Chapter 4

Taking the Passive Approach

IN THIS CHAPTER

![]() Researching real estate investment trusts (REITs)

Researching real estate investment trusts (REITs)

![]() Considering tenants in common real estate investments

Considering tenants in common real estate investments

![]() Exploring triple net properties

Exploring triple net properties

![]() Understanding tax lien certificate sales

Understanding tax lien certificate sales

![]() Looking at limited partnerships

Looking at limited partnerships

Many investors want the diversification and solid returns offered by real estate but aren’t qualified for or interested in actively managing their real estate holdings. These real estate investors often look for investment opportunities that require no management or even minimal interaction with a property manager. Real estate investment trusts (REITs) are probably the easiest such option to understand and access, but other avenues allow you to passively invest in real estate, including tenants in common, triple net properties, notes and trust deeds, tax lien certificate sales, and limited partnerships.

Current federal tax laws favor real estate investments in which the real estate investors qualify as active investors, and this book focuses on real estate investment strategies that qualify as active activities in order to garner the full tax benefits. If you’re seeking a passive investment, though, this chapter is for you.

Using Real Estate Investment Trusts

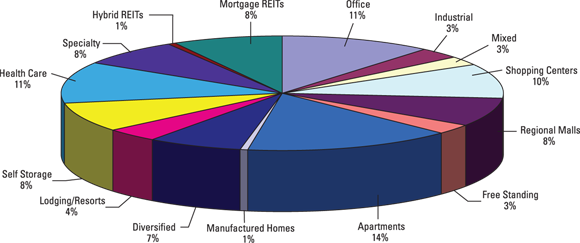

Real estate investment trusts (REITs) are for-profit companies that own and generally operate different types of property. The options for REIT investments are extremely broad and cover virtually every type of real estate. You can choose your favorite REIT from the following property types:

- Office: Ranging from Class “A” urban skyscrapers to single-story or low-rise suburban Class “C” buildings

- Residential: Apartments, student housing, manufactured homes, single-family homes

- Retail: Regional malls, outlet centers, grocery-anchored shopping centers

- Industrial: Warehouses, distribution centers

- Lodging: Hotels, resorts

- Healthcare: Hospitals, medical/dental office buildings, senior living facilities, skilled nursing and memory care facilities

- Self-storage

- Cell towers

- Other rental income properties, even timberlands

These property-holding REITs (see Figure 4-1) are known as equity REITs. Some REITs, known as mortgage REITs (or mREITs), focus on the financing end of the business; they lend to real estate property owners and operators or provide credit indirectly through buying loans (mortgage-backed securities).

Source: National Association of Real Estate Investment Trusts.

FIGURE 4-1: Property types invested in by REITs.

Equity REIT managers typically identify and negotiate the purchase of properties that they believe are good investments and manage these properties directly or through an affiliated advisory and management company, including all tenant relations. Thus, REITs can be a good way to invest in real estate for people who don’t want the hassles and headaches that come with directly owning and managing rental property. You can also invest in different property type REITs to diversify your portfolio, but check their returns and expense ratios as not all REITs within the same property type field are equivalent. This is similar to the reality that while most mutual funds all invest in the same pool of NYSE listed stocks, not all have the same expenses or results.

Equity REIT managers typically identify and negotiate the purchase of properties that they believe are good investments and manage these properties directly or through an affiliated advisory and management company, including all tenant relations. Thus, REITs can be a good way to invest in real estate for people who don’t want the hassles and headaches that come with directly owning and managing rental property. You can also invest in different property type REITs to diversify your portfolio, but check their returns and expense ratios as not all REITs within the same property type field are equivalent. This is similar to the reality that while most mutual funds all invest in the same pool of NYSE listed stocks, not all have the same expenses or results.

Distinguishing between public and private REITs

We recommend that investors not be shy about asking for full disclosure of the relationship between the REIT, its advisors, and the management companies. REITs often involve conflicts of interest that aren’t clearly disclosed or pay significant above-market fees to directly or indirectly related entities or affiliates that ultimately lower the cash flow and return on investment available for distribution.

