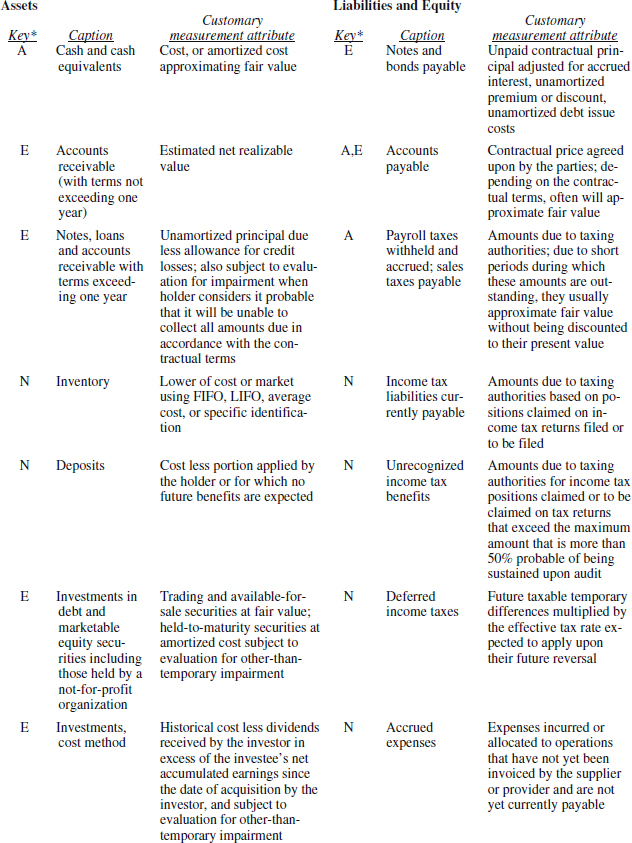

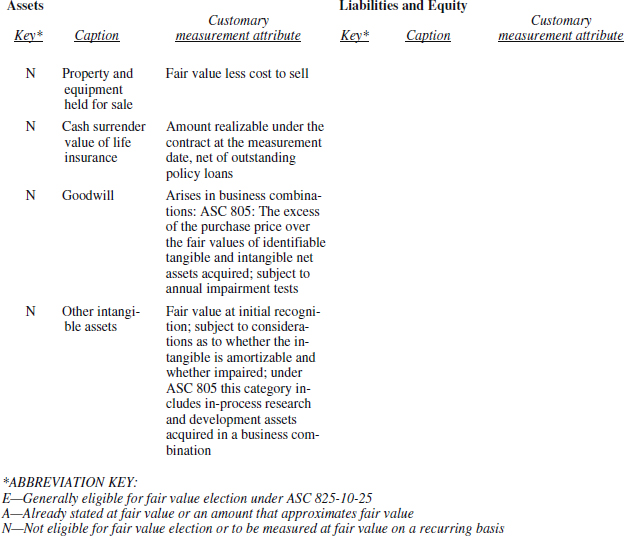

The Mixed Attribute Model

Under longstanding US GAAP, assets, liabilities, and equity are measured and presented on a reporting entity's statement of financial position by applying a disjointed, inconsistent assortment of accounting methods. This current state of affairs is sometimes referred to as the “mixed attribute model.” The following table summarizes the current state of the mixed attribute model and the effects of ASC 820 and ASC 825-10-25 (if any) on specified assets and liabilities of reporting entities that are not financial institutions, investment companies, or insurance companies.

Objectives

Definition.

The term “fair value” was coined by the FASB to replace the previously used term “market value” (for which the term “fair market value” was sometimes used interchangeably) in authoritative accounting literature. This change was made to emphasize the fact that, even in the absence of active primary markets for an asset or liability, the asset or liability can be valued by reference to prices and rates from secondary markets as well. Over time, this concept has been expanded further to include the application of various fair value estimation models, such as the discounted probability-weighted expected cash flow model first introduced in CON 7.

As these broader fair value concepts were evolving in the literature and in practice, the preexisting “market-based” literature had not been revised. Further, the concepts and definitions of fair value were not consistently understood or applied in similar situations by similar reporting entities.

Measurement Principles and Methodologies

It is helpful to break down the measurement process under ASC 820 into a series of steps. Although not necessarily performed in a linear manner, the following procedures and decisions need to be applied and made, in order to value an asset or liability at fair value under ASC 820. The process will be discussed in greater detail.

- Identify the item to be valued and the unit of account. Specifically identify the asset or liability, including the unit of account to be used for the measurement.

