6

THE POWER OF AUTOMATION: LEVERAGING

TECHNOLOGY TO REACH THE RICH LIFE

The real problem is not whether machines

think but whether men do.

—B. F. Skinner

The rich don't think about money.

Well, not all the time. When they do think about money, they contemplate it in a rich way. They think about maximizing their returns, reducing risk, paying low management fees, and building a financial ecosystem that works for them, day and night. The rich think about automating their money.

Successful business leaders and philosophers often opine on the acute benefits of habit and daily routine. Minting momentum in money management is no different. So far, you have learned about the massive benefits of building better financial habits. In this chapter, you are going to explore how to reap the harvest of cumulative advantage, focus on outsourcing your financial decisions, and learn to invest on a consistent basis.

These two modern pearls of the wealthy, routine and automation, have been have proven to be the gifts that keep on giving. Mastering the automation process and outsourcing the chores necessary to build wealth is a rich decision.

Once your financial ecosystem is constructed properly, you will be able to focus on calibrating your wealth-generating machine. Automating your finances is one of the easiest steps you can take to drastically change your financial future. It will provide you with the infrastructure to handle everything that you should already be doing without lifting a finger. The time has come to let the professionals work for you and leverage technology to accelerate your path to the rich life.

Master Your Rice

In the documentary Jiro Dreams of Sushi, eighty-five-year-old head chef Jiro Ono details out his daily routine, which he has been following for over forty years. His focus on routine has allowed him to relentlessly concentrate on perfecting his craft, one day at a time.1 Jiro passes this worldview on to his apprentices, who often have to spend years mastering how to cook the basics of sushi, like rice. This tireless dedication and pursuit of perfection has paid off. Jiro's sushi restaurant has become internationally recognized. Celebrity notables, such as former president Barack Obama, have visited Jiro's eight-seat restaurant in Tokyo for a taste of the world-famous sushi.

Jiro continually stresses the importance of sticking to a daily routine. In fact, he credits his success to that consistency, and if he finds himself falling out of that routine, he takes drastic measures to ensure he falls back into his daily cadence.

Although not all of us will become world-renowned chefs, Jiro's routine provides a relevant analogy: Success is bred in schedule. The consistency of routine allows the mind the necessary time for exploration. Whether you are trying to form a new habit or break an old one, your ability to create a good routine will define your success.

It is much the same with your finances. Most people haphazardly approach their money management. They watch month in and month out as their paychecks hit their bank accounts, only to find at the end of the month they have nothing left. To give success a chance, this undisciplined approach must stop.

You cannot expect to manage the growth of your money well if you have no cadence to your approach. In the past decade, there has been an explosion of growth in innovative companies whose core mission is to help people solve the problem. This movement has given individuals the power to automate their finances and increase their chances of long-term success. Leveraging the power of technology has never been easier. In this chapter, you are going to learn how to practice good financial habits, keep to a routine, and in the end, master your rice.

The Triple D

Automating your financial decisions gives you the advantage of maintaining a consistent approach. By doing this, you protect yourself against decision fatigue. Continuously deciding when to pay off your debt, how much money to invest, the percent to allocate to each fund, or whether to invest at all erodes your willpower.

Human behavior is a funny thing; we can change our habits virtually overnight by creating the appropriate framework for success. The best way to execute creating a money system that works is to implement what I call the Triple D: design, delegate, and defer.

Design

The first step to set up your money flow system is to design its overall structure. You need to have a handle on your accounts—savings, credit cards, student loans, and retirement. This provides the scaffolding to construct the perfect system.

Once you have a clear understanding of where you want your money to go each month, you can begin designing your system to reach your short-term and long-term goals. For example, if you are going to save 10 percent of your take-home pay, then construct an automatic deposit of 10 percent from your paycheck into a savings or investment account.

Delegate

Once you have designed your money flow system, you need to become comfortable with delegating responsibility. There is no need to check your savings or investment account each day, each month, or even each year. Instead, have faith in the system that you constructed in the design step and delegate the responsibility of moving money around to your system. Outsource that headache. This will free your mind of worry and reduce the manual errors caused by human interaction. Let the machines do the heavy lifting.

Defer

Now that you have designed a beautiful money flow system and delegated virtually all thoughts of monthly management, the final step is to defer as much of your income as possible to the future. The wonder of money flow systems is that they trick you psychologically. Embrace this hack.

For example, if you make $5,000 per month and designate $1,500 to your 401(k), $1,000 toward automated rent payments, $300 to your slush fund, $100 to your emergency fund, and $100 to your vacation fund, you are left with $2,000 of guilt-free spending money for the month. Enjoy this money and spend it passionately.

