Designing the Enterprise-Level Portfolio Management System

2.3 Doing the Financial Calculations

2.5 Dealing With Strategic Changes

Alice: What road shall I take?

Cheshire cat: Where are you going?

Alice: I don’t know

Cheshire cat: Then any road will do!

—From Alice in Wonderland, by Lewis Carroll

Now that the organization is ready to accept change, it’s time to decide what types of projects will be part of the portfolio and how to select and prioritize them. We need to determine this before we can design the system. To do it, we need continuous feedback from the decision makers so that we can select the right filters and prioritize the projects properly to support strategy just as they would do if these decision makers were perfectly rational and objective.

This is not quite as simple as it sounds for two reasons. The first reason is that many of the executives will not agree with each other on what is most important. People at this level are used to having their decisions carried out, and your EPMS will remove their ability to pick and choose their pet projects. There will be a lot of discussion about the “right” filters to use so that pet projects are approved as well as discussions about excluding projects from the system that don’t make the cut but are politically important.

We can accommodate this by developing an approach that handles different types of projects differently. We’ll look at the possible categories of projects and decide how much to fund each category.

The second reason is that the strategic goals will change over time and the portfolio has to continually adapt to the changes, so the EPMS must be designed to accommodate changes. It is very rare for decision makers to kill projects even if they no longer make sense. The reasons for keeping dead projects walking is purely emotional. The EPMS will remove the emotional buy-in and more quickly kill projects that are no longer needed and tie up resources that could be better used elsewhere. The second reason is more challenging, but its impacts can be mitigated by developing a flexible approach to the selection process.

Why should we worry about the requirements of the filters? Because the filtering criteria we will build into the EPMS reflect the values of the executive level. They want to select the projects that will provided the greatest value to the organization and reject the projects that provide little value.

But, value is relative. What is highly valued to one person may be a low-value item to another. The executives will have to determine what value means before you can create the filters. The following Table 2.11 shows the different types of value that are important to the executive level:

Table 2.1 Values important to executives

Value Type |

Benefit definition Financial |

Examples |

||

Financial |

Nonfinancial |

|||

Tangible |

Defined |

Value can be predicted with certainty. |

Cost reduction |

Less steps in the process |

Expected |

Value can be forecast based on historical data with high degree of confidence. |

Increase in sales |

Fulfilling the tasks more rapidly |

|

Anticipated |

Benefits are anticipated, but its value cannot be forecasted with certainty. |

Lower insurance premiums |

Higher customer satisfaction |

|

Intangible |

Can be anticipated but not substantiated. Proxy (indirect) measures can be used to verify their realization. |

Image enhancement. (evidence: higher number of positive comments in the press) |

||

We’ll talk about requirements in more detail in the next chapter, but we’ll discuss them here at a high level to get you started thinking about them.

There are two major cautions here:

First, DO NOT get too detailed. The EPMS should not cure cancer or bring about world peace. Keep it simple or you will get so stuck in trying to do everything that you will accomplish nothing. Because your company’s infrastructure, applications, and projects have become so intertwined, you do what seems natural: You try to untangle the mess at the root.

A lot of companies have tried the same kind of “detailed, bottom-up” approach to project and portfolio management. Very few are successful. As Gartner analysts explained:2

[many early customers] believed they must implement PPM* software automation at painful levels of detail (such as task- and assignment-level time reporting).... Unfortunately, many initial PPM software investments failed when this bottom-up approach to project portfolio management was chosen, due mainly to the high levels of complexity, low levels of adoption and extensive organization change management required to get the entire execution side of a project organization using the same system.

In other words, a “bottom-up” effort at PPM gets mired in the tactical details, where many hands touch projects and many infrastructure components collide, and where change is, therefore, difficult to enforce.

Second, do not include “exploration” projects in here. Exploration projects are those that lie somewhere between pure research and detailed development. This projects have a history of being high risk with a low probability of successful financial return. By contrast, the small percentage that are financially successful tend to be very successful, with large benefits from new product development and new markets. Any normal “filtering” process is much more likely to kill these projects than to approve them3.

Finally, there are also operational aspects that need to be included during the design effort. These are covered in Step 3.

2.1.1 You Need Requirements

Is it important to have the requirements before you start? Only if you want to be successful and give the organization something it will actually use. In the implementation of major software systems such as Enterprise Resource Planning (ERP) applications, there is an extremely high failure rate due to new business processes being put in place but nobody using it. (Recall our section on implementing changes in an organization). Kimberly–Clark ($14 billion, 64,000 employees worldwide) installed SAP. After one week, they had fewer than 30 problems reported worldwide. Their 24/7 customer support center for the project was cut back after only two days due to the low volume of problems. Why? Because their strong requirements traceability process ensured all requirements were captured and managed. The project manager understood what the need for the new system was and satisfied those needs.

We’re going to go into more detail in requirements in the next section.

Story

During one ERP audit at a US Government agency the author was leading, the audit team was asking questions about how the requirements for the new system were determined and managed. The different agencies involved each set up their own requirements teams to determine what their specific needs were and created cross-agency teams to determine common requirements such as security and access. The implementation team captured and tracked these requirements in the tool Rational Rose. They got good audit points for their disciplined approach

(Unfortunately, when we asked for a current copy of the requirements for our records, we were told that the entire requirements database was stored on one contractor’s hard drive and the hard drive had crashed two weeks before. All of the data was lost because there was no digital backup. The only data available was on the last printout.)

Requirements gathering is NOT documenting what the users want, because they often do not know. Requirements gathering IS helping the users determine what they need and want.

If you cannot identify what people expect, then you cannot deliver it. In this situation, the project should be shut down immediately, rather than wasting more time and effort. A significant cause of the high failure rate of technology projects is that they cannot deliver a final product that people will actually use.

Law of Project Management |

Users will start to change the requirements as soon as they understand what it is they originally asked for. |

As just stated, this is the process of gathering and analyzing the business requirements. We’re doing this for the business, not just to implement something new. So, our primary responsibility is to identify what those needs and expectations are and plan for how we can satisfy them.

Let’s start out by defining what a requirement is. For our purposes a requirement is a specific statement of a need, sufficiently detailed that there is no misunderstanding about what is being said. Business requirements are very high level and, from the viewpoint of an engineer or a programmer, are very vague and unspecific. These high-level requirements are then taken down into much greater levels of detail in a process called requirements decomposition to the point where the technical people can design solutions to satisfy them.

When most people think about requirements, they focus on what the end product is supposed to be or to do. Is it an e-commerce website? A new car or plane? A hospital? These requirements are called functional requirements. They are directly tied to the goal of the final product. But, there are many other types of requirements. In most projects, these nonfunctional requirements will be the majority of the requirements you have to identify and manage.

At the highest level, we have the business needs. We obtain these in a variety of methods that we’ll talk about shortly. The next level down is where we break out the functional requirements (what is it that this end product should do) and a variety of nonfunctional requirements:

“ilities”—Maintainability, reliability, upgradability, sustainability, and so on. For the EPMS, we really don’t care about these, except as they apply to any tools we might buy or build.

Performance—How well does this new system perform? If I send a request for information, how fast and how accurately does it respond to my request? Is the system available 24/7, or are there planned outages for maintenance? This is a really critical category for the users.

Privacy and security—How secure is the data? Are there levels of security so that different users have different levels of access? Are there built-in privacy protections?

Usability—This is the interface between the users and the system itself. While many developers consider this a low-priority requirement, the reality is that most complex systems (such as ERP systems) fail because the users won’t use the system once it is installed. It is actually a very high-priority requirement to make the system easy to use.

Health and safety—For the purposes of defining the EPMS requirements, we don’t have to worry about this category.

