3

THE WEALTH CONNECTION

It is not because things are difficult that we do not dare. It is because we do not dare that things are difficult.

—SENECA

Welcome to the fascinating world of personal finance. Though I imagine, for some of you, this world feels more foreboding than fascinating. I quite understand. In this chapter, I will do my best to quell your fears by demystifying, simplifying, and clarifying what may be unfamiliar, if not forbidden territory. We’ll do this by delving into four questions.

1. What is wealth?

2. How do I create wealth?

3. Why is building wealth so scary?

4. How can I best protect myself?

As you read the following pages, I want you to notice when your mind begins to wander, when you start spacing out or fogging up. If this happens, take a moment to look at why you lost focus. Maybe you’re tired and need a break. Or perhaps your Ego, from its perch in the primitive brain, is trying to restrict your entry into what it considers a high-risk zone.

Just notice and either take a break, resume reading, or journal about your reaction. Of course, it’s perfectly normal to glaze over when you come across unfamiliar terms or perplexing jargon. But instead of getting overwhelmed and giving up, or ignoring it and moving on, I urge you to immediately look up the word or phrase online as a way to further educate yourself.

WHAT IS WEALTH?

Wealth is not [hers] that has it, but [hers] that enjoys it.

—BENJAMIN FRANKLIN

Before we begin, I want you to answer this question: How much money do you need to be wealthy?______________ . Write down the first number that comes to mind. Don’t read any further until you have your number.

Of course, you may argue, there’s more to wealth than amassing money. There’s love, health, freedom, and friendship. All true. But for the purpose of this chapter, let’s stick with a specific figure.

If you’re like most, you chose an amount that’s more than you have now. Maybe a lot more. But here’s what I want you to understand. Wealth is not an amount. It’s a mindset.

I’ve met women worth millions who are financially insecure. I know many who have far less and consider themselves bountiful. Wealth without well-being is not the aim of this book. Financial well-being means you’re in control of your money, not at its mercy.

I propose a different definition of wealth, one that describes the desired mindset: Wealth means you have more than enough . . . and you know it. You not only have some disposable income, but a buffer against debt, a prudent reserve for unpredictable expenses, and a safety net that lets you sleep all night. And you’re fully aware that you’re in good shape. In other words, wealth is that sweet spot where money is no longer a source of stress or distraction, but a powerful tool for crafting a secure and meaningful life.

Like any tool, however, you must understand how to skillfully use it for maximum benefit with negligible risk. I think of my husband’s chainsaw, which he expertly operates. In my hands, I shudder to think of the havoc I’d cause.

This chapter is meant to be an operator’s guide to confidently, competently enjoying the incredible tool we call money.

HOW DO I CREATE WEALTH?

Never spend your money before you have it.

—THOMAS JEFFERSON

To create wealth, all you need do is follow four rules, in this order:

1. Spend less.

2. Save more.

3. Invest wisely.

4. Give generously.

Admittedly, adhering to the first three can be a formidable challenge. It’s tempting to head straight to the fourth, which is much more fun. After all, giving releases those feel-good hormones, like dopamine, in the brain. But the rules must be followed in this sequence. Bypassing the first three not only jeopardizes your future security but diminishes the impact you can make with your money.

Rewire in Action

RATING YOUR RELATIONSHIP TO WEALTH

Rate your relationship to each rule on a 1–5 scale: 1 is terrible; 5 is terrific.

Spending: ______________

Saving: ______________

Investing: ______________

Giving: ______________

Then ask yourself the following questions, jotting down your answers.

If you could change one score to 5, what would it be? ______________

What if raising that one score to 5 was part of your intention for reading this book? Rewrite your intention from the Introduction (page xxvii) to include raising that score: ____________________________

![]()

On a scale of 1–5, how motivated and how committed are you to change it? ______________

Pay special attention to those you rated 4 or less as you read through this chapter. Ask yourself: What’s preventing this category from being a 5? Your responses reveal where you need to concentrate (and where you’ll likely fog up) as you read.

The first three rules are the How-tos. Consistently repeating these behaviors—spending less than you have, saving more than you need, and investing in assets that beat inflation—is precisely how you rewire for wealth. What you repeatedly focus your attention on is what gets wired in your brain. The fourth is the Why, the reason you’ll stick with the other three rules, despite your resistance. Let’s take a closer look at each rule.

Rule #1: Spend Less

Too many people spend money they haven’t earned, to buy things they don’t want, to impress people they don’t like.