Create a Flowchart to Help You Dominate

As a budding CPA, there is no way to get around taking some rather dry accounting classes. The more mundane courses revolved around internal controls and flowcharts. During these lectures, it was all I could do to keep my eyes open. They consisted of monotone professors mapping out detailed business processes and converting those processes into visual schematics. These classes were artwork for accountants. As you can imagine, this was nothing short of terrible. Flowcharts were my least favorite topic.

But that all changed one day when I made the connection between automating my finances and the value of flowcharts. From that point, I understood the beauty of a well-crafted and efficient flowchart.

You too can appreciate this beauty by mapping out your monthly money flow chart. The process begins with a holistic view of all of your sources of income, checking accounts, savings accounts, retirement accounts, and savings goals. Luckily, all you have to do is flip back to Chapter 3 and take a look at your passion budget. This will provide you with everything you need to get started.

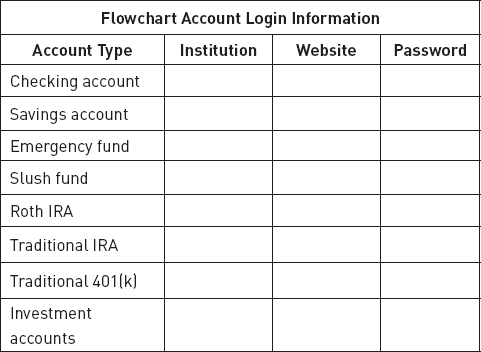

Depending on where you are in your money makeover, the following list can give you a good idea of the accounts you should have set up.

- Checking account

- Savings account

- Emergency fund

- Slush fund

- Roth IRA

- Traditional IRA

- Traditional 401(k)

- Investment account

Open these in succession of your money makeover progress. Once you have your accounts set up, you can get started designing your money flow system. This is the fun part.

List Your Accounts

One of the first questions you should ask yourself when getting your finances in order is: Where is all of my money? You should be able to recite an itemized list of your accounts and fund balances. This should include all of your checking accounts, savings accounts, emergency fund, Roth IRA, Traditional IRA, and Traditional 401(k). After all of your money is accounted for, the next task is to gather all of the information in one area. Keeping it consolidated makes for easy maintenance.

Download the following spreadsheet at MillennialMoneyMakeover.com to help with organization during this process.

It is surprising how consolidating all of your financial information improves your spirit. You will find that reducing clutter and streamlining accounts is great for your long-term well-being. This newly constructed repository acts as the heart of your centralized operating system.

Now that all of your login information is in one location, you can concentrate on trying to reduce the number of institutions holding your money. Personally, I have my Roth IRA, Traditional IRA, employee stock, and investment accounts all at one brokerage. This helps me coordinate all of my retirement and investment accounts in one place and reduces the headache of managing multiple logins. Another advantage is that it allows me to see all of my money in one spot, which always makes me smile.

Connect the Dots

Having all of your accounts aggregate in one location is helpful, but only if you use this efficiency to your advantage. To do this, you need to link your checking account to the rest of your financial structure in the correct order. This is where overall design meets delegation.

Linking your accounts to your financial infrastructure should be done in the proper order, mirroring your makeover progression. Most payment processing systems give you the ability to link your paycheck to multiple accounts. Let's review how to set up each of the five funds flow.

Link Your Checking to Your Credit Card and Student Loans

If you have debt, the first step is to link your credit cards to your checking account. You can do this by logging into your credit card's website and scheduling an automatic monthly payment. If you are trying to pay off credit card debt aggressively, make the automatic payments in your “stretch zone.” To ensure you don't incur overdraft fees, scheduled your payments for one or two days after your paycheck hits your checking account.

If you have student loans to pay off, the concept is the same. Schedule automatic payments from your checking account. Put as much as you can toward these balances. You will thank yourself later for being aggressive today.

Link Your Checking to Your Emergency Fund

Accidents, injuries, and layoffs are an inevitable part of life. Money makeover graduates hedge against this reality. An excellent way to avoid financial submersion after an emergency is to plan for the crisis now. That is where your $3,000 emergency fund from Chapter 5 comes into play.

After you are debt free, you will start contributing regularly to your emergency fund, which you can set up at your bank. This account should be connected to your checking account and will be the holding spot for your emergency fund. Your goal should be to pad this account regularly to prepare for the unexpected. Once you surpass the recommended $3,000 in your emergency fund, you can continue to make small contributions.