Environmental—Another category we won’t worry about for our EPMS. It will not have any environmental impact.

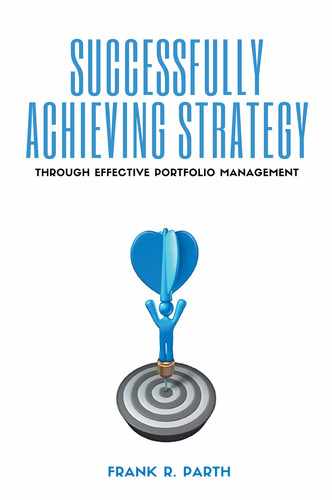

For the PMO itself, the requirements tree might look something like this:

These are the requirements that you must discover through the requirements gathering processes we will talk about later. Once you have a good handle on these, now you can start designing the system and assessing any commercial tools you will purchase. Having collected this level of requirements, now you can decompose them into more details and document the more detailed and more technical requirements:

• Specific business processes

• Detailed architecture and technical design requirements

• Integration and Test (I&T) needs

• Interface requirements (internal to the EPMS and between the EPMS and the organization)

• Implementation requirements showing how you’re going to put the system into operations

Figure 2.1-1 Requirements decomposition tree

And then finally, how are you going to document the system? How are people going to operate it? How are you going to train them in the system and in their new jobs?

Notice that there are requirements here in the form of constraints. When designing the new EPMS, you must take into account the existing processes for selecting and prioritizing projects. If the new EPMS gives radically different results than the existing system, it will be dismissed as useless. Organizational constraints, such as the communications culture or resource limitations, also need to be included in the design. The organizational structure is another area to consider. An EPMS designed for a fully projectized organization is very different than one in a purely functional organization.

Each EPMS must be designed with regard to the existing organization, its goals, its culture, and its constraints. This varies by industry and by the specific organization. Each is different. Let’s look at the large construction/engineering industry for example. The projects owners engage in are generally high value (therefore very risky organizationally) and long term (increasing the risks). What are the evaluation criteria and constraints they typically concern themselves with in selecting which projects to accept?4:

Financial

• Life cycle return on investment (ROI)

• Return on assets employed

• Net present value of cash flows (NPV)

• Payback period

• Total capital expenditures

• Product/project gross margins

Market

• Market share

• Market growth and duration

• Period of profitable production product flexibility

• Customer impacts

Strategic

• Flexibility

• Resiliency

• Contribution to overall portfolio performance

• Enablement of Strategic Business Objective (SBO) achievement

• Enablement of other portfolio projects

• Critical resource utilization

Sustainability or triple bottom-line-focused criteria

• Economic

Social

• Community impacts

• Capacity building

• New industry/business creation

• Workforce impacts

• Environmental, health and safety

• Airborne emissions

• Water consumption

• Discharge water quality

• Environmental degradation

• Worker health and safety

• Public health and safety

Risk

• Economic or market uncertainties

• Other event risks

• Financing uncertainties

• Cost uncertainties

• Schedule uncertainties

• Labor risks

• Stakeholder risks

• Sovereign and legislative risks

• Political risks

• Technology risks

• Intellectual property risks

• Business model risks

• Project execution risks

You can see why the BOGGSAT approach mentioned in the Preface would have severe limitations in selecting which projects to do when you take into account all of the constraints and our limited decision-making capabilities.

2.1.2 Requirement Priorities

Once you have gathered the needs of upper management, you take the answers you’re given and compile and analyze them. Did they give you needs that you can satisfy? Do any of the needs given by different managers contradict needs from other managers? Are there needs that are duplicated? Once you have removed the duplicates and resolved any conflicts, meet as a group with the managers again and present the list of requirements for their approval.

At this point, you will start prioritizing the requirements. They will want everything they told you, but almost never is there enough time and resources to do everything. So, the requirements need to be prioritized into:

Mandatory

A mandatory requirement is an essential feature of the EPMS. Failure to implement the requirement means the system will not meet management’s needs. All mandatory requirements must be implemented in the first planned release.

Highly Desirable

A highly desirable requirement describes a requirement that is important to the effectiveness and efficiency of the system. The missing features cannot easily be provided by software or processes.

Lack of inclusion of an important feature may affect management’s satisfaction with the EPMS, but the planned release will not be delayed due to lack of any highly desirable feature. Think about implementing these in the first upgrade if you can’t do them now.

Desirable

A desirable requirement describes a management need that, if implemented, will have a negligible impact on the functionality of the system.

Desirable requirements would be more likely than highly desirable requirements to be deferred or deleted if time or resources become scarce.

Optional

An optional requirement describes a requirement or features that will be used less frequently, or for which reasonably efficient workarounds can be achieved. The planned release will not be delayed due to lack of an optional priority feature. It’s a “nice to have” feature, rather than something that is absolutely needed.

Some consultants use the simple “MoSCoW” rule. The acronym stands for Must, Should, Could, and Would:

• M—Must complete this requirement to meet management’s needs

• S—Should do this requirement if possible, but project success does not rely on it

• C—Could do this requirement if it does not affect anything else on the project

• W—Would like to have this requirement later, but cannot be done now

Priorities must be determined through constant coordination with the top-level decision makers. It is their priorities that have to be built into the EPMS. But, they must be made to understand that there are compromises that will be necessary.

If management tells you that all their requirements are equally important, push back and ask them what could be cut out if there are schedule problems or cost over-runs? As a general guideline, no more than 25 percent of the requirements should be mandatory. These are the core requirements. These are the ones you concentrate your resources on implementing.

One common approach, when you have too many requirements to satisfy with the resources and schedule you have, is to develop the EPMS in multiple stages. This is a highly recommended approach. Satisfy the primary requirements first, then once the basis of the EPMS is implemented, develop a follow-on project to satisfy remaining requirements. This has the benefit of providing a more useful set of requirements during the follow-on project because people now can see what they got in the first rollout.

2.1.3 Requirements Documentation and Management

Law of Project Management |

Always document your requirements, a verbal requirement isn’t worth the paper it’s written on. |

Requirements must be documented. This is not negotiable. Never accept a verbal request for a requirement or a change to a requirement. If you do, in six months, what you remember will be different than what the requestor remembers. And, because they own the requirements, not you, you will have implemented the wrong requirement. If a stakeholder meets you in the hallway and asks you for a new requirement, always follow up the conversation with an e-mail documenting what you heard. Even better, ask them to fill out a requirements request sheet. That way it is in their own words.

Story

At one US Federal government organization the author led an audit team doing an independent review of an ERP package that was being installed. When interviewing the CIO the question was asked: “Do you accept verbal requirements?” The CIO emphatically said no, only written requirements were accepted by the project. The next day the author interviewed the project manager and asked the same question “Do you accept verbal requirements?” The project manager’s reply? “Sure, we get them all the time. No problem.”

There is one additional advantage to having stakeholders fill out a request sheet if they want to add or to change a requirement. Software history shows that as much as 50 percent of requirements requests go away if they have to fill out a document to request it!

It is best not to put all the requirements into one document. There should be a business requirements document that captures the pure business-level requirements (functional, performance, and maybe some other requirements). This document is best developed as a joint effort between the project manager (or project team members) and Business Analysts. This document is signed by upper management before any architecture or design work is done.

For each requirement, managing it requires the following information be captured and documented:

• Type of requirement—functional, performance, security, and so on

• Design implementations—in hardware, software, processes

• Priority of the requirement—mandatory, highly desirable, or desirable

• Source of the requirement—who gave you the requirement (in case you ever need clarification of it)

• What change requests have been opened against it

• Which test cases test it

• What is the current status—implemented, in process, not started

• Which phase it will be implemented in (for a multiphase implementation)

This can be done very simply in a requirements management tool, a small database, or even in a spreadsheet. Note that documenting and maintaining this will require some administrative resources. This tracking can be done in a Requirements Traceability Matrix that captures not only this information but in which the requirements are numbered in such a way it is easy to identify which requirements have been decomposed from higher-level requirements.