—WILL ROGERS

Obviously, if you spend more than you have, you’ll never have more than enough. At best you’ll be teetering on a tightrope of barely enough. At worst, you’ll be caught in the chaos of overdue bills and creditors calling. Debt and well-being can never coexist.

But even if you’ve always been frugal, I invite you to look closely at your spending habits. The best way to do this is by tracking your expenses, writing down everything you spend. Believe me, this exercise is not just for those with limited means. The numbers tell a story about your life. You’ll discover bad habits and blind spots, where you’re putting your time and energy, what’s missing in your life, and where you’re not living your values.

Rewire in Action

TRACKING YOUR SPENDING

Here’s how it works. Buy a small notebook or find an empty checkbook register that fits into your pocket or purse. Whenever you buy something—a yoga class, a subway ticket, a cup of coffee, or pair of shoes—whether you use cash, check, debit, or credit—jot down the item along with the cost. Try to do this at the point of purchase. Otherwise, as receipts pile up, you’ll likely get overwhelmed and give up.

I want you to do this exercise by hand, not electronically, at least for the first few months. Using an app may be easier, but the physical act of writing keeps you mindful and connected to your money. Otherwise, it’s easy to rationalize your behavior and ignore potential consequences.

I’m not asking you to change anything, either. You can if you wish, but in the beginning of this process I want you to simply note, without judgment, how much you spend and on what. This is meant to be a consciousness-raising exercise. And it’s powerful!

After a few weeks of tracking, my client Betsy Furler was excited. “Writing down what I spend, seeing it, made me feel so in control!” she exclaimed. “It made me think before spending. I felt so powerful. Every decision is my decision.”

Don’t be surprised, however, if your brain rebels against tracking. I remember when my mentor, Karen McCall, a pioneer in financial recovery counseling, first gave me this assignment, I resisted it for months. I’d start and stop, forget to write stuff down, and angrily refuse to do it. But as Karen kept reminding me, “Tracking is a tool, not a weapon to beat yourself up.” I say the same to you. Don’t make yourself wrong if you fall off the wagon. Just get back on as soon as you can.

When I finally kept at it, I had some unexpected surprises. For example, I saw I was spending a fortune on face creams, and they weren’t even working. Karen gently explained what I was doing here: “You’re trying to fill a hole in your soul that no amount of money can ever fill,” she said softly. I knew she was right. All the moisturizer on the planet wouldn’t erase my deep sense of shame and unworthiness.

At the same time, Karen noticed how often I used a magnifying glass to read, even while wearing store-bought readers. When she asked why I didn’t get prescription glasses, I heard myself say, “They’re so damn expensive.”

“Now that’s deprivation,” she said. “You’re not giving yourself what you really need—good eyesight. But you’re splurging on wrinkle removers.” Then she said the words that deeply resonated: “You can never get enough of what you don’t really need.”

Tracking is not about sacrifice or deprivation. It’s about consciously choosing to practice healthier behaviors. I remember Karen saying to me, “It’s OK to have massages, but what if you had one a month instead of every week and deposited what you would’ve paid into your savings?” This advice applies to all kinds of things, from dining out to ordering online.

Tracking also stimulates the rewiring process by focusing your attention on healthier behaviors. In his book The Power of Habit, Charles Duhigg talks about a four-month study on willpower designed by two Australian researchers, Ken Cheng and Megan Oaten. After participants wrote down every purchase for four months, not only did their finances improve, but they smoked and drank less, ate less junk food, and were more productive.

“As people strengthened their willpower muscles [i.e., neuropathways] in one part of their lives [i.e., brain],” Duhigg wrote, “that strength spilled over into what they ate or how hard they worked. Once willpower became stronger, it touched everything.”1

Eventually, you’ll sort your expenses into various categories: mortgage, car, groceries, dining out, medical, and so on. Include categories you might be neglecting, like vacations, clothing, or personal care. For this, I suggest you use one of the many popular budgeting apps.

Once you see which items are fixed costs, you’ll know where you can shave and save and, of course, pay down debt. I urge you to pay off your debt as quickly as possible. And stop using credit cards. Wealth is unsustainable while your bills go unpaid.

Rule #2: Save More

For every ten coins thou placest within thy purse take out for use but nine.

—GEORGE SAMUEL CLASON

The first rule, spend less, sets you up for the second, save more by paying yourself first. Every time money comes in, put a portion into personal savings. How much? Ten percent is ideal, but less is absolutely fine.