Link Your Checking to Your Slush Fund Account

When your money flow system is ready, you can link your checking account to a new savings account. This account is in addition to your emergency fund account and should be at a separate institution than your checking and emergency fund. This will ensure you don't raid this account in a moment of weakness.

Once you set up this new account, make sure that your slush fund and checking account are linked to one other, can perform transfers for no fee, and have a low minimum balance threshold. To make sure your idle cash is garnering some momentum find savings accounts with high annual percentage yields (APYs).

The power of linking these accounts comes when you want to schedule automatic transfers and manage your cash flow. Your goal with this account is to reach a monthly expense covered ratio between 3 and 6 (refer to Chapter 5). Once you meet this goal, it will be time to start investing the extra cash.

Link Your Checking to Your Retirement Funds

Once you have set up your Roth IRA, Traditional IRA, Traditional 401(k), and investment accounts, the next step is to start making healthy contributions. Don't fall into the trap of thinking that you don't need to set up these accounts because you can't start saving for retirement. Even if you are only putting away $100 a month, it is still better than nothing.

Construct an automatic deposit from your paycheck to these accounts. Most payroll providers have this capability and can make real-time deductions. Remember to make them before money gets routed to your checking account. This is essential when saving for retirement. If you don't see the money hit your checking account, you won't be tempted to spend it.

Link Your Checking to Your Happy Money

This is by far everyone's favorite account. Your happy money account is your savings account for that upcoming trip, vacation, or wedding that you are preparing for. This account is for what you daydream about at work.

To achieve this, set up a checking account and name it something fun. Then, allocate money to the account based off of your goals. This happy money account comes last because you should always focus on making sure your foundation is cemented—no debt, cash for emergencies, and retirement savings—before going on vacation. That way you can enjoy it stress free.

Percentage Allocation

Once you know what your fully constructed money flow system will look like, you can focus on determining the percentage of income you want transported to each account. Refer back to Chapter 3 during which you built your passion budget. What percentage of your income did you set aside for paying off credit cards, student loans, savings, or happy spending? Let's discuss three common scenarios with benchmarked goals for allocating your expenses. Download a blank version at MillennialMoneyMakeover.com to record your own plan.

The milestone you are on in your money makeover will determine which plan is right for you. For example, if you have $7,000 in credit card debt to repay, then begin with the credit card repayment plan. Are you saddled with annoying student loans? Then concentrate your efforts on the student loan repayment plan. Once you are debt free, turn your attention to the accumulation plan. This will help you build as much wealth as possible. Be aggressive and be bold enough in the beginning so that you can pull yourself back later.

Once you set up all of your accounts and start to link your income accounts to your savings account, the proportion of benefit to effort will lean in your favor. In other words, if you concentrate on setting up your accounts right the first time, you will reap the tremendous reward of automation. The following diagram takes a look at an example of a fully constructed money flow system.

Now that you have your financial ecosystem running in synchronization, it is time to focus on growing the nest egg that you started in Chapter 5. Once you have accumulated enough hard-earned cash to fully fund an emergency fund and slush fund, it is time to put any extra savings to work. The world of investing can be confusing, but there are professionals here to help.

The Rise of Robo-Advisors

In our modern economy, the use of technology is ubiquitous. From leveraging the latest software to making businesses run more efficiently to harnessing the power of robotics in the surgery room, the benefits gained from the historic advancement in technology over the past several decades have been tremendous. The next frontier for machine learning and algorithms lies in the FinTech, or financial technology, community and has the capacity to disrupt the entire financial advice and wealth management industries.

Human financial advisors have long been the conduit for receiving sophisticated, albeit expensive, financial advice. In recent years, human financial advisors have leveraged robo-advisors to deliver on client expectations but only behind the scenes. Robo-advisors—a class of financial advisors that provides automated financial services online by using software programs and algorithms to provide financial advice and investment management services—were commonly used among human financial advisors who were juggling large books of business and using robo-advisors to reduce their workload.2

In the wake of the great recession, robo-advisors finally wheeled out from behind the desk and plugged into the mainstream financial services community. In 2008, robo-advisors were delivered straight to consumers with a lack of human intermediates, and the response has been unprecedented. But this acceptance was a long time coming.