Requirements are critically important, because everything else in the project is based on capturing, managing, and understanding them. We’ll talk more about requirements for our EPM system in the next step.

Step 2.2 Design Considerations

In designing the EPMS, we will take into consideration all work in the organization, not just projects in specific areas such as information technology (IT). Why? Because there is work outside of projects that can significantly impact project success. Blichfeldt et al.5 have shown there is an impact due to projects that are outside the EPMS:

Although companies manage project portfolios concordantly with project portfolio theory, they may experience problems in the form of delayed projects, resource struggles, stress, and a lack of overview. Based on a research project compromised of 128 in-depth interviews in 30 companies, we propose that a key reason why companies do not do well in relation to project portfolio management (PPM) is that PPM often only covers a subset of on-going projects, while projects that are not subject to PPM tie up resources that initially were dedicated to PPM projects. We address and discuss the dilemma of wanting to include all projects in PPM, and aiming at keeping the resource and cognitive burden of doing PPM at a reasonable level.

There are going to be a lot of different considerations that you will take into account as you design the EPMS. One of the major design influences is the type, or types, of project that the new system will be dealing with. Once we understand the types of projects, we can decide on the filtering criteria to filter in all possible project types and the scoring system to select the most beneficial projects within the different types.

Obviously, not all projects are the same or even the same type. This is important because different types of projects will require different justifications and filters that we need to build into our system. In order to obtain the largest number of beneficial projects across multiple parts of the organization, part of what we need to do is to balance out the different asset classes, from short-term IT projects to expensive, strategic capital expenditure (CAPEX) projects.

In Section 2.2, we’re going to cover some of the core topics in the design of the EPMS—how to balance out the different classes, types of projects, criteria for filtering them, and finally, determining how to score them. We will go into the detailed design of the system in Chapter 3.

It is important to ensure that the portfolio is balanced among the different types of projects. According to Kendall and Rollins6,

Every organization has two constraints that limit how many projects can be active at any point in time. One is the amount of money the organization has or is willing to invest in change. The other is the organization’s strategic resources – the one most in demand across many projects or the most heavily loaded resource across most projects. This determines how many projects can be active at any point in time.

Figure 2.2-1 EPMS inputs

Each portfolio, whether at a business unit or at the top-level organization, should be reasonably well balanced to minimize risk. Some parts of the organization, such as the IT department, are going to have lower-level portfolios that are exclusively within one area. The larger organization should provide more overall balance to the portfolio.

By inputting the data required by the EPMS, you are expanding on the business case for each proposed project. One decision that must be made early in the selection effort is to determine whether the effort is worthwhile for every project. While this may sound strange because the whole purpose of the EPMS is to select projects, there may be circumstances where it may not be worthwhile.

If the project is below a certain dollar or effort amount, it may not be worthwhile to filter it through the EPMS. For projects under 100 hours, as an example, the overhead associated with the EPMS may not be worth the effort.

Other projects, such as those mandated by regulatory requirements, are guaranteed to be done regardless of the financial benefits. However, they should still be entered into the portfolio so that their risks and impacts to other projects can be identified.

Some projects are research-oriented projects that may, or may not, produce a marketable-able result. They take time and resources, but it is extremely challenging to schedule them or prioritize them. We will discuss these types of projects in more detail later. These are sometimes called innovation or exploration projects and can produce highly innovative new products. Despite their management challenges, they can be the most critically important for the organization’s future.

The categories of projects must be decided by management in the way that makes most sense for the organization. A software development company will select and prioritize projects that make the most sense from their business perspective. Other organizations will select different categories and priorities. The international mining company Anglo-American has created the following categories for their own projects as shown in the following table.

Table 2.2 Anglo-American project categories

Anglo definition |

Category |

Subcategory |

Description |

Major Project |

Expansion |

|

Material expansions or increase in production capacity |

Replacement |

|

Replacement of existing production capacity |

|

Stay in Business Project |

Replacement (of equipment) |

General replacement— simple |

Replacement of existing commodity equipment— single item as part of planned maintenance |

General replacement— complex |

Replacement of existing equipment/groups of commodity equipment across multiple sites as part of planned maintenance or potential failure |

||

General replacement— systems and plant |

Replacement of existing systems and plant that my involve multiple vendors and/or design and/or construction |

||

|

Safety risk |

Replacement of plant and equipment (including IT systems) that has failed or is proved to be about to fall and/or will materially impact safety |

|

Legal risk |

Replacement of plant and equipment (including IT systems) that is no longer legally complaint |

||

Business risk |

Replacement of plant and equipment (including IT systems) that has failed or is proved to be about to fail and will materially impact operations |

||

Business improvement |

Business improvement— plant and equipment |

New or replacement of plant and equipment with alternatives intended |

|

Business improvement— business processes |

Any nonoperational initiative intended |

||

IT projects |

IT system development |

IT system development |

Any IT initiative intended to improve business efficiency/effectiveness or achieve a strategic priority objective |

In order to minimize the influence of strong stakeholders who are primarily interested in advancing projects that benefit only their part of the organization, a questionnaire should be developed for each asset class that identifies and prioritize those projects that best support the overall organization. An example of such a questionnaire is shown in Appendix 2.2.

In business, assets are everything of value that is owned by an organization. The two major asset classes are tangible assets and intangible assets. Tangible assets are items such as financial assets and fixed assets. Financial assets include accounts receivable, bonds, stocks and cash, and other monetary items; fixed assets include such items as buildings and equipment.

Intangible assets are nonphysical resources and rights that have a value to the firm because they give the firm some kind of advantage in the marketplace. Examples of intangible assets are goodwill, copyrights, trademarks, and patents.

From a portfolio standpoint, we are interested in any project that needs to be funded and completed by the organization. Some of the projects are going to produce tangible assets such as new facilities or a new product for sale. Some of the projects are going to produce intangible assets such as a new IT infrastructure or business process improvements. All of them take time and resources.

Projects, regardless of what type of asset they produce, are part of the portfolio and must go through the project selection process. The only exceptions are mandatory projects that we will discuss later.

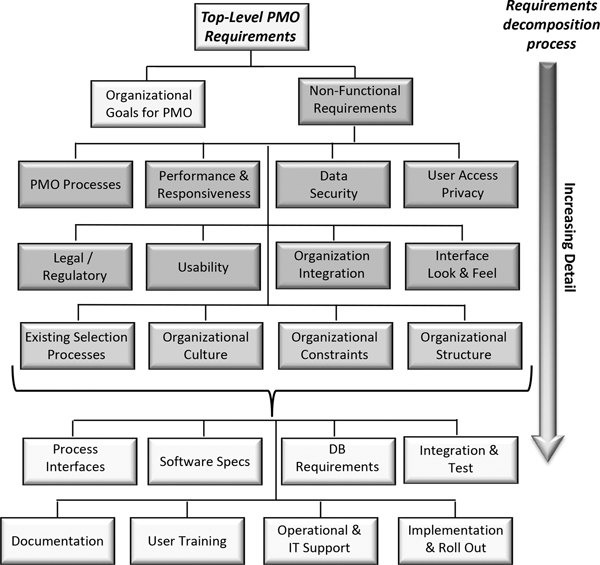

We are going to classify the universe of projects into four categories: infrastructure projects, operations-related projects, new product development (NPD) projects, and capital investment projects. There are other approaches to categorizing projects, and not all of these categories may apply to your particular organization. That’s alright. Select the categories that apply to you. Delete the others from the analysis, and add any new ones that are not covered by these. For example, the U.S. National Aeronautics and Space Administration’s (NASA) Jet Propulsion Laboratory (JPL) in California has five criteria for filtering projects7:

