CHAPTER 3

Your Financial Foundation: Master Some Core Principles

You need the same knowledge and tools to make sound investments, regardless of whether they are values-aligned or not. Since our society has not done a great job of educating women about basic investment concepts, investing can be intimidating or overwhelming for a lot of us. Lisa Leff Cooper, an investment expert and contributor to this chapter, has witnessed over and over again how knowledge about a few key investment concepts can go a very long way toward empowering individuals in making wise and informed investment decisions. She has found this to be true for all types of investors, such as recent graduates new to saving and investing, mid-term careerists, newly single women, recipients of new wealth, and women entering retirement.

Even though this book is not intended to teach the basics of personal finance, there are a few important concepts that anyone diving more deeply into their investments needs to understand. This chapter touches on those fundamentals. After reading it, you'll know if you're ready to invest, where you stand financially, and what your investment priorities are. You will also be introduced to the major asset classes as well as the concepts of portfolio diversification and asset allocation. When you complete this chapter, you'll have the foundational elements you need and the beginnings of your own investment strategy.

If you feel confident with your overall investing knowledge, feel free to skip ahead to the next chapter. If you want even more information about the basics after completing this chapter, you will find additional resources on our companion website.

Before You Invest

This book assumes you're ready to invest and already have some of the basics of your financial life in order. You're ready to invest once the following qualifiers are true:

- Your income comfortably covers your ongoing expenses;

- You have manageable debt, which means you can avoid high-interest debt and comfortably afford your monthly debt repayments; and

- You have at least three to six months of readily available (e.g., “liquid”) funds to cover needed expenses in case of an emergency or other unexpected event.

If you're not quite there yet, don't worry or be ashamed. Whether you are young or old, you're not alone. A study by Charles Schwab1 found that only 28% of Americans have a written financial plan. Those who do, however, feel more financially stable and demonstrate better saving and investing behavior.

Saving Is Important, But It's Not Enough

As women, we tend to save. That's what we've been told to do by family, society, and personal finance gurus. The good news is we've listened. The bad news is we're more likely than men to keep our savings in cash, because we're worried about losing our money.2 Unfortunately, keeping the bulk of our money in cash or low-risk/low-return investments is usually not sufficient to achieve our financial goals, particularly over the long term. When we keep our money in cash, inflation outpaces the interest we are being paid. So we're actually losing money year by year. Even more significant is the asset growth that's being left on the table.

Assume you save $500 per month in a bank that's paying you 1% interest per year. Over a 30-year period you will have accumulated $210,000. If that money had been placed in a bond fund that returned 3% per year, you'd have $294,000. But if the money went into investments that returned 6% over the same term, you'd have more than $500,000.3

To build your wealth, you should be putting aside as much money as you can as soon as you can, and you should be investing your money rather than putting it in a savings account. While virtually any form of investing is going to be riskier than just putting your money in a bank, chances are you will not reach your financial goals without it.

How Much Money Do You Have?

It's going to be impossible for you to invest your money wisely if you don't know how much money you have and where it is. You'd be surprised by how few of us actually know where all our money is being held and what it's invested in. So the first thing to do, if you haven't done so already, is to take inventory. If you haven't done this, we'll help you get started in the “Take Action” section at the end of this chapter.

The hardest part of this exercise might be pulling together all the sources of information you have about your money. Once you are done, though, you'll have a way to keep all the information in one place, going forward. You'll also know what you own, what you believe is values-aligned, and how your money is spread, or allocated, across different asset classes.

Where Do You Stand Compared to Other People?

When you calculate how much you have, where it is, and your financial net worth, you might be interested to know how your level of wealth compares to other Americans. Many people do not have a realistic sense of what wealth—or a lack thereof—looks like in this country.

According to data from the Federal Reserve's 2016 Survey of Consumer Finances (SCF), the median net wealth of households in the United States was $97,300.4 Thus, half of Americans had a net wealth below this number and the remainder had a net wealth above it. Table 3.1 highlights how much money the average household needed to be in the top 50 percentile, top 20 percentile, and top 10 percentile by age.

