Chapter 11

Inventory – Valuation

LEARNING OBJECTIVES

After studying this chapter, you will be able to:

Understand the Meaning of Inventory and Inventory Valuation

Recognise the Importance of Inventory Valuation

Assess the Technical Features of Inventory Records System

Distinguish between Periodic Inventory System and Perpetual Inventory System

Understand the Concepts – Cost of Purchase, Costs of Conversion and Other Costs as per Accounting Standard (AS)–2 (Revised)

Apply Cost Formula

Understand the Specific Identification Costs Method

Understand the Meaning and Features of First-In-First-Out (FIFO) Method

Prepare Stock Ledger Under FIFO Method and to Compute Costs of Goods Sold Under Both Systems (Periodic System and Perpetual System)

Understand Last-In-First-Out (LIFO) Method (not Recognised by AS–2)

Apply Weighted Average Method

Prepare Stock Ledger Applying Weighted Average Method and to Compute the Value of Ending Inventory Under Both the Systems

Decide the Choice of Inventory Valuation Methods

Ascertain the Value of Inventory as on the Balance Sheet Date

Salient Features of AS–2 (Revised) Relating to Inventory

INTRODUCTION

Inventory is a current asset. It constitutes a major part in financial statements of trading and, more specifically manufacturing concerns. After cash and receivables, this plays an important role. The term inventory refers to “the stock pile of the products a firm is offering for sale and the components that make up the product.” It is a well-known fact that inventories have their own effect on the liquidity of enterprises. The correct financial position of a firm can be determined only if the inventories are valued precisely. The gross profit of a firm is closely associated with the cost of goods sold, whereas the cost of goods sold is directly affected by inventories (both opening and ending). The following equation exposes its close relationship.

Cost of Goods Sold = Opening Stock + Purchases – Closing Stock and Expenses

The closing stock of an accounting period will become the opening stock of the next period. Hence, the valuation of inventory has attained greater significance. Despite such a high level of significance, the valuation of inventories is quite often not accurate because of the policies of the management of the firm and the accounting procedures adopted by the accountants. Hence, to ensure objective measurement and present an accurate income and position statement, proper valuation of inventory is necessary for keeping proper stock registers, stock verification, proper pricing of issues and following a consistent policy or method. These factors for the valuation of inventories are of vital importance. This chapter analyses such factors in detail by following the standard requirements envisaged in Accounting Standard (AS)–2 issued by the Institute of Chartered Accountants of India (ICAI).

OBJECTIVE 1: MEANING

1. Simple Meaning: Inventory is an asset. However, in the broad sense, the term inventory means an exhaustive list of assets – goods that a company holds from the stage of purchase till the stage they are sold off.

According to AS–2 (Revised), “Inventories are assets held for sale in the ordinary course of business; in the process of production for such sale; or in the form of materials or supplies to be consumed in production process or in the rendering of services.”

Inventories cover the goods purchased and held for resale, for example, merchandise (goods) purchased by a retailer and held for resale, computer software held for resale, land and other property held for resale. Inventories also include finished goods produced or work in progress being produced by the enterprises and include materials, maintenance supplier consumables and loose tools awaiting to be used in the production process. Inventories vary according to the nature of the business.

2. Trading Concern: Inventories under this type encompass products purchased for resale in the existing form, an inventory of supplies such as wrapping paper, cartons and stationery.

3. Manufacturing Concern: Inventories under this type consist of raw materials, work in process and finished products.

According to AS–10, accounting for fixed assets machinery spares is not included in the inventory and are to be treated as per AS–10.

OBJECTIVE 2: SIGNIFICANCE OF INVENTORY VALUATION

1. Backbone: “Inventory” is the major asset for any business enterprise (trading as well as manufacturing). It constitutes more than 75% of the total current assets. It is the backbone of the entire business edifice.

2. Liquidity: Creditors always have an eye on the liquidity position of the business entity. An easy way to judge the liquidity position of an enterprise is to compute accounting ratios. The current assets” role is very important. As inventories constitute the major proportion of current assets, its valuation is of vital importance to judge the liquidity of a concern. As such, the role of inventories cannot be minimised.

3. Determination of True Income: To determine true income, proper valuation of assets is important.

Gross Profit = Sales – Cost of Goods Sold

As gross profit is directly affected by the valuation of stock, true profit cannot be ascertained unless proper valuation of stock is carried out. Its impact on the income statement is high.

4. Determination of True Financial Position: The true financial position of a concern cannot be arrived at improper valuation of inventories from their initial stage. Its importance is confirmed again by the following equation:

Cost of Goods Sold = Opening Stock + Purchases – Closing Stock + Direct Expenses

The main components of the above equation are Opening Stock, Purchases and Closing Stock – all the above components represent the inventories. Unless it is valued properly, it will affect the Income Statement and the Balance Sheet. Hence, the valuation of inventory is significant to determine the true financial position of the enterprises.

OBJECTIVE 3: INVENTORY RECORD SYSTEMS

To determine the physical quantities and rupee value of inventories sold and in hand, the following systems are adopted: 1. Periodic Inventory System and 2. Perpetual Inventory System.

3.1 Periodic Inventory System

Meaning: Periodic inventory system is a method of ascertaining inventory by taking the actual physical count (measure or weight) of all the inventory items on hand at a particular date, usually at the end of an accounting period. It is also known as the physical inventory system because of the actual physical count. The physical count of the stock may be undertaken on any date (not necessarily at the end of an accounting period), whenever information about inventory is required. The cost of goods sold is determined using the following equation:

Cost of Goods Sold = Opening Inventory + Purchases – Closing Stock

The cost of goods sold includes cost of lost goods also.

Accounting Procedure:

- Record all purchases of inventories (as debits) to Purchase Account.

- No entry is to be made at the time of sale for cost of goods sold.

- Stock of Inventory Account is made up-to-date by way of adjusting entries.

(The balance in an Inventory Account remains unchanged because purchases and sales are not through the Inventory Account.)

3.2 Perpetual Inventory System

The perpetual inventory system is a system of records that reveals the physical movement of stocks and their current balance. It is a method of recording inventory balances after each purchase and sale takes place. The closing inventory is calculated as a residual factor, which is calculated by using the following equation:

Closing Inventory = Opening Inventory + Purchases – Cost of Goods Sold

Accounting Procedure:

- A separate account for each type of inventory is maintained in a card to record the purchase and sale of each such inventory item.

- The detailed inventory records for each different item show receipts (purchases), issues (sales) and balance on hand in both quantities and amount.

- The increases (purchases) in inventory items are recorded as receipts (or debits) to the respective accounts and the decreases (sales) are recorded as issues (or credits). The balances of the inventory items accounts are known as the Book Inventories of the Items on Hand.

- The physical inventory of each item of inventory is also undertaken periodically, at least once a year (at the end of the accounting period).

- Finally, the records maintained under the perpetual inventory system are compared with actual quantities of each item on hand. If any discrepancy arises, it has to be corrected.

