51 ASC 830 FOREIGN CURRENCY MATTERS

Translation of Foreign Currency Financial Statements

Selection of the functional currency

Example of the current rate method

Example of the remeasurement method

Cessation of highly inflationary condition

Applying ASC 740 to foreign entity financials restated for general price levels

Summary of Current Rate and Remeasurement Methods

Application of ASC 830 to an investment to be disposed of that is evaluated for impairment

Foreign Operations in the United States

Translation of Foreign Currency Transactions

Example of foreign currency transaction translation

Intercompany Transactions and Elimination of Intercompany Profits

Example of intercompany transactions involving foreign exchange

Example of hedge effectiveness measurement

Example of a forward exchange contract

Accounts to Be Remeasured Using Historical Exchange Rates

PERSPECTIVE AND ISSUES

Subtopics

ASC 830 contains five subtopics:

- ASC 830-10, Overall

- ASC 830-20, Foreign Currency Transactions

- ASC 830-30, Translation of Financial Statements

- ASC 830-250, Statement of Cash Flows

- ASC 830-740, Income Taxes.

ASC 830 provides guidance about

- Foreign transaction and

- Translation of financial statements.

Scope and Scope Exceptions

ASC 830 applies to all entities. ASC 830-20 does not apply to derivative instruments. Preparers should look to ASC 815 for guidance on derivatinves.

Overview

To facilitate the proper analysis of foreign operations by financial statement users, transactions and financial statements denominated in foreign currencies must be expressed in a common currency (i.e., US dollars). The GAAP governing the translation of foreign currency financial statements and the accounting for foreign currency transactions are found primarily in Accounting Standards Codification (ASC) 830, Foreign Currency Matters. These principles apply to the translation of:

- Foreign currency transactions (e.g., exports, imports, and loans) that are denominated in other than a company's functional currency

- Foreign currency financial statements of branches, divisions, subsidiaries, and other investees that are incorporated into the financial statements of a company reporting under US GAAP by combination, consolidation, or application of the equity method.

The objectives of translation are to provide

- Information relative to the expected economic effects of rate changes on an enterprise's cash flows and equity

- Information in consolidated statements relative to the financial results and relationships of each individual foreign consolidated entity as reflected by the functional currency of each reporting entity.

Companies sometimes use hedging strategies to attempt to manage their risk and minimize their exposure to fluctuations in the exchange rates of foreign currencies. Hedge accounting under ASC 815, Derivatives and Hedging, is addressed at the end of this chapter.

Technical Alert

In March 2013, the FASB released ASU 2013-05, Foreign Currency Matters (Topic 830) Parent's accounting for the Cumulative Translation Adjustment upon Derecognition of Certain Subsidiaries or Groups of Assets within a Foreign Entity or of an Investment in a Foreign Entity. The ASU is designed to eliminate the diversity in practice as to how a parent releases to net income the foreign currency adjustment when the parent sells or no longer holds a controlling interest in a foreign entity or a group of assets that is a nonprofit activity or business within a foreign entity. The ASU requires that when a parent ceases to hold a controlling interest within a foreign entity, the parent should apply ASC 830-30 and release any cumulative foreign translation adjustment into net income. For an equity method investment in a foreign entity, the partial sale guidance in ASC 830-40 still applies.

The update is effective prospectively for fiscal years beginning after and December 15, 2013 and a year later for nonpublic companies. Prior periods should not be adjusted. Early adoption is permitted.

DEFINITIONS OF TERMS

Conversion. The exchange of one currency for another.

Current exchange rate. The rate at which one unit of a currency can be exchanged for (converted into) another currency. For purposes of translation of financial statements in accordance with ASC 830, the current exchange rate is the rate at the end of the period covered by the financial statements or at the dates of recognition in those statements with respect to revenues, expenses, gains, and losses.

Discount or premium on a forward contract. The foreign currency amount of the contract multiplied by the difference between the contracted forward rate and the spot rate at the date of inception of the contract.

Foreign currency. A currency other than the functional currency of the reporting entity being referred to (for example, the US dollar could be a foreign currency for a foreign entity). Composites of currencies, such as the Special Drawing Rights on the International Monetary Fund (SDR), used to set prices, denominate amounts of loans, and the like have the characteristics of foreign currency for purposes of applying ASC 830.

Foreign currency statements. Financial statements that employ as the unit of measure a functional currency that is not the reporting currency of the enterprise.

Foreign currency transactions. Transactions whose terms are denominated in a currency other than the reporting entity's functional currency. Foreign currency transactions arise when an enterprise (1) buys or sells goods or services on credit whose prices are denominated in foreign currency, (2) borrows or lends funds and the amounts payable or receivable are denominated in foreign currency, (3) is a party to an unperformed forward exchange contract, or (4) for other reasons, acquires or disposes of assets or incurs or settles liabilities denominated in foreign currency.

Foreign currency translation. The process of expressing in the enterprise's reporting currency amounts that are denominated or measured in a different currency.

Forward exchange contract. An agreement to exchange at a specified future date currencies of different countries at a specified rate (forward rate).

Functional currency. The currency of the primary economic environment in which the entity operates; normally, the currency of the environment in which the entity primarily generates and expends cash.

Local currency. The currency of a particular country being referred to.

Monetary items. Cash, claims to receive a fixed amount of cash, and obligations to pay a fixed amount of cash.

Nonmonetary items. All statement of financial position items other than cash, claims to cash, and cash obligations.

Remeasurement. If an entity's accounting records are not maintained in its functional currency, remeasurement is the process necessary to convert those records into the functional currency, with the objective of reflecting the same results as if the records had been maintained in the functional currency. Monetary balances are translated by using the current exchange rate, and nonmonetary balances are translated by using historical exchange rates. In the event that remeasurement into the functional currency is required, it must be done prior to translation into the reporting currency.

Reporting currency. The currency used by the entity to prepare its financial statements.

Reporting enterprise. An entity or group of entities whose financial statements are being referred to. For the purposes of this discussion, those financial statements reflect (1) the financial statements of one or more foreign operations by combination, consolidation, or equity method accounting; (2) foreign currency transactions; or (3) both.

Spot rate. The exchange rate for immediate delivery of currencies exchanged.

Transaction date. The date on which a transaction (for example, a sale or purchase of merchandise or services) is recognized in accounting records in conformity with GAAP. A long-term commitment may have more than one transaction date (for example, the due date of each progress payment under a construction contract is an anticipated transaction date).

Transaction gain or loss. Transaction gains or losses result from a change in exchange rates between the functional currency and the currency in which a foreign currency transaction is denominated. They represent an increase or decrease in (1) the actual functional currency cash flows realized upon settlement of foreign currency transactions and (2) the expected functional currency cash flows on unsettled foreign currency transactions.

Translation adjustments. Translation adjustments result from the process of translating financial statements from the entity's functional currency into the reporting currency.