The same SCF study concludes that only 7.6 million, or 6% of, households have $2 million or more, 1.3 million, or 1% of, households have $10 million or more, and a mere 84,000 households in this country have a net wealth of $50 million or more.5 A different study looking at individuals showed that by the end of 2019, 45% of millionaires in the United States were women.6

TABLE 3.1 Wealth Percentiles

| Age | Top 50% | Top 20% | Top 10% |

|---|---|---|---|

| 18–25 | $4,000 | $22,750 | $65,510 |

| 26–30 | $12,000 | $82,500 | $142,710 |

| 31–35 | $30,400 | $144,950 | $259,780 |

| 36–40 | $47,700 | $218,400 | $464,100 |

| 41–45 | $85,600 | $379,000 | $721,800 |

| 46–50 | $131,590 | $546,200 | $1,173,100 |

| 51–55 | $134,920 | $586,470 | $1,224,500 |

| 56–60 | $188,250 | $998,100 | $2,456,300 |

| 61–65 | $209,700 | $1,015,350 | $1,957,700 |

| 66–70 | $218,500 | $852,300 | $1,712,000 |

| 71–75 | $255,900 | $990,500 | $2,118,600 |

| 76–99 | $259,900 | $1,003,800 | $2,079,069 |

This data is important because part of our money beliefs relate to where we think we stand relative to others. Since so much about money is taboo, we don't actually know. So we make up stories about our personal situations. Perhaps you're young and already have a few hundred thousand dollars stashed away in retirement funds and other investments, and you think that everyone else is in the same situation. Or maybe you have a few million dollars, but you don't think you're rich, because you compare yourself to those who are much wealthier than you. Only a small fraction of the population are millionaires, and only the top 1% has $10 million or more.

How Much Will You Need to Retire?

While some Americans are set up to enjoy a comfortable retirement, far too many are woefully unprepared to support themselves in their later years because they aren't planning sufficiently and aren't on track to reach their goals. Social Security can play a role in filling the gap, especially for those at the lower end of the wealth spectrum. However, Social Security alone is often not enough to cover expenses through the retirement years, particularly with growing concerns about the continued availability and sustainability of this government funding.

So how much is enough? Well, that depends. Different people have wildly different points of view. One of the men who kicked off the Financially Independent, Retire Early (FIRE) movement, “retired” in his early 30s with only $800,000.7 He and his family had a low-cost lifestyle and pulled their annual expenses from the dividends and other revenue that their portfolio generated each year. On the other hand, a well-known personal finance pundit initially hated the FIRE movement because, among other things, she thought it left too many unknowns unaccounted for. In her view, you need at least $10 million to retire early.8 Whereas, Schwab 401(k) participants believe they need $1.7 million, on average, to retire.9 So who's right?

There is probably no right answer. How much you need to retire is a very personal decision. It is based on your current age, earning potential, expected return on your assets, age of retirement, expected cost of living at retirement, and a number of other factors. At first glance, it seems difficult to know all of those variables, particularly if you are still young and in the earlier stages of your career. So much can happen between now and the time you retire. How can you possibly know? Fortunately, the power of technology makes it easy to get a reasonable estimate of your long-term financial situation. You simply enter some key data, which you should be able to easily gather, into any one of the retirement calculators that you can find online, and the tool does the rest.

The retirement calculators allow you to play what-if games. By entering different values in the calculator, you can determine the impact that lifestyle changes would have on your long-term goals. For example, if the calculator shows you aren't going to meet your retirement objectives, then you could consider getting a better-paying job, saving more of your assets, taking additional investment risks, reducing your expenses in retirement, or working longer than you had planned. For those close to, or in, retirement, another calculator can determine how long your existing assets will last at your current spending rates.10 You'll find the links to these tools on our companion website.

Your Investment Criteria

As you begin your investment journey, it's helpful to clarify your priorities and tendencies. There are three essential criteria to consider: your personal investment objectives, your time horizon, and your risk tolerance. As you consider these criteria, ask yourself: What do you want to do with your money? How much time do you have? How much risk can you handle?

The way you answer these questions will guide just about every investment decision you make going forward.

What Are Your Investment Objectives?

Investing is highly personal. Each of us has our own goals for deciding how we invest and spend our money.

For example:

- Do you want to put a down payment on a house?

- Are you saving for your children's education?

- Are you planning for a long and secure retirement?

- Does your money need to generate regular cash flow to support you or someone else, now or in the future?

Defining your personal financial goals can be highly challenging! A lot of people simply think, “More is better” when it comes to money, without recognizing there can be significant trade-offs to seeking high levels of growth, particularly in terms of portfolio safety and stability. Others—especially those with newly acquired wealth—approach the goal-setting process by saying, “Well, what can my money do?” without first delving into the question of where they would like to make an impact. While money can provide the means for reaching your goals, it can't provide answers about what those goals are. That's something only you can decide.