Public REITs are traded on the major stock exchanges and thus must meet strict SEC reporting requirements:

- Liquidity: Public REITs trade every business day on a stock exchange and thus offer investors the ability to buy and sell as they please. Of course, as with other similarly liquid investments (like stock in companies in a variety of industries), liquidity can have its downside. More-liquid real estate investments like REITs may inspire frequent trades caused by making emotional decisions or trying to time market movements.

- Independent board of directors: A public company must have directors, the majority of whom are independent of its management. Shareholders vote upon and elect these directors, but that is no guarantee of their competency.

- Financial reporting: Public REITs, like other public companies, must file comprehensive financial reports quarterly.

We recommend that you stay away from private REITs unless you’re a sophisticated, experienced real estate investor willing to do plenty of extra research and digging. Because they’re not publicly traded, private REITs don’t have the same disclosure requirements as public REITs. This difference means an investor in a private REIT had better carefully scrutinize the prospectus and realize that the private REIT has the ability to make changes that may not be in the investor’s best interests but that reward the private REIT sponsors or their affiliates. Ask what commission is deducted from your gross investment to arrive at your net investment. You may be surprised at the “acceptable commission rates” for private REIT investments, especially when you compare your experience with most mutual funds with very low competitive fees and no commissions with no-load funds.

We recommend that you stay away from private REITs unless you’re a sophisticated, experienced real estate investor willing to do plenty of extra research and digging. Because they’re not publicly traded, private REITs don’t have the same disclosure requirements as public REITs. This difference means an investor in a private REIT had better carefully scrutinize the prospectus and realize that the private REIT has the ability to make changes that may not be in the investor’s best interests but that reward the private REIT sponsors or their affiliates. Ask what commission is deducted from your gross investment to arrive at your net investment. You may be surprised at the “acceptable commission rates” for private REIT investments, especially when you compare your experience with most mutual funds with very low competitive fees and no commissions with no-load funds.

Taking a look at performance

So what about performance? Over the long term, REITs have produced total returns comparable to stocks in general. In fact, REIT returns historically have been as good as or better than stock returns, whereas REITs have also generally been less volatile than stocks. In the context of an overall investment portfolio, REITs add diversification because their values don’t always move in tandem with other investments.

One final attribute of REITs we want to highlight is the fairly substantial dividends that REITs usually pay. Because these dividends are generally fully taxable (and thus not subject to the lower stock dividend tax rate), you should generally avoid holding REITs outside of retirement accounts if you’re in a high tax bracket (for instance, during your working years).

Investing in REIT funds

You can research and purchase shares in individual REITs, which trade as securities on the major stock exchanges. An even better approach is to buy a mutual fund or exchange-traded fund that invests in a diversified mixture of REITs. Some of the best REIT mutual funds charge 1 percent per year or less in management fees, have long-term track records of success while taking modest risks. Vanguard’s Real Estate Index Fund charges just 0.12 percent per year in fees and has produced average annual returns of about 10.2 percent since its inception in 1996.

Vanguard also offers an REIT ETF (exchange-traded fund) through most discount brokers and boasts a low management fee of 0.12 percent. (You can buy it without any brokerage fees through Vanguard.)

In addition to providing you with a diversified, low-hassle real estate investment, REITs offer an additional advantage that traditional rental real estate doesn’t. You can easily invest in REITs through a retirement account such as an IRA or Keogh. As with traditional real estate investments, you can even buy REITs and mutual fund REITs with borrowed money (in nonretirement accounts). Although risky, you can buy with 50 percent down, known as buying on margin, when you purchase such investments through a brokerage account.

Table 4-1 contains a short list of the best REIT mutual funds and ETFs currently available.

