Chapter 5a

Accounting Process — From Trial Balance to Final Accounts and Final Accounts of Non-corporate Business Entities

LEARNING OBJECTIVES

After studying this chapter, you will be able to

Know the Accounting Process — the Final Phase of Preparation of Final Accounts

Understand the Concept of Income Statement and the Position Statement — Important Constituents

Understand the Concepts of Trading Account

Prepare Trading Account

Know the Meaning of Manufacturing Account and Prepare a Manufacturing Account

Differentiate between Trading Account and Manufacturing Account

Understand the Meaning of Profit and Loss Account

Know the Various Uses of Profit and Loss Account

Understand Some of the Accounting Terms Associated with Profit and Loss Account

Prepare Profit and Loss Account with Needed Adjustments

Understand the Meaning and Contents of the Balance Sheet

Arrange the Contents According to the Grouping and Marshalling

Differentiate Between Trail Balance and Balance Sheet

To Prepare a Balance Sheet with Required Adjustments

Understand “Goods Sent on Approval” and to Treat in Final Accounts

Redraft a (Mistaken) Trial Balance with Mistakes and then Prepare Final Accounts

INTRODUCTION

As explained earlier, the process of accounting starts with the recording of entries of business transactions in the books of journal, passing through various stages and reaches the final stage of preparing final accounts. The term “final accounts” usually represents three types of various accounts, viz. Trading Account, Profit and Loss Account and Balance Sheet. In the accounting principle, Balance Sheet is only a statement and not an account. But for all practical uses, Balance Sheet forms part of Final Accounts.

OBJECTIVE 1: ACCOUNTING PROCESS — PREPARATION OF FINAL ACCOUNTS FROM TRIAL BALANCE

The final phase — preparation of final accounts from Trial Balance — is discussed in detail in this chapter. The final accounts are to be prepared to ascertain the net profit or loss for a period (Trading and Profit and Loss Account) and the financial position of the business entities on the last date of a period (Balance Sheet).

OBJECTIVE 2: TRADING ACCOUNT

2.1 Trading Account: A Constituent of Final Accounts

Trading account is a constituent of financial statements. In practice, it is treated along with Trading and Profit and Loss Account, as one account and one unit. The Trading and Profit and Loss Account consists of two parts — the first part or stage or section is called Trading Account and the second part or stage or section is called Profit and Loss Account. The next stage after preparing the Trial Balance is the preparation of Trading Account. Trading Account is to be prepared for a particular accounting period, as this is not a static statement. It is important to mention here that trading account is not prepared at a particular time or date. Hence it is headed as “Trading and Profit and Loss Account for the period ended on….”

Trading Account is prepared to know whether a business enterprise has earned profit or suffered loss. Here profit or loss represents only gross profit or gross loss. Gross profit means the excess of operating revenues over direct operating expenses. To put in other words, gross profit is the excess of net sales revenue over cost of goods sold. In the preparation of Trading Account, selling prices of goods and services are matched with cost of goods sold and services rendered. Some concepts and terms associated with Trading Account are explained now.

- Net Sales Revenue = Cash Sales + Credit Sales − Sales Returns

- Cost of Goods Sold = Opening Stock + Net Purchases − Closing Stock (stock at the end) + Direct Expenses

- Net Purchases = Cash Purchases + Credit Purchases − Purchases Returns

- Gross Profit = Net Sales Revenues − Cost of Goods Sold

Opening Stock refers to the goods existing at the beginning of the (accounting) period.

Direct expenses refer to the expenses that incurred from the purchase of goods till the conversion of goods into saleable goods.

This includes:

- Freight inwards

- Carriage inwards

- Cartage inwards

- Wages

- Import duty

- Octroi

- Packing expenses

- Forwarding charges

- Transit — insurance

- Dock dues

Closing Stock refers to goods remain unsold at the end of the (accounting) year.

2.2 Preparation of Trading Account

The balances of accounts of all related items have to be transferred to the Trading Account by way of passing entries. The entries needed for such transfer are termed as “Closing Entries.” By passing such closing entries, the respective accounts will be closed. The closing entries are as follows:

- For closing of debit accounts:

Trading Account

Dr.

To Opening Stock

To Purchases Account

To Sales Returns Accounts

To Purchases Account

To Wages Account

To Direct Expenses Account

(Direct expenses to be shown separately)

- For closing of credit accounts:

Sales A/c

Dr.

Purchase Returns A/c

Dr.

To Trading Account

- For closing of Trading Account:

- For Gross Profit:

Trading Account

Dr.

To Profit and Loss Account

- For Gross Loss:

Profit and Loss Account

Dr.

To Trading Account

- For Gross Profit:

Note: The Trading Account is closed by transferring Gross Profit/Loss (balance in the account) to the Profit and Loss Account, i.e. to the second section (stage) of the account.

While preparing the Trading Account, care should be taken to treat the closing stock.

- In case, if the Closing Stock does not appear in the Trial Balance (appear outside the Trial Balance), the following entry is passed to incorporate the closing stock:

Stock A/c

Dr.

To Trading A/c

Net effect: It appears both on the credit side of the Trading Account and on the Assets side of the Balance Sheet.

- In case, if Closing Stock appears in the Trial Balance, Closing Stock will not be shown separately in the Trading Account because as it was already adjusted in Purchases or Cost of Goods Sold. But Closing Stock will be shown in the Balance Sheet.

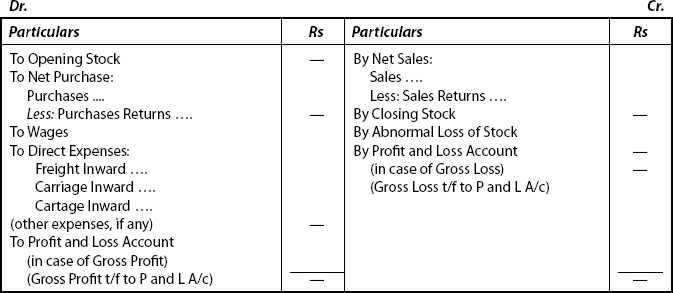

Format (or) Pro-forma Trading Account of …. for the year ended on ……

Note: Prefixes “To” and “By” are not practiced nowadays.

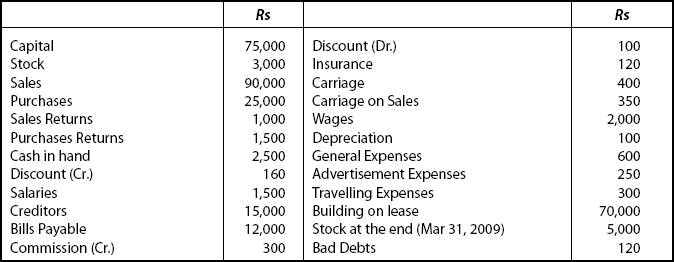

Illustration: 1

From the following information prepare Trading Account for the year ending on Mar 31, 2009:

Opening Stock Rs 30,000; Cash Purchases Rs 70,000; Carriage Inwards Rs 5,000; Cartage Inwards Rs 3,000; Freight Inward Rs 2,500; Wages Rs 7,500; Credit Purchases Rs 50,000; Cash Sales Rs 60,000; Credit Sales Rs 1,50,000; Purchases Return Rs 10,000; Sales Returns Rs 15,000; Stock at the end Rs 40,000; Carriage Outwards Rs 10,000; Office Rent Rs 12,000.

Solutions: |

*Carriage Outwards and Office Rent (expenses relating to office) are not to be entered in Trading A/c. |

|

*All the other items are recorded in the format as follows: |

Trading Account of …. for the year ended on Mar 31, 2009

Illustration: 2 (Treatment of Closing Stock)

Prepare the Trading Account for the year ended on Mar 31, 2009 from the following information:

Purchases (after adjustments) Rs 4,70,000; Sales Rs 5,65,000; Freight Rs 3,000; Carriage Rs 5,000; Freight and Carriage Outward Rs 7,000; Wages Rs 24,000; Closing Stock Rs 27,000; Sales Returns Rs 15,000.

Solution:

Step 1: |

Purchases are shown as after adjustments. This means that closing stock is adjusted with purchases. |

Step 2: |

Hence it will not entered in the Trading Account. |

Step 3: |

Freight and carriage are not to be recorded in Trading Account because they are not direct expenses. |

Step 4: |

Draw the format and enter the figures. |

Step 5: |

Finally, balance the account as the net effect (Gross Profit or Gross Loss) has to be transferred to the next stage of the accounts, i.e. Profit and Loss Account. |

Trading Account for the year ended on Mar 31, 2009

Illustration: 3

Prepare the Trading Account for the year ending on Mar 31, 2009 from the following information:

Cost of Goods Sold Rs 7,63,500;

Sales Rs 8,13,500; Sales Return Rs 40,000

Closing Stock Rs 15,500

Solution:

In this illustration, cost of goods sold and closing stock are given.

As explained earlier, closing stock may be adjusted either with purchases or cost of goods sold. Here, cost of goods sold is given. It means closing stock is adjusted with cost of goods sold and hence it will not appear in Trading Accounts.

Trading Account for the year ended on Mar 31, 2009

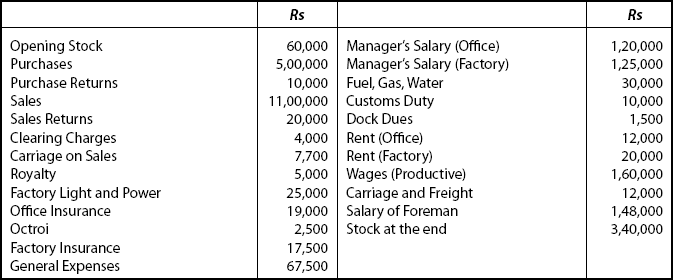

Illustration: 4

From the following particulars of Raj Chand, prepare the Trading Account for the year ending on Dec 31, 20…..

Solution

Raj Chand Trading Account for the year ending on Dec 31, 20….

- Expenses relating to office are not recorded in the Trading Account. In this illustration such expenses are:

Carriage on sales

Office insurance

Rent (office)

Manager’s salary (office)

General expenses

- Closing stock is included because it is not adjusted with purchases or cost of goods sold.