Sadly, few people do this. A 2019 Federal Reserve report found that only two in five Americans could cover an unexpected $400 expense. Why do so many save so little? The fault may lie in our brains. The Wall Street Journal reported that Cornell University neuroscientists discovered that our brains are biased toward earning and against saving.2 Perhaps it’s the immediate gratification our paychecks offer, while putting aside small amounts feels about as gratifying as watching grass grow.

“Fundamentally it comes down to this: saving is less valuable to our brains, which devote less attentional resources to it,” study coauthor Adam Anderson, associate professor of human development, told the Journal. “Our brains find saving more difficult to attend to.”

Yet fixating on earnings can be foolhardy. I call it the illusion of affluence. I see it all the time. Successful women spending too much, saving too little, and plowing all profits back into their businesses or into classes for personal growth (deceptively calling it “an investment”). Their ample earnings give them the illusion, but not the security, of true abundance. As I’ve said before, wealth doesn’t come from what you earn, but from what you do with what you earn (which we’ll be covering next).

For many, setting aside savings is akin to self-imposed poverty, as expressed in a recent email I received from a fan: “How can I SAVE money to create wealth (which means cutting back spending) and still have a feeling of ABUNDANCE (which means the desire to SPEND) and not a mentality of LACK?”

In her mind, spending provided the pleasurable pretense of prosperity, while savings felt like self-denial. But a brain wired for wealth views it quite differently. Saving means you’re giving the money to you (not Visa or Starbucks) so that ultimately you can purchase whatever you please without pressure or worry. The difference between the two mindsets is not deprivation but delayed gratification. The ability to delay gratification is a sign of maturity and the quickest way to accumulate more than enough.

The best part: Saving is so easy when you automate. Simply contact your bank (online or in person), fill out a form instructing them to automatically transfer a certain amount (no matter how small) each month from your checking account to your savings account. You don’t miss what you don’t see. And, with little effort, you set the rewire process in motion. As you watch your savings swell, the reward centers of your brain light up, and your inclination to save more increases by the day.

But what if you can’t come up with even a few spare dollars by month’s end? I remember asking my client Dionne Thomas, who had zero savings, what she did with extra money.

“Extra money?” she gasped incredulously. “What’s that?”

She, like most, frittered away more than she realized on frivolous items leaving little if anything left over. It actually never occurred to her she had a choice. No one in her family ever saved.

“I never understood extra money,” she laughed when I interviewed her much later. “But once I started tracking my money and paying attention to it, I always put a portion of what I don’t spend into the bank.”

After making savings a priority, within a few months she had several hundred dollars sitting in a savings account. “Now at the end of every week, I’m able to pay my bills and still save. I’ve never been so excited about savings,” she said, telling me how amazing it was that she had enough set aside to get an abscessed tooth fixed when she was in terrible pain and buy new tires when she needed them for a road trip.

Here’s a simple way to start making savings a habit. Each night drop any loose change from your wallet into a jar, and every month, bank the savings. I once had a client who, on the day her grandson was born, quit smoking, putting the daily cost of the cigarettes directly into savings. By the time her grandson graduated from high school, she could pay his college tuition. Another began collecting coins she found in pockets doing laundry and cash from the coupons she redeemed at the market to make her first purchase of stock—three shares of Disney. Never underestimate the power of small amounts consistently saved.

Rewire in Action

SHAVE AND SAVE

Let’s look at where can you shave and save. As you keep track of your spending, start noticing where you could possibly spend a little less and deposit that amount into a savings account. During our Rewire Mentorship Program, New Yorker Jazmine Roberts made an appointment for a massage, which her body desperately needed. When she found out it cost $180, she did some research and found a place in Chinatown that charged $39. She deposited the difference. She did the same with eating out, which she discovered she and her husband did almost every night. Now they dine out only once a week during weekends.

I recommend setting aside at least 8 to 12 months in living expenses. That may take some time, but it’s a good goal to shoot for. I also recommend having two types of savings accounts: First, start an untouchable account for emergencies and unexpected expenses. And since a shoe sale isn’t an emergency, open a touchable account for fun things like new shoes, a vacation, or movie nights. Having the latter keeps you from dipping into your emergency savings or feeling deprived.

Rule #3: Invest Wisely

How many millionaires do you know who have become wealthy by investing in savings accounts? I rest my case.

—ROBERT G. ALLEN

When you comply with the third rule—invest wisely by putting money into assets that grow faster than inflation—you move into the world of wealth creation. (Warning: In this section you may stumble on some confusing or unfamiliar terms. As I suggested earlier, look them up before you read further.)