- Determine the principal or most advantageous market and the relevant market participants. From the reporting entity's perspective, determine the principal market in which it would sell the asset or transfer the liability. In the absence of a principal market, consider the most advantageous market for the asset or the liability. Once the principal or most advantageous market is identified, determine the characteristics of the market participants. It is not necessary that specifically named individuals or enterprises be identified for this purpose.

- Select the valuation premise to be used for asset measurements. If the item being measured is an asset, determine the valuation premise to be used by evaluating whether marketplace participants would judge the highest and best use of the nonfinancial asset on a stand-alone basis or in combination with other assets as a group or with other assets and liabilities. Note that the highest and best use and valuation premise concepts only apply to measuring of nonfinancial assets.

- Consider the risk assumptions applicable to liability measurements. If the item being measured is a liability, identify the key assumptions that market participants would make regarding nonperformance risk including, but not limited to, the reporting entity's own credit risk (credit standing).

- Identify available inputs. Identify the key assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. In identifying these assumptions, referred to as “inputs” by ASC 820, maximize the inputs that are relevant and observable (i.e., that are based on market data available from sources independent of the reporting entity). In so doing, assess the availability of relevant, reliable market data for each input that significantly affects the valuation, and identify the level of the fair value input hierarchy in which it is to be categorized.

- Select the appropriate valuation technique(s). Based on the nature of the asset or liability being valued, and the types and reliability of inputs available, determine the appropriate valuation technique or combination of techniques to use in valuing the asset or liability. The three broad categories of techniques are the market approach, the income approach, and the cost approach.

- Make the measurement. Measure the asset or liability.

- Determine amounts to be recognized and information to be disclosed. Determine the amounts and information to be recorded, classified, and disclosed in interim and annual financial statements.

Item identification and unit of account.

In general, the same unit of account at which the asset or liability is aggregated or disaggregated by applying other applicable GAAP pronouncements is to be used for fair value measurement purposes. ASC 820-10-35-44 prohibits adjustment to the valuation for a “blockage factor.” A blockage factor is an adjustment made to a valuation that takes into account the fact that the investor holds a large quantity (block) of shares relative to the market trading volume in those shares. The prohibition applies even if the quantity held by the reporting entity exceeds the market's normal trading volume—and that, if the reporting entity were, hypothetically, to place an order to sell its entire position in a single transaction, that transaction could affect the quoted price.

There is an exception for a financial assets and financial liabilities with offsetting positions in market risks or counterparty credit risk that are managed on the basis of the entity's net exposure to the risks. If certain criteria are met, the entity can measure the fair value of net position in a manner that is consistent with how market participants would price the net position. To use the exception, ASU 820-10-35-18E indicates all the following conditions must be met. The company:

- Manages the group of financial assets and financial liabilities on the basis of the reporting entity's net exposure to a particular market risk (or risks) or to the credit risk of a particular counterparty in accordance with the reporting entity's documented risk management or investment strategy.

- Provides information on that basis about the group of financial assets and financial liabilities to the reporting entity's management

- Is required or has elected to measure those financial assets and financial liabilities at fair value in the statement of financial position at the end of each reporting period.

Principal or most advantageous market and market participants.

ASC 820 requires the person performing the valuation to maximize the use of relevant assumptions (inputs) that are observable from market data obtained from sources independent of the reporting entity. In making a fair value measurement, management is to assume that the asset or liability is exchanged in an orderly transaction between market participants at the measurement date.

To characterize the exchange as orderly, it is assumed that the asset or liability will have been exposed to the market for a sufficient period of time prior to the measurement date to enable marketing activities to occur that are usual and customary with respect to transactions involving such assets or liabilities. It is also to be assumed that the transaction is not a forced transaction (e.g., a forced liquidation or distress sale).

ASC 820 also specifies that if there is a principal market for an asset or liability (determined under the SEC's Accounting Standards Release [ASR] No. 118, Accounting for Investment Securities by Registered Investment Companies, or otherwise), the measure of fair value is the price in that market (whether directly observable or determined indirectly using a valuation technique), even if the price in a different market is potentially more advantageous at the measurement date.

Management identifies the principal market for the asset or liability, if such a market exists. If the entity has access to more than one market, the principal market is the market in which the reporting entity would sell the asset or transfer the liability that has the greatest volume and activity level for the asset or liability. The greater volume of activity ensures that the measurement is based on multiple transactions potentially between multiple counterparties, and is thus more representative of fair value than if the measurement were based on less extensive data.

Note that the determination of the principal market is made from the perspective of the reporting entity. Thus, different reporting entities engaging in different specialized industries, or with access to different markets, might not have the same principal market for an identical asset or liability. Inputs from the principal market are to be used irrespective of whether the price is directly observable or determined through the use of a valuation technique.

