CHAPTER 9

How to Abuse the System

“No.3 Commando was very anxious to be chums with Lord Glasgow, so they offered to blow up an old tree stump for him and he was very grateful and said dont spoil the plantation of young trees near it because that is the apple of my eye and they said no of course not we can blow a tree down so it falls on a sixpence and Lord Glasgow said goodness you are clever and he asked them all to luncheon for the great explosion. So Col. Durnford-Slater D.S.O. said to his subaltern, have you put enough explosive in the tree. Yes, sir, 75lbs. Is that enough? Yes sir I worked it out by mathematics it is exactly right. Well better put a bit more. Very good sir.

And when Col. D. Slater D.S.O. had had his port he sent for the subaltern and said subaltern better put a bit more explosive in that tree. I don't want to disappoint Lord Glasgow. Very good sir.

Then they all went out to see the explosion and Col. D.S. D.S.O. said you will see that tree fall flat at just the angle where it will hurt no young trees and Lord Glasgow said goodness you are clever.

So soon they lit the fuse and waited for the explosion and presently the tree, instead of falling quietly sideways, rose 50 feet into the air taking with it 1/2 acre of soil and the whole young plantation.

And the subaltern said Sir, I made a mistake, it should have been 71/2 lbs not 75.

Lord Glasgow was so upset he walked in dead silence back to his castle and when they came to the turn of the drive in sight of his castle what should they find but that every pane of glass in the building was broken.

So Lord Glasgow gave a little cry and ran to hide his emotions in the lavatory and there when he pulled the plug the entire ceiling, loosened by the explosion, fell on his head.

This is quite true.”

—Letter by Evelyn Waugh to his wife (31 May 1942).

“The guys who made the world go kablooey.”

—Answer to the survey question: “How would you describe quantitative finance at a dinner party?” at wilmott.com

Any system, whether it's financial, business, social, or governmental, ought to be set up so that the natural selfish or cooperative actions of individuals can benefit the organization as a whole. An alternative is that the system encourages a certain type of selfish behavior that harms the whole. Guess which of these two is the current financial system? In this chapter, we'll see how the bonus system based on using other people's money encourages dangerous practices such as concentration of risk, and the selling of things for less than they're worth. And that's just the legal stuff. We'll see the gray area in which models can be used to hide risk, and to encourage risk taking. We'll expose just how dangerous it is to rely solely on the numbers, without any sanity checking. And we'll show how mistakes – deliberate or otherwise – can make the ceiling fall in.

In earlier chapters we have introduced you to some of the elegantly beautiful math that forms the basis of quantitative finance. We have shown how these methods allow quants to derive prices for all kinds of complex derivatives. We have given some flavor of their working practices, their amazing salaries, and their blind spots. So now, it's time to see if you, the reader, have actually been paying attention – and if you have what it takes to work in the exciting world of quantitative finance. Can you put this learning into practice? Can you think like a quant?

Or maybe you are a quant? In which case, this is your chance to prove you deserve that magnificent pay package and rid yourself of any lingering traces of “imposter syndrome”!

We are going to set you three exercises. You must answer them as if you were working in a bank or a hedge fund. You can draw inspiration from classical economic ideas, from behavioral finance, from your own experiences. There are 30 points up for grabs.

Exercise 1: The Newbie Trader

Scenario: Imagine that you have just finished your PhD in modeling credit risk and probability of default. Your work was so groundbreaking and relevant that you walked into a job at a large bank and into their credit-instrument department. This department has a couple of dozen seasoned traders and you, the newbie, are going to be joining them. The pay is okay, but it's the potential bonus that makes this your dream job. You are being introduced to the other traders: “Hi, I'm Ralph, I went to MIT and I trade CDOs.” “Hi, Ralph.” “Hey, I'm Charles, I went to NYU and I trade CDOs.” “Hey, Charles.” “Yo, dude, I'm Paul. I went to Stanford and I trade CDOs.” “Yo, Paul.” And even Larry (he of Harvard) trades CDOs. You are surprised that everyone seems to have the same strategy. And you know from your studies that CDOs are dangerous, and that at most there's a 60% chance of making money with them. Meanwhile, your research has given you some trading ideas that are 80% likely to pay off. That's why you were hired, right?