TABLE 4-1 The Best REIT Funds

Fund |

Toll-Free Number |

Web Site |

Cohen & Steers Realty Shares |

800-437-9912 |

|

Fidelity Real Estate Investment |

800-544-8888 |

|

TIAA-CREF Real Estate |

800-223-1200 |

|

T. Rowe Price Real Estate |

800-638-5660 |

|

Vanguard REIT ETF |

800-662-7447 |

|

Vanguard Real Estate Index |

800-662-7447 |

If you really have your heart set on becoming the next Warren Buffett and you enjoy the challenge of selecting your own stocks, you can research and choose your own REITs to invest in. Both of the investment research publications Morningstar and Value Line, which can be found at many local libraries as well as online (www.morningstar.com and www.valueline.com ), produce individual stock page summaries on various REITs. In addition to having a professional manager deciding what REITs to buy and when, the mutual fund REITs listed in Table 4-1 also provide consolidated financial reporting. If you purchase individual REITs, you have to deal with tax statements for each and every REIT you’re invested in.

Understanding Tenants in Common

Tenants in common (TIC) real estate investments have been heavily promoted as the common man’s opportunity to own a piece of institutional-grade (commonly known as trophy) properties that the average investor could never acquire on her own. Due to a March 2002 IRS real estate tax ruling, tenants in common real estate ownership gained momentum.

Tenants in common ownership is arranged by sponsors that form a TIC investment group for each property; each individual investor actually receives a title deed for an undivided fractional share in a large institutional-grade property. The TIC sponsors either already have purchased or at least control these properties.

Often the TIC sponsor will purchase the property at a lower price and then sell it to the TIC investors at a higher price so they make a very healthy return right at the formation of the TIC investment. The IRS Revenue Procedure 2002-22 even requires the TIC sponsor to take their profits upfront. The justification for this guaranteed quick profit for the TIC sponsor is that the investors don’t have to locate the property (a major factor for an owner in a tax-deferred exchange with time limits looming) and can invest in a small ownership share in a prepackaged property with a smaller cash investment.

TIC sponsored properties available for investment include regional shopping malls, large luxury apartment buildings, or even class A (with the best-quality locations, construction, and finishes) high-rise office buildings in major metropolitan areas.

These TIC investments do have some limitations: For instance, there are often limits on the number of investors (usually 35, and married couples count as a single investor); each investor is proportionately responsible for the debt on the property, if any; and each owner must actually hold a specific fractional deeded interest in the property. All owners must share and pay all profits and losses proportionately, and the TIC sponsor can’t advance funds to cover any expenses. The IRS also requires each owner to have a vote equal to his percentage of ownership.

Don’t feel too confident about your voting rights, because you probably own only a small percentage (sometimes as little as 1 or 2 percent of the total property); you may find that the majority make decisions about management and leasing. Plus, the IRS requires unanimous approval of all co-owners to borrow against the property or sell — which may or may not coincide with your goals and needs. This limitation alone is concerning.

Our advice is that although TICs provide some advantages for real estate investors seeking passive tax-sheltered income, new real estate investors and those with modest assets who may need to liquidate or sell their interest should avoid this investment now because the current TIC offerings are typically overpriced investments at full-market or retail pricing with extremely high sales commissions and costs (typically up to 7 to 10 percent of your initial investment). TICs aren’t right for many investors, and the number of sponsors offering these products has greatly diminished whereas the number of TICs in expensive and exasperating litigation has increased dramatically. We question whether there will ever be a large market for these investments and believe that investors should look to invest in real estate with more traditional investment methods or sell their real estate and invest in REITs.

Our advice is that although TICs provide some advantages for real estate investors seeking passive tax-sheltered income, new real estate investors and those with modest assets who may need to liquidate or sell their interest should avoid this investment now because the current TIC offerings are typically overpriced investments at full-market or retail pricing with extremely high sales commissions and costs (typically up to 7 to 10 percent of your initial investment). TICs aren’t right for many investors, and the number of sponsors offering these products has greatly diminished whereas the number of TICs in expensive and exasperating litigation has increased dramatically. We question whether there will ever be a large market for these investments and believe that investors should look to invest in real estate with more traditional investment methods or sell their real estate and invest in REITs.