CONCEPTS, RULES, AND EXAMPLES

Translation of Foreign Currency Financial Statements

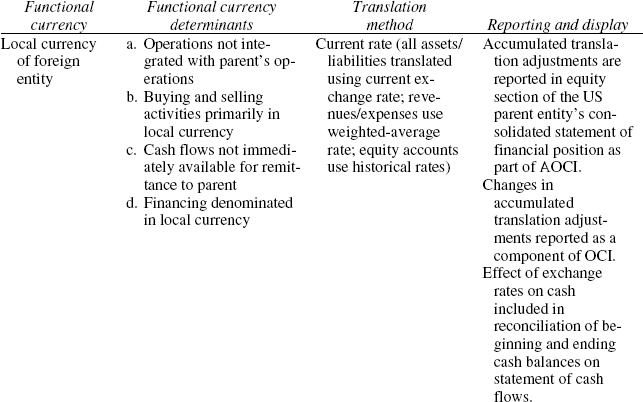

Selection of the functional currency.

Before the financial statements of a foreign branch, division, or subsidiary are translated into US dollars, the management of the US entity must make a decision as to which currency is the functional currency of the foreign entity. Once chosen, the functional currency cannot be changed unless economic facts and circumstances have clearly changed. Additionally, previously issued financial statements are not restated for any changes in the functional currency. The functional currency decision is crucial, because different translation methods are applied which may have a material effect on the US entity's financial statements.

FASB defines functional currency but does not list definitive criteria that, if satisfied, would with certainty result in the identification of an entity's functional currency. Rather, realizing that such criteria would be difficult to develop, FASB listed various factors that were intended to give management guidance in making the functional currency decision. These factors include:

- Cash flows (Do the foreign entity's cash flows directly affect the parent's cash flows and are they immediately available for remittance to the parent?)

- Sales prices (Are the foreign entity's sales prices responsive to exchange rate changes and to international competition?)

- Sales markets (Is the foreign entity's sales market the parent's country or are sales denominated in the parent's currency?)

- Expenses (Are the foreign entity's expenses incurred primarily in the parent's country?)

- Financing (Is the foreign entity's financing primarily from the parent or is it denominated in the parent's currency?)

- Intercompany transactions (Is there a high volume of intercompany transactions between the parent and the foreign entity?).

If the answers to the questions above are predominantly yes, the functional currency is the reporting currency of the parent entity (i.e., the US dollar). If the answers are predominantly no, the functional currency would most likely be the local currency of the foreign entity, although it is possible for a foreign currency other than the local currency to be the functional currency.

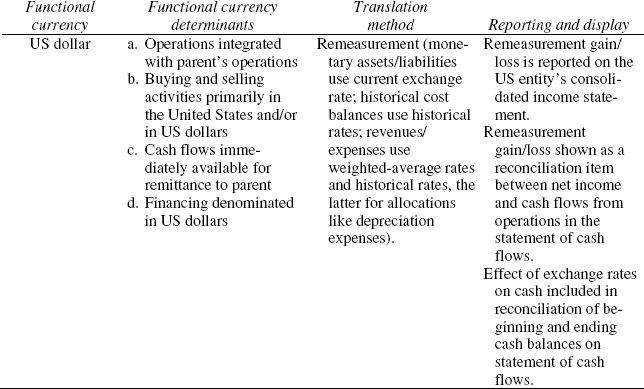

Translation methods.

To deal with discrete circumstances, FASB chose two different methods to translate an entity's foreign financial statements into US dollars: the current rate method and the remeasurement method. These are not alternatives, but rather are employed as circumstances dictate. The primary distinction between the methods is the classification of assets and liabilities (and their corresponding income statement amounts) that are translated at either the current or historical exchange rates.

The first method, known as the current rate method, is the approach mandated by ASC 830 when the functional currency is the foreign currency (e.g., the domestic currency of the foreign subsidiary or operation). All assets and liabilities are translated at the current rates, while stockholders' equity accounts are translated at the appropriate historical rate or rates. Revenues and expenses are translated at rates in effect when the transactions occur, but those that occur evenly over the year may be translated at the weighted-average rate for the year.

Note that weighted-average, if used, must take into account the actual pace and pattern of changes in exchange rates over the course of the year, which will often not be varying at a constant rate throughout the period nor, in many instances, monotonically increasing or decreasing over the period. When these conditions do not hold, it is incumbent upon the reporting entity to develop a weighted-average exchange rate that is meaningful under the circumstances. When coupled with transactions (sales, purchases, et al.) that also have not occurred evenly throughout the year, this determination can become a fairly complex undertaking, requiring careful attention.

The theoretical basis for the current rate method is the “net investment concept,” wherein the foreign entity is viewed as a separate entity in which the parent invested, rather than being considered part of the parent's operations. FASB's reasoning was that financial statement users can benefit most when the information provided about the foreign entity retains the relationships and results created in the environment (economic, legal, and political) in which the entity operates. Converting all assets and liabilities at the same current rate accomplishes this objective.

The rationale for this approach is that foreign-denominated debt is often used to purchase assets that create foreign-denominated revenues. These revenue-producing assets act as a natural hedge against changes in the settlement amount of the debt due to changes in the exchange rate. The excess (net) assets—which are the US parent entity's net equity investment in the foreign operation—will, however, be affected by this foreign exchange risk, and this effect is recognized by the parent.

The second utilized method, the remeasurement method, has also been referred to as the monetary/nonmonetary method. This approach is required by ASC 830 when the foreign entity's accounting records are not maintained in the functional currency (e.g., when the US dollar is designated as the functional currency for a Brazilian subsidiary). This method translates monetary assets (cash and other assets and liabilities that will be settled in cash) at the current rate. Nonmonetary assets, liabilities, and stockholders' equity are translated at the appropriate historical rates. The appropriate historical rate would be the exchange rate at the date the transaction involving the nonmonetary account originated. Also, the income statement amounts related to nonmonetary assets and liabilities, such as cost of goods sold (inventory), depreciation (property, plant, and equipment), and intangibles amortization (patents, copyrights), are translated at the same rate as used for the related statement of financial position translation. Other revenues and expenses occurring evenly over the year may be translated at the weighted-average exchange rate in effect during the period, subject to the considerations discussed above.

Thus, to summarize, if the foreign entity's local currency is the functional currency, ASC 830 requires use of the current rate method when translating the foreign entity's financial statements. If, on the other hand, the US dollar (or other nonlocal currency) is the functional currency, ASC 830 requires the remeasurement method when translating the foreign entity's financial statements. Both of these methods are illustrated below. All amounts in the following two illustrations, other than exchange rates, are in thousands.

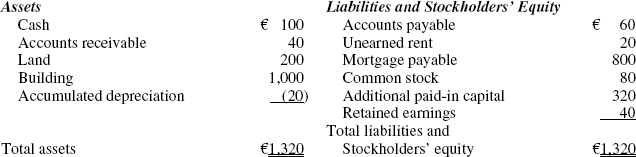

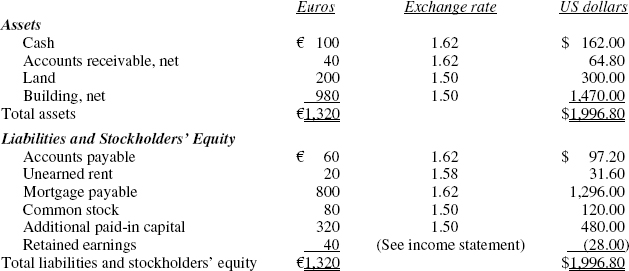

Assume that a US entity has a 100% owned subsidiary in Italy that commenced operations in 2011. The subsidiary's operations consist of leasing space in an office building. This building, which cost one million euros, was financed primarily by Italian banks. All revenues and cash expenses are received and paid in euros. The subsidiary also maintains its accounting records in euros. As a result, management of the US entity has decided that the euro is the functional currency of the subsidiary.