How Much Time Do You Have?

Another important criterion to specify is the length of time you're able and willing to invest. This is known as your time horizon. In other words, how long can your money stay invested and grow without your needing to tap into it for funds? This is an important question, because there are big differences between appropriate investment strategies for money you may need in a near-to-intermediate time frame and for money that can stay invested long term.

Finance professionals refer to short-, medium-, and long-term time horizons. Short-term time horizons are up to 3 years, while mid-term horizons are 3 to 10 years, and long-term is considered to be 10 years or more. If you have a short time horizon, you will likely want to minimize the risk of loss and invest conservatively. If your investment horizon is longer, your portfolio will have time to weather shorter-term ups and downs, giving you the opportunity to withstand a higher level of risk, which allows you to earn higher returns over time.

Many investors and investment professionals overlook the importance of time, especially in periods when markets are making dramatic moves. We saw this during the 2008 financial crisis and again with COVID-19 when many people pulled their money in panic, only to watch the market recover. History has demonstrated that market downturns are followed by recovery—and if you have time to weather downturns, staying invested produces the best outcome, typically by a significant amount.

Some investors believe they can choose exactly when to move money in and out of markets, investing when prices are at a bottom and exiting at high points before a crash. This strategy is known as market timing. In practice, it rarely works out well. Most investment professionals urge investors to focus on “time in the market” rather than “timing the market.”

The amount of time we have in the market has particular significance for women, because, on average, we live longer than men and need our money to last longer. We also tend to have fewer years in the workforce (e.g., taking time away to have children), resulting in less time to accumulate wealth. Combined, these factors present an added challenge for women and contribute to the wealth gap that we face relative to men.

What Is Your Risk Tolerance?

All investing involves the risk of loss. Some types of investments are subject to more risk, whereas others are subject to less. There is generally a trade-off between the level of risk associated with an investment and the potential return of that investment. This is known as the “risk-return trade-off.” As an example, speculative small-cap stocks involve a higher level of risk but also the possibility of higher returns. High-quality bonds, on the other hand, tend to offer increased certainty but only low-to-moderate returns.

Your tolerance for risk is determined by a number of personal factors, including your time horizon, your financial capacity to withstand losses, and your emotional response to seeing the value of your portfolio fluctuate or drop. For many investors, the emotional component plays a significant, sometimes oversized, role in investment decision-making. A fear of loss generates strong emotions. We tend to remember our financial losses more than we do our financial gains. Being aware of this emotional bias can help you mitigate your own fears, as will increasing your investment knowledge and experience.

In general, each type of investment tends to have a unique position along a risk-return continuum. Figure 3.1 identifies the relative positions of cash alternatives and some types of fixed income and public equity investments.

FIGURE 3.1 Risk-Return Spectrum

There are special considerations for women around risk. Generally speaking, we can be more conservative investors than men. The problem with this too-conservative approach is that it can lead to low portfolio growth over time, or even a portfolio that struggles to keep up with inflation and taxes. This presents a significant risk of not being able to meet long-term financial goals, such as buying a house, putting children through college, or being prepared for retirement.

Introduction to Asset Classes

Once you have a sense of what you want your money to do and you have insight into your time horizon and risk tolerance, it's time to consider where and how to invest. For better or worse, you have a very wide array of options from which to choose, and investing can get complex. The goal of this section is providing a basis for your choices by introducing you to the major asset classes, each of which will be explained in detail in the next part of the book.

In general, each asset class offers a distinct combination of risk-return characteristics. But this is not a hard-and-fast rule, because there can be variations within a single asset class. What's more, there can be wide fluctuations from one year to the next. Table 3.2 shows the average returns for several asset classes over the 15-year period from 2005 to 2019.11 It also shows the best and worst returns in any one year during that same period. Notice the dramatic shifts that can occur, particularly with emerging markets and high-yield bonds. Also note the relative stability afforded by high-grade bonds.