During the early 2000s, there was shift in online consumer behavior. Consumers were becoming remarkably familiar with the Internet, and its proliferation into our economy largely changed the way we conduct business, interact socially, learn new information, and manage money. Digitally native Millennials helped spur the trend in how consumers share personal information online and the reduced the previous anxiety around divulging private information to online businesses. As a result, Millennials have a propensity to share personal information—age, location, profession, salary, and financial goals—if they believe they will receive a superior product or service in return. In fact, 57 percent of Millennials are prepared to share their detailed savings plans and targets with others if they perceive that doing so would offer a more tailored approach to reaching their financial goals.3 Queue the propagation of support for robo-advisors in the investment community.

Silicon Valley woke up to this changing trend in 2006 with the success of Mint, an online semi-automated personal finance management business. In 2009, Aaron Patzer, the founder of Mint, sold his company to Intuit for $170 million and provided the necessary proof of concept to investors and entrepreneurs.4 Robo-advising and the digital age of investing were here to stay.

After robo-advising crossed into the collective mainstream consumer consciousness as a viable alternative to human financial advisors, a significant industry shift began to take place. New companies like Betterment, which made a splashing debut at TechCrunch Disrupt in 2008, began to pave the way for the robo-advising industry as they saw a massive opportunity in the marketplace to make investing simple. Jon Stein, the founder of Betterment, says he started his company to “tell you how much to invest and manage your money for you, all throughout your life, in a way that gives you better outcomes. We do it all so that you don't have to.”5 As the market opportunity became clear, more established financial services players, like Vanguard and Charles Schwab, began to pivot to offer this newly desired service. Since then, the flood of assets under management into robo-advising companies has been unprecedented.

In the early days, robo-advisors helped retail investors with automated asset allocation and portfolio management. And as technology improved, so too has the flood of competition to democratize financial services previously only offered to the rich. Elite services such as tax-loss harvesting, detailed planning for college savings, and cash-flow management are now available at scale to consumers for a fraction of their former cost.

The case for using robo-advisors is garnering massive support as the benefits that such technologies provide to young investors, and those looking to get their financial house in order, continue to surge. Additionally, advocates point out that this technology offers superior advantages from the traditional “Do It Yourself” investment approach.6 Millennials are taking note by augmenting robo-advice with conventional human interaction, which seems to be a successful strategy for improving their financial position.

As the advancement in wealth management software continues, the incremental progress will lead to an automating of the financial services industry. There are now tremendous benefits to using robo-advisors, several of which we will examine in the next section. As these financial services scale, costs will continue to decrease, and you will have information previously reserved for the rich right at your fingertips.

Four Reasons You Should Use Robo-Advising

Robo-advising is the wave of the future in money management. The financial management industry is scrambling to keep up with the flood of money pouring into this segment of the market, as investors are placing their money on technological improvements in a historically opaque money management industry. The old gatekeepers are soon to be ousted by a more refined, technologically advanced, and appealing way of managing money.

A recent study by consulting firm Deloitte estimated that “assets under automated management” in the United States will grow from the present $300 billion to a staggering $5–$7 trillion by 2025.7 This growth would represent between 10 and 15 percent of the total retail financial assets under management. Here are four reasons many investors, Millennials among them, are clamoring toward this new wave of money management—and why you might be drawn to it too.

1. Ease of Use

Technology is ubiquitous in young investors' daily lives. Millennials are plugged into the digital world. It is no surprise that the traditional means of finding a financial advisor seems outdated to this cohort.

Recognizing this market opportunity, investment companies have started to offer robo-advising, which is an automated way investment platforms use algorithms to allocate, invest, and manage investors' funds. Robo-advising takes the inefficiencies of human interaction out of the equation and leverages investors' risk appetite with technology to offer a robust investing strategy.

Companies that use robo-advising have made the process extremely user friendly, increasing its overall appeal. To get started, potential investors can simply visit a website and fill out an automated sign-up form. Once investors complete the onboarding phase, they can begin investing and regularly check in on their investment performance. Additionally, many robo-advisors offer investors a transparent and easily accessible investment management portal, which includes analytics, fund performance, transparent fee schedules, and portfolio allocation.

2. Lower Management Fees

Robo-advisors are offering this innovative service for a fraction of the traditional investment management cost. Historically, investment management fees are made off a portion of assets under management, or AUM. These fees usually ranged from 1 to 2 percent of AUM and were meant to compensate the investment manager for their analysis, insights, trades, and overall market advice. Robo-advisors have slashed these fees.

Fees for robo-advising range well below 1 percent of AUM, typically hovering around 0.50 percent, or four times lower than the traditional means of investment management.8 Lower investment fees matter because they can have a material impact on your investment performance over the long haul.