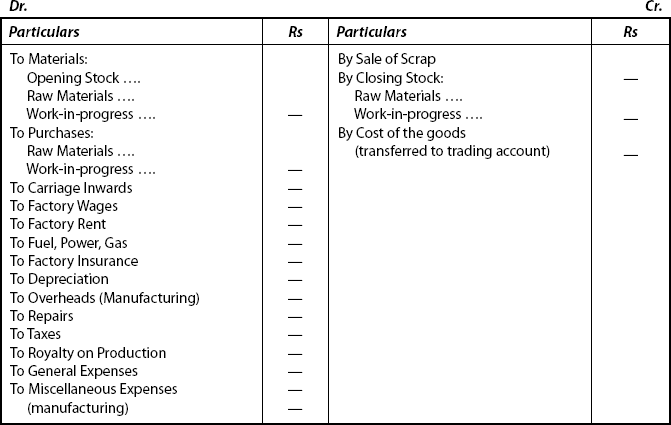

OBJECTIVE 3: MANUFACTURING ACCOUNT

3.1 Meaning of Manufacturing Account

Manufacturing Account is prepared by the business enterprises that are engaged in manufacturing activities. In order to ascertain the cost of goods manufactured, the Manufacturing Account is prepared. In this account, both direct and indirect expenses relating to the process of manufacturing are recorded (i.e., debited to this account). The Manufacturing Account is closed by transferring its balance (cost of goods produced) to the Trading Account.

3.2 Pro-forma of a Manufacturing Account

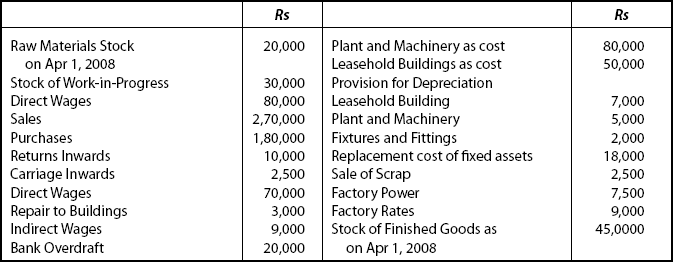

The following were some of the ledger balances in the books of Dev and co. on Mar 31, 2009.

Additional Information

- Factory buildings are held on a 60-year lease

- Stocks on Mar 31, 2009: Raw materials Rs 25,000; Work-in-Progress Rs 35,000; Finished Goods Rs 60,000

- Depreciate the Plant and Machinery @10% p.a.

- The factory production was charged to finished goods at cost

- Prepare a Manufacturing Account for the year ended on Mar 31, 2009.

Solution:

Notes

- Figures relating to finished goods are not taken into account.

- Bank Overdraft and “provisions” are also not recorded.

- Items relating to Fixed Assets are also not entered.

- Depreciation on Plant and Machinery is worked out as Rs 80,000 × 10/100 = Rs 8,000 for a year. In practice for 6 months, Rs 4,000 only is recorded as the exact date of purchase of machinery is not given. (Provision for Depreciation given in the question is to be ignored.)

- It is customary to show one figure for raw materials as:

Raw materials (opening stock):

—

Add: Purchases:

—

Less: Closing stock:____

—

….

But, Closing Stock is shown separately on the credit side.

Dev and Co. Manufacturing Account for the year ended on Mar 31, 2009

3.3 Differences Between Trading Account and Manufacturing Account

A Trading Account differs from Manufacturing Account on the following aspects:

| Basis of Distinction | Trading Account | Manufacturing Account |

|---|---|---|

1. Main objective of preparation |

This is prepared to ascertain the gross profit or gross loss |

The main object is to ascertain the cost of goods manufactured |

2. Transfer of A/c |

This is transferred to the Profit and Loss Account |

This is transferred to Trading Account |

3. Stock of finished goods |

This account shows the stock of finished goods (opening and closing) |

This account does not show the stock of Finished Goods (both opening and closing) |

4. Raw Materials and work-in-progress |

Trading Account does not deal with raw materials and work-in-progress. This deals with only finished goods |

This account deals with raw materials and work-in-progress. This does not deal with finished goods |

OBJECTIVE 4: PROFIT AND LOSS ACCOUNT

As already explained, Trading and Profit and Loss Account, a constituent of Final Accounts is divided into two sections (stages or parts). The first section is Trading Account. After the preparation of Trading Account, the next step in the accounting process is to prepare the Profit and Loss Account.

4.1 Profit and Loss Account: Meaning and Features

Profit and Loss Account is prepared to ascertain the net profit earned or net loss suffered by a business enterprise during an accounting period. This account starts with gross profit on the credit side much which is brought forward from the Trading Account. It is followed by any other item of revenue income. It is important to mention here that only items of revenue incomes and revenue losses will be recorded in this account. But profit or loss on sale of capital items is recorded here. On the debit side it starts with gross loss, in case of gross loss brought forward from Trading Account. It is followed by items relating to revenue expenses. (Items that are not recorded in Trading Account will have to be recorded in this account.)

After recording all items, both sides of the Profit and Loss Account are totalled. If the credit side total exceeds the debit side total, the difference is Net Profit. On the other hand, if the debit side exceeds the credit side such difference is termed as Net Loss. Profit and Loss Account is closed by transferring the Net Profit/ Loss to Capital Account in the Balance Sheet. Net profit is added to the Capital Account in the Balance Sheet while net loss is deducted from the Capital Account in the Balance Sheet.

4.2 Closing Entries Relating to Profit and Loss Account

The preparation of Profit and Loss Account requires the transfer of all items (nominal accounts relating to Profit and Loss Account) in the Trial Balance to the Profit and Loss Account with the help of the following closing entries:

- For Debit: (items of revenue expenses and losses) (or for items other than those record in debit side of Trading Account)

Profit and Loss A/c

Dr.

To Respective items A/c

(individually)

- For Credit: (items of revenue income and gains) (or for items other than those recorded in credit side of Trading Account)

Respective items A/c

(individually)Dr.

To Profit and Loss Account

-

- For Net Profit:

Profit and Loss Account

Dr.

To Capital account

- For Net Loss:

Capital Account

Dr.

To Profit and Loss Account

- For Net Profit:

4.3 Pro-forma of Profit and Loss Account

Refer Chapter 15.

4.3.1 Uses of Profit and Loss Account

- Determination of net income: It is very essential for any kind of business entities to know the profit earned periodically for which this account facilitates the task of computing the net income with accuracy.

- Capital maintenance: Capital should be maintained at an optimum level in business organisations. The preparation of this account extends a helping hand in determining how much amount can be kept in capital and how much can be earmarked for the other areas in the business firms. The income statement plays a vital role in this aspect.

- Tool of financial planning: Only after ascertaining net profit, financial planning can be carried on without much hindrance. The business entities can plan how much to earmark to replace the assets and how much to keep in reserve to meet any unforeseen eventualities which may arise in future and the like.

- Source of internal financing: It helps in maintaining the level of retained income which will act as a source for all other activities relating to finance within any enterprise.

- Basis for tax computation: This account provides accurate basic data to calculate tax. But for this, it will not be easy to compute tax.

- Future investment decisions: Level of earnings in future can be estimated based on the past level of earnings. This P and L Account throws much light on this aspect by which a proper investment decision can be made by a careful analysis of incomes and expenses occurred in the previous years.

- Managerial use: Information regarding profitability can be had from income statement which is useful for management to streamline the different and varied activities of the larger enterprises.

4.4 Explanation of Some of the Terms Appearing in Profit and Loss Account

Some of the items that frequently appearing in the preparation of Profit and Loss Account have to be understood in the proper context. They are as follows:

- Outstanding income: The amount which is due and receivable but not yet received is referred to as “outstanding income.” A person is entitled to receive the “outstanding income” once it becomes due legally.

- Accrued income: The amount which is earned but not yet due and receivable is referred to as “Accrued Income.” This is calculated periodically. A person is not entitled to receive the “accrued income” legally.

- Net profit: Excess of operating revenues over operating expenses and losses is termed as “Operating Profit” (Operating Profit = Gross Profit — Operating Expenses). Operating expenses are such expenses that form part of normal business activities.

- Operating loss: Excess of operating expenses over the gross profit is known as operating loss:

Operating Loss = Operating Expenses − Gross Profit

- Non-operating profit = Non-operating profit arises from sources other than normal activities of the business entities. (In order to understand the concept of operating activities in detail, students are asked to refer the chapter “Cash Flow Statement”.)

Illustration: 6

From the following information, prepare the Profit and Loss Account for the year ending on Mar 31, 20….

Solution:

Notes

- As gross profit is given, Trading Account need not be prepared. Profit and Loss Account can be prepared straight away.

- Gross profit is entered on the credit side and all the incomes of revenue nature are recorded one by one.

- All expenses are entered (revenue nature) on the debit side.

- Sale of machinery — only the loss on sale (Rs 15,000 − Rs 12,000) (book value — sale). Rs 3000 is entered on the debit side. Sale amount Rs 12,000 is not recorded in Profit and Loss Account.

- Reinvestment on fixed assets is capital expenditure and hence not recorded in Profit and Loss Account.

Profit and Loss Account for the year ended on Mar 31, 20….

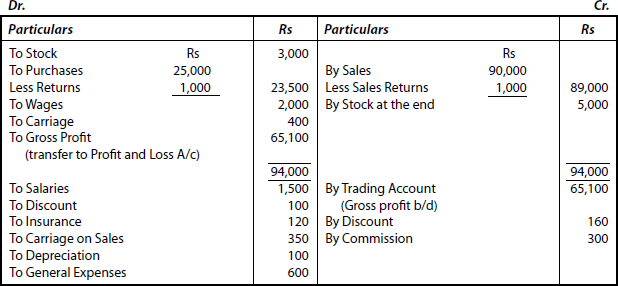

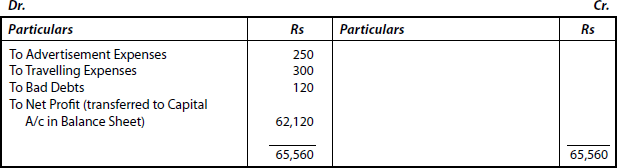

From the following balances of Raj and Sons, prepare a Trading and Profit and Loss Account for the year ending Mar 31, 2009.

Solution

Raj and Sons Trading and Profit and Loss Account for the year ended on Mar 31, 2009

Note:

- Items relating to capital nature are not recorded in Profit and Loss Account.

- Trading Account and Profit Loss Account is a single account and always has to be prepared, as explained in this illustration.