If there is no principal market for an asset or liability from the perspective of the reporting entity, then management uses the most advantageous market for the measurement. In determining the most advantageous market, management considers transaction costs. However, once the most advantageous market had been identified, transaction costs are not used to adjust the market price used for the purposes of the fair value measurement.

ASC 820 provides a typology of markets that potentially exist for assets or liabilities. (See the “Definitions of Terms” section at the beginning of this chapter for descriptions of each of these markets.)

Market participants in the principal or most advantageous market are buyers and sellers that

- Are unrelated third parties

- Have the ability to enter into a transaction for the asset or liability

- Have the motivation to voluntarily enter into a transaction for the asset or liability without being forced to do so under duress

- Are knowledgeable about the asset or liability since they would possess a reasonable understanding of the asset or liability and the terms of the transaction based on all available information including information obtainable through the performance of usual and customary due diligence procedures.

The person determining the measurement is not required to identify specific individuals or enterprises that would potentially be market participants. Instead, it is important to identify the distinguishing characteristics of participants in the particular market by considering factors specific to the asset or liability being measured, the market identified, and the participants in that market with whom the reporting entity would enter into a transaction for the asset or liability.

Measurement considerations when markets become illiquid or less liquid. Questions have arisen regarding whether transactions occurring in less liquid markets with less frequent trades might cause those market transactions to be considered forced or distress sales, thus rendering valuations made using those prices not indicative of the actual fair value of the securities.

Under ASC 820, orderly transactions are occurring in the marketplace for an asset or liability when knowledgeable buyers and sellers independent of the reporting entity are willing and able to transact and are motivated to transact without being forced to do so. If orderly transactions are occurring in a manner that is usual and customary for the asset or liability, then the transactions are not to be characterized as forced or distress sales. Just because transaction volume in a market drops significantly from prior periods does not necessarily mean that the market is no longer active.

Determining whether there has been a significant decrease in level of activity. Management is to consider the volume and level of activity in the market compared with normal market activity for the asset or liability (or similar assets or liabilities) being measured. In making that comparison, the following indicators of declining activity may point to a decrease that is considered significant. The indicators include, but are not limited to the following (which are not to be considered of equal significance or relevance, when evaluating the weight of evidence):

- Few recent transactions

- Price quotations based on information that is not current

- Price quotations vary substantially over time or among market makers (e.g., in some brokered markets)

- Indexes that were previously highly correlated with the fair values of the asset or liability have become demonstrably uncorrelated with recent indications of fair value for that asset or liability

- There has been a significant increase in implied liquidity risk premiums, yields, or performance indicators (such as delinquency rates or loss severities) for observed transactions or quoted prices when compared with management's estimate of expected cash flows, taking into consideration all available market data about credit and other nonperformance risk for the asset or liability being measured

- There is a wide bid-ask spread or a significant increase in that spread

- There is a significant decline or absence of a market for new issuances (that is, a primary market) for the asset or liability (or similar assets or liabilities)

- Little information is publicly released (e.g., in a principal-to-principal market).

(ASC 820-10-35-54C)

Management evaluates the relevance and significance of these indicators as well as whether other indicators might be present to determine whether, based on the weight of the evidence, there has been a significant decrease in the volume and level of activity for the asset or liability.

If management concludes that a significant decrease has occurred, it must perform further analysis of the transactions or quoted prices in that market in order to determine whether it is necessary to significantly adjust the quoted prices to estimate fair value in accordance with ASC 820. It is important to note that, for the purpose of estimating fair value, management's own intention to hold an asset or liability is not relevant. Fair value is a market-based measurement, not an entity-specific measurement.

Other unrelated circumstances might also necessitate significant adjustments to quoted prices, such as when a price for a similar asset requires a significant adjustment in order to compensate for characteristics or attributes of the comparable asset that are different from those of the asset whose fair value is being measured, or when a quoted price may not be sufficiently close to the measurement date.

FASB stresses that, even if there has been a significant decrease in the market volume and level of activity for the item being measured, it is inappropriate, based solely on that judgment, to conclude that all transactions occurring in that market are not orderly transactions. Factors to consider in judging whether a transaction might not be orderly include, but are not limited to

- Insufficient time period of exposure to the market prior to the measurement date to allow for usual or customary marketing activities for transactions involving assets or liabilities under the current market conditions

- The marketing exposure period was sufficient, but the seller only marketed the item being measured to a single market participant

- The seller is in or near bankruptcy or receivership (in other words, the seller is “distressed”), or the seller is being compelled to sell in order to meet legal or regulatory requirements (in other words, the sale is “forced”)

- The transaction price is an outlier when compared with recently occurring transactions for the same or similar item.

