Chapter 33

A Series Expansion for the Bivariate Normal Integral

Journal of Computational Finance, 1 (4) (1998), 5–10.

Abstract

An infinite series expansion is given for the bivariate normal cumulative distribution function. This expansion converges as a series of powers of ![]() , where ρ is the correlation coefficient, and thus represents a good alternative to the tetrachoric series when ρ is large in absolute value.

, where ρ is the correlation coefficient, and thus represents a good alternative to the tetrachoric series when ρ is large in absolute value.

Introduction

The cumulative normal distribution function

with

appears frequently in modern finance: Essentially all explicit equations of options pricing, starting with the Black-Scholes formula, involve this function in one form or another. Increasingly, however, there is also a need for the bivariate cumulative normal distribution function

where the bivariate normal density is given by

This need arises in at least the following areas:

- Pricing exotic options. Options with payout depending on the prices of two lognormally distributed assets, or two normally distributed factors, involve the bivariate normal distribution function in the pricing formula. Examples include the so-called rainbow options (such as calls on maximum or minimum of two assets), extendible options, and spread and cross-country swaps.

- Correlations of derivatives. While the instantaneous correlation of two derivatives is the same as the correlation of the underlying assets, calculation of the correlation over noninfinitesimal intervals often requires the bivariate normal function.

- Loan loss correlations. If a loan default occurs when the borrower's assets fall below a certain point, the covariance of defaults on two loans is given by a bivariate normal formula. This covariance is needed when evaluating the variance of loan portfolio losses.

A standard procedure for calculating the bivariate normal distribution function is the tetrachoric series,

where

are the Hermite polynomials. For a comprehensive review of the literature, see Gupta (1963).

The tetrachoric series (3) converges only slightly faster than a geometric series with quotient ρ, and it is therefore not very practical to use when ρ is large in absolute value. In this note, we give an alternative series that converges approximately as a geometric series with quotient ![]() .

.

The Expansion

The starting point of this chapter is the formula

which is proven in the Appendix.

Because of the identity

for ![]() , we can limit ourselves to calculation of

, we can limit ourselves to calculation of ![]() . Suppose first that

. Suppose first that ![]() . Then by integrating Equation (4) with

. Then by integrating Equation (4) with ![]() from ρ to 1 we get

from ρ to 1 we get

where

To evaluate the integral, substitute

to obtain

Using the expansion

we get

Because

for ![]() and

and ![]() , the series in Equation (7) converges uniformly in the interval

, the series in Equation (7) converges uniformly in the interval ![]() and can be integrated term by term. It can be easily established that

and can be integrated term by term. It can be easily established that

for ![]() . Substitution into (7) then gives

. Substitution into (7) then gives

where

Equations (5), (9), and (10) give an infinite series expansion for ![]() with

with ![]() . When

. When ![]() , integration of Equation (4) from –1 to ρ yields

, integration of Equation (4) from –1 to ρ yields

with Q still given by (9) and (10).

A convenient procedure for computing the terms in the expansion (9) is using the recursive relationships

with

To determine the speed of convergence of (9), integrate the first half of inequality (8) from 0 to ![]() . This results in the bound

. This results in the bound

for ![]() , and therefore the series (9) converges approximately as

, and therefore the series (9) converges approximately as ![]() . As the tetrachoric series for

. As the tetrachoric series for ![]() ,

,

converges approximately as ![]() , a reasonable method for calculating

, a reasonable method for calculating ![]() is to use the tetrachoric series (12) when

is to use the tetrachoric series (12) when ![]() and expressions (5) and (11) with the series (9) when

and expressions (5) and (11) with the series (9) when ![]() .

.

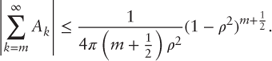

The error in the calculation of ![]() resulting from using m terms in the expansion (9) is bound in absolute value by

resulting from using m terms in the expansion (9) is bound in absolute value by

Numerical Results

A comparison of the convergence of the tetrachoric series (12) and the alternative calculations (5) or (11) with the series (9) in calculating ![]() for high values of the correlation coefficient is given in Tables 33.1 and 2.

for high values of the correlation coefficient is given in Tables 33.1 and 2.

Table 33.1 Partial Sums of the Tetrachoric and Alternative Series

| Number of Terms | Tetrachoric | Alternative | Tetrachoric | Alternative |

| 1 | .171033 | .158632 | .174894 | .158655 |

| 2 | .171033 | .158631 | .174894 | .158655 |

| 3 | .167298 | .158631 | .170304 | .158655 |

| 5 | .161764 | .158631 | .162651 | .158655 |

| 10 | .157961 | .158631 | .156068 | .158655 |

| 20 | .158466 | .158631 | .158068 | .158655 |

| 30 | .158660 | .158631 | .159374 | .158655 |

| 50 | .158632 | .158631 | . 158599 | .158655 |

| 100 | .158631 | .158631 | .158711 | .158655 |

| 200 | .158631 | .158631 | .158657 | .158655 |

| 300 | .158631 | .158631 | .158654 | .158655 |

| Exact | .158631 | .158655 | ||

Table 33.2 Number of Terms Necessary for Precision 10–4

| ρ = .8 | ρ = .9 | ρ = .95 | ρ = .99 | |

| Tetrachoric series | ||||

| 8 | 16 | 30 | 121 | |

| 7 | 14 | 22 | 75 | |

| 6 | 11 | 18 | 42 | |

| Alternative series | ||||

| 4 | 3 | 2 | 1 | |

| 3 | 1 | 1 | 1 | |

| 1 | 1 | 1 | 1 | |

Appendix

We prove equation (4) by stating a slightly more general result. Let

and

be the p-variate normal density function and cumulative distribution function, respectively, where ![]() is a

is a ![]() vector and

vector and ![]() is a

is a ![]() symmetric positive-definite matrix. We now prove the following lemma:

symmetric positive-definite matrix. We now prove the following lemma:

Lemma. Let ![]() . Then for

. Then for ![]()

Here ![]() is the

is the ![]() vector of

vector of ![]() is the

is the ![]() vector of the remaining components of x, and

vector of the remaining components of x, and ![]() are the

are the ![]() , and

, and ![]() decompositions of Σ into the i-th and j-th row and column and the remaining rows and columns.

decompositions of Σ into the i-th and j-th row and column and the remaining rows and columns.

Proof. We have

Define ![]() by

by ![]() and put

and put ![]() . Since for

. Since for ![]()

where Eij is the matrix having unity for the (i,j)-th element and zeros elsewhere, we get on substitution

On the other hand,

and

and therefore

Integrating with respect to ![]() and exchanging the order of integration and differentiation yields the first equality of the lemma. The second equality follows from the factorization

and exchanging the order of integration and differentiation yields the first equality of the lemma. The second equality follows from the factorization

References

- Gupta, S.S. (1963). “Probability Integrals of Multivariate Normal and Multivariate t.” Annals of Mathematical Statistics, 34, 792–828.

- Johnson, N.L., and S. Kotz. (1972). Distributions in Statistics: Continuous Multivariate Distributions. New York: John Wiley & Sons.

- Vasicek, O.A. (1997). “The Loan Loss Distribution.” Working paper, KMV Corporation.