Granted, investing can be daunting and easy to ignore, even for women who work in the financial industry. I can’t tell you how many bankers, CFOs, financial advisors, mortgage brokers, and money coaches come up to me after a speech and say in total embarrassment, “I do this for a living, but my own finances are a wreck” or “I manage millions of dollars, but when it comes to my own checkbook, I feel like a klutz.”

Just now as I write, I’m interrupted by an email from an investment advisor that says: “Even knowing the facts, I get stopped dead in my tracks, unable to manage my own money.”

This makes perfect sense if you remember our discussion in the last chapter. Financial literacy doesn’t predict financial efficacy. Knowledge has no power against a highly activated primitive brain.

Investing doesn’t need to be complicated or intimidating, as long as you do the work of rewiring for wealth. Paraphrasing the legendary stock picker Peter Lynch, there’s nothing about investing that a fifth grader couldn’t understand. To which your Ego angrily retorts, “That’s bulls**t!”

Let me show you how simple investing really is. There are only two ways to invest. You either own or loan. And there are only five places to invest, known as asset classes:

1. Stocks. You own shares in a company.

2. Bonds. You loan money to a company, state, city, or government.

3. Real estate. You own houses, buildings, or land.

4. Cash or cash equivalents. You loan money to the bank, a money market fund, a certificate of deposit (CD), or short-term Treasury bills.

5. Commodities. You own raw materials, like gold or oil, or agricultural products, like wheat or pork bellies.

Let’s compare how each asset class has performed against inflation. After all, one reason you invest is to prevent your entire savings from being gobbled up by rising prices.

• Inflation has averaged 3.5 percent annually.

• Cash has averaged about 3 percent annually (though at this writing, returns are less than 2 percent).

• Stocks average just over 9 percent annually.

• Real estate averages about 6.2 percent annually.

• Bonds average about 5 percent annually.

• Commodities return 6.9 percent annually.

Can you see why at least a portion of your cash needs to be in assets that outpace inflation? According to the 2019 Ellevest Census, women who fail to invest leave anywhere from $50,000 to over $1 million on the table. Avoidance comes with a high price tag.

We can’t talk about investing without mentioning the Rule of 72, a formula to determine how long your investment will take to double. The formula is simple: Divide the annual rate of return into 72. Let’s say you own a fund that returns an average of 8 percent annually. If you divide 72 by 8, it will take 9 years to double your money. Put that same amount in the bank, paying 1 percent interest, and it’ll take 72 years to double. Even if interest goes up to 3 percent, you’ll need 24 years to double that cash.

(This formula applies to debt as well. Let’s say you’re paying 12 percent on your credit card. Divide 72 by 12, and you’ll see that your debt will double in 6 years.)

Rule #4: Give Generously

Only those who have a real and lasting sense of abundance can be charitable.

—A COURSE IN MIRACLES

Often, during a speech, I’ll ask the audience: “How many of you are knowledgeable or somewhat knowledgeable about investing?” Very few hands go up.

“Why not?” I ask.

“I don’t have time,” most will say. “It’s too confusing.” Or “I don’t know where to start.”

“Interesting,” I muse. Then I pose another question.

“What if a doctor told you that you have a serious condition that would dramatically affect your quality of life as you age? I bet, no matter how busy you are, or how complicated it feels, you’d find a way to research the best treatment and make sure you get it.”

Heads nod in agreement.

“Well, if you’re ignoring money, you’re saying that quality of life is not a priority.”

Indeed, rewiring for wealth can be tough without having a strong why, especially for women. Unlike men, once we’re financially stable, we’re rarely motivated by more money. What drives us is knowing we can use our money to improve the quality of life for ourselves and for others.

In a Simmons School of Management survey, more than 70 percent of women polled report they are driven not by “perks, position, or personal gain,” but to help others, contribute to communities, and make the world a better place.

If you’re struggling with the first three rules or find yourself in a financial rut, try this. Focus on what inspires you and stop dwelling on what scares you. It’s called selective attention, a powerful technique for rewiring your brain, which we’ll discuss again in Chapter 6. Instead of obsessing about everything that can go wrong, try turning your thoughts to what investing offers you. Think about how having more than enough allows you to give money to causes you feel passionate about, helping your kids, your parents, people you love. Think about the exhilarating sense of freedom, security, and self-confidence wealth brings.

That’s what I finally did. I started thinking about the kind of a role model I wanted to be for my daughters instead of fixating on my fear of screwing up. When I made that deliberate shift, I had no choice. Financial avoidance was no longer an option. And if my experience is any indication, you’ll be saying what I hear every woman say when she finally takes the financial reins: “I feel so powerful.” Because when you take control of your money, you take control of your life. In the 2019 Ellevest study, both sexes agree, “Money is key for feeling in charge of your life.” And for women, taking control of their money is “the number one confidence booster.”