1. New capability

2. Maintaining existing capability

3. Innovation projects

4. Visionary projects

5. Compliance projects

The projects are reviewed on an annual basis and adjusted to meet organizational priorities. The distribution of JPL’s effort is shown here:

Figure 2.2-2 JPL’s project distribution

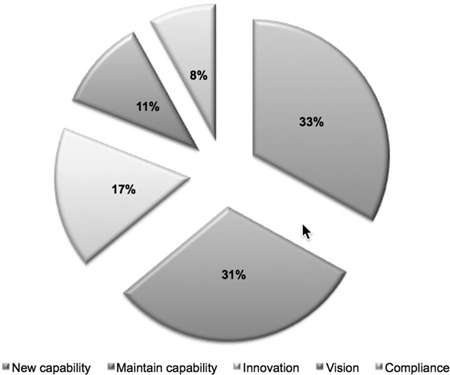

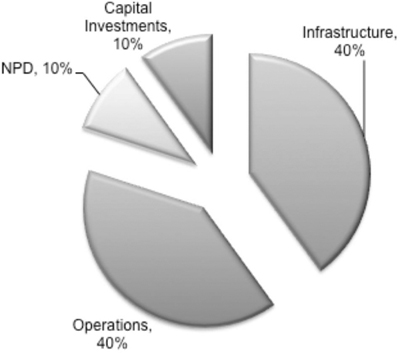

JPL is a government organization heavily devoted to research and engineering projects. For categories normal to private industry, let us look at four categories and draw them visually:

Figure 2.2-3 Business project categories

Infrastructure projects are crucial to the efficient running of the organization. This class includes both IT projects and non-IT projects, such as facility maintenance projects or equipment maintenance projects. For many organizations, the majority of infrastructure projects are IT projects. These are also the most likely to be challenged and to suffer scope creep, schedule slippage, and cost over-runs. We’ll talk more about all of these later.

Operational projects are projects for specific operational groups such as marketing, HR, or legal. Marketing projects can improve brand image and corporate visibility and have great potential benefits, but they tend to be high cost projects with “soft” benefits—benefits that are difficult to quantify. Human resource (HR) projects are lower cost and low risk, but may be mandated by regulation and will fall into the type of project we will later call “mandatory.”

Other classes of operational projects include business process improvement projects. These can be highly beneficial, but are also very risky due to impacts on how people work.

New product development (NPD) projects are those that produce a new product that the company can market. These are highly risky, with up to 90 percent of new products failing in the marketplace. But, they can also be highly rewarding, with the 10 percent of products that are commercially successful compensating for those that fail. This is an especially critical area for new technology-based firms (NTBFs)8, which tend to be entrepreneurial, do not have a long history of operational development, and tend to use project management techniques far more readily than old established organizations.

Projects for NPD follow the company’s NPD philosophy: first to market, fast follower, or low-cost leader. Companies that produce a brand-new product can obtain very high profits from it, but also face high development costs for a product that may not be successful. Companies that use a fast follower approach wait until a competitor comes out with a new product and waits to see if it is commercially successful, then comes out with a competitive product. Think of Apple’s iPod followed by Microsoft’s Zune.

Companies that utilize a low-cost leader approach wait until a product’s market matures, and then undercut everyone on price. This is low risk, but also highly competitive because many other companies will be doing the same thing. Companies that use this approach rarely add any new features, but are highly skilled at cost-cutting the manufacturing of products.

Capital investment (CAPEX) projects that those that cost a lot of money with no short-term payback. These are the projects that produce new manufacturing factories, new aluminum plants, or new oil refineries. They cannot be justified in the same way that an IT upgrade is justified. We’ll talk more about these later in this chapter.

2.2.2 Balancing Asset Classes and Capital Rationing

If every asset were equally important to the organization, the portfolio may be represented as shown in this figure:

Figure 2.2-4 Balanced portfolio

However, we know that no organization will ever have a completely balanced portfolio, except temporarily by accident. Upper management, when they are laying out the annual budgets, will emphasize those areas that support the organization’s strategic goals.

Removed from the following calculations are the money allocated for daily operations. In most organizations, the operations money will require the majority of the funds. These are funds that must be expended just to keep the organization going and are not available for projects. We’re going to take operational budgets out of any consideration and only concentrate on budgets allocated for project work.

All projects cost money and people, and there is a limited supply of both. Investments in projects are balanced out with investments in less risky financial instruments such as investing in certificates of deposit (CDs) or bonds. How the organization rations its capital is an activity that takes a lot of time and effort by the executives to ensure that the risks inherent in projects is balanced out by the more assured returns of safe investments. Part of capital rationing is also involved with just what types of projects the money should be spent on, the topic of much of this chapter.

The executives in the finance department are charged with spending the organization’s money in a way that provides the greatest benefit while balancing risk. If all financial decisions were left to the accountants, the money would be invested in savings accounts, Certificates of Deposit (CDs), and in safe financial investments. Rarely are these people comfortable in investing in projects whose outcome is uncertain and which have higher risks. Fortunately, the financial department is only one voice in how the organization allocates its financial resources. If it were left to the finance department, the organization would never create new products because there are safer places to put the money. Organizations that put too much of their money into “safe” investments eventually lose out to more innovative competitors.

The money needed for operations is highly dependent on the outside business environment and is, therefore, reactive to changes in that environment. In a growing economy, organizations put more money into growth and select more projects. In a downsizing economy, organizations pull money away from growth-related projects and use the money to improve internal efficiencies, to simply survive, or not spend money on projects at all. The COVID-19 crisis caused most organizations to stop spending money on anything except survival.

Graphic representations of the portfolio are more informative to management than simply stating “We’re putting 30 percent of our money into infrastructure projects.” They show quickly when the portfolio is not balanced in the way management thought.

2.2.2.1 Growth-Oriented Portfolio—Version A

An organization that is interested in future growth might take more of the project funds away from operational areas and safe investments and use the money to fund NPD or for increased capital expenditures. The pie chart looks like:

Figure 2.2-5 Growth-oriented portfolio Option A

In this allocation, money has been moved to new product development by reducing the funding for operational projects. Infrastructure and capital investment projects have been left at existing levels. Unfortunately, many organizations tend to be short-sighted when it comes to decreasing expenses and tend to reduce departments such as HR or corporate training. Good in the short term, not so good in the long term. Blindly removing money from operations to put it somewhere else just increases inefficiencies in those parts of the organization that have been cut back. If money is to be taken from operations, it should be done by increasing operational efficiencies and using the savings to fund other works.

2.2.2.2 Growth-Oriented Portfolio—Version B

A company that is growing rapidly because of high sales volumes on its existing product line just needs to expand its facilities. These are capital investment projects and are expensive. They can be high risk or low risk depending on whether the economy is moving up or down.

The allocations might look like this:

Figure 2.2-6 Growth-oriented portfolio Option B

2.2.2.3 Growth-Oriented Portfolio—Version C

In the allocation shown here, both operational projects and infrastructure projects have been reduced, with more emphasis being placed on NPD and capital investments.

This is a typical arrangement in a rapidly growing economy, where companies are going to heavily fund NPD and as well as new facilities.