The subsidiary's statement of financial position at December 31, 2012, and its combined statement of income and retained earnings for the year ended December 31, 2012, are presented below in euros.

Italian Company

Statement of Financial Position

At December 31, 2012

(€000 omitted)

Italian Company

Statement of Income and Retained Earnings

For the Year Ended December 31, 2012

(€000 omitted)

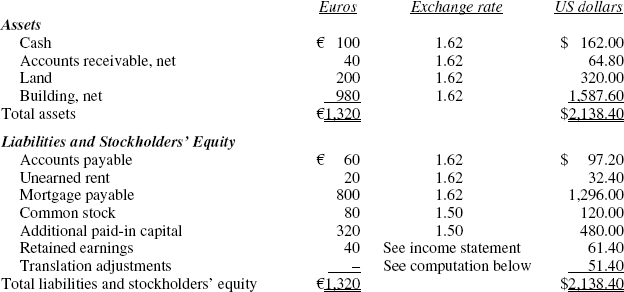

Various exchange rates for 2012 are as follows:

| €1 = | $1.50 at the beginning of 2012 (when the common stock was issued and the land and building were financed through the mortgage) |

| €1 = | $1.55 weighted-average for 2012 |

| €1 = | $1.58 at the date the dividends were declared and paid and the unearned rent was received |

| €1 = | $1.62 at the end of 2012 |

Since the euro is the functional currency, the Italian Company's financial statements must be translated into US dollars by the current rate method. This translation process is illustrated below.

Italian Company

Statement of Financial Position Translation

(The euro is the functional currency)

At December 31, 2012

(€/$000 omitted)

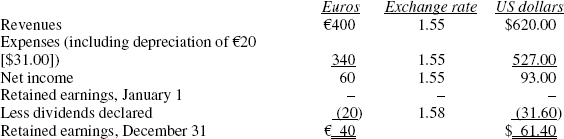

Italian Company

Statement of Income and Retained Earnings

Statement Translation

(The euro is the functional currency)

For the Year Ended December 31, 2012

(€/$000 omitted)

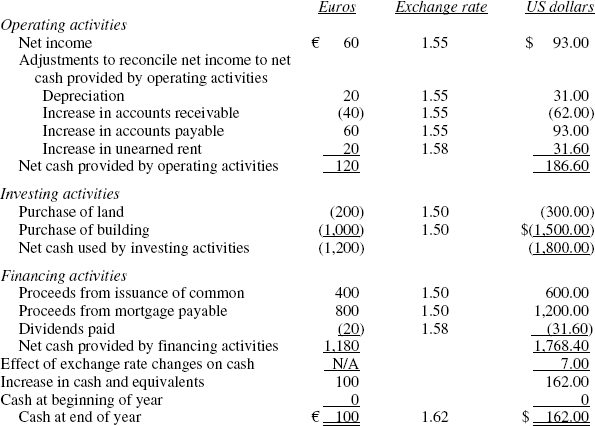

Italian Company

Statement of Cash Flows

Statement Translation

(The euro is the functional currency)

For the Year Ended December 31, 2012

(€/$000 omitted)

Note the following points concerning the current rate method:

- All assets and liabilities are translated using the current exchange rate at the date of the statement of financial position (€1 = $1.62). All revenues and expenses are translated at the rates in effect when these items are recognized during the period. Due to practical considerations, however, weighted-average rates can be used to translate revenues and expenses (€1 = $1.55).

- Stockholders' equity accounts are translated by using historical exchange rates. Common stock was issued at the beginning of 2012 when the exchange rate was €1 = $1.50. The translated balance of retained earnings is the result of the weighted-average rate applied to revenues and expenses and the specific rate in effect when the dividends were declared (€1 = $1.58).

- Translation adjustments result from translating all assets and liabilities at the current rate, while stockholders' equity is translated by using historical and weighted-average rates. The adjustments have no direct effect on cash flows. Also, the translation adjustment is due to the net investment rather than the subsidiary's operations. For these reasons, the cumulative translation adjustments balance is reported as a component of accumulated other comprehensive income (AOCI) in the stockholders' equity section of the US parent entity's consolidated statement of financial position. This balance essentially equates the total debits of the subsidiary (now expressed in US dollars) with the total credits (also in dollars). It also may be determined directly, as shown next, to verify the translation process.

- The translation adjustments credit of $30.70 is calculated as follows for the differences between the exchange rate of $1.62 at the end of the year and the applicable exchange rates used to translate changes in net assets:

- The translation adjustments balance that appears as a component of AOCI in the stockholders' equity section is cumulative in nature. Consequently, the change in this balance during the year is disclosed as a component of other comprehensive income (OCI) for the period. In the illustration, this balance went from zero to $51.40 at the end of 2012. In addition, assume the following occurred during the following year, 2013:

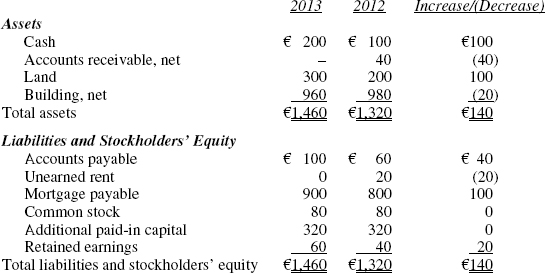

Italian Company

Statement of Financial Position

At December 31

(€000 omitted)

Italian Company

Statement of Income and Retained Earnings

For the Year Ended December 31, 2013

(€000 omitted)

Exchange rates were

€1 = $1.62 at the beginning of 2013 €1 = $1.65 weighted-average for 2013 €1 = $1.71 at the end of 2013 €1 = $1.68 when dividends were declared in 2013 and additional land bought by incurring mortgage The translation process for 2013 is illustrated below.

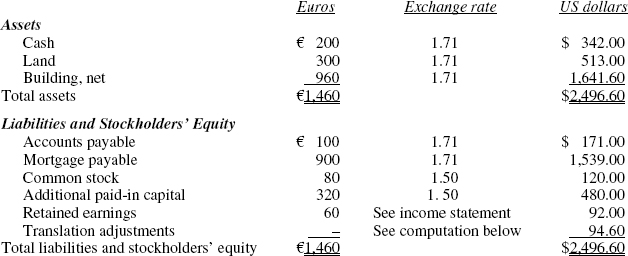

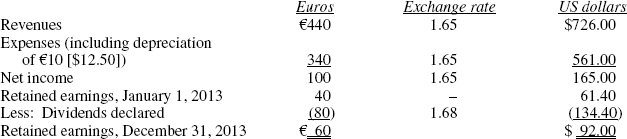

Italian Company

Statement of Financial Position Translation

(The euro is the functional currency)

At December 31, 2013

(€/$000 omitted)

Italian Company

Statement of Income and Retained Earnings

Statement Translation

(The euro is the functional currency)

For the Year Ended December 31, 2013

(€/$000 omitted)

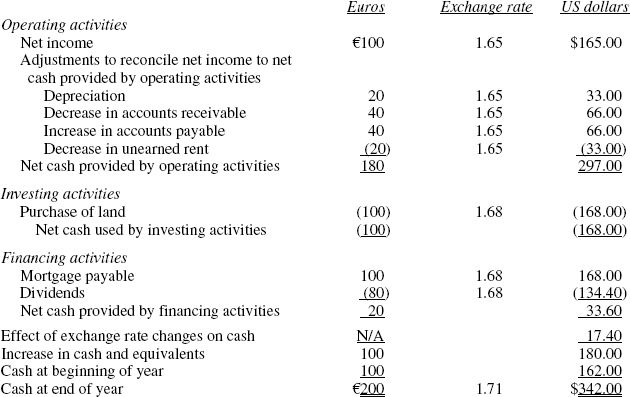

Italian Company

Statement of Cash Flows

Statement Translation

(The euro is the functional currency)

For the Year Ended December 31, 2013

(€/$000 omitted)

Using the analysis presented before, the change in the translation adjustment attributable to 2013 is computed as follows:

The balance in the cumulative translation adjustment component of AOCI at the end of 2013 is $94.60. ($51.40 from 2012 and $43.20 from 2013.)