OBJECTIVE 5: BALANCE SHEET

5.1 Meaning and Features of a Balance Sheet

The next step in the process of accounting after preparing Trading and Profit and Loss Account is the preparation of Balance Sheet. The process that started with the recording of Journal entries ends (as the last step) in the preparation of Final Accounts. But this term “Final Accounts” is applied collectively to comprise the three accounts, i.e. Trading Account, Profit and Loss Account and the Balance Sheet. Balance Sheet is not an account but a statement summarising the financial position of a business enterprise at a particular date. All the accounts that have not been closed by transfer to either the Trading Account or the Profit and Loss Account are to be recorded in the Balance Sheet. It summarises on the one side — the right-hand side — the assets of the business enterprise and on the left hand side the liabilities of the business. The capital — the business owes to the owner is recorded on the liabilities side. Net profit is added to it, while net loss is deducted from the capital. At the same time, Drawings (owner’s debt to the business) is not recorded as a separate item on the assets side but it is deducted from Capital Account. Consequently, the total of two sides must show equal amounts. This equality is a proof of arithmetical accuracy. Hence, a Balance Sheet may be called a Statement of Assets and Liabilities of a business entity at a particular date.

5.2 Contents of the Balance Sheet

The right-hand side of a Balance Sheet is called the “Assets” side and the left-hand side is called the “Liabilities” side.

Items shown on the Assets side of a Balance Sheet: The debit balances of the ledger accounts that were not transferred to the Trading and Profit and Loss Account are to be shown on the Assets side of the Balance Sheet, because a debit balance in the real account and the personal account represents an “Asset.” Assets are generally classified as Current Assets, Investments and Fixed Assets.

Further, fixed assets are classified into two categories: Tangible Assets and Intangible Assets.

Current Assets: Current Assets are those assets which are held for a short period and can easily be converted into cash (or sold or consumed).

Example: Cash in hand, cash at bank, raw material, stock of goods, bills receivable, debtors, prepaid expenses and so on. The current assets are also called floating assets or circulating assets. Turnover of these assets occur quickly and frequently. Generally, current assets are valued at cost price or market price whichever is less.

Investments: Acquisition of assets which in turn earn interest, dividend, rent or any other incomes are referred to as investments. For example, Shares, Debentures, Bonds and Fixed Deposits. These are usually held in business for a long period, generally more than a year.

Fixed Assets: The term “Fixed Assets” refer to those assets which are acquired for use in business activities rather than for resale in the course of the business. They are usually held in the business for a relatively longer period. Fixed assets are classified into Tangible Fixed Assets and Intangible Fixed Assets.

Tangible Fixed Assets can be seen and they posses concrete physical existence. For example, Land, Building, Plant, Machinery, Furniture and Fixtures, Vehicles and so on.

Intangible Fixed Assets cannot be seen and they do not possess any physical existence. Example: Goodwill, Patents, Copyrights, Trademarks and so on.

Someother assets also appear in the assets side because of the nature of account, i.e. a debit balance relating to special items such as “Suspense Account” of Advertisement, Interest, etc. Because of its status as a debit balance, it is shown as an asset.

Wasting Fixed Assets such as mines, oil wells, quarries also have the status of assets appearing on the Assets side of the Balance Sheet.

It is to be noted here that Contingent Assets are not shown on the assets side of the Balance Sheet, but they are shown as notes to the Balance Sheet now.

Items shown on the “Liabilities side” of a Balance Sheet: The credit balances of the ledger accounts that were not transferred to the Trading and Profit and Loss Account are to be shown on the “Liabilities side” of the Balance Sheet, because a credit balance in personal account is a liability. Liabilities may broadly be classified as follows: (i) Current Liabilities and (ii) Long-term Liabilities.

Current liabilities: Current liabilities represent the debts that have to be paid within a short period. For example, Creditors, Bills Payable, Outstanding Liabilities and Income received in advance.

- Creditors: These include both trade and nontrade creditor’s purchases of goods on credit basis, for use of services amount not yet paid are some of the examples for trade creditors. Money borrowed for a short period is nontrade creditor. All creditors are clubbed together and entered under the head “Creditors.”

- Outstanding liabilities: Amount not yet paid (for the expenses already incurred) till the date of preparation of Balance Sheet is called outstanding liabilities. For example, outstanding rent, tax, salary, wages, interest, etc.

- Income received in advance: As on the date of Balance Sheet, amount would have been received but expense for which will incur on a later date.

- Bills payable: It is an instrument to pay money to the creditor for purchase of goods or services.

Long-term liabilities: Long-term liabilities represent the debts that need not be paid in a short period. Due date for payment of such liabilities will be usually for a period of more than a year. Long-term liabilities may be classified as (i) Secured Loans and (ii) Unsecured Loans.

- Secured Loans: In case, if loan is obtained by mortgaging a fixed asset as security, such loan is said to be a secured loan, i.e. loans are availed against security.

- Unsecured Loans: No security is to be provided to secure a loan in this type of liability.

Examples: Debentures and loan from financial institutions.

Contingent liabilities: A contingent liability is not a liability on the date of Balance Sheet, but it may be a liability or may not be a liability on a future date. Uncertainty clouds over the amount pertaining to those liabilities. The obligation to discharge these liabilities on the date of Balance Sheet is uncertain.

Examples: Bills of exchange discounted; law suit against business enterprises, still pending, surety or guarantee given to others and arrears of dividends on cumulative preference shares.

As contingent liability is not an actual liability on the date of Balance Sheet, it will not be recorded on the liabilities side of the Balance Sheet but it is shown as footnote or explanation to the Balance Sheet.

5.3 Grouping and Marshalling of Assets and Liabilities: Meaning of Grouping and Marshalling

Grouping: Arranging items of a similar nature together under a common heading is known as “grouping.”

Examples: Creditors, Debtors.

Creditors: This includes accounts of all the supplies from whom goods were purchased on credit.

Debtors: This includes accounts of all debtors arising from the credit sales of goods, i.e. the balances of all the ledger accounts of debtors are totalled and written under the head “Debtors.”

Marshalling: The order in which the assets and liabilities are recorded in the Balance Sheet is referred to as marshaling. The items in the Balance Sheet are generally marshald in the following two ways: (i) in the order of liquidity and (ii) in the order of permanency.

5.4 In the Order of Liquidity

- Assets are arranged in the order of liquidity (liquidity means the ability to convert the asset into cash or time taken to convert the asset into cash) — the most liquid asset is shown first and the least is shown last.

- The liabilities are arranged in the order in which they have to be paid off— the most emergent amount has to be made is recorded first and other liabilities are arranged in the order of emergency to be paid off.

The sole proprietorship, partnership firms, banking and financial entities usually adopt this kind of preparing balance sheets in order of liquidity.

Format of Balance Sheet (items shown in the order of liquidity) Balance Sheet as on ….

5.5 In the Order of Performance

Items are arranged in the order of performance according to the purpose. This order is just the reverse of the liquidity order.

The assets are arranged in the order of their performance — the least liquid asset is to be recorded first and the most liquid asset is recorded last, i.e. just the reverse order of the liquidity order.

The liabilities (also the reverse of the liquidity order), the least urgent payment is to be recorded first and vice versa.

It is mandatory for companies incorporated under the Companies Act 1956 to prepare the Balance Sheet in the order of performance.

Format of Balance Sheet (items shown in the order of performance) Balance Sheet of …. as on ….

OBJECTIVE 6: USES OF BALANCE SHEET

- To ascertain the nature and value of assets of business entities at a particular date.

- To ascertain the nature and value of the liabilities and their values of the business on a particular date.

- To assess the solvency of the business.

- To examine how much capital is distributed among the various assets to strengthen the efficiency of the firms.

- To assess exactly the financial position of a business.

- To facilitate comparison within the enterprise and with the enterprises of similar nature in the market.

OBJECTIVE 7: DIFFERENCES BETWEEN TRIAL BALANCE AND BALANCE SHEET

A Trial Balance may differ from Balance Sheet in the ways as shown in the tabular column.

| Basis of Distinction | Trial Balance | Balance Sheet |

|---|---|---|

1. Object of preparation |

The main object is to test the arithmetical accuracy of the ledger postings |

This is prepared to ascertain the financial position of a firm |

2. Periodically of preparation |

Trial balance may be prepared more than once in a year |

Balance Sheet is prepared only once at the end of an accounting period |

All types of accounts, i.e. personal, real and nominal accounts are recorded |

Only personal and real accounts are recorded |

|

4. Contents |

All the ledger accounts are shown |

The balances of ledger accounts, which were not closed till Trading and Profit and Loss Account is prepared, are shown |

5. Stock |

It always contains opening stock and only rarely closing stock |

It contains only closing stock |

6. Headings |

The headings of the Trial Balance columns are “Debit balance” and “Credit balance” |

The headings in the Balance Sheet are “Liabilities” and “Assets” |

7. Adjustments |

Adjustments (in respect of outstanding expenses, prepaid, accrued income, etc.) are not necessary in the preparation of a Trial Balance |

Adjustments relating to certain items are absolutely necessary to prepare a Balance Sheet |

8. Net Result |

Net profit or net loss cannot be known from the Trial Balance |

Net result can be best obtained from the Balance Sheet |

9. Mandatory |

Preparation of Trial Balance is only obligatory. It is not mandatory |

Preparation is mandatory for companies registered under Companies Act |

10. Ends or means |

A Trial Balance is a means to know the financial position of a business enterprise |

A Balance Sheet is the end to know the financial position of an enterprise |

Adjustments

To be made at the time of preparing Balance Sheet — (Final Accounts)

Adjustments of various items in the preparation of Final Accounts

At times, balances in the Trial Balance do not show the correct amounts for the full accounting period.

Revenue recognition is one kind of principle to be followed for making adjustments. According to this principle, the revenue should be recognised in the period in which the sale is said to have taken place.

Matching principle is another kind of principle which emphasises that the expenses will have to be recognised in the same accounting period with revenues. Any expense is recognised in relation to its revenue. “No revenue, No expense” policy is the motive behind such principle.

As final accounts are prepared on accrual basis, adjustments are necessary to record all assets and liabilities at their correct values. For this, the amount relating to a transaction may be received/spent in the previous year, such amount must be added this year. Similarly, if any amount has been received/spent for the next year, it must be deducted as it relates only to the next accounting period. Irrespective of the year in which it was received/spent, MUST be brought to this year, if it pertains to this year and get adjusted with that time. Such adjustments are made to ensure a proper match of revenue and expense.

