| CHAPTER 5 |

Theoretical Evaluation

In an arbitrage-free market, where no arbitrage profit is available, the expected value for a contract at maturity (its average value at maturity) must be equal to its forward price.

1. The following diagram represents the price distribution and associated probabilities for an underlying contract three months from now.

a. If there is no arbitrage opportunity, what should be the three-month forward price for the underlying contract?

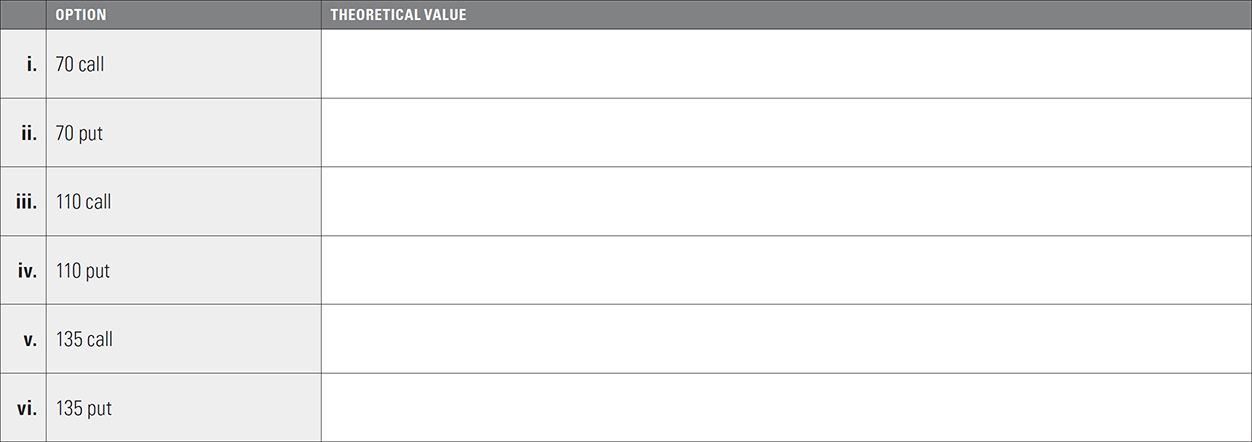

b. What are the expected values for the following options?

c. Can you identify a relationship between the expected value of a call and put with the same exercise price?

d. The theoretical value of an option is the present value of its expected value at expiration.

If all options are European and subject to stock-type settlement, there are three months to expiration, and annual interest rates are 6.00%, to the nearest .01 what is the theoretical value of each option?

e. Suppose the underlying contract is a stock that is expected to pay a dividend of .75 over the next three months. Ignoring interest on dividends, to the nearest .01 what should be the current price of the stock?

2. The following diagram represents the probability and price distribution for an underlying stock six months from now.

a. If the stock is currently trading at a price of 72.50, annual interest rates are 8%, and the stock pays no dividend, to the nearest .01 what is the stock’s six-month forward price, F?

b. Suppose we assign a value of 5.00 to each interval, I. What are the stock prices, F – 2I through F + 2I, on the above probability distribution?

c. Using these price intervals, what is the expected value for the underlying stock?

d. Given the forward price and expected value for the underlying stock, what strategy might you pursue?

e. If all options are European and subject to stock-type settlement, there are six months to expiration, and annual interest rates are 8.00%, to the nearest .01 what is the expected value and theoretical value of each option?

3. In question 1c the following relationship seemed to be true:

call expected value – put expected value = forward price – exercise price

a. Using the values in question 2, does this relationship still hold true? If not, is there an alternative relationship?

b. What annual interest rate will result in the six-month forward price for the stock being equal to the stock’s expected value?

c. Suppose we increase the value of I in question 2 to 10.00. What are the new underlying prices, F – 2I through F + 2I, on the above probability distribution?

d. What is the expected value for the underlying contract?

e. If all options are European and subject to stock-type settlement, there are six months to expiration, and annual interest rates are 8.00%, to the nearest .01 what is the expected value and theoretical value of each option?

f. Now what is the relationship between the expected value of a call and put at the same exercise price?