TABLE 3.2 Asset Class Returns

| Asset Class | Average | Best | Worst |

|---|---|---|---|

| US large cap | 9.00% | 32.4% | –37.0% |

| US small cap | 7.92% | 38.8% | –33.8% |

| International developed | 5.33% | 32.5% | –43.1% |

| Emerging markets | 7.85% | 79.0% | –53.2% |

| Investment-grade bonds | 4.15% | 7.8% | –2.0% |

| High-yield bonds | 7.11% | 57.5% | –26.4% |

| Cash | 1.30% | 4.7% | 0.0% |

Cash

Cash provides immediate liquidity. Your funds are extremely safe, as they are federally insured up to $250,000 in any certified financial institution. However, returns are usually well below the rate of inflation. Thus, over time, funds left in cash decline in value.

Cash Alternatives

Cash alternative investments include money market funds, certificates of deposit (CDs), and some specialized financial products. These investments tend to be relatively safe, and some are even federally insured. They provide less liquidity than cash, tying up your assets for 3–12 months. In turn, they tend to offer a somewhat higher return than you will get from your savings or checking accounts. Cash alternatives can play an important role in a portfolio by providing safety for capital that you will need in the short term, but they should not be expected to provide real growth over time.

Fixed Income

Fixed-income investments include longer-term CDs, promissory notes, bonds, and bond funds. When you invest in fixed income, you're essentially making a loan to a borrower. In return, the borrower vows to pay you back with interest. Most often, their payments are made on a regular schedule. Fixed-income investments usually carry low to modest risk—more than cash but less than public equities. But they also provide more modest returns than stocks. Some types of bonds, however, carry higher risk. This is an example of the diversity and differing risk-return trade-offs that can exist within a single asset class. The most common reason for adding lower-risk fixed income into a portfolio is to provide stability and safety while generating a predictable stream of reliable income.

Public Equities

When you buy stock in a company, you own a portion of the company. That portion is allocated to you in shares and represents your ownership, or equity, in the firm. As the value of the company goes up or down, so does the worth of your shares. Most public equities trade actively throughout the day and offer a high degree of liquidity. You can basically buy and sell these assets whenever you want. However, there can be exceptions, especially in the cases of smaller companies, which may have fewer interested buyers, making these stocks harder to sell and therefore less liquid.

The purpose of including stocks, or public equities, in a portfolio is to deliver growth over the long term. However, stocks can be volatile, with lots of ups and downs in the shorter term. This volatility makes them a riskier asset class than cash or fixed income.

Private Investments

Private debt and private equity are investments in companies that are not traded on the public stock market. The restaurants, shops, and businesses in your neighborhood are prime examples, as are the technology start-ups that we hear so much about in the news. Because these companies are not publicly traded, it's much harder to find buyers and sellers. The difficulty in selling your shares in a privately held company is what makes these assets illiquid.

Private investing can be a lot of fun. What makes investing in this asset class engaging is that you can target your investments directly to the entrepreneurs, start-ups, and other early-stage businesses that excite or inspire you. You can also choose to invest in companies that have high social impact, are located in your community, and/or are run by traditionally underfunded founders, such as women and minorities. You can actually engage with the entrepreneurs directly. Depending on the size of your investment, you could even take an observer or board seat to provide assistance and oversight to the business.

Private investments can offer high returns and compelling targeted opportunities for social impact, but they also often involve considerable risk, because most companies go out of business within their first five years of operation.12 In addition, private companies are not bound by the same disclosure requirements as public companies, so it can be harder to access financials and other key information that an investor needs to assess risk.

Alternative Investments

A number of additional asset classes that investors can use to diversify their portfolios are grouped together under the term “alternatives.” This broad category includes virtually anything that can be traded and that doesn't fall into one of the other asset classes. Currency markets, commodities, real estate, natural resources, and collectables are all examples. Many of these investments require specialized knowledge to achieve a successful outcome and tend to have limited liquidity. As you might expect given the range of options, risk levels and return potentials of alternative investments can vary widely.

A Note on Accredited versus Non-Accredited Investor Status

In the US, investors are separated into different categories based on their annual income and net worth. Individuals can be non-accredited, accredited, or qualified investors. These designations are set by the US Securities and Exchange Commission (SEC) to protect smaller investors from putting their money into high-risk ventures, such as private and alternative investments. The SEC traditionally believed that only financially sophisticated investors had the knowledge and financial resources to invest in these riskier financial products. This changed, to some degree, with the passage of the 2012 JOBS Act, which opened private and alternative investing to everyone. However, there are limits on how much a non-accredited person can invest in these opportunities.