3.3 Distinction Between Periodic Inventory System and Perpetual Inventory System

| Basis of Distinction | Periodic Inventory System | Perpetual Inventory System |

|---|---|---|

1. Basis |

It is based on the actual physical count |

It is based on records |

2. Method and cost |

It is a simple method and cost-wise, it is economical |

It is comparatively complex and cost-wise, it is not economical as records have to be maintained |

3. Valuation of inventory |

Inventory is directly ascertained by applying the method of valuation of inventories |

Inventory is ascertained by applying the equation: Closing Inventory = Opening Inventory + Purchases – Cost of Goods Sold |

4. Calculation of cost of goods sold |

Cost of goods sold is ascertained by applying the equation: Cost of Goods Sold = Opening inventory + Purchases – Closing Inventory |

Cost of goods is ascertained directly by applying the method of valuation of inventories |

5. Continuous checking |

Inventory checking is not frequent and continuous |

Inventory checking is continuous and frequent |

6. Lost goods |

Cost of sales includes lost goods |

Inventory includes lost goods |

7. Residual factor |

Cost of sales is a residual factor |

Closing inventory is the residual factor |

8. Inventory control |

It does not provide a basis for inventory control |

It provides a basis for inventory as physical checkups are compared with records |

9. Application of method of valuation |

The method of valuation is applied only once at the end of the accounting period to ascertain the cost of closing inventory |

The method of valuation is applied continuously to ascertain the cost of goods sold |

OBJECTIVE 4: VALUATION OF INVENTORIES

AS–2(Revised) stipulates that inventories should be valued at the lower of the cost and net realisable value.

4.1 Important Concepts

As such, the basis of valuation is cost. According to the provisions of AS–2 (Revised), “the cost of inventories comprises all costs of purchase, costs of conversion and other costs incurred in bringing the inventories to their present location and condition.”

Costs of Purchase: The costs of purchase consist of the purchase price that includes:

(i) Duties, (ii) Taxes, (iii) Freight inwards, (iv) Cost of packing, (v) Insurance, (vi) Transportation, (vii) Storage.

By deducting

(i) Trade discount, (ii) Rebates, (iii) Other relevant items.

Note: Cash discount is not to be taken into account for inventory valuation.

Costs of Conversion: In case of production it includes:

- Direct labour.

- Fixed production overheads: depreciation, maintenance of factory and the like.

- Variable production overheads – indirect material, indirect labour and so on.

Other Costs: All other costs incurred in bringing inventories to the present location and condition.

Costs Excluded

- Interest and other borrowing costs.

- Abnormal loss (materials).

- Abnormal loss (labour).

- Abnormal loss (production).

- Other costs that are not related to inventories (from purchase to the present location and condition).

4.2 Cost Formulae

AS–2 (Revised) provides certain rules for the valuation of inventories. Among them the most important are:

The cost of inventories of items that is not ordinarily inter-changeable, and goods or services produced and segregated for specific projects should be assigned by Specific Identification of their individual Costs.

The cost of inventories other than those dealt with, as explained in Section 4.1 should be assigned using the First-In-First-Out (FIFO) or Weighted Average Cost Formula.

According to these provisions of AS–2 (Revised), only the following methods of inventory valuation are permitted.

- Specific Identification (of costs) Method

- FIFO Method

- Weighted Average Cost Method

OBJECTIVE 5: SPECIFIC IDENTIFICATION OF COSTS

Specific identification of costs means that specific costs are attributed to identified items of inventory. For items which are segregated for a specific project (purchased or produced – it is immaterial), appropriate treatment for such items will be of much importance. The process of assigning costs involves the following two procedures:

- One has to keep track of the purchase price of each specific unit.

- To know which specific units were sold.

The most important feature of this method is that business enterprise must keep track of the cost of each individual item purchased and sold. This process is relatively less complicated, say simple, as the cost is marked on the unit or on its container or can be traced to cost record. This method is suitable where the purchases are not frequent and where the old purchased items do not mix up with the newly purchased items i.e. items purchased a few years ago should not be mingled with those items purchased now, for example, furniture, automobiles and so on. Under this method, matching cost with revenue is perfect because actual costs form the basis for cost of goods sold and closing inventory.

This method has its own short comings. This is not suitable,

- when units are identical and interchangeable

- when there are frequent changes in acquisition costs

- when identical units of a particular item of inventory is purchased at different costs at different times

- under such circumstances described above, it is difficult to assign appropriate cost to cost of goods sold and to the closing inventory.

Notwithstanding the efforts taken by ICAI to establish an appropriate method of valuing the inventories, this approach also suffers from certain limitations as discussed above.

OBJECTIVE 6: FIRST-IN-FIRST-OUT METHOD

- This method is based on the assumption that flow of cost is in the order in which the expenditures were made.

- To explain, the units that are received first will be sold first, i.e. the units are sold in the order in which they were acquired (purchased).

- The flow of costs is presumed to be the same as flow of goods.

- The closing (ending) inventory consists of the latest lots and is valued at the price paid for such lots.

- The results achieved under this method may be more or less similar to those obtained under specific identification method.

6.1 Merits

- This method is suitable for items of perishable goods because goods purchased first are sold first.

- FIFO is easy to operate – in situations where price fluctuation is less.

- This method does not give room for manipulation of income.

- Assignment of cost against revenue is matched, as they are fixed in the order in which costs are incurred.

- This method is alive to the price trend in the market.

- Closing (ending) inventory valuation reflects the true financial position due to its recent purchase.

- No unrealised inventory profit or loss can be made under this method as it is based on cost.

6.2 Demerits

- In the periods of rising prices, higher income will be reported resulting in higher tax liability.

- In a period when prices are fluctuating, the cost of purchase do not represent current market price.

- In case where production cycle is lengthy, true profit cannot be shown in income statements.

- This method does not match current cost of goods sold with current revenues.

- Comparison among similar jobs is not easy.

- This method involves more mathematical work if prices fluctuate.

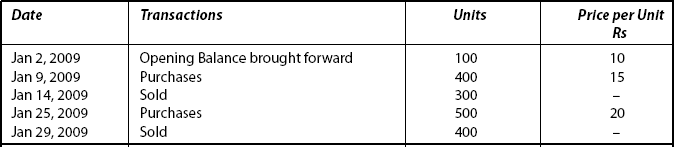

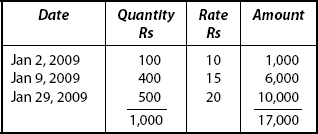

Illustration: 1

From the following information, you are required to calculate the value of Ending Inventory and Cost of Goods Sold assuming (a) Perpetual System and (b) Periodic Inventory System under FIFO method.

