Chapter 9

The Business Use of Your Home

IN THIS CHAPTER

![]() Understanding the new rules for home office deductions

Understanding the new rules for home office deductions

![]() Looking at allowable deductions for using your home for your business

Looking at allowable deductions for using your home for your business

![]() Realizing the downsides to home office deductions

Realizing the downsides to home office deductions

Everybody who runs a small business needs a place to work. Even if your business is a laptop computer and your office is wherever you choose to locate your posterior, you should think through the decisions of where to work and how much space you need. In Chapter 4, I discuss these “real estate” decisions for your small business.

In this chapter, I explain how the home office deduction tax rules work, including the recent and simplified home office deduction. I detail what deductions you may and may not take for using your home for your business. I also discuss the downsides to home office deductions, including audit risks and issues that crop up when you go to sell your home.

The New, Simplified Home Office Deduction

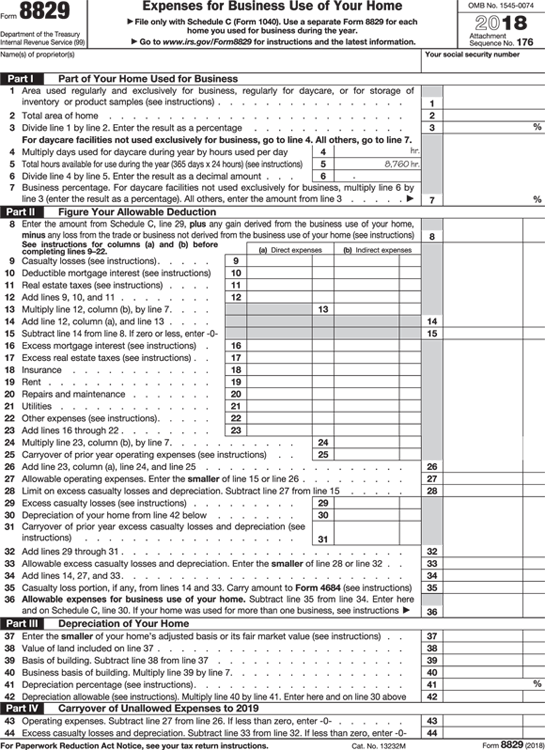

To claim expenses for the business use of your home — or the so-called home office deduction — you have to complete a fairly complicated form: Form 8829, “Expenses for Business Use of Your Home,” to be exact. Form 8829 weighs in at 43 lines (see the 2018 version in Figure 9-1; the most recent version is available at www.irs.gov/pub/irs-pdf/f8829.pdf, and the Introduction has the username and password you need).

Courtesy of the Internal Revenue Service

FIGURE 9-1: Form 8829, “Expenses for Business Use of Your Home.”

The IRS may be slow, but it eventually finds ways to simplify the tax code. And it often chooses to simplify tax laws by making them more complicated! For example, rather than simplifying Form 8829, the IRS has created a new filing option for some tax filers.

Folks who qualify for claiming a home office deduction (which I explain in the next section) can now do so with the simplified home office deduction. Here are the details of this newer option:

- Your deduction is limited to $1,500 per year, which is based on a deduction of $5 per square foot for up to a 300-square-foot home office.

- No depreciation deduction is allowed.

- You claim your mortgage interest and property tax deductions on Schedule A of Form 1040 (which you can access at

www.irs.gov/pub/irs-pdf/f1040sa.pdf). - You can’t deduct any other actual expenses related to your home.

- You can’t carry forward a loss.

- You may use either the simplified method or the regular method for any taxable year.

- You choose a method by using that method on your timely filed, original federal income tax return for the taxable year.

- After you choose a method for a taxable year, you can’t later change to the other method for that same year.

- If you use the simplified method for one year and use the regular method for any subsequent year, you must calculate the depreciation deduction for the subsequent year using the appropriate optional depreciation table. This is true regardless of whether you used an optional depreciation table for the first year the property was used in business. (See Chapter 8.)

