|APPENDIX|

Useful Formulas and Relationships

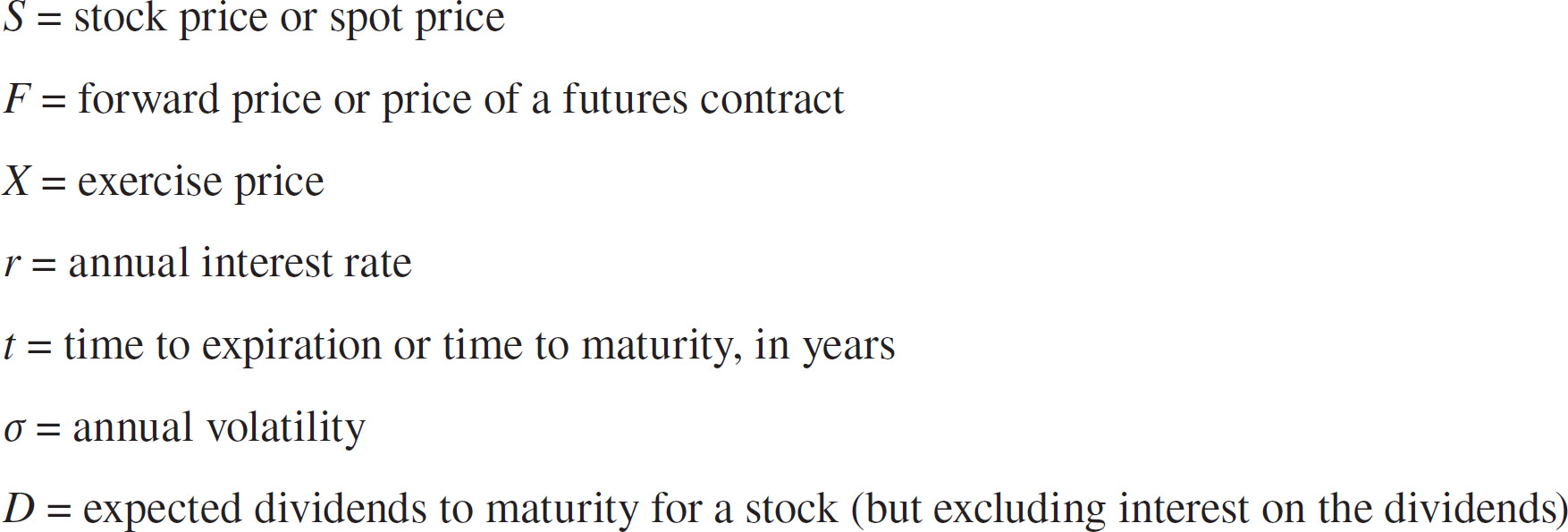

In the following,

The Forward Price (F)

Volatility (σ)

Probabilities (Approximate)

68¼% of all occurrences fall within one standard deviation of the mean.

95½% of all occurrences fall within two standard deviations of the mean.

99¾% of all occurrences fall within three standard deviations of the mean.

The “Greeks”

Delta (Δ). The sensitivity of an option’s theoretical value to a change in the underlying price.

Gamma (Γ). The sensitivity of an option’s delta to a change in the underlying price; usually expressed as the change in delta per one point change in the underlying price.

Theta (Θ). The sensitivity of an option’s theoretical value to the passage of time; usually expressed as the change in value per one day’s passage of time.

Vega. The sensitivity of an option’s theoretical value to a change in volatility; usually expressed as the change in value per one percentage point (1.00%) change in volatility. Often interpreted as the sensitivity of an option’s price to a change in implied volatility.

Rho (P). The sensitivity of an option’s theoretical value to a change in interest rates; usually expressed as the change in value per one percentage point (1.00%) change in interest rates.

