18

KNOWING WHEN TO SELL AND HOW TO SELL

The longer you hold a house that is appreciating and producing cash flow, the more money it will make you. However, there are reasons and a time to sell your investments.

BEFORE YOU SELL, ANSWER THESE QUESTIONS

1. What is your market doing today? Are properties selling quickly? Is the inventory down and are prices moving up? If so it’s an opportunity to sell your weaker properties.

If prices are declining, ask why. Is it because of a significant event that will affect your housing market long term, like a large business or military base closing causing a drop in population? Or is the downturn due to overbuilding, or a change in the credit market?

If you think it will be many years before prices come back, selling today and buying back in at cheaper prices may be a good decision. But kicking out good tenants, and giving up the income, is giving up a lot. Before you sell, know your after-tax net. If your houses are in good shape and have long-term tenants, holding through a recession is often a better strategy than trying to sell at the top and buy back at the bottom.

2. What is happening on the streets where you own property? Properties on different streets within a neighborhood, are constantly changing. Study each street where you own and determine whether holding for five more years is a good plan. Neighborhoods improve and property values increase when landlords or banks sell to owners who then fix up houses. Neighborhoods decline and property values drop when landlords or banks let properties deteriorate.

3. Does your house have a long-term tenant in residence or a record of attracting long-term tenants? If so, it is cranking out cash flow for you.

In the long run, your profits from cash flow will often be greater than your profits from appreciation. Rents go up with inflation, just like prices. As my house prices have climbed from $50,000 to $200,000, my rents have increased from $400 to $1,600 on those same houses. The big difference is that I get the rent every month but have to wait until I sell for the appreciation. Said another way, the profits from the rents that I receive today are much more valuable to me than the profit I will receive ten years from now.

4. Can you refinance today on good terms? I like owning property free and clear but am also a big fan of monthly cash flow. If I can refinance a loan and increase my cash flow, I do. If you increase your cash flow when you refinance, you reduce your risk from having debt. Debt is risky when you cannot repay it.

Refinancing is a great strategy when you can pay off one or more loans with high payments with one new low-payment loan. I refinanced one house with a new low-interest-rate, thirty-year loan and paid off three older loans with high payments. My one, new loan payment was less per month than my previous payment. Plus, I ended up with two free-and-clear houses.

5. Is your house in rentable shape and does it operate with reasonable maintenance costs? Most foreclosures and short sales I look at are not in good enough shape to attract a decent tenant. Some landlords are renting houses without getting them into good condition, but I’ve found that when you advertise a nasty-looking house for rent, the tenants you attract look a lot like the house.

6. Is your rental market strong? When we have tenants competing for houses, it is a good time to rent, not sell, your houses. Rents go up in spurts. Remember, you will often make more from the rents than appreciation.

7. Is the house located close to where you live or work? At one time I owned property in ten states, and that was an education. I learned that I made more money and spent less time traveling when my properties were in my town. Over the years, I have disposed of everything out of state and now will not buy a house unless it’s within a ten-minute drive of my office.

Unless you live where no one makes money investing in real estate, learn to invest where you live, or move to where it is easier. My favorite Jim Rohn quote is, “Don’t wish it was easier, wish you were better.”

It is not as easy if you live in a higher-priced market, but if you get better, you will make a lot more money than an investor who lives in a low-priced market. Many of my most successful students started with little money in very expensive markets, such as Orange County, California. Today they own houses worth many times what my houses are worth, and, predictably, their cash flow is higher than mine. It takes far fewer houses to make you rich in an expensive market.

8. Are there some houses that you own today that you want to keep forever? If not, do you want to acquire one or more properties that you will own for the rest of your life?

What qualifies a house as one that you want to “keep forever”?

Houses that attract long-term, low-maintenance tenants.

Houses that are well built and have lower-than-average maintenance costs.

Houses with taxes and insurance that are in line with the rents.

Houses with a low-interest, long-term loan or are free and clear, that will produce cash flow even at reduced rents.

Houses that are located in neighborhoods that are improving.

GOOD REASONS TO SELL A HOUSE

Houses grow old, neighborhoods change, and landlords get tired. Here are some good reasons to sell a house:

1. Neighborhood changing for the worse. Neighborhoods have cycles. When owners sell out and landlords buy many houses in a neighborhood, property values often will drop. Sell when you see this happening.

2. Worn-out house. It costs a lot of money and takes a lot of time to fix up a house that needs a new kitchen, baths, plumbing, roof, and so on. Most improvements you make only increase the value of a house by a fraction of what you spend. An investment in a new kitchen, one of the best things you can do, will increase the value of the house only by about 75 percent of what you spend. It is smarter to buy another house in good repair and sell your worn-out house to a buyer looking for a project. There are a lot of buyers in that category.