3. Automated Investment Process

Another major attraction of robo-advisors is that the investment process is automated. This allows investors to access benefits that were previously only utilized by the wealthy. Two main strategies automated in robo-advising are automatic rebalancing and tax-loss harvesting.9

Automatic rebalancing is the process of dynamically realigning the weight of a portfolio of investments. As an investor, you choose your desired level of risk allocation, which is then baked into your portfolio by spreading your investments among different risk categories to meet your original risk appetite. When the market fluctuates, your level of investment performance changes with it. The rebalancing process ensures that your portfolio retains your original risk allocation, which could mean selling overexposed areas like stock and acquiring less risky investments like bonds.

Tax-loss harvesting is another significant advantage to robo-advising. This process occurs when an investment is sold at a loss. Those losses are “harvested,” or kept to offset future taxable gains. This process optimizes your portfolio's return. Tax-loss harvesting, along with tax advantaged investment strategies, have the ability to add as much as 1 percent a year in value to your portfolio. Accumulated over your investment life, this can boost your overall returns, letting you keep more of your money.

The automated process of investing and the advantages of digital advising have led many investors to question the value of traditional financial advisors. With this decline in value perception, there appears to be a shift to commoditize financial planning.10 This means Millennials will quickly gain access to sophisticated investing technology, which will help them invest more, early, and often.

4. Lower Balances and Maintenance

Robo-advising is perfect for a certain type of investor: one who has a demanding career or family life and doesn't have the time to focus on money management. Additionally, it allows investors to outsource the bulk of the money management process for a fraction of the traditional cost.

For young investors, robo-advisors offer another carrot: low minimum account balances. A traditional investment advisor can require a high minimum balance to get started, some as high as $200,000, leaving many potential clients behind. That is where robo-advising has gained ground. Some robo-advisors require no minimums, while others offer professional investment management on balances of $5,000 or more.11

Investing means you are winning. Being able to allocate your money to a robo-advisor can free an investor's time to do other things. This outsourcing allows investors to maintain piece of mind and put other people to work, no matter how much you have to invest.

Millennials' attitude toward technology and investing seems to create a perfect scenario for robo-advising. However, robo-advising is not right for everyone. Do your research and investigate which robo-advising companies are right for you, if any.

For those looking to invest hard-earned cash after they have built their emergency fund and slush fund, robo-advisors or a more traditional route can accelerate your wealth creation. By learning how to get both investment professionals and technology on your side, you are beginning to act like the wealthy.

Modern Money Management

Whereas the shift in demand to robo-advising is certainly garnering tremendous attention from industry experts, many companies are honing in on the strategy of the future: a hybrid approach of robo-advisors and personal investment management. Investment managers and advisors know that they need more than just algorithms to win over Millennials. This intersection, where algorithmic investing meshes with human intellect, is a terrific place for you to thrive. This is the modern approach to money management.

Personal interaction, or the human side of the business, is still a critical part in the investment process, and it gives the hybrid model a tremendous advantage. The human touch to investing can be powerful for your portfolio because financial advisors and investment experts can offer a catered approach to help you determine your risk appetite, pick specific investments, assist in retirement planning, resolve nuanced tax and estate planning, and allow you to implement a holistic and synchronized approach in order for you to achieve your long-term goals.

Millennials are highly inquisitive when it comes to investing and wealth generation. Knowing that they have someone (literally) on their side allows for a more confident and coordinated investment philosophy. It alleviates the fear of the unknown. Investment professionals are lining up in droves to help Millennials manage their money because Millennials are now entering a period of reaching many of life's milestones. Millennials also stand as benefactors to a historic shift in wealth during the next several decades.

Professionalizing your approach now can be the catalyst you need for maximizing your wealth accumulation. Get the professionals on your side early to help bolster your returns. The investment community is awash with talented individuals waiting to help accelerate your path to the rich life.

![]()

Action Items

Hopefully, this chapter taught you the value of automating your finances and outsourcing the decision of money management. By leveraging technology to accelerate your growth, learning how to build the perfect money flow system, and working with investment professionals, you have reached the last milestone of your money makeover.

When implementing these steps, remember the following items:

- Recognize that mastering your money takes time, practice, and intention.

- Design your financial ecosystem for success.

- Implement your automated money flow system.

- Get professionals and technology on your side.

- Win the long game.

Your money makeover is now complete. You have received the tools for financial success. But this book ends where it began. Knowing the path to complete the money makeover is only half the battle. The challenge and decision is yours alone. It is up to you to act, change your financial life, and keep momentum on your side. Continue your progress and secure the rich life. Do not wait. Do it now.

Welcome to your financial awakening.