| CHAPTER 14 |

The Black-Scholes Model

For the questions in this section, you will probably need to use a computer spreadsheet.

For the formulas in this section, if:

S = the spot price or underlying price

X = the exercise price

t = the time to expiration in years

r = the annual interest rate

σ = the annualized volatility

ex = exp(x) = the exponential function

ln = the natural logarithm

n(x) = the standard normal distribution function

N(x) = the cumulative normal distribution function

(The standard normal distribution and cumulative normal distribution functions are commonly included in most spreadsheets.)

then the value of a European call, C, and a European put, P, are given by

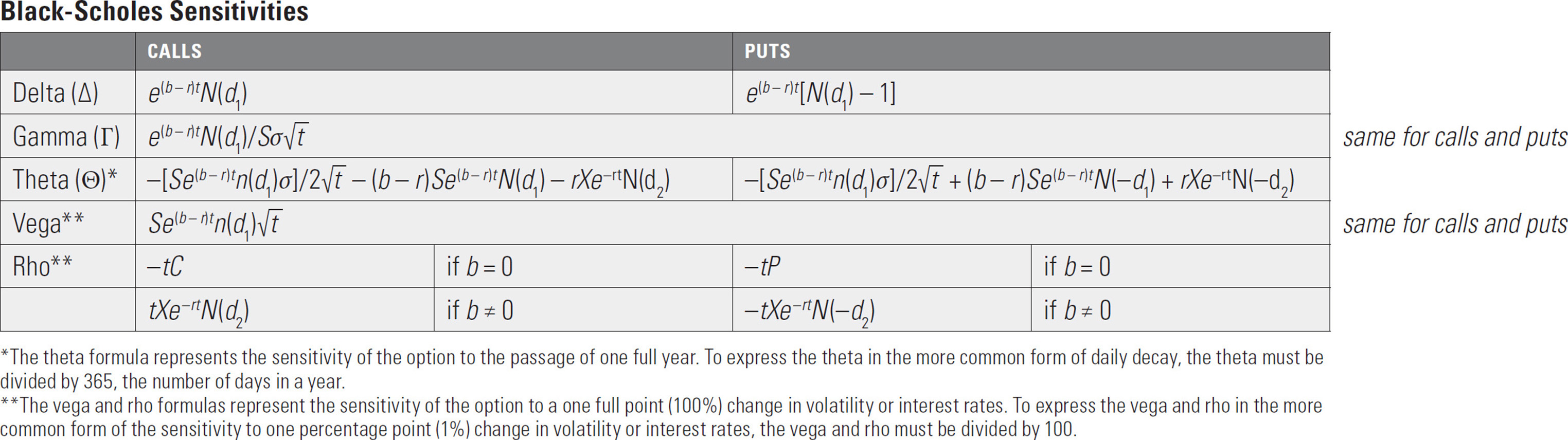

The common variations on the original Black-Scholes model are determined by the value of b.

1. stock price (S) = 71.60

exercise price (X) = 75

time to expiration (t) = 86 days

interest rate (r) = 5.45%

volatility (σ) = 29.30%

dividend = 0

a. Using the above inputs, calculate, step-by-step, the Black-Scholes theoretical value and delta for a stock option call.

S/X

ln(S/X)

t (in years)

![]()

σ![]()

rt

e–rt

d1

d2

N(d1)

N(d2)

call value

call delta

b. What is the probability the 75 call will finish in-the-money?

2. futures price (S) = 1,200

exercise price (X) = 1,200

time to expiration (t) = 149 days

interest rate (r) = 3.60%

volatility (σ) = 18.85%

a. Using the above inputs, calculate, step-by-step, the theoretical value, delta, gamma, theta (per day), vega (per one percentage point), and rho (per one percentage point) for a futures option put that is subject to stock-type settlement.

F/X

ln(F/X)

t (in years)

![]()

σ![]()

rt

e–rt

d1

d2

N(d1)

N(d2)

N(–d1)

N(–d2)

n(d1)

put value

put delta

put gamma

put theta

put vega

put rho

b. The “40% rule” states that the expected value of an option whose exercise price is exactly equal to the forward price of the underlying contract (the option is “at-the-forward”) is approximately equal to 40% of a one standard deviation price change at expiration. The theoretical value is the present value of the expected value.

Using the “40% rule,” what is your estimated value for the 1200 put? How does this compare to your calculated value in question 2a?