Figure 2.2-7 Growth-oriented portfolio Option C

2.2.2.4 Cost-Savings-Oriented Portfolio

When the economic conditions are on a downward slope, organizations have shown a strong tendency to reduce funding for NPD and for new facilities and either cut out all projects totally or put money into projects that increase internal efficiencies and produce cost savings. Or, as mentioned before, simply cut all project work no matter how beneficial. While the short-term financial benefits of cutting all costs are easily quantifiable, the long-term damage to the organization is less quantifiable but no less real. Multiple studies have shown that organizations that emphasize cost-cutting during economic downturns do significantly worse than their competitors once the economy starts picking, up as it always does.

Figure 2.2-8 Cost-savings portfolio

Portfolio Alignments

The aforementioned allocations are generic and could be considered starting points for discussions with the decision makers. The exact allocations will be determined by the executive committee and will be dependent on both strategic goals and current economic conditions. As either one of these changes, the portfolio will be adjusted as needed.

2.2.3 Three Project Priorities

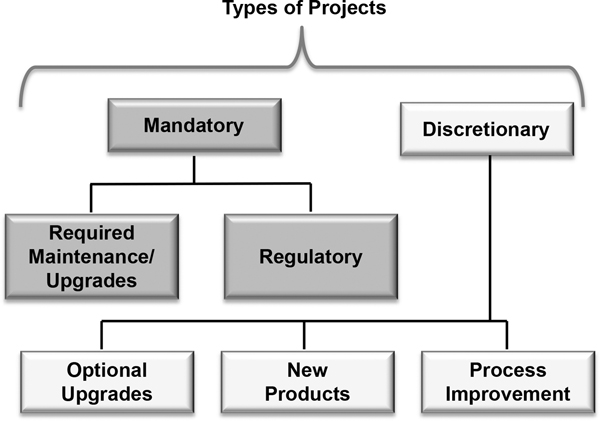

While there are a large number of projects that an organization can do within each asset class, we can divide them into just three basic types:

1. Regulatory-driven (“killer” projects)

2. Maintenance projects

3. Discretionary projects

Each asset category mentioned earlier can contain any one of these types of projects.

Figure 2.2-9 Project types

2.2.3.1 Regulatory-Driven Projects

Mandatory projects are “must-do” projects. We have no choice. They disrupt our carefully planned existing work. Regulatory-driven projects are driven by changes in laws and regulations and are mandatory if they apply to you. Consider the HIPAA (Health Insurance Portability and Accountability Act) legislation that was passed by the U.S. Congress in 1996. Part II of HIPAA required that a patient’s privacy be protected in several ways, one of which was their medical data. This mandated that all companies providing medical-related services, including insurance companies, had adequate security and privacy processes in their IT system to protect patient medical data. Implementing this new requirement disrupted the existing planned project work. With the passage of the Affordable Care Act (Obamacare), the industry faced many more mandatory projects as the full effects of the law are understood. Worse, as the act was being debated in the courts and with a proposed repeal by the subsequent administration, there is a great deal of uncertainty about whether companies should comply or not. The massive failure of the Enron company in 2001 led to mandatory changes in forcing executives to approve all of the financial statements, leading to significant process and IT changes in publicly owned organizations.

Regulatory changes can have unexpected consequences, so be prepared to make changes to the prioritized list of projects when those unexpected consequences are discovered. Because HIPAA made your medical data private, what is the impact of new technologies, such as wearable wristwatches, that monitor blood pressure, heartbeat, and other personal medical data and upload it to a cloud-based storage service? Does the storage service have to meet HIPAA requirements? Changes to long-term priorities can happen in cases like this, and those changes can be disruptive to our careful plans.

U.S. credit reporting companies such as Experian, Trans Union, and Equifax are subject to national-level legislation through federal legislation as well as dealing with separate legislation from each of the 50 states. Because these rules are coded into the software (leading to hundreds of business rules that must be checked for every credit report request), any change to any of the regulations leads to a considerable amount of work to find out where that existing rule is coded in the software and determine if the new change impacts any of the other hundreds of rules.

Companies that are subject to any regulatory-related controls must be aware of the possibilities of such interruptions and prepare accordingly. Regulatory-drive projects are sometimes referred to as killer projects because they basically kill any projects you already have in work or as “Orange Jumpsuit” projects because orange is the color of many jail uniforms—you don’t do the project, you go to jail, or at the least, pay heavy fines.

The right solution to the problem of disruption is for organizations that are subject to frequent changes in laws and regulations to compensate by not selecting so many projects that their personnel are allocated 100 percent of the time. They should leave some schedule room so that when a regulatory project comes in, they can start on it with minimal disruption to existing work. However, politically, this is often not palatable to upper management. They feel that people should be working on as many projects as possible and just deal with the schedule disruptions created by regulatory changes and the loss of morale caused by canceling a lot of projects when the regulations change.

2.2.3.2 Maintenance Projects

Maintenance projects fall between regulatory-driven projects and those that are completely discretionary. Some maintenance projects are mandatory. These include work such as commercial aircraft maintenance and refurbishments of processing lines in chemical plants. Both of these types of projects are required to ensure that the equipment remains safely operational for long periods of time. These types of projects are predictable and preplanned and therefore not disruptive to planned work.

Other maintenance projects fall into the category of discretionary. An IT department that plans on upgrading Windows or implementing the latest Oracle updates has a choice as to whether it does so and, if it chooses to upgrade, when the most appropriate time is. These types of maintenance projects can be preplanned and again are not disruptive to planned work. They should be included in the selection, prioritization, and planning processes that we will discuss next for discretionary projects. The cost justification for these projects must be done carefully so that only really needed projects get approved. Because these types of projects are not strictly mandatory, they are simply cost sinks and do not generate any new revenue. The best that can be said about them is that they may improve productivity, a thing that can be very hard to quantify. The maintenance projects that are discretionary should be treated as all other discretionary projects are and justified as to their benefits.

Emergency maintenance projects, such as equipment breakdowns, are those that are required to be done immediately to fix a problem. They are often highly disruptive to planned work but are unpredictable and so do not figure into our discussions here. However, in an environment where such breakdowns happen, such as a steel mill, a complex chemical processing plant, or even a complex IT network, the best approach again is not to overload people with planned work, so there is some overhead in the schedule to accommodate outages.

Story

The author spent some time helping develop project management processes at the Qatar Ammonia and Fertilizer Company (QAFCO) in Messaieed, Qatar. QAFCO is one of the world’s largest producers of urea and ammonia, both used in fertilizers. There were three major sets of processing lines, called trains, that took the locally abundant natural gas and processed it into the final products.

The processing required high temperatures and pressures of corrosive gases and liquids to produce the urea and ammonia. The job of the Systems Engineering department was to plan regular outages to replace major pieces of processing equipment before they wore out or broke to keep the trains processing as efficiently and as safely as possible. However, each train had a senior manager in charge who was bonused based on the train’s output. Their goal was to keep the trains running as hard and as long as possible. As you would expect, there were a significant number of arguments about when maintenance should be scheduled.

2.2.3.3 Discretionary Projects

Discretionary projects are mostly what this book is about. These are the projects that an organization has full choice as to whether it does them or not. Categories of discretionary projects include:

• Capital investment projects

• NPD projects

• Infrastructure projects

• Operational projects

• Discretionary maintenance projects

• Dedicated marketing, HR, and other department-specific projects

Capital investment projects include items like new facilities, property purchases, or major machinery and equipment purchases. These are high-cost purchases and are usually done during good economic times to increase capacity. New facility projects are also long-term investments that will tie up funds for several years. The cost of these is generally large enough that only top-level management can make these commitments. These tend to be low-risk projects that will provide substantial returns as long as economic conditions stay stable during a period long enough to justify their expenditures. If economic conditions change rapidly, these projects can lead to equally substantial losses.