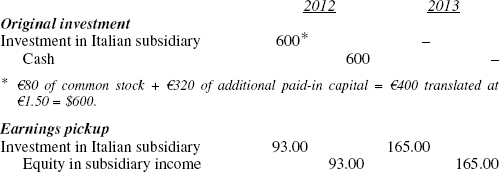

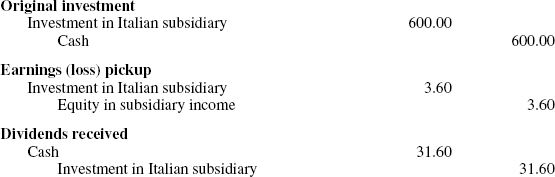

- The use of the equity method by the US parent entity in accounting for the subsidiary would result in the following journal entries (in $000s), based upon the information presented above:

Note that in applying the equity method to record this activity in the US parent entity's accounting records, the parent's stockholders' equity should be the same whether or not the Italian subsidiary is consolidated. Since the subsidiary does not report the translation adjustments on its financial statements, care should be exercised so that it is not forgotten in the application of the equity method.

- If the US entity disposes of its investment in the Italian subsidiary, the cumulative translation adjustments balance becomes part of the gain or loss that results from the transaction and is eliminated. For example, assume that on January 2, 2014, the US entity sells its entire investment for €465 thousand. The exchange rate at this date is €1 = $1.71. The balance in the investment account at December 31, 2013, is $786,600 as a result of the entries made previously.

The following entries would be made by the US parent entity to reflect the sale of the investment:

If the US entity had sold only a portion of its investment in the Italian subsidiary, only a pro rata portion of the accumulated translation adjustments balance would have become part of the gain or loss from the transaction. To illustrate, if 80% of the Italian subsidiary was sold for €372 on January 2, 2013, the following journal entries would be made:

An exchange rate might not be available if there is a temporary suspension of foreign exchange trading. ASC 830-30-55 provides that, if exchangeability between two currencies is temporarily lacking at a transaction date or the date of the statement of financial position, the first subsequent rate at which exchanges could be made is to be used to implement ASC 830.

In the previous situation, the euro was the functional currency because the Italian subsidiary's cash flows were primarily in euros. Assume, however, that the financing of the land and building was denominated in US dollars instead of euros and that the mortgage payable is denominated in US dollars (i.e., it must be repaid in US dollars). Although the rents collected and the majority of the cash flows for expenses are in euros, management has decided that, due to the manner of financing, the US dollar is the functional currency. The accounting records, however, are maintained in euros.

The remeasurement of the Italian financial statements is accomplished by use of the remeasurement method (also known as the monetary/nonmonetary method). This method is illustrated below using the same information that was presented before for the Italian subsidiary.

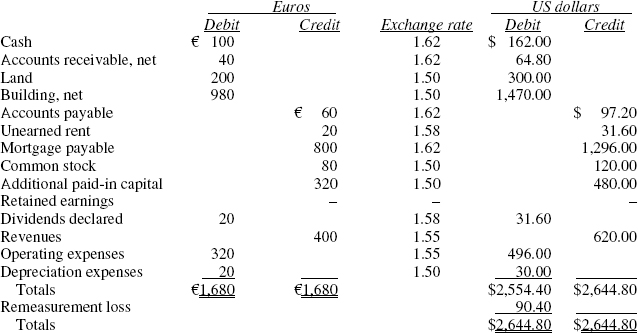

Italian Company

Statement of Financial Position (Remeasurement)

(The US dollar is the functional currency)

At December 31, 2012

(€/$000 omitted)

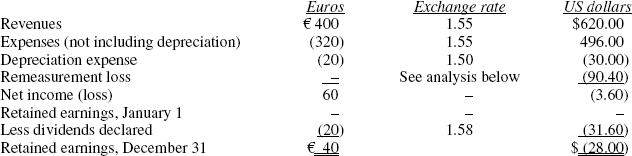

Italian Company

Statement of Income and Retained Earnings (Remeasurement)

(The US dollar is the functional currency)

For the Year Ended December 31, 2012

(€/$000 omitted)

Italian Company

Remeasurement Loss

(The US dollar is the functional currency)

For the Year Ended December 31, 2012

(€/$000 omitted)

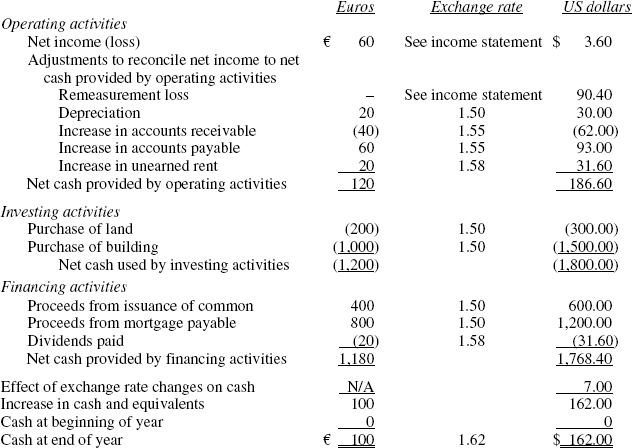

Italian Company

Statement of Cash Flows (Remeasurement)

(The US dollar is the functional currency)

For the Year Ended December 31, 2012

(€/$000 omitted)

Note the following points concerning the remeasurement method:

- Assets and liabilities that have historical cost balances (nonmonetary assets and liabilities) are remeasured by using historical exchange rates (i.e., the rates in effect when the transactions giving rise to the balance first occurred). Monetary assets and monetary liabilities, cash and those items that will be settled in cash, are remeasured by using the current exchange rate at the date of the statement of financial position. In 2012, the unearned rent from year-end 2012 of €10 would be remeasured at the rate of €1 = $1.58. The unearned rent at the end of 2012 is not considered a monetary liability. Therefore, the $1.58 historical exchange rate is used for all applicable future years. See the the final section of this chapter, titled “Accounts to Be Remeasured Using Historical Exchange Rates” for a listing of accounts that are remeasured using historical exchange rates.

- Revenues and expenses that occur frequently during a period are remeasured, for practical purposes, by using the weighted-average exchange rate for the period. Revenues and expenses that represent allocations of historical balances (e.g., depreciation, cost of goods sold, and amortization of intangibles) are remeasured using historical exchange rates. Note that this is a different treatment as compared to the current rate method.