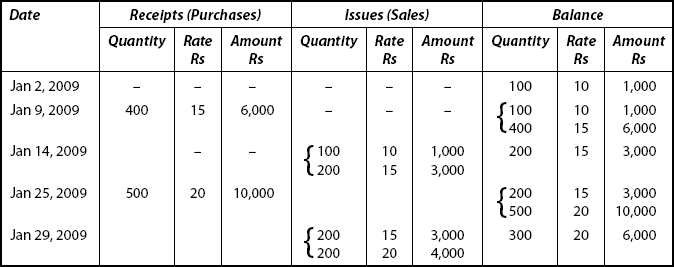

Solution: Step 1

Stock Ledger under FIFO Method Perpetual System

Step 2 Calculation of Value of Ending Inventory

|

|

|

Rs. |

|

1. |

Opening Inventory |

1,000 |

|

2. |

Add: Purchases |

|

|

|

6,000 + 10,000 |

16,000 |

|

|

|

17,000 |

|

3. |

Less: Cost of Goods Sold |

|

|

|

(1000 + 3000 + 3000 + 4000) |

11,000 |

|

4. |

Value of Ending Inventory |

|

|

|

(1 + 2 – 3) |

6,000 |

Step 3 Statement Showing the Value of Inventory and Cost of Goods Sold (Periodic System)

|

|

|

Rs. |

|

1. |

Opening Inventory |

1,000 |

|

2. |

Add: Purchases |

|

|

|

(Rs 6,000 + Rs 10,000) |

16,000 |

|

|

|

17,000 |

|

3. |

Less: Ending Inventory (300 × Rs 20) |

6,000 |

|

4. |

Cost of Goods Sold (1 + 2 – 3) |

11,000 |

Notes

- Units (in quantity) and Rate (in rupees) are shown within brackets for easy comprehension, which was purchased first and which has to be sold first.

- In case, see the sale on Jan 14, 2009 – the selling unit is 300 units. First from the opening balance 100 units @ Rs 10 and the remaining 200 units from the part that was purchased on Jan 9 @ Rs 15 were taken into account, i.e. units purchased first, were sold first.

- In the valuation of Ending Inventory under Perpetual System, the Closing Inventory consists of the latest lots and is valued at the price paid for such lots.

- In Periodic System, the Cost of Goods Sold is the residual factor, and the steps involved in its computation are shown in Step 3.

OBJECTIVE 7: LAST-IN-FIRST-OUT METHOD (LIFO)

Though this method is not recognised by AS–2 (Revised), this method is explained here for academic interest. The salient features of this method are:

- Under this method, goods which are purchased last are sold first.

- This assumption is made for the purpose of assigning costs and not for physical flow of goods.

- As such, the goods sold contest of the latest lots, which are valued at the price paid for such lots.

7.1 Merits

- Under this method, current costs are in tune with current revenues.

- The Closing Inventory is valued at lower cost of old purchases, which will not reflect the current price level trend.

- As current costs are matched with current revenues/lower income may be reported in periods of rising prices.

- As it is based on cost, unrealised inventory profit/loss cannot be worked out.

7.2 Demerits

- Cost flows do not correspond to the physical flow of goods.

- Measurement of income is not in conformity with utilisation of income.

- Value of Ending Inventory does not reflect the current price level.

- In periods of falling prices, higher income is reported thereby increases tax liability.

- It involves more calculation work.

Illustration: 2

Based on the figures in Illustration 1, you are required to compute the value of Ending Inventory and Cost of Goods Sold under LIFO Method in the following cases alternatively.

Case (a): Perpetual Inventory System

Case (b): Periodic Inventory System

Solution: Step 1

Stock Ledger under LIFO Method

Case (a): Calculation of Ending Inventory (Perpetual System)

|

|

|

Rs. |

|

1. |

Opening Inventory |

1,000 |

|

2. |

Add: Purchases |

16,000 |

|

|

(Rs 16,000 + Rs 10,000) |

17,000 |

|

3. |

Less: Cost of Goods Sold |

|

|

|

(300 × 15: Rs 4,500 + 400 × Rs 20 = Rs 8,000) |

12,500 |

|

4. |

Ending Inventory (1 + 2 – 3) |

4,500 |

Hence, value of Ending Inventory = Rs 4,500

Now, compare this with FIFO Method where the value of Ending Inventory is Rs 6,000.

Step 3

Case (b): Calculation of Valuation of Inventory and Cost of Goods Sold (Periodic System)

|

|

|

Rs. |

|

1. |

Opening Inventory |

1,000 |

|

2. |

Add: Purchases (Rs 6,000 + Rs 10,000) |

16,000 |

|

|

|

17,000 |

|

3. |

Less: Ending Inventory |

|

|

|

(100 × Rs 10 + 100 × Rs 15 + 100 × Rs 20) |

|

|

|

Rs 1000 + Rs 1,500 + Rs 2000 |

4,500 |

|

4. |

Cost of Goods Sold (1 + 2 – 3) |

12,500 |

|

|

Cost of Goods Sold = Rs 12,500 |

Now, compare this under LIFO Method where the value of Cost of Goods Sold is Rs 11,000 under Periodic System.

OBJECTIVE 8: WEIGHTED AVERAGE METHOD

The Weighted Average Price Method is based on the assumption that:

- Each sale of goods consists of a due proportion of the earlier lots.

- Such sale is valued at the weighted average price.

(whereas Total cost = Quantity × Cost per unit)

8.1 Procedure Under Periodic Inventory System

- In case a Perpetual Inventory System is used, the above explained weighted average cannot be applied because weighted average cost cannot be calculated until the end of the accounting period. To set right this defect, a MOVING WEIGHTED AVERAGE COST is applied.

Moving Average Cost: Under this procedure, a new unit cost is provided after every purchase.

8.2 Procedure Under Perpetual Inventory System

- Prices for units in the opening inventory and in each purchases are multiplied by number of units in the opening inventory and in each purchase and are then averaged (to be divided by total number of units) to find out the weighted average cost per unit.

- When goods are sold, this moving average cost existing at that time is used.

- It should be noted that a new weighted average unit cost is calculated after each purchase at different price and this figure is used to price all units sold till the next purchase date.

8.2.1 Merits

- This method is realistic, objective and consistent.

- Manipulation may not be possible.

- It averages out the effect of price fluctuations.

- It is most suitable for process type industries.

8.2.2 Demerits

- This method needs more calculation work at each and every stage.

- The Ending Inventory differs from the conventional method of valuation of closing date.

- It is not suitable for job order type industries.

Illustration: 3

Using the information given in Illustration 1, you are required to apply Weighted Average Method to compute the value of Ending Inventory and Cost of Goods Sold in each of the following alternatives:

- Perpetual Inventory System

- Periodic Inventory System

Solution

Case (a): Stock Ledger under Weighted Average Method

Step 1

Step 2 Valuation of Ending Inventory

|

|

|

Rs. |

|

1. |

Opening Inventory |

1,000 |

|

2. |

Add: Purchases |

|

|

|

(Rs 6,000 + Rs 10,000) |

16,000 |

|

|

|

17,000 |

|

3. |

Less: Cost of Goods Sold |

|

|

|

(Rs 4,200 + Rs 7,316) |

11,516 |

|

4. |

Value of Ending Inventory |

5,484 |

|

|

(1 + 2 – 3) |

Case (b): Statement Showing the Weighted Average Cost per Unit under Weighted Average Method (Applying Periodic Inventory System)

Weighted Average Cost = Rs 17,000/1,000 = Rs 17 per unit

Step 4 |

Valuation of Ending Inventory and Cost of Goods Sold under Weighted Average Method using Periodic Inventory System |

|

|

|

Rs. |

|

1. |

Opening Inventory |

1,000 |

|

2. |

Add: Purchases |

|

|

|

(Rs 6,000 + Rs 10,000) |

16,000 |

|

|

|

17,000 |

|

3. |

Less: Ending Inventory |

|

|

|

(300 × Rs 17) |

5,100 |

|

4. |

Value of Cost of Goods Sold |

11,900 |

OBJECTIVE 9: CHOICE OF INVENTORY VALUATION METHODS

Compare the solutions to Illustrations 1, 2 and 3, and you will be able to judge to decide the choice of valuation method. Only simple figures and less number of transactions are used in the illustrations so as to enable the students to understand the techniques involved in each such method.