3. Worn-out landlord. Some landlords enjoy their work into their eighties. It is one job that you can keep for life if you want it. A skilled landlord with twenty properties may work only an hour or two a month. You can delegate all the bad jobs and keep the ones that you like. Should you reach the point where you are not having any fun, consider selling to a family member whom you can teach the business or to another, younger investor. See more details below.

4. The house is far away. I obviously prefer to invest in my own back yard. If you own a property in a faraway town, you have to weigh the benefits or cost of holding it until the market improves against selling it now. If you have a loss, you may consider selling it for a loss that could offset the profit you could make from selling another property for a gain.

5. The house loses money. Whenever I find myself with a losing property, I am aggressive about selling it. I’d rather take a loss today and be free to pursue another opportunity than try to squeeze a few more dollars out of a losing investment. It may be a loser because of bad financing, or bad construction, or bad neighbors. Unless I can fix it quickly and at a cost that makes sense, I sell and buy another, better property.

SELLING FOR THE WRONG REASONS

It can be a mistake to sell. Once you have bought a property that makes you money every month, don’t sell it unless it is part of your plan.

1. You have an empty house. If it has attracted good tenants in the past, don’t sell, hold it. If it does not attract well-behaved, long-term tenants, then selling an empty house is better than selling one with a tenant in it. Tenants are not an asset when you sell, because it is not in their best interest. They may have to move. Because of this, they may not cooperate in showing the house, and it may not look its best. Most buyers will not want to move in.

2. No leverage. I have had financial advisors tell me that owning free-and-clear properties is a terrible idea, and they are right, to a point. They say the rate of return is low. What they do not consider is that if you own ten houses, you can own five of them free and clear and five with loans, and increase your rate of return with the leverage.

Once you have enough property to produce all the cash flow you need, your focus should be to pay off your debt, not borrow more. It is easier to borrow money than to pay it back. If your strategy is to refinance, do it when rates are low.

3. No depreciation.* If you own a house long enough, you will run out of depreciation. If the house is in a great neighborhood and making you money, keep it. Would you sell a stock that goes up every year and pays a big dividend? No, you wouldn’t, and stocks have no depreciation. If you want more depreciation, buy more property; don’t sell off your winners.

4. Someone wants to buy your house. Someone always will want to buy your best properties. If you are going to sell one, sell your weakest property. When you begin to acquire properties, keep a list with your favorite property at the top and your least favorite at the bottom. If you are married, share this with your spouse, and tell your spouse that if he or she ever needs to sell, sell the ones on the bottom of the list first.

HOW TO SELL

You can use an agent to sell your property or you can sell it yourself. If you have no experience selling, the agent may do a better job. If you learn how to sell property yourself, then you may be able to get as high a price as the agent and save the commission.

My favorite way to sell is using lease/options, as described in Chapter 15. Selling on lease/options allows me to sell to a homeowner who is struggling to buy a house, often their first house, and yet sell at a retail price. I sell the house in “as is” condition and have the buyer pay the closing cost. This increases my net profit by at least 10 percent.

A student of mine who had accumulated many houses, systematically sold his houses one at a time to young investors. He gave these investors a chance to make a profit off their first house while selling at a good price without any advertising or expense. If they did not exercise their option and close, he still owned the house. He could then renegotiate at a higher price and rent or sell to another.

SELL TO AN OWNER OCCUPANT WITH SELLER FINANCING

Owner financing, where your buyer pays you a down payment and then pays you monthly payments until he pays for the house, is similar to selling with a lease/option with a few important differences. When you sell a house using owner financing, regardless of the paperwork that you use, you have a sale for tax purposes.

That sale can be treated as an installment sale, if you qualify. An installment sale allows you to report your profit as you receive it, not all in the first year of the sale.

It is important to note that “dealer property” cannot be sold using an installment sale. Dealer property is inventory. For a builder, it’s a house he is building to sell. For a “flipper,” it is a house he has fixed up and is selling. If you are a builder or flipper, any sale of your inventory does not qualify. This is an important point.

You must elect to take an installment sale and file IRS Form 6252. Check with your accountant for details. See IRS Publication 537 for a complete explanation.

An advantage to the buyer is lower closing costs and a lower down payment than a bank would require. The seller needs to be able to judge whether the buyer has the income to make the payments. The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 H.R. 4173 has regulations that apply to those who sell more than one house a year to a homeowner with owner financing. It does not apply to sales to investors. You can sell several houses with owner financing in one year to investors. You can sell multiple houses a year to owner occupants, but you must comply with the provisions of this law.

Should the buyer stop making payments, be aware of the cost to get the buyer out of the house and out of title. This may require a foreclosure. Foreclosing, like evicting, should be used only as a last resort. It is nearly always cheaper and faster to negotiate with a buyer who can no longer make his payments and to buy out his interest rather than pay an attorney to have him evicted or foreclosed. If you do this, have an attorney or title company prepare the documents.