- If the functional currency is the US dollar rather than the local foreign currency, the amounts of specific line items presented in the reconciliation of net income to net cash flow from operating activities will be different for nonmonetary items (e.g., depreciation).

- The calculation of the remeasurement gain (loss), in a purely mechanical sense, is the amount needed to make the dollar debits equal the dollar credits in the Italian entity's trial balance.

- The remeasurement loss of $90.40 is reported on the US parent entity's consolidated income statement because the US dollar is the functional currency. When the reporting currency is the functional currency, as it is in this example, it is assumed that all of the foreign entity's transactions occurred in US dollars (even if this was not the case). Accordingly, remeasurement gains and losses are taken immediately to the income statement in the year in which they occur as they can be expected to have direct cash flow effects on the parent entity. They are not deferred as a translation adjustments component of AOCI, as they were when the functional currency was the euro (applying the current rate method).

- The use of the equity method of accounting for the subsidiary would result in the following entries by the US parent entity during 2012:

Note that remeasurement gains and losses are included in the subsidiary's net income (net loss) as determined in US dollars before the earnings (loss) pickup is made by the US entity.

- In economies in which—per ASC 830-10-45—cumulative inflation is greater than 100% over a three-year period, FASB requires that the functional currency be the reporting currency, that is, the US dollar. Projections of future inflation cannot be used to satisfy this threshold condition. The remeasurement method must be used in this situation even though the factors indicate the local currency is the functional currency. FASB made this decision to prevent the evaporation of the foreign entity's fixed assets, a result that would occur if the local currency was the functional currency.

Cessation of highly inflationary condition.

When a foreign subsidiary's economy is no longer considered highly inflationary, the entity converts the reporting currency values into the local currency at the exchange rates on the date of change on which these values become the new functional currency accounting bases for nonmonetary assets and liabilities.

Furthermore, ASC 830-740 states that when a change in functional currency designation occurs because an economy ceases to be highly inflationary, the deferred taxes on the temporary differences that arise as a result of a change in the functional currency are treated as an adjustment to the cumulative translation adjustments portion of stockholders' equity (accumulated other comprehensive income).

Applying ASC 740 to foreign entity financials restated for general price levels.

Price-level-adjusted financial statements are preferred for foreign currency financial statements of entities operating in highly inflationary economies when those financial statements are intended for readers in the United States. If this recommendation is heeded, the result is that the income tax bases of the assets and liabilities are often restated for inflation. ASC 830-740 provides guidance on applying the asset-and-liability approach of ASC 740 as it relates to such financial statements. It discusses (1) how temporary differences are to be computed under ASC 740 and (2) how deferred income tax expense or benefit for the year is to be determined.

With regard to the first issue, temporary differences are computed as the difference between the indexed income tax basis amount and the related price-level restated amount of the asset or liability. The consensus reached on the second issue is that the deferred income tax expense or benefit is the difference between the deferred income tax assets and liabilities reported at the end of the current year and those reported at the end of the prior year. The deferred income tax assets and liabilities of the prior year are recalculated in units of the current year-end purchasing power.

On a related matter, ASC 830-10-45 states that, when the functional currency changes to the reporting currency because the foreign economy has become highly inflationary, ASC 740 prohibits recognition of deferred income tax benefits associated with indexing assets and liabilities that are remeasured in the reporting currency using historical exchange rates. Any related income tax benefits would be recognized only upon their being realized for income tax purposes. Any deferred income tax benefits that had been recognized for indexing before the change in reporting currency is effected are eliminated when the related indexed amounts are realized as income tax deductions.

Summary of Current Rate and Remeasurement Methods

- Before foreign currency financial statements can be translated into US dollars, management of the US parent entity must select the functional currency for the foreign entity whose financial statements will be incorporated into theirs by consolidation, combination, or the equity method. As the examples illustrated, this decision is important because it may have a material effect upon the financial statements of the US entity.

- If the functional currency is the local currency of the foreign entity, the current rate method is used to translate foreign currency financial statements into US dollars. All assets and liabilities are translated by using the current exchange rate at the date of the statement of financial position. This method insures that all financial relationships remain the same in both local currency and US dollars. Owners' equity is translated using historical rates, while revenues (gains) and expenses (losses) are translated at the rates in existence during the period when the transactions occurred. A weighted-average rate can be used for items occurring frequently throughout the period. The translation adjustments (debit or credit) that result from the application of these rules are reported in other comprehensive income and then accumulated and reported as a separate component of stockholders' equity of the US entity's consolidated statement of financial position (or parent-only statement of financial position if consolidation is deemed not to be appropriate).

- If the functional currency is the parent entity's reporting currency (the US dollar), the foreign currency financial statements are remeasured in US dollars. All foreign currency balances are restated in US dollars using both historical and current exchange rates. Foreign currency balances that reflect prices from past transactions are remeasured using historical rates, while foreign currency balances which reflect prices from current transactions are remeasured using the current exchange rate. Remeasurement gains/losses that result from the remeasurement process applied to foreign subsidiaries that are consolidated are reported on the US parent entity's consolidated income statement.

The above summary is arranged in tabular form as shown below.

Application of ASC 830 to an investment to be disposed of that is evaluated for impairment.

Under ASC 830, accumulated foreign currency translation adjustments are reclassified to net income only when realized upon sale or upon complete or substantially complete liquidation of the investment in the foreign entity. ASC 830-30-45 addresses whether a reporting entity is to include the translation adjustments in the carrying amount of the investment in assessing impairment of an investment in a foreign entity that is held for disposal if the planned disposal will cause some or all of the translation adjustments to be reclassified to net income. The standard points out that an entity that has committed to a plan that will cause the translation adjustments for an equity-method investment or consolidated investment in a foreign entity to be reclassified to earnings is to include the translation adjustments as part of the carrying amount of the investment when evaluating that investment for impairment. An entity would also include the portion of the translation adjustments that represents a gain or loss from an effective hedge of the net investment in a foreign operation as part of the carrying amount of the investment when making this evaluation.

Foreign Operations in the United States

With the world economy as interconnected as it is, entities in the United States are sometimes the subsidiaries of parent companies domiciled elsewhere in the world. The financial statements of the US entity may be presented separately in the United States or may be combined as part of the financial statements in the foreign country.

In general, financial statements of US companies are prepared in accordance with US GAAP. However, adjustments may be necessary to conform these financial statements to the accounting principles of the foreign country of the parent entity where they will be consolidated.

Translation of Foreign Currency Transactions

According to ASC 830, a foreign currency transaction is a transaction “. . . denominated in a currency other than the entity's functional currency.” Denominated means that the amount to be received or paid is fixed in terms of the number of units of a particular foreign currency regardless of changes in the exchange rate. From the viewpoint of a US entity, a foreign currency transaction results when it imports or exports goods or services to or from a foreign entity or makes a loan involving a foreign entity and agrees to settle the transaction in currency other than the US dollar (the functional currency of the US entity). In these situations, the US entity has “crossed currencies” and directly assumes the risk of fluctuating exchange rates of the foreign currency in which the transaction is denominated. This risk may lead to recognition of foreign exchange transaction gains or losses in the income statement of the US entity. Note that transaction gains or losses can result only when the foreign transactions are denominated in a foreign currency. When a US entity imports or exports goods or services and the transaction is to be settled in US dollars, the US entity is not exposed to a foreign exchange gain or loss because it bears no risk due to exchange rate fluctuations.