Rewire in Action

FINDING MY MOTIVATION

Ask yourself these questions and jot down some ideas here:

Why am I reading this book? ____________________________

![]()

![]()

Where in my life would I love to give more (to myself, to those I love, to causes I feel passionate about)? ____________________________

![]()

![]()

WHY IS BUILDING WEALTH SO SCARY?

In investing, what is comfortable is rarely profitable.

—ROBERT ARNOTT

Investing is scary for one simple reason: it’s risky. Neuroscience research proves that you and I hate to lose more than we love to win. After all, losing had deadly consequences for our ancient predecessors. To this day, when markets crash, the media will declare a “flight to safety,” as hordes of investors rush into safer investment (like US Treasuries) faster than a pack of panicked Neanderthals fleeing a saber-toothed tiger. There’s even a benchmark, The VIX, or Volatility Index, that actually gauges investor fear. The market is the fearmongering Ego’s favorite playground.

But here’s where we need to put risk in perspective. Cash in a bank or CD (certificate of deposit) is considered the safest investment of all. There’s virtually no uncertainty. But even with a government guarantee of return, is cash really risk-free? No. Of course not. You have inflation risk. Over time, as prices climb, your purchasing power plummets.

On the other hand, buying stocks, or shares of a company, definitely carries more risk. Share prices, even in the best companies, are always going up and down and up and down. However, when we talk about risk in this way, we’re referring to volatility, how much an asset fluctuates, known as market risk. And you need market risk to protect you from inflation risk.

Keep in mind: Price swings only matter when you sell. Everything else is just “noise,” the sound of the market doing what markets are supposed to do, bounce around like a rowboat on the open seas.

In my early interviews with savvy women, I’d always ask each one: “How do you have the guts to put money in the market?” After all, that’s how my first husband lost my money. Their responses radically shifted my thinking: “I know my investments will fluctuate. I accept that,” one woman explained. “I am also confident that over the long term, I will do well.”

That was my moment of revelation. Risk is not synonymous with loss. Risk is an opportunity for gain. Understanding risk is what makes you wealthy.

You want to know your most dangerous risk? It’s not the market gyrations. It’s your emotional reactions. Our brain registers risk even before we’re conscious of it. Consequently we tend to make rash decisions that rarely end well, even if we know better.

So when markets take a tumble, our emotions, especially fear, take over. And we make very bad decisions. It also happens in reverse. When the market is on a big run, there’s a tendency to take on too much risk and follow the herd, like so many did during the tech and real estate booms. Either way, it’s easy to go along with the crowd and invest too aggressively during good times and too conservatively in bad times.

“The investor’s chief problem—and his worst enemy — is likely to be himself,” one of the greatest investment advisors of the twentieth century, Benjamin Graham, wrote in his timeless classic The Intelligent Investor. “In the end, how your investments behave is much less important than how you behave.”3

Now, for the good news. I’m about to show you how you can significantly minimize risk, shield yourself from devastating losses, and successfully stack the odds in your favor.

HOW CAN I BEST PROTECT MYSELF?

Be okay with not knowing for sure what might come next, but know that whatever it is, you’ll be okay.

—ANONYMOUS

The question we’re really exploring in this section is: How do I deactivate a triggered limbic system (my fear center) so I can invest with confidence and not overreact with excessive fear? Yes, the market is scary. No, you can’t eliminate risk. But you can calm your primitive brain by practicing these five proven strategies to manage risk and keep your emotions in check, regardless of the market’s dips and dives.

Strategy #1: Educate

Now that I know better, I do better.

—MAYA ANGELOU

Warren Buffet once said: “Risk comes from not knowing what you’re doing.”4 He got that right. Your best protection against loss is making decisions based on knowledge, not fear, ignorance, or habit. And no matter how knowledgeable you are, there’s always more to learn. That’s what makes investing fun.

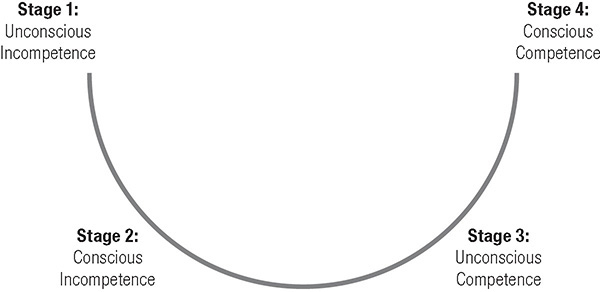

If you’re new to the subject, however, learning about investing can feel like navigating a minefield. Your ego will shriek: “Get me out of here! It’s dangerous!” That’s how I felt for years. Until I understood the four stages of the Learning Curve. To get smart about money, or anything else, you much travel through what educators call a Learning Curve (Figure 3.1). Let me explain.