Paying for 1031 availability and “hassle free” management

Although we prefer REITs, tenants in common (TIC) can be right for certain investors with significant net worth and no desire to directly own real estate — as long as they fully understand the benefits and drawbacks. The minimum investment for most TICs is measured in the hundreds of thousands of dollars, although some TIC sponsors offer fractionalized ownership for as little as $50,000.

Traditionally, owners with significant equity can use a tax-deferred exchange (also known as a 1031 exchange) to either sell or exchange into a larger property, or simply continue to hold and refinance the highly appreciated property to generate cash for additional real estate investments, which also offer additional tax benefits. But TIC candidates are usually real estate owners currently in or contemplating a tax-deferred exchange and are facing the strict time limits and haven’t been able to find a suitable property on their own. (See Chapter 18 for a discussion of the tax-deferred exchange.)

If you’re considering a TIC as an alternative for your tax-deferred exchange, verify in advance with your tax advisor that your transaction qualifies. Doing so is critical. Don’t overlook this important step. A tax-deferred exchange is limited to like-kind property with specific rules about how you hold title of both the relinquished and replacement properties. If the property being sold is directly owned, the transaction most likely meets the requirements and isn’t taxable at the time of sale as long as the TIC property is a direct ownership of real estate and not a security. But many investors may find that the property they’re selling is a partnership interest in real estate and doesn’t qualify for the tax-deferred treatment because the two investments aren’t like-kind. It’s also true if the IRS deems the replacement property ownership interest to be a security or anything other than direct ownership of real estate. Obtaining competent legal and tax advice in advance is essential, or you may have a very unpleasant surprise when the IRS declares that your transaction is fully taxable.

However, the TIC sponsors know that their product can be a tough sell, so they target owners of highly appreciated properties who are considering a tax-deferred exchange but are at a stage in their lives in which they’re not interested in expanding their real estate empire. Or they may have used all of the tax benefits of depreciation (see Chapter 18) and really should sell their property and simply pay the capital gains but are just simply unable to stomach the thought of paying the taxes even if it is not their best investment decision.

A downside of these TIC investments is that they’re often extremely expensive. Because the majority of the potential purchasers for these real estate investments are coming out of a tax-deferred exchange, they’re subject to tight time limits. The IRS requires 1031 exchanges to identify the replacement property within 45 days of the close of escrow of the property being sold. And the replacement property transaction must be completed within 180 days. Please see Chapter 18 for more details.

Thus, the syndicators of the tenants in common product are always standing by with a pending real estate acquisition for those buyers whose time limits are running short and who need to identify and close on a property within the time limits imposed by the IRS. If the owner is unable to meet the deadlines, they lose all of the tax deferral benefits, so they’re often willing to overpay. The TIC sponsors know that many real estate investors panic and commit to real estate investments that aren’t prudent or suited to them just to avoid paying the capital gains tax.

In exchange for this flexibility and readily available product, the syndicators have prepurchased these properties and rolled them over to the tenants in common investors at full market value, which is a higher price than the properties would sell in an arm’s-length transaction in a competitive free market. (An arm’s-length transaction simply means between an independent buyer and seller — for example, not related parties like relatives.) Further, the syndicators usually associate with financial advisors who receive hefty sales commissions of 5 to 7 percent and even as high as 10 percent of the investors’ initial investment, plus a spread to the TIC sponsor to cover its internal marketing and administration costs. Then many TIC sponsors have separate advisory firms that are closely held by the principals of the sponsor, and they commonly charge upfront, plus ongoing, consulting fees. Thus, the purchaser of a tenants in common real estate investment is paying top dollar for the property and is only receiving the benefit of as little as 90 percent of her gross investment because of commissions and fees paid upfront.

