How Bitcoin Fits in Your Portfolio

Enemy analysis plays an important role in mission planning in the armed forces. We examine composition, to include number of enemy personnel by weapon type and take note of the max effective range of each enemy weapon. We examine disposition, which is how the enemy arrays itself on the battlefield and how they generally fight. We examine strength, simply a percentage of their fully manned composition. We also examine and brief two potential futures—the most likely course of action and the most deadly course of action.

In truth, investing is not much different from studying and fighting an enemy force. The planner first gathers and examines all available information. He or she determines the most likely outcome of future events based on that information, and allocates capital or creates a plan depending on the mission and information given. In investing, that mission is always to preserve and grow your capital. The Platoon Leader and his or her subordinate leaders execute the plan but have a contingency if the most deadly course of action manifests itself, even if that contingency constitutes a simple break contact. In investing, this is our stop loss. The leader incorporates as many forms of contact as possible. This includes direct fire from rifles or machine guns, indirect fire from artillery or mortars, obstacles to block or canalize a force, electronic warfare to jam communications systems, even air support or chemical if the rules of engagement allows it. This is diversification. Relying on a single form of contact is simply too risky.

Just as with mission planning, I would like to lay out to the reader the most probable outcome and most dangerous outcome with Bitcoin’s future. The most probable outcome is that Bitcoin becomes an alternative investment class and several sovereignty minded individuals, corporations, and nation-states choose to adopt it as their reserve asset. It incrementally takes market cap from gold seeing as it better performs the functions of gold and has a small part as an alternative asset in nearly every retail, hedge fund, and pension portfolio. Outside of the investment management space, an increasing number of corporations and sovereign nations hold Bitcoin as a reserve asset. Though many retailers may accept it, Bitcoin never truly displaces fiat currency as the dominant medium of exchange because tax regimes vary from state to state. The Bitcoin maximalist proposition states that hard money will eventually drive out fiat money in what is known as Thier’s Law, the inverse of Gresham’s Law. Free market actors will converge on Bitcoin as a superior form of money, and governments everywhere will be forced to adopt the Bitcoin Standard.

In terms of institutional adoption, hedge fund titans Paul Tudor Jones and Stan Druckenmiller have already gone public saying they invest in Bitcoin. The Massachusetts insurance giant MassMutual purchased $100 million Bitcoin for its investment account in late 2020. CashApp, PayPal, and Square have moved to accepting Bitcoin payments. The National Football League’s Russell Okung opted to receive half his salary in Bitcoin and had the request approved. El Salvador also declared Bitcoin as legal tender in 2021. My base case is that this trend continues into the future. These are the first movers whose decision most will see as overtly risky but will pay off immensely as adoption rates increase.

Ironically, the latecomer to this party thus far has been Wall Street. Goldman Sachs published a report in May 2020 that likened Bitcoin to the Dutch tulip mania of the 17th century and labeled it a “conduit for illicit activity.”1 Goldman Sachs reached a $3.9 billion settlement that same year for admitted money laundering with the 1Maylasia Development Berhad.2 Additionally, Bitcoin received legal status an asset by the Commodity Futures Trading Commission in 2015. Many major banks such as Chase, Wells Fargo, and Bank of America also prohibit Bitcoin purchases using their debit or credit accounts. Wall Street and conventional banking’s reluctance to accept Bitcoin makes intuitive sense. Bitcoin’s peer-to-peer nature disrupts the hierarchical, fee and interest-based models of conventional banking. However, their initial hostility is slowly fading as the opportunity to generate profit in the space becomes clear. The banks can either become involved in the space or become less relevant. I believe they are choosing the latter as evidenced by J.P. Morgan Chase and Goldman Sachs appointing new heads of digital assets strategy in 2020 and creating custody solutions. Additionally, after years of lambasting the best performing asset of the decade to ultrawealthy private clients, wealth management divisions of these megabanks risk losing a large source of income if they ignore the transformation to digital assets and growing ecosystem. Recent trends indicate they recognize this.