Designing Your Portfolio

Now that you have a basic understanding of your own financial situation and the different asset classes open to you, let's look at how you can put them together into a portfolio that is designed to fit your specific goals, time horizon, risk tolerance, and investor class.

Don't Put All Your Eggs in One Basket

One of the first things to understand is the importance of diversifying your portfolio, which means dividing your money across different investments and asset classes. Diversification is one of the most powerful concepts in investing. It can help you build a portfolio that's more resilient to market downturns. While diversification does not eliminate the risk of losing money, it does reduce the risk by spreading funds across different asset classes that behave differently under certain market conditions. Diversification, however, can also reduce the overall return of the portfolio. The goal is to introduce enough diversification to reduce risk without adding so much that you undermine your investment returns. There are opportunities for diversification across different asset classes as well as within a particular asset class.

Diversification is essentially adding an uncorrelated asset to a portfolio. This is basically an asset that behaves differently from the rest of your portfolio. When you add an asset with a lower correlation to your current portfolio, the asset has the potential to increase the portfolio's expected return and simultaneously decrease its overall risk.

For example, large-cap and small-cap stocks are closely correlated. Their values tend to move in the same direction under similar market conditions. When the US economy is healthy and employment levels are high, these assets do well. But when economic growth is lagging, they tend to suffer. Under these conditions, the government may lower interest rates to stimulate renewed growth. When interest rates go down, the value of bonds goes up. Thus, in an economic downturn, the value of stocks and bonds moves in opposite directions. By holding stocks and bonds, you alter the level of correlation in your portfolio, thereby reducing your overall risk. Including other asset classes, such as private investments and alternatives, can decrease the level of correlation even more and further diversify your portfolio.

Professional investment managers use diversification as they seek to deliver the highest level of return relative to risk. A typical professionally managed portfolio will contain a mix of some, if not all, of the asset classes outlined here. These managers can also bring additional diversification into a portfolio through a single asset class. For example, investments in public equities could be segmented by company size, geographic location, and business sector. Other asset classes have similar diversification potential.

Individually managed portfolios often lack an appropriate level of diversification. Most often portfolios are not diversified enough. Having too much of your money in a single investment or asset class can have a negative, potentially disastrous, impact on your entire portfolio if something goes wrong with the few investments you hold. You can also over-diversify a portfolio. Investing too broadly across a wide range of investments can reduce the return of your overall portfolio. The goal is to find a balance between risk and return.

Diversification is used to mitigate risk in most economic conditions, but it's not a silver bullet. Even a well-diversified portfolio cannot protect us in all circumstances. In certain economic situations, asset classes that normally react differently to market conditions can unexpectedly all move in sync. This was the case in 2008, when many asset classes were affected by the mortgage crisis.

Include Asset Allocation

Asset allocation is a strategy for portfolio management that splits assets among broad categories of investments, such as cash, fixed income, public equities, and alternatives.

You decide which asset classes you want to hold and how much money you will invest in each. When you allocate your money, you are literally determining the percentage of your total assets you want in cash, fixed income, public equities, and so on.

Establishing asset allocations lies at the heart of designing your portfolio. Your goal is to choose a mix of asset types, which, over the long term, will deliver a high probability of meeting your financial goals while exposing you to a manageable level of risk. Ideally, your asset allocation should seek to tap the power of diversification so your assets are distributed across relatively uncorrelated asset categories.

Asset allocation typically involves setting a target allocation for each asset class, along with tolerance bands that specify the minimum and maximum amounts you want in each asset class. This allows for fluctuations that are likely to take place in your portfolio over time.

Asset Allocation Examples

To help illustrate, let's revisit some of the sample investors you met in Chapter 2 and see how asset allocations play out for them. These allocations are based on each woman's investment priorities, time horizon, and risk tolerance.

JADE: A FIRED-UP IDEALIST Jade and her husband are saving for a down-payment on a two- to three-unit building that will include their housing and provide an additional income stream. They are more than halfway to their goal and expect to have the full downpayment in three to four years. Jade and Denzel are non-accredited investors; however, they enjoy making investment decisions together and want to allocate some of their assets to public and private companies that align with their environmental values.

As you can see in Table 3.3, their current asset allocation is extremely conservative because of their immediate savings goal. However, it also takes into account their interest in investing a bit of their money in the public and private equities markets. After Jade and her husband buy their property, their financial priority will shift to investing for an early retirement, and their asset allocations will become more aggressive, reflecting their young age, upward career potential, long time horizon, and comfort with risk.