Question: What do you trade? Do you follow the better strategies that you've been researching for the last four years, or do you follow the herd and trade CDOs like everyone else?

Hint: What does classical finance tell you about eggs and baskets?

Write your answer and justification here:

___________________________________________________________

___________________________________________________________

___________________________________________________________

___________________________________________________________

_________________

Correct answer: You trade CDOs, of course! Diversification is for suckers! (Apologies for trying to mislead you with the hint, it won't happen again.)

Explanation: First you have to ask yourself what you are trying to achieve here. There are many things you might be interested in, such as how much money you make, not getting fired, a pleasant working environment, making your parents proud, doing the best for the shareholders. The best strategy for the first four of these goals is achieved by doing the same strategy as the rest of the credit team.

How much money do you make? Well, we know that the vast bulk of your pay will be in the form of the bonus. And to get the bonus you need to be a good trader. So if you follow your strategy then you'll be profitable 80% of the time, and therefore get a bonus 80% of the time. Right? No. Bonuses are typically assessed on the performance of both you individually, and the entire team. So you will only get a bonus if both you and the entire desk make money. If all the rest of the credit team lose money, then there ain't going to be bonuses for them… or you. There's just no money, lads. Do the math. Assuming that their trades and yours are independent, then the probability of both you and the others making money is 0.8 × 0.6 = 48%. Less than half of the time. Whereas if you join them in trading CDOs, you have a 60% chance of making money and getting a bonus.

If you are part of the herd, it also decreases your chance of getting fired. You are already in a dangerous position being last in. But if you also lose money with your crazy ivory-tower ideas then it will just be a matter of time before one morning you find your card reader won't open the door, and the receptionist asks you to wait in the lobby while someone brings your things. (In finance, job security is tenuous to say the least, which is why everyone is in such a hurry about their bonus.)

Being part of the herd, rather than being a bit unusual, is also good for self-esteem in your working environment.

Money, (relative) security, a nice working environment… every mother's dream for her baby.

In contrast, it is true that the bank's interest and the shareholders’ interests are best served by as much diversification as possible. Especially diversification that actually increases expected return. But who cares about shareholders?

Points: Give yourself 5 points for the correct answer. Also, 1 point for each of the above (or similar) five angles to this question. For a total of 10 possible points.

This is not just an academic exercise, but it is nice to see this simple idea illustrated with numbers. The concept behind those numbers is as elementary as the concepts behind Markowitz's portfolio management, you're just trying to optimize something different.

This might not strictly be an abuse of the system, since the newbie trader is just doing what's best for him. Selfish it may be, but it's not his job to look after the shareholders. That's for the bank's directors. What we have here is a fault within the system, a fault that encourages putting all eggs into one basket. And as is so often the case, it could well be your eggs that are put at risk. They're your eggs in someone else's basket. It's simply a case of incentives being aligned with potentially bad outcomes. We are always hearing how bonuses encourage people to work harder. But it's more likely that they encourage that hard work to be whatever makes the most bonus, not what is most beneficial for the system as a whole. And traditionally, and legally, it's the shareholders who are supposed to be the ones ultimately benefitting, since they are the ones taking the financial risk, the risk of serious downside.

Does this matter? Does this really happen in practice? You bet. We chose the example of CDOs for a reason, since they became such an enormous business in the run up to the crisis of 2008.

Exercise 2: The Hedge Fund Manager

Scenario: You are a clever statistician. Thanks to your reputation, you have been able to set up a hedge fund. A small part of the assets under management are your own, but this is a negligible portion of your wealth (most of which is tied up in property, Manhattan, the Hamptons, Barbados, …, and some Damien Hirsts); the rest is other people's money. You have a statistical model of various complex assets. Your model tells you that some instrument, let's say a put option, has a theoretical value of 10 cents. But that theoretical value is based, like classical quant theory, on an average. Actually, the contract could end up being worth zero or $100. The contract has a maturity of one month.

Question: What should your strategy be? Do you buy the contract or sell it? And for how much?

Hint: What would Oscar Wilde do?

Write your answer and justification here:

___________________________________________________________

___________________________________________________________

___________________________________________________________

___________________________________________________________

_________________

Correct answer: Sell as many and as often as possible for 5 cents! Oscar Wilde would have made a great hedge fund manager!

