Chapter 5 The Power of Compound Interest and the Erosive Effect of Inflation

So far in Money Mindset I have stressed the importance of having a plan to accomplish your financial goals. After you determine your goals and construct your plan, the wealth management process begins to unfold. There is a lot to learn and digest about the process, and in upcoming chapters I will break down for you the impact of taxes and asset allocation, how to evaluate your risk tolerance and build an investment portfolio, and finally, how to monitor your portfolio and rebalance it when needed.

But first, this chapter discusses the power of compound interest and the erosive effect of inflation. Remember, you need to have the right financial mindset in order to meet your goals and have your investments live up to their full potential.

The Power of Compound Interest

Albert Einstein, a Noble Prize Laureate in physics who studied the biggest mysteries of our universe, said, “Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.”

Let’s explore the power of compounding by learning the mathematical Rule of 72.

The Rule of 72 is a simplified way to estimate how long an investment will take to double, given a fixed annual rate of interest. By dividing 72 by the annual rate of return, you can get a rough estimate of how many years it will take for the initial investment to duplicate itself. For example, the rule of 72 states that if a $100,000 grew by an annual return of 10 percent per year, it would take approximately 7.2 years [(72/10) = 7.2] to turn into $200,000.

Rule of 72

Rate of Return

Approx. # of Years for Money to Double

2%

36 years

3%

24 years

5%

14.4 years

7%

10.3 years

9%

8 years

10%

7.2 years

12%

6 years

Now, let me share with you a story about when I first learned and understood the power of compound interest. I was in Dr. Fawley’s sixth-grade math class. One day in class, Dr. Fawley asked us if we liked money. Of course, we responded, and just like that he had our undivided attention. He then went on to say that he wanted to give each student a choice between two imaginary options. Would you rather receive (a) $1,000 per day for 30 days ($30,000 over the 30 days) or (b) a penny the first day, two pennies the next day, four pennies the following day, and so on, with the amount doubling every day for 30 days in all?

He gave us a few seconds to decide which of the two options we would choose. He then asked everyone who wanted the $30,000 of free imaginary money to raise their hand; most hands went up, including mine. Then he asked who wanted the penny compounded daily for 30 days. Few students raised their hands. My guess, now looking back, was that those students who chose option (b) must have known there was a trick involved.

Those few students who thought it was a trick question were right; compound interest is one of the best-known tools for growing wealth. By day 22, assuming the value to double daily, the compounded amount would have been $20,971.52. By day 30, it would be valued at $5,368,709.12.

Day 1: $.01

Day 6: $.32

Day 11: $10.24

Day 16: $327.68

Day 21: $10,485.76

Day 26: $335,544.32

Day 2: $.02

Day 7: $.64

Day 12: $20.48

Day 17: $655.36

Day 22: $20,971.52

Day 27: $671,088.64

Day 3: $.04

Day 8: $1.28

Day 13: $40.96

Day 18: $1,310.72

Day 23: $41,943.04

Day 28: $1,342,177.28

Day 4: $.08

Day 9: $2.56

Day 14: $81.92

Day 19: $2,621.44

Day 24: $83,886.08

Day 29: $2,684,354.56

Day 5: $.16

Day 10: $5.12

Day 15: $163.84

Day 20: $5,242.88

Day 25: $167,772.16

Day 30: $5,368,709.12

Compound interest is often called the eighth wonder of the world (as Einstein said) because it seems to possess magical powers. Compound interest can help us to achieve our financial goals, such as becoming a millionaire, retiring comfortably, or being financially independent. Yet, this is easier said than done….

Make Time Work for You

Many people don’t recognize the power of how their money can grow if invested over the long term. The challenge is making sure dollars are truly allocated appropriately and that some portions of your savings are kept liquid for life’s unanticipated emergencies. That’s why it’s important to be a disciplined and consistent saver with a plan for how your investments are allocated.

I always tell people that there’s never a “right” time to invest. When the markets are down, people don’t want to invest because they’re afraid of losing money. That’s human nature. They think, “Oh, I’ll just wait until we hit bottom and then I’ll start investing.” The problem with that thinking is no one knows when the bottom will occur or how to detect it. If the markets are up, people are nervous about investing because they’re afraid of buying high and experiencing a crash with their money. If you’re waiting for the ideal time to start investing, you will be waiting indefinitely because there will always be ups and downs, always reasons why you may not want to invest or why you want to spend those dollars on other things. There’s never a perfect time to invest, but the sooner you start investing and begin a habit of saving, the money you accumulate can grow substanitally over the years.