TABLE 3.3 Extremely Conservative Asset Allocation

| Asset Class | Target | Minimum | Maximum |

|---|---|---|---|

| Cash / cash alternatives | 75% | 50% | 100% |

| Fixed income | 10% | 5% | 50% |

| Public equities | 13% | 0% | 85% |

| Private investments | 2% | 0% | 10% |

| Alternatives | 0% | 0% | 10% |

TONI: A RETIRED SAVER Toni is retired and lives with her husband and disabled daughter, Nina. Although neither she nor her husband had high-paying jobs, they lived simply and saved their money from an early age. They rarely touched their assets and let them grow over time. As a result, they are now accredited investors and have enough money to meet their monthly needs without having to touch their principal. Their primary goal is to safeguard the funds they have for the remainder of their retirement and to have enough left over to ensure Nina's safety and happiness after they die.

Toni and her husband's risk tolerance is low, and their asset allocations are conservative. They are worried, however, that this strategy may not provide sufficient capital for Nina's life expectancy. As a result, they are reconsidering the allocations shown in Table 3.4.

TABLE 3.4 Conservative Asset Allocation

| Asset Class | Target | Minimum | Maximum |

|---|---|---|---|

| Cash / cash alternatives | 5% | 2% | 20% |

| Fixed income | 60% | 40% | 70% |

| Public equities | 35% | 25% | 45% |

| Private investments | 0% | 0% | 0% |

| Alternatives | 0% | 0% | 0% |

AVA: A CARETAKER AND “RETURNER” Ava is a recently divorced mother of two, who is reentering the workforce. While married, her husband managed their assets and was invested primarily in the stock market. She decided to hire a financial advisor, who is now working with Ava to diversify her portfolio. Ava needs some of her money to supplement her income until she finds a job. She also wants some portfolio growth to ensure she can have a comfortable retirement, even if it has to be delayed slightly.

Ava's advisor is moving her toward a moderate asset allocation, highlighted in Table 3.5. Given her lack of familiarity with investing, Ava's risk tolerance and time horizon are medium.

TABLE 3.5 Moderate Asset Allocation

| Asset Class | Target | Minimum | Maximum |

|---|---|---|---|

| Cash / cash alternatives | 5% | 2% | 20% |

| Fixed income | 30% | 5% | 40% |

| Public equities | 55% | 50% | 70% |

| Private investments | 0% | 0% | 5% |

| Alternatives | 5% | 0% | 10% |

ANIKA: A YOUNG GUARDIAN Anika is under 30 and hypervigilant with her money. Her primary goal is a comfortable retirement, for which she has a long time horizon (30+ years). When she started saving, Anika was reluctant to invest. However, a mentor has been helping her understand investing, which is building her confidence. As a result, her risk tolerance is higher than it used to be, because she now understands the benefits of a long time horizon and compounding. With her mentor, Anika developed an investment strategy and plan. This has helped her relax a bit around money.

Anika's asset allocation, depicted in Table 3.6, is moderately aggressive, given her young age, long time horizon, and remaining level of discomfort with risk.

TABLE 3.6 Moderately Aggressive Asset Allocation

| Asset Class | Target | Minimum | Maximum |

|---|---|---|---|

| Cash / cash alternatives | 5% | 2% | 20% |

| Fixed income | 20% | 5% | 25% |

| Public equities | 75% | 60% | 85% |

| Private investments | 0% | 0% | 5% |

| Alternatives | 0% | 0% | 5% |

MARIA: AN EMPIRE BUILDER The start-up business Maria co-founded was recently acquired, making her a multimillionaire. As a result, Maria's investment goals of financing her daughters' college educations and having a comfortable retirement are already covered. She realizes that she has enough wealth now to do more. Maria is grateful for her good fortune and wants to use her wealth to create deep impact. She is an accredited investor and a qualified purchaser.

Maria's asset allocation is aggressive, thanks to her overall level of wealth, high-risk tolerance, and minimal needs for income and liquidity. As you can see in Table 3.7, Maria is in a good position to invest in private and alternative investments.