The choice of the method will be based on the following factors:

- In case of the period of rising prices:

Use of FIFO will result in

- Highest inventory valuation

- Lowest cost of goods sold

- As a result, net income will be high

Use of LIFO will reverse the above results.

- When a fall in price is the situation:

Use of FIFO will result in

- Lowest inventory valuation

- Highest cost of goods sold

- As a result, net income will be low

Use of LIFO will reverse the above results.

- To determine the method of valuation, prevailing trend in price level should be taken into consideration.

- It should be observed here, if price level is stable (see the three illustrations given above) – the result will be more or less same under all the three methods, i.e. FIFO, LIFO and Weighted Average Method.

- It should further be noted that the use of FIFO does not match recent costs with revenue but use of LIFO matches the latest costs with revenue. For this concept, use of LIFO is better than FIFO.

- Comparing FIFO and LIFO, “the Weighted Average Method gives a middle course between the effects of FIFO periodic and LIFO periodic methods.”

Under stable price level, the values of Closing Inventory, Cost of Goods Sold and net income will lie between LIFO and FIFO methods if Weighted Average Method is used (compare the results in all the 3 illustrations). - Weighted Average Method and FIFO Method will give the same result if the turnover ratio of inventory is very high.

To put in a nutshell, choice of the method depends on:

- Price level changes,

- Stock turnover,

- Company’s policy on profit,

- Accounting policy and procedure.

Illustration: 4

Purchases and sales of a certain product during Jan 2009 are given below.

Purchases

On Jan 2, 2009 100 units @ Rs 5

On Jan 12, 2009 200 units @ Rs 4.80

On Jan 17, 2009 100 units @ Rs 4.60

On Jan 22, 2009 100 units @ Rs 4.50

Sales

On Jan 7, 2009 50 units

On Jan 14, 2009 150 units

On Jan 28, 2009 100 units

There was no Opening Inventory.

You are required to compute the Cost of Goods Sold under the methods:

- FIFO

- LIFO and

- Weighted Average Cost

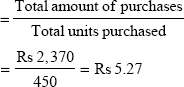

Solution: Step 1

Stock Ledger in the format has to be prepared and FIFO Method is to be used.

After that, Cost of Goods Sold is to be computed under both the systems – Perpetual and Periodic.

Stock Ledger (FIFO Method)

- Cost of Goods Sold (Perpetual System) = Rs 1,460

(Rs 250 + Rs 730 × Rs 480)

- Cost of Goods Sold (Periodic System)

= Opening Inventory + Purchase –Closing Inventory

= Nil + Rs 2,370 – Rs 910 = Rs 1,460

Stock Ledger (LIFO Method)

- Cost of Goods Sold (Perpetual System) = Rs 1,420

(Rs 250 + Rs 720 + Rs 450)

- Cost of Goods Sold (Periodic System)

= Opening Inventory + Purchases –Ending Inventory

= Nil + Rs 2,370 – Rs 1,190 = Rs 1,180

Stock Ledger (Weighted Average Method)

- Cost of Goods Sold (Perpetual System) = Rs 1,441

(Rs 250+ Rs 726 + Rs 465)

- Cost of Goods Sold (Periodic System)

Weighted Average Cost of 300 units sold = 300 × Rs 5.27 or Rs 2,370 × 300 = Rs 1,581

Illustration: 5

Renu Ltd started on Jan 1, 2008, purchased raw materials during 2008 as stated below:

|

|

|

Rate per kg Rs |

|

Jan 5 |

750 kg |

51 |

|

Jan 25 |

1,200 kg |

49 |

|

Feb 20 |

2,300 kg |

47 |

|

Mar 15 |

2,500 kg |

48 |

|

Oct 2 |

1,250 kg |

50 |

|

Dec 10 |

1,000 kg |

55 |

While preparing final accounts on Dec 31, 2008, the company had 1,200 kg of raw materials in its godown. You are required to compute the values of Closing Stock of raw materials and the Cost of Sales according to:

- First-In-First-Out (FIFO) Basis,

- Last-In-First-Out (LIFO) Basis, and

- Weighted Average Price (WAP) Basis.

Solution

First quantity of sales (raw materials consumed) is calculated.

|

Total Purchases in the year 2008 |

= |

9,000 kg |

|

Less: Closing Stock |

= |

1,200 kg |

|

Sales (consumed) |

= |

7,800 kg |

(a) FIFO Basis

|

|

|

Rs |

Cost of Ending Inventory |

1,000 × 55 |

= |

55,000 |

|

200 × 50 |

= |

10,000 |

|

|

|

65,000 |

Cost of Sales |

750 × 51 |

= |

38,250 |

|

1,200 × 49 |

= |

58,800 |

|

2,300 × 47 |

= |

1,08,100 |

|

2,500 × 48 |

= |

1,20,000 |

|

1,050 × 50 |

= |

52,500 |

|

|

|

3,77,650 |

(b) LIFO Basis

Cost of Ending Inventory |

750 × 51 |

= |

38,250 |

|

450 × 49 |

= |

22,050 |

|

|

|

60,300 |

Cost of Sales |

1,000 × 55 |

= |

55,000 |

|

1,250 × 50 |

= |

68,750 |

|

2,500 × 48 |

= |

1,20,000 |

|

2,300 × 47 |

= |

1,08,100 |

|

750 × 49 |

= |

36,750 |

|

|

|

3,84,600 |

(c) Weighted Average Basis

Total cost of Purchases is calculated as:

|

750 × 51 |

= |

38,250 |

|

1,200 × 49 |

= |

58,800 |

|

2,300 × 49 |

= |

1,08,100 |

|

2,500 × 48 |

= |

1,20,000 |

|

1,250 × 50 |

= |

68,750 |

|

1,000 × 55 |

= |

55,000 |

|

|

|

4,48,900 |

Weighted Average = 4,48,900/9,000 = Rs 49.88

Cost of Ending Inventory |

= |

1,200 × Rs 49.88 |

|

= |

Rs 59,856 |

Cost of Sales |

= |

7,800 × Rs 49.88 |

|

= |

Rs 3,89,064 |

Illustration: 6

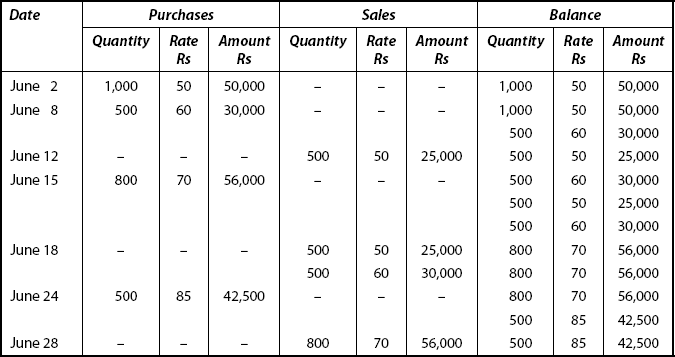

A retail shop dealing in knitwear has the following transactions during June 2008.