Again, my base case is that Bitcoin becomes a highly sought-after asset due to its unique qualities as a scarce and liquid store of value, arriving at a $9 trillion market capitalization, on par with gold, for $500,000 a coin within the next decade. Much of the world adopting the Bitcoin Standard constitutes a positive tail risk event. Though most countries will not willingly give up the privilege of seigniorage, others are highly incentivized to adopt Bitcoin as a currency or reserve asset. These include countries such as El Salvador that use the dollar as their primary medium of exchange and have their monetary policy imposed upon them by unelected officials in the United States, or countries seeking to escape the rat race of constant competitive devaluation that is the inevitable byproduct of a floating exchange rate system. A globally coordinated ban of Bitcoin constitutes a negative tail risk event with low likelihood of occurring due to its difficulty to achieve. For readers who believe that Bitcoin could never displace gold as the go-to global store of value, I remind them that Bitcoin solves the liquidity and physical storage issues of gold with a programmed higher stock-to-flow ratio. Bitcoin is to gold what the car was to the horse and carriage. In a 1911 article in the Saturday Evening Post, Alexander Winton, whose Winton Motor Carriage Company sold the first automobile in 1897, wrote about his discouragement regarding global skepticism about the automobile. His banker told him, “You’re crazy if you think this fool contraption you’ve been wasting your time on will ever displace the horse.”3 Motor vehicles were a 10× improvement on the horse and carriage in terms of speed and maintainability. Decades later, we know that history took sides with Mr. Winton.

Just as in tactics, we must examine the most dangerous course of action, which is that all G7 nations collude to ban Bitcoin. I include a more in-depth description of why this is unlikely in the counterarguments section later in the book. While most Bitcoin enthusiasts will claim that Bitcoin can never be banned because it is open source code, governments colluding to make Bitcoin payments illegal or shut down exchanges will undoubtedly destroy the price. However, it must be all nations making it illegal and at the same time due to international arbitrage if banning occurs in a haphazard manner. For example, if one country made Bitcoin payments, storage, or mining illegal, those whose businesses depended on it would simply move to a country where it is legal. In fact, the country who made it illegal would be losing an entire industry while the open country would gain one. Using game theory, countries are better off accepting Bitcoin than banning it. A similar dynamic has already occurred with mining operations in China migrating to the United States, Kazakhstan, and Malaysia. International cooperation has always proven difficult and a different country would simply reap the benefits of a ban.

Additionally, I believe that institutional acceptance is too broad and only broadening for it to be made illegal. Hedge funds, corporations, investment banks, pension funds, insurance companies, and sovereign nations have all begun moving a small percentage of their assets to Bitcoin or have become involved in the space. Unless governments act now, outlawing it would create insolvencies in an already underfunded pension system. On the other side, the capital gains acquired from Bitcoin could actually save those pension systems that act as first movers. The incentives are heavily in favor of Bitcoin’s adoption. The only seemingly negative proposed regulation for mass adoption is the government’s rumored desire to increase regulation on self-hosted or cold storage wallets, which has already faced opposition from lawmakers. Cold storage involves keeping one’s Bitcoin offline and off of exchanges in a hardware wallet, paper wallet, desktop wallet, or USB drive. It is the equivalent of owning your own physical gold away from the financial system. The reason cold storage makes the government wary is due to its intractability and the fear of terrorist financing. While certainly against the libertarian nature of early Bitcoin adopters, a ban on cold storage will not destroy Bitcoin. In fact, the news of Secretary Mnuchin’s rumored ban in 2020 barely put a dent in Bitcoin’s price and never came to fruition. Price action ignored the rumors as it moved to all-time highs.

Alternatively, I believe Central Banks and governments are moving more toward accepting Bitcoin than banning it. I will discuss Central Bank Digital Currencies (CBDCs) later in the book and how countries and central bankers have already expressed their desires to create them in order to provide more effective stimulus. Blockchain based, government-issued tokens provide easy on-ramps for would-be crypto investors. In other words, CBDCs will enable the transition from physical dollars and gold to digital dollars and Bitcoin. In a system of Bitcoin acting as an internationally recognized global reserve asset, the price per coin would be in the several millions.