Explanation: In Lady Windermere's Fan, Cecil Graham says “What is a cynic?” to which Lord Darlington answers “A man who knows the price of everything, and the value of nothing.” We know the theoretical value of the contract, it's 10 cents. And everyone knows that you should aim to buy something for less than fair value, and sell for more. That's just plain business sense. Even if you are making jam in your kitchen, you add up the cost of the ingredients, the fruit, sugar, and pectin, the fuel used, the packaging, jars, lids, labels, marketing, transport, etc., and divide by the number of jars produced, and that's the very least you must sell each jar for. Think of this calculation as giving you the theoretical value of a jar of jam. It's not unlike valuing a derivative, where the delta hedging with the underlying takes the role of making the jam from its ingredients. If you sell the jam for less, then you are going to go out of business. Rarely do you aim to make a loss. One notable exception is the supermarket loss leader, where the cheaper-than-fair-value product is the lure to get you into the shop. And really that loss is a cost that should be allocated to your advertising budget. But surely hedge funds try to make money everywhere, there's no role for loss leaders in rational high finance.

The contract in question is special in that it has a very skewed payoff. Almost always it pays off zip at the end of the month. But every now and again it pays off $100. Now, for the average of zero and $100 to be $0.1, you need to have a very small chance of getting the big one. Just solve

for p, the probability of getting $100. That's a probability of 0.001, or 1 in 1000. Each month there'd be a 99.9% chance of getting zero. In 10 years there's only an 11.3% chance of getting a nonzero payoff.1 The average lifespan of a hedge fund is three years. Sorry, but buying these contracts, even if you could get them for a couple of cents, way below their fair value, is not a viable business, you won't even make that three-year average.

No, a better business is to sell them. If you sell them then very, very rarely will you have to pay out that $100. So, virtually every month you will collect the premium. Obviously you'll sell them for as much as you can. Or rather you'll sell them for whatever optimizes your income. Assuming that you'll sell fewer the higher the price, then there might be an optimal value for the price and a maximum income. But crucially it doesn't matter whether the price you sell them for is above or below the fair value. Let's see why this is.

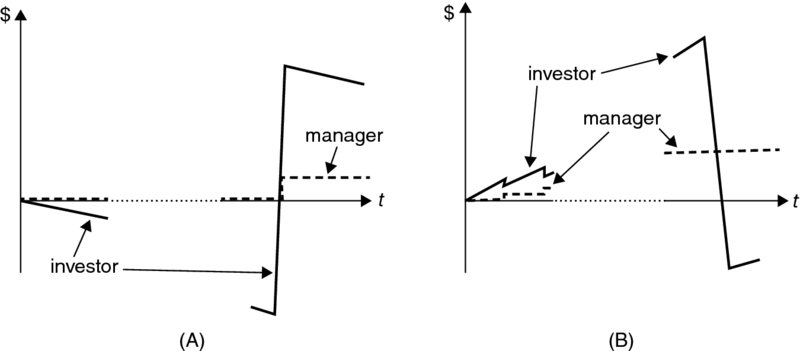

Take a look at Figure 9.1. Strategy A is to buy for less than fair value, assuming such a thing is even possible. The investor, the solid line, loses year after year, decade after decade. Eventually the contract pays off and his P&L makes it into the black. And that's when the manager gets his performance fee, typically based on a percentage of the profit. But what investor is going to have the patience to wait for this to happen?2 Long before this, the investor will have taken their money out and you will have closed down your fund.

Figure 9.1 Two extreme strategies: (A) successful for both investor and manager in the long run; (B) successful for the manager, but ultimately catastrophic for the investor

Now look at strategy B. This is selling for less than fair value. The investor's P&L is rising to start with. At the end of every year 20%, say, of the year's profit goes to the manager as his performance fee. His P&L increases in annual jumps. (There's an equal and opposite fall in the investor's P&L.) Eventually the big one hits and the investor loses, big time. We've represented the fact that the sale price is less than fair value by having this investor P&L fall far below the starting value of zero. Meanwhile, the manager's P&L has been increasing annually. And even though the investor ends up losing, the manager, of course, doesn't have to hand anything back.