Some of the items of adjustments required to be made at the end of the accounting period are explained below.

7.1 Stock at the End or Closing Stock

The stock at the end or closing stock or closing inventory is valued properly (i.e., at cost or net realizable value that is less) and then it is incorporated in the final accounts.

Accounting treatment

A: Journal entry

|

Closing Stock Account |

Dr. |

|

To Trading Account |

|

B: In Trading Account |

Recorded on the Credit Side |

C: In Balance Sheet |

Recorded on the “Assets Side” As a “Current Asset.” |

If the closing stock appears in the Trial Balance,

(a) Journal entry |

Stock at the End A/c |

Dr. |

|

To Purchase A/c |

|

(b) In Trading Account |

No entry |

|

(c) In Balance Sheet |

On the Assets side as “Current Asset.” |

|

Illustration: 8

Closing stock as on Mar 31, 2009 Rs 1,750 appears outside the Trial Balance. Accounts are closed on Mar 31. Pass an adjusting entry and how will you record in the trial accounts.

Solution

- Adjusting entry

- Trading Account

- Balance Sheet

Balance Sheet as on Mar 31, 2009

7.2 Accrued Expenses or Outstanding Expenses

Usually expenses are recorded only when they are paid. It means that expenses were actually incurred but not paid during the accounting period.

Adjustment:

(A) Journal entry |

Expenses A/c |

Dr. |

|

To Outstanding Expenses A/c |

|

|

Enter: |

|

(B) Trading Account |

On the debit side to be added to the respective expenses account. |

|

(direct expenses only) |

|

|

(C) Profi t and Loss A/c |

On the debit side to be added to the respective expense account |

|

(for indirect expenses) |

|

|

(D) Balance Sheet |

On the liabilities side under the head: current liability |

|

Note: If Outstanding Expenses appear in the Trial Balance, no adjusting entry is needed. Such outstanding expenses are shown only on the liabilities side of the Balance Sheet. Further it is not shown in Profit and Loss Account too.

Illustration: 9

A private business enterprise disburses salary to its staff on the fifth day of the next month. The monthly salary bill is Rs 30,000. Pass an adjusting entry and how will you record in final accounts.

Solution

- Adjusting entry

Journal

- Profit and Loss Account

Profit and Loss Account for the year ended Dec 31, 20.….

- Balance Sheet

Balance Sheet as on Dec 31, 20….

7.3 Prepaid Expenses

Payments for certain expenses will be paid in advance, i.e. expenses are paid in the current accounting period, but the benefit to a certain extent will occur in the next accounting period. For example, insurance premium, rent, etc.

Accounting treatment

(A) Adjusting entry |

Prepaid Expenses A/c |

Dr. |

|

To Respective expenses A/c |

|

(B) Trading Account |

It is deducted from the concerned expenses on the debit side |

|

(for direct expenses only) |

|

|

(C) Profi t and Loss Account |

It is deducted from the concerned expenses on the debit side. |

|

(for indirect expenses only) |

|

|

(D) Balance Sheet |

It is to be recorded on the “Assets Side” under “Current Assets” |

|

Note: If it appears in Trial Balance it will be shown only on the assets side of the Balance Sheet. No adjustment entry is required in that case.

Illustration: 10

A firm pays Insurance Premium Rs 3,600 on June 1 every year. The accounting period ends on Dec 31. Make the adjustment entry in order to prepare final accounts.

Solution

- Adjusting entry

Journal

- Profit and Loss Account

Profit and Loss Account for the year ended Dec 31, 20….

- Balance Sheet

Balance Sheet as on Dec 31, 20….

7.4 Accrued Income

Income that has been earned but not received during the accounting period is referred to as “accrued income.”

(A) Adjustment entry |

|

|

|

Accrued Income A/c |

Dr. |

|

To Respective Income A/c |

|

(B) Profi t and Loss Account |

To be entered on the credit side and added with respective income |

|

(C) Balance Sheet |

To be entered on the assets side as Current Asset in Balance Sheet. |

|

If accrued income appears in Trial Balance, no adjusting entry is needed. It will not be shown in Profit and Loss Account, but accrued income is to be shown in the Balance Sheet.

A business firm owns Rs 20,000, 12% debentures on which interest is receivable on Sep 30 and Mar 31. Accounting year is the financial year. The interest was received on June 30 only. Pass an adjusting entry and how will this appear in final accounts.

Solution

- Adjusting entry

Journal

- Profit and Loss Account

Profit and Loss Account for the year ended Mar 31, 20….

- Balance Sheet

Balance Sheet as on Mar 31, 20….

7.5 Income Received in Advance (or) (Unearned Income or Unaccrued Income)

The income or revenue that has been received in advance for the goods or services to be provided in the near future is generally known as unearned income. For example, subscription, insurance premium, etc. Income received in advance is a liability in the sense that the amount has to be repaid or an equal value of goods or services will have to be provided in the near future.

(A) Adjusting entry |

Respective income A/c |

Dr. |

|

To Income received in advance A/c |

|

(B) Profit and Loss Account |

Entered in the credit side, has to be deducted from the respective account |

|

(C) Balance Sheet |

Entered on the liabilities side as “Current Liability” |

|

Note: As usual, if it appears in Trial Balance, no adjusting entry is needed. It will be shown only in the Balance Sheet.

Illustration: 12

A social service organisation receives subscriptions from its members Rs 30,000, of which Rs 3,500 relates to next accounting year. Pass the necessary adjustments in final accounts.

- Adjusting entry

- Profit and Loss Account

Profit and loss account for the year ended…..

- Balance Sheet

Balance Sheet as on….

7.6 Description of Fixed Assets

Depreciation of Fixed Assets: A certain portion of the cost of a fixed asset (its use in business) is charged as an expense which is referred to as depreciation.

Accounting treatment:

(A) Adjusting entry |

Depreciation Account |

Dr. |

|

To (the concerned) Asset A/c |

|

(B) Profit and Loss Account |

Recorded as a separate item on the debit side |

|

(C) Balance Sheet |

Recorded on the Assets side of the Balance Sheet. It should be deducted from the respective “Fixed Asset” |

|

Note: In general, deprecation is provided after the preparation of Trial Balance. But at times, it is shown in Trial Balance. In that case, no adjustment entry is needed. It will be shown only in Profit and Loss Account. It will not be shown in Balance Sheet.

Illustration: 13

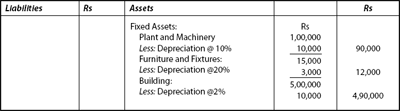

The following balances were extracted at the end of an accounting period from the books of Renu:

Plant and Machinery |

Rs 1,00,000 |

Furniture and Fixtures |

Rs 15,000 |

Building |

Rs 5,00,000 |

Depreciation is to be charged as 10% on Plant and machinery, 20% on Furniture and Fixtures and 2% on Buildings. You are required to pass adjusting entry and show this will appear in the final accounts.

Solution:

First, calculate the charge, i.e. depreciation amount for each item individually as:

Plant and Machinery: |

Rs 1,00,000 × 10/100 |

= |

Rs 10,000 |

Furniture and Fixtures: |

Rs 15,000 × 20/100 |

= |

Rs 3,000 |

Building: |

Rs 5,0,000 × 2/100 |

= |

Rs 10,000 |

Total amount of depreciation |

= |

Rs 23,000 |

|

Then, pass the adjusting entry in the books of Journal as follows:

- Adjusting entry

Journal

- Profit and Loss Account

Profit and Loss Account for the year ended….

- Balance Sheet

Balance Sheet as on….

7.7 Bad Debts

Accounting Treatment of Bad Debts: Losses that arise due to liability to recover debt are called “Bad Debts.”

(A) Accounting treatment: |

Bad Debts A/c |

Dr. |

|

To Debtors A/c |

|

(B) Profi t and Loss Account |

To be recorded on the debit side as a separate account |

|

(C) Balance Sheet |

To be entered on the Assets side by deducting from Debtors |

|

If “Bad Debts” appear in the Balance Sheet, no adjusting entry is required. It will be entered in the Profit and Loss Account.

Illustration: 14

Mr Dilip, a debtor for Rs 25,000 is declared insolvent. Debtors appear in the Trial Balance at Rs 3,00,000 (including Dilip’s Debt). Write up the adjustment entry and prepare the final accounts. Accounting year ends on Dec 31.

Solution

- Adjusting entry

- Profit and Loss Account

Profit and Loss Account for the year ended on Dec 31…..

- Balance Sheet

Balance Sheet as on Dec 31…

7.8 Provision for Bad and Doubtful Debts

In addition to the bad debts written off, as explained in the previous illustration, a provision is created by way of a pre-determined percentage of debtors.

(A) Accounting entry |

Profit and Loss Account |

Dr. |

|

To Provision for Doubtful Debts |

|

(B) Profit and Loss Account |

To be entered on the debit side as separate item |

|

(C) Balance Sheet |

To be recorded on the Assets side of the Balance Sheet by deducting from Sundry Debtors |

|

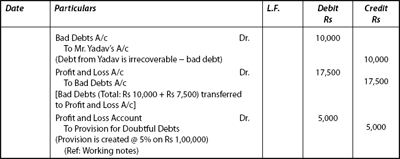

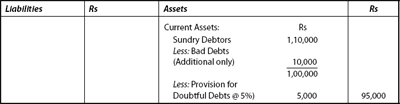

Illustration: 15

Following is the extract of a Balance Sheet (relating to this particular item Debtors and Bad Debt) as on Mar 31, 2009:

| Dr. Balance Rs |

Cr. Balance Rs |

|

|---|---|---|

| Sundry Debtors | 1,10,000 |

|

| Bad Debts | 7,500 |

- After preparing Trial Balance, it is surfaced that one Mr. Yadav has become insolvent and the entire amount of Rs 10,000 was not recoverable from him.

- It is desired to make a provision of 5% on debtors. Write up the relevant adjustment entry and prepare the final accounts.

Solution

|

Rs |

Sundry Debtors (as given) |

1,10,000 |

Less: Bad Debts (given in additional information) |

10,000 |

|

1,00,000 |

Provision @ 5% (5% of Rs 1,00,000) |

5,000 |

|

95,000 |

Note: Provision for doubtful debts, i.e. Rs 5,000 is calculated after deducting the additional bad debt (i.e., Rs 7,500 was shown as bad debt already in final balance). As such Rs 1,10,000 − Rs 10,000 = Rs 1,00,000. 5% on Rs 1,00,000 − Rs 5,000 is the provision for doubtful debts.