(ASC 820-10-35-54I)

Management considers the weight of the evidence in determining whether a particular market transaction is orderly. In making that determination, management is to consider the following guidance:

- Transactions considered orderly. If the weight of the evidence indicates a transaction is orderly, management considers that transaction price when estimating fair value or market risk premiums. The weight to be placed on that transaction price versus other indications of fair value is dependent on the specific facts and circumstances such as

- Transactions considered not orderly. If the weight of the evidence indicates a transaction is not orderly, management is to place little, if any, weight on that transaction price as compared to other indications of fair value when estimating fair value or market risk premiums.

- Insufficient information to determine whether or not transactions are orderly. If management lacks sufficient information to conclude whether or not a transaction is orderly, the transaction price is to be considered when estimating fair value or market risk premiums. However, that transaction may not be the sole or even the primary basis for estimating fair value or market risk premiums. Management is to place less weight on transactions of this nature, where sufficient information is not available to conclude whether the transaction is orderly when compared with other transactions that are known to be orderly.

(ASC 820-10-35-54J)

In making the determinations above, management is not required to make all possible efforts to obtain relevant information; however, management is not to ignore information available without undue cost and effort. Obviously, management would be prevented from asserting that it lacks sufficient information with respect to whether a transaction is orderly when the reporting entity was a party to that transaction. (ASC 820-10-35-54J)

Irrespective of what valuation technique or combination of techniques is used to measure fair value, the measurement is to include appropriate risk adjustments. According to ASC 820-10-55-8, risk-averse market participants seek compensation for bearing the uncertainties inherent in the estimated future cash flows associated with an asset or liability. This compensation is referred to as a risk premium or market risk premium and it reflects the amount that the market participant would demand in order to obtain adequate compensation for that market participant's perception of the risks associated with either the amounts or timing of the estimated future cash flows. Absent such an adjustment, a measurement would not faithfully represent fair value. While determination of the appropriate risk premium may be difficult, the degree of difficulty alone is an insufficient rationale for management excluding a risk adjustment from its fair value measurement. The risk premium adjustment, however, is to reflect an orderly transaction between market participants at the measurement date under current market conditions.

Quoted prices obtained from third-party pricing services or brokers may be used as inputs in the fair value measurement if management had determined that those quoted prices were determined by the third party in accordance with the principles of ASC 820 which in practical terms means that management will need to inquire of the information provider as to, among other things, the origin of the quote, the methodology followed to compute it, the types of inputs used and their sources, the level of activity in the market for market-based quotes, the age of the data used (its proximity to the measurement date), and other information relevant in the circumstances.

When there has been a significant decrease in the volume and level of activity for the asset or liability, management is to evaluate whether those quoted prices are based on current information that reflects orderly transactions (mark-to-market) or are based on application of a valuation technique reflecting market participant assumptions, including assumptions about risk premiums (mark-to-model). Management is to place less weight on quotes that are not based on the results of actual market transactions than on other indications of fair value. The type of quote is also to be considered, for example, whether the quote represents a binding offer or an indicative price, with a binding offer to be given greater weight than an indicative price.

Selection of the valuation premise for asset measurements.

The measurement of the fair value of a nonfinancial asset is to assume the highest and best use of that asset from the perspective of market participants. Generally, the highest and best use is the way that market participants would be expected to deploy the asset (or a group of assets within which they would use the asset) that would maximize the value of the asset (or group). This highest and best use assumption might differ from the way that the reporting entity is currently using the asset or group of assets or its future plans for using it (them).

At the measurement date, the highest and best use must be physically possible (given the physical characteristics of the asset), legally permissible (taking into account any legal restrictions), and financially feasible (based on income or cash flows). Determination of the highest and best use of the nonfinancial asset will establish which of the two valuation premises to use in measuring the asset's fair value, the in-use valuation premise, or the in-exchange valuation premise.

Strategic buyers and financial buyers. ASC 820 differentiates between two broad categories of market participants that would potentially buy an asset or group of assets.

- Strategic buyers are market participants whose acquisition objectives are to use the asset or group of assets (the “target”) to enhance the performance of their existing business by achieving benefits such as additional capacity, improved technology, managerial, marketing, or technical expertise, access to new markets, improved market share, or enhanced market positioning. Thus, a strategic buyer views the purchase as a component of a broader business plan and, as a result, a strategic buyer may be willing to pay a premium to consummate the acquisition and may, in fact, be the only type of buyer available with an interest in acquiring the target. Ideally, from the standpoint of the seller, more than one strategic buyer would be interested in the acquisition which would create a bidding situation that further increases the selling price.