The TIC sales pitch also places a heavy emphasis on the desirability of eliminating the trials and tribulations often associated with an owner trying to manage his own property. TIC sponsored properties are professionally managed by the sponsor or a property manager of their choice, and not at the most competitive fees.

Asking whether TICs are right for you

Be aware that TIC sponsors often provide attractive teaser rates of return that are guaranteed only for the first couple of years. For example, a review of the private placement offering may indicate that investors will receive a 7 percent cash distribution per year for the first two years only. This rate may potentially entice investors who have built up significant equity in their real estate holdings but haven’t seen their cash flow increase as fast.

Also, like many other financial products, a lot of effort goes into the promotion and sales of TICs, often through independent investment advisors, which translates to a lot of overhead to cover. You typically get slick marketing materials and are referred to fancy websites or supposedly free seminars reminiscent of the late-night infomercial gurus. These promotional efforts are high on fluff and scarce on details.

You need to determine whether TICs are right for you by asking your investment advisor and the TIC sponsor for written answers to some basic questions before sending them your money:

- Who’s receiving commissions and how much? The TIC sponsor receives a commission or spread right off the top, plus the investment advisors (broker) who refer their clients get a piece of the action, too.

- Was the offered property recently acquired and at what price? Many TIC investors purchase the properties and then resell them within days or months at full retail or top of the market pricing, so it may be informative to know how much the TIC sponsor has made on the investment in addition to the commissions.

- How much of my net investment is actually invested in the property? At the end of the day, after everyone has been paid, how much of my investment actually is invested into the property?

- How solid is the tenant(s) occupying the property and what are the terms and length of their lease? The property may be a Class “A” building with a Fortune 500 tenant today, but how long is the tenant committed to the space? Are there out clauses in case of a merger or the tenant relocates? (Out clauses are any language in the lease that would allow the tenant to legally and unilaterally break the lease with only limited or no further financial obligation.) What is the likely demand for this property should the unexpected happen and the Class “A” anchor tenant leaves? What are the rent increases, and do they keep up with expected inflation?

- What’s the amount and timing of the cash distributions? If based on a certain percentage rather than actual operating results, are the distributions guaranteed, and if so, for how long and by whom? Many TIC sponsors use an above-average cash distribution as a hook to entice new investors, but property performance may not generate enough cash to cover the distributions, and investors may actually be required to cover operating losses. Where’s that fact in the fancy slick-paper full-color brochure?

- What are the charges for property and asset management? Most TIC sponsors have affiliated property management firms that handle the day-to-day management — but at fees always toward the high end of reasonable. Also, there may be another layer for an asset manager or advisory firm that supervises the property management company, and they’re also often controlled by or associated with the TIC sponsor. You have no guarantee that the asset or property management is qualified or competent, so be sure to ask questions about their experience and credentials; excellent management is extremely important. Remember that this is a passive investment, so you have little say in making any changes if they don’t meet your expectations.

- How liquid is my investment, and does the sponsor offer a buyback or loan program? Currently, there’s no viable secondary market for TIC investments, so you’re at the mercy of the TIC sponsor or possibly another investor who’d be willing to buy you out. Anyone buying a fractional ownership is going to expect and receive a significant discount from the actual asset value. Have you ever tried to sell a timeshare interest at the price you paid originally from the developer?

Of course, many investors are attracted to the fact that someone else (all TIC sponsors claim to be experts) is tracking down the properties and doing all of the due diligence, and you definitely pay a price for these benefits. So follow the money and make sure you’re comfortable with this investment, because it isn’t easy to sell should your needs change.

Our advice for investors considering TIC: Buyer beware. Do your due diligence and speak to your independent real estate, legal, and tax advisors before making any investment. Also, explore the alternatives of other forms of real estate investments or simply sell the real estate and pay your capital gains taxes and taxes on any recapture of depreciation.

Comprehending Triple Net Properties

Triple net property is a common term for a type of net lease where the tenant pays some or all of the property operating and repair and maintenance expenses in addition to the rent. Many investors are attracted to the minimal property management and maintenance requirements of triple net properties because the tenant is responsible for the majority of all operating costs and maintenance.