Clearly, what's good for the investor and what's good for the manager can be very different, even though the manager is compensated for his success. In Chapter 2 we told the story of John Law in Venice, betting his 10,000 pistoles against the chances of any comer rolling six sixes (expected payout 0.21 pistoles). In the modern version, you can happily increase the prize to 100,000 pistoles, so the long-term odds are against you – but you don't care because it's not your money.

Points: Give yourself 2 points for saying you should sell these contracts. And 8 points if you said you could sell them for less than they are worth.

This is definitely abuse. You could argue that the results of Exercise 1 were just unfortunate or unintended, but to knowingly sell something for less than its value in order to profit from someone else's misfortune is definitely immoral. The performance-related pay again has unintended consequences, but we've shown how a devious mind might easily exploit this. It also requires a plausible “story” for the fund. Why are they selling for less than it's worth? Or perhaps, like some Mafia accountant, they have the books/model for public view and the private books/model for internal use.

There is a slightly toned-down version of this situation. Imagine going into your hedge fund office and looking at your model's predictions. On this day your model says that there are no new trading opportunities, all contracts have negative expectations. Okay, so you won't be putting on any new trades today. Never mind, the weather's good, might as well go to the golf course, perhaps pick up some new business among the members. Next day, same story. All contracts are losers. And it's the same for the rest of the week. The month. Uh oh, what's going on? Maybe this will be a temporary blip. Or maybe your model has just broken, the market has changed, there's been a regime shift. The decent and rational thing to do is to stop trading, tell investors, and check (or, if necessary, redesign) your model. Unfortunately, if you stop trading, even with the best and most logical of reasons, your investors will take their money out and invest it elsewhere. However, equally logical and equally best, at least for you, is to keep trading while you do the redesign. Even if that means buying contracts that have negative expectations. Investors are used to funds occasionally losing money. They expect it, even if they don't exactly like it. They could tolerate several months of small losses without withdrawing their money. Again, the incentives of the hedge fund are not aligned with the best interests of the investors.

In Chapter 5, we spoke about the market price of risk, which is the amount that investors demand in return for accepting risk. Usually it is depicted by a line sloping upwards in the risk–reward diagram, so expected return increases with risk. But in this example, the graph has the wrong sign – investors are paying to take risks. They just don't know it.

Exercise 3: The Risk Manager

Scenario: You are a risk manager in a bank. You have been asked by a trader to measure the risk in a portfolio of assets. The problem with this portfolio is that it's not clear how diversified the portfolio is. It's possible that all of the assets are independent of each other, but you could imagine times when they become more correlated. You give a number to the trader, your estimate of the risk. It's clear from his facial expression that this number is too high, perhaps there's a limit to the risk he's allowed to take.

Question: What action do you suggest?

Hint: What's the quant equivalent of playing the man not the ball?

Write your answer and justification here:

___________________________________________________________

___________________________________________________________

___________________________________________________________

___________________________________________________________

_________________

Correct answer: You must have made a mistake. Go back to your calculations and “correct” them to show that there is less risk! (We gave an example of this from a real trader back in Chapter 3.)

Explanation: Let's be clear, the trader is the boss. Without traders there's no bank. We aren't talking about a Mary-Poppins-and-Dick-Van-Dyke-style bank here. The bank exists for the trader, and it is risk management's job to provide the justification for the traders’ trades. Obviously not in theory, but in practice. The theory is that risk management is supposed to quantify the risks and the probabilities on the downside, and thereby show how to reduce that risk to acceptable levels by hedging, diversifying, or simply closing positions. However, the practice is that risk-management tools can be used in more nefarious ways.

How easy is this to do? We're not experts, but it only took minutes with real data to figure out plausible ways to game the numbers.

Let's take some real data. In Table 9.1 are the volatilities and correlations for five US stocks using two years’ worth of data.