- Financial buyers are market participants who seek to acquire the target based on its merits as a standalone investment. A financial buyer is interested in a return on its investment over a shorter time horizon, often three to five years, after which time their objective would typically be to sell the target. An attractive target is one that offers high growth potential in a short period of time resulting in a selling price substantially higher than the original acquisition price. Therefore, even at acquisition, a financial buyer is concerned with a viable exit strategy. A financial buyer, unlike a strategic buyer, typically does not possess a high level of industry or managerial expertise in the target's industry.

The combination valuation premise. This premise assumes that the maximum fair value to market participants is the price that would be received by the reporting entity (seller) assuming the asset would be used by the buyer with other assets as a group and further, that the other assets in the group would be available to potential buyers. The target might continue to be used as presently installed or may be configured in a different manner by the buyer. The assumptions regarding the level of aggregation (or disaggregation) of the asset and other associated assets may be different than the level used in applying other accounting pronouncements. Thus, in considering highest and best use and the resulting level of aggregation, the evaluator is not constrained by how the asset may be assigned by the reporting entity to a reportable or operating segment under ASC 820, a business, reporting unit, asset group, or disposal group (ASC 820-10-35). The assumptions regarding the highest and best use of the target should normally be consistent for all of the assets included in the group within which it would be used. Generally, the market participants whose highest and best use of an asset or group of assets would be in combination are characterized as strategic buyers, as previously described.

The stand-alone valuation premise. This premise assumes that the maximum fair value to market participants is the price that would be received by the reporting entity (seller) assuming the asset would be sold principally on a stand-alone basis.

Risk assumptions when valuing a liability.

Many accountants, analysts, and others find the concept of computing fair value of liabilities and recognizing changes in fair value as they occur to be counterintuitive. Consider the case when a reporting entity's own credit standing declines (universally acknowledged as a “bad thing”). A fair value measurement that incorporates the effect of this decline in credit rating would result in a decline in the fair value of the liability and a resultant increase in stockholders' equity (a “good thing”). The justification provided in ASC 820 (and by referencing CON 7) is that

A change in credit standing represents a change in the relative positions of the two classes of claimants (shareholders and creditors) to an entity's assets. If the credit standing diminishes, the fair value of creditors' claims diminishes. The amount of shareholders' residual claims to the entity's assets may appear to increase but that increase is probably offset by losses that may have occasioned the decline in credit standing. Because shareholders usually cannot be called on to pay a corporation's liabilities, the amount of their residual claims approaches, and is limited by zero. Thus a change in the position of borrowers necessarily alters the position of shareholders, and vice versa. (CON 7, Paragraph 82)

The hypothetical transaction and operational difficulties experienced in practice. Under ASC 820, fair value measurements of liabilities assume that a hypothetical transfer to a market participant occurs on the measurement date. In measuring the fair value of a liability, the evaluator assumes that the reporting entity's obligation to its creditor (i.e., the counterparty to the obligation) will continue at and after the measurement date (i.e., the obligation will not be repaid or settled prior to its contractual maturity). This being the case, this hypothetical transfer price would most likely represent the price that the current creditor (holder of the debt instrument) could obtain from a marketplace participant willing to purchase the debt instrument in a transaction involving the original creditor assigning its rights to the purchaser. In effect, the hypothetical market participant that purchased the instrument would be in the same position as the current creditor with respect to expected future cash flows (or expected future performance, if the liability is not settleable in cash) from the reporting entity.

The evaluator further assumes that the nonperformance risk related to the obligation would remain outstanding and the transferee would fulfill the obligation. Nonperformance risk is the risk that an entity will not fulfill its obligation. It is an all-encompassing concept that includes the reporting entity's own credit standing but also includes other risks associated with the nonfulfillment of the obligation. For example, a liability to deliver goods and/or perform services may bear nonperformance risk associated with the ability of the debtor to fulfill the obligation in accordance with the timing and specifications of the contract. Further, nonperformance risk increases or decreases as a result of changes in the fair value of credit enhancements associated with the liability (e.g., collateral, credit insurance, and/or guarantees).

Liabilities with inseparable third-party credit enhancements. Creditors often impose a requirement that, in connection with granting credit to a debtor, the debtor obtain a guarantee of the indebtedness from a creditworthy third party. Under such an arrangement, should the debtor default on its obligation, the third-party guarantor would become obligated to repay the obligation on behalf of the defaulting debtor and, of course, the debtor would be obligated to repay the guarantor for having satisfied the debt on its behalf.

In connection with a bond issuance, for example, the guarantee is generally purchased by the issuer (debtor) and the issuer then combines (bundles) the guarantee (also referred to as a “credit enhancement”) with the bonds and issues the combined securities to investors. By packaging a bond with a related credit enhancement, the issuer improves the likelihood that the bond will be successfully marketed as well as reduces the effective interest rate paid on the bond by obtaining higher issuance proceeds than it would otherwise receive absent the bundled credit enhancement.