Triple net properties are often promoted as another real estate option for investors looking to avoid the headaches of day-to-day management. These investments may seem like real estate investments, but they’re primarily an investment in the net cash flow (after debt service) from a lease to a credit tenant, and they’re promoted based on the cash-on-cash rate of return or cap rate (see Chapter 12 for information on these measures of investment return).

For years, these properties have been the favorites of real estate investors who like the steady income stream and safety usually associated with bonds. But net leases come in all varieties, and though all net leases are often referred to generically as triple net leases, the reality is that there is no standardization of terms or definitions. So, the challenge is always to determine exactly which responsibilities belong to the landlord and which are the tenant’s, and it’s those vagaries that often make it difficult to precisely evaluate these investments.

Thinking ahead about landlord/tenant division of duties

There are several different types of net properties. However, many are erroneously called triple net leases when they are not. So you need to be careful and review the actual lease document to determine the true net aspects, as not all leases are the same.

The one common denominator is that all net leases have some aspect of the tenant paying for a portion or all of the operating expenses, taxes, insurance, maintenance, repairs, and even capital improvements. But, there are absolute triple net leases (sometimes referred to as bond leases) where the total responsibility rests with the tenant. In a bond lease, the tenant is fully responsible for the repairs, maintenance, and operating expenses (including taxes and insurance) of the entire property without any limitations.

The net net net leases (or NNN leases or triple net leases) are similar to the bond lease, with the tenant being responsible for all operating and fixed costs of the property, while the owner is still responsible for the maintenance and repair of the building envelope (roof, foundation, structural bearing walls), plus there are limitations on capital improvements or upgrades that the landlord can pass on to the tenant.

Another type of net lease is the net net lease (or NN lease or double net lease), which is an investment where the tenant pays most operating expenses. As in the net net net lease, the landlord retains responsibility for the structural components such as the foundation, bearing walls, and roof, but is also responsible for major building systems such as HVAC equipment, electrical, plumbing, and driveways and parking areas.

If you’re considering an investment in any type of net lease, you must carefully review the lease to determine exactly who is responsible for each of the components of the building. You should also be very specific on your requirements or expectations about the quality of the maintenance of the property as well as the details of the insurance coverage, including making sure you’re named on all polices as an additional insured. If you’re a novice, be sure to use the services of a real estate attorney or lease expert to prepare a lease abstract, which is a summary of the pertinent information from the lease. Robert is often retained as an expert in lease interpretation where expensive litigation is driven by even experts who can’t agree on the exact nature of who is responsible for what aspect of the building maintenance and repairs and certain other expenses.

The type of triple net lease that is most often available to investors typically involves a fast-food franchise, restaurant chain, local chain drugstore, or similar retail outlet. The owner buys the building, which is built precisely to the tenant’s specifications, and the tenant then enters a long-term, fixed-rent lease in which she pays for almost everything, including the property taxes, insurance, utilities, and most of the maintenance. Many companies rely heavily on the sale/leaseback of their newly built locations. The advantage to the tenants is that they free up capital to expand and grow their primary business, which isn’t real estate.

Originally, these investments were offered by developers who worked exclusively with such companies, but now many brokers and real estate firms specialize in the marketing and sale of triple net properties.

The owner should regularly inspect the property under any type of net lease that isn’t a bond lease because she retains ultimate control — and thus the liability — if the tenant fails to properly maintain the building. Also, many triple net lease tenants will perform only cosmetic repairs, especially as they approach the end of their lease commitment. For example, under their net lease they may be required to replace very expensive roof-mounted HVAC units, but if fewer than five years remain, they will make Band-Aid repairs or even just live without the HVAC and let the landlord regain possession of a severely depleted building with excessive wear and tear. Then, the owner has the difficult challenge of attempting to recoup her costs to bring the building back to a marketable condition to lease to a new tenant. Owners of any type of building with a net lease would be wise to hire a competent property manager who specializes in that property type and pay them the reasonable management fee that they charge to manage the property, including property inspections and demand letters to tenants requiring them to address deferred maintenance. If you do this throughout the net lease, you avoid the almost impossible task of determining why the property is in poor condition at the end of the lease period.