Table 9.1 Volatilities and correlations using two recent years of data

| Correlations | ||||||

| Stock | Volatility | JNJ | AAPL | PG | IBM | CCE |

| JNJ | 0.14 | 1 | 0.14 | 0.638 | 0.316 | 0.402 |

| AAPL | 0.259 | 0.14 | 1 | 0.181 | −0.005 | 0.037 |

| PG | 0.143 | 0.638 | 0.181 | 1 | 0.192 | 0.303 |

| IBM | 0.18 | 0.316 | −0.005 | 0.192 | 1 | 0.47 |

| CCE | 0.16 | 0.402 | 0.037 | 0.303 | 0.47 | 1 |

The ones on the diagonal represent the correlation of a stock with itself, which is 1. The negative correlation between IBM and AAPL (Apple) is because they tend to move in opposite directions.

Now suppose that we hold $100 in each of these stocks. We can easily calculate the standard deviation, a measure of risk, over the next year, say.3 This calculation gives us a standard deviation (risk) of $55. This is not acceptable. Our limit is $50.

The natural, and indeed probably morally correct, response is to cut back on one or more positions to reduce the $55 down to $50. But that means a smaller portfolio and smaller profits. Not to mention it also means that the risk manager holds some power over the trader. No, let's rethink those numbers.

Suppose we work with four years’ worth of data? Surely two years is just too small a data set; think of the possible statistical errors. If we go back four years, we get the parameters in Table 9.2

Table 9.2 Volatilities and correlations using four recent years of data

| Correlations | ||||||

| Stock | Volatility | JNJ | AAPL | PG | IBM | CCE |

| JNJ | 0.132 | 1 | −0.001 | 0.542 | 0.22 | 0.392 |

| AAPL | 0.253 | −0.001 | 1 | 0.173 | 0.217 | 0.116 |

| PG | 0.133 | 0.542 | 0.173 | 1 | 0.103 | 0.285 |

| IBM | 0.158 | 0.22 | 0.217 | 0.103 | 1 | 0.419 |

| CCE | 0.159 | 0.392 | 0.116 | 0.285 | 0.419 | 1 |

Now we find that the risk is $52. Bugger, so close! (Of course, it could have been that four years of data made things worse, maybe we'd then look at one year of data, which after all is more recent. Muahaha!)

Notice that the volatilities all just happen to be lower using the larger data set, but only marginally so. In contrast, the correlations have changed quite a lot. Hmm… that gives us an idea. Clearly, correlations are moving around a lot (true). And who is to say that the correlations we've measured are statistically accurate (also true). And, you know, there's clearly a trend here (er, hang on a sec’). Inspired by these thoughts, let's tweak the correlations. Let's change them by 0.1, that's of the order of magnitude of the movement/error/trend. And by doing this we can get the risk down to a mere $46. Below the risk limit. Job done.

And you know what? It also means that the trader can now even increase his positions by almost 10%!

None of this is difficult to do. Think of all the different ways there are to measure volatility and correlation, using moving windows, weighted in various ways, using daily, weekly, monthly, etc. data. It's almost impossible to have a data set in which you are confident anyway.

The end result of this is a (temporarily) happy trader. But you're smarter than him, no? And if you're really clever then you'd go one step further. You'd fiddle the risk figure to make it as bad as possible to start with; that is, going in the wrong direction. When you then reduce the risk to acceptable levels, you'll get even more credit (more bonus?). Using the above data, two years, and adding in a margin for error, we can get the risk all the way up to a starting value of $60. Now we can boast a reduction of almost a quarter.

Points: Have 5 points for realizing that if you want to keep your job you'll have to fiddle the numbers, and 5 points if you could think of an example.

Of course, such fiddling is not something you want to make a habit of. Or at least, be subtle about it. If there's a forensic quant looking at your numbers he might easily spot a pattern. But equally, this simple experiment took us minutes to conduct using a spreadsheet and Excel's Solver add-in, and we're almost certainly not making six figures with this book. (At least the authors aren't.) Had we been compensated sufficiently, who knows how low we could get the risk with a day's work?

In another context, someone at Volkswagen clearly thought it worthwhile to do something not dissimilar when they adjusted the behavior of their diesel engines during test conditions so as to make emissions look lower. This is their cunning “defeat device.” The act of monitoring risk seems to cause people to adjust the way that risk is measured rather than reducing the risk, in an evil Heisenbergian way.

On the subject of being subtle about it, suppose you've got a kinda justifiable way of adjusting parameters to reduce the risk, then you can just automate the procedure. That gives you two levels of cover. A regulator has to first find the fiddling (but it's hidden deep inside the code), and then prove that the fiddling is malicious.