The following example illustrates the terminology and procedures applicable to the translation of foreign currency transactions. Assume that US Company, an exporter, sells merchandise to a customer in Italy on December 1, 2012, for €10,000. Receipt is due on January 31, 2013 and US Company prepares financial statements on December 31, 2012. At the transaction date (December 1, 2012), the spot rate for immediate exchange of foreign currencies indicates that €1 is equivalent to $1.30. To find the US dollar equivalent of this transaction, the foreign currency amount, €10,000, is multiplied by $1.30 to get $13,000. At December 1, 2012, the foreign currency transaction is recorded by US Company in the following manner:

![]()

The accounts receivable and sales are measured in US dollars at the transaction date using the spot rate at the time of the transaction. While the accounts receivable is measured and reported in US dollars, the receivable is denominated or fixed in euros. This characteristic may result in foreign exchange transaction gains or losses if the spot rate for the euro changes between the transaction date and the date the transaction is settled (January 31, 2013).

If financial statements are prepared between the transaction date and the settlement date, all receivables and liabilities denominated in a currency other than the functional currency (the US dollar) must be restated to reflect the spot rates in effect at the statement of financial position date. Assume that on December 31, 2012, the spot rate for euros is €1 = $1.32. This means that the €10,000 are now worth $13,200 and that the accounts receivable denominated in euros has increased by $200. The following adjustment is recorded on December 31, 2012:

![]()

Note that the $13,000 credit to sales recorded on the transaction date is not affected by subsequent changes in the spot rate. This treatment exemplifies the two-transaction viewpoint adopted by FASB. In other words, making the sale is the result of an operating decision, while bearing the risk of fluctuating spot rates is the result of a financing decision. Therefore, the amount determined as sales revenue at the transaction date is not altered because of the financing decisions to wait until January 31, 2013, for payment of the account and to accept payment denominated in euros. The risk of a foreign exchange transaction loss can be avoided by (1) demanding immediate payment on December 1, 2012, (2) fixing the price of the transaction in US dollars instead of in the foreign currency, or (3) by entering into a forward exchange contract to hedge the exposed asset (accounts receivable). The fact that, in the example, US Company did not take any of these actions is reflected by recognizing foreign currency transaction gains or losses in its income statement (reported as financial or nonoperating items) in the period during which the exchange rates changed. This treatment has been criticized, however, because earnings will fluctuate because of changes in exchange rates and not because of changes in the economic activities of the enterprise.

The counterargument, however, is that economic reality is that earnings are fluctuating because the management chose to commit the reporting entity to a transaction that exposes it to economic risks and, therefore, the case can be made that the volatility in earnings faithfully represents the results of management's business decision.

On the settlement date (January 31, 2013), assume the spot rate is €1 = $1.31. The receipt of €10,000 and their conversion into US dollars is recorded as follows:

The net effect of this foreign currency transaction was to receive $13,100 in settlement from a sale that was originally measured (and recognized) at $13,000. This realized net foreign currency transaction gain of $100 is reported on two income statements—a $200 gain in 2012 and a $100 loss in 2013. The reporting of the gain or loss in two income statements causes a temporary difference in the basis of the receivable for income tax and financial reporting purposes. This results because the 2012 unrealized transaction gain of $200 is not taxable until 2013, the year the transaction was ultimately completed or settled. Accordingly, deferred income tax accounting is required to account for the effects of this temporary difference.

It is important to note that all monetary assets and liabilities of US Company that are denominated in a currency other than US Company's functional currency (the US dollar) are required to be remeasured at the date of each statement of financial position to the extent that they are affected by increases or decreases in the exchange rate. For example, a US Company whose functional currency is the US dollar holds a bank account in France that is denominated in euros. At the date of each statement of financial position, by reference to the spot rate for the euro, US Company would remeasure the carrying amount of its French bank account and record any resulting transaction gains and losses in the same manner as above.

Intercompany Transactions and Elimination of Intercompany Profits

Gains or losses from intercompany transactions are reported on the US company's consolidated income statement unless settlement of the transaction is not planned or anticipated in the foreseeable future. In that case, which is atypical, gains and losses arising from intercompany transactions are reflected in the accumulated translations adjustments component of accumulated other comprehensive income in stockholders' equity of the US entity. In the typical situation (i.e., gains and losses reported on the US entity's income statement) gains and losses result whether the functional currency is the US dollar or the foreign entity's local currency. When the US dollar is the functional currency, foreign currency transaction gains and losses result because of one of the two situations below:

- The intercompany foreign currency transaction is denominated in US dollars. In this case, the foreign subsidiary has a payable or receivable denominated in US dollars. This may result in a foreign currency transaction gain or loss that would appear on the foreign subsidiary's income statement. This gain or loss would be translated into US dollars and would appear on the US entity's consolidated income statement.

- The intercompany foreign currency transaction is denominated in the foreign subsidiary's local currency. In this situation, the US entity has a payable or receivable denominated in a foreign currency. Such a situation may result in a foreign currency transaction gain or loss that is reported on the US parent entity's income statement.

The above two cases can be easily altered to reflect what happens when the foreign entity's local currency is the functional currency. The gain or loss from each of these scenarios would be reflected on the other entity's financial statements first (i.e., the subsidiary's rather than the parent's and vice versa).

The elimination of intercompany profits due to sales and other transfers between related entities is based upon exchange rates in effect when the sale or transfer occurred. Reasonable approximations and averages are allowed to be used if intercompany transactions occur frequently during the year.

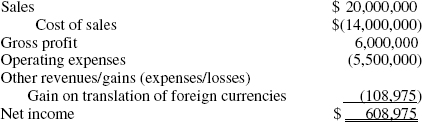

Cassiopeia Corporation buys an observatory-grade telescope from its Spanish subsidiary for €850,000, resulting in a profit for the subsidiary of €50,000 on the sale date at an exchange rate of $1: €0.6 (euros). The profit is eliminated at $1: €0.6. The payable to the subsidiary is due in 90 days, and is denominated in euros. On the payment date, the exchange rate has changed to $1: €0.65. Thus, rather than paying $1,416,667 to settle the payable, as would have been the case on the sale date, Cassiopeia must now pay $1,307,692 on the payable date. Cassiopeia presents the $108,975 exchange gain in its income statement in the following manner:

In a separate series of transactions, the subsidiary sends a weekly shipment of telescope repair parts to Cassiopeia, totaling €48,000 of profits for the entire year. For these transactions, the exchange rate varies from $1: €0.6 to $1: €0.75. A reasonable estimate of the average exchange rate for all the transactions is $1: €1.67. Consequently, the €48,000 profit is eliminated at the $1: €1.67(= $71,642) average exchange rate.