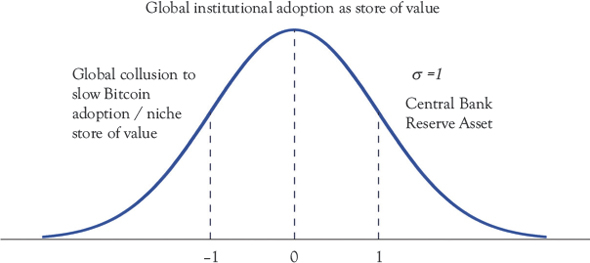

Figure 2.1 Normal distribution of bitcoin probabilities

A concerted international effort to ban Bitcoin and sovereign adoption are both tail risks in the distribution of probabilities as shown in Figure 2.1. However, the odds are heavily skewed in favor of continued price appreciation. The most likely scenario involves its institutional adoption as an alternative asset class. In this case, the asset will remain significantly undervalued for years. Now that we have examined the possible distribution of outcomes, the next sections explore the practical reasons to own Bitcoin.

Diversification and Risk

Diversification plays a vital role in portfolio construction and management. Ray Dalio, founder and chief investment officer of Bridgewater Associates, one of the largest hedge funds in existence with $138 billion assets under management, claims that “diversifying well is the most important thing you need to do in order to invest well.”4 His “Holy Grail” of diversification involves 15 uncorrelated bets. For one, how many investors can say they have even 10 uncorrelated bets? Additionally, as the next chapter suggests, false diversification is a true threat to portfolios as stocks, government bonds, and corporate bonds are all markets that see artificial demand from Fed policy and anticorrelation based on a Fed reaction function that has run its course.

Statistically, according to coinmetrics.io, Bitcoin’s correlation with traditional assets such as the S&P 500, the dollar, gold, and volatility as measured by the VIX, has ranged from 0.22 to −0.21. Historically, the correlation remained closer to zero for each. The S&P correlation and VIX anticorrelation peaks both occurred in November 2020, as Bitcoin and U.S. equities rallied simultaneously and volatility decreased after March’s COVID-19-related spike. I believe investors’ risk appetite returned after the March shock and Fed response, causing both assets to rally simultaneously. However, a correlation range between 0.22 and −0.21 throughout its history tells investors that Bitcoin is not correlated to traditional assets. If investors know they should seek diversification, Bitcoin provides a solution as a statistically proven uncorrelated return stream.

In addition to diversification, Bitcoin also decreases risk in a portfolio as outlined in the article “Efficient Market Hypothesis and Bitcoin Stock-to-Flow Model.”5 The article presents the risk/return profile of traditional assets such as the S&P 500, government bonds, and gold. It defines risk as maximum historical annual loss and return as average annual returns. Bonds have the lowest of each, with the lowest risk of 8 percent but the lowest returns of 6 percent. Gold has a risk of 33 percent maximum loss and an average return of 7.5 percent. U.S. equites fell opposite to bonds with 40 percent risk of loss and 8 percent average return. How did Bitcoin fall on this metric? Two hundred percent average annual return and a maximum 80 percent loss. No other asset in existence provides even one-tenth of the alpha that Bitcoin has brought its investors. Bitcoin investors must know that it is a volatile asset but undoubtedly the best performing one due to the macroeconomic role that it plays. Since 2009, if you allocated 1 percent of your portfolio to Bitcoin and 99 percent to cash, you would achieve over 8 percent returns while only risking 1 percent of your capital. A 1 percent allocation to Bitcoin would have outperformed the S&P.

The Sharpe Ratio was developed by Nobel Prize winning economist William Sharpe. The equation takes the expected or historic rate of return, subtracts the risk-free rate of return (government bond yield matching the investment duration), and divides it by the volatility, or how widely prices disperse from their mean. It is seen as a measure of risk in traditional portfolio management. Personally, I believe most traditional portfolio managers conflate volatility with risk. For example, as the next chapter will explain, there is systemic risk to government bonds but their volatility is suppressed with Fed purchases. This leads to the false impression that bonds are not risky when in fact they are just not volatile. Nonetheless, using traditional financial logic, Bitcoin beats every other asset on this risk model.