Capital investment projects are sometimes referred to as CAPEX projects because of their high dollar value (hundreds of millions or billions of dollars) and long return on investment (often years). These projects are better managed using program management techniques rather than pure project management techniques. Industry terminology is confusing by often referring to these efforts as projects rather than their true descriptions as programs. Despite the confusion, we will follow industry practices and refer to them as projects. You should be able to tell from the context whether it is a simple project or a true program.

These kinds of projects consume large amounts of money and a lot of organizational resources. They are typically approved only at the very top levels of management, and the filtering criteria need to be design to approve them in stages. The first approval should be for the project overall as a strategic goal, and later approvals should be for each individual stage gate to decide whether or not the financial numbers look good enough to proceed compared to the risks.

This size/complexity of project is susceptible to being killed any time the numbers don’t look promising. In Fall 2013, Anglo-American Mining backed out of a joint venture to develop a gold/copper mine in Alaska at the end of Phase 3 because the risks of doing the project and the long timeframes for revenue did not look promising. They backed out of the project after spending $500 million in the early stages. That takes more courage than most executives have.

NPD, including research and development (R&D) projects and other exploratory projects, are highly risky and initial revenue from such projects may not happen for years if ever. History shows that the majority of new products do not become financially profitable. However, the small percentage that do can provide enough profit to more than make up for the losing projects. Some companies, such as Minnesota Mining and Manufacturing Company (3M), devote a large proportion of their financial assets to supporting NPD projects. Only a small percentage of them become profitable, but many of those become highly profitable (think of Sticky Notes). 3M typically spends about 5.5 percent of its operating expenses in R&D projects, but that is 5.5 percent of U.S. $3 billion in income from operations, a significant amount of money†. Google is another organization that allows people to work on their own pet projects, leading to many of the newer products that Google has released.

Of course, it’s not just how much money you spend, it’s how you spend it. Between 2004 and 2009, Apple Computer obtained a 72 percent growth in revenues from their $4.6 billion R&D investment‡. By comparison, Microsoft Corporation spent $31 billion during the same period and obtained only a 32 percent growth from R&D, Cisco spent $19 billion and got a 25 percent growth, while Intel Corporation spent $23 billion but received no revenue growth from their R&D investment.

How did Apple do so much better than these other companies? A strong NPD culture and processes allow them to filter among many possible projects to select the best ones. Google also has such a innovation-oriented culture. Most of its new product have come from individual research by employees who came up with an idea and were given the freedom to work on it. In 2019, their R&D spending had grown to $16.217 billion.

Best practice in the NPD arena is to use a stage-gate process. On a regular basis, during the early phases (called stages) of the project, a review is held to assess whether the project will satisfy strict profitability criteria. If not, the project is killed and the resources allocated to more promising projects. Each project must go through several of these gates in order to continue. It is not unusual for a company to kill 50 percent of their projects at the early gates. This winnows down the large number of projects to those that are most likely to be winners in the consumer market.

As Maniak3 points out, there are actually two benefits to these risky exploration projects. The first benefit, and the most obvious one, is that the final product that comes out of such a project is often highly innovative and can produce significant market advantage to the company. At least for a while, it is the only company producing such a product, and anyone who wants the product must buy it from them and only them. Examples include personal electronic devices such as the Sony Walkman or the much more recent Apple iPod.

Infrastructure projects can be reasonably divided into IT projects and non-IT projects. There has been a strong interest shown in portfolio management by many IT departments in the past few years because of the increasing amount of IT work being done as projects. According to research9 performed by PriceWaterhouseCoopers, IT-related productivity has been declining since the early 2000s even while the costs of IT have been increasing. More and more IT spending is going to maintain existing systems rather than benefiting the organization. This makes justifying IT projects much more difficult.

A strong emphasis on reducing costs has led to more projects to improve IT effectiveness but with no increase in the personnel to do the projects. More people are multitasking with concomitant reductions in productivity and an increase in the percentage of IT projects that are late and over budget. Portfolio management is a perfect solution to this type of an environment. Fewer, but more critical projects will be selected, waste and duplication will be reduced, costs will be reduced. Fewer mistakes will be made, quality will improve as will schedules and costs, and a higher percentage of projects will be completed successfully. No wonder, IT departments have been looking so strongly at EPM systems.

Non-IT infrastructure projects include anything required to keep the organizations facilities and equipment operating and usable. This category will include facilities upgrades and equipment repair/maintenance/ upgrade projects. It may also include equipment purchase and installation projects that are not sufficiently large to be considered a major capital expense.

Operational improvements form another category of discretionary projects. These are done to improve operations by increasing efficiencies or to support one particular department. The marketing department, for example, runs marketing and sales campaigns as a project—identifying the goals, planning out the work and the budget, assigning resources, and monitoring how successful the effort is.

Included in operational improvements are Business Process Improvement (BPI) projects. In the past 25+ years (since the reengineering trend in the early/mid-1990s), these have become increasingly important to companies. These are efforts to improve internal efficiencies in how we operate, especially since the economic downturn that began in 2008.

These are a peculiar type of project compared to more “normal” projects such as IT projects or NPD projects. These can be very complex, long-lasting projects and can be fraught with dangers. There are two reasons BPI projects have problems: the first is that business processes affect how people work, and any time you change people’s work, you will face resistance as we talked about earlier (remember the story about the utility in the last section?). The second is that all business processes link to other business processes. There is no such thing as an isolated business process. If you change one, you have to change the other processes that interact with it, and your project will very quickly grow out of control unless you put strict boundaries around which processes you are changing and which ones you are not. This is needed so that people will not assume you are changing processes that you are not. In the project charter, you should have a section on project exclusions specifically stating what process you are changing and whether or not you are changing the interfaces to other processes.

We see that there is a large variety of projects an organization can undertake, but they fall within just a few broad types. The type of project that lends itself best to being managed through portfolio management techniques is the discretionary project. The organization has a full choice whether to do this project or put its money somewhere else.

The following insert is about a fictional company, MegaNews International, whose motto is “We don’t just report the news, we create the news!” The Corporate chief information officer (CIO) has just returned from the annual strategic planning session held at corporate HQ in Australia and finds a list of projects on his desk. How does he select the “right” projects?

Table 2.3 MegaNews project options

MegaNews International |

As stated at the end of Step 1, the CIO of MegaNews has been given a list of proposed projects for her IT department to complete. She has called her senior staff together and lays out the following projects: |

A. New privacy laws that will take effect in 12 months in Europe require us to strengthen our website registration database. B. A new law in California requires us to change our website so that viewers must “opt-in” to receive our e-mail newsletters rather than “opt-out” from receiving it. This must be completed within three months. C. Corporate finance wants to install a data warehouse to manage all of the financial information. No given timeframe. D. We want to have a new website to compile news from other sources and allow viewers to buy it from us. E. We are opening new U.S. headquarters in Los Angeles and need to tie their LAN into the corporate network. The construction schedule says it will be ready for IT within four months. F. United Press International, a major news feed for us, is upgrading their news distribution network within the next six months, and we need to modify our IT infrastructure to tie into it. G. We need a new service to allow us to deliver user-customized financial news via iPhones, iPads, and PDAs with wireless connections. H. We are going to put news screens into each Starbucks Coffee Shop in the United States showing news headlines from around the world. This will be done over the next three years. I. Our website is currently written in English, we intend to internationalize it by creating versions in multiple languages. J. Half of our employees are using Macintosh computers, the rest are using Windows 8. The Windows component needs to be upgraded to Windows 10 once it has been tested for compatibility, a 12-month effort. This will improve productivity of the Windows side by 2 percent after the initial loss of productivity that follows any major upgrade. |

Using MegaNews as an example, let’s discuss what criteria should be used to select projects.