FIGURE 3.1 Learning Curve

I lived most of my life in Stage 1 of the Learning Curve, Unconscious Incompetence. I didn’t even know what I didn’t know. The term “ignorance is bliss” explains why I never wanted to leave this stage. I fooled myself into feeling safe here, despite living with a ticking time bomb for a spouse.

It took a crisis—a huge tax bill I couldn’t pay—to kick me into Stage 2, Conscious Incompetence. I had no choice now. I needed to get smart. Yet the moment I picked up a financial book, I was seized by anxiety. I couldn’t understand a word I read. Everything in me yearned for the perceived comfort of the previous stage.

But I was committed. Big tax bills, three young daughters, and no money in the bank will do that. Despite my fear and confusion, I forced myself to keep reading, keep taking classes, and keep asking questions. Every once in a while, I’d get glimpses that I had moved into Stage 3 of the Learning Curve—Unconscious Competence. Someone mentioned the phrase “mutual fund” and, aha, I knew what it was. I actually read a whole page in the Wall Street Journal without once glazing over. But those moments were fleeting.

Finally, after months of flailing in the dark, I realized I was in Stage 4 of the Learning Curve, conscious competence. Yes, I still needed to keep learning, but I finally felt like I had a good grasp on the subject.

Staying on the Learning Curve can be extremely challenging. To keep myself going without holding back (at least not for long), I devised a simple two-step system I came to call The Osmosis School of Learning. I was amazed, in just a few months, how much smarter I felt. Small steps, consistently taken, lead to remarkable results.

• Every day read something about money. Even if it’s just for a minute or two. Even if you only glance at the headlines of the business section of the newspaper, or leaf through Money magazine while in line at the grocery. So much of getting smart or smarter about money is familiarizing yourself with the jargon, the current trends.

I remember, early on, subscribing to the Wall Street Journal. I’d lay it on the kitchen counter, and every day I’d walk by it, figuring that by osmosis I’d pick something up. To this day, if I do nothing else, I’ll glance at the headlines. You can do the same with financial programs on TV or the radio. But beware the hype. Bad news sells. “The key to making money in stocks,” declared Peter Lynch, “is not to get scared out of them.”

• Every week, have a conversation about money. Preferably with someone who knows more than you. I learned so much from the women I interviewed, so whenever I met anyone who was financially savvy, I’d pick their brain, asking them how they got smart, the mistakes they made, the best advice they were given, and for any other suggestions they might have. Generally, people were very generous with their time and knowledge.

I also attended classes. Podcasts are great too. But listening to financial experts made me wish I had a translator. Financialese is truly a foreign tongue. I finally realized I needed to speak up, ask for clarification, and keep asking until I understood.

Strategy #2: Plan

It takes as much energy to wish as it does to plan.

—ELEANOR ROOSEVELT

Not long ago, a woman in one of my groups proudly announced that she’d maxed out her 401(k) and had been buying stocks outside her retirement fund based on recommendations from a friend who worked at a brokerage firm.

She had a right to be proud. But when I asked if she was following a plan, she looked puzzled.

“How do you know whether or not your portfolio is properly diversified?” I asked her. “Or if you’re taking too much or too little risk?”

Creating a personalized financial plan is what separates investing from gambling. Picking stocks or bonds haphazardly, following a hot tip or purchasing the hottest fund, trying to time the market (buying when it’s high, freaking out and selling when it’s falling), or just simply deferring investment decisions to another and turning your back—that’s gambling, and it’s genuinely risky in the worst possible sense.

Investing, on the other hand, is a means to an end. The whole point of investing is to put together a portfolio that ensures you meet your goals and protect your future, no matter what the market is doing.

The best way to measure your investing success,” explained the illustrious investor Benjamin Graham in his book The Intelligent Investor, “is not by whether you’re beating the market but by whether you’ve put in place a financial plan and a behavioral discipline that are likely to get you where you want to go.”5

A good financial plan addresses three questions:

• Where are you now?

• Where do you want to go (short term and long-term goals)?

• What do you need to do get from here to where you want to be?