Scope exceptions. The following guidance does not apply to

- Credit enhancements provided

- By a government or government agency (such as deposit insurance provided by the US Federal Deposit Insurance Corporation [FDIC])

- Between reporting entities within a consolidated or combined group

- Between entities under common control

- The holder of the issuer's credit-enhanced liability.

Measurement. In accordance with ASC 820-10-35-18a, the issuer is not to include the effect of the credit enhancement in its fair value measurement of the liability. Thus, in determining the fair value of the liability, the issuer would consider its own credit standing and would not consider the credit standing of the third-party guarantor that provided the credit enhancement. Consequently, the unit of accounting to be used in the fair value measurement of a liability with an inseparable credit enhancement is the liability itself, absent the credit enhancement.

In the event that the guarantor is required to make payments to the creditor under the guarantee, it would result in a transfer of the issuer's obligation to repay the original creditor to the guarantor with the issuer then obligated to repay the guarantor. Should this occur, the obligation of the issuer to the guarantor would be an unguaranteed liability. Thus, the fair value of that transferred, unguaranteed obligation only considers the credit standing of the issuer.

Upon issuance of the credit-enhanced debt, the issuer is to allocate the proceeds it receives between the liability issued and the premium for the credit enhancement.

Disclosure. An issuer of debt with an inseparable credit enhancement that is covered by the scope of this guidance is required to disclose the existence of the third-party credit enhancement.

Inputs.

For the purpose of fair value measurements, inputs are the assumptions that market participants would use in pricing an asset or liability, including assumptions regarding risk. An input is either observable or unobservable. Observable inputs are either directly observable or indirectly observable. ASC 820 requires the evaluator to maximize the use of relevant observable inputs and minimize the use of unobservable inputs.

An observable input is based on market data obtainable from sources independent of the reporting entity. For an input to be considered relevant, it must be considered determinative of fair value. Even if there has been a significant decrease in the volume and level of market activity for an asset or liability, it is not to be automatically assumed that the market is inactive or that individual transactions in that market are disorderly (that is, are forced or liquidation sales made under duress).

An unobservable input reflects assumptions made by management of the reporting entity with respect to assumptions it believes market participants would use to price an asset or liability based on the best information available under the circumstances.

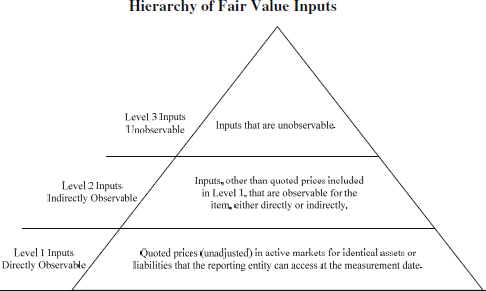

ASC 820 provides a fair value input hierarchy (see diagram below) to serve as a framework for classifying inputs based on the extent to which they are based on observable data.

Level 1 inputs. Level 1 inputs are considered the most reliable evidence of fair value and are to be used whenever they are available. These inputs consist of quoted prices in active markets for identical assets or liabilities. The active market must be one in which the reporting entity has the ability to access the quoted price at the measurement date. To be considered an active market, transactions for the asset or liability being measured must occur frequently enough and in sufficient volume to provide pricing information on an ongoing basis.

A Level 1 input should be used without adjustment to measure fair value whenever possible. One should not adjust a Level 1 input except in these cases:

- When the entity has a large number of similar assets or liabilities, and it would be difficult to obtain pricing information for each individual item on the measurement date.

- When a quoted price in an active market does not represent the fair value of an asset or liability on the measurement date.

- When the quoted price needs to be adjusted for factors specific to the item.

The use of Level 2 or Level 3 inputs is generally prohibited when Level 1 inputs are available.

Level 2 inputs. Level 2 inputs are quoted prices for the asset or liability (other than those included in Level 1) that are either directly or indirectly observable. Level 2 inputs are to be considered when quoted prices for the identical asset or liability are not available. If the asset or liability being measured has a contractual term, a Level 2 input must be observable for substantially the entire term. These inputs include

- Quoted prices for similar assets or liabilities in active markets

- Quoted prices for identical or similar assets or liabilities in markets that are not active.

- Inputs other than quoted prices that are observable for the asset or liability (e.g., interest rates and yield curves observable at commonly quoted intervals; implied volatilities; credit spreads; and market-corroborated inputs).

Adjustments made to Level 2 inputs necessary to reflect fair value, if any, will vary depending on an analysis of specific factors associated with the asset or liability being measured. These factors include

- Condition or location

- Extent to which the inputs relate to items comparable to the asset

- Volume or level of activity in the markets in which the inputs are observed.