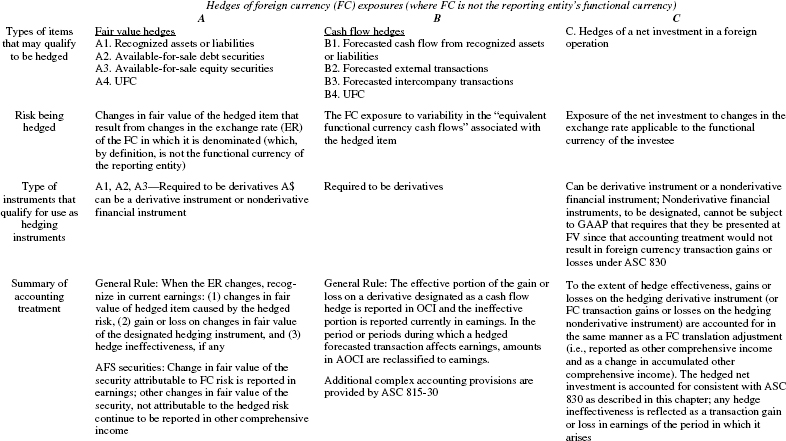

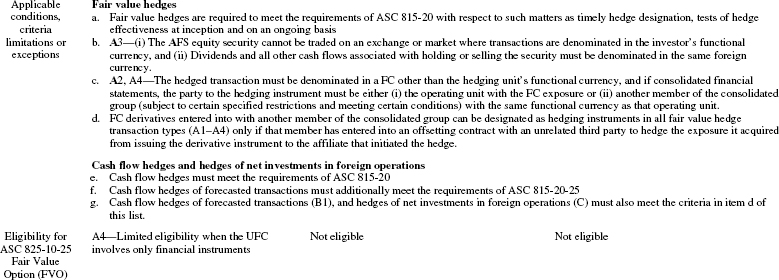

Foreign Currency Hedging

ASC 815, provides complex hedging rules that permit the reporting entity to elect to obtain special accounting treatment relative to foreign currency risks with respect to the following items:

- Recognized assets or liabilities

- Available-for-sale debt and equity securities

- Unrecognized firm commitments

- Foreign-currency-denominated forecasted cash flows

- Net investment in a foreign operation.

The chapter on ASC 815 provides a detailed discussion of derivatives and hedging. The table on the next page provides a high-level summary of the complex provisions that apply to hedges related to foreign currency exposures.

Measuring hedge effectiveness.

While any entity may use hedging strategies, under the provisions of ASC 815 the transaction must meet a number of important conditions to qualify for hedge accounting. Among these conditions are the establishment, at inception, of criteria for measuring hedge effectiveness and ineffectiveness. Periodically, each hedge must be evaluated for effectiveness, using the preestablished criteria, and the gains or losses associated with hedge ineffectiveness must be reported currently in earnings and not deferred to future periods. In the instance of foreign currency hedges, ASC 815 states that reporting entities must exclude from their assessments of hedge effectiveness the portions of the fair value of forward contracts attributable to spot-forward differences (i.e., differences between the spot exchange rate and the forward exchange rate).

In practice, this means that reporting entities engaging in foreign currency hedging will recognize changes in the above-described portion of the derivative's fair value in earnings, in the same manner that changes representing hedge ineffectiveness are reported, but these are not considered to represent ineffectiveness. These entities must estimate the cash flows on forecasted transactions based on the current spot exchange rate, appropriately discounted for time value. Effectiveness is then assessed by comparing the changes in fair values of the forward contracts attributable to changes in the dollar spot price of the pertinent foreign currency to the changes in the present values of the forecasted cash flows based on the current spot exchange rate(s).

Hedging Foreign Currency Exposures

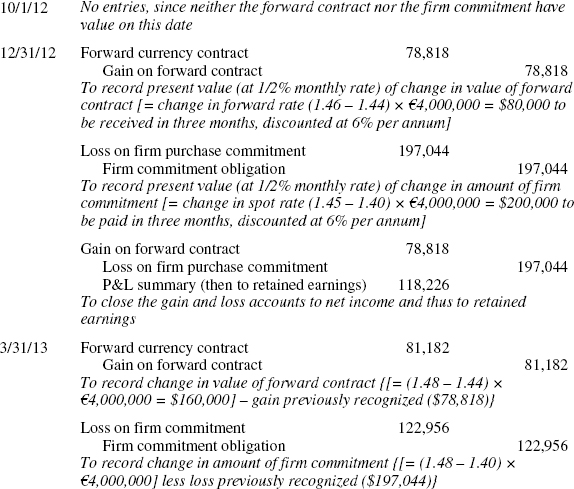

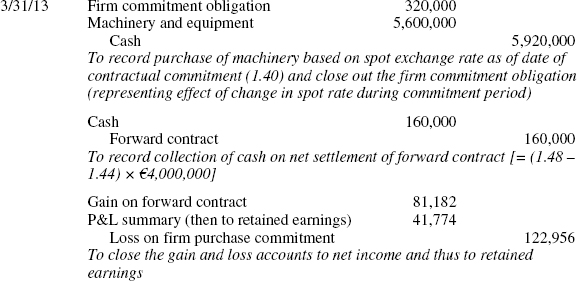

On October 1, 2012, Braveheart Co. (a US entity) orders from its European supplier, Gemut-lichkeit GmbH, a machine that is to be delivered and paid for on March 31, 2013. The price, denominated in euros, is €4,000,000. Although Braveheart will not make the payment until the planned delivery date, it has immediately entered into a firm commitment to make this purchase and to pay €4,000,000 upon delivery. This creates a euro liability exposure to foreign exchange risk; thus, if the euro appreciates over the intervening six months, the dollar cost of the equipment will increase.

To reduce or eliminate this uncertainty, Braveheart desires to lock in the purchase cost in euros by entering into a six-month forward contract to purchase euros on the date when the purchase order is issued to and accepted by Gemutlichkeit. The spot rate on October 1, 2012, is $1.40 per euro and the forward rate for March 31, 2013 settlement is $1.44 per euro. Braveheart enters into a forward contract on October 1, 2012, with the First Intergalactic Bank to pay US $5,760,000 in exchange for the receipt of €4,000,000 on March 31, 2013, which can then be used to pay Gemutlichkeit. No premium is received nor paid at the inception of this forward contract.

The transaction is a firm commitment consistent with the requirements of ASC 815, and fair value hedge accounting is used in accounting for the forward contract.

Assume the relevant time value of money is measured at 1/2% per month (a nominal 6% annual rate). The spot rate for euros at December 31, 2012, is $1.45, and at March 31, 2013, it is $1.48. The forward rate as of December 31 for March 31 settlement is $1.46.

Entries to reflect the foregoing scenario are as follows:

Observe that in the foregoing example the gain on the forward contract did not precisely offset the loss incurred from the firm commitment. Since a hedge of an unrecognized foreign currency denominated firm commitment is accounted for as a fair value hedge, with gains and losses on hedging positions and on the hedged item both being recorded in current earnings, it may appear that the matter of hedge effectiveness is of academic interest only. However, according to ASC 815, even if both components (that is, the net gain or loss representing hedge ineffectiveness, and the amount charged to earnings that was excluded from the measurement of ineffectiveness) are reported in current period earnings, the distinction between them is still of importance.

With respect to fair value hedges of firm purchase commitments denominated in a foreign currency, ASC 815 directs that “the change in value of the contract related to the changes in the differences between the spot price and the forward or futures price would be excluded from the assessment of hedge effectiveness.” As applied to the foregoing example, therefore, the net credit to income in 2012 ($118,226) can be further analyzed into two constituent elements: the amount arising from the change in the difference between the spot price and the forward price, and the amount resulting from hedge ineffectiveness.