A Sharpe Ratio of one is considered good and two is considered excellent, while a zero or negative Sharpe Ratio indicates that the asset will not outperform the risk-free rate. Since mid-2014, Bitcoin’s Sharpe Ratio has never dipped below two and is currently at three. The S&P and gold are at roughly 1.3, while U.S. real estate is just below that at 1.1.6 Using traditional measures of risk, Bitcoin is a superior and less risky investment than stocks, bonds, gold, and real estate at nearly double the Sharpe Ratio. Given Bitcoin’s volatility, most investors could not stomach overallocation. However, adding Bitcoin to a traditional portfolio will optimize it by substantially increasing the risk-adjusted returns.

Bitcoin is an uncorrelated asset with a super risk/return profile. Adding it to your portfolio is akin to adding a proven venture capital arm to your investments. It does not correlate with traditional market movements unless in a liquidity event and its returns are astounding—even when compared to its volatility or existential risk. I believe that at some point, all portfolio managers and investment advisors will catch on to the fact that they can optimize their investments by adding even a small allocation to Bitcoin. If they already do, they are ahead of the game. If they do not, then much like some Wall Street banks, they will be forced to adopt by their clients or be forced into irrelevancy.

High Growth Potential and Network Effects

Bitcoin is a hard money monetary network. Facebook is a social media network. The telephone operates on a voice communications network. What matters to a network is the number of users. The features of Facebook mean nothing if there are no other users on the platform to share and connect with, just as owning a telephone means nothing if there is no one to communicate with. The incentive structure of Bitcoin is rather straightforward. As it attracts more users to adopt the network as a store of value for their savings or as a payment mechanism to avoid time and fees involved with traditional banking, the price appreciates.

Metcalfe’s Law, named after Internet pioneer Robert Metcalfe, explains how growth in networks differ from growth in typical businesses. Metcalfe’s Law states that the value of a network increases by the square of the number of nodes or users. While a typical business increases linearly depending on the number of users, networks increase exponentially. In a typical business, each customer interacts with the business owner on an individual basis to conduct a transaction. In a network, each user becomes connected to each other user in the network, which in turn increases value for all users. This law quantifies the network effect.

Each user makes the network more robust and provides a node that all users can exchange value with on the network. Metcalfe’s Law explains the parabolic growth rate of Google, Facebook, and Amazon as dominant networks in their fields. If each additional user increases the price exponentially, and institutional finance is just now joining the network in a large way, Bitcoin has astounding growth potential. If Bitcoin becomes the dominant store of value network, equaling or surpassing gold in market capitalization, the price per coin will be $500,000 per coin or greater. I believe that this is the realm that Bitcoin will eventually be relegated to—the monetary network that solved the gold/dollar dilemma. However, it has the potential to become much more.

Nothing Else Makes Sense

In this section, I will take the reader around the world of traditional asset classes to explain why, on a valuation basis, nearly every other asset cannot provide the same returns as Bitcoin. Investors need to take a value-minded framework yet understand technology and nuance in order to avoid being stuck in a 1970s-style stock picking mental model that will undoubtedly lead to lower returns. Bitcoin is undervalued not on a discounted cash flow basis but based on the network effects of the adoption curve.

The post-2008 stock market is liquidity driven, not fundamentals driven. Barring a deflationary shock, equities will remain objectively overvalued because policy makers need stocks to rise to prevent a stock market recession from reverberating into the real economy. The following is a list of six common S&P 500 valuation metrics and their historical percentile only eight months after the coronavirus-created recession:7