Depending on the level of the fair value input hierarchy in which the inputs used to measure the adjustment are classified, an adjustment that is significant to the fair value measurement in its entirety could render the measurement a Level 3 measurement.

Level 3 inputs. Level 3 inputs are unobservable inputs. These are necessary when little, if any, market activity occurs for the asset or liability. Level 3 inputs assumptions that a market participant would use when pricing the asset or liability including assumptions about risk. The best information available in the circumstances is to be used to develop the Level 3 inputs. This information might begin with internal data of the reporting entity. Cost-benefit considerations apply in that management is not required to “undertake all possible efforts” to obtain information about the assumptions that would be made by market participants. Attention is to be paid, however, to information available to management without undue cost and effort and, consequently, management's internal assumptions used to develop unobservable inputs are to be adjusted if such information contradicts those assumptions.

Inputs based on bid and ask prices. Quoted bid prices represent the maximum price at which market participants are willing to buy an asset; quoted ask prices represent the minimum price at which market participants are willing to sell an asset. If available market prices are expressed in terms of bid and ask prices, management is to use the price within the bid-ask spread (the range of values between bid and ask prices) that is most representative of fair value irrespective of where in the fair value hierarchy the input would be classified. ASC 820 permits the use of pricing conventions such as midmarket pricing as a practical alternative for determining fair value measurements within a bid-ask spread. The use of bid prices for asset valuations and ask prices for liability valuations is permitted but not required.

Categorizing inputs. Categorization of inputs as to the level of the hierarchy in which they fall serves two purposes. First, it provides the evaluator with a means of prioritizing assumptions used as to their level of objectivity and verifiability in the marketplace. Second, as discussed later in this chapter, the hierarchy provides a framework to provide informative disclosures that enable readers to assess the reliability and market observability of the fair value estimates embedded in the financial statements.

In making a particular measurement of fair value, the inputs used may be classifiable in more than one of the levels of the hierarchy. When this is the case, the inputs used in the fair value measurement in its entirety are to be classified in the level of the hierarchy in which the lowest level input that is significant to the measurement is classified.

It is important to assess available inputs and their relative classification in the hierarchy prior to selecting the valuation technique or techniques to be applied to measure fair value for a particular asset or liability. The objective, in selecting from among alternative calculation techniques, would be to select the technique or combination of techniques that maximizes the use of observable inputs.

Valuation techniques.

In measuring fair value, management employs one or more valuation techniques consistent with the market approach, the income approach, and/or the cost approach. As previously discussed, the selection of a particular technique (or techniques) to measure fair value is to be based on its appropriateness to the asset or liability being measured, maximizing the use of observable inputs and minimizing the use of unobservable inputs.

In certain situations, such as when using Level 1 inputs, use of a single valuation technique will be sufficient. In other situations, such as when valuing a reporting unit, management may need to use multiple valuation techniques. When doing so, the results yielded by applying the various techniques are evaluated considering the reasonableness of the range of values. The fair value is the point within the range that is most representative of fair value in the circumstances.

Management is required to consistently apply the valuation techniques it elects to use to measure fair value. It would be appropriate to change valuation techniques or how they are applied if the change results in fair value measurements that are equally or more representative of fair value. Situations that might give rise to such a change would be when new markets develop, new information becomes available, previously available information ceases to be available, valuation techniques improve, or market conditions change. Revisions that result from either a change in valuation technique or a change in the application of a valuation technique are to be accounted for as changes in accounting estimate under ASC 250.

Market approach. The market approach to valuation uses information generated by actual market transactions for identical or comparable assets or liabilities (including a business in its entirety). Market approach techniques often will use market multiples derived from a set of comparable transactions for the asset or liability or similar items. The evaluator needs to consider both qualitative and quantitative factors in determining the point within the range that is most representative of fair value. An example of a market approach is matrix pricing. This is a mathematical technique used primarily for the purpose of valuing debt securities without relying solely on quoted prices for the specific securities. Matrix pricing uses factors such as the stated interest rate, maturity, credit rating, and quoted prices of similar issues to develop the issue's current market yield.

Cost approach. The cost approaches are based on quantifying the amount required to replace an asset's remaining service capacity (i.e., the asset's current replacement cost). A valuation technique classified as a cost approach would measure the cost to a market participant (buyer) to acquire or construct a substitute asset of comparable utility, adjusted for obsolescence. Obsolescence adjustments include factors for physical wear and tear, improvements to technology, and economic (external) obsolescence. Thus, obsolescence is a broader concept than financial statement depreciation which simply represents a cost allocation convention and is not intended to be used as a valuation technique.