- Adjusting entry

Journal

- Profit and Loss Account

Profit and Loss Account for the year ended on Mar 31, 2009

- Balance Sheet as on Mar 31, 2009

Illustration: 16

Following is the extract from the Trial Balance of a business entry as on Mar 31, 2009:

| Account | Dr. Balance Rs | Cr. Balance Rs |

|---|---|---|

Sundry Debtors |

1,10,000 |

|

Provision for Doubtful debts |

|

5,000 |

Bad Debts |

7,500 |

|

Additional Information

- Additional Bad debts Rs 20,000

- Maintain the provision for doubtful debts @ 5% on debtors make the necessary journal entries, ledger accounts and final accounts.

Solution:

Note

Sundry Debtors |

Rs 1,10,000 |

(given) |

|

Less: Bad Debts (given in additional information) |

Rs 20,000 |

|

Rs 90,000 |

Provision @ 5% on Rs 90,000 |

4,500 |

|

Rs 85,500 |

Journal

Provision for Doubtful Debts

Profit and Loss Account for the year ended on Mar 31, 2009

Balance Sheet as on Mar 31, 2009

7.9 Provision for Discount on Debtors

Accounting Treatment and Provision for Discount on Debtors: After the treatment of provision for bad and doubtful debts (i.e., provision for bad and doubtful debts are deducted from total debtors), the balance represents sound debtors. Such debtors may claim discount for prompt payments. Such discount allowed on sound debtors is also treated as business expense.

Accounting treatment

(A) Adjusting entry |

Profit and Loss Account |

Dr. |

|

To Provision for discount on Debtors A/c |

|

(B) Profit and Loss A/c |

To be entered on the debit side as a separate item |

|

(C) Balance Sheet |

To be recorded on the assets side of the Balance Sheet by deducting from Sundry Debtors |

|

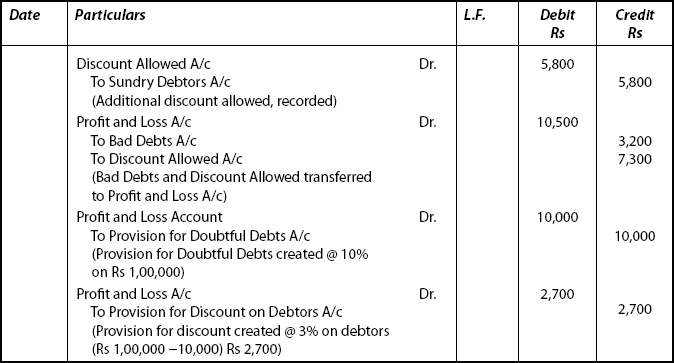

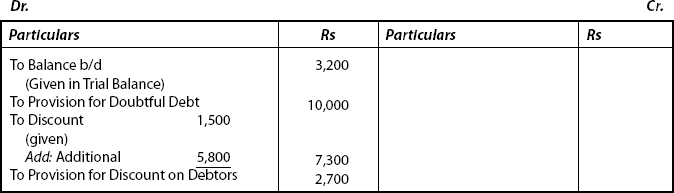

An extract of Trial Balance as on Mar 31, 2009:

| Account | Dr. Balance Rs | Cr. Balance Rs |

|---|---|---|

Sundry Debtors |

1,05,800 |

|

Bad Debts |

3,200 |

|

Discount |

1,500 |

|

Additional Information

- Create a provision for doubtful debts @ 10% on debtors.

- Create a provision of discount on debtors @ 3% on debtors.

- Additional discount given to debtors Rs 5,800.

Pass necessary Journal entries and make necessary ledger accounts.

Solution

Sundry Debtors |

Rs 1,05,800 |

Less: Additional discount |

5,800 |

|

1,00,000 |

Less: Provision for Doubtful Debts @ 10% |

10,000 |

|

90,000 |

Less: Provision for Discount 3% |

2,700 |

|

87,300 |

Journal

Provision for Doubtful Debts

Discount Allowed Account

Provision for Discount on Debtors Account

Profit and Loss Account for the year ended on Mar 31, 2009

7.10 Provision (or) Reserve for Discount on Creditors

Provision for discount which would be allowed by the creditors is similar (as in the above) to the treatment discussed in the case of debtors.

Accounting treatment

(A) Adjusting entry |

Provision for discount on creditors account |

Dr. |

|

To Profit and Loss A/c |

|

(B) In Profit and Loss A/c |

Entered on the credit side as a separate item |

|

(C) In Balance Sheet |

Recorded on the Liabilities side by deducting from the Sundry Creditors |

|

Note: Discount likely to be earned from creditors occurs occasionally.

7.11 Adjustment of Interest on Capital

In individual proprietorship or partnership firms, interest is charged on the capital employed by the owners (proprietor or partner).

Accounting treatment:

(A) Adjusting entry |

Interest on Capital A/c |

Dr. |

|

To Capital A/c |

|

(B) Profit and Loss A/c |

To be entered on the debit side as a separate item |

|

(C) Balance Sheet |

To be entered on the Liabilities side by adding to the Capital |

|

Note: When interest on capital appears in Trial Balance, it will be transferred to the debit side of Profit and Loss Appropriation Account only.

7.12 Interest on Drawings

Interest is charged on drawings. Interest is charged due to the reason if the same amount is obtained from other sources, one has to pay interest.

Accounting treatment

(A) Adjusting entry |

Capital A/c |

Dr. |

|

To Interest on Drawings A/c |

|

|

or |

|

|

To Profit and Loss Appropriation A/c |

|

(B) Profit and Loss A/c |

Entered on the credit side as a separate item |

|

(C) Balance Sheet |

Entered on the liabilities side by deducting from capital |

|

Note: If this item appears in the Trial Balance, it will be credited to Profit and Loss Appropriation Account only.

7.13 Abnormal Loss of Stock

The abnormal loss of stock arises due to natural calamities, fire, flood, breakage, pilferage, etc.

|

(A) Adjusting entry |

Loss of stock (or) Profit and Loss A/c |

Dr. |

|

|

To Trading Account |

|

|

(B) Trading Account |

Shown on the credit side |

|

|

(C) Profit and Loss Account |

(Total loss - Amount received from insurance company). The arrived value is entered on the debit side |

|

|

(D) Balance Sheet |

The amount due from the insurance company is recorded as an asset |

|

Illustration: 18

Stock at the end of a business of a business firm is Rs 30,000. It came to notice that goods amounting to Rs 4,000 were destroyed by fire during the current accounting period. Make necessary adjusting entries in each of the following alternative situations:

- The stock is not insured

- The stock is fully insured

- The stock is partly insured, the insurance company has agreed to pay Rs 1,000.

Solution: For “stock at the end”

In all the three situations “stock at the end” is treated as above:

Case (a): Three situations “stock at the end” is treated as above:

Case (a): Not insured

Adjusting entry |

Profit and Loss A/c |

Dr. |

4,000 |

|

|

To Trading A/c |

|

|

4,000 |

Trading A/c |

Shown in credit side of Trading A/c |

|

|

|

Profit and Loss |

Losses and expenses are shown on the debit side of Profit and Loss A/c |

|||

Case (b): Fully insured

Adjusting entry |

Insurance company |

Dr. |

4,000 |

|

|

To Trading A/c |

|

|

4,000 |

Balance Sheet |

Entered in the Assets side under the insurance company’s head Rs 4,000 |

|||

Case (c): Partly insured

Adjusting entry |

|

|

|

|

|

Insurance company |

Dr. |

1,000 |

|

|

Profit and Loss A/c |

Dr. |

3,000 |

|

|

To Trading A/c |

|

|

4,000 |

In the Balance Sheet, Rs 1,000 is shown on the Assets side under the insurance company’s name in this case.

7.14 Insurance Premium

- Life Insurance Premium: Life insurance premium is a personal expense. The accounting treatment is similar to that of drawings as explained already.

- Insurance Premium: If no specific information is given, it is entered on the debit side of Profit and Loss Account. If it is mentioned specifically such as factory machinery, goods stored (stock), then it is treated as direct expense. Hence it is shown in Trading Account.

7.15 Salaries and Wages

Salaries and wages are treated as follows:

- If it is shown as “Salaries and Wages,” i.e. Salary first and then followed by Wages, wages portion is to be treated as non-productive. Hence it is shown in the Profit and Loss Account.

- If it is shown as “Wages and Salaries,” i.e. Wages first followed by Salaries, just reverse of the above salaries portion is to be treated as non-productive and the combined amount is taken to trading account.

- In case, if there is no manufacturing activity, Wages and Salaries will have to be recorded in the Trading Account.

7.16 Commission on Profit

Profit before and after Charging Commission: In practice, managers are paid commission on Net Profit before charging such a commission or after charging such a commission.

In case, if the commission is payable as a percentage of Net Profit before charging commission, manager’s commission is calculated as:

In case, if the commission is payable at a fixed percentage on Net Profit then

In case if there is no specific information, manager’s commission is calculated as a percentage on Net Profit before charging such commission:

(A) Adjusting entry |

Manager’s Commission A/c |

Dr. |

|

To Outstanding Commission |

|

(B) Profit and Loss A/c |

Entered on the debit side |

|

(C) Balance Sheet |

Recorded on the Liabilities side as a current liability |

|

Illustration: 19

From the following information, calculate the manager’s commission at 12% of profit (i) before charging such commission and (ii) after charging such commission.

|

Rs |

Rs |

Gross Profit |

— |

70,000 |

Salaries |

24,000 |

|

Rent and Rates |

4,800 |

|

Office Expenses |

8,000 |

|

Selling Expenses |

10,000 |

|

Advertisement |

12,000 |

|

|

|

58,800 |

Profit before Commission: |

|

11,200 |

You are also required to show how this will appear in final accounts.

Solution

- Calculation of Manager’s Commission

Case (i):

Commission

=

Net Profit before Commission × Rate/100

=

Rs 11,200 × 12/100 (Given) = Rs 1,344

(Given)

Case (ii):

Commission

=

Net Profit before Commission × Rate/Rate + 100

=

Rs 11,200 × 12/12 + 100

=

Rs 11,200 × 12/112 = Rs 1,200

- Profit and Loss Account for the year ended on Mar 31, 200….