Now that we have a picture of the types of projects we might be dealing with, how do we score and prioritize them so that they most strongly align with organizational strategy? Everyone in management has their own interpretation of what the priorities are, a situation that usually leads to conflicting priorities, confusion, subversive stakeholders, and sometimes outright conflict. “Decibel decision making” may have worked in the past, but it always suboptimizes the organization’s effectiveness as well as reducing morale.

Simple or complex criteria?

How should we select and score the projects? It depends on what is important to our organization. There are several approaches that can be taken.

The United Kingdom’s Cabinet Office’s Office of Government Contracting has developed a Portfolio Management Guide. In it, they propose some very simple filtering criteria (Figures 6.3 and 6.4 from the Final Public Consultation Draft, 2009).

The proposed projects are then compared against each other after going through the filtering process. These are very simple criteria and apparently adequate for the process they were designed for.

For a more complex, and therefore more thorough, set of filters, we also have a number of choices. Cooper10 has proposed the following scorecard for NPD:

Factor 1: Strategic fit and importance

• Alignment of project with our business strategy

• Importance of project to the strategy

• Impact on the business

Factor 2: Product and competitive advantage

• Product delivers unique customer or user benefits

• Product offers customer/user excellent value for money (compelling value proposition)

• Differentiated product in eyes of customer/user

• Positive customer/user feedback on product concept (concept test results)

Contribution |

|||||||

|

Weight |

None |

Some |

High |

Score |

Total |

|

|

Prioritizing change criteria |

|

|

|

|

|

|

1 |

Supports at least one strategic objective |

20% |

0 |

5 |

10 |

10 |

2 |

2 |

Realizes significant benefits in a short time with low risk |

20% |

0 |

5 |

10 |

5 |

1 |

3 |

Contributes to external targets |

10% |

0 |

5 |

10 |

0 |

0 |

4 |

Complies with a legislative requirement |

25% |

0 |

5 |

10 |

10 |

2.5 |

5 |

Addresses an area of under-performance |

5% |

0 |

5 |

10 |

5 |

0.25 |

6 |

Improves efficiency |

5% |

0 |

5 |

10 |

5 |

0.25 |

7 |

Mitigates against corporate risk |

10% |

0 |

5 |

10 |

10 |

1 |

8 |

Honors an existing contractual obligation |

5% |

0 |

5 |

10 |

10 |

0.5 |

Change priority score |

7.5 |

||||||

Factor 3: Market attractiveness

• Market size

• Market growth and future potential

• Margins earned by players in this market

• Competitiveness—how tough and intense competition is (negative)

Factor 4: Core competencies leverage

• Project leverages our core competencies and strengths in:

• Technology

• Marketing

• Distribution/sales force

Factor 5: Technical feasibility

• Size of technology gap (straightforward to do)

• Technical complexity (few barriers, solution envisioned)

• Familiarity of technology to our business

• Technical track record on these types of projects

• Technical results to date (proof of concept)

Factor 6: Financial reward versus risk

• Size of financial opportunity

• Financial return (NPV, ECV, IRR)

• Productivity index (PI)

• Certainty of financial estimates

• Level of risk and ability to address risks

Part of your job in designing the EPMS is to identify which of these factors, or others, are most important to your upper management. They cannot all be equally important, they have to be prioritized (we will talk about how to do that later).

Not everything that is important can be measure financially. Our goal here is to create a set of objective filters that focuses on the organizational strategic goals while still giving some flexibility to management. That flexibility is important to allow growth in an area where we might not have a strong product presence, but rounds out our product line.

The majority of our filters will be oriented toward the project’s financial benefits and the project risk. However, nonfinancial benefits should also be taken into account when appropriate.

As shown in the scorecard just listed, many of these factors are not financially measurable. For example, the IT department of the Project Management Institute uses “benefit to members” as a major criterion for selecting projects. How can this be done if we’re not calculating the financial benefits? For projects where nonfinancial criteria are important, the steering or governance committee should pick the perceived benefits from a range of 1 to 5 (or 1 to 10 if that is more customary in your organization), where 5 is highly beneficial, 4 is mostly beneficial, 3 is neutral, 2 is somewhat detrimental to the organization, and 1 indicates the project may harm the organization if performed. All projects in this category go through the same ranking process.

So, other types of benefits are possible, but for most projects, the filtering criteria will be financial ones. Projects are paid for by money, and it is the responsibility of the executives to spend the organization’s money as wisely as possible. In the next chapter, we will discuss the details of various financial filters, such as ROI (ROI—an annualized rate of return expressed as a percentage), internal rate of return (IRR), payback period, and others. However, the purely financial approach has limitations, and some very worthwhile projects, such as R&D projects, will never pass a purely financial filter. This is one of the biggest limitations of most EPMS implementations and a major reason why the approach often fails after being tried.

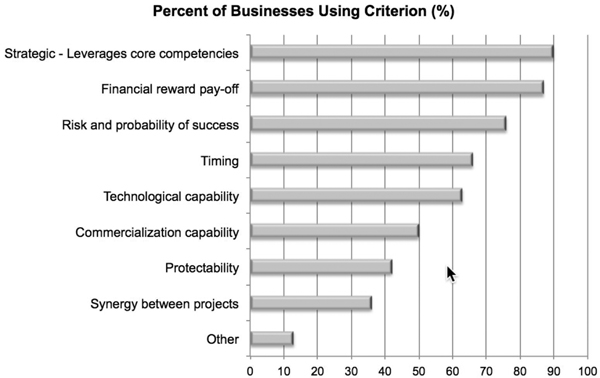

Research done in the field of NPD3 shows that financial filters are only one of a series of criteria used, and are not the most important. As shown in the next figure from that article, strategic fit outweighs financial benefits:

Figure 2.2-10 NPD filter criteria

For example, the major manufacturers of small digital cameras try to have a variety of products at different price points so they can compete directly with each other. They might approve a project to develop a new camera that fits a price point they do not already cover, knowing that they will never be the market leader at that price point.

According to the following figure from the same research, over 24 percent of companies engaged in NPD do not use financial methods at all. So, other, nonfinancial criteria need to be developed for them.

Figure 2.2-11 Financial metrics versus hurdle

2.2.5 Detailed Scoring

Now that we have a reasonable list of questions that will allow us to filter and score the proposed projects, just how do we score them?

If you are developing the software internally instead of purchasing commercial software, create a database for each of the questions. As each question is answered by clicking on the appropriate box, it is automatically scored.

Here we have designed-in the possibility that sections may have different weights. If annual revenues are much more important than the initial investment, you would put in an appropriate weighting factor. These weighting factors can be changed easily in response to the feedback obtained during the initial pilot project. If the list of projects presented to the steering committee for feedback doesn’t reflect how they would make decisions, this is the place to adjust the scores to more accurately reflect how decisions should be made.

The total scores are then presented, along with the project risk assessment, as a rank-ordered list to the steering committee. Because the numbers we present them are rough numbers, they should be allowed some flexibility in selecting projects that are close to one another. For instance, if two projects are within 50 points of each other and have similar risk profiles, they should be considered equivalent investments.

2.2.6 Weighting Criteria

Many authors such as Wood11 suggest weighting the criteria to avoid the limitations inherent in a purely financial approach. We might first identify the criteria themselves as follows:

• ROI

• Risk

• Confidence level of benefit delivery

• Impact to other projects

These do not have to be the same for every category of project, and in fact, should be different for every type of project. For capital expenditures on a new manufacturing facility, ROI would be a reasonable filter. For new product development, one filtering factor may be whether the new product differentiates us in the marketplace and gives us a sustainable advantage.