- The gross profit earned during June,

- The value of stock held on June 30, 2008 using each of the following alternative basis of valuation:

- FIFO,

- LIFO,

- Weighed Average Cost.

(B.Com – Madras, Modified)

Solution

Computation of Total Sales |

|

Rs |

|

June |

12 500 × 70 |

= |

35,000 |

June |

18 1,000 × 85 |

= |

85,000 |

June |

28 800 × 100 |

= |

80,000 |

Total Sales |

|

|

2,00,000 |

(a) Stock Ledger (FIFO)

- Cost of Sales = Rs 25,000 + Rs 25,000 + Rs 30,000 + Rs 56,000 = Rs 1,36,000

- Gross Profit = Sales –Cost of Sales = Rs 2,00,000 – Rs 1,36,000 = Rs 64,000

- Closing Stock = Rs 42,500

(b) Stock Ledger (LIFO)

- Cost of Sales = Rs 30,000 + Rs 56,000 + Rs 10,000 + Rs 42,500 + Rs 15,000 = Rs 1,53,500

- Gross Profit = Sales –Cost of Sales = Rs 2,00,000 – Rs 1,53,500 = Rs 46,500

- Closing Stock = 500 × Rs 50 = Rs 25,000

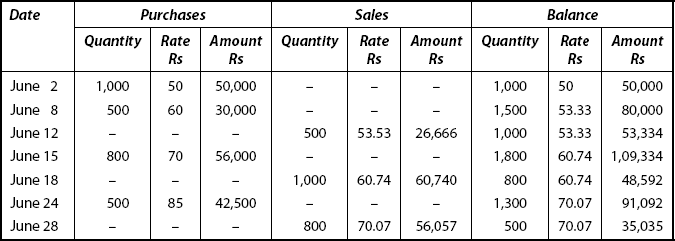

(c) Stock Ledger (WAP)

- Cost of Sales = Rs 26,666 + Rs 60,740 + Rs 56,057 = Rs 1,43,463

- Gross Profit = Sales –Cost of Sales = Rs 2,00,000 – Rs 1,43,463 = Rs 52,537

- Value of Closing Stock = Rs 35,035

OBJECTIVE 10: VALUATION OF INVENTORY AS ON THE BALANCE SHEET

In case the value of inventory is taken on a date other than the Balance Sheet date, some adjustments relating to Sales, Purchases, Returns – inwards and outwards are required to be made for the purpose of ascertaining the value of inventory as on the Balance Sheet.

The adjustment procedure differs depending on the date on which the computation of value of inventory takes place.

10.1 Method I

Computation of value of inventory, if an inventory is taken prior to the Balance Sheet (for example, inventory date is Mar 10 … and Balance Sheet is Mar 31 …).

| Rs | ||

|---|---|---|

Step 1: |

Value of Inventory as per books on … |

…… |

Step 2: |

Less: Cost of Goods Sold between two dates |

…… |

Step 3: |

Add: Cost of unsold goods lying with others |

…… |

Step 4: |

Add: Cost of goods purchased and Sales Returns |

…… |

Step 5: |

Less: Cost of unsold goods lying with us (received upto stock taking) |

…… |

Step 6: |

Value of Inventory as per books as on Mar 31 the date of Balance Sheet |

____ …… ____ |

10.2 Method II

Computation of Value of Inventory, if an inventory is taken after the Balance Sheet date (for example, inventory date is Apr 10 … and Balance Sheet date is Mar 31 …) .

Procedure: Just reverse the procedure discussed under Method I (i.e., Items that are all added will be deducted under this method – refer Step 3, Step 4) and items that are all deducted will be added (refer Step 2, Step 5).

Examples of unsold goods: Cost of goods relating to consignment basis, joint venture basis, approval basis, hire-purchase basis (goods sent [lying with others] or received [lying with us]).

Stock as per books may be different from the stock found as per physical verification. Such difference arises due to the following reasons:

- Goods purchased – recorded in the books but not yet received,

- Goods sold – recorded in the books but not yet delivered,

- Returns Inwards – not recorded in books but received,

- Returns Outwards – not recorded in books but delivered.

Methods of valuation differ here also:

Case (a): If the physical inventory is taken prior to the Balance Sheet date while computing the value of inventory:

|

|

Rs |

Step 1: |

Value of Physical Inventory as on (date prior to Balance Sheet date) |

…… |

Step 2: |

Add: Cost of Goods Purchased and Cost of Sales Returns |

…… |

Step 3: |

Less: Cost of Goods Sold and Cost of Purchase Returns |

…… |

Step 4: |

Result: Value of Inventory as on Balance Sheet date |

____ …… ____ |

Case (b): If the physical inventory is taken after the Balance Sheet date while computation of value of inventory:

Just reverse the procedure adopted in Case (a), i.e. the items added in the above procedure are to be deducted and the items deducted in the above method are to be added.

Note: To determine the value of stock at a given date, the above procedure has to be adopted.

Illustration: 7

Determine the value of stock as per books of Vas Ltd on Mar 31, 2009 from the following information:

- The cost of stock as per physical verification as on Mar 20, 2009 amounted to Rs 5,00,000.

- Purchases as per Purchase Book after stock taking till Mar 31, 2009 amounted to Rs 5,00,000 and included the following:

- Rs 20,000 for goods received till Mar 19

- Rs 40,000 for goods received on Apr 1

- Sales as per Sales Book after stock taking, till Mar 31, amounted to Rs 5,00,000 and include the following:

- Rs 20,000 for goods delivered till Mar 19

- Rs 40,000 for goods delivered on Apr 1

- Goods are sold by the trader at a profit of 25% on cost.

Solution

- Physical inventory is taken on Mar 19, i.e. prior to the date of Balance Sheet.

- So, necessary adjustments (addition/deduction) have to be made (as discussed already).

- Here, one more information is given in the question, i.e. goods are sold at a profit of 25% on COST. That is equal to 20% on sales.

Note: While computing the stock as per books, whether the goods are not received/delivered is immaterial. As such, so adjustments under this method. But while valuing the stock as per physical verification such items are not to be included but deducted.

|

|

Rs |

Step 1: |

Stock as per physical verification as on Mar 19, 2009 |

5,00,000 |

Step 2: |

Add: Cost of goods purchased between two dates |

|

|

Rs 5,00,000 − Rs 20,000 (received already) = Rs 4,80,000 |

4,80,000 9,80,000 |

Step 3: |

Less: Cost of goods sold between the dates 20% of (Rs 5,00,000 – Rs 20,000) 20/100 × 4,80,000 = Rs 96,000 = Rs 96,000 Rs 4,80,000 – Rs 96,000 = Rs 3,84000 |

3,84,000 |

|

Directly 80% (Rs 5,00,000 – Rs 20,000) 80/100 × 4,80,000 = 3,84,000 |

_______ |

Step 4: |

Stock as per books as on Mar 31, 2009 |

5,96,000 |

Illustration: 8

Calculate the cost of physical stock as on Mar 31, 2009 by using the figures in Illustration 7.