- Balance sheet as on Mar 31, 20…..

7.17 Goods Sent on Approval: Meaning and Accounting Treatment

Goods sent to customers with a tag “Sale or return” (or) “retain or return” (within a specified period) is referred to as “Goods sent on Approval.” Such transactions are treated as

- Adjusting entry

- Sales A/c Dr. (with selling price)

To Debtor A/c

- Stock with customer’s A/c (with cost price)

To Trading A/c

- Sales A/c Dr. (with selling price)

- Trading Account

- Sales value of goods is entered by deducting from sales

- Cost of goods is recorded on the credit side by adding to the closing stock

- Balance Sheet

- Sale value of goods is recorded on the assets side by deducting from Debtors

- Cost of goods is recorded on the assets side by adding to closing stock

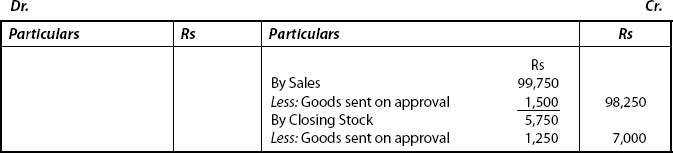

Illustration: 20

An extract of Trial Balance as on Mar 31, 20009 is given below:

| Particulars | Dr. Balance Rs | Cr. Balance Rs |

|---|---|---|

Sales |

|

99,750 |

Debtors |

12,625 |

|

Additional Information

Goods costing Rs 1,250 were sent to a customer on sale or return for Rs 1,500 on Mar 30, 2009 and was recorded as actual sales. Stock-in-hand on Mar 31, 2009 was valued at Rs 5,750.

How will these items appear in Final Accounts?

Solution:

In Trading Account, goods sent on sale or return for Rs 1,500 is to be recorded by deducting it from sale Rs 99,750. Goods costing Rs 1,250 (sent on approval) is to be added to losing stock, i.e. Rs 5,750.

This is shown as follows:

Trading Account for the year ended on Mar 31, 2009

7.18 Goods-in-transit

Goods that have been purchased but not received till the end of the accounting period are referred to as Goods-in-transit. Generally, these goods are treated as a form and part of closing stock.

Accounting treatment

(A) Adjusting entry |

Goods-in-transit A/c |

Dr. |

|

To Trading A/c |

|

(B) Trading Account |

Recorded on the credit side |

|

(C) Balance Sheet |

Entered on the Assets side as a current Asset |

|

Illustration: 21

Goods costing Rs 70,000 were sent on Mar 25, 2009 but they were not yet received till Mar 31, 2009. Accounting year is financial year. Pass the necessary adjusting entry and show how this is treated in the final accounts.

Solution

(A) Adjusting entry |

Goods-in-transit A/c |

Dr. |

70,000 |

|

|

To Trading A/c |

|

|

70,000 |

Goods purchased not yet received, i.e. Goods-in-transit

Trading Account for the year ended Mar 31, 2009

Balance Sheet as on Mar 31, 2009

7.19 Bad Debts Written off Recovered

When the amount written off as bad debt but recovered in future, it is generally treated as an item of gain:

Accounting treatment

(A) Adjusting entry |

Cash/Bank A/c |

Dr. |

|

To Bad Debts Recovered (amount) A/c |

|

(B) Profit and Loss A/c |

It will be recorded on the credit side |

|

(Because, Bad Debts Recovered is a gain. It is transferred to the Profit and Loss Account and the usual entry is: |

||

Bad Debts Recovered A/c |

Dr. |

|

To Profit and Loss A/c) |

||

7.20 Withdrawals, Samples and Free Gifts

Accounting Treatment of Samples, Free Gifts, etc.: Goods are being distributed by way of samples and free gifts as a part of sales promotion scheme. Goods distributed free to the staff and taken for personal use by the proprietor are all to be treated in a different way. They are not to be treated as part of sale.

Accounting treatment |

|

Adjusting entry |

Purchases are to be adjusted (by crediting) as: |

Respective items Account |

Dr. |

To Purchase A/c |

|

Illustration: 22

A proprietor is dealing with “Knit Wear” — a hosiery product

- He took for personal use Rs 2,500

- Rs 12,000 worth were distributed to his staff, free

- Distributed by way of samples Rs 9,000

- Given free to his valuable customers (dealers Rs 3,000 pass the necessary adjusting entries)

Solution:

In the above illustration, all the transactions are to be treated as follows:

- Goods taken for personal use is “Drawings” A/c

- Distributed free to his staff is Salaries A/c

- and (iv) Sales promotion items are Sales Promotion A/c

Hence entry will be:

|

|

Rs |

|

(i) Drawings A/c |

Dr. |

2,500 |

|

(ii) Salaries A/c |

Dr. |

12,000 |

|

(iii + iv) Sales promotion A/c |

Dr. |

12,000 |

|

To Purchases A/c |

|

|

24,500 |

7.21 Income Tax

The Income tax, for sole proprietors, has to be treated as a personal expense for them. Hence it is to be deducted from the Capital Account in the Balance Sheet.

But interest on advance income tax received, if any, the same is also to be treated as a personal income. Hence it is to be added to the Capital Account in the Balance Sheet.

7.22 Provident Fund: Employee’s and Employer’s Contribution

Both employer and employee contribute a certain amount every month in the employee’s name for a future benefit. It may be said this scheme is called as Provident Fund Scheme. Contribution to this scheme is to be treated as:

(A) For Employee’s contribution to P.F. |

|

Salary and Wages A/c |

Dr. |

To Employee’s contribution to P.F. A/c |

|

To Cash A/c |

|

(B) For Employer’s contribution to P.F. |

|

Salary and Wages A/c |

Dr. |

To Employer’s contribution to P.F. A/c |

|

(C) For both the contributions to P.F. |

|

Employee’s contribution to P.F. A/c |

Dr. |

Employer’s contribution to P.F. A/c |

Dr. |

To Cash A/c |

|

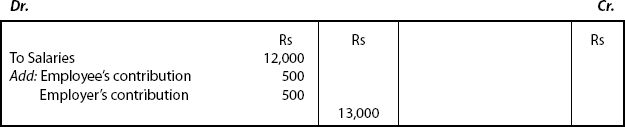

Example 1: Following are the extracts from a Trial Balance of a firm as on Mar 31, 2009.

Salaries |

Dr. Balance |

Cr. Balance |

|

20,000 |

|

P.F. deducted from Salaries |

|

2,000 |

Additional information: Provide for employer’s share of P.F. equivalent to employee’s share to P.F. Pass Journal entries. Show how will this appear in final accounts?

Answer

- Journal entry

Dr.

Salaries A/c

2,000

To Employer’s contribution to P.F. A/c

2,000

(Employer’s contribution to P.F. entered)

- Profit and Loss Account for the year ended on Mar 31, 2009

- Balance Sheet as on Mar 31, 2009

Example 2: Following are the extracts from a Trial Balance of a firm as on Mar 31, 2009

|

Dr. Balance |

Cr. Balance |

Salaries Less P.F. |

12,000 |

|

P.F. Remittance (including 50% employer’s contribution) |

1,000 |

|

Pass the necessary Journal entry. How will you treat in Final Accounts?

Answer

Entry (1)

Salaries A/c |

Dr. 1,000 |

|

To Employee’s contribution to P.F. |

|

500 |

To Employer’s contribution to P.F. |

|

500 |

| (P.F. remittance transferred to Salary) |

|

|

|

|

|

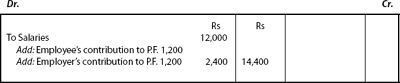

Example 3: Following is the extract from a Trial Balance

|

Dr. Balance Rs |

Cr. Balance Rs |

Salaries Less P.F. |

12,000 |

|

Employee’s Contribution to P.F. |

1,200 |

|

Information: Provide for employee’s share of P.F. equivalent to employee’s share to P.F.

Answer

Entry:

-

Salary A/c

Dr. 1,200

To Employee’s contribution to P.F.

1,200

(employee’s contribution transferred to Salary A/c)

-

Salary A/c

Dr. 1,200

To Employer’s contribution to P.F.

1,200

(employer’s contribution provided for)

- Profit and Loss Account for the year ended ….

- Balance Sheet as on …..

Illustration: 23

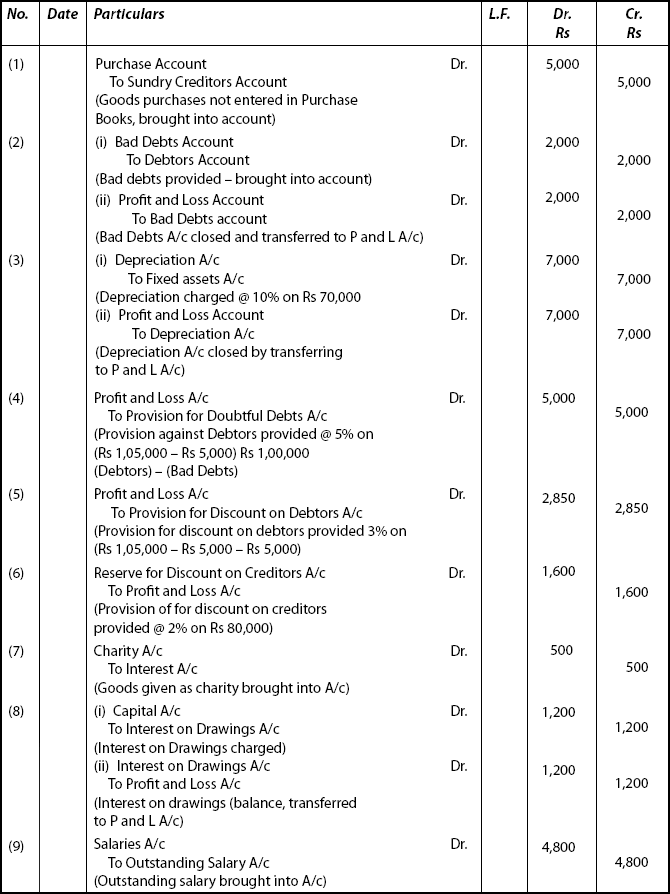

You are required to pass the necessary adjusting entries for the following items appearing in the Trial Balance as on Mar 31, 2009.