The Cost of Procrastination

Let’s say you have a goal to accumulate $1 million dollars by the time you turn 65. Assuming that you are 25 years old right now, how much do you think you would need to start saving per month to reach your goal? Mathematically speaking, you would need to begin saving approximately $353 per month, earning a 7.27 percent rate of return per year, for 40 years, in order to amass $1,000,000.

As a side note, over a 20-year time period, ending December 31, 2012, the S&P 500 index, “the U.S. stock market,” earned an 8.21 percent rate of return per year, while an investment in the Barclay’s Aggregate Bond Index, “the U.S. bond market,” earned 6.34 percent. A weighted portfolio of 50 percent stocks (S&P 500 Index), and 50 percent bonds (Barclay’s Aggregate Bond Index) resulted in a blended return of 7.27 percent per year over those 20 years.

As I mentioned, it’s never the perfect time to invest. People live their lives, have their families, send their kids to school and they think, “Oh, once the kids are out on their own, that’s really when we’ll start investing for our retirement.”

Well, the problem with waiting is that the longer you wait, the more you have to save per month because you have less time for your money to earn at a compounded rate.

What if you are 55 years old right now and are just beginning to save for retirement? How much do you think you would need to start saving per month to reach the goal of $1,000,000 by the time you turn 65? You would need to begin saving approximately $5,692 per month, earning a 7.27 percent rate of return per year, for 10 years in order to amass $1,000,000.

This amount, $5,692, is a lot of money to save each month, and is more than most households’ total monthly income.

Time begins to work against you the longer you delay saving for retirement. The chart below demonstrates the differences.

Monthly Investment

Age 25 $353

Age 35 $777

Age 45 1,857

Age 55 $5,692

The chart is based on the premise of a 7.27 percent rate of return, solving for a future value of $1,000,000 and present value of $0, for the number of years remaining before the age of 65.

The Story of Larry and Earl

Let me tell you the story of Larry and Earl, two college roommates of the same age. While in college, they both enjoyed dreaming about their future. To help make their dreams become a reality, they determined they each would need to start saving a portion of their income upon graduation. Larry and Earl made a commitment to each other to save at least $4,000 per year until age 65.

After graduation, they both went their separate ways, building their careers, and eventually they lost touch with each other. Time quickly passed and before they knew it, it was time for their 20th college reunion. They were excited to see each other after so many years, and were eager to catch up. Larry shared with Earl the ups and downs of his life and why he was not able to live up to their shared commitment to save $4,000 each year like he had hoped. Larry confessed that for the first 10 years after college he had focused on everything except saving. However, he was proud to announce to Earl that he began saving $4,000 a year for the past 10 years.

After hearing Larry’s story, Earl then shared how he diligently saved, prioritizing it above spending his money frivolously. He explained how he did this. He told him that saving money quickly became a positive habit and he didn’t miss the money that he had been saving. The process of saving and seeing that balance grow in his account became a rewarding experience. Both Larry and Earl were now savers. But, “Late Larry” missed out on years of compounding, while “Early Earl” had the benefit of his money compounding for a much longer period of time.

Fast-forward another 20 years, while both Larry and Earl stayed true to their renewed commitment to save at least $4,000 per year. Forty years after their original promise to each other, their investments had grown to impressive amounts. Larry had invested $120,000 over a 30-year time period that earned him a 7.27 percent rate of return. His nest egg had grown to $431,599.35. Earl, on the other hand, invested $160,000 over a 40-year time period that earned him a 7.27 percent rate of return.

How much more money does “Early Earl” have than “Late Larry”?

“Early Earl” saved $40,000 more than “Late Larry,” but did that make much of a difference? Absolutely it did. Earl’s $160,000 grew to $949,879. By investing a decade earlier, Earl’s savings were twice as large as Larry’s.