TABLE 3.7 Aggressive Asset Allocation

| Asset Class | Target | Minimum | Maximum |

|---|---|---|---|

| Cash / cash alternatives | 3% | 2% | 10% |

| Fixed income | 17% | 5% | 25% |

| Public equities | 30% | 25% | 60% |

| Private investments | 20% | 10% | 25% |

| Alternatives | 35% | 10% | 40% |

While these examples are designed to be instructive, your specific situation is likely to be different. There's no exact formula for determining an appropriate asset allocation, as each case depends on your investment objectives, time horizon, and risk tolerance. It's also important to realize your asset allocation is likely to change over time, as your life situation, goals, and time horizon shift. It may also change as you become more confident with your investing. A financial advisor may add a great deal of perspective and value to this process.

Make Time to Rebalance Your Portfolio

Once you've established your asset allocation targets and built a portfolio to meet them, you'll need to monitor and make adjustments to keep your allocations in line. This is an important part of managing your investments. Even in relatively calm times, market movements are likely to create shifts in your portfolio's asset allocations over time. For example, if you—like Anika—set your allocation to public equities at a targeted 75% and the stock market then enjoys a particularly strong period of relative returns, the percentage of your portfolio allocated to public equities will rise to some level higher than 75%. This can expose your portfolio to unintended risk. When this happens, a prudent strategy is to rebalance your investments back to the targeted allocations.

While there are no hard-and-fast rules around when to rebalance, many investors and financial advisors do so either quarterly or annually. Some investors have a policy of rebalancing when there's a big swing in the markets, so a move in any single asset class—say, up or down 10%—serves as a trigger to rebalance. Many advisors suggest investors rebalance at least once a year to keep their portfolios appropriately allocated. If you have a financial advisor, you may want to confirm they are performing this service for you on a routine basis.

Tracking How Your Investments Perform

It's important for investors to be able to monitor their returns over time. Seeing whether your portfolio value has gone up or down is simple, but evaluating how your individual investments and overall portfolio have performed—compared with how they could, or should, have performed—is a more complicated exercise. In addition, not all investments are equal when it comes to assessing performance.

Measuring investment returns for cash, cash alternatives, and private debt is relatively easy, because you receive regular dividends or interest payments. It's also relatively easy to calculate the total return on individual fixed income and public equities investments. This information is freely available online at any number of financial sites. When you get into private equity and some of the other alternatives, however, measuring return can be considerably more difficult because information is harder to find, track, and assess.

Challenges also exist at the overall portfolio level, where accurately measuring a portfolio's growth rate typically involves sophisticated calculations that take trades, cash flows, and other transactions that occurred in the portfolio into consideration. Providing meaningful reporting on investment performance is a valuable service investment advisors can provide.

To assess performance on a specific investment, it's critical to make sure you're looking at how your investment behaved relative to investments with similar characteristics over the same period of time. To do this, you'll use benchmarks, which are designed to reflect specific segments of the market. The S&P 500 is one of the best-known benchmarks for US public equities. You'll find more information about benchmarks and how to use them in Chapter 7.

Online Tools Make Investment Analysis Easy

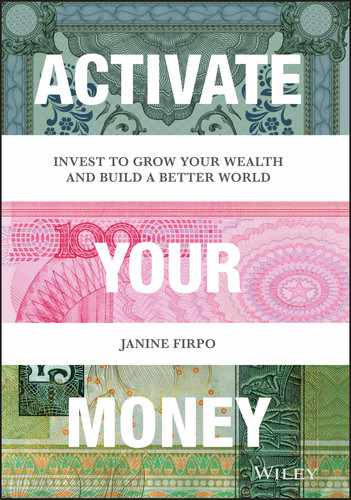

If you want to better understand your public holdings, their performance, or how they compare to other investments, there are some wonderful online financial reporting tools, such as Google Finance and Morningstar. These free sites can provide a wealth of information about your investments, as the snapshot in Figure 3.2 shows.

FIGURE 3.2 Morningstar Snapshot

The Voya Russell Large Cap Growth fund is a values-aligned index fund. Its stock symbol, also known as the ticker, is IRLSX. The ticker is an easy way to identify a fund. When you search for IRLSX on Morningstar, you are rewarded with this summary screen. This snapshot from October 5, 2020, shows you that a total of $1.4 billion was invested in the fund. You can see that investors pay 0.68% per year to own the fund (expense ratio) and that this fee is considered below average (fee level). You can also tell that this is a US large-cap growth fund, which means it holds primarily large companies with growth potential. There is no minimum initial investment to buy into this fund, and it's available, or open, for purchase (status). By looking at the turnover, you can see 19% of the total holdings in the fund are sold, or turned over, on an annual basis. And you can tell that this fund received a 4-star rating from Morningstar.