- Closing stock in hand as on Mar 31, 2009 Rs 12,500

- Rent unpaid Rs 1,200

- Rent received in advance Rs 900

- Interest due but not received Rs 750

- Drawings in goods Rs 1,400

- Insurance for the next period paid Rs 450

- Wages paid Rs 1,000 for installation of plant

- Goods worth 1,100 distributed as free samples

- Capital as on Apr 1, 2008: Rs 75,000. Allow interest on capital @ 12% p.a.

Solution

Journal

Illustration: 24

You are required to pass the necessary adjusting entries for the following that appear outside the Trial Balance as on Mar 31, 2009:

- Goods purchased Rs 5,000 were taken to stock but brought to enter in purchases book.

- Bad debts to be written off Rs 2,000

- Depreciation is to be provided on fixed assets @ 10%

- Create provision for doubtful debts @ 5%

- Provide a provision for discount on debtors @ 3%

- Create reserve for discount on creditors @ 2%

- Goods worth Rs 500 were given as charity

- Allow interest on drawings @ 12%

- Salaries unpaid Rs 4,800 further information: Fixed Assets: 7,000

Debtors: 1,05,000

Creditors: 80,000

Drawings: 10,000

Solution

Journal

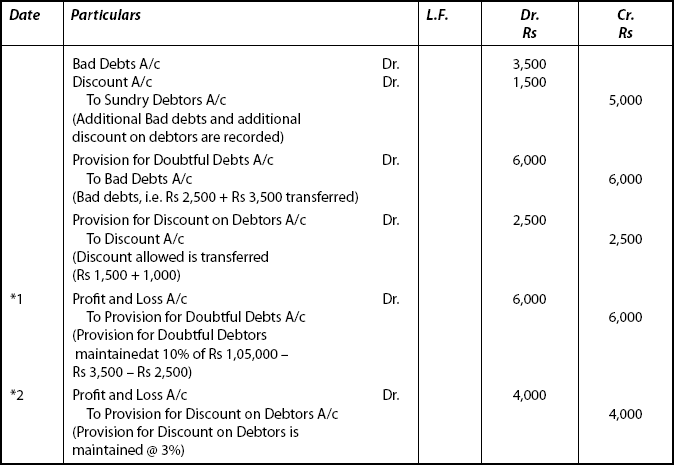

Illustration: 25

Following are the extracts from a Trial Balance of a business firm as on Mar 31, 2009

| Name of Account | Dr. Balance Rs |

Cr. Balance Rs |

|---|---|---|

Sundry Debtors |

1,05,000 |

|

Provision for Doubtful Debts |

|

10,000 |

Provision for Discount on Debtors |

|

1,200 |

Bad Debts |

2,500 |

|

Discount |

1,000 |

|

Additional Information

- Additional bad debts: Rs 3,500

- Additional discount allowed to debtors Rs 1,500

- Provision for bad debts to be maintained @ 10% on debtors

- Maintain a provision for discount @ 3% on debtors

You are required to

- Pass the necessary journal entries

- Prepare the necessary (ledger) accounts

- Prepare the final accounts (relating to these items only).

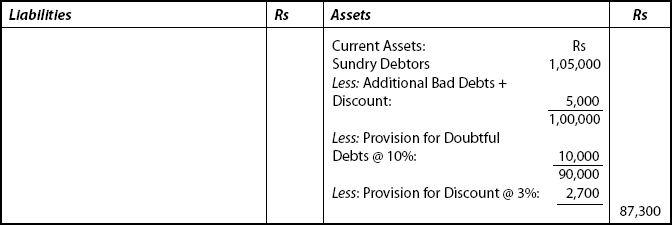

Solution:

Step 1: Adjusting Entries have to be Recorded in the Books of Journal

Journal

Step 2: Preparation of Ledger Accounts

(i) Sundry Debtors Account

*1(iii) Provision for Doubtful Debts Account

(iv) Discount Allowed Account

*2(v) Provision for Discount on Debtors Account

Final Accounts

An Extract of Profit and Loss Account for the year ended on Mar 31, 2009

Illustration: 26

A book-keeper has submitted to you the following Trial balance of Mr. Patel wherein the total of debit and credit balances is not equal:

| Particulars | Debit Balance Rs | Credit Balance Rs |

|---|---|---|

Capital |

— |

15,340 |

Cash in hand |

— |

60 |

Purchases |

17,980 |

— |

Sales |

— |

22,120 |

Cash at bank |

1,770 |

— |

Fixtures and Fittings |

450 |

— |

Freehold Premises |

3,000 |

— |

Lighting and Heating |

130 |

— |

Bills Receivable |

— |

1,650 |

Returns Inwards |

— |

60 |

Salaries |

2,150 |

— |

Creditors |

— |

3,780 |

Debtors |

11,400 |

— |

Stock (Apr 1, 2008) |

6,000 |

— |

Printing |

450 |

— |

Bills Payable |

3,750 |

— |

Rates, Taxes and Insurance |

380 |

— |

Discounts Received |

890 |

— |

Discounts Allowed |

— |

400 |

|

48,350 |

43,410 |

- You are required to redraft the Trial Balance correctly.

- Prepare a Trading and Profit and Loss Account and a Balance Sheet after taking into account the following adjustments:

- Stock in hand on Mar 31, 2009 was valued at Rs 3,600

- Depreciate fixtures and fittings by Rs 50

- Rs 700 was due and unpaid in respect of salaries

- Rates and insurance has been paid in advance to the extent of Rs 80

Solution:

First note down the following mistakes.

- Cash in hand is entered wrongly in the credit balances column. It has to be corrected by entering in the debit balances column.

- Similarly, returns inwards will have to be corrected by entering it in debit balances column.

- Bills Receivable and Bills Payable — both wrongly entered. This mistake has to be set right by interchange of amount.

- Discount allowed and Discount received are to be interchanged.

Redrafted Trial Balance as on Mar 31, 2009

| Particulars | Debit Rs | Credit Rs |

|---|---|---|

Capital |

— |

15,340 |

Cash in hand |

60 |

— |

Cash at bank |

1,770 |

— |

Purchases |

17,980 |

— |

Sales |

— |

22,120 |

Fixtures and Fittings |

450 |

— |

Freehold Premises |

3,000 |

— |

Lighting and Heating |

130 |

— |

Bills Receivable |

1,650 |

— |

Returns Inwards |

60 |

— |

Salaries |

2,150 |

— |

Creditors |

— |

3,780 |

Debtors |

11,400 |

— |

Stock (Apr 1, 2008) |

6,000 |

— |

Printing |

450 |

— |

Bills Payable |

— |

3,750 |

Rates, Taxes and Insurance |

380 |

— |

Discounts Received |

— |

890 |

Discounts Allowed |

400 |

— |

|

45,880 |

45,880 |

Mr. Patel Trading and Profit and Loss Account for the year ended on Mar 31, 2009

Illustration: 27

From the following Trial Balance of Mr. Reddy, you are required to prepare Trading and Profit and Loss Account for the year ended on Mar 31, 2009 and a Balance Sheet on that date:

| Particulars | Debit Balance Rs | Credit Balance Rs |

|---|---|---|

Capital |

— |

1,00,000 |

Drawings |

12,000 |

— |

Sundry Creditors |

— |

40,000 |

Cash-in-hand |

5,000 |

— |

Cash-at-bank |

11,600 |

— |

Sundry Debtors |

51,000 |

— |

10% Loan (taken on Sep 1, 2008) |

— |

20,000 |

Provision for Doubtful Debts |

— |

4,000 |

Furniture |

12,000 |

— |

Machinery |

28,400 |

— |

Stock (Apr 1, 2008) |

80,000 |

— |

Purchases |

1,80,000 |

— |

Rent and Taxes |

6,800 |

— |

Salaries |

18,000 |

— |

Manufacturing Wages |

25,000 |

— |

Sales |

— |

2,80,800 |

Sundry Expenses |

2,000 |

— |

Insurance (including a premium of Rs 600 per annum paid Sep 30, 2009) |

800 |

— |

Commission |

— |

1,400 |

Carriage |

4,000 |

— |

Travelling Expenses |

1,600 |

— |

Bills Receivable |

8,000 |

— |

|

4,46,200 |

4,46,200 |

- Stock on Mar 31, 2009 was Rs 76,000

- Write off bad debts Rs 1,000 and maintain the provision for doubtful debts at 5% on debtors

- Manufacturing wages include Rs 1,600 for erection of new machinery on Mar 1, 2009

- Depreciate machinery by 5% and furniture by 10%

[B. Com (Hons)—Modified]

Solution

Note:

- Bad Debts are shown outside the Trial Balance. That amount has to be deducted from debtors (i.e., Rs 1,000)

- Calculation to maintain provision for doubtful debts @ 5%

-

Debtors

=

Rs 51,000

Less: Bad Debts

=

Rs 1,000

(Given in adjustments)

Rs 50,000

Less: Provision @ 5%:

2,500

Rs 47,500

To be shown in balance sheet

-

Provision for Bad Debts:

Rs 4,000

(Given)

Less: 5% as

computed above:

Rs 2,500

Rs 1,500

To be shown in P and L A/c

-

Mr. Reddy Trading and Profit and Loss Account for the year ended on Mar 31, 2009

Illustration: 28

The following is the Trial Balance extracted from the books of Shri Arvind as on Dec 31, 2008:

| Particulars | Debit Balance Rs | Credit Balance Rs |

|---|---|---|

Capital |

— |

2,00,000 |

Plant and Machinery |

1,56,000 |

— |

Furniture |

4,000 |

— |

Purchases and Sales |

1,20,000 |

2,54,000 |

Returns |

2,000 |

1,500 |

Opening Stock |

60,000 |

— |

Discount |

850 |

1,600 |

Sundry Debtors/Creditors |

90,000 |

50,000 |

Salaries |

15,100 |

— |

Manufacturing Wages |

20,000 |

— |

Carriage Outwards |

2,400 |

— |

Provision for Doubtful Debts |

— |

1,050 |

Rent, Rates and Taxes |

20,000 |

— |

Advertisements |

4,000 |

— |

Cash |

13,800 |

— |

|

5,08,150 |

5,08,150 |

Adjustments

- Closing stock was valued at Rs 68,440

- Provision for doubtful debts is to be kept at Rs 1,000

- Depreciate plant and machinery @ 10%

- The proprietor has taken goods worth Rs 10,000 for his personal use and additionally distributed goods worth Rs 2,000 as samples

- Purchase of furniture Rs 1,840 has been passed through purchases book

[B. com. Hons—(Modified)]

Solution

Note:

- The proprietor took goods worth Rs 10,000 for his own personal use. It has to be treated as drawings. Adjustment: In trading account it has to be deducted from purchases. Further in the balance sheet it has to be deducted from the capital.