Armed with the answers, you’re ready to create a game plan based on your time horizons, budgetary restrictions, and risk tolerance (your ability to stomach large swings in your portfolio).

For years, I worked with a series of financial advisors who put me in individual stocks. And I followed the guidance of my second husband, an expert on mutual funds. But I had no plan.

Then I met Eileen Michaels, a feisty, redheaded East Coast financial advisor who was whip smart and passionate about educating women. I instantly knew I wanted to work with her. Initially my intention was for her to manage only my individual stock portfolio. She wouldn’t have it.

“You can’t invest like that, without a strategic plan,” she told me. “Keeping your investments fragmented is how you’re keeping yourself small.” She had me at “small.”

“What is your criteria for investing?” she asked. I had no idea. So I gave it some thought and came up with a list.

First and foremost, I wanted to be extremely diversified because, by that time, I knew this was important. (We’ll talk more about this in the following section.)

I also wasn’t as concerned if my investments went up sky high in a bull market, but I wanted to be damn sure I was protected when the market tanked.

I was souring on the outrageous expenses of mutual funds, so I wanted everything in individual equities.

And I was very clear: I wanted to be involved in the decision making. That’s how I’d learn.

Eileen then asked about my goals. How did I want to use my money? This was easy. I wanted a sizable cash savings, probably more than she’d advise, but after being married to a gambler, I needed a hefty cushion to feel safe. We talked about how my second husband and I were thinking of moving, so I’d probably need money for a house. We discussed my kid’s education, my income as a writer, my fantasy of flying private someday.

Based on these conversations, she drew up a plan making sure I was taking enough risk to have growth, but not so much that I’d get spooked. Then she put that plan into action, creating a diversified portfolio of stocks and bonds. There was one problem, however. I was traveling so much for work, she could never get ahold of me when she wanted to make changes.

So back to the table we went. In the year 2000, she introduced me to two investment vehicles I’d never heard of: Index funds and exchange traded funds (ETF). Index funds are bought and sold when the market closes, and ETFs are traded like stocks on an exchange. Both mimic the indexes (carrying the exact stocks that are in a particular index, say the S&P 500 or the Russell 1000, for example), allowing me to be quite diversified at much lower fees than my managed funds. Best of all, these funds outperform over 85 percent of the high-priced managers, as illustrated by the following story.

In 2007, legendary investor Warren Buffett made a $1 million bet with a noted hedge fund manager. Buffet wagered that the Vanguard 500 Index Fund would outperform more sophisticated, high-priced hedge funds over a 10-year period. Guess who won? In 2017, the index fund returned 7.1 percent, while the basket of hedge funds returned 2.2 percent.

Strategy #3: Diversify

Diversify. In stocks and bonds, as in much else, there is safety in numbers.

—SIR JOHN TEMPLETON

I once saw a cartoon that cracked me up. A financial advisor sat across the desk from the Easter Bunny holding a basket of eggs. The advisor, leaning forward, warns the bunny sternly: “Never put all your eggs in one basket!”

The advisor, of course, was impressing on his client the importance of diversification, or spreading your money (eggs) into different asset classes (baskets), like stocks, bonds, cash, real estate, or maybe even commodities.

Furthermore, each asset class can be divided into subclasses. For example:

• Stocks can be carved into small, medium, and large company stocks (otherwise known as small, medium, and large cap stocks).

• Bonds can be separated into corporate, municipal, and government bonds.

• Both stocks and bonds can be further subdivided into different regions, like the US, Europe, Asia, and emerging markets (underdeveloped countries).

• Real estate can be subdivided into raw land, residential, and commercial buildings.

The idea is that different asset classes or subclasses react differently to various conditions and time periods. So when, say, small cap stocks take a hit, large companies may be doing great. Or when US stocks are tanking, overseas companies may be holding their own, and emerging markets may be soaring—or vice versa. And since you never know which sector will take the next beating, diversification reduces the volatility of your whole portfolio.

In fact, a well-known study showed that diversification accounts for 93 percent of a portfolio’s overall performance, 3 percent comes from stock picking, and 4 percent from luck. Index funds or ETFs make diversification easy and inexpensive.

How you diversify depends on your goals, which is why it’s so important to have a plan. Let me remind you, a long-term diversified portfolio can mitigate many risks, but none of it matters if you can’t keep your emotions in check.

Strategy #4: Time

The stock market is designed to transfer money from the active to the patient.