Robert has seen a litany of litigation between the owner and tenant over issues of exactly what type of net lease exists, with the key dispute being an interpretation of who is responsible for the repair and maintenance of building components. These lawsuits often result from third-party injuries, with the landlord and the tenant each accusing the other of failing to properly inspect, maintain, and/or repair the property.

Minimizing the risks of triple net investments

Lately, the returns available on these triple net properties have been low due to the perception that they’re essentially a risk-free investment. However, should the tenant find that the location isn’t profitable, you may find yourself owning a customized taco stand that requires a lot of modifications to be a viable location for another business.

Triple net real estate investments are suitable for some, but stay away from them unless you’re really comfortable with the tenant and the location and are willing to accept relatively low rates of return. Also, look closely at the rent structure because most leases have many years of flat, fixed rental income with an occasional upward adjustment that’s likely to be lower than the future market rent. Triple nets may make some sense if you can consistently earn a return that’s higher than a comparable bond investment. But you always run a risk with any single-tenant investment property, and major national-brand fast-food and drugstore chains can (and do) go out of business. We advise investors interested in this type of investment to consider the diversification and lower risk associated with purchasing REITs (discussed earlier in this chapter) that hold triple net properties (among others) rather than a direct purchase of a triple net property.

Robert is aware of many triple net properties that probably seemed like great deals at the time buyers purchased them with a national credit tenant (an expanding company that has a very solid financial balance sheet) on a long-term lease. What could go wrong? A lot. With leases as long as 50 years and set rents that are modestly adjusted over time, you run a serious inflation risk unless the rents can adjust to fair market rent at least every 5 to 10 years. The more specialized the use of the building by the tenant, the more challenging your life can be if the tenant vacates, so consider whether the tenant improvements are suitable or can be modified at a reasonable cost to suit the needs of a replacement tenant.

Eyeing Notes and Trust Deeds

Although the vast majority of real estate loans for purchasing or renovating properties comes from conventional lenders, some private sources of money make loans backed by notes or trust deeds. Real estate investors have found that they can benefit from the strong demand for real estate in their area by acting as a lender. They purchase notes and trust deeds that are backed by pledged real estate. Pledged real estate is the collateral or security interest provided to the investors to protect them from nonpayment by giving them the ability to foreclose on the real estate. Besides the interest earned on the investment, the note or trust deed holder has the collateral of the underlying real property if the borrower defaults on the loan.

Real estate investors who buy and sell trust deeds are also often interested in making private hard money loans (loans on top of the first mortgage made by a traditional lender) to property owners or other real estate investors. These hard money loans are secured by the owner’s equity in the property and offer potentially favorable returns for the lender willing to make loans to borrowers that often have poor credit. Although your risk increases when the borrower has credit issues, the terms can be quite attractive — typically above-market interest rates ranging from 10 to 15 percent, plus loan fees of 3 to 5 points (a point is 1 percent of the loan amount and is essentially prepaid interest), plus prepayment penalties that lock in the high interest rates or require a hefty payment for the privilege of refinancing.

Your loan is secured by a mortgage or deed of trust against the property, so it’s extremely important to be conservative with the loan-to-value ratio or the amount of money you actually lend the borrower, versus the fair market value of the property. At times, borrowers damage or neglect the property if they fall behind on the payments, so we advise real estate investors to limit their exposure to no more than 50 to 60 percent of the value of the property.

Although making and purchasing real estate notes and trust deeds can be a lucrative investment vehicle, acting as a real estate lender can be risky for the novice. Properties with latent problems or unrecorded tax liens are just some of the potential pitfalls. Should you decide that lending money on real estate offers you the high returns you’re looking for without the headaches of ownership, proceed with caution. Also be sure that you have an experienced real estate advisor and/or your real estate attorney review the documents before making an agreement or advancing any funds (see Chapter 6).