Solution

Note: While calculating the cost of physical stock, adjustments have to be made for goods not yet received or delivered. This is the main difference between these two methods

| Rs | ||

|---|---|---|

Step 1: |

Stock as per physical verification as on Mar 20, 2009 |

5,00,000 |

Step 2: |

Add: Cost of goods purchased between the dates |

|

|

[Rs 5,00,000 – Rs 20,000 (already received) – Rs 40,000 (not yet received)] |

4,40,000 |

Step 3: |

Less: Cost of goods sold |

9,40,000 |

|

[80% of (Rs 5,00,000 – Rs 20,000 – Rs 40,000)] |

3,52,000 |

Step 4: |

Cost of physical stock in hand as on Mar 31, 2009 |

5,88,000 |

Illustration: 9

Calculate the value of stock to be taken to Balance Sheet of PVR Ltd as on Mar 31, 2009 from the following information.

The stock was physically verified on Mar 21, 2009 and was valued at Rs 3,00,000. After stock taking, the following transactions took place till Mar 31.

- Purchases of Rs 1,60,000 out of which 25% of goods were returned

- Sales of Rs 1,60,000 out of which 20% of goods returned by customers

- Goods are sold at a profit of 25% on cost

Solution

Notes:

- 25% on COST = 20% on sales,

- Stock was verified prior to date of Balance Sheet, necessary adjustments have to be made as.

|

|

Rs |

Step 1: |

Stock as per physical verification as on Mar 21, 2009 |

3,00,000 |

Step 2: |

Add: Cost of goods purchased after stock taking till Mar |

|

|

Rs 1,60,000 – Rs 40,000 |

1,20,000 4,20,000 |

Step 3: |

Less: Cost of goods sold |

96,000 |

|

80% of (Rs 1,60,000 – 25% of 1,60,000 |

______ |

Step 4: |

Stock as per books at Mar 31, 2009 |

3,24,000 |

Illustration: 10

Calculate the value of stock to be taken to Balance Sheet of PVR Ltd as on Mar 31, 2009.

The stock was physically verified on Apr 9, 2009 and was valued at Rs 3,00,000. After Mar 31, the following transactions took place till the date of stock taking.

- Purchases of Rs 1,60,000 out of which 25% were returned.

- Sales of Rs 2,00,000 out of which 25% were returned by customers.

- Goods are sold by the trader at a profit of 25% on cost.

Solution

Particulars are shown after the date of Balance Sheet. So, the procedure here is to be reversed.

|

|

Rs |

Step 1: |

Stock as per physical verification as on Apr 9, 2009 |

3,00,000 |

Step 2: |

Less: Cost of goods purchased after Mar 31, 2009 till Apr 9, 2009 |

1,20,000 1,80,000 |

Step 3: |

Add: Cost of goods sold after Mar 31, 2009 to Apr 9, 2009 |

96,000 |

Step 4: |

Stock as per books as on Mar 31, 2009 |

2,76,000 |

Illustration: 11

The stock was physically verified on Mar 21, 2009 and was valued at Rs 5,00,000. Goods are sold by the trader at a profit of 25% on COST. After stock taking, the following transactions took place till Mar 31, 2009.

Sales of Rs 5,54,000 include

- Sales of Rs 27,000 @ 20% more than normal selling price.

- Sales of Rs 27,000 @ 10% less than normal selling price.

You are required to compute the value of stock to be taken to the Balance Sheet of RBS Ltd as on Mar 31, 2009.

Solution

- Physical inventory took place prior to the date of Balance Sheet.

- Here, an additional information to normal sales is shown in the problem. As such, abnormal sales value has to be calculated as:

Normal sales = (Rs 5,40,000 – Rs 27,000 – Rs 27,000) × 80%

∴ Profit = 25% on cost 25% on cost = 20% on sale 100 – 20 = 80% = Rs 5,00,000 × 80 = Rs 4,00,000 ∴ Abnormal loss.

Calculation 1

| (i) For sales of Rs 27,000 – 20% more than normal selling price. | ||

| Let normal selling price be Rs 100 | ||

| 20% more means | = | 100 + 20% |

| If abnormal sale is | 120 | |

| Normal sale | = | 100 |

| For Rs 27,000 | = | Rs 27,000 × 100/120 |

| = | Rs 22,500 | |

| 80% (of 22,500) | = | Rs 18,000 |

Calculation 2

| (ii) In the same way, for abnormal sales – 10% less than normal sale. | ||

| Rs 27,000 × 100/90 | = | Rs 30,000 |

| 80% (of Rs 30,000) | = | Rs 24,000 |

Now, transfer these values for calculation as follows:

|

|

Rs |

Step 1: |

Valuation of stock as on Mar 21, 2009 |

5,00,000 |

Step 2: |

Less: Cost of goods sold |

|

|

(i) Normal sales: |

|

|

80% of (Rs 5,54,000–Rs 27,000–Rs 27,000) |

4,00,000 |

|

(ii) Abnormal sales: |

|

|

(a) For 20% above normal selling price |

|

|

(refer calculation 1) |

18,000 |

|

(b) For 10% less than normal selling price |

|

|

(refer calculation 2) |

24,000 |

|

|

4,42,000 |

Step 3: |

Value of stock as on Mar 31, 2009 |

58,000 |

Illustration: 12

The stock was physically verified on Mar 24, 2009 and was valued at Rs 2,75,000. Goods are normally sold by the trader at a profit of 25% on cost.

You are required to compute the value of stock to be taken to the Balance Sheet of VRS Ltd as on Mar 31, 2009 in each of the following alternative cases:

Case (a): |

On Mar 21, goods of the sale value of Rs 50,000 were sent on sale or return basis to customer, the period of approval being two weeks. |

Case (b): |

On Mar 21, goods of the sale value of Rs 50,000 were sent on sale or return basis to a customer, the period of approval being two weeks. He returned 20% of the goods on Mar 31. |

Case (c): |

On Mar 21, goods of the sale value of Rs 50,000 were sent to on sale or return basis to a customer, the period of approval being two weeks. He approved 80% of the goods on Mar 31. |

Case (d): |

On Mar 21, goods of the sale value of Rs 50,000 were sent on sale or return basis to a customer, the period of approval being two weeks. He returned 20% of the goods and approved 80% of the remaining on Mar 31. |

Solution

Notes

- Goods were sent on approval basis, which means the customer may return or (retain) approve the goods on the agreed basis, usually in percentage.

- Option period is also provided.

- Students have to see whether the goods have been returned or retained by the customer as on the date of balance sheet.

- Generally, goods lying with the customers cannot be treated as sold.

- Note the date –the most important feature –in the computation of stock as on (Mar 21) –the Balance Sheet date – whether it is prior to the date of physical verification of stock or after the date of physical verification. Accordingly, adjustments (addition/deduction) have to be made.

- Statement showing the valuation of stock as on Mar 31, 2009.