With the tax bill that took effect in 2018, know that you may only deduct up to $10,000 in state and local taxes including property taxes on Schedule A. And, you may only deduct mortgage interest on new mortgages of up $750,000 of debt. So, if you have more than these amounts, that would argue for you to consider using the “Regular Method.”

With the tax bill that took effect in 2018, know that you may only deduct up to $10,000 in state and local taxes including property taxes on Schedule A. And, you may only deduct mortgage interest on new mortgages of up $750,000 of debt. So, if you have more than these amounts, that would argue for you to consider using the “Regular Method.”

Every now and then, the IRS actually produces a table or summary that’s useful. Table 9-1 is its summary comparing the simplified and regular home office deduction.

TABLE 9-1 The Simplified Option versus the Regular Method

Simplified Option |

Regular Method |

Deduction for home office use of a portion of a residence allowed only if that portion is exclusively used on a regular basis for business purposes |

Same |

Allowable square footage of home used for business (not to exceed 300 square feet) |

Percentage of home used for business |

Standard $5 per square foot used to determine home business deduction |

Actual expenses determined and records maintained |

Home-related itemized deductions claimed in full on Schedule A |

Home-related itemized deductions apportioned between Schedule A and business schedule (Schedule C or Schedule F) |

No depreciation deduction |

Depreciation deduction for portion of home used for business |

No recapture of depreciation upon sale of home |

Recapture of depreciation on gain upon sale of home |

Deduction can’t exceed gross income from business use of home less business expenses |

Same |

Amount in excess of gross income limitation may not be carried over |

Amount in excess of gross income limitation may be carried over |

Loss carryover from use of regular method in prior year may not be claimed |

Loss carryover from use of regular method in prior year may be claimed if gross income test is met in current year |

Source: www.irs.gov

Filling Out Form 8829, “Expenses for Business Use of Your Home”

The rule allowing taxpayers to claim a deduction for the portion of their home that they use to perform administrative and management activities was originally designed to help doctors who perform their primary duties in hospitals, salespeople who spend most of their time calling at their customers’ offices, and house painters and other tradespeople who spend their time at job sites but use an office (space) in their home to do all their paperwork. Use Form 8829, “Expenses for Business Use of Your Home,” to claim the deduction. The following sections explain who can use the form, compare the simplified and original deduction methods, and walk you through the different parts of the form.

Recognizing who can use Form 8829

You’re entitled to claim a home office deduction if you have a dedicated space in your house that you use for your business, even if you use it only to conduct administrative or management activities for your company, provided you have no other office or other place of business where you can perform the same tasks. To qualify as a “home office” for tax purposes, your home office doesn’t have to be the place where you meet customers or the principal place where you conduct business.

You’re entitled to claim a home office deduction if you have a dedicated space in your house that you use for your business, even if you use it only to conduct administrative or management activities for your company, provided you have no other office or other place of business where you can perform the same tasks. To qualify as a “home office” for tax purposes, your home office doesn’t have to be the place where you meet customers or the principal place where you conduct business.

So a person who simply brings work home is out of luck. So is the person who spreads out work over the dining room table. So long as you eat there, that table isn’t dedicated solely to the pursuit of your business.

A carpenter who sets up his computer and desk in a corner of that dining room so he can price jobs and bill his clients has a valid deduction. The reason: because that corner of his dining room is set aside solely for his company’s administrative and management activities.

If you use a portion of your home to store inventory or samples, you’re also entitled to deduct your home office expenses. Say that you sell cosmetics and use part of your study to store samples. You can deduct expenses related to the portion of your study that you use to store the cosmetics, even if you use the study for other purposes.

You can use Form 8829 whether you’re a renter or a homeowner:

- If you’re a renter, filling out Form 8829 correctly means that you first determine your total rent — including insurance, cleaning, and utilities. Then you deduct the portion you use for business. For example, if you rent four rooms and use one room for business, you’re entitled to deduct 25 percent of the total. (If the rooms are the same size, you can use this method. If not, you have to figure out the percentage on a square-footage basis.)