The next step is to weight each filter. For example, we might give the following weights to the criteria we listed above.

• ROI = 50 percent

• Risk = 20 percent

• Confidence level = 20 percent

• Impact to other projects = 10 percent

These are examples of types of criteria, there are others that might be used depending on what is important to the organization. For example, a professional organization might give a high weight to “benefits to members.” Or, a filter that might be used in new product development might be “increase in market share.”

Now we can go a step further and, for each project, give them a score between 1 and 10. A score of 10 shows the project will provide a lot of that criteria such as a strong ROI, and a score of 1 indicates it will not.

Except for risk and impact. These are negatives. Because the risk score identifies how risky the project is, the risk score should be done from 10 to 1, just the opposite of how the others are scored. A low risk project would get a score of 8, 9, or 10. A high-risk project would get a score of 1, 2, 3, or 4, and a medium risk project would get scores of 5, 6, or 7.

Similarly, a project that has a high impact to other projects in work would be scored in the range of 1 to 4, medium impact 4 to 7, and low impact 8 to 10. We multiply these scores by the weights, add them up, and this gives us an overall score for the project.

Table 2.5 Project weighting example

Project 1 |

Project 2 |

Project 3 |

Project 4 |

||||||

|

Weight |

Score |

Adj. Score |

Score |

Adj. Score |

Score |

Adj. Score |

Score |

Adj. Score |

ROI |

0.50 |

5 |

20.50 |

4 |

20.00 |

2 |

10.00 |

7 |

30.50 |

Risk |

0.20 |

3 |

00.60 |

5 |

10.00 |

9 |

10.80 |

4 |

00.80 |

Confidence level |

0.20 |

5 |

10.00 |

8 |

10.60 |

8 |

10.60 |

3 |

00.60 |

Impact |

0.10 |

9 |

00.90 |

8 |

00.80 |

4 |

00.40 |

4 |

00.40 |

Total |

10.00 |

|

50.00 |

|

50.40 |

|

40.80 |

|

50.30 |

Based on this approach, Project 2 would score the highest and has the best chance for approval. Its ROI score is only moderate, but we have a high degree of confidence we can do it. By comparison, Project 4 has a very good ROI score, but it is moderately risky, and we are not sure we can successfully accomplish it.

It is important to have consistency in decision making. Everyone who looks at a project should score it reasonably the same. Otherwise, one member of the steering committee might say the project has a very high risk, while another member says the same project has a very low risk. During the design period of the EPMS project, some definition of what the criteria are should be established and agreed-upon by the executives. For example:

Table 2.6 Sample weights

ROI Range |

0-5% |

5–10% |

10–20% |

20–25% |

25–30% |

30–40% |

40–50% |

50–100% |

100–150% |

>150% |

Score |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

10 |

An ROI range above 50 percent may seem high to a financial person, but venture capitalists often demand ROIs above 100 percent to compensate for the high risk of their investments. Your own breakdown will be determined by what is normal for your company. These numbers should be adjusted to the different types of projects being considered. In the next chapter, we will talk more about ROI and about the hurdle rate.

Because no scoring system is perfect, the executives should be given the latitude to select two projects that have scores relatively close together. Projects 2 and 4 in our example score close to one another and either one could be selected.

2.2.7 Determining the Scores

So, how do we determine what those scores should be? The best way is to derive those scores from a series of questions that each proposed project must answer. These questions are then given a score based on the answers to the questions.

Many of these answers are a best guess right now. You haven’t done the newly proposed project, so we don’t have real numbers to analyze. In order to minimize the possibility of wildly inaccurate guesses, make the questions and possible answers as detailed as possible so that the person answering it has to think about it.

For example, instead of asking if the project will increase customer retention, phrase it as follows:

Does or will the project increase customer retention?

2. By 0–5 percent?

3. By 6–15 percent?

4. By 15–20 percent?

5. By more than 20 percent?

And, then weight the answers. Answer #5 would have a higher weight than Answer #1 because increasing customer retention is very important.

MegaNews International Projects

Now let’s return to MegaNews International. We left the corporate CIO facing a series of proposed projects, wondering which ones to approve. The first thing he noticed was that two of the projects were mandatory because they were in support of regulatory changes. These projects were:

New privacy laws that will take effect in 12 months in Europe require us to strengthen our website registration database (Project A).

A new law in California requires us to change our website so that viewers must “opt-in” to receive our e-mail newsletters rather than “opt-out” from receiving it. This must be completed within three months (Project B).

So, these two were moved immediately to the approved list. Project A is estimated to cost $1 million and requires 10 people for six months. Project B is estimated to cost $500,000 and requires 2 people for two months. The executives will approve these projects because they must be done. But, the CIO is worried about how many resources these projects will tie up that will not be available for other work.

Let us now look at Project F: United Press International, a major news feed for us, is upgrading their news distribution network within the next six months, and we need to modify our IT system to tie into it. While this is not a regulatory project, if MegaNews International wants to stay connected to a major source of news in the future, it must upgrade its own IT infrastructure, so this really falls into the category of a “must do” project. It is estimated to cost $3.5 million and requires three people for four months.

To make intelligent decisions on the remaining projects, the CIO will need more information. After sending e-mails to the people who proposed the projects and getting more details, the CIO now had the following information:

C. Corporate finance wants to install a data warehouse to manage all of the financial information. No given timeframe.

• Estimated cost: $2.5 million

• Estimated benefit: $50,000 per year in improved productivity by corporate finance

• Resources required: 10 people for six months.

D. We want to have a new website to compile news from other sources and allow viewers to buy it from us.

• Estimated cost: $4 million

• Estimated benefit: $1.5 million/year

• Resources required: 10 people for six months.

E. We are opening new U.S. headquarters in Los Angeles and need to tie their LAN into the corporate network. The construction schedule says it will be ready for IT within four months.

• Estimated cost: $0.5 million

• Estimated benefit: $100,000 per year

• Resources required: five people for three months.

G. We need a new service to allow us to deliver user-customized financial news via iPhones, iPads, and PDAs with wireless connections.

• Estimated cost: $5 million

• Estimated benefit: $2 million/year from advertising

• Resources required: 25 people for six months

H. We are going to put news screens into each Starbucks Coffee Shop in the United States showing news headlines from around the world. This will be done over the next three years.

• Estimated benefit: $10 million/year from advertising

• Resources required: six people for 36 months

I. Our website is currently written in English, we intend to internationalize it by creating versions in multiple languages.

• Estimated cost: $6 million

• Estimated benefit: $2 million/year from advertising

• Resources required: 25 people for six months

A. Half of our employees are using Macintosh computers, the rest are using Windows 8. The Windows component needs to be upgraded once it has been tested for compatibility, a 12-month effort. This will improve productivity of the Windows users by 5 percent.

• Estimated cost: $5 million

• Estimated benefit: unknown

• Resources required: 10 people for 12 months

The calculations for this last project, the Windows upgrade, has a lot of assumptions and soft numbers that are needed. How can you judge how much productivity will increase because of an operating system upgrade? How can you even judge whether it will increase or decrease? For the purposes of performing the calculations, let’s make the assumption that productivity will decrease by 10 percent for the first six months until people are familiar with the new software, then it will increase by 2 percent. After one year, we can reduce the Help Desk and IT headcount by 25 people.

2.2.8 Stakeholder Involvement

The scoring questions should cover enough areas to determine the development costs of the project, the future benefits from it, impacts to other projects, and its risks.

But, there is no one group in the typical company that can answer all of these different questions. So, how do we get them answered?

The answer is that we have to involve other parts of the organization. Each section of our questionnaire is answered by someone in the group that has the best information.