Case (a): Statement Showing the Valuation of Stock as on Mar 31, 2009

|

|

Rs |

1. |

2,75,000 |

|

2. |

Add: Cost of goods sent on approval and still with customer Sales – Gross Profit (20% on sale) |

|

|

Rs 50,000 – 20% (Rs 50,000 – Rs 10,000) |

40,000

|

3. |

Value as on Mar 31, 2009 |

3,15,000 |

Case (b)

1. |

Value of stock as on Mar 24, |

2,75,000 |

2. |

Add: Cost of goods sent on approval |

Received back 20% (20% of 50,000 – 20% of Rs 10,000) |

8,000 |

Case (c): Statement Showing the Valuation of Cost as on Mar 31, 2009

|

|

Rs |

1. |

Value of stock as on Mar 24, 2009 |

2,75,000 |

2. |

(a) Cost of goods sent on approval and received back |

|

|

(20% of Rs 50,000 – 20% of Rs 10,000) |

8,000 |

|

(b) Cost of good sent on approval and still with customer |

|

|

(20% of 80% of Rs 50,000 – 20% of Rs 8,000) |

6,400 |

|

|

2,89,400 |

Illustration: 13

The stock was physically verified on Mar 24, 2009 and was valued at Rs 5,00,000. Goods are normally sold by the trader at a profit of 25% on cost.

You are required to compute the value of stock to be taken to Balance Sheet of VRV Ltd as on Mar 31, 2009 in each of the following alternative cases.

Case (a): |

On Mar 28, goods of sale value of Rs 2,00,000 were sent on sale or return basis to a customer, the period of approval being two weeks. |

Case (b): |

On Mar 28, goods of the sale value of Rs 2,00,000 were sent on sale or return basis to a customer, the period of approval being two weeks. He returned 20% of goods on Mar 31. |

Case (c): |

On Mar 28, goods of the sale value of Rs 2,00,000 were sent on sale or return basis to a customer, the period of approval being two weeks. He returned 20% of the goods and approved the remaining on Mar 31. |

Case (d): |

On Mar 28, goods of the sale value of Rs 2,00,000 were sent on sale or return basis to a customer, the period of approval being two weeks. He returned 20% of goods and approved 80% of the remaining on Mar 31. |

Solution

Note: Date of physical verification of stock is Mar 24, and transaction date is Mar 28, i.e. after the date of verification. So, the procedure has to be reversed.

|

|

Rs |

1. |

Value of stock as on Mar 24, 2009 |

5,00,000 |

2. |

Less: Cost of goods sent on approval which was approved |

|

|

Rs 1,60,000 – Rs 32,000 |

1,28,000 |

3. |

Value of stock as on Mar 31, 2009 |

3,72,000 |

Note: Approval item – Amount deducted

Case (d): Statement Showing the Valuation of Stock as on Mar 31, 2009

|

|

Rs |

1. |

Value of stock as on Mar 24 |

5,00,000 |

2. |

Less: Cost of goods sent on approval which was approved |

1,02,400 |

3. |

Value of stock as on Mar 31, 2009 |

3,98,600 |

Illustration: 14

The stock was physically verified on Apr 9, 2009 and was valued at Rs 3,20,000. Goods are normally sold by the trader at a profit of 25% on cost.

You are required to compute the value of stock to be taken to the Balance Sheet of Vasant Ltd as on Mar 31, 2009 in each of the following alternative cases.

Case (a): |

On Mar 29, goods of the sale value of Rs 50,000 were sent on sale or return basis to a customer, the period of approval being two weeks. |

Case (b): |

On Mar 29, goods of the sale value of Rs 50,000 were sent on sale or return basis to a customer, the period of approval being two weeks. He returned 20% of the goods on Apr 8, 2009. |

Case (c): |

On Mar 29, goods of the sale value of Rs 50,000 were sent on sale or return basis to a customer, the period of approval being two weeks. He approved 80% of the goods on Apr 8. |

Case (d): |

On Mar 29, goods of the sale value of Rs 50,000 were sent on sale or return basis to a customer, the period of approval being two weeks. He returned 20% of the goods and approved the remaining on Apr 8. |

Case (e): |

On Mar 29, goods of the sale value of Rs 50,000 were sent on sale or return basis to a customer, the period of approval being two weeks. He returned 20% of goods and approved 80% of the remaining on Apr 8. |

Solution

Note 1: Date of physical verification of stock is Apr 9, 2009 and the date of transactions are on Mar 29, i.e. prior to stock verification.

Note 2: Goods are sent on approval basis. Considering these two factors, the computation is made as:

Case (a): Statement Showing the Valuation of Stock as on Mar 31, 2009

|

|

Rs |

1. |

Value of stock as on Apr 9, 2009 |

3,20,000 |

2. |

Add: Cost of goods sent on approval are still with customers (Rs 50,000 – 20% of Rs 50,000) |

40,000 |

3. |

Value of stock as on Mar 31, 2009 |

36,000 |

Case (b): |

1. |

Value of stock as on Apr 9 |

3,20,000 |

|

2. |

Add: Cost of goods sent still with customer |

32,000 |

|

3. |

Value of stock as on Mar 31, 2009 |

3,52,000 |

Case (c): For case (c), the treatment is same and the value of stock is Rs 3,60,000.

Cases (d) and (e): Treatment is same. Hence, the value of stock is Rs 3,52,000.

Illustration: 15

The Profit and Loss of Account of Renu for the year ended on Dec 31, 2008 showed a net profit of Rs 3,360 after taking into account the physical closing stock of Rs 5,664. On a scrutiny of the books, the information was extracted and furnished as:

- Renu took goods valued Rs 1,800 for her personal use without making entry in the books.

- Purchases of the year included Rs 720 spent on purchase of a fan for her shop.

- Invoices for goods amounting to Rs 4800 have been entered on Dec 20, but such goods were not included in stock.

- Rs 600 was included in closing stock in respect of goods purchased and invoiced on Dec 18, but included in purchases of Jan.

- Sales of goods amounting to Rs 732 and delivered in Dec had been entered in Jan sales.

You are required to compute the value of closing stock as on Dec 31, 2008 and adjusted net profit for the year ended on that date.

[C.A (Inter) – Modified]

Solution

Note

- Value of closing stock is shown in the problem. But it has to be adjusted.

- Further, profit is given and after making adjustments, correct Net Profit has to be computed by preparing Profit and Loss (Adjustment) Account.

- Except Transaction 3, all the others need not be taken into account, while computing the value of stock as on Dec 31, 2008.

(a) Statement Showing the Valuation of Stock as on Dec 31, 2008

|

|

Rs |

1. |

Stock (given already in the problem) |

5,664 |

2. |

Add: Purchases (Invoice: entered but goods not included in stock) |

4,800 |

3. |

Value of stock as on Dec 31, 2008. |

10,464 |

Note: Students should once again refer to the procedure already described and the transactions given in this problem and how they are treated here.