Spreading Strategies

Synthetic Relationships

The six basic synthetic long and short contracts; all options have the same exercise price and expiration date:

long call + short put ≈ long underlying contract

short call + long put ≈ short underlying contract

long put + long underlying contract ≈ long call

short put + short underlying contract ≈ short call

long call + short underlying contract ≈ long put

short call + long underlying contract ≈ short put

box = synthetic long underlying contract at one exercise price + synthetic short underlying contract at a different exercise price where all options expire at the same time

= bull call spread + bear put spread

roll = synthetic long underlying contract at one expiration date + synthetic short underlying contract at a different expiration date where all options have the same exercise price

= call calendar spread – put calendar spread

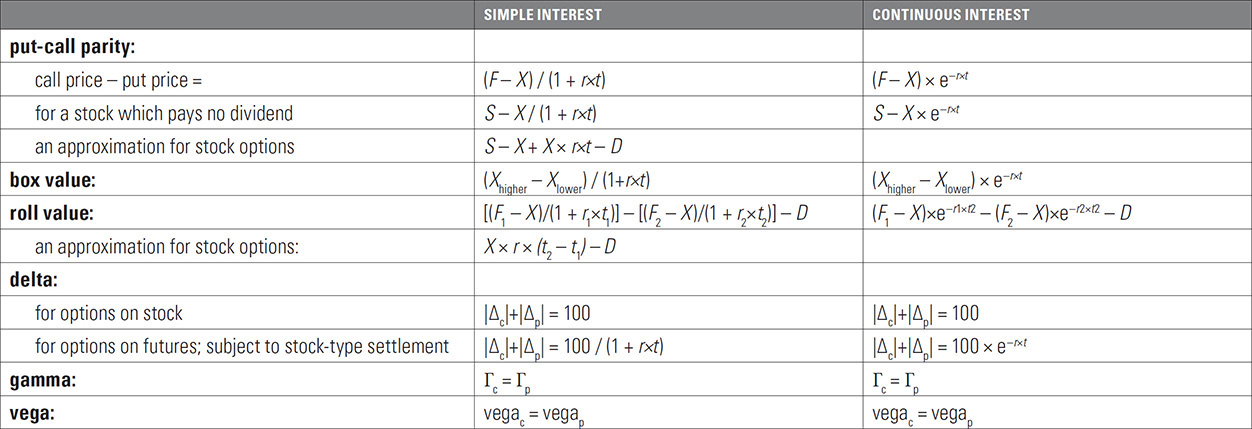

Arbitrage Relationships for European Options

Criteria for Early Exercise

Criteria must apply over the entire life of the option as well as over the next day.

Black-Scholes Model

For the complete Black-Scholes model refer to Chapter 14.

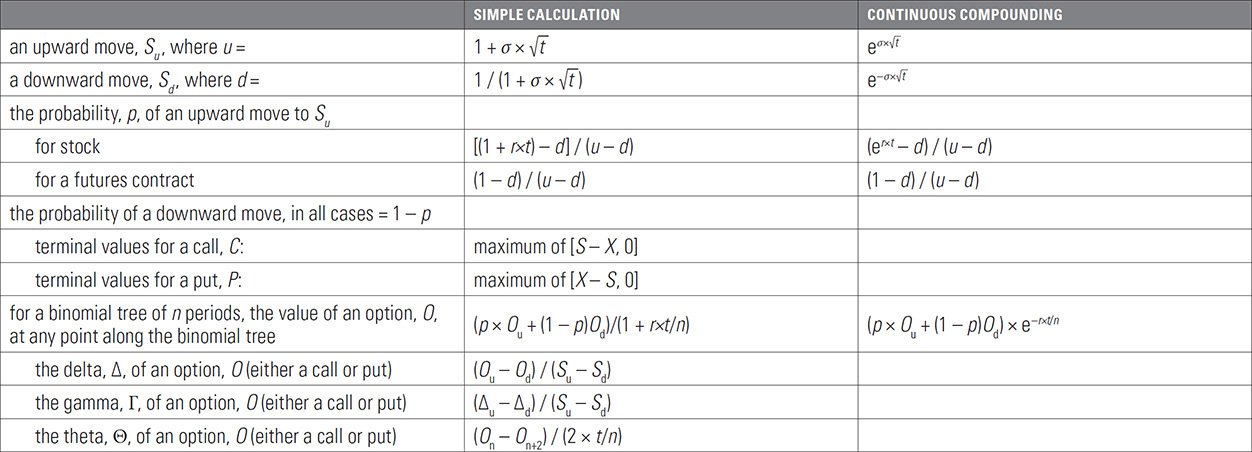

Binomial Option Pricing