| CHAPTER 15 |

Binomial Pricing

At any point along a binomial tree the price of underlying contract, i, can move up to Su or down to Sd. In a risk-neutral market the average price of Su and Sd must be equal to the forward price. For a non–dividend paying stock, the probability of an up move, p, must be:

[(1 + rt) – d] / (u – d)

and the probability of a down move must be:

1 – p

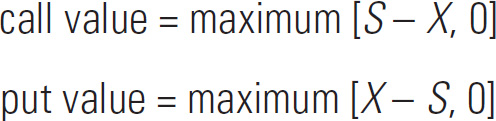

If the underlying price moves up to Su or down to Sd, the terminal values of a call (Cu or Cd) or put (Pu or Pd) are:

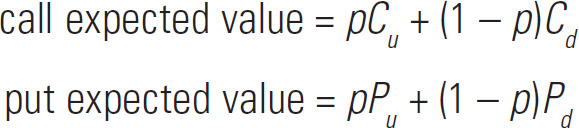

The expected values for a call or put are:

The theoretical value is the present value of the expected value (the expected value discounted by interest).

The delta values for a call and put in a binomial tree are:

1. stock price (S) = 82.50

time to expiration (t) = 2 months

interest rate (r) = 6%

u (an upward move) = 1.15

d (a downward move) = .90

a. What are the risk-neutral probabilities of an upward move, p, and a downward move, 1 – p?

b. What are the values of S for both an upward move (Su) and downward move (Sd)?

c. What are the values of the 80 call and 80 put at both Su and Sd?

d. What are the theoretical values of the 80 call and 80 put?

e. Show that put-call parity is maintained for the 80 call and 80 put.

f. What are the delta values of the 80 call (Δc) and 80 put (Δp)?

g. Show that if you buy the 80 call at its theoretical value and correctly hedge the position, regardless of whether the stock moves up to Su or down to Sd, you will just break even.

h. Show that if you buy the 80 put at a price .25 less than its theoretical value and correctly hedge the position, regardless of whether the stock moves up to Su or down to Sd, you will always show a profit of .25.

i. An American option can never be worth less than intrinsic value. Therefore the value of an American option at any point along a binomial tree must be maximum [European value, intrinsic value].

Suppose this stock is expected to pay a dividend of 1.50 over the next two months. What is the value of the 70 call if it is both European and American? If you own the 70 call and it is American, what action should you take?

j. Suppose we are in a hyperinflationary market where interest rates are 100% annually. Using the same u (1.15) and d (.90), what are the new values of p and 1 – p? What can you conclude from the new probabilities?

2. In this section, depending on whether the calculations are done with a spreadsheet or by hand, there may be slight rounding errors.

time to expiration = 30 weeks (1 week = 1/52 year)

annual interest rates = 4%

annual volatility = 27%

stock index price = 1,278.00

expected dividends = 0

a. In a 3-period binomial tree, what is the discounting factor (using simple interest) over each period in the tree?

b. If ![]() and

and ![]() in a 3-period binomial tree what are the values of u (an upward move), d (a downward move), and the risk neutral probabilities of an upward move (p) and downward move (1 – p)?

in a 3-period binomial tree what are the values of u (an upward move), d (a downward move), and the risk neutral probabilities of an upward move (p) and downward move (1 – p)?

c. What are the terminal values for the index at the end of the three periods?

d. Using the probabilities, p and 1 – p, what is the probability of reaching each terminal price?

e. How many different paths lead from the initial price of 1,278 (S0,0) to each terminal price?

f. What are the values of the 1300 put at each terminal price?

g. Using the terminal values for the 1300 put, the number of paths to each terminal price, the values of p and 1 – p, and the discount factor over each period, calculate the initial (theoretical) value of the European 1300 put in a 3-period binomial tree.

h. Insert the index prices at each branch in the 3-period binomial tree below.

i. Using the terminal prices in the above tree, and using the values of p and 1 – p, insert the European values for the 1300 put at each branch in the binomial tree. (Remember to discount the expected value by interest in order to obtain the present value at each branch.)

j. The gamma values for either a call or put in a binomial tree are:

Γ = (Δu – Δd) / (Su – Sd)

Using the values in the above tree, where possible, insert the delta and gamma at each branch in the binomial tree.

k. What is the approximate weekly theta for the European 1300 put?

3. Suppose the 1300 put in question 2 is an American option.

a. Using the underlying prices from your binomial tree in question 2h, fill in the theoretical value, delta, and gamma for the 1300 put at each branch on the 3-period binomial tree below.

b. What is the approximate weekly theta for the American 1300 put?