CHAPTER 2

Wealth Is More Than Money

In the introduction to his transformational guidebook Family Wealth: Keeping It in the Family, James Hughes mentions that a family's wealth “consists primarily of its human capital (defined as all the individuals who make up the family) and its intellectual capital (defined as everything each individual family member knows), and secondarily of its financial capital.”1 Later in the book, he mentions a fourth type of capital: social capital, which I define as the networks of people of means who use their wealth and influence for the benefit of society.

If, in fact, human, intellectual, and social capital make up 75 percent of a family's actual wealth, giving 90 percent of the family's and advisors' attention to only 25 percent of the assets doesn't make a lot of sense. Yet this is the way traditional wealth managers and those they advise tend to view their roles.

Hughes makes exactly this point. In his view, a family that loses its wealth usually does so because of too great a concentration on financial capital and too little attention paid to the other types of capital the family possesses. Hughes goes on to say that “a family's financial capital is a tool to support the growth of the family's human and intellectual capital.”2 In other words, money is simply a means to a more important and meaningful end. Money, rightly considered, can empower an entire family, but if there is too much emphasis on balance sheets and not enough on family relationships, talents, roles, and strategic planning, the family can be enfeebled as its wealth trickles away.

Families who focus strictly on their financial assets usually do not sustain wealth over time and enjoy the fruits of their labor. They frequently have deep‐rooted resentments about the uses of money, as well as relationship challenges, values clashes, and arguments about the place of money in their personal value systems. As a result, the wealth may disappear by the third generation, even if it is well‐managed and invested.

The Rockefellers: An Emphasis on Wealth‐Building and Philanthropy

If the Vanderbilt clan is the exemplar of wealth planning run amok, then the Rockefeller family is the other side of the coin. Although the Rockefellers no longer stand at the top of the heap of America's richest families, they still control more than $11 billion, settling in at #22 on the 2015 Forbes list of America's wealthiest families.

John D. Rockefeller, although probably no more ruthless than the other titans of his era—Vanderbilt, Carnegie, and Morgan, for example—could be savagely competitive, but buried within him was also a strand of philanthropy that grew as his assets expanded. An article in Philanthropy Roundtable highlights Rockefeller's charitable bent.

The article mentions that a few days after the sixteen‐year‐old Rockefeller landed his first job, he bought a ledger in which he accounted for virtually every cent of income and outgo. What is noticeable is that even when he was working for pennies each day, he already was sharing his resources. “‘When I was only making a dollar a day,’ Rockefeller later recalled, ‘I was giving [away] five, ten, or twenty‐five cents.’”3

As Rockefeller's wealth increased, so did his charitable donations. By 1865, he was giving away more than $1,000 annually. Not surprisingly, Rockefeller was inundated with requests for money. “At breakfast, he made it a habit to say grace and then open review of requests for charity . . . asking his children to further investigate promising appeals,”4 thus setting the stage for their understanding of the need both for making money and making an impact; this understanding has continued into the succeeding generations.

Because of his immense fortune, Rockefeller's philanthropy, much of which was orchestrated and shepherded by his son, John D. Rockefeller Jr., was virtually boundless, from his founding of the University of Chicago to the Rockefeller Institute for Medical Research (now Rockefeller University) to the General Education Board to funding for Morehouse College and Spelman College (which was named for his wife, Laura Spelman Rockefeller). The contributions of the various organizations he funded are staggering to contemplate: a vaccine for yellow fever; prevention and cure of hookworm diseases; and support of sixty‐four Nobel Prize winners in the fields of chemistry and medicine, to mention only a few. By the time of his death at age 97, Rockefeller had given away approximately $540 million and had changed countless lives forever.

In his adulthood, John D. Rockefeller Jr. also gave more than $500 million to conservation causes, historic preservation, art, and religious—primarily Baptist—institutions. He was the driving force behind New York's Rockefeller Center. Through the establishment of the Rockefeller Brothers Fund (which also included their sister by 1954), the family contin ued the legacy of philanthropy, making grants to “organizations working to expand knowledge, clarify values and critical choices, nurture creative expression, and shape public policy.”5 Some of the trustees of the fund today are fourth and fifth generations of the Rockefeller family.