—WARREN BUFFETT

I’ll never forget my first foray in the market. It was 1986, and I invested a small amount with a broker. A year later, October 1987, the market crashed, big-time! I called him in a panic, instructing him to sell everything. He begged me not to. I didn’t listen. Of course, the market rebounded, quite quickly. I’d be a lot richer today had I stayed put.

Ten years later, almost to the day, in October 1997, the market took another nosedive. This time, I called my advisor, telling her to buy. I didn’t see a crash. I saw a sale! Stock prices were cheap. I wouldn’t need this money for at least 10 years. I trusted time would eventually reward my patience. And it certainly has.

As James Mackintosh, columnist for the Wall Street Journal, wrote, “Those who bought on the day the S&P 500 hit its top on Oct. 9, 2007, and held on through the subsequent panic and market collapse, have more than doubled their money. including dividends.”6

If you were to look at a graph of the market over the past 100 years, you would see a jagged line resembling a roller coaster that, despite the dips and dives, keeps steadily climbing in an upward arc.

What I want you to remember: it’s the overall direction, not the day-to-day bouncing, that matters. Those dips and dives only matter when you sell your holdings.

Here’s how to use time to your advantage:

• Money you’ll need in the next 3 to 5 years should be in cash (so you don’t have to sell when the market is down).

• Money you’ll need in 5 to 10 years can be in conservative stocks and bonds.

• Money you won’t need for 10+ years can be in more volatile stocks, bonds, real estate, or commodities (because you have more time to ride out the highs and lows).

In 2016, Marketwatch reported: “There has literally never been a 20-year period in the past century or so that has resulted in a negative return for stocks, so investors with the patience and constitution to see their portfolio through a rough year should be rewarded regardless of the gloom and doom.”

Trying to time the market, figuring out when it’s reached it’s high, selling because it’s ready to fall, is a recipe for loss. Countless people have tried and failed. A few luck out, but never consistently. “After nearly 50 years in this business,” wrote the late Jack Bogle, founder of Vanguard and creator of the first index fund, “I do not know of anybody who has timed the market successfully and consistently. I don’t even know of anybody who knows anybody who has done it successfully and consistently.”7

Strategy #5: Unplug

Don’t let the bearers of bad news become the pallbearers of your happiness.

—STEWART STAFFORD

Once you have these four strategies in place, I highly recommend that next time the market takes a tumble, you do this immediately: Turn off the TV. Shut down the computer. Don’t look at your portfolio. Ignore the naysayers. Instead, take a walk or get a massage and remind yourself that the markets will go back up—because they always do.

This is what I’m doing and what I urge others to do while we are smack-dab in a global pandemic that, as of this writing, has yet to peak, creating unprecedented economic pandemonium. No one knows what the future holds. But if there’s one lesson I’ve learned, and as I’ve warned earlier in this chapter, it is this: Making decisions based on fear, greed, or any emotion is never a good strategy. Instead, I’m doing a lot of yoga and taking long walks every day. Sometimes I’ll call my advisor to check in. I don’t think I could’ve approached this period with so little stress if I hadn’t worked on rewiring my brain.

It’s one thing to read about investing, but it’s equally important to enhance your sense of self-efficacy and believe you can successfully build wealth over time. For this, we turn to Part II: “Rewiring,” where you will learn how to rewire your brain for wealth and well-being. But before you go, take some time to fill out the Wealth Builder’s Checklist, your guide for creating wealth.

Rewire in Action

Check the statements that are true for you. Let any statements left blank be the next steps you take to create wealth . . . and well-being.

![]() I am clear on my financial goals. They are:

I am clear on my financial goals. They are:

![]()

![]()

![]()

![]() I know my net worth. It is: ____________________________

I know my net worth. It is: ____________________________

![]() I have no credit card debt. If I do, the total is: ______________

I have no credit card debt. If I do, the total is: ______________

![]() I have enough savings to support me for three to six months. The amount is: ____________________________

I have enough savings to support me for three to six months. The amount is: ____________________________

![]() I have money invested in a retirement account. The amount is: ____________________________

I have money invested in a retirement account. The amount is: ____________________________

![]() I have investments outside a retirement account. The amount is: ____________________________

I have investments outside a retirement account. The amount is: ____________________________

![]() I understand the investments I own.

I understand the investments I own.

![]() I will have enough money to support me in retirement.

I will have enough money to support me in retirement.

![]() I have a will, power of attorney, and health directive.

I have a will, power of attorney, and health directive.

![]() I feel assured that if I died today, my affairs would be properly handled.

I feel assured that if I died today, my affairs would be properly handled.

![]() I know where all my financial documents and records are.

I know where all my financial documents and records are.