Income approach. Techniques classified as income approaches measure fair value based on current market expectations about future amounts (such as cash flows or net income) and discount them to an amount in measurement date dollars. Valuation techniques that follow an income approach include the Black-Scholes-Merton model (a closed-form model) and binomial or lattice models (open-form models), which use present value techniques, as well as the multiperiod excess earnings method that is used in fair value measurements of certain intangible assets such as in-process research and development.

Measurement considerations

Initial recognition. When the reporting entity first acquires an asset or incurs (or assumes) a liability in an exchange transaction, the transaction price is an entry price, the price paid to acquire the asset and the price received to assume the liability. Fair value measurements are based not on entry prices, but rather on exit prices—the price that would be received to sell the asset or paid to transfer the liability. While entry and exit prices differ conceptually, in many cases they may be identical and can be considered to represent fair value of the asset or liability at initial recognition. This is not always the case, however, and in assessing fair value at initial recognition, management is to consider transaction-specific factors and factors specific to the assets and/or liabilities that are being initially recognized. Examples of situations where transaction price might not represent fair value at initial recognition include

- Related-party transactions, unless the entity has evidence that the transaction was entered into at market terms.

- Transactions taking place under duress or the seller is forced to accept the price, such as when the seller is experiencing financial difficulties.

- Different units of account that apply to the transaction price and the assets/liabilities being measured. This can occur, for example, where the transaction price includes other elements besides the assets/liabilities that are being measured such as unstated rights and privileges that are subject to separate measurement or when the transaction price includes transaction costs (see discussion below).

- The exchange transaction takes place in a market different from the principal or most advantageous market in which the reporting entity would sell the asset or transfer the liability. An example of this situation is when the reporting entity is a securities dealer that enters into transactions with customers in the retail market, but the principal market for the exit transaction is with other dealers in the dealer market.

(ASC 820-10-30-3A)

If another ASC Topic requires or permits fair value measurement initially and the transaction price differs from fair value, the resulting gain or loss is recognized in earnings, unless other specified.

Transaction costs. Transaction costs are the incremental direct costs that would be incurred to sell an asset or transfer a liability. While, as previously discussed, transaction costs are considered in determining the market that is most advantageous, they are not used to adjust the fair value measurement of the asset or liability being measured. FASB excluded them from the measurement because they are not characteristic of an asset or liability being measured. (ASC 820-10-35-9B)

Transportation costs. If an attribute of the asset or liability being measured is its location, the price determined in the principal or most advantageous market is to be adjusted for the costs that would be incurred by the reporting entity to transport it to or from that market. (ASC 820-10-35-9C)

Fair Value Disclosures

Substantial disclosures regarding fair value are required by various ASC Topics. In the preparation of the financial statements, these disclosures are often placed in different informative notes including descriptions of the entity's accounting policies, financial instruments, impairment, derivatives, pensions, revenue recognition, share-based compensation, risks and uncertainties, certain significant estimates, etc. ASC 820 encourages preparers to combine disclosure requirements under ASC 820 with those of other subtopics. Plan assets of a defined benefit pension plan or other postretirement plans accounted for under ASC 715 are not subject to the ASC 820 requirements and should apply the disclosure requirements in the relevant paragraphs of ASC 715.

Objectives.

ASC 820-10-50-1 requires a reporting entity to disclose information that helps financial statements users to assess:

- For assets and liabilities that are measured at fair value on a recurring or nonrecurring basis in the statement of financial position after initial recognition, the valuation techniques and inputs used to develop those measures.

- For recurring fair value measurements using significant unobservable inputs (Level 3), the effect of the measurements on earnings (or change to net assets) or other comprehensive income for the period. (ASC 820-10-50-1)

To meet these objectives, preparers must consider the level of detail necessary to satisfy the requirement, how much emphasis to place on each of the requirements, how much to aggregate or disaggregate, and whether additional information is needed to evaluate the information disclosed. (ASC 820-10-50-1A)

ASU 2011-04 expanded and revised the fair value disclosures, including new requirements for Level 3 measurements, disclosures regarding transfers between levels, and highest and best use of a nonfinancial asset. There are no exceptions for public companies. However, nonpublic entities are not required to

- Disclose information regarding transfers between Levels 1 and 2,

- Include a narrative description regarding the sensitivity of fair value measurements to changes in unobservable inputs that result in significant changes,

- Disclose related items not reported at fair value, but for which fair value is disclosed.

ASU 2013-03 further clarified that nonpublic entities are not required to disclose the level of the fair value measurement for items that are not measured at fair value in the statement of financial position but for which fair value is disclosed.

A list of the required disclosures can be found in the Appendix.