The former item, not attributed to ineffectiveness, arose because the spread between spot and forward price at hedge inception, (1.44 − 1.40 =) .04, fell to (1.46 − 1.45 =) .01 by December 31, for an impact amounting to (.04 − .01 =) .03 × €4,000,000 = $120,000, which, reduced to present value terms, equaled $118,227. The net credit to earnings in December 2012, ($78,818 + 118,226 =) $197,044, relates to the spread between the spot and forward rates on December 31 and is identifiable with hedge ineffectiveness.

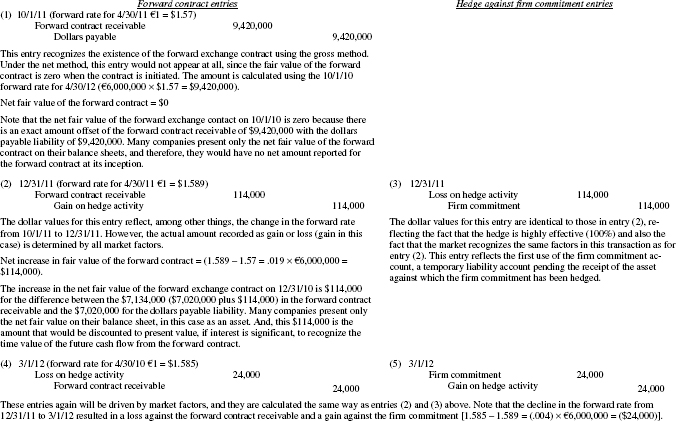

Forward Exchange Contracts

Foreign currency transaction gains and losses on assets and liabilities that are denominated in a currency other than the functional currency can be hedged if a US entity enters into a forward exchange contract. The following example shows how a forward exchange contract can be used as a hedge, first against a firm commitment and then, following delivery date, as a hedge against a recognized liability.

A general rule for estimating the fair value of forward exchange rates under ASC 815 is to use the changes in the forward exchange rates, and discount those estimated future cash flows to a present-value basis. An entity will need to consider the time value of money if significant in the circumstances for these contracts. The following example does not apply discounting of the future cash flows from the forward contracts in order to focus on the relationships between the forward contract and the foreign currency denominated payable.

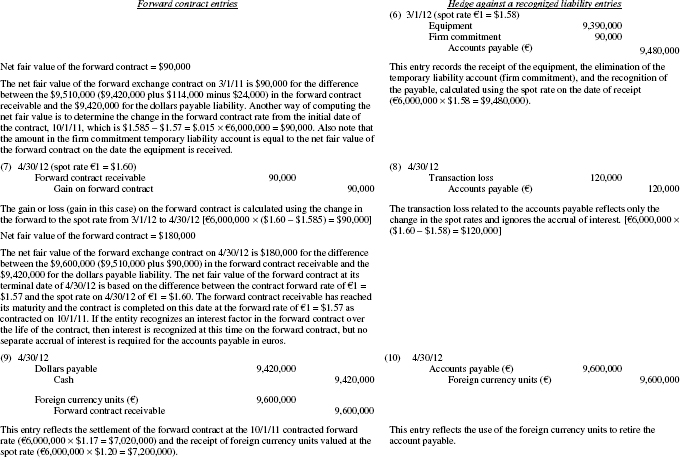

Durango, Inc. enters into a firm commitment with Dempsey Ing., Inc. of Germany, on October 1, 2012, to purchase a computerized robotic system for €6,000,000. The system will be delivered on March 1, 2013, with payment due sixty days after delivery (April 30, 2013). Durango, Inc. decides to hedge this foreign currency firm commitment and enters into a forward exchange contract on the firm commitment date to receive €6,000,000 on the payment date. The applicable exchange rates are shown in the table below.

The example on the following pages separately presents both the forward contract receivable and the dollars payable liability in order to show all aspects of the forward contract. For financial reporting purposes, most companies present just the net fair value of the forward contract that would be the difference between the current value of the forward contract receivable and the dollars payable liability. Note that the foreign currency hedges in the illustration are not perfectly effective. However, for this example, the degree of ineffectiveness is not deemed to be sufficient to trigger income statement recognition per ASC 815.

The transactions that reflect the forward exchange contract, the firm commitment and the acquisition of the asset, and retirement of the related liability appear at the end of this section. The net fair value of the forward contract is shown below each set of entries for the forward exchange contract.

In the case of using a forward exchange contract to speculate in a specific foreign currency, the general rule to estimate the fair value of the forward contract is to use the forward exchange rate for the remainder of the term of the forward contract.

The Fair Value Option

ASC 825-10-25, encourages reporting entities to voluntarily elect to use fair value to measure eligible financial assets and financial liabilities in their financial statements. This election is referred to as the Fair Value Option (FVO). Changes in the fair values of these assets and liabilities would be reflected in earnings as they occur.

In issuing ASC 825-10-25, FASB indicated that, among the reasons it decided to permit this election was that the election would “enable entities to achieve consistent accounting and, potentially, an offsetting effect for the changes in the fair values of related assets and liabilities without having to apply complex hedge accounting provisions, thereby providing greater simplicity in the application of accounting guidance.”1

As noted in the table “Hedging Foreign Currency Exposures” presented earlier in this chapter, the provisions of ASC 825-10-25 have limited applicability with respect to foreign currency risks. The election does not affect cash flow hedges or hedges of a net investment in a foreign operation. With respect to fair value hedges, the reporting entity may elect the FVO for eligible nonderivative financial assets or liabilities. An unrecognized firm commitment (UFC) may qualify as a financial instrument if it only involves financial assets and liabilities. ASC 825-10-25 provides, as an example, a forward purchase contract for a loan that is not readily convertible to cash. This instrument would qualify for the FVO. In order to achieve the desired economic offsetting that would resemble hedge accounting, the reporting entity would also have to hold assets denominated in the same foreign currency (which is not the entity's functional currency) that give rise to foreign currency transaction gains or losses that would partially or fully offset changes in the fair value of the forward purchase contract during its term and at settlement.

Elections made under the FVO are irrevocable and, if made by early adopting ASC 825-10-25, also require the reporting entity to early adopt the disclosure provisions of ASC 820 that otherwise would not be effective until the same date as ASC 825-10-25.

ACCOUNTS TO BE REMEASURED USING HISTORICAL EXCHANGE RATES

- Marketable securities carried at cost (equity securities and debt securities not intended to be held until maturity)

- Inventories carried at cost

- Prepaid expenses such as insurance, advertising, and rent

- Property, plant, and equipment

- Accumulated depreciation on property, plant, and equipment

- Patents, trademarks, licenses, and formulas

- Goodwill

- Other intangible assets

- Deferred charges and credits, except policy acquisition costs for life insurance companies

- Deferred income

- Common stock

- Preferred stock carried at issuance price

- Revenues and expenses related to nonmonetary items

- Cost of goods sold

- Depreciation of property, plant, and equipment

- Amortization of intangible items such as goodwill, patents, licenses, and the like

- Amortization of deferred charges or credits, except policy acquisition costs for life insurance companies.

Source: ASC 830.

1 ASC 825-10-25, Financial Instruments—Fair Value Option. Norwalk, CT: Financial Accounting Standards Board, 2007.