The safest approach to making secured loans on property is to thoroughly evaluate the pledged collateral to protect your investment and determine the fair market value if you had to foreclose. Never make a loan on a property that you wouldn’t be willing to own if that becomes your best way to protect your investment. Some lenders actually hope that the borrower does default so they can obtain the property for a fraction of its market value.

However, don’t forget that you’re responsible for legal fees and foreclosure costs in addition to the unpaid balance of your loan and accrued interest in the event that the borrower defaults.

Looking at Tax Lien Certificate Sales

Real estate owners who fail to pay their property taxes in a timely manner find that the local county files a lien on their property. A lien is any legal claim or charge against real or personal property for the satisfaction of a debt or duty that includes the right to take the property if the obligation isn’t discharged. The county ultimately sells the property in a tax lien certificate sale auction to generate the funds necessary to satisfy the unpaid real estate property taxes, along with the accrued penalties and fees.

But local municipalities don’t want to foreclose or wait for payment because they need the funds today to pay the costs of government, so they auction off these tax lien certificates to investors.

Tax lien certificates can be a good investment regardless of the economic cycle, because some property owners will always be unable to pay their property taxes. When you buy a real estate tax lien, you’re simply providing the government entity with the funds for the delinquent taxes and buying the rights to collect those taxes from the property owner (plus penalties and a fixed rate of interest that can range from 12 to 24 percent per year).

The property owner can’t sell or pledge her real estate without paying the outstanding tax liens, so over 90 percent of the tax lien certificates are redeemed within 24 months (or the maximum allowable redemption period set by each state or county). Look for tax lien certificates in certain types of real estate, such as owner-occupied properties, because these tend to have nearly a 100 percent redemption rate. You may ultimately have to give the required legal notices and foreclose on the underlying real estate to achieve your return of capital and realize your return on investment, so always limit your purchase of tax lien certificates to properties that you’re willing to own.

Tax lien certificates aren’t available in every state, and you don’t have any way to control the timing of the redemption. Savvy real estate investors that have done quite well with tax lien certificate sales generally buy multiple liens to spread out their anticipated payoffs. Also, they read the fine print of the government rules and regulations concerning these sales, because the rules vary greatly from state to state — and each county within a state may have different rules. Contact your county tax collector to see whether real estate tax lien certificates are a viable investment alternative in your area.

You have to devote the time necessary to really find out about the underlying properties even though finding information is difficult. The conventional sources of local real estate knowledge — brokers and agents — don’t work in this market because they offer no opportunities for them to earn commissions.

Considering Limited Partnerships

Unlike a general partnership, in which every partner has full management authority and accountability, a real estate limited partnership is an investment program in which general partners manage property and accept unlimited liability, and the limited partners don’t participate in management decisions and their liability for losses is limited to their investment. A limited partnership offers advantages to real estate investors who want to participate in the market while limiting their day-to-day involvement and liability.

The disadvantage of limited partnerships is that limited partners don’t have any authority, so limited partnerships are passive investments.

In a limited partnership, the general partner makes all the decisions of management and even decides when to sell the property. Upon disposition, many limited partnerships provide for the general partner to receive a portion of the appreciation (usually from 10 to 25 percent) right off the top — prior to distributions to the limited partners who get a share of the remaining realized appreciation based on their ownership percentage. This equity kicker for the general partner is typically in addition to brokerage fees upon acquisition and disposition, plus market rate or higher fees for property management and asset management.

Although some limited partnerships are formed by general partners who treat each partner as an equal, the majority is structured by general partners with the perspective of “Heads: I win! Tails: You lose!” Some limited partnerships are nothing more than a pure profit play for the general partner in which they get their money upfront — often while the limited partners are held captive and can only hope to see the return of their capital and some appreciation in the distant future.