1. U.S. Market Cap to GDP: 100 percent

2. Price to Sales: 100 percent

3. Price to Book: 100 percent

4. Enterprise Value to EBITDA: 100 percent

5. Price to Earnings: 98 percent

6. Cyclically Adjusted Price to Earnings (CAPE): 97 percent

This stock market is the most expensive in history by nearly every measure at a time where every large sell-off is quickly backstopped by the Fed. If future returns are a function of the price paid, the above metrics scream stay away from U.S. stocks. As the first sentence of this section suggests, I have a more nuanced view on the U.S. stock market. While they are objectively at nosebleed levels, they are only slightly overvalued on a liquidity basis. My advice to subscribers at Seeking Alpha is to remain cautiously long. Equity prices have a high correlation to global liquidity. Ratios such as asset prices to global liquidity and equity to safe assets matter more than the value investor metrics of decades ago. As a relatively scarce claim on a company’s cash flows and growth, stocks act as a buffer against an inflating money supply. Demonstrating the importance of available liquidity, the Venezuelan stock market has returned 2,578 percent from January 2020 to March 2021. On a fundamental basis, nothing occurring in Venezuela would warrant such an increase besides a hyperinflating currency. The second metric, the equity to safe haven ratio, displays the level of widespread investor participation compared to treasuries and gold. A large percentage of investors positioning themselves defensively indicates that markets have not reached bubble territory. If equities should continue to rally, it will be on a liquidity basis.

Many renowned value investors will argue that fundamentals must converge onto inflated asset prices through the wealth effect or asset prices must converge onto weaker fundamentals through a sustained recession. These investors, including Warren Buffett, will patiently and confoundedly sit on mountains of cash waiting for opportunities to arise that seem to never materialize. They are right to note the disconnect between value and fundamentals. Apple’s stock gained 92 percent in 2020 despite only increasing revenue by 1 percent. However, I will take readers back to my previous comment about understanding nuance and outdated mental models. The stock market is not the economy—even though economic activity has previously proven a successful barometer of present and future stock prices. We have unprecedented Central Bank activity aimed at preventing asset price collapse. As the system currently stands, tell me the direction of the Fed balance sheet and I will tell you the direction of U.S. equities.

The next chapter will take a closer look at why this disconnect occurs through the Cantillon Effect. In essence, the mechanism by which the Fed infuses the economy with liquidity leads to asset price inflation. In addition to this, velocity of money stops at banks as that money rarely makes it to the real economy. As previously mentioned, the system inadvertently takes money from savers and wage earners to boost asset prices. For the sake of this chapter, readers must know that newly created money most frequently goes to stocks before the real economy. Therefore, investors who allocate capital based on a framework of fundamental valuation will not do well in this environment. I do not recommend putting 100 percent of one’s capital into equities. While they may have more upside on a liquidity basis, the only thing propping up equity markets is Central Bank liquidity.

Because financial markets are a complex system, I usually refrain from making normative statements. However, some relations are obvious. Anyone who makes a fundamental argument for stocks based on future earnings or valuation metrics will have a difficult time explaining equity prices when priced in things other than the dollar. Divide the U.S. stock market capitalization by G4 Central Bank liquidity and the stock market peaked in 2007 as quantitative easing began in earnest following the Global Financial Crisis. Divide the stock market capitalization by a hard asset such as gold and the stock market peaked in 2001. Divide it by a harder asset in Bitcoin and the stock market breaks down completely. Quantitative easing went into hyperdrive following the coronavirus recession. In March of 2020 alone, global Central Banks purchased $1.4 trillion worth of assets. It is important to not examine equities through a silo. In terms of price, stocks always seem to go up. In terms of hard money, they have gone nowhere at all.

Investors overallocated to U.S. stocks should feel uneasy knowing that the only thing preventing prices from mean reversion is artificial demand from a cash infusion mechanism that benefits financial assets over real economic activity. Hard assets benefit even more from this monetary creation and should therefore play a larger role in future portfolios. This regime of high-powered monetary creation will not end in the foreseeable future.

Government and Corporate Bonds

Buying the 10-year Treasury note at near-zero rates a bet that yields will go zero or negative. When investors purchase a bond fund, the fund appreciates in price as yields decrease. That is because the fund rolls over its bonds, the equivalent of refinancing, and takes advantage of the gains acquired from the lower rate. Based on this dynamic, both government and corporate bond prices have remained on a steady uptrend for the past 40 years as the Federal Reserve forced interest rates lower and lower. If widespread inflation occurs, selling will force yields to rise. This constitutes an enormous risk amidst the current level of money printing. Similar to the Reserve Bank of Australia, the Fed will likely resort to yield curve control to prevent rising yields from pricking bubbles in the financial and real economy.

Buying bonds is the equivalent of picking up pennies in front of a steamroller. For long-term investors, I do not recommend them. For tactical traders, yields may eventually go to zero or even negative as they have in Europe and Japan. However, the gains acquired from a bond position when yields go negative is likely not worth the pain that will result if persistent inflation arises. The reason Europe and Japan have negative rates is simple. They need negative real yields to service their massive amount of debt and continue deficit spending. If real yields are equal to nominal yields minus the inflation rate, and the inflation rate in those countries are at zero or negative due to terrible demographics, low growth, and technological advances, nominal yields must be negative to keep real yields negative. These countries are victims of their own poor choices in economic governance. Japan did it first, Europe followed, and the United States is on a crash course to negative yields unless they change course. The only thing that will force the United States to change course is inflation brought about by poor policy choices. I believe the United States has implicitly stated it will inflate the debt away—a boon for Bitcoin and a death knell for bonds. Trillions of dollars in the bond market will need to find a new home in this paradigm shift from debt-based growth to inflation-based growth. Bitcoin will certainly be one of those homes. While bond prices may appreciate in the interim, better opportunities for generating alpha exist.

Government and corporate bonds have historically played an integral role in portfolio management due to their anticorrelation with equities. Investors purchase bonds to protect their portfolio in case of a large sell-off in equities. However, bonds moved opposite of stocks because the Federal Reserve pushed interest rates lower in the face of weaker economic activity as a counter to the business cycle. They were able to do this because there was no inflation risk as measured by a low Consumer Price Index. This is a modern phenomenon that began with the end of the inflationary regime of the 1970s and the beginning of accommodative monetary policy in the Greenspan era. Since 1883, stocks and bonds have had a highly positive correlation 30 percent of the time and a highly negative correlation 11 percent of the time. In a world where much of the financial system is leveraged to a 60/40 portfolio based on an assumption of anticorrelation, negative returns in both assets will devastate most portfolios and expose a gigantic recency bias.8 While correlations may swing wildly, stocks do not always move opposite bonds. In fact, for most of history they moved in lockstep. Stocks, government bonds, and corporate bonds all benefit from Fed policy and have reached historical highs because of it. If they are destined to underperform due to their current valuations, what other assets exist?

Gold

Gold is seen as a safe haven asset and inflation hedge due to its scarcity value and its proven 5,000-year track record as a store of value. Some investors claim that gold and Bitcoin both play important roles in this macroeconomic environment of unprecedented money creation. However, I will take readers back to an argument made previously. If Bitcoin has perfected all of the characteristics that make gold valuable, why would investors still allocate to gold aside from an appeal to tradition bias? In fact, if paper currencies only came into existence to overcome the physical limitations of gold, and the technology exists to send digital gold via communications channels, there is theoretically no need for physical gold or paper currencies.

Nevertheless, with money being devalued at historic rates, a scarce store of value matters. A perfectly liquid and perfectly scarce store of value is preferable to an illiquid store of value with a near 2 percent inflation rate. Investors need to travel from point A to point B. Their options are a horse and buggy or an automobile. Both options allow them to achieve their goal but Bitcoin gets you there faster. Many investors see regulation risk as a legitimate reason to own some gold instead of Bitcoin. Though a reasonable objection, I believe much of that risk is overstated.

Real Estate

I am slightly more constructive on real estate than the previously mentioned asset classes. While prices generally are at historic highs due to decades of monetary debasement and low borrowing costs, pockets of value exist in real estate markets. Megacity real estate markets will have a brush with reality as ever-increasing house prices meets a millennial and Gen-Z generation entering the workforce after decades of stagnant wages and saddled with student debt. I do not recommend buying property or even Real Estate Investment Trusts (REITs) in mega-cities such as New York City or Los Angeles. However, in certain areas, an investor can pay a low price for a property that provides cash flow and has room to appreciate in price based on demand for that location.

Real estate can be profitable with a research-intensive and bargain-based approach. Prices should continue to rise with current rates of monetary debasement. However, real estate falls into the same category as U.S. equities in that I would be “cautiously long.” Turning off the monetary spicket or substantially raising interest rates will hurt the real estate market. The notion that real estate prices always go up is simply a misunderstanding. House prices do not always go up, fiat always goes down.

Other Assets and Final Thoughts

From a value perspective, I am bullish on emerging market equities. I do not see the dollar losing reserve currency status in the near-term future but I see it as less dominant in the coming decades. Asia and Latin America constitute two areas with demographic tailwinds and a less significant debt burden to drag on future growth. With a weaker dollar and less dollar dominance in global trade, their dollar denominated debt burden will decrease, unlocking growth that rivals the post-World War II boom of the United States. Commodities are also beaten up from a valuation perspective and will benefit from both the economic reflation and monetary inflation narratives. Both assets have yet to outperform U.S. stocks. A strong dollar keeps debt burdens high for countries with dollar-based debt and slow economic activity prevents the industrial use of commodities. I believe these assets will see their decade in the sun but that time may be several years away.

Therefore, global assets fall into one of two categories. Stocks, bonds, and real estate are all at historical highs. They have limited upside and substantial downside. Gold is set to perform well but Bitcoin is theoretically superior to gold and has outperformed it by over 200 percent year over year. If one purchases gold and Bitcoin for the exact same reasons, yet Bitcoin outperforms by 200 percent, it questions the original thesis of why own both. Emerging markets and commodities are worthwhile future investments but will take time before the narrative catches on and their value is unlocked. Though I recommend diversification and several uncorrelated investment streams for most traditional investors, nothing else is set to perform like Bitcoin.

Conclusion

This chapter has outlined the reasons why investors should allocate some Bitcoin to their portfolio. It is an uncorrelated asset that provides true diversification. Using the Sharpe Ratio, it optimizes the risk-free returns of any portfolio. It has high growth potential due to network effects and continued adoption from institutional finance. Lastly, every other asset class is either severely overvalued or has not seen the flows to appreciate in price despite a bullish narrative.

Given these facts, how much should an investor allocate to Bitcoin? I offer three options depending on one’s conviction. For skeptical investors, I hope the chapter on Bitcoin counterarguments will eliminate or reduce skepticism. However, I recommend a 1 to 5 percent allocation simply for portfolio optimization purposes. Another way to think about it is to invest whatever you are willing to lose. Past performance shows that even a 1 percent allocation to Bitcoin and 99 percent cash would have outperformed the S&P 500 since 2009. For those that desire true diversification, I recommend 10 to 15 percent. This allows you to gain from the massive appreciation I see coming with the macroeconomic tailwinds and have enough outside exposure to survive dreaded crypto bear markets—even though Chapter 4 will go over ways to know it is time to reduce exposure. The final option is not necessarily a percentage of one’s investable assets but more of a lifestyle change. It involves adopting the Bitcoin Standard in one’s personal life. Money intended for future consumption gets placed on the Bitcoin network. It serves as the hard money savings account that inflationary policy never let you have.

Michael Saylor is the Founder and CEO of MicroStrategy, a business analytics software company. He has garnered massive attention for his business decision to place over half of his company’s cash holdings in Bitcoin. In essence, Bitcoin is his treasury reserve asset instead of the dollar. This is what I mean by adopting Bitcoin as a savings technology in one’s personal life or business. If savings will be losing value daily and no worthwhile investments exist, simply place that savings in a hard money monetary network until the time comes to make a purchase. Thus far, companies such as Microstrategy, Square, and Tesla have been rewarded by the market with stock price appreciation for their business decision to place some cash reserves in Bitcoin.

I believe my journey is a typical one for investors. I allocated 5 percent to Bitcoin as an interested skeptic in 2018. As opposed to rebalancing in the face of price appreciation, I continued my research and grew in conviction. Once an investor has skin in the game, his or her perspective on money and portfolio management will change. My one recommendation involves starting small and getting off zero. The desire for diversification and greater risk adjusted returns may even morph into a modus operandi after investors realize that no other asset makes quite as much sense.