- Samples Rs 2,000 is also to be deducted from purchases in the trading account and it has to be shown in profit and loss account as “advertisement expenses.”

- Furniture purchases are entered through purchases book. Hence it has to be deducted from purchases in the Trading Account. It is shown as an asset by way of addition to the existing furniture.

- Provision for bad debts is to be kept at Rs 1,000. It is shown as Rs 1,050. So (Rs 1,050 − Rs 1,000) Rs 50, is to be shown in Profit and Loss Account and Rs 1,000 is shown by way of deduction from the debtors on the Assets side of the Balance Sheet.

Balance Sheet of Shri Arvind as on Dec 31, 2008

Illustration: 29

The following Trial Balance is extracted from the books of Shri Gulsar on Mar 31, 2009

| Particulars | Dr. (Rs) | Cr. (Rs) |

|---|---|---|

Capital |

— |

25,000 |

Furniture and Fittings |

1,280 |

— |

Motor cycle |

12,500 |

— |

Building |

15,000 |

— |

Bad Debts |

250 |

— |

Provision for Doubtful Debts |

— |

400 |

Sundry Debtors/Creditors |

7,600 |

5,000 |

Stock (as on Apr 1, 2008) |

6,920 |

— |

Purchases and Sales |

10,950 |

30,900 |

Bank Overdraft |

— |

5,700 |

Returns |

400 |

250 |

Interest on Bank Overdraft |

236 |

— |

Advertising |

900 |

— |

Commission |

— |

750 |

Cash |

1,300 |

— |

Taxes and Insurance Premium |

1,564 |

— |

General Expenses |

2,500 |

— |

Salaries |

6,600 |

— |

|

68,000 |

68,000 |

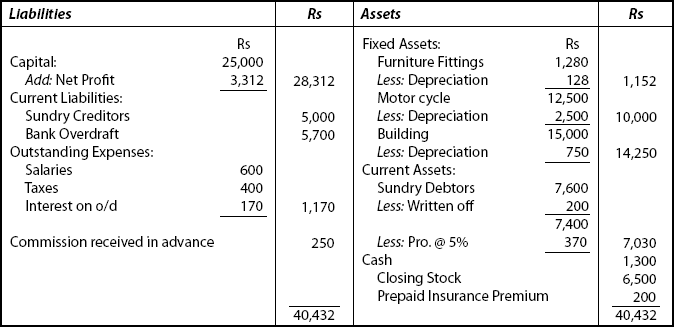

Adjustments

- Stock on hand (as on Mar 31, 2009) Rs 6,500

- Depreciate building @ 5% p.a.; furniture @ 10% p.a.; motor cycle @ 20% p.a.

- Rs 170 is due for interest on bank overdraft

- Salaries Rs 600 and taxes Rs 400 are outstanding

- Insurance premium Rs 200 is prepaid

- One-third of the commission received is in respect of work to be done next year

- Write off a further sum of Rs 200 as bad debts from the debtors

- Create provision for doubtful debts @ 5% on debtors, you are required to prepare a Trading and Profit and Loss Account for the year ended on Mar 31, 2009 and a Balance Sheet on that date

Solution:

Provision for doubtful debts is calculated as |

||

Debtors |

7,600 |

(given in Trial Balance) |

Less: Written off |

200 |

(given in adjustments) |

|

7,400 |

|

Less: Provision @ 5% |

370 |

|

|

7,030 |

(to be shown in Balance Sheet) |

For Profit and Loss Account |

|

|

Bad Debts |

Rs 250 |

(shown in Trial Balance) |

Add: Written off |

Rs 200 |

(shown in adjustments) |

|

450 |

|

Add: Provision |

370 |

|

|

820 |

|

Less: Existing Provision |

400 |

(given in Trial Balance) |

|

420 |

(to be shown in P and L A/c) |

Balance Sheet of Shri Gulsar as on Mar 31, 2009

Illustration: 30

Prepare Trading and Profit and Loss Account and Balance Sheet from the following particulars as on Mar 31, 2009.

Trial Balance

| Particulars | Dr. (Rs) | Cr. (Rs) |

|---|---|---|

Capital/Drawings |

2,800 |

20,000 |

Cash-in-hand |

3,000 |

— |

Purchases/Sales |

24,000 |

30,000 |

Returns |

2,000 |

4,000; |

Bank Overdraft @ 5% |

— |

4,000 |

Salaries |

5,000 |

— |

P.F. remittance (deducted from salary) |

— |

1,000 |

Taxes and Insurance |

1,000 |

— |

Provision for Doubtful debts |

— |

2,000 |

Bad Debts |

1,000 |

— |

Sundry Debtors and Creditors |

10,000 |

3,700 |

Commission |

— |

1,000 |

Investments |

8,000 |

— |

Stock (as on Apr 1, 2008) |

6,000 |

— |

Furniture |

2,200 |

— |

Bills Receivable and Bills Payable |

6,000 |

5,000 |

Sales Tax Collected |

— |

300 |

|

71,000 |

71,000 |

Further, you are required to take into account the following information:

- Salary Rs 200 and taxes Rs 800 are outstanding but insurance Rs 100 pre-paid

- Commission Rs 200 is received in advance for work to be done next year

- Provision for doubtful debts is to be maintained at 20%

- Depreciation on furniture is to be charged @ 10% p.a.

- Interest accrued on investments Rs 420

- Stock as on Mar 31, 2009 is valued at Rs 9,000

- A fire accrued on Mar 1, 2009 in the godown which destroyed the goods worth Rs 8,000, and insurance claim was received for Rs 6,000

- Provide for employer’s share of P.F. equivalent to employee’s share to P.F.

Solution:

Note:

- P.F. Contribution = Rs 1,000 (shown in Trial Balance)

Contribution by employer 100% = Rs 1,000

In P and L A/c this P.F. employer contribution amount has to be added to salary

In Balance Sheet, this has to be shown in Liabilities side (i.e., Rs 2,000)

-

Loss by fire = Goods worth =

Rs 8,000

Insurance received:

Rs 6,000

Loss (Abnormal):

RS 2,000

This is shown in Trading A/c on the credit side and again in P and L on the debit side.

Balance Sheet as on Mar 31, 2009

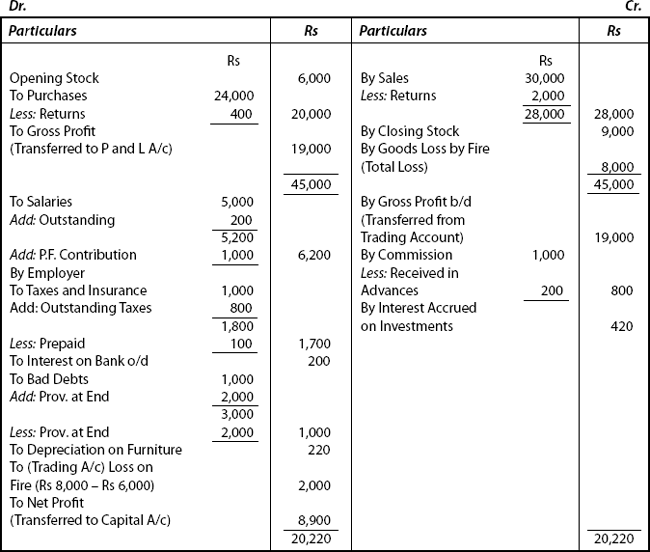

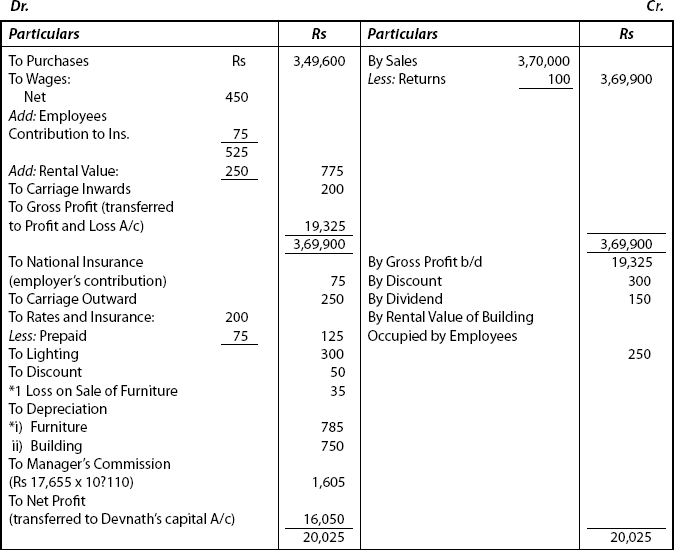

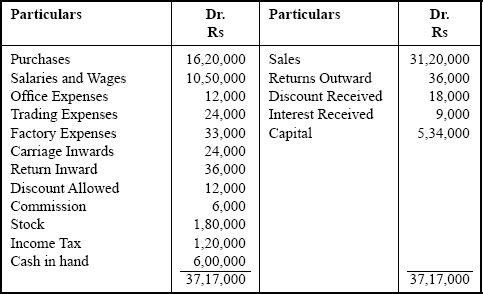

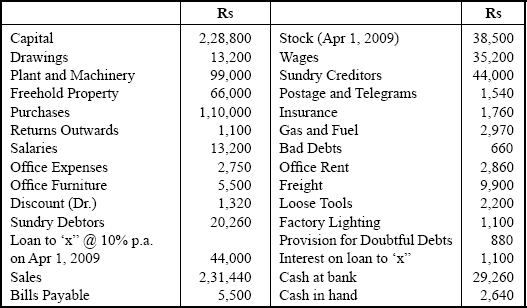

Illustration: 30 (another approach)

- Loss by fire: This may be treated in another way. Goods worth destroyed by fire Rs 8,000 is shown in Trading Account.

- Actual loss incurred, i.e. goods worth lost by fire — insurance claim allowed Rs 8,000 — Rs 6,000 = Rs 2,000 is debited to Profit and Loss Account

- Claim allowed by the insurance company, i.e. Rs 6,000 is shown on the assets side of the Balance Sheet.

Trading and Profit and Loss Account for the year ended on Mar 31, 2009

Balance Sheet as on Mar 31, 2009

Illustration: 31