| CHAPTER 2 |

Forward Pricing

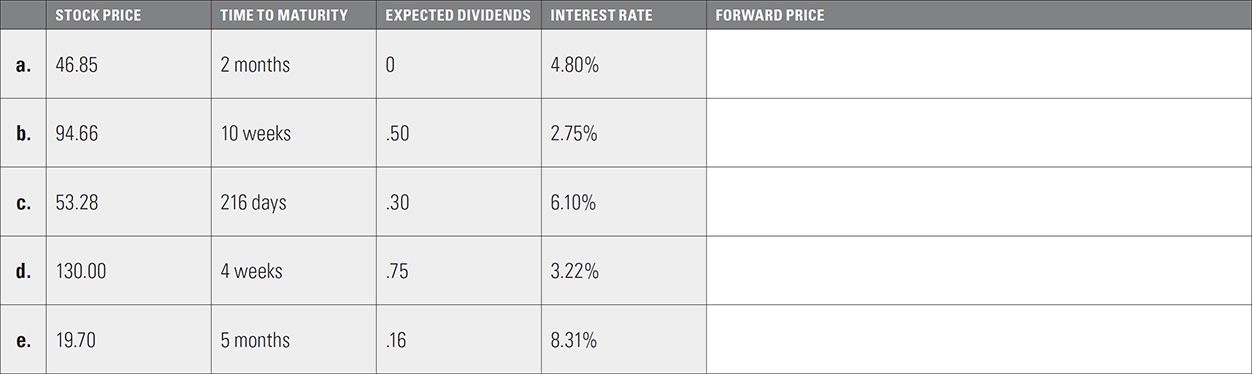

1. If S is the current stock price, t is the time to maturity, r is an annual interest rate, and D are the expected dividends prior to maturity, then using simple interest, and ignoring interest on dividends, the forward price F for a stock can be approximated as:

F = S × (1 + r×t) – D

Using this relationship, what are the following forward prices? For purposes of this exercise assume that a year is made up of 365 days, 52 weeks, or 12 months.

2. A stock that is currently trading at 123.15 is expected to pay a semiannual dividend of 2.60, with the next dividend payment occurring in two months. Including interest earned on dividends, if annual interest rates are 5.30%, what is a one-year forward price for the stock? (Assume that the same interest of 5.30% applies to all cash flows.)

3. A futures contract can be thought of as an exchange-traded forward contract. Using simple interest, and ignoring interest on dividends, calculate the following stock prices. For purposes of this exercise assume that a year is made up of 365 days, 52 weeks, or 12 months.

4. A stock forward contract with 84 days to maturity is trading at 76.95.

a. Ignoring interest on dividends, if the underlying stock is trading at 76.60 and interest rates are 4.25%, what is the implied dividend?

b. The same stock forward contract with 84 days to maturity is trading at 77.30. If the underlying stock is trading at 76.70 and a dividend of .51 is expected over the life of the forward contract, what is the implied interest rate?

5. If C is the current price of a commodity, t is the time to maturity, r is an annual interest rate, and s is storage and insurance costs to maturity, then using simple interest, the forward price F for a physical commodity can be approximated as:

F = C × (1 + r×t) + s

a. A physical commodity is currently trading at a cash price of 463.25 per unit. It costs 2.75 per month per unit to store and insure the commodity. If interest rates are currently 6.40%, what is a fair five-month forward price?

b. Suppose you are an end user of the commodity and require delivery of the commodity in five months. If the price of a five-month futures contract is currently 496.00, what would you do?

c. If the price of the same five-month futures contract is currently 480.00, now what would you, as an end user, do?

d. The additional amount that buyers are willing to pay right now for immediate access to a commodity is sometimes referred to as the convenience yield. Using the interest rate and storage costs in the previous question, if the commodity is still trading at a cash price of 463.25 and a two-month futures contract is trading at a price of 468.50, what is the two-month convenience yield?

6. If S is the current exchange rate for a foreign currency (the foreign currency in domestic currency units), t is the time to maturity, rd is the domestic currency interest rate, and rf is the foreign currency interest rate, then, using simple interest, the forward price F for a foreign currency can be approximated as:

F = S × (1 + rdt) / (1 + rft)

Suppose that at the current exchange rate one British pound is equal to 1.24 euros (£1.00 = €1.24). If the pound interest rate is 3.78% and the euro interest rate is 2.32%, what should be a three-month forward price for the pound expressed in euros?