6.1. The Role of Information Capital in Enhancing the Value of an Enterprise

The various technologies and applications of business intelligence (BI) described earlier all have the potential to enhance the value of an enterprise. However, this value is often only potential value and is therefore hard to quantify. In this chapter, this problem will be investigated at length by examining value-based management1 and the current trends in management. Studies of the relationship between the use of business decision support systems and the value of an enterprise are quite complex, as information assets are intangible. This issue merits special attention because the proper selection and application of innovative technologies may considerably enhance the value of an enterprise.

6.1.1. Intangible Assets

Tangible assets, such as financial resources, can be easily identified. They are the basis of financial analysis and are commonly accepted in determining the value of an enterprise. However, recent developments in business practices have led to an increased interest in determining the value of intangible assets. That is also how Robert Kaplan and Peter Norton’s balanced scorecard concept emerged.2 Business decision support systems are a part of information capital, which in turn is intangible. According to Kaplan and Norton, intangible assets fall into three categories that are essential for the realization of a company’s strategy:

- Human capital. Skills, abilities, and knowledge of employees.

- Organizational capital. Organizational culture, quality of leadership, people’s adjustment to strategic tasks, and their ability to share knowledge with others.

- Information capital.

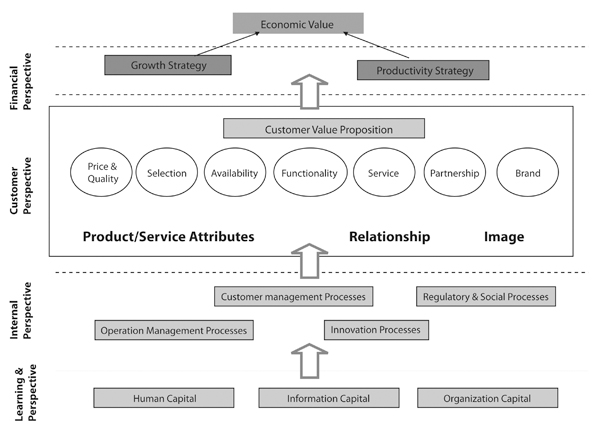

These resources are connected to the company’s strategy by a strategy map (see Figure 6.1), and they belong to the learning and development perspective in the balanced scorecard. The realization of a strategy is supposed to enhance the value of an enterprise. A widely used method of determining the value of a company in the financial perspective is to work out its economic value added (EVA).3 The strategy map, as an attempt to represent the sources of value in the enterprise, is an extension of the value chain concept from chapter 3. There are a few vital differences between determining the value of intangibles and tangible and financial assets:4

- Indirect value creation. Intangibles seldom have direct influence on financial results. They usually influence the finance of an enterprise by a complex chain of cause-and-effect relationships.5 For instance, information capital has an impact on the decisive internal processes from the angle of creating value for customers, reducing the costs of realizing processes, or both. As a result, income growth, the reduction of operational costs, or both translate directly into the value of an enterprise, which is monitored by certain financial indicators grouped in the financial perspective.

- Potential value. The value of intangibles is potential—that is, it can be used to create the value of a company, but the investment itself in those assets does not make the value grow. Investment in intangibles that support internal processes but do not increase revenue from customers may even generate unexpected costs and reduce the value of the company.

- Integration. Intangibles hardly ever create value themselves, so they have to be integrated with other assets from the same perspective. For example, investments in information technology (IT) bring results only if they are integrated with training and suitable motivational programs for employees.6

- Time. The potential value chain generated by intangibles is strongly time dependent. The primary competitive advantage gained by the implementation of an innovative IT system may be rapidly lost if the competition imitates it. If intangibles are not properly managed, they may become outdated very fast, and that may have a negative influence on the value of an enterprise. The classic example is the implementation of an electronic ordering system by American Hospitals Supply, which initially generated superb financial results. However, after a few years, due to obsolete technology and the lack of modernization, it reduced the company’s market position and hindered its development.7

6.1.2. Information Capital

Attitudes toward the use of IT such as BI in enterprises vary from an enthusiasm for IT to disappointment and harsh criticism. IT has become so ubiquitous that the services and products it produces have become almost invisible. An even stronger charge against IT is the argument that we are witnessing the twilight of the strategic value of IT systems.8 Among such critical voices, Lester Thurow’s reflection9 seems to be particularly important, despite being somewhat overstated: “There are single cases, where new technologies contributed to production growth and reduction of costs. However, when it comes to more general statements, there is no unambiguous evidence that new technologies enhanced productivity and profitability.” Such a firm conclusion is based on situations in which IT systems are implemented without being clearly linked to enhancing the value of the company. Having said this, it should be stressed that the failure to implement IT technologies properly does not automatically imply that they have no influence on the competitive advantage of a company. Instead, we should pay attention to the revolutionary impact of IT on the contemporary economy. Such criticism seems to emphasize how difficult it is to select, implement, and keep appropriate IT solutions up and running. The recent rapid development of IT systems implies countless classifications and attempts at their synthesis. Kaplan and Norton suggested the division of information capital, as is shown in Table 6.1. IT infrastructure allows for the application of two basic kinds of programs: transactional and analytical systems. Both can be the basis of transformation applications, which determine the business model of the company. Analytical applications—that is, BI systems—are information capital.

Figure 6.1. Role of intangibles in the strategy map.

Source: Based on Kaplan and Norton (2004).

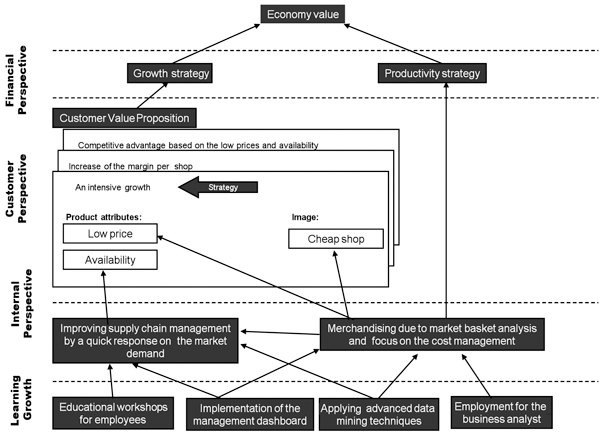

Case Study 6.1 shows a strategic map for a chain store.

Table 6.1. Information Capital

Source: Based on Kaplan and Norton (2004).

Case Study 6.1.

Here is a fragment of the strategy map for the chain store ALFA (see Figure 6.2), which was devised from the company’s strategy (see Case Study 1.1), which includes the following:

- From the perspective of learning and growth, implementation of the managerial dashboard and application of data-mining methods

- From the perspective of internal processes, improvement of logistics processes, merchandising optimization, and cost control

Figure 6.2. The ALFA chain store strategy map

Source: author.