$4,000 per Year, 7.27% Return

Age

Larry

Earl

25–34

$0

$4,000

35–64

$4,000

$4,000

Amount Invested

$120,000

$160,000

Value at 65

$431,599.35

$949,879.31

This story should help send the message that it is essential to start planning for your future and saving as early as possible. You can’t just sit back and think, “Oh, I’ve got plenty of time, I’ll think about that later, I’ve got a lot of years ahead of me.” However, those years go by fast. For Millennials and Gen X-ers, your most valuable financial asset is time. You may not have a lot in net worth or income, but you have the time to invest and save. You’re going to be much better off 20 or 30 years from now than you would be if you focus on the YOLO (you only live once) mindset.

Henry David Thoreau said, “Wealth is the ability to fully experience life.”

The Erosive Effects of Inflation

My father explained to me at a young age that inflation occurs when we have too many dollars chasing too few goods. As the purchasing price of the dollar declines, it takes more to buy less. For example, during World War I, Germany created an enormous amount of debt by issuing bonds and was freely rolling out more German marks via the printing press. Germany was planning to have its surrendered enemies pay the debt after their victory. As we all know, the opposite happened. After Germany surrendered, they were forced to sign the Treaty of Versailles. The Treaty meant that Germany had to pay reparations to the allies and large swaths of its territory were divided, which created hyperinflation in Germany. In October 1923, German prices rose at a rate of 41 percent per day. By November 1923, one dollar equaled one trillion marks. This resulted in people using wheelbarrows full of marks to buy a single loaf of bread.1 This all happened because the German government spent more money than they were bringing in, and eventually, devalued its currency so much that it became nearly worthless.

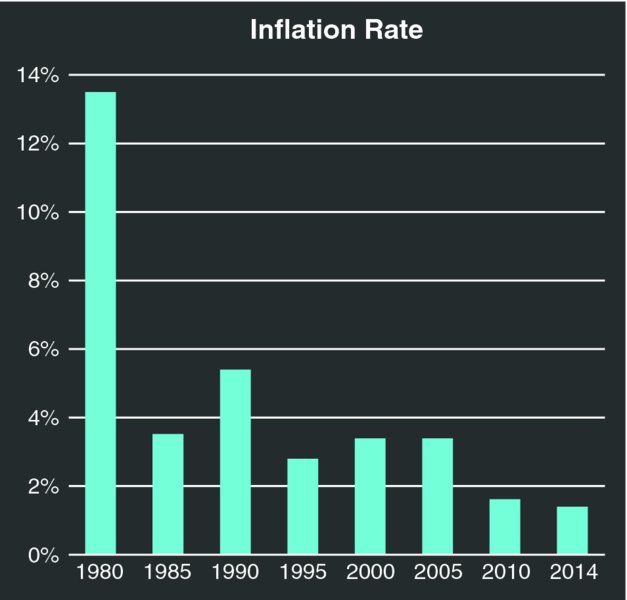

Looking at Inflation Today

It is important to remember that while you are working, your income usually goes up with the cost of living, and you won’t exponentially feel the pain of inflation. That will change when you are retired and living on a fixed income; inflation will erode the purchasing power of your money. It is helpful to adjust your income every year to keep up with inflation, which means that you have to be taking out more and more every year. Inflation has been very volatile over the past 30 years. Yet, people should anticipate at least 2 to 3 percent inflation every year, and some years it could be a lot more than that.

If you were to use a 3 percent inflation rate, how much do you think inflation would negatively affect your purchasing power over 20 years?

If you need $100,000 a year today to cover all your fixed and variable expenses, in 20 years you will need $180,000 to maintain the same standard of living. The other way to look at it is that $100,000 a year, 20 years from now, will be worth only $55,367 in today’s dollars.

You need to save enough to draw an income to cover your current expenses, but you’ve got to put enough away to cover those current expenses and then have those expenses adjusted for inflation. Otherwise, when you are retired, you’re going to see that your dollar will not go as far every year.

With life expectancy getting longer, some people could be retired for more years than they actually worked.

Do you remember what the cost of a movie ticket was when you were a kid? Look how little a postage stamp cost back in 1980 and what it is today. It is worth repeating: Inflation is real, prices will increase, and this is a compelling reason to begin investing early so that compounding interest can work for us. The goal is to create enough net worth so that inflation doesn’t negatively affect us in retirement.

What’s Ahead?

Next we will focus on the execution of your plan, using knowledge of today’s investment world to grow, build, protect, and transfer your wealth.