SELLING AND REINVESTING WITHOUT PAYING A TAX ON YOUR GAIN

If you are going to sell and then invest in other investment real estate, you can defer paying any tax until you sell by making an IRC Section 1031 tax-deferred exchange. Note that the new property must be held for investment. It does not have to be the same type of investment property. You could sell a house and buy a duplex or commercial property or even land that you planned to hold as an investment. The replacement property cannot be your personal residence or a vacation home.

If you do an exchange with a related party, certain rules apply. Related parties include, but are not limited to, immediate family members, such as brothers, sisters, spouses, ancestors, and lineal descendants. Related parties do not include stepparents, uncles, aunts, in-laws, cousins, nephews, nieces, and ex-spouses.

Corporations, limited-liability companies, or partnerships in which more than 50 percent of the stock, membership interests, or partnership interests, or more than 50 percent of the capital interests or profit interests is owned by the taxpayer is also considered to be a related party.

Related parties who concurrently exchange properties with each other must hold the properties for two years following the 1031 exchange. Both related parties will recognize their respective depreciation recapture and capital gain income tax liabilities if either party disposes of its respective property within two years after the simultaneous 1031 exchange or transfer.

If you plan to use IRC Section 1031 to defer your tax, have the next property that you want to buy identified before you sell. Section 1031 currently requires you to identify your replacement property within fortyfive days from your first closing and then close on it in 180 days. No extensions are allowed. The first forty-five days goes by quickly, so knowing what you want to buy and even having it under contract will improve your chances of completing the exchange.

Get good legal and tax counsel before you sign a contract to ensure that your paperwork and strategy comply with the IRS requirements.

If you sell you will owe recapture tax on the depreciation you have taken, which is 25 percent of the amount of depreciation you claimed. This is called depreciation recapture. Check with your CPA. You can avoid the recapture tax by successfully completing a Section 1031 exchange.

If you have properties with large gains, most of your profit is due to appreciation, so the amount of depreciation you have to recapture will be less significant. If you buy a house for $100,000 and hold it until you sell it for $300,000, you will only have depreciation to recapture on the part of the $100,000 that you have depreciated.

In addition to not paying taxes, an exchange forces you to reinvest your profits into another property. Keeping your investment capital invested continuously makes a huge difference in your net worth in the long run.

ACCEPT A SMALLER HOUSE AS A DOWN PAYMENT

If the house you are trying to sell is a “move up” home, then it is likely that the buyers will already be owners of a smaller house. An excellent way to make a deal is to accept their existing house as a down payment on the house you are trying to sell.

If the buyers like your house, they need to sell their house before they can buy yours. Car dealers discovered the solution to the same problem years ago. You don’t have to sell your old car before you buy a new one, it is easy; they will take your old car on a trade. Do they make money on your old car? Sure.

You can make money taking a house on a trade. Remember, the seller is thinking that they will have to pay a commission and perhaps reduce their price to get their house sold. If you simply accept it as a down payment, they can avoid the trauma of having people walk through their house making disparaging remarks before receiving a low-ball offer.

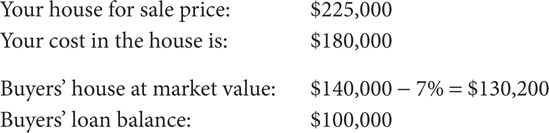

If you sell your more expensive house at a retail price and accept the buyers’ house as a down payment, you will make a profit.

You accept their $30,200 equity as a down payment on your $225,000 house.

They get a new loan for $194,800 ($225,000 less their $30,200 equity).

You get their house subject to their loan and $194,800 in cash at the closing.

If you have a loan on your house, you will pay it with part of the cash you receive.

If they have a loan on their property, you can assume it or take title subject to the loan.

If the house is not one that you want to keep, consider selling it on a one-year lease/option. A good strategy is to take title subject to, because you will have a plan to pay off their loan in a short time (one year or less).

If you are contacted by the seller’s lender, you can explain that the house is under contract and the new buyers are working on securing financing. It is exactly what a lease/option buyer should be doing. They may have a year to close, but they should not wait to qualify for a loan. Set up a meeting with a lender before you agree to sell to them to see what they need to do to qualify for a loan. Unless they have a good chance of getting a new loan, don’t sell to them on a lease/option.

KNOW HOW MUCH YOU WILL OWE IN TAXES BEFORE YOU SELL

Learn about the taxes you will owe as a result of owning and selling real estate before the sale is complete. For more practical information on how to avoid or minimize taxes, read John T. Reed’s excellent book Aggressive Tax Avoidance for Real Estate Investors (www.johntreed.com). It is a clear explanation of tax-deferred exchanges and installment sales and is a must-read for real estate investors.

*Depreciation is an income tax deduction that allows a taxpayer to recover the cost or other basis of a house held for investment. It is an annual deduction a landlord can use to offset rental income on his or her tax return. See IRS form 4562 with the instructions for a complete explanation.