And you learned all that just by looking at a single screen. If you go through the tabs immediately above this data to “Fund Analysis,” “Performance,” “Risk,” and so on, you can find even more information about this fund. The “Performance” tab allows you to track the return on this investment over 1-, 3-, 5-, 10-, and even 15-year time horizons and provides information about the benchmark used with the fund. The “Portfolio” tab lists the companies held by the fund and shows Morningstar's sustainability ratings. If you try researching a few of your public equities holdings this way, you might be surprised by what you learn.

Your Investment Policy Statement

An investment policy statement (IPS) is a document that helps you put all the information you learned in this chapter together in one place. Your IPS will help guide your investment decision-making over time. This document, which can be as simple or as complex as you want, defines your investment goals, asset allocation targets, rebalancing objectives, and other key information.

Institutional investors, such as large foundations or university endowments, often have elaborate and detailed IPSs. Your IPS doesn't need to be fancy or lengthy. It just needs to address the critical elements that are most important to you and your financial advisor, if you have one. Some advisors use an IPS, or something like it, when they're establishing their relationship with new clients. An IPS is a living document, designed to be updated and revised as your lifestyle and goals change over time.

Take Action

The following actions are the foundational elements that you should consider developing if you want to take control of your financial future.

- Determine what you have

Download the “What You Have Workbook” from our companion website. This Excel tool will provide you with full instructions and help you place your current holdings in appropriate asset classes. Once completed, the “What You Have Workbook” will show how much money you have invested in each asset class, along with the total monetary value of all your holdings. It will also automatically calculate your asset allocations, or the percentage of your total assets that are held in each asset class.

You can use the same workbook to enter your liabilities. The “Your Net Worth” tab will automatically calculate your net wealth.

- Determine how much you need to retire

Use the retirement tools referenced on our companion website to get a better understanding of your current retirement situation and your retirement options. Play around with the calculators to see what happens under differing scenarios, such as retiring later, increasing your current income, and saving more now.

- Determine your asset allocations

You have already reviewed the asset allocations for Toni, Jade, Ava, Anika, and Maria. If you want to know more or you don't feel those personas represented your situation, check our companion website. There you'll find references to more portfolios that you can study.

- Track your investments' performance

If you have not done so already, delve into the details and performance history of some of your public equity and fixed income holdings using the Morningstar website or any other online platform.

- Create your IPS

Building your own IPS is a helpful and important part of your investment journey. If you're currently working with a financial advisor or investment manager, you may already have a personalized IPS. Take it out and review it. Do you understand it? Does it still reflect your current situation and goals? If things have changed, it might be time to consider this document anew.

If you don't have an IPS yet, download the “IPS Template” and example from our website and work to develop your own document. Don't worry if you cannot fill everything out right now. As you get more comfortable with investing, it will become easier. This is also a great document to share with family, friends, and others with whom you discuss your financial situation. Once developed, you may want to revisit it on an annual basis to ensure it still reflects your goals.

Endnotes

- 1 https://content.schwab.com/web/retail/public/about-schwab/Charles-Schwab-2019-Modern-Wealth-Survey-findings-0519-9JBP.pdf.

- 2 https://www.ellevest.com/magazine/newsletter/2019-01-23.

- 3 These sums were obtained using a MoneyChimp calculator and assumed interest was compounded monthly. http://www.moneychimp.com/calculator/compound_interest_calculator.htm.

- 4 https://www.federalreserve.gov/econres/scfindex.htm.

- 5 https://dqydj.com/how-many-millionaires-decamillionaires-america/.

- 6 https://thequantum.com/financial-facts-for-womens-history-month/.

- 7 https://www.mrmoneymustache.com/2011/09/15/a-brief-history-of-the-stash-how-we-saved-from-zero-to-retirement-in-ten-years/.

- 8 https://affordanything.com/153-hate-fire-movement-suze-orman/.

- 9 https://www.aboutschwab.com/schwab-401k-participant-study-2019.

- 10 https://www.nerdwallet.com/blog/investing/how-long-will-your-retirement-savings-last/.

- 11 https://novelinvestor.com/asset-class-returns.

- 12 https://www.fundera.com/blog/what-percentage-of-small-businesses-fail.