Not surprisingly, with the family's emphasis on public service, some of the third generation of Rockefellers found their way onto a larger stage—the political arena. Nelson Rockefeller served four terms as governor of New York and three years as vice president of the United States under Gerald Ford. His brother Winthrop was governor of Arkansas from 1967 to 1971.

In the minds of many, David Rockefeller was the embodiment of the Chase Manhattan Bank and later the Chase Manhattan Corporation. Beginning his affiliation with Chase Manhattan in 1946, he became chairman of the board of directors of Chase Manhattan Bank, NA, in March 1969 and CEO of Chase Manhattan Corporation in May of that year. He wielded immense influence in both corporate and international affairs.

Laurance Rockefeller carried on his father's work in conservation and was also an early venture capitalist. According to the Washington Post, “[he] also was a chief advocate for investing family money in new, often bold enterprises. Particularly fascinated by aviation, he poured money into new projects so they would not be snuffed out by a merger because of a lack of financing.”6 He was awarded the Presidential Medal of Freedom, the nation's highest civilian honor, for his unparalleled work in conservation.

John D. Rockefeller III, the eldest of the third generation, was active in the establishment of Lincoln Center in New York. He chaired the Rockefeller Foundation but used his own money to found the Population Council, an organization that dealt with world overpopulation issues; he later was appointed by President Richard Nixon to the Commission on Population Growth and the American Future. He was also an extensive collector of Asian art, which he bequeathed to the Asia Society, an organization he founded.

The only female among the third generation, Abigail (Babs) Rockefeller was a benefactor of note. The organizations that benefited from her philanthropy included Memorial Sloan‐Kettering Cancer Center, the Metropolitan Museum of Art, the Museum of Modern Art (which was founded by her mother), the Population Council, the American Red Cross, and many more.

The fourth generation was represented in part by John D. “Jay” Rockefeller IV, son of John D. III. He was first elected governor of West Virginia in 1977, and in 1985 moved on to the U.S. Senate, where he served for thirty years.

In the nineteenth century, John D. Rockefeller amassed a fortune and became arguably the richest man in history. He saw around corners, seizing opportunities and acting aggressively in his own behalf, all the while giving away vast sums for the betterment of humankind. During that period, he was also the target of harsh criticism for some of his methods and actions, including monopolistic practices that were outlawed by the Sherman Antitrust Act. However, as the current head of the family, the centenarian David Rockefeller said, “Grandfather never breathed a sigh of remorse to my father, his grandchildren or anyone else. He believed Standard Oil benefited society.”7

Thus, the Rockefeller slant on wealth certainly does not eschew continuing to acquire assets and to manage them for growth through Rockefeller & Co., which “serve[s] members of the Rockefeller family as they pursue their investment goals and further their heritage of public service and philanthropic endeavors.”8 However, the accumulation of wealth still is coupled with the family's agenda of “promoting the well‐being of humanity around the world”9 by making substantial grants to organizations that help the family realize their desire to do good. Today, a fifth generation of leaders is being groomed to take leadership of the family enterprise.

To cite only one example, in 2013, thirty‐seven‐year‐old Justin Rockefeller, one of Jay Rockefeller's sons and a trustee of the Rockefeller Brothers Fund, co‐founded (along with other social entrepreneurs and venture capitalists) The ImPact, a nonprofit NGO whose mission is “to inspire families to make more impact investments more effectively.”10

The website of The ImPact lists several beliefs that John D. Rockefeller probably would have embraced. One can almost envision him nodding his head in agreement. Some of these beliefs include:

- Big problems require bold action.

- We need to use all the tools in our belt to solve big problems.

- Profit and social impact are not mutually exclusive.

- Families can play a leading role.11

Clearly, certain deeply held capitalistic principles and socially beneficial behaviors have been generationally transmitted. The family has attended not only to its financial capital but also to its intellectual, human, and social capital. The Rockefellers espouse a family philosophy of living well and doing good.