(b) Profit and Loss (Adjustment) Account

|

i. |

Items not related to goods – item ii – a fan for the office is credited to this a/c, |

|

ii. |

Items not related – personal use – item (ii) is credited to this account, |

|

iii. |

Goods in transit and items relating to next period (after the date of Balance Sheet) are credited or debited depending on the nature of items, |

|

*iv. |

Net Profit (adjusted) is the balancing figure, |

|

*v. |

Items iv and v are to be cancelled. |

Illustration: 16

A firm could do physical stock taking on Jan 9, 2009. The accounts of the firm are closed on Dec 31, every year. The stock on Jan 7, 2009, as disclosed by the store-keeper was valued at Rs 91,500. You are required to compute the value of stock as on Dec 31, 2008 taking into consideration the following:

- Purchases from Jan 1, 2009 to Jan 7, 2009 as per invoice book amounted to Rs 17,800. On a careful analysis it was found that a fan purchased for Rs 1,600 was passed through invoice book; purchase book was carried forward Rs 20 less on page 15, and purchase of Rs 2,400 duly recorded in the book is still in transit.

- Goods of Rs 2,700 received on consignment were lying in the store room and were included in stock taking.

- Sales from Jan 1, to Jan 7, 2009 amounted to Rs 20,800. This, however, included the following:

- Goods sent on consignment Rs 2,000, at invoice price is made of cost + 25%.

- Goods sent to branch at invoice price of Rs 840. Invoice price is made at a profit of 1/6th of sale.

- Goods sold at Rs 1,600, loss being 20% on cost.

Sales in the business are made at a profit of 1/3rd of cost.

You are required to prepare a statement showing the actual value of stock as on Dec 31, 2008.

[B.Com (Hons.) – Calcutta University, Adapted and Modified]

Solution

In this problem, total purchases and total sales are shown. In addition, some transactions relating to these items are given. In such a situation, Analysis of Purchases and Analysis of Sales are calculated as shown below:

Step 1: Analysis of Purchases

Rs |

||

|

Total purchases |

17,800 |

|

Less: Purchase of a fan |

1,600 |

|

|

16,200 |

|

20 |

|

|

|

16,220 |

|

Less: Goods in transit |

2,400 |

|

|

13,820 |

Step 2: Cost price for each type (on sale) is calculated by analysing transactions relating to sale

|

|

Rs |

1. |

Goods sent on consignment |

2,000 |

|

Profit margin: 20% on sale (therefore it is given as cost + 25%) |

|

|

20% of Rs 2,000 – Profit |

400 |

|

Cost price |

1,600 |

2. |

Goods sent to branch (invoice price) |

840 |

|

Profit margin 1/6 of sale (given) |

|

|

1/6th × 840 = Profit 140 |

140 |

|

Cost price |

700 |

3. |

Abnormal sale |

1,600 |

|

Loss margin 20% on cost = 25% on sale |

|

|

Loss = 1/4 th × Rs 1,600 |

400 |

|

Cost price |

2,000 |

4. |

Normal sale |

16,360 |

|

Profit margin (1/3rd of Cost (given) = 1/4 of sale) |

|

|

Profit: (1/4 × Rs 16,360) |

4,090 |

|

Cost price |

12,270 |

*Total cost price = (1 + 2 + 3 + 4) |

|

|

|

= Rs 1,600 + 700 + 2,000 + 12,270 = Rs 16,570 |

|

Step 3: Statement Showing the Value of Stock as on Dec 31, 2008

Rs |

||

1. |

Stock as on Jan 7, 2009 |

91,500 |

2. |

Less: Stock on consignment |

(2,700) |

|

|

88,880 |

3. |

Less: Goods received between the date of balance sheet and stock taken, i.e. from 31.12.2008 to 7.1.2009 |

13,820 |

|

|

74,980 |

4. |

*Add cost of goods sold (refer Step 2) |

16,570 |

5. |

Closing Stock as on Dec 31, 2008 |

91,550 |

|

Actual value of stock as on Dec 31, 2008 |

91,550 |

Illustration: 17

The financial year of Bhagya ends on Dec 31, 2009, but the stock in hand was physically verified only on Apr 9, 2009.

You are required to calculate the value of Closing Stock at cost as on Mar 31, 2009 from the following information:

- The stock at cost as verified on Apr 9, 2009 was Rs 30,000.

- Sales have been entered in the sales day book only after the despatch of goods and sales return only on receipt of goods.

- Purchases have been entered in the purchases day book only on receipt of the purchase invoice irrespective of the date of receipt of goods.

- Sales as per sales day book for the period from Apr 1 to Apr 9, 2009 (before actual verification) amounted to Rs 12,000 of which goods of the value of Rs 2,000 had not been delivered at the time of verification.

- Purchases as per the purchases day book for the period from Apr 1 to 9, Apr 2009 (before the actual verification) amounted to Rs 12,000 of which goods for purchases of Rs 3,000 had not been received at the date of verification and goods for purchases Rs 10,000 has been received prior to Mar 31, 2009.

- In respect of goods costing of Rs 10,000 received prior to Mar 31, 2009, invoices had not been received upto date of verification of stocks.

- Gross profit is 20% on sales.

[B.Com (Hons.) – Calcutta University, Modified]

Solution

|

|

|

Rs |

|

1. |

Stock on Apr 9, 2009 |

30,000 |

|

2. |

Sales (adjustments made) |

|

|

|

Rs |

|

Add: |

|

|

|

|

(i) Sales from 1.4.2009 to 9.4.2009 |

12,000 |

|

|

(ii) Less: Goods not delivered |

|

|

|

(not included in stock – refer item “d”) |

(2,000) |

|

|

|

10,000 |

|

|

(iii) Less: Gross Profi t (20% on 10,000) |

(2,000) |

|

|

|

8,000 |

|

|

Amount to be added to stock |

|

8,000 |

|

|

|

38,000 |

3. Purchases (adjustments made)

Less: |

|

|

|

|

(i) Purchases from 1.4.09 to 9.4.2009 |

12,000 |

|

|

(ii) Less: Goods not received till date (item: e) |

(3,000) |

|

|

|

(9,000) |

|

|

(iii) Less: Goods received prior to date of Balance Sheet |

|

|

|

(no invoice received) (item: f) |

(10,000) |

|

|

|

(19,000) |

|

|

Amount to be deducted from stock |

|

(19,000) |

4. Stock as on Mar 31, 2009 |

|

19,000 |

|

Value of Closing Stock (at cost) as on Mar 31, 2009 = Rs 19,000

OBJECTIVE 11: ACCOUNTING STANDARD-2 (REVISED)

Salient Features (or) Important Provisions: Accounting Standards issued by the Institute of Chartered Accountants of India would bring Indian accounting practises at par with international accounting practises. This AS–2 (Revised) is issued relating to item of inventories and net realisable value. It is mandatory.

Inventory valuation: Acceptable basis for inventory valuation is

- Cost

or

- Net realisable value

whichever is less.

Cost: It dispenses the use of direct costing method. It recommends the use of standard cost and retail method of inventory valuation.

The cost includes:

- all costs of purchase,

- costs of conversion,

- other costs incurred to bring the inventories to their present location and condition.

The cost does not include:

- interest and other borrowing costs,

- abnormal amounts of wasted materials, labour or other production costs,

- storage costs,

- administrative overheads which do not contribute to bringing the inventories to their present location and condition,

- selling and distