Chapter 4c

Accounting Process – Subsidiary Books

LEARNING OBJECTIVES

After studying this chapter, you would be able to understand

Meaning of Subsidiary Books

Kinds of Subsidiary Books and Their Purpose

Advantages of Subsidiary Books (or) Special Journals

Differences Between Subsidiary Books and Ledger

Meaning and Type of Cash Book

Meaning, Format and Recording of Transaction in Single Column Cash Book

Meaning and Format of Double Column Cash Book (Cash Book with Discount and Cash Column) and Preparation of a Two Column Cash Book from the Given Transactions

Method of Entering Bank Transactions in Two Column (Bank and Discount Column), i.e. Bank Column Instead of Cash Column

Meaning of Triple Column Cash Book (Cash, Bank and Discount Column) and the Procedure of Recording Business Transaction in Triple Column Cash Book

Meaning of Petty Cash Book – Salient Features of Petty Cash Book – Advantages of Petty Cash Book

Format of Petty Cash Book and Method of Recording the Transactions in the Analytical Form of Petty Cash Book

Meaning of Purchases Book – Format of Purchases Book – Method of Preparing Purchases Book and Ledger Accounts Related to This

Meaning of Sales Books – Format of Sales Book – Procedure of Constructing Sales Book and Necessary Ledger Accounts Related to It

Meaning of Purchases Returns Book – Procedure for Recording Purchases Returns Transactions

Meaning of Sales Returns Book – Procedure for Recording Transactions in Sales Returns Book and Posting them to the Ledgers

Meaning of Bills of Exchange and Meaning of Important Terms Associated with Bills of Exchange

Procedure of Recording Transactions in Bills Receivable and Bills Payable Books

Journal Proper and the Different Kinds of Entries to be passed in Journal Proper

OBJECTIVE 1: MEANING OF SUBSIDIARY BOOKS

Subsidiary books refer to the books meant for specific transactions of similar nature. It is used to record only one type of business transaction. These subsidiary books are also called Books of Original Entry. These are also referred to as Special Journals.

As the number of transactions of a business enterprise increase in volume, as some transaction are of repetitive in nature, the need arises to classify and group the business transaction so as to suit the needs of enterprises.

The main journal is subdivided into different types of subsidiary journals or subsidiary books as follows.

OBJECTIVE 2: KINDS AND PURPOSES OF SUBSIDIARY BOOKS

Kinds of Subsidiary Books

Purpose of Subsidiary Books

| Kinds of Subsidiary Books | Purpose |

|---|---|

1. Single Column Cash Book |

To record cash transactions (cash receipt and cash payments) |

2. Double Column Cash Book |

To record cash and discount transactions |

3. Triple Column Cash Book |

To record cash transactions, bank transactions and discount transactions |

4. Petty Cash Book |

To record other petty transactions |

5. Purchases Book |

Credit purchase of goods to be recorded |

6. Purchase Returns Book (Returns Outward Book) |

Goods returned to the suppliers are to be recorded |

7. Sales Book |

To record credit sales |

8. Sales Returns Book (Returns Inward Book) |

To record goods returned to customers |

9. Bills Receivable Book |

To record bills receivable (receipts of bills) drawn |

10. Bills Payable Book |

To record bills payable (issue of bills) accepted |

11. Journal Proper |

To record entries, which cannot be entered in any of the above books |

OBJECTIVE 3: ADVANTAGES OF SUBSIDIARY BOOKS (OR) SPECIAL JOURNALS

The advantages of maintaining subsidiary books are:

1. Division of Labour: The division of journal facilitates the division of work (recording transactions) among its employees. In large organisations, it becomes inevitable to divide the work and allot it to its various employees (clerks and other officials) so that they can work independently and quickly.

2. Delegation of Work: Work is delegated to each employee, which ensures in evaluating the efficiency of individual workers, as specialisation always results in efficiency.

3. Detection of Errors: Accounting work is divided to record transactions in various subsidiary books. If the work is divided in such a manner that the work of one person is automatically checked by another person, it would be easy to detect errors and rectify them immediately.

4. Facilitates Quick Reference: The information regarding the same type of transactions is available at one place. As such, information relating to any particular item of transaction can be obtained easily.

5. Effects Saving in Time, Labour: The amount of space needed for recording same type of transaction is reduced. The number of postings to ledger accounts is also reduced. Posting again and again from the Journal to a Ledger involves a tedious and monotonous work, which is avoided to a great extent by keeping special subsidiary books.

6. Simultaneous Recording: As many persons are involved, the subdivision of journal enables them to record all transactions simultaneously and at the same time without giving disturbance to the other persons engaged in the work.

OBJECTIVE 4: DIFFERENCE BETWEEN SUBSIDIARY BOOKS AND LEDGER

The differences between subsidiary books and ledger can be presented in the summarised form in the following tabular column:

| Basis of Distinction | Subsidiary Books | Ledger |

|---|---|---|

1. Caption of the book |

These are books of Original Entry (or) Books of Prime Entry. |

This is a book of Secondary Entry (or) Book of Final Entry. |

2. Basis of recording |

These are recorded on the basis of source documents. |

These are recorded on the basis of the books of Prime Entry. |

3. Order of recording |

Transactions are recorded in order of their occurrence. |

Transactions are recorded from subsidiary books irrespective of the date of their occurrence. |

4. Aspects of (transaction) recording |

Both aspects (debit and credit) of a transaction are recorded. |

Posting is made relating to either debit aspect or credit aspect of a transaction in the ledger. |

5. Net effect of transactions |

These do not disclose the complete position of an account. |

The ledger account indicates the net effect of each account. |

6. Balancing |

Except cash book, balancing is not done. |

Except nominal accounts, balancing is done. |

7. Next stage in the process of accountant |

The next step is the transfer of entry to ledger account. |

The next step is to draw Trial Balance. |

OBJECTIVE 5: MEANING AND TYPE OF CASH BOOK

5.1 Meaning

A cash book is a special journal used to record all cash receipts and cash payments. Without passing entries in the journal, all transactions relating to cash receipts and cash payments are entered straight in this separate book called “Cash Book.”

Cash book, a journalised ledger serves both as a journal and a ledger. Cash book performs the functions of both ledger and journal simultaneously. Cash book is a book of original entry as transactions are recorded from source documents for the first time. Like journal, all transactions (relating to cash) are recorded chronologically and at times with narration. The Cash book is like a ledger in the format (having debit side and credit side), balanced like a ledger account for these reasons. The cash book is called a journalised ledger because it serves both as a journal or a ledger.

5.2 Types of Cash Book

As explained in the diagrammatic classification of the subsidiary books, the cash book may be classified into the following types:

- Single Column Cash Book (Simple Cash Book)

-

- Double Column Cash Book (Cash and Discount Columns)

- Double Column Cash Book (Bank and Discount Columns)

- Triple Column Cash Book (Cash, Bank and Discount Columns)

- Petty Cash Book (for recording small expenses)

Let us explain each type of Cash book.

OBJECTIVE 6: MEANING, FORMAT AND RECORDING OF TRANSACTIONS IN SINGLE COLUMN CASH BOOK

6.1 Meaning

Single column cash book, also called as simple cash book, contains one amount column in each side, that is, debit side and credit side. All cash receipts are to be recorded on the debit side and all cash payments are to be recorded on the credit side of the cash book. This book is very similar to that of Cash Account in the Ledger.

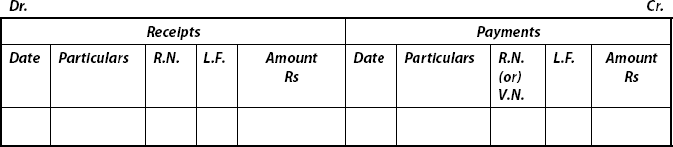

6.2 Format of Single Column Cash Book

Single Column Cash Book

Format explanation:

- Date Column: This column appears on both debit and credit side. The date of receiving the cash is recorded in the “Date Column” on the debit side and the date of paying cash is recorded on the credit side in the “Date Column.”

- Particulars Column: This column appears on both the sides. Names of parties (personal account), heads (nominal account) and items (real account) from whom payment has been received and to whom payment has been made, are to be recorded in the “Particulars Column.”

- Receipt Number (R.N.): Serial No. of the cash receipt is to be recorded in this column.

(Some enterprises use V.N. (Voucher Number) on the credit side in the place of R.N. V.N. refers to the Voucher Number for which payment is made.)

- Ledger Folio (L.F.): This appears on both the sides. The ledger page of the related account is to be recorded on the debit side.

- Amount: This column also appears on both the sides. Cash received amount (actual amount of cash receipts) is to be recorded in the Amount Column on the debit side. The actual payments are to be recorded in the Amount Column on the credit side of the Cash Book.

6.3 Balancing of Cash Book

The cash book is balanced like any other account. The amount columns on both sides are totalled. The total of the receipt column (debit side) will always be greater than the total of the payment column (credit side). The difference indicates the amount of cash-in-hand. Cash balance will always show debit balance. The difference is written on the credit side as “By Balance c/d.” In the beginning of the next period, to show the cash balance in hand, it is recorded in the debit side as “To Balance b/d,” that is, as the opening balance for the next period.

Illustration: 1

Enter the following transactions in a single column cash book of Mr. Dev Anand.

|

2009 |

|

Rs |

|

Jan |

2 Started business with cash |

10,000 |

|

|

3 Purchased goods for cash |

2,000 |

|

|

6 Sold goods |

2,000 |

|

|

7 Cash paid for mobile recharge |

200 |

|

|

8 Paid cheque to a creditor |

1,800 |

|

|

9 Cash received from Babu |

1,000 |

|

|

12 Bought furniture |

1,750 |

|

|

14 Received commission |

250 |

|

|

15 Sale of securities |

7,000 |

|

|

17 Part payment to suppliers X Ltd. Rs 1,000 against their previous bill for |

5,000 |

|

|

19 Cash sales |

12,000 |

|

|

20 Goods purchased by credit |

10,000 |

Solution

- Record all cash receipts on the debit side and all cash payments on the credit side of cash book.

- Ignore bank transactions.

- Goods purchased by credit are not entered in cash book.

- Draw the format and enter the transaction, as per the format and enter the transactions as per the procedure already explained.

Cash Book (Single Column)

OBJECTIVE 7: MEANING AND FORMAT OF DOUBLE COLUMN CASH BOOK (CASH BOOK WITH DISCOUNT AND CASH COLUMN)

When cash discounts are allowed and received, one more column on the debit side for discount is allowed and another column on the credit side of the cash book for discount is received. In the double column cash book, cash column is balanced like any other ledger account. But the discount column is not balanced as it is a nominal account. It is to be totalled, not to be balanced.

Format of (Two) Double Column Cash Book (Cash Book with Discount and Cash Column)

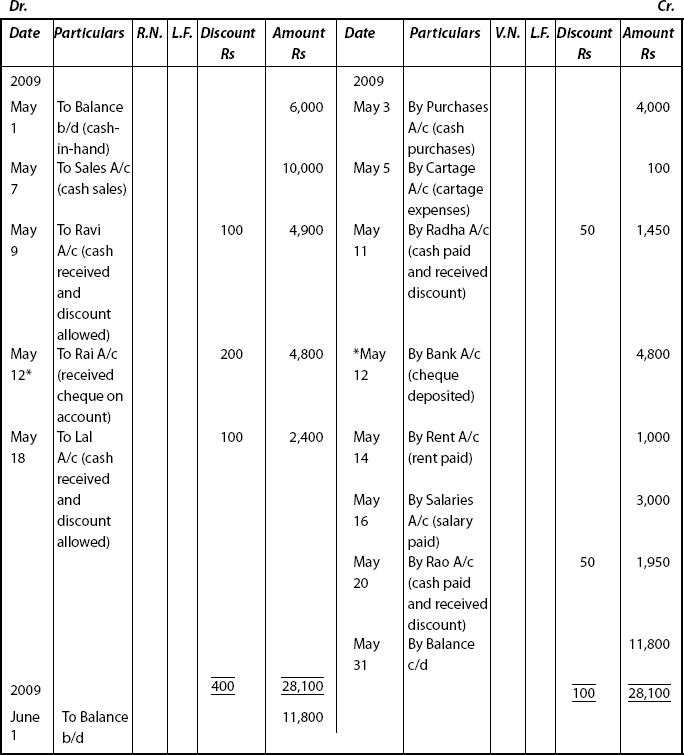

Illustration: 2

Prepare a two column cash book from the following transactions of Mr. Ravisankar.

2009 |

|

|

Rs |

|

May |

1 Cash-in-hand |

6,000 |

|

|

3 Cash purchase |

4,000 |

|

|

5 Cartage paid |

100 |

|

|

7 Cash sales |

10,000 |

|

|

9 Cash received from Ravi |

4,900 |

|

|

and allowed him discount |

100 |

|

|

11 Cash paid to Radha and |

1,450 |

|

|

discount received |

50 |

|

|

12 Received cheque from Rai and |

4,800 |

|

|

allowed him discount |

200 |

|

|

14 Rent paid |

1,000 |

|

16 Salaries paid |

3,000 |

|

|

|

18 Cash received from Lal |

2,400 |

|

|

and allowed him discount |

100 |

|

|

19 Cash paid to Rao and |

1,950 |

|

|

received discount |

50 |

Double Column Cash Book of Mr. Ravisankar

Note: *For transactions by cheque, its accounting treatment should be carefully recorded.

Illustration: 3

Enter the following transactions in the cash book with discount columns for the month of May 2009.

|

|

|

|

Rs |

|

May |

1 |

Cash sales |

15,000 |

|

|

2 |

Goods sold to Tandon on credit |

30,000 |

|

|

3 |

Goods purchased on credit from Hemant |

40,000 |

|

|

4 |

Cash withdrawn for L.I.C. Premium |

2,000 |

|

|

10 |

Received cash Rs 24,800 and a cheque for Rs. 5,000 from Tandon as a fi nal settlement |

|

|

|

12 |

Cash sale of goods; Cash sent to Bank |

17,000 |

|

|

14 |

Paid Hemant Rs 20,000 cash and the balance Rs 19,800 by cheque and his account was closed |

|

|

|

15 |

Received from Ashok cash |

50,000 |

|

|

|

and allowed him discount |

1,000 |

|

|

16 |

Received insurance claim |

2,000 |

|

|

17 |

Cash recovered from Sachin, which was written off bad in January |

7,500 |

|

|

19 |

Withdrawn from Bank |

3,500 |

|

|

20 |

Withdrawn from offi ce to meet the medical expenses of the proprietors parents |

2,500 |

|

|

21 |

Parents deposited with Bank |

25,000 |

Solution

Notes:

|

May 4 |

Cash withdrawn for L.I.C. premium is a personal expense. It has to be recorded as Drawings A/c. |

|

May 12 |

There are two transactions. Entries should appear on both sides. |

|

May 16 |

Insurance claim is to be treated as business receipt. |

|

May 17 |

As debts is written off, the name of such debtors is to be removed from the books. As such, the amount recovered is recorded as “Bad Debts Recovered Account.” |

|

May 19 |

Withdrawal from bank is treated as business use, as no other words are mentioned specific. |

|

May 20 |

Personal expense – “Drawings A/c” to be recorded. |

General Note: Credit transactions should not be recorded in cash book.

Cash Book with Discount Columns

OBJECTIVE 8: METHOD OF ENTERING BANK TRANSACTIONS IN TWO COLUMNS (BANK AND DISCOUNT COLUMN)

Now-a-days, in business enterprises almost all transactions are done only through banks. All receipts are deposited with the bank and all payments are made by cheques only. For such concerns, Bank Column in the place of Cash Column will serve the purpose. No change regarding “Discount Column” takes place. Such a cash book is called as “Cash Book with Bank Column and Discount Column.”

Illustration: 4

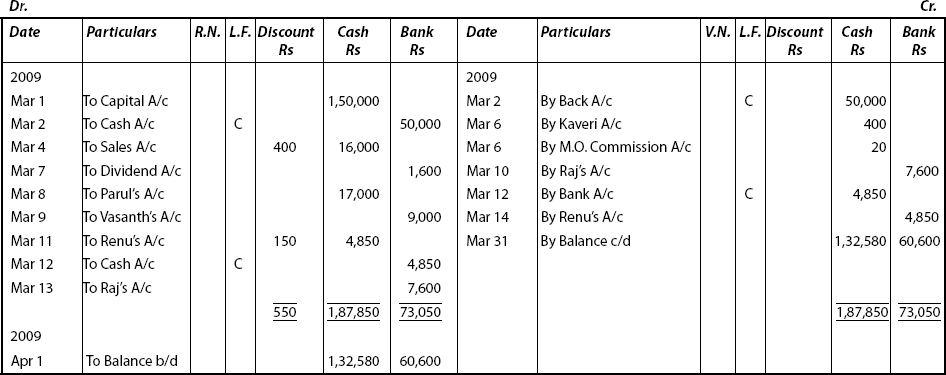

From the following transactions of Mr. Ganesh, prepare a cash book with bank and discount columns for the month of Mar 2009.

|

Mar 1 |

Bank balance was Rs 20,000 as per his cash book. The counter-foils of his pay-in-slips provide the following information: |

|

Mar 5 |

Total deposits Rs 40,000 consisting of Rs 28,000 from cash sales, a cheque from Panda for Rs 10,000 and a cheque of Rs 1,900 from Lata in full settlement of her account of Rs 2,000. |

|

Mar 15 |

Total deposits of Rs 50,000 consisting of sale of Surya for Rs 40,000 and Cash sales of Rs 10,000. |

|

Mar 26 |

Total deposits of Rs 25,000 comprising of Rs 23,000 from Khan for payment on account (discount allowed Rs 155), Rs 345 from sale of old articles and the balance from commission. |

|

Mar 25 |

Total outgoings of Rs 14,800 comprising of Rs 12,000 purchase and a cheque of Rs 2,800 to Balaji (discount received Rs200). |

The counter-foils of his cheque book disclose the following:

|

May 10 |

Reddy and Co. Rs 18,000 (in full settlement of Rs 20,000) |

|

Mar 13 |

Gupta Rs 8,500, discount received Rs 500 |

|

Mar 17 |

Petty cash Rs 1,200; in favour of his son Rs 5,000 |

|

Mar 19 |

Self: Rs 3,000 |

|

Mar 26 |

Purchase paid by cheque Rs 17,000 |

Two Column Cash Book (Bank and Discount Column Only)

OBJECTIVE 9: MEANING OF TRIPLE COLUMN CASH BOOK WITH DISCOUNT, CASH AND BANK COLUMNS AND PROCEDURE OF RECORDING BUSINESS TRANSACTIONS IN TRIPLE COLUMN CASH BOOKS

Large business enterprises receive and make payments in cash and by cheques. As a result, a combined cash book to record cash and bank transactions along with discount is used. This type of cash book is called as Triple Column Cash Book (or) Cash Book with Discount, Cash and Bank Column. This cash book has “Three Amount Columns” on each side (debit and credit side).

All cash receipts are entered in the debit side cash column and all cash payments are recorded in the credit side cash column. Discount allowed and discount received are recorded in the usual manner, that is, discount allowed on the debit side and discount received on the credit side of the cash book. Cheques received are entered on the debit side in the bank column and payments by cheques are entered on the credit side in the bank column.

The following procedure has to be followed in addition:

- Cash paid into bank or deposit of cash in bank: In this type of transaction, cash goes out of the business, a decrease in cash balance, cash comes into the bank, an increase in bank balance. As such, bank column is to be debited and cash column is to be credited. Such an entry affects both cash and bank accounts. This is known as a Contra Entry. As this cash book is a combined cash and bank account, both the aspects of transaction must be entered in the same book.

- In the Debit side, write “To Cash A/c” in the Particulars Column, write “C” (i.e., as per contra) in the L.F. Column and the amount in the “Bank Column.”

- In the Credit side, write “By Bank A/c” in the Particulars Column, put the letter “C” in the L.F. Column and enter the amount in the “Cash Column.”

- Cash withdrawn from the Bank: Both the cash and bank balances are affected. Hence it is also a Contra Entry.

In the debit side, write “To Bank A/c” in the Particulars Column, letter “C” in the L.F. Column and the amount in the Cash Column.

In the credit side, write “By Cash A/c” in the Particulars Column, the letter “C” in L.F. Column and the amount in the Bank Column.

- Payment by cheque: When payment is made by cheque, cash is not affected. As such, only one entry is enough.

Enter in the credit side of the cash book – write the name in whose favour the cheque stands in the “Particulars Column” and the amount in the “Bank Column.”

- Receiving cheques and depositing in the Bank:

- The receipt and deposit of the cheque takes place on the same date:

Only one entry is made of the customer from whom it is received in the “Particulars Column” and the amount in the “Bank Column.”

- If the cheque is received on one date and deposited on the other date:

- On receipt of cheque:

In the debit side: Write the name of the customer from whom cheque is received in the “Particulars Column” and enter the amount in the “Cash Column.”

- On depositing the cheque:

Contra Entry:

In the debit side: Write “To Cash A/c” in the “Particulars Column”, the letter “C” in the “L.F. Column” and the amount in the “Bank Column.”

In the credit side: Write “By Bank A/c” in the “Particulars Column”, the letter “C” in the “L.F. Column” and the amount in the “Cash Column.”

- On receipt of cheque:

- The receipt and deposit of the cheque takes place on the same date:

- Bank charges: Enter in the credit side of the cash book. Write “Bank Charges A/c” in the Particulars Column and the amount in the “Bank Column.”

- Periodic interest allowed by the Bank: Entry is made in the debit side of the cash book. Write “Interest A/c” in the Particulars Column and the amount in the “Bank Column.”

Important Note

- For the transaction “Receipt and Deposit a cheque” in the Bank [Ref: 4 above], if two different dates for receipt and deposit are not given (or silent on the date, i.e., no date is provided), we have to take into account that the cheque received are deposited immediately into the bank on the SAME DAY.

- As mentioned earlier, the cash book always show the debit balance. But the Bank Column may at times show credit balance.

Illustration: 5

Record the following transactions in the cash book with cash and bank column (Three Column Cash Book).

|

2009 |

|

|

Rs |

|

May |

1 |

Cash balance |

500 |

|

|

|

Bank balance |

1,000 |

|

|

2 |

Deposited into Bank |

10,000 |

|

|

3 |

Cash received from sale of shares |

50,000 |

|

|

4 |

Purchases by credit |

15,000 |

|

|

5 |

Purchases by cheque |

5,000 |

|

|

6 |

Received cheque from Anand |

9,900 |

|

|

|

Discount allowed |

100 |

|

|

7 |

Paid Vijay by cheque |

1,500 |

|

|

8 |

Withdrew from Bank for office use |

10,000 |

|

|

9 |

Anand’s cheque deposited in the Bank |

|

|

|

10 |

Paid to Ajay by cheque Rs 1,980 in full |

|

|

|

11 |

Drawn from Bank |

500 |

|

|

12 |

Cash withdrawn for personal use |

1,000 |

Solution

Notes:

- Transactions on May 2, 8, 9 and 11 are recorded as Contra entries.

- Cheque received from Anand on May, 6 was deposited on another date, that is, on May 9.

- Credit purchase is not entered in cash book.

- Drawn from bank is meant for offi ce use only.

Cash Book with Discount, Cash and Bank Columns

Note:

- Transactions involving Contra Entry have to be entered carefully by denoting letter “C” in L.F. Column.

- Discount Column need not be balanced. They are only totalled.

Illustration: 6

Enter the following transactions in the three column cash book of Bhagya Shree.

|

2009, Mar |

1 |

Bhagya Shree started business with cash Rs 1,50,000 |

|

|

2 |

Deposited into bank Rs 50,000 |

|

|

4 |

Sold goods to Sathyan for Rs 20,000, cash discount allowed 2% and received cash for the balance |

|

|

5 |

Bought goods Rs 20,000 on credit |

|

|

6 |

Sent to Kaveri by money order Rs 400, the money order commission Rs 20 |

|

|

7 |

Dividend collected by the bank as per Pass Book Rs 1,600 |

|

|

8 |

Received repayment of loan from Parul Rs 17,000 |

|

|

9 |

Vasanth, one of our customers, paid directly into the Bank Account Rs 9,000 |

|

|

10 |

Cheque issued in favour of Raj, for the purchase of office equipment Rs 7,600 |

|

|

11 |

Renu settled her account for Rs 5,000 by giving cheque for Rs 4,850 |

|

|

12 |

Renu’s cheque sent for collection to the bank |

|

|

13 |

Raj, to whom she issued a cheque was dishonoured |

|

|

14 |

Renu’s cheque returned dishonoured |

Solution

Notes:

|

Mar |

1 |

Business started with cash is entered as “Capital A/c” |

|

|

2 |

Contra Entry |

|

|

5 |

Goods purchased on credit is not entered in cash book |

|

|

6 |

M. O. commission is treated as expense |

|

|

7 |

Dividend collected by bank entered in Bank Column directly |

|

|

8 |

Repayment of Loan – Personal, entered as Parul’s A/c |

|

|

9 |

Vasanth’s direct payment to bank – direct entry in the Bank Column |

|

|

12 |

Contra Entry |

|

|

13 |

Our enterprise’s cheque dishonoured – entered in the debit side |

|

|

14 |

Customer’s cheque dishonoured – entered in the credit side |

Cash Book with Discount, Cash and Bank Column

OBJECTIVE 10: MEANING, SALIENT FEATURES AND ADVANTAGES OF PETTY CASH BOOK

10.1 Meaning

In every business enterprise, whatever may be its size, there are a large number of transactions of small value of money and that too in cash. Some such transactions are postage, travelling expense, printing, carriage and the like. Such expenses are repetitive in nature.

A cash book in which transactions of an enterprise, having small value and of recurring nature are recorded is called “Petty Cash Book.” It is also a subsidiary book.

Expenses incurred in these transactions are of small value. Those transactions occur again and again and often. Further these expenses are to be paid in cash.

Petty Cashier: A person who maintains the petty cash book is called the Petty Cashier. That person – the petty cashier is a cashier in addition to others who maintain other type of subsidiary books. The petty cashier receives a quantum of amount for the estimated expenses for a specified period of time, often. He is authorised to make payment against vouchers.

Imprest System: Imprest means “money advanced on loan.” The method of dealing with petty cash payments is called the “Imprest System.”

How does it function: Under imprest system, a specified amount is sanctioned to the petty cashier. To begin with, that is, at the beginning of the accounting period, this specified amount is given to the petty cashier. At regular intervals or when the petty cashier spends the entire amount allotted to him, he is given a new cheque for the exact amount spent by him. Hence, the petty cashier has the same fixed amount at the beginning of each new period. The specified sum is referred to as the imprest amount. This type of reimbursement of amount spent by the petty cashier at fixed period is known as the imprest system of petty cash.

10.2 Advantages

- Recording petty expenses is relatively a very simple task.

- The Petty Cash Book can be maintained by persons who even do not have specialised knowledge of accounting.

- The chief cashier is relieved to a great extent from the cumbersome work of maintaining a large number of transactions of small value.

- It requires minimum time in recording and maintaining petty cash books. Even in the ledger, only totals are posted.

- At each time of reimbursement, the chief cashier checks the amount spent by the petty cashier. This process minimises the chances of mistakes and frauds.

- As it facilitates the task of internal check by the main cashier, it enhances the responsibility and accountability of the petty cashier. The efficiency of cash management is strengthened at the grass root level.

10.3 Salient Features

This is also known as “Column Cash Book” because this book consists of many columns. For each petty expense, there is a separate column. This book also has both debit and credit side. But the debit side column is so small because cash received from the main cashier has to be entered only once for the period. The credit side is so vast in order to accommodate all petty expenses, a separate column for each important item of such petty expenses. Each petty payment is first entered in the total payment column, and then recorded in the respective analytical column.

OBJECTIVE 11: FORMAT AND METHOD OF RECORDING TRANSACTIONS IN THE ANALYTICAL FORM OF PETTY CASH BOOK

11.1 Format of Analytical Petty Cash Book of…

Analytical Petty Cash Book

11.2 Explanations of Column and Procedure for Recording

1. Receipt: Opening balance is shown in this column along with the amount received by the petty cashier is recorded in this column.

2. C.B.F.N. Cash Book Folio Number, that is, the page number of the cash book where the cash paid by the cashier is to be recorded in this column.

3. Date: Date of receipt or date of payment is recorded.

4. Particulars: Details of receipts and payments are written as “To Cash.” All payments of petty expenses are written as “By …….” (name of the expense).

5. V.N: The serial number of voucher (Payment of cash) is recorded.

6. Total Payments: Amount of every expense is written. At the end of the stipulated period, expenses are totalled. The total expenses in this column is compared with the total of the receipts column and the balance is arrived at.

(7 to 11) |

Column representing the category of expense for various items have to be recorded separately. In case, if the item of expense cannot be classified, such expenses can be recorded in the column “Sundries.” To put in other words, expenses which do not have specific columns, are to be entered in this column. |

12. L.F: Page number of ledger (where the respective account is recorded) is shown here.

13. Personal Account: Payments made to individuals (small account) are recorded in this column.

11.3 Balancing Procedure

At the end of the specified period, the Total Payments Column are totalled. Then individual payments column are totalled. Both should be always equal.

After ascertaining this, the total payments thus arrived at, shall be compared with the total amount received from the Receipt column and the balance is obtained.

The closing balance is recorded as “By Balance c/d.” The closing balance is carried forward to the beginning of the next period and is written as “To Balance b/d” in the Particulars Column.

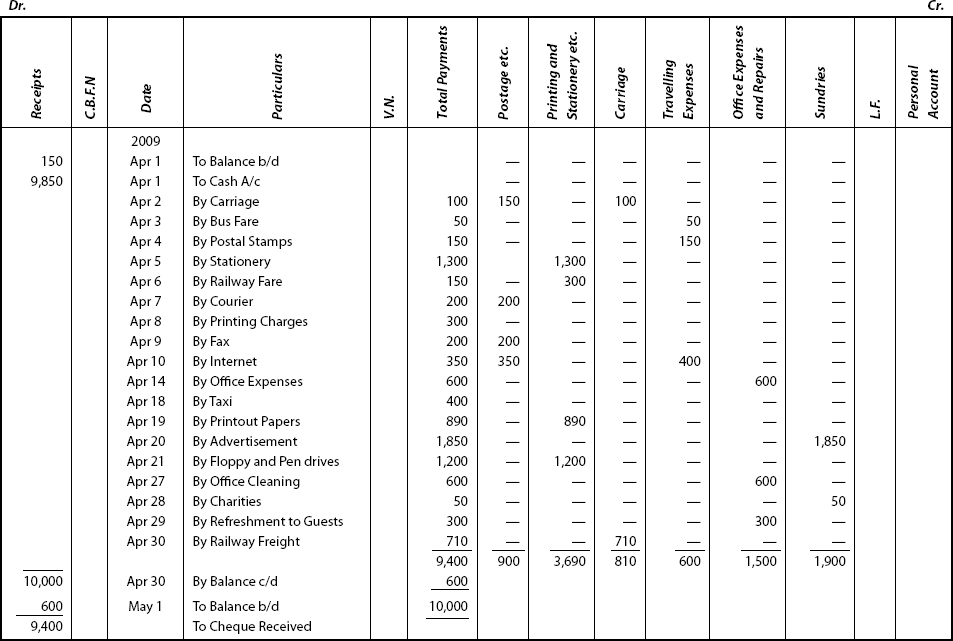

Illustration: 7

On Apr 1, 2009 a cheque of Rs 9,850 was given to the petty cashier to pay petty cash expenses for which the transactions are as follows:

|

|

|

|

Rs |

|

Apr |

1 |

Petty cash-in-hand |

150 |

|

|

2 |

Carriage |

100 |

|

|

3 |

Bus fare |

50 |

|

|

4 |

Postal stamps |

150 |

|

|

5 |

Stationery |

1,300 |

|

|

6 |

Railway fare |

150 |

|

|

7 |

Courier service expenses |

200 |

|

|

8 |

Printing charges |

300 |

|

|

9 |

Fax expenses |

200 |

|

|

10 |

Internet expenses |

350 |

|

|

14 |

Office expenses |

600 |

|

|

18 |

Taxi |

400 |

|

|

19 |

Paper to take print outs |

890 |

|

|

20 |

Advertisement |

1,850 |

|

|

21 |

Floppy and Pen drives |

1,200 |

|

|

27 |

Office cleaning |

600 |

|

|

28 |

Charities |

50 |

|

|

29 |

Refreshment to customers in the form of cool drink/coffee who visit office |

300 |

|

|

30 |

Railway freight |

710 |

Enter these transactions in the analysis form of petty cash book.

Analytical Petty Cash Book

11.4 Passing of Journal Entries

1. On receipt of advance:

Petty Cash A/c Dr.

To Cash A/c

2. On totalling of various petty expenses:

- …… A/c

(Name of Expenses) Dr.

- …… Dr.

- …… Dr.

To Petty A/c

11.5 Posting to Ledger

- A Separate Petty Cash Account is opened. Petty Cash A/c is to be debited and total of all expenses will be credited under the head Sundries. Then this account has to be balanced. This balance will be shown in the Balance Sheet as part of cash balance.

- Then individual ledgers for all times of expenses have to be opened.

Taking the figures format from the previous Illustration 7, the procedure for passing journal entries and posting is described as below:

Journal

Petty Cash A/c

Postage A/c

Printing and Stationery A/c

Carriage Account

Travelling Expenses A/c

Office Expenses A/c

Sundries A/c

OBJECTIVE 12: PURCHASES BOOK – MEANING AND FORMAT AND METHODS OF PREPARING PURCHASE BOOK AND LEDGER ACCOUNTS

12.1 Meaning of Purchase Book

This is another special subsidiary book. Transactions relating to goods purchased on credit, which are meant for resale are to be recorded in this book. This is also called as Bought Day Book. Hence, the two essential ingredients of a transaction to be recorded in the Purchases Book are:

- Purchase of goods for resale only.

- Purchase of goods on credit basis only.

Hence, cash purchase of goods are not to be recorded in the Purchases Book. And purchase of assets (cash and credit) should not be recorded in this book of original entry.

Before going to the main part of recording business transactions in “Purchases Book,” one has to understand the following terms (which have been discussed already refer Chapter 4b) – Invoice, Cash Discount and Trade Discount. No need to explain again in detail. Just to remind they are put in short version:

Invoice: It is a statement of goods bought item-wise, price-wise.

Cash Discount: This discount is allowed to customers to encourage prompt payment within a short, stipulated time. An important part to be noted is that this discount is not deducted from invoice price. It is shown in the books of accounts by opening separate account.

Trade Discount: This discount is allowed to customers and is deducted from the list price. It is not shown in the books of accounts. This may be in the form of a certain quantity or a certain amount.

12.2 Format

Purchases Book

12.2.1 Explanation and Procedure of Recording

|

Date Column |

Enter the date on which the transaction takes place. |

|

Particulars Column |

Name of the seller (supplier) and the particulars of goods purchased are shown in the column. |

|

Inward Invoice No. Column |

The serial number of the inward invoice is to be entered. |

|

L.F. Column |

The page number of the suppliers account in the ledger account is to be entered. |

|

Details Column |

The amount of goods purchased and the amount of trade discount are entered. |

|

Total Column |

The net price of goods (after adjusting discount and expenses), that is, the amount which is payable to the creditors will have to be recorded. |

|

Remarks |

Any additional information has to be shown in this column. |

Illustration: 8:

Prepare the Purchases Book and ledger accounts related to this, from the following transactions of Good Luck Enterprises for June 2009.

|

2009 |

|

|

June 8 |

Bought from Vivek and Co. on credit: |

|

|

10 Washing Machines @ Rs 9,000 |

|

|

5 Micro Wave Ovens @ Rs 7,000 |

|

|

Trade Discount @ 20% |

|

June 15 |

Purchased for cash from Rahman and Bros. |

|

|

2 Computers @ Rs 47,500 |

|

June 28 |

Purchase on credit from Lalit and Co. |

|

|

2000 CDs @ Rs 25 |

|

|

100 Pen Drives @ Rs 500 |

|

|

Trade Discount @ 10% |

|

June 29 |

Purchased on credit, from Robert and Bros. |

|

|

2 Lap-Tops @ Rs 80,000 |

Solution

Books of Good Luck Enterprises Purchases Book

Notes:

- Cash purchase on June 15, is not recorded in Purchases Book.

- Even though Lap-tops are purchased on credit, it is presumed that they were not for resale. As such it is also not shown in this account.

- Trade Discount is calculated and deducted.

Ledger Accounts Purchases Accounts

Vivek and Co. Account

Lalit and Co. Account

Illustration: 9

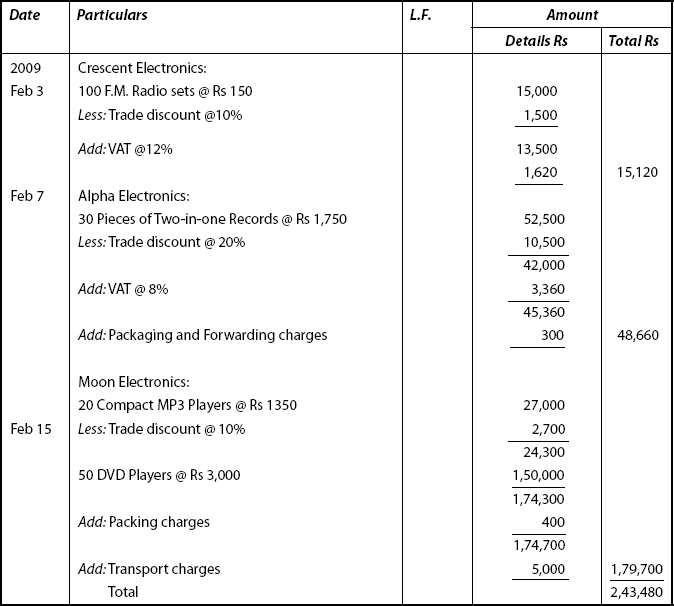

Modern Electronics purchased the following goods on credit during February 2009. Enter them in the Purchases Book.

|

2009 |

|

|

Feb 3 |

Bought from Crescent Electronics, 100 F.M. Radio sets @ Rs 150 per set. Trade discount @ 10%. VAT paid by us @ 12%. |

|

Feb 7 |

Purchased from Alpha Electronics, 30 pieces of Two-in-one Tape Records @ Rs 1,750. Trade discount 20%. Packing and forwarding charges Rs 300. VAT @ 8%. |

|

Feb 15 |

Purchased from Moon Electronics, compact MP3 Players @ Rs 1,350-20 players. Trade discount 10%. DVD players 50 pieces each costing Rs 3,000. Packing charges Rs 400. Transport charges Rs 5,000. All expenses to be borne by purchasing firm. |

Solution

First, Trade discount is to be deducted.

Then, from the total amount, that is, after deducting trading discount, VAT and Packing and to forwarding charges are added one after the other separately.

Modern Electronics Purchase Book

OBJECTIVE 13: MEANING, FORMAT AND FEATURES OF SALES BOOK

This is another unimportant subsidiary book. This is also called as Sales Day Book. All credit sales of goods (dealt by the trader in his business) are recorded in this book. Cash sales of goods and sale of assets (cash as well as credit) and sale of goods other than those involved in this business on credit are not recorded in this book.

13.1 Format of Sales Book

Sales Book

13.2 Explanation and Procedure for Recording Transaction

Date |

Date on which the transaction takes place is entered in this column. |

Outward Invoice No. |

The serial number of outward invoice is written in this column. |

The name of purchasers and details of goods sold are recorded in this Particulars Column. | |

L.F |

The page number of the customers’ accounts in the ledger is shown in this Ledger Folio Column. |

Amount Details |

Amount of goods sold (and trade discount amount) is recorded in this column. |

Amount Total |

The net amount, which is receivable from the customers is to be recorded in this column. |

Illustration: 10

From the following transactions, prepare the Sales Book of Venkatesh for Apr 2009 and necessary ledger accounts related to it.

2009 |

|

Apr 2 |

Sold on credit to Sun Traders 10 Titan watches @ Rs 1,500 10% discount is allowed. |

Apr 5 |

Sold to Banu for cash 5 Titan (crystal) watches @ Rs 2,000. |

Apr 7 |

Sold to Singh and Co. 10 Titan (digital) watches @ Rs 2,500 10% discount is allowed. |

Apr 10 |

Sold on credit an old show case Rs 9,000. |

Solution

In the Books of Venkatesh Sales Book

Note:

Apr 5: Cash sales is not recorded in Sales Book.

Apr 10: An old show case (the firm does not deal in furniture) is not entered. Only credit sale of merchandise is recorded.

But, in practice, only net amount is recorded, as details can be had from respective Invoice. It is shown as below:

Sales Book (Sales Journal)

Ledger Accounts Sales Account

Sun Traders Account

Singh and Co. Account

Illustration: 11

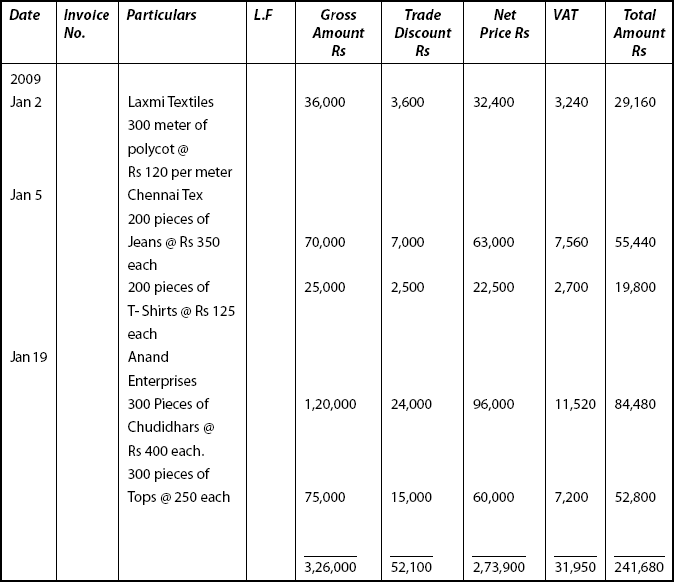

Enter the following transactions in Sales Day Book and post them to ledger.

2009 Jan 2 |

Sold to Laxmi Textiles, 300 metres of polycot quality @ Rs 120 per metre. Trader discount 10%, VAT @ 10%. |

Jan 5 |

Sold to Chennai Tex, 200 pieces of Jeans @ Rs 350 each; 200 pieces of T-shirts @ Rs 125 each. Trade discount @ 10%, VAT @ 12%. |

Jan 19 |

Sold to Anand Enterprises, 300 pieces of chudidhars @ Rs 400 each; 300 pieces of Tops @ Rs 250 each. Trade discount 20%. VAT @ 12%. |

|

Use separate columns. |

Solution:

This can be depicted in columnar Sales Book as follows:

Columnar Sales Book

Columnar Sales Book Ledger Accounts Sales Account

Vat Payable Account

Laxmi Textiles Account

Chennai Tex A/C

Anand Enterprises Account

OBJECTIVE 14: MEANING AND FEATURES OF PURCHASES RETURNS BOOK

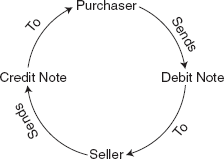

The return of goods by the purchaser to the seller is called as Purchaser returns or Returns outwards. The transactions relating to Purchases returns and recorded in a separate book (subsidiary book or book of original entry). This book is known as Purchases Returns Book. This book is used to record the returns of goods by the purchaser to the seller.

But, generally the transactions in Purchase Returns Book are recorded on the basis of “Debit Note.” A debit note is a source document. It is prepared by the purchaser to be sent to the seller. Main object is to inform the supplier that his account has been debited with the amount mentioned and for the reasons stated in.

We call it a debit note because the supplier’s account is debited with the amount (value of goods returned). The same note acts as a ‘credit note’ from the supplier’s point of view because he will credit the account of the purcher from whom the supplier has received that note along with goods. The flow of note (debit note and credit note) is represented as:

Format of Purchases Returns Book

14.1 Explanation and Procedure for Recording Purchases Returns Transactions

Date |

The date on which the goods were returned to the suppliers is entered in this data column. |

Particulars |

The suppliers name, description of goods, trade discount percentage-all are recorded in this particulars column. |

Debit Note No. |

The serial number of the Debit Note prepared by the purchaser is shown. |

L. F. |

The page number of suppliers A/c entered in ledger account is entered here. |

The amount of goods returned, trade discount amount are recorded in this column. | |

Total |

The net value of goods (after adjustments) is to be recorded in this column. |

Remarks |

Reasons for return of goods are recorded in this column. |

General reasons for return of goods are:

- Goods are spoiled

- Damaged in transit

- Excess of quantity than in the order

- Inferior in quality

- Not supplied in time

- Mechanical defects.

Start any of the seasons in short short-version.

Note:

- Net value of goods is determined after deducting trade discount.

- Allowances, if any are to be deducted.

14.2 What is an ‘Allowance’?

Under certain circumstances, it may not be possible to return goods physically due to reasons beyond control. In such a situation, the supplier compensates the purchaser by extending concessions in the form of monetary value. This is known as allowance. To put it in other words, allowance means reduction in the amount of purchase price payable by the purchaser, allowed by the supplier.

14.2.1 Accounting Treatment

Such an allowance is recorded in the Purchase Returns Book (amount will be equal to the net price of goods to be returned). (Supplier) Seller is debited with that amount of allowance.

This amount is debited from the total amount of purchases while preparing Trading Account.

Illustration: 12

Enter the following transactions in the Purchases Returns Book of Veena Traders and prepare the ledger books related to it:

|

2000 |

May 10 |

Returned to Sonal Enterprises 5 kgs of Coffee Powder @ Rs 200 per kg. net |

|

|

May 16 |

Returned to Moonar Tea Co, 20 kgs of Tea Dust @ Rs 180 per kg.net |

|

|

May 20 |

Returned to Aruna Sugars 100 kgs of Sugar @ Rs 12 per kg. net (Trade discount @ 10% to all the goods applicable) |

Solution

In the Books of Veena Traders Purchases Return Book

Ledger Accounts In the Books of Veena Traders Purchase Return Book

Sonal Enterprises Account

Moonar Tea Co Account

Aruna Sugars Account

OBJECTIVE 15: MEANING AND FEATURES OF PURCHASES RETURNS BOOK

This is another special subsidiary book. This book is used to record the goods returned to the business enterprises by the customers. As goods are coming into the business, this is also known as Returns Inward Book. The entries in the Sales Return Book are made on the basis of credit notes.

In fact, when the goods are sold to the customers, their accounts are debited. Hence, when the goods are returned by the customers, the business firms will have to credit their accounts. This is carried on by sending a Credit Note to the customers.

15.1 Format

Sales Returns Book

Explanation and Procedure for recording transactions:

|

Date |

The date on which sales return took place is shown in this column. |

|

Particulars |

The name of the customers who returned the goods, details of goods and discount terms are recorded in this column. |

|

Credit Note No. |

The serial number of Credit Note is entered here. |

|

L.F. |

This column shows the page number of customer’s account in the ledger column |

|

Details |

Amount of goods and amount of discount are to be recorded in this column |

|

Total |

The net amount (after adjustments) is recorded in this column. |

|

Remarks |

Reasons for goods returned by customers are recorded in this column |

Illustration 13

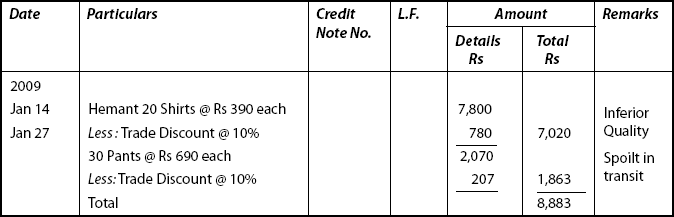

Enter the following transactions in the books of Tiwari and post them to the ledger:

|

2009 Jan 14 |

Returned by Hemant 20 shirts each costing Rs, 390 each Trade discount 10% |

|

2009 Jan 27 |

Returns from Pande 30 Pants each costing Rs 690 each Trade discount 10% |

Solution

In the Books of Tiwari Sales Return Book

Sales Returns Account

Hemant Account

Pande Account

OBJECTIVE 16: MEANING OF BILLS OF EXCHANGE SPECIMEN AND MEANING OF SOME IMPORTANT TERMS

16.1 Bills of Exchange

Detailed procedure for recording transactions relating to bills of exchange is not explained in this chapter. Only certain important terms relating to bills are discussed in this chapter, which are needed to understand how does it act as a source document.

Bill of Exchange’s role in credit transactions attains much significance. “Bill of Exchange is an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money. Only to, or to the order of a certain person or to the bearer of the instrument.”

16.2 Specimen or Format of Bill of Exchange

Stamp |

1015, Babu Market |

|

New Delhi-23 |

Rs 25,000/- |

1-3-2009 |

Two months after date Pay to me or to my order the sum of Rupees Twenty Five Thousand only for value received.

Sameer

To

Mr. Jaleel

3012-C, Janpath,

Bhubaneswar

16.3 Meaning of Important Terms

- Drawing of a bill: The creditor (seller) prepares the bill. The act of preparing the bill in its complete form with his signature is called “Drawing” a bill.

- Parties to a bill:

- Drawer: The person who prepares the bill is called the “Drawer”. (He is the creditor or seller). In the format, Sameer is the Drawer.

- Drawee: The person who accepts to make the payment is called the “Drawee.” (He is the debtor). In the above format Jaleel is the Drawee.

- Payee: The person who receives the payment is called “Payee.” The payee may be the drawer or some third party. In the above format, Sameer himself is the Payee.

Acceptance: In a bill, the drawee gives his acceptance by writing the word “Accepted” and signing with date. In this format, the drawee, Jaleel writs accepted and signs with date. This process is termed as “Accepted.” Once a bill is accepted, then the bill attains the legal status under the Negotiable Instruments Act 1881.

Endorsement: In order to transfer the title of the bill to another person, one signs on the face or on the backside of the bill. This is called “Endorsement”. The person who endorses (signs) is called “Endorser’. The person to whom a bill is endorsed is called “Endorsee”. The endorsee thereby acquires the title of the Bill (property).

Due date: The date on which the payment has to be made is called “Due Date”. In the above format, the date of bill is 1.3.2009. Here, the bill is payable after a specified period i.e. two months (i.e.) 1.5.2009 (May 1).

Day of Grace: In practice, three extra days are given. These three days have to be added with the due date i.e. 1.5.2009 + 3 days = 4.5.2009 (4th May). These three extra days allowed is called “Days of Grace” as such the due date of this bill is 4.5.2009. If this date is notified as holiday under Negotiable Instrument Act, then the previous day i.e. 3.5.2009 will be the due date.

Discount: If a person, wants money before the due date, he may do so by surrendering the for a lesser amount with a bank. This is called “discounting of a bill.” The banker deducts a certain amount from its face value, i.e. the amount written on the bill. This is called discount. He can get the balance immediately.

Retirement: Under certain circumstances, before the due date, payment is made by an acceptor. His liability is discharged thereby. This is called “retirement.” In such a case, the holder of the bill allows a concession called rebate in order to compensate the drawee for the unexpired period of the “Bill”.

Dishonour and Noting: If the obligation of payment is not fulfilled, on its presentation demanding payment. Then it is called “Dishonour of Bill.”

In case if the bill is dishonoured, the drawer of the bill can approach the court to recover the amount for documentary evidence, he has to approach a lawyer, who in turn after proper enquiry with the drawee, the lawyer gets the document signed by the drawee, endorsed by the lawyer. This process is called “noting.” The certificate issued by the lawyer (Notary Public) is called “Protest.”

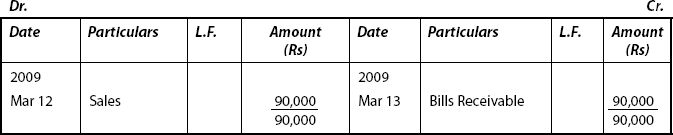

OBJECTIVE 17: PROCEDURE OF RECORDING TRANSACTIONS IN B/R AND B/P BOOKS

17.1 Bills Receivable and Bills Payable Books

When large number of bills are drawn and accepted, passing journal entries for each and every transaction relating to the bills will be an arduous task. Hence it becomes necessary to record them in Special Subsidiary Books called the Bills Receivable Book and Bills Payable Book. These special subsidiary books record only the transactions relating to “drawing” and “acceptance” of bills. All the other transactions relating to bills such as endorsement, discount, retirement, renewal and so on are not recorded in these subsidiary books.

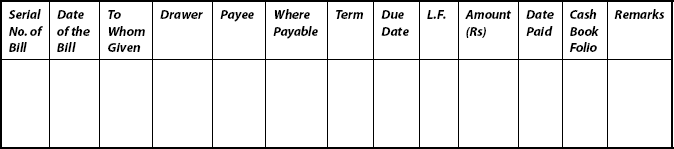

17.2 Bills Receivable Book

This book consists of a summary of transactions regarding a duly accepted bill received by a drawer. Main object of this book is to provide a future reference, despite the fact that this book contains other details of a bill. The name of the acceptor (debtor) due date, the amount and terms of payment are to be recorded in Bills Receivable Book.

17.2.1 Proforma of Bills Receivable Book

Bills Receivable Book

17.3 Bills Payable Book

This is also a Special Subsidiary Book. All the particulars of Bills Payable (proforma specimen shown in page 36) accepted by a person or party for the purpose of paying the amount at a future date to its creditors.

17.4 Posting of Bills Receivable and Bills Payable Books

17.4.1 Bills Receivable Book

This is totaled periodically as other subsidiary books. The total is debited to the Bills Receivable Account. The account of every individual debtor from whom the bills have been received, is credited in the ledger. The Bills Receivable Account is the account of an asset and as such it will always have a debit balance. The debit balance on any date will represent the amount of bills receivable unmatured and on hand.

17.4.2 Bills Payable Book

Amount of each bill payable is posted to the debit side of the drawer’s account. The total of the amount column in the Bills Payable Book is credited to Bills Payable Account. Bills Payable Account will always have a credit balance. The credit balance of this account on any date will be the same as the total amount worth of bills yet to be presented for payment.

Proforma (Specimen) of Bills Payable Book

Illustration: 14

Record the following transactions in Bills Receivable and Bills Payable Books alongwith postings in the ledge accounts:

|

2009 |

|

|

Mar 1 |

Received from Srinivasan bill duly accepted for Rs 1,27,500 dated Feb 20, 2009 payable three months after date |

|

Mar 7 |

Accepted Vasu’s draft for 77,000 at two months |

|

Mar 10 |

Prabhu drew on his trader at three months date and the same was accepted for Rs 50,000 |

|

Mar 12 |

Drew on Rajesh at two months for Rs 90,000 and was accepted by him the next date (day) |

|

Mar 16 |

Gave acceptance at three months for Rs 27,000 to Shiva |

|

Mar 19 |

Received from Gopi his acceptance for Rs 1,10,000 at three months |

|

Mar 21 |

Received from David, Anand’s acceptance for Rs 45,000 at two months from Mar 15 |

|

Mar 24 |

Kesav accepted my draft at two moths for Rs 27,500 |

|

Mar 27 |

Received from Satish bill for Rs 61,000 dated Mar 20, accepted by Ram and drawn by Mohan payable one month after date |

|

Mar 30 |

Gave acceptance for Rs 99,000 at two months to Arora |

Solution

Bill Receivable and Bill Payable Accounts have to be recorded after drawing the standard formats.

Then posting bill transactions from these two books to the accounts of debtors and creditors are made on the presumption that all the necessary sales and purchases entries have been duly recorded.

Bills Receivable Book

Bills Payable Book

Ledger Accounts Srinivasan’s Account

Rajesh’s Account

Gopal’s Account

David’s Account

Kesav’s Account

Satish’s Account

Bills Receivable Account

Vasu’s Account

Prabhu’s Account

Shiva’s Account

Arora’s Account

Bills Payable Account

OBJECTIVE 18: JOURNAL PROPER AND DIFFERENT KINDS OF ENTRIES

The transactions which cannot be recorded in any of the subsidiary books are entered in a book – which is known as Journal Proper. This is also called Journal Residual or General Journal.

Following transactions are recorded in Journal Proper.

- Opening Entries: In order to open new set of books in the beginning of new accounting year and record the opening balances of assets, liabilities and capital, the opening entry is made in the journal.

- Closing Entries: Closing entries are recorded at the end of the accounting year for closing accounts relating to expenses and revenues (nominal accounts). These accounts are closed by transferring the balances to the Trading and Profit and Loss Account.

- Adjustment Entries: In order to update ledger accounts, some unrecorded items like prepaid expense, depreciation are made at the end of accounting period.

- Transfer Entries: Transfer entries are passed in the journal for transferring an account from one account to another account. E.g: Drawing Account is transferred to Capital Account at the end of the accounting year. Accounts relating to operation of business like sales, income, expenses are closed at the end of the year and their total or balances are transferred to Trading and Profit and Loss Account after recording journal entries.

- Rectification Entries: Rectifying entries are passed for rectifying the various errors committed in the books of accounts such a totaling, balancing etc.

- Miscellaneous Entries or Entries of casual nature: They are:

- Purchase and sale of items on credit other than goods.

- Goods withdrawn for personal use by the owner

- Endorsement of bills receivable to a creditor

- Dishonour and cancellation of bills.

- Goods distributed as samples for sales promotion

- Transactions relating to consignment and joint venture

- Loss of goods by theft, spoilage etc

- Bad Debts written off

Illustration: 15

|

2009 |

Mar 1 |

Purchased on credit two computers with system for Rs 50,000 from Delhi Computers. |

|

|

Mar 3 |

Purchased on credit from Tiruppur Tex, 100 hosiery products @ Rs 100 each. |

|

|

Mar 5 |

Purchased for cash electronic goods Rs 40,000 from Sharma Traders |

|

|

Mar 6 |

Purchased for cash from Royal Furniture 4 chairs @ Rs 750 each |

|

|

Mar 9 |

Returned one chair Rs 750 which was purchased for cash |

|

|

Mar 11 |

Returned to Tiruppur Tex 10 hosiery products @ Rs 100 |

|

|

Mar 13 |

Returned one computer @ Rs 50,000 to Delhi computers |

You are required to pass entries in Journal Proper.

Solution

First short list the transactions which will not be recorded in the Journal Proper: (can be recorded in subsidiary books)

|

Mar |

3 |

It will be recorded in the Purchases Book |

|

Mar |

11 |

It has to be recorded in Purchases Return Book |

|

Mar |

5 |

Cash purchase is to be recorded in Cash Book |

|

Mar |

6 |

Cash purchase is to be recorded in Cash Book |

|

Mar |

9 |

To be recorded in Cash Book |

Only two transactions which cannot be recorded in other subsidiary books, have to be entered in the Journal Proper as follows:

Journal Proper

Summary

- Subsidiary Books refer to the books meant for specific transactions of a similar nature.

- Kinds of Subsidiary Books: (i) Day Books, (ii) Bill Books, (iii) Cash Book and (iv) Journal Proper

- Day Books: (i) Purchases Book, (ii) Sales Book, (iii) Purchases Returns Book, (iv) Sales Returns Book. Bill Books: (i) Bills Receivable Book and (ii) Bills Payable Book; Cash Book: (i) Single Column Cash Book, (ii) Double Column Cash Book (iii) Triple Column Cash Book and (iv) Petty Cash Book and Journal Proper are the classifications of Subsidiary Books.

- Advantages: (i) Facilitates division of labour, (ii) Delegation of work, (iii) Detection of errors, (iv) Effects saving in time and labour and (v) Facilitates quick reference

- Distinction between Subsidiary Books and Journal (ref: The Tabular Column in the Text)

- Cash Book: All cash receipts and payments are recorded from the source books chronologically. Single Column Cash Book is similar to that of Cash Account in Ledger.

- Cash Book with Discount Columns: When cash discounts are allowed and received, one more column on both sides under ‘Discount’ is added to Cash Book columns. Discount Column need not get balanced as it is a Nominal Account

- In case, if all transactions are made only through banks, Bank Column is used instead of Cash Column.

- Triple Column Cash Book i.e. Cash Book With Discount, Cash and Bank Columns are in use when transactions are by cash and through bank with discount. In this book, when cash is deposited in bank or withdrawn from the bank, Contra Entry is made. Because this book is a combination of both cash and bank accounts both the aspects of transactions have to be recorded.

- Petty Cash Book is a kind of cash book in which transactions of an enterprise having of small value and recurrence in nature are recorded.

- Purchases Book: Purchases of goods for resale ONLY and on credit basis are recorded. Entry of trade discount, VAT and packing and forwarding charges have to be recorded.

- Sales Book: All credit sales (only) are to be recorded. Cash sales, sale of assets (cash and credit) and sale of goods other than involved in his business are to be excluded.

- Purchases Returns Book: (Returns Outward) – The return of goods by the purchaser to the seller (on the basis of Debit Note) are recorded.

- Sales Return Book: (Returns Inward) – The return of goods by the customers to the enterprises (on the basis of Credit Note) are recorded.

- Bills of Exchange is an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of a certain person or to the bearer of the instrument.”

- Bills Receivable Book contains a summary of transactions regarding a duly accepted bill received by a drawer. The name of the acceptor, due date, the amount and terms of payment are to be recorded.

- Bills Payable Book is another Subsidiary Book – an instrument accepted by a person for the purpose of paying the amount at a future date to its creditors.

- Journal Proper: The transactions that cannot be recorded in any of the Subsidiary Books are entered in this book. Such entries: (i) Opening entries, (ii) Closing entries, (iii) Adjustment entries, (iv) Transfer entries, (v) Rectification entries and (vi) Some miscellaneous entries.

Note: Method or procedure of recording transactions in various Subsidiary Books is not repeated in the Summary. Hence, the students have to refer the main part of the text.

A Objective-type Questions

I State whether the following statements are True or False

- Each one of the subsidiary books is a special journal and a book of original or prime entry.

- Journal entries are passed in all the subsidiary books.

- Purchases Book records all purchases of goods by the trader.

- Purchases Return Book records the goods returned by the customers.

- Sales Book is meant for recording only credit sales of goods.

- Sales Return Book records the goods returned by the trader to suppliers.

- Bills Receivable Book records the receipt of bills

- Bills Payable Book records the acceptance of Bills Receivable.

- Cash Book is used for recording only cash transactions.

- Journal Proper is the journal which records the entries which cannot be entered in any of the subsidiary books.

- When a customer returns the goods, a Debit Note is sent to him.

- When the goods are sent to a supplier, a Credit Note is sent to him.

- Cash Book is Journal as well as Ledger.

- Closing entries are recorded in Balance Sheet.

- The source document used for recording entries in Sales Book is invoice sent out.

- The Sales Day-Book is a part of the Ledger.

- The debit notes issued are used to prepare Sales Return Book.

- Trade discount is not recorded in the books.

- Cash discount is shown in the invoice.

- In the calculation of the due date five extra days are added to the specified period of the bill are known as “Days of Grace.”

- Cash Book will always show debit balance.

- When an entry affects both cash and bank accounts, it is called a Contra Entry.

- Discount Account must be balanced in the Cash Book.

- The balance in the Cash Book shows net income.

- Petty Cash is an expense.

- A cheque received and paid into the bank on the same day is recorded in the cash column of Three Column Cash Book.

- When a cheque received from a customer is dishonoured his account is debited.

- In Triple Column Cash Book, cash withdrawn from the bank for office use will appear on credit side of the Cash Book only.

- The total of Journal Proper will be debited Cash Account.

- The total of Return Inward Book is posted to Purchase Returns Book.

Answers

1. True |

2. False |

3. False |

4. False |

5. True |

6. False |

7. True |

8. False |

9. True |

10. True |

11. False |

12. False |

13. True |

14. False |

15. True |

16. False |

17. False |

18. True |

19. False |

20. False |

21. True |

22. True |

23. False |

24. False |

25. False |

26. False |

27. True |

28. False |

29. False |

30. False |

II Choose the Correct Answer

- Purchase Book is used to record

- all purchases

- Only cash purchases

- Only credit purchases

- none of the above

- Sales Book is kept to record

- all sales of goods

- all credit sales of goods

- all cash sales of goods

- all goods sent on consignment

- Purchase of Machinery is recorded in

- Sales Book

- Purchases Book

- Cash Book

- Journal Proper

- Purchases Return Book is used to record

- returns of goods purchased on credit

- returns of goods purchased for cash

- returns of goods purchased by cash and credit

- returns of goods by the seller

- Sales Return Book is used to record

- returns of goods sold for cash

- returns of goods sold on credit

- returns of goods sold on both cash and credit

- none of the above

- On 1st May 2009, Vivek draws a bill on Bhaskar for three months, its due date is:

- 1st August, 2009

- 4th August, 2009

- 31st July, 2009

- none of the above

- The Cash Book records

- all cash payment

- all cash receipts

- all cash receipts and cash payments

- goods purchased for cash only

- The balance of Cash Book indicates

- cash in hand

- cash in bank

- net profit

- only the difference between creditors and debtors

- If a cheque issued by us is dishonoured the credit is given to:

- bank account

- supplier’s account

- customer’s account

- none of the above

- The balance in the Petty Cash Book is

- a liability

- profit

- an asset

- an income

- On 1 January 2009, Rs 1,750 was given to a petty cashier. The amount spent by him was Rs 1,250. On 1 February the cashier under the imprest system will receive:

- Rs 1,250

- Rs 500

- Rs 1,750

- Rs 3,000

Answers

- (c)

- (b)

- (d)

- (a)

- (b)

- (b)

- (c)

- (a)

- (b)

- (c)

- (a)

III Fill in the blanks with suitable word(s)

- Subdivisions of the journals into various books for recording transactions of similar nature are known as __________.

- Each one of the Subsidiary books is a special journal and a book of ________ entry.

- Purchases book is meant for recording ________.

- Only credit sales are recorded in ___________.

- Goods returned by customers are recorded in ________.

- The goods returned by their trader to suppliers are recorded in ________.

- The person who prepares the bill of exchange is called the ________.

- Bills Receivable Book records the _____ of Bills

- Entries which cannot be entered in any of the subsidiary books are entered in ________.

- When a customer returns the goods, a ________ note is sent to him.

- When the goods are sent to a supplier, a ________ note is sent to him.

- Purchase – Day-Book is a part of ________.

- Closing entries are recorded in ________.

- In general, Cash Book shows ________ balance

- Petty cash is an ________.

Answers

- Subsidiary

- Original/Prime

- Credit purchases

- Sales Book

- Sales Return

- Purchases Return

- Drawer

- Receipt

- Journal Proper

- Credit

- Debit

- Subsidiary book/ journal

- Journal Proper

- Debit

- Asset

B Short Answer-type Questions

- What is a source document?

- What is an “Invoice”?

- What is a “Cash Memo”?

- What is a “Receipt”?

- What is a “Pay-in-slip”?

- What is a “Debit-note”?

- What is a “Credit-note”?

- What do you mean by “subsidiary books”?

- What is a trade discount?

- What is cash discount?

- What is a “Purchase Book”?

- What is a “Sales Book”?

- What is a “Purchase Returns Book”?

- What is a “Sales Returns Book”?

- Define a “Bill of Exchange”.

- What do you mean by endorsement of bill?

- Explain “Returning” of a bill.

- How can a bill of exchange be renewed?

- What is Journal Proper?

- Give four examples that appear in Journal Proper.

- What do you mean by an “Opening Entry”?

- Write a note on “Closing Entries”.

- Name the parties involved in a Bill of Exchange.

- What is a Cash book?

- What are the various kinds of Cash Book?

- What do you mean by Double Column Cash Book?

- What are the contents of Triple Column Cash Book?

- What is an “Imprest System”?

- Explain: “Contra Entry”.

- What are the advantages of Petty Cash Book?

- Distinguish between trade discount and cash discount.

C Essay-type Questions

- What is a subsidiary book? Name the various types of subsidiary books. Give a specimen of each subsidiary book. Explain the procedure of posting each such subsidiary book. Explain the nature of balance of each such subsidiary book.

- What do you mean by a “Source Document”? Give some examples and explain how they act as source documents with examples.

- Despite all the subsidiary books are kept in a business enterprise, explain the necessity of passing various entries through a journal with examples.

- Distinguish between cash book with two columns and Triple Column Cash Book. Explain with illustration, how bank transactions are entered in Triple Column Cash Book.

D Exercises

1. Enter the following transactions in the Purchase Book of Mr. Ramkumar.

|

2009 |

Jan 1 |

Purchased 100 Kg of tea dust from Nilgiris and Co @ Rs 300 per kg. |

|

|

Jan 5 |

Purchased 100 Kg of coffee seeds from Coorg and Co @ Rs 350 per kg. |

|

|

Jan 10 |

Purchased 50 Kg of chicory seeds from Mysore Agencies @ Rs 100 per kg. |

|

|

Jan 15 |

Purchased coffee roaster machine from Crescent Agencies for Rs 45,000. |

2. Enter the following transactions in the Sales Day Book of King Electricals.

|

2009 |

Feb 1 |

Sold on credit to Azhar and Co: |

|

|

|

(i) 100 Osram bulbs @ Rs 190 each |

|

|

|

(ii) 100 electrical main switches @ Rs 150 each |

|

|

Feb 10 |

Sold to Thomas and Co: |

|

|

|

(i) 1 H.P. motors, 15 each at the cost of Rs 2,100 |

|

|

|

(ii) 50 fans each @ Rs 1,200 |

|

|

Feb 20 |

Sold to Bhamini Mart: |

|

|

|

(i) 15 electric chimneys @ Rs 4000 each |

|

|

|

(ii) 100 exhaust fans @ Rs 2000 each |

3. Enter the following transactions in the proper subsidiary books and post them to the respective ledger accounts:

|

2009 |

Mar 1 |

Purchased goods from Kamala and Co. Rs 25,000 |

|

|

Mar 4 |

Sold goods to Susheela Rs 15,000 |

|

|

Mar 7 |

Goods purchased from Vimala Rs 20,000 |

|

|

Mar 10 |

Sold goods to Kala Rs 22,000 |

|

|

Mar 14 |

Sold goods to Surya Rs 17,000 |

|

|

Mar 17 |

Goods returned by Kala Rs 2,000 |

|

|

Mar 19 |

Goods returned to Kamala and Co. Rs 3,000 |

|

|

Mar 21 |

Goods returned to Vimala Rs 1,250 |

|

|

Mar 23 |

Goods returned by Surya Rs 700 |

|

|

Mar 27 |

Sold goods to Vijaya Rs 12,500 |

4. Enter the following transactions in the proper subsidiary books

|

2009 |

Apr 1 |

Bought goods from Mr. A. Rs 20,000 less trade discount at 10% |

|

|

Apr 3 |

Sold goods to Mr. B Rs 25,000. Trade discount at 5% |

|

|

Apr 5 |

Purchased goods Rs 40,000 from Mr. C. Trade discount at 10% |

|

|

Apr 6 |

Returned to Mr. A. goods Rs 5,000 |

|

|

Apr 10 |

Mr. B returned goods Rs 6,000 |

|

|

Apr 15 |

Returned goods to Mr. C Rs 4,500 |

5. Enter the following transactions in the appropriate special journal of M/s Vas and Co.

|

2009 |

May 1 |

Bought goods from Mr. X Rs 30,000 as per invoice No. 15 |

|

|

May 3 |

Sold goods to Mr. Y Rs 40,000 as per invoice No. 32 |

|

|

May 3 |

Sold goods to Mr. Y Rs 40,000 as per invoice No. 32 |

|

|

May 7 |

Returned to Mr. X goods Rs 1,000 as per debit note No. 1 |

|

|

May 9 |

Y returned goods Rs 7,500 as per credit note No. 7 |

|

|

May 15 |

Purchased goods from Mr. Z Rs 50,000 as per invoice no. 51 |

|

|

May 19 |

Returned goods to Mr. Z Rs 1,600 as per debit note no. 9. |

6. Write up the appropriate journals of Aishwarya for June 2009 from the following information.

|

1 June |

Received invoice from Sneha: |

|

|

100 chudidhars at Rs 275 each |

|

|

100 top ups at Rs 250 each |

|

|

|

|

6 June |

Sent invoice to Shreya: |

|

|

40 chudidhars at Rs 325 each |

|

|

50 top ups at Rs 270 each |

|

|

All subject to 10% discount |

|

10 June |

Received credit note from Sneha: |

|

|

2 chudidhars damaged as invoiced on June 1 |

|

15 June |

Invoiced to Banu: |

|

|

100 baba suits at Rs 600 each |

|

|

All subject to 25% trade discount |

7. Write up the appropriate journals of the following business transaction in the books of Hans Raj and Co.

|

2009 June |

1 |

Bought goods from Mr. P., less 10% trade discount Rs 5,000 |

|

|

3 |

Sold goods to Mr. Q. less 20% trade discount Rs 8,000 |

|

|

5 |

Returned goods to Mr. P. Rs 500 (Gross) |

|

|

7 |

Mr. Q. returned goods Rs 200 (Net) |

|

|

9 |

Advised Mr. R. to dispatch goods worth Rs 6,000 gross to Mr. S. under advice to us. |

|

|

10 |

Mr. R. advised us of the dispatch of goods to Mr. S. and sent their invoice for Rs 6,000 off 10% trade discount. |

|

|

12 |

Mr. S returned to us goods invoiced to them Rs 350 which we promptly returned to Mr. R with our debit note. |

8. Enter the following transactions into a Single Column Cash Book of Mr. Sekhar:

|

2009 June |

1 |

Cash in hand |

1,00,000 |

|

|

2 |

Introduced additional capital |

1,00,000 |

|

|

3 |

Purchased goods for cash |

50,000 |

|

|

5 |

Sold goods to Moon Enterprises for cash |

75,000 |

|

|

6 |

Paid for stationery purchased |

2,500 |

|

|

7 |

Bought ceiling fans |

7,500 |

|

|

9 |

Received form Kashyap, a customer |

10,000 |

|

|

12 |

Paid to Anju, a creditor |

7,000 |

|

|

15 |

Paid to Verma an account |

20,000 |

|

|

17 |

Purchased goods |

70,000 |

|

|

20 |

Sales (cash) |

50,000 |

|

|

30 |

Paid salaries |

36,000 |

9. Enter the following transactions in Cash Book with cash and discount columns and balance the same.

|

|

|

|

Rs |

|

2009 July |

1 |

Cash in hand |

25,000 |

|

|

2 |

Received from Stalin (discount Rs 1,500) |

60,000 |

|

|

3 |

Paid cash to Gopi |

7,500 |

|

|

5 |

Paid to Senthil (discount Rs 700) |

9,300 |

|

|

7 |

Purchased goods from Narayana |

12,500 |

|

|

9 |

Cash Sales |

35,000 |

|

|

11 |

Received from Raj on account (Discount Rs 800) |

20,800 |

|

|

13 |

Paid rent |

3,200 |

|

|

15 |

Received interest on bank account in cash |

1,500 |

|

|

17 |

Received commission |

1,750 |

|

|

19 |

Paid cartage |

500 |

|

|

20 |

Paid to Narayana on account (discount Rs 400) |

10,400 |

|

|

22 |

Paid electricity bill |

600 |

|

|

25 |

Paid telephone bill |