The Rockefellers can continue their outsize influence on the world by showing other wealthy families how to live well while also bringing about positive change. As Robert Frank said in a blog for the Wall Street Journal, “They are [. . .] an example of how rich families can stay together over multiple generations—largely through their family rituals and constant communication. . . . The Rockefellers may no longer be a force in business. But when it comes to unity and purpose, the name means as much as ever.”12

Yes, the family has had its share of scandals and missteps, but in general, it has kept its eye on the ball. Family members know what matters to them as individuals and as a family, and they are a multigenerational success story.

The Rockefellers have chosen philanthropy as the way to act on their interests and passions. Other wealthy families may opt for avenues such as investing in new businesses, traveling the world, funding cutting‐edge research in a disease that perhaps has affected a family member, or investing in groundbreaking technologies. The fact is that wealth is about the power of money or capital to bring about the results that matter to the wealth owner. Wealth is also about putting money in motion as a tool to create change.

All about Oprah

Take, for example, the only self‐made African American woman billionaire in the United States: Oprah Winfrey. Although the talk show that made her a household name is no more, she continues to use her fortune to raise awareness about race in America and has produced a variety of African American–themed television programs and movies. She emphasizes the importance of education, especially of girls throughout the world, and she funds the Leadership Academy for Girls in South Africa. She is a tireless advocate for women and children's rights and has testified during congressional hearings on these topics. Her three foundations donate to such projects as the Charlize Theron Africa Outreach Project, Free the Children, Peace over Violence, Women for Women International, Women in the World Foundation, 46664 (Nelson Mandela's program that raises awareness of HIV/AIDS), and many others.

She also is involved in raising awareness of spirituality issues, regularly bringing thoughtful national and international spiritual leaders, writers, and artists—believers, atheists, and agnostics—to share points of view on the multiple award‐winning Super Soul Sunday television program. Guests have ranged from the late Elie Wiesel and Wayne Dyer to Marianne Williamson and Thich Nhat Hanh, and millions of people have watched and listened to these programs.

Her wealth increases as her media empire expands, with ventures such as OWN (Oprah Winfrey Network) and O magazine—and through her own hard work. It is clear that her passion is for one thing: the empowerment of all people to help them live better lives, whether through education, spirituality, or some combination. She speaks little about money, but a great deal about the ability of people to raise themselves up, as she did, from whatever life circumstances claimed them at the beginning of their lives. That's where she puts her money, and that's where her heart seems to be. The Academy of Achievement, into which she was inducted in 1989, features her quote: “It doesn't matter who you are, where you come from. The ability to triumph begins with you. Always.”

Finding a Singular Purpose

Maverick. Yachtsman. Founder of CNN and inventor of the 24‐hour news cycle. Business mogul. Sports team owner. Time magazine's 1994 Man of the Year. Largest private landowner in the United States. They're all Ted Turner. With an independent streak and a fierce work ethic, Turner is a largely self‐made success. Today, Forbes lists his fortune at approximately $2.2 billion, and Turner is using much of his wealth to foster the environmental causes in which he believes.

“I love this planet . . . I want to see the environment preserved and I want to see the human race preserved,” he has said. “And I'd like to see everybody living decently in a more equitable, kind‐hearted, thoughtful, generous world.”13 He has backed his philosophy with his treasure. By the mid‐1990s, he owned approximately 1.7 million acres in Montana and began a project to reintroduce the Northern American bison to its native habitat by returning untold acres to their original natural state.

“It depends on what your area of interest is,” he said in an interview for the March/April 2000 issue of Philanthropy Roundtable. “If you want to give to a university, they can use it in 20 years just as well. But if you care about the environment or population [his particular areas of concern], there are critical needs now.”

That is not to say that Turner has not given to educational institutions. He has, and generously, but he concentrates now on challenges to the sustainability of the planet. He has found a mission and a passion and is using his wealth to support it.