You know what we've just reinvented? Calibration! Calibration is a simple way of hiding model risk; you choose the parameters so that your model superficially appears to value everything correctly when really it's doing no such thing. Instead of doing the boring “road calibration,” you can go for the exciting “dyno calibration,” which allows extra performance at the expense of a little unseen risk. And since regulators are actively encouraging banks to calibrate, you are absolutely safe. Here we see the advantage of having a flawed model that needs constant adjustment in order to fit the data. If you want to understand how regulators think, you couldn't do better than study Inspector Clouseau in the Pink Panther movies.

We can take this idea a lot, lot further.

On the wilmott.com forum there are always students asking for mathematical finance research topics:

“Hi, We are required to write up a dissertation for the summer term as part of our MSc in Financial Mathematics & Computation. Any suggestions on how/where I can start if I want to come up with a topic on my own? Thank you.”4

We have one for you if you are interested. It's about building a mathematical model for some instrument, let's say an interest-rate product so we'll need an interest-rate model. You have to design a rates model with the following characteristics.

- It must be simple enough to use in practice.

- It must be possible to calibrate this model, and recalibrate if necessary, to as many liquid instruments as possible.

- It must be possible to optimize parameters in the model with the following goal: to maximize the contract's value at some time in the future, specifically at bonus time.

- It doesn't matter whether the model matches statistical data for how interest rates behave.

- And how well it performs in terms of making money is irrelevant.

- Also irrelevant is how it performs after bonus time.

You can see where we are going with this. Cash flow can be irrelevant for profit. Profit can depend on perceived value and in some cases a mathematical model. So your bonus can be linked to a number you've made up. No chance of abuse there then! And after bonus time, you'll probably move on to an even better paid job at another bank so you're not concerned how the model performs.

Given the intellectual limitations of anyone monitoring your model, why not go the whole hog and try to make as much money for yourself as possible? Make this the topic of your PhD thesis and that quant job at Goldman Sachs is yours.

Anyway, it's now time to assess your performance. Add up the sum of your scores. If the answer is:

- 0–9. You recently completed an economics degree.

- 10–19. Please try harder.

- 20–29. Good effort! You definitely have a future, even if the world financial system doesn't.

- 30. Hah! We just included this to tell if you cheated by looking at the answers! Bonus star.

Triple-A

Now, we don't want to give the impression that quantitative finance is necessarily more corrupt than other areas – vehicle emission controls, say, or politics. However, quantitative finance is unique in a couple of respects. One is the scale of the problem – it's one thing to do a favor in return for a handout, it's another to blow up a quadrillion-dollar credit bubble and charge commission on it. The other is the way that quants can avoid charges of corruption. The financial crisis of 2007/8 may have been partly caused by quants, but hardly anyone went to jail for their role, except in Iceland, which is a complete no-go zone for quants (in the UK, zero bankers received a custodial sentence; in the USA, one did; in Iceland, 26 did).5 And this is where the models show their more sinister side.

The common thread in the three test questions above is the industrial-scale abuse of mathematical models in order to optimize the quant's interests rather than those of the client.

- Using flawed but industry-standard models because they are safe, for the quant.

- Selling products which are destined to eventually blow up, but only after the manager has collected his fee.

- Adjusting the model to give the desired result.

In each of these cases, the model is there less to elucidate the truth, than to provide a plausible story for a particular course of action. Quants use the apparently objective, detached, and impartial nature of mathematical formulas as a kind of concealment, but also as a stamp of certification.

Consider again the example of CDOs, which played such an important role in the financial crisis. These relied on collecting a large number of instruments such as household mortgages, repackaging them into separate bundles, and assigning each bundle a specific investment grade. The resulting products were then sold off to investors around the world. The process was therefore like sausage making – the inputs were a lot of messy parts, but the outputs were easily traded, plastic-wrapped products with a tailored degree of risk.

Key to making this work was the copula pricing model. Originally invented by quants, it was also adopted by rating agencies such as Standard & Poor's. Both groups had an incentive to provide favorable ratings – quants because they were selling the products, and rating agencies because the quants were their clients. According to a US civil complaint against S&P, the company's internal S&P documents showed that model results were adjusted to give the right (i.e., triple-A) answers. As Tony West from the US Justice Department put it, “It's sort of like buying sausage from your favorite butcher, and he assures you the sausage was made fresh that morning and is safe. What he doesn't tell you is that it was made with meat he knows is rotten and plans to throw out later that night.”6

That landmark case ended in a 2015 settlement, where S&P did not admit to violating laws on those mortgage deals. However, they did agree to pay $1.37 billion, with about half going to the Justice Department and the rest being divided between 19 states and the District of Columbia.7 For comparison, the firm claimed that it made about $900 million on the deals. No individual was punished or found to be at fault. Which is a little strange, when you think about it – how big would the fine have been if someone had actually done something wrong? Models are the perfect get-out-of-jail card.

Defeat Device

It still seems remarkable that an industry which is so important to society can get away with manipulating models in this way, with only the occasional profit-denting fine to worry about. But one of the advantages of mathematical models, if defending them is the aim, is that they can only be understood by a relatively small number of experts. The only people debating copula models in the early 2000s were those working in that particular part of the financial sector. At the same time, mathematical equations can seem imposing to those outside the field, which grants a degree of immunity. While journalists, anthropologists, film makers, and so on have investigated the banking industry to great effect, they usually have to get their information secondhand from anonymous sources (the non-anonymous type get fired) and tend to avoid getting into the nitty gritty of the equations (it's hard, and makes lousy TV).

Again, this problem is not unique to finance. In the early 1980s, a paper by Will Keepin and Brian Wynne showed that a model used by nuclear scientists to predict future energy requirements was drastically overestimating the need for nuclear power plants – not to mention the nuclear scientists to design them. As Keepin described it, the model was so flexible that “It was a bit like the Wizard of Oz… Some guy was pulling on levers and making a big show, but it was a show determined by the little guy behind the curtain.”8 In physics, authors such as Lee Smolin and Peter Woit have written about the sociology of university departments, where promotion is based on fitting in with what Smolin describes as “groupthink” about correct modeling approaches.9

However, this still doesn't seem to quite explain what is going on in finance. Few journalists or readers care much about string theory, but they are certainly interested in where their money is going. So barriers which might put off a detailed investigation of a university physics department surely won't dissuade someone bent on an exposé of quantitative finance. Quants may be afraid to speak to journalists because they will lose their jobs, but so are most professionals, and whistleblowers still appear. So how is it that the finance sector – after nearly blowing up the world financial system through its miscalculations – can continue to escape serious scrutiny? What makes it special?

The answer to this question, we believe, lies in the fact that only finance has learned to fully exploit the power of the ultimate defeat device – which as any math-phobe will remember from school is mathematical equations. It doesn't just use formulas to dazzle – it imbues them with a kind of higher moral authority. It makes them into a consistent story. And by doing so it has achieved a remarkable degree of buy-in not just from those working in the field, but also from regulators, academia, the media, and the general public.

Whenever you make a mathematical model of a process, you are moving the system to the abstract plane of number. It seems to become objective and rational, free from the vagaries of human behavior or emotion. But quant finance (with its economist apologists) goes further, because it manages to transfer these properties to the system itself. Market prices are seen as objective, rational, and intrinsically fair. If the price of a commodity, a currency, a stock, or a complex derivative spikes or plunges, that's just the system at work. To criticize quantitative finance is therefore to criticize the markets themselves, which makes no sense because they are as objective and impartial as a physical phenomenon. It is as effective as yelling abuse at a storm.

In an area such as engineering or biology, one can argue about a particular model and use experiment as a guide – the model and the system are seen as separate things. But the dominant lesson of mainstream economics, with its assumptions of stability, efficiency, and rationality, is that market price and value are one and the same.10 Models based on this theory are therefore seen as inviolable. The only human factor comes in during calibration, which can always be interpreted as human error. There is little account for the fact, not only that the models are wrong, but that their use can affect the system itself.

Consider, for example, the testimony that Alan Greenspan provided to the House Committee of Government Oversight and Reform in 2008. “In recent decades, a vast risk-management and pricing system has evolved, combining the best insights of mathematicians and finance experts supported by major advances in computer and communications technology. A Nobel Prize was awarded for the discovery of the pricing model that underpins much of the advance in derivatives markets. This modern risk management paradigm held sway for decades. The whole intellectual edifice, however, collapsed in the summer of last year because the data inputted into the risk management models generally covered only the past two decades, a period of euphoria” (our emphasis).11 He went on: “Had instead the models been fitted more appropriately to historic periods of stress, capital requirements would have been much higher and the financial world would be in far better shape today, in my judgment.” So according to Greenspan, there was nothing wrong with the math – some over-enthusiastic young people just plugged the wrong numbers into the formula, and blew out all the windows. The global financial crisis, in other words, was all due to a naive and innocent calibration error.

Of course, while the media and the general public might be willing to go along with this story, there should be at least a few academics who can see the flaws in the model. Such experts have in fact been around for a long time, and are collectively known as heterodox economists – or more colloquially as cranks. Despite being taken slightly more seriously since the crisis, and aided also by the recent shift toward empirical data-driven approaches in the social sciences, they generally don't win important prizes or get invited to the White House for policy meetings, and their intellectual edifices are the mental equivalent of shanty towns surrounding the gleaming high-rent downtown core of mainstream economics.12 Now, are we saying that money in the form of, for example, grants and consulting opportunities could possibly affect the intellectual output of university economics departments, and decide who gets power and influence? Or that the influence of wealthy benefactors on economists did not stop with Adam Smith (Box 1.1)? Well, how many other fields have their “Nobel Prize” paid for by a bank? As economist Barry Eichengreen notes, university economists “do not object to the occasional high-paying consulting gig. They don't mind serving as the entertainment at beachside and ski-slope retreats hosted by investment banks for their important clients.” The result is “a subconscious tendency to embrace the arguments of one's more ‘successful’ colleagues in a discipline where money, in this case earned through speaking engagements and consultancies, is the common denominator of success.”13 (The 2010 documentary film Inside Job did a revealing take on economists’ supporting role in the crisis.)

Finally, there are the regulators. We'll discuss this topic more in the next chapter, but here is what author and journalist Joris Luyendijk wrote about it, after conducting a series of interviews with people in the financial sector after the crisis. “Perhaps the most terrifying interview of all the 200 I recorded was with a senior regulator. It was not only what he said but how he said it: as if the status quo was simply unassailable. Ultimately, he explained, regulators – the government agencies that ensure the financial sector is safe and compliant – rely on self-declaration; what is presented by a bank's internal management. The trouble, he said with a calm smile, is that a bank's internal management often doesn't know what's going on because banks today are so vast and complex. He did not think he had ever been deliberately lied to, although he acknowledged that, obviously, he couldn't know for sure. ‘The real threat is not a bank's management hiding things from us, it's the management not knowing themselves what the risks are.’”14

Well, other industries are complicated as well, but regulators somehow manage to cope. And since the financial sector, unlike most lines of business, has the power to destroy the world economy, you would think it deserves especially close attention. However, part of the economic story which policy makers such as Greenspan bought into was that finance is inherently efficient and therefore self-regulating – so it is no surprise that regulators lack the resources or even the motivation to dig a little deeper. As Ben Bernanke reassured Congress in 2006, “the best way to make sure the hedge funds are not taking excessive risk or excessive leverage is through market discipline.”15 And anyway, who needs fallible, human regulators when the mathematical models used by quants can compute and control risk automatically.

This trust in the system – or confusion of the reality with the model – is what Adair Turner called “regulatory capture through the intellectual zeitgeist.” Abandoning it would put regulators “in a much more worrying space, because you don't have an intellectual system to refer each of your decisions.”16 (That is, it would no longer be enough to politely ask hedge funds to self-report their VaR.) One respondent to our survey described attending a finance conference two years after the crisis, with the leaders of the major banks and regulatory officers from G20 countries. The take-home message was: “We don't want any more regulation, as it kills financial innovation. What is the use of state treasury departments? They are for the good of the financial sector. We need them for these bad days.”

Quantitative finance has therefore pulled off a truly amazing stunt, by bringing all the relevant players together on the same page. And here again we see the connection between making models and writing fiction – both involve creating a universe that people can believe in. The difference is that quants spin their stories out of mathematical formulas. In the next chapter, though, we show how the story is at risk of falling apart.