- For homeowners, you compute the total cost of maintaining your home, including depreciation, mortgage interest, taxes, insurance, repairs, and so on. Don’t forget to deduct the cost of your cleaning service if your office is cleaned in addition to the rest of the house. Then deduct the percentage you use for business.

Measuring the part of your home used for business

Complete lines 1 through 7 on Form 8829 to determine what portion of your home you used exclusively for your business.

- Line 1: Enter the area, in square feet, of the part of your home that you used for business (for example, 500 square feet).

- Line 2: Enter the total area, in square feet, of your home (for example, 2,500 square feet).

- Line 3: To determine the percentage of your home that you used for business, divide line 1 by line 2 and enter the result as a percentage here. In the preceding example, you’d enter 20 percent (500 ÷ 2,500). Keep this percentage handy; it’s the percentage of the expenses for the whole house — such as interest, real estate taxes, depreciation, utility costs, and repairs — that you use on Form 8829 to determine your deduction.

- Line 7: Unless you use your home as a day-care facility, you can skip lines 4 through 6 (which calculate the percentage of your home that you use for your day care) and enter your deduction percentage from line 3 on line 7. If you use your home to provide day-care services, multiply the result from line 6 by the number on line 3 and enter the result here.

Figuring your allowable home office deduction

Lines 8 onward on Form 8829 get into some pretty involved calculations, much more than space allows in this book to fully detail. In this section, I walk you through the basics that apply to most people. (Take a look at IRS Publication 587, “Business Use of Your Home,” for additional information.)

- Line 8: Enter the amount from line 29 of your Schedule C (this amount is what you earned after expenses), plus any net gain or loss shown on Form 1040’s Schedule D or Form 4797, “Sales of Business Property,” that derives from your business. Your home office deduction can’t exceed this amount.

- Lines 9 through 22, column (a): Expenses that apply exclusively to your office go in this column. Repairs and maintenance, such as painting your office, are two such items.

Lines 9 through 22, column (b): Enter your expenses that apply to the entire house on these lines. The IRS refers to them as indirect expenses.

Note: If you rent, the rent that you paid goes on line 18, column (b).

- Lines 23 through 35: It’s number-crunching time — enough to make us wonder who came up with this form!

- Line 36: This is your allowable deduction. Carry it over to line 30 on Schedule C.

If you use part of your residence for business, you can deduct the mortgage interest, real estate taxes, depreciation, insurance, utilities, and repairs related to that part of your house. (You deduct the remainder of your mortgage interest and property taxes, subject to the tax law limits, on Schedule A.) Renters get to deduct their business portion of the rental expenses.

If you had more home office expenses than you could use last year, don’t forget to add the amount you had left over from your prior year’s Form 8829, onto line 25 of this year’s Form 8829. The same goes for excess casualty losses from your prior year’s Form 8829. Enter that amount on line 31.

Determining your home office’s depreciation allowance

If you own your home, you also have to apply your home office deduction percentage (from line 7 of Form 8829) to your home’s depreciation allowance. This section includes a line-by-line breakdown of the appropriate part on Form 8829.

Line 37: Your home’s value

Here’s where you compute your depreciation deduction. You get to write off the percentage of your home that you claim as a home office (20 percent in my example from the earlier section “Measuring the part of your home used for business”) depending on when you set up your office (see the later section on line 40 instructions). Residential property usually is written off over 27½ years, but because the office is used for business, it’s considered business property and has a longer life.

On line 37, enter the smaller of what you paid for your home (including the original and closing costs, as well as any improvements you’ve made to the property) or its fair market value at the time you first started to use it for business. You don’t have to make this comparison every year — only when you started claiming a home office deduction.

Line 38: Land not included

Because you can’t depreciate land, you have to subtract the value of the land that your home sits on from your home’s cost so that you calculate the house’s net cost. A value of 15 percent for the land is a safe subtraction unless you know for certain what you paid for your building lot, although a higher percentage may make sense in high-cost areas.

Line 39: Basis of building

Subtract line 38 from line 37. This amount is your home’s basis after subtracting the value of the land that you can’t depreciate.