Bill and Melinda Gates and Warren Buffett, among the richest of all the people in the world, originated the Giving Pledge, which is “an effort to help address society's most pressing problems by inviting the world's wealthiest individuals and families to commit to giving more than half of their wealth to philanthropy or charitable causes, either during their lifetime or in their will.”14 It is a moral commitment rather than a legal contract, and each individual or family who signs the pledge may designate where the money goes. Ted Turner is a signer, as are many household names who possess great wealth: David Rockefeller, Elon Musk, Richard Branson, Sara Blakely, Mark Zuckerberg and Priscilla Chan, Barry Diller and Diane von Furstenberg—and more than 160 other individuals and families who may live a bit farther from the spotlight. The pledge, begun in the United States, now has signatories from other countries as well.

The Giving Pledge and The ImPact are sterling examples of Hughes's fourth component of wealth: social capital. Social capital is “the network of social connections that exists between people, and their shared values and norms of behavior, which enable and encourage mutually advantageous social cooperation.”15 Putting together people of like means increases their knowledge and understanding of the scope of the world's needs and encourages cooperation in solving thorny social problems through the application of wealth.

Certainly, all the people represented in The Giving Pledge continue to live richly, with perhaps only Buffett consciously choosing a more modest lifestyle. They continue to invest and increase their holdings. However, the majority of them also give away very large sums because they have found that wealth is not simply an accumulation of assets. They use those assets to make a difference in what matters to them.

The Advantages of Great Wealth . .

The effects of extensive holdings on individuals and families have been exhaustively studied, with results of various research projects sometimes seeming to contradict one another. In some ways, wealth appears to be an unalloyed good. It allows people to concentrate on their passions by offloading specialized tasks to family office personnel, household staff, and personal assistants. Wealth also makes it possible to seek the best society has to offer, often bypassing the traditional bureaucracy and processes that most other people have to endure.

The rich also have the means to pursue high‐level experiential spending, and according to research published in the journal Psychological Science, experiential purchases, such as a family trip or an arts or educational endeavor, offer greater happiness than material purchases, such as houses, cars, planes, and expensive technology. “The anticipatory period [for experiential purchases] tends to be more pleasant . . . less tinged with impatience relative to future material purchases we're planning on making,” said Amir Kumar, one of the study's authors.16

Cornell University psychology professor Thomas Gilovich added, “People often make a rational calculation. [With limited money]. . . I can either go there, or I can have this. If I go there, it'll be great, but it'll be done in no time. If I buy this thing, at least I'll always have it. That is factually true, but not psychologically true.”17 This situation is called hedonic adaptation, and as soon as the novelty wears off a purchase, we are likely to be searching for the next one, which eventually we also will adapt to—and the cycle continues. Material goods, while often fun and pleasant to own, are not the road to happiness.

Ryan Howell, assistant professor of psychology at San Francisco State University, concurred with Gilovich. “What we find is that there's this huge misforecast,” he says. “People think that experiences are only going to provide temporary happiness, but they actually provide both more happiness and more lasting value.”18

Great wealth also makes great giving possible, and great giving produces happiness on both sides of the equation. Giving money away to people, institutions, and causes in which the donor believes has proven to be enjoyable, especially if the donor has a choice among options. Of course, it's also of great value to those who receive the gifts.

Elizabeth Dunn, who has conducted a variety of studies on the effects of giving money away, discovered that “while . . . research has shown that people with more money are somewhat happier than people with less money, our research demonstrates that how people spend their money also matters for their happiness. . . . Both correlational and experimental studies show that people who spend money on others report greater happiness.”19

. . . and the Drawbacks

Although great wealth can bring considerable happiness, it also can cause anxiety. In a major study titled “The Joys and Dilemmas of Wealth,” conducted by the Boston College Center on Wealth and Philanthropy, the authors uncovered veins of discontent that often attend wealth.20

The 165 respondents to the survey had an average net worth of $78 million, with 120 exceeding $25 million. Among other concerns, the mega‐rich who answered the survey mentioned that their biggest worry was their children's futures. If the children came into a large inheritance, they might become aimless, rudderless, and never find a satisfying career or other life purpose. However, if the parents left a huge legacy to charity instead, the children might be resentful and angry. With regard to inheritance, Warren Buffett has famously said, “A very rich person should leave his kids enough to do anything, but not enough to do nothing.”

Additionally, if the children became wealthy in their own right, would they find mates who truly loved them or would they fall prey to fortune hunters? One respondent said poignantly, “I'm not super‐rich. However, I do worry about affection; whether my wife married me . . . for my money.”

Some of the respondents noted that their friends believed the rich to be insulated from all concerns, not just financial problems. They mentioned that their friends sometimes discounted their griefs and worries because of the depth of their financial resources. As one wealthy interviewee put it, “When you are known to have money, people . . . act like you can buy your way out of any problem. They think you are impervious to . . . tragedy, sorrow or depression.”

The wealthy are aware that some relationships are dependent on riches—that if people couldn't benefit financially from the friendship, they eventually would prove themselves to be false friends.

A surprising finding from the Boston College study was that the majority of respondents did not consider themselves to be financially secure and would require at least a quarter more than they currently had to achieve a feeling of security.

It's clear, then, that while wealth brings advantages, it's not all there is to living a rich life. If, as Hughes posits, money is an instrument families use to enhance their human and intellectual capital, and if wealth is aligned with a family's values, it may do much to cement relationships for generations. Concentration on money alone, however, can wreak havoc on family harmony. As one family member put it, “You really don't know your brothers and sisters until you share an inheritance with them. In our situation, it was pretty awful, even though I know my parents thought they had planned appropriately for all of us.”

Helping individual family members and the family collective lead rich lives requires that financial capital serve as a catalyst to productivity and happiness. Under this definition of a rich life, if family members are happy and productive, and their wealth is aligned with their feelings of personal self‐worth and an ongoing sense of fulfillment, they are likely to stay together and contribute to the sustainability and growth of the financial assets.

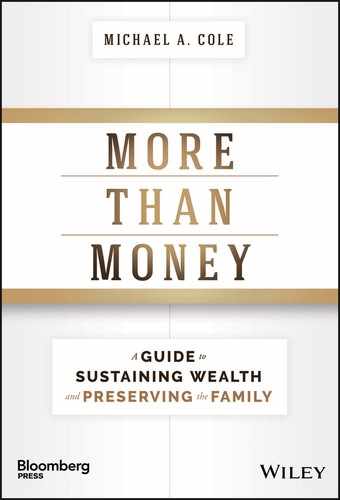

The Rich Life: A Case Study

A rich life can be visualized as a triangle, with each point representing an aspect of financial and personal success. When the triangle is too heavily weighted to one side, life is out of balance and can be unsatisfying, no matter the amount of money involved.

For example, Mark Allison* graduated from a prestigious Eastern business school and began a career in entrepreneurship. After building his business for fifteen years, he was successful, drawing a salary of about $300,000 per year. He employed 150 people, and his business continued to grow exponentially. Mark was excited to go to work every morning because he not only felt good about his personal success, but he also believed his accomplishments were useful and worthwhile, and he was proud of the business he continued to lead. He was happy to provide employment to talented people and to pay them well. He served on a few community boards he believed in, and he had a pleasant home life with his wife and three small children. His feelings of self‐worth were high.

He also noted a sense of fulfillment because he was attaining goals he had set for himself and was driving toward even greater success. He worked fifty hours per week but he loved it because he was passionate about his vision for the future. He felt on track and that he was doing what he was called to do.

At this time, if Mark had been asked to graph the three factors of wealth, personal fulfillment, and self‐worth, the resulting chart would likely have looked like this:

| Financial Assets | Sense of Self‐Worth | Feelings of Fulfillment | |

| 5 (high) | |||

| 4 | |||

| 3 | |||

| 2 | |||

| 1 (low) |

His graph shows all three factors in relative balance. Mark was reasonably financially successful, and his life also felt meaningful and rewarding.

After a few more years of business growth, Mark received an offer to buy his company for $250 million. He saw this offer as an opportunity to secure the future for himself and his family and to realize the rewards of his business accomplishments and success. If he continued to handle his money well, increasing his fortune through good management, he also could leave a legacy of wealth for future generations.

Yet within six months Mark was in the midst of a gut‐wrenching identity crisis. He had all the money he could ever need, but his business, which had been his chief reason to get up in the morning, was gone. His creativity shriveled and he was miserable. His wealth, sense of self‐worth, and his purpose were no longer in alignment. He was not motivated. He felt guilty and anxious about the immense responsibility of managing his newfound wealth. Mark's reaction is far more common than people realize, because living a rich life is about more than money.

If he had been asked to draw his chart at that time, it would have reflected his out‐of‐balance life and his great unhappiness.

| Financial Accomplishment | Sense of Self‐Worth | Feelings of Fulfillment | |

| 5 (high) | |||

| 4 | |||

| 3 | |||

| 2 | |||

| 1 (low) |

After months of personal reflection, Mark engaged in a process that helped him understand his values, his strengths, and his passions. He was able to reconnect with what he loved about starting and building his business, and that discovery brought renewed joy to his life. Over time, Mark saw that a new way of living was possible. He could use his skills and drive for success to make a real difference in the lives of other talented entrepreneurs by investing in their companies and sharing his expertise with them. He could invest in the United States or in small companies in developing countries.

Although he did some investing in American firms, Mark found that his greatest happiness came from working in the developing world, where a relatively modest outlay could have amazing beneficial effects on villages and regions. He invested in schools, startup ventures, and infrastructure enhancements. Cooperating with local business leaders, he preserved cultural practices while also helping to raise the standard of living for everyone in the area. His sense of purpose was reignited, and he felt fulfilled as he achieved new goals and used his talents in novel and exciting ways. He took pleasure in his personal wealth and collaborated with his advisors to preserve and increase it, while at the same time using it in ways that made him happy. His previous success was now replicated on a much wider stage, and his new life was filled with zest and excitement.

His wife and children, who observed the reawakening of Mark's entrepreneurial genius, now have joined him in his gratifying pursuits. The children are comfortable in cultures throughout the world and look forward to continuing their father's work after they have completed their educations.

“If I had to draw my chart today,” Mark says, “here's where I see myself. Providing my health holds out, I can imagine doing this for the rest of my life.”

| Financial Accomplishment | Sense of Self‐Worth | Feelings of Fulfillment | |

| 5 (high) | |||

| 4 | |||

| 3 | |||

| 2 | |||

| 1 (low) |

Another View

In a 2015 graduation speech at the USC Marshall School of Business, Evan Spiegel, founder and CEO of Snapchat, explained why he turned down a $3 billion offer to buy the company, saying, “The fastest way to figure out if you are doing something truly important to you is to have someone offer you a bunch of money [for] it. If you sell, you . . . know . . . it wasn't the right dream . . . and if you don't sell . . . you're probably onto something.”21

Spiegel created the company and obviously loves what he created. He also made a good business decision because between 2013, when he rejected the offer, and 2015, when he made the graduation speech, Snapchat's value had soared to approximately $15 billion, even though the company had yet to turn a profit. The valuation in mid‐2016 was even higher, at approximately $20 billion. He has challenges to meet and apparently intends to stay the course, at least for the moment.22 “There are very few people in the world who get to build a business like this,” Spiegel said in an interview with Forbes. “I think trading that for some short‐term gain isn't very interesting.”23 Apparently even if that short‐term gain is in the billions.

Mark Allison's and Evan Spiegel's stories show that obsessing about money is to miss the point of life. Yes, to keep a fortune going throughout the generations, it's necessary to tend to and increase it so the assets are not diminished as the family grows through marriages and the addition of children. Equally important, however, is asking the hard strategic questions: What really matters to this family, and how will we make a difference, now and forever? What are our passions? What do we believe in, and how can we make our fortune serve those beliefs? Only a balanced combination of tactical and strategic planning adequately answers those questions and prepares the family for long‐term influence and success.

Notes

_____________