Line 40: Business portion of your home

Multiply line 39 by your home office deduction percentage from line 7. In my earlier example, that’s the 20 percent of the house used for business that you can write off.

Line 41: Depreciation percentage

The depreciation percentage you take for your home office depends on when you established your home office. If you set up your office before May 12, 1993, it’s a 31½-year write-off. If you set up your office after May 12, 1993, the write-off is over 39 years. Use Table 9-2 to determine your depreciation percentage. (See Publication 946, “How to Depreciate Property,” for more details.)

TABLE 9-2 Depreciation Percentage for Business Use of Home

If you first used your home for business … |

Then the percentage to enter on line 41 is … |

after May 12, 1993, and before 2012 (except as noted in the following exception), |

2.564%.* |

after May 12, 1993, and before 1994, and you either started construction or had a binding contract to buy or build that home before May 13, 1993, |

the percentage given in Publication 946. |

after May 12, 1993, and you stopped using your home for business before the end of the year, |

the percentage given in Publication 946 as adjusted by the instructions under Sale or Other Disposition Before the Recovery Period Ends in that publication. |

after 1986 and before May 13, 1993, |

the percentage given in Publication 946. |

before 1987, |

the percentage given in Publication 534, “Depreciating Property Placed in Service Before 1987.” |

* Exception: If the business part of your home is qualified Indian reservation property (as defined in section 168(j)(4), see Publication 946 to figure the depreciation.

Now, in the very first year you set up your home office, you don’t take the full percentage in Table 9-2. See the depreciation tables at www.irs.gov/pub/irs-pdf/i4562.pdf (see the Introduction for the username and password you need).

Line 42: Depreciation allowable

Multiply line 40 by line 41. This number is your depreciation deduction, based on the business use of your home. Enter this amount on lines 42 and 30 of Form 8829.

Many people avoid taking depreciation on their homes for a variety of reasons. Some may not understand how depreciation works. For others, the idea of trying to figure out their home’s adjusted basis leaves them in tears. Yet others think that, if they depreciate now, they’ll have a hard time calculating their gain or loss on the sale of that home down the road. What you may fail to realize is that the IRS deems that your home’s value has depreciated whether or not you deduct the depreciation to which you’re entitled. When you go to sell that home, you may be required to recapture that depreciation, even if you didn’t actually take the deduction as part of your home office deductions on your tax return. (This admittedly esoteric example could occur if you qualify for and take other home office deduction costs on your tax return but don’t take the depreciation.)

Many people avoid taking depreciation on their homes for a variety of reasons. Some may not understand how depreciation works. For others, the idea of trying to figure out their home’s adjusted basis leaves them in tears. Yet others think that, if they depreciate now, they’ll have a hard time calculating their gain or loss on the sale of that home down the road. What you may fail to realize is that the IRS deems that your home’s value has depreciated whether or not you deduct the depreciation to which you’re entitled. When you go to sell that home, you may be required to recapture that depreciation, even if you didn’t actually take the deduction as part of your home office deductions on your tax return. (This admittedly esoteric example could occur if you qualify for and take other home office deduction costs on your tax return but don’t take the depreciation.)

Carrying over what’s left

Keep in mind that you can’t take a loss because of the home office deduction. You can, however, carry over an excess deduction amount to another year’s tax return.

On lines 43 and 44, compute the amount of your home office deduction that you couldn’t deduct. You get to deduct it in future years, provided that you have enough income.

On Schedule A, don’t forget to deduct the balance (in my earlier example, 80 percent) of your total mortgage interest from line 10(b) of Form 8829, and the balance of your total real estate taxes from line 11(b). Your mortgage interest balance goes on line 8 of Schedule A; the real estate taxes balance goes on line 5 of Schedule A.

A home office deduction can’t produce a loss (exception: you can create a loss to the extent of mortgage interest, property tax, casualty loss, and qualified mortgage insurance premiums). For example, suppose that your business income is $6,000. You have $5,000 in business expenses and $1,500 in home office expenses ($1,000 of which is for the portion of your mortgage interest and real estate tax allocated for the use of the office). First, you deduct the interest and taxes of $1,000, which leaves a balance of $5,000 for possible deductions. Then you deduct $5,000 of business expenses, which brings your business income to zero. You can’t deduct the remaining $500 of your home office expenses, but you can carry it over to the next year. If you don’t have sufficient income to deduct the $500 next year, you can carry it over again.

Understanding the Downsides to Home Office Deductions

Because taking home office deductions can lower your tax bill, why would you not want to take them? Well, assuming that you may legally take home office deductions and that they actually lower your tax bill, by all means take them. But just be aware that taking these deductions can have some real drawbacks.

In this section, I discuss the increased audit risks for home-based businesses, especially those that regularly lose money, at least on paper for tax purposes. Also, I discuss the arcane-sounding topic of depreciation recapture, which can lead to a larger tax bill when you sell a home for which you’ve previously taken a home office deduction.

Audit risk and rejection of repeated business losses

According to the IRS, a sideline activity that generates a loss year in and year out isn’t a business but a hobby. Specifically, an activity is considered a hobby if it shows a loss for at least three of the past five tax years. (Horse racing, breeding, and so on are considered hobbies if they show losses in at least five of the past seven tax years.)

Certainly, some businesses lose money. But a real business can’t afford to do so year after year and still remain in business. Who likes losing money unless the losses are really just a tax deduction front for a hobby?

When the hobby loss rules indicate that you’re engaging in a hobby, the IRS will disallow your claiming of the losses. To challenge this ruling, you must convince the IRS that you’re seriously attempting to make a profit and run a legitimate business. The IRS will want to see that you’re actively marketing your services, building your skills, and accounting for income and expenses. The IRS also will want to see that you aren’t having too much fun! When you derive too much pleasure from an activity, in the eyes of the IRS, the activity must not be a real business.

The Tax Cuts and Jobs Act bill, which took effect in 2018, toughened the hobby loss rules further. Specifically, the IRS now requires you to report your revenue from a hobby, but you may not deduct any expenses from that hobby.

Unfortunately, some self-anointed financial gurus claim that you can slash or even completely eliminate your tax bill by setting up a sideline business. They say that you can sell your services while doing something you enjoy. The problem, they argue, is that — as a regular wage earner who receives a paycheck from an employer — you can’t write off many of your other (that is, personal) expenses. These hucksters usually promise to show you the secrets of tax reduction if you shell out far too many bucks for their audiotapes and notebooks of inside information.

“Start a small business for fun, profit, and huge tax deductions,” one financial book trumpets, adding that, “The tax benefits alone are worth starting a small business.” A seminar company that offers a course on “How to Write a Book on Anything in 2 Weeks … or Less!” also offers a tax course titled “How to Have Zero Taxes Deducted from Your Paycheck.” This tax seminar tells you how to solve your tax problems: “If you have a sideline business or would like to start one, you’re eligible to have little or no taxes taken from your pay”.

Suppose that you’re interested in photography. You like to take pictures when you go on vacation. These supposed tax experts tell you to set up a photography business and start deducting all your photography-related expenses: airfare, film, utility bills, rent for your “home darkroom,” and restaurant meals with potential clients (that is, your friends). Before you know it, you’ve wiped out most of your taxes.

Sounds too good to be true, right? It is. Your business spending must be for the legitimate purpose of generating an income.

What’s the bottom line? You need to operate a legitimate business for the purpose of generating income and profits — not tax deductions. If you’re thinking that it’s worth the risk of taking tax losses for your hobby, year after year, because you won’t get caught unless you’re audited, better think again. The IRS audits an extraordinarily large number of small businesses that show regular losses.

Depreciation recapture when selling a home with previous home office deductions

If you’ve taken depreciation for your home office deduction after May 6, 1997, when you go to sell your home, you’ll have to pay tax through depreciation recapture. Specifically, you’ll owe tax at the rate of 25 percent on the amount of depreciation taken for your home office.

But if you qualify for the home office deduction, this shouldn’t be a bad thing to have happen to you because the value of those deductions over the years should far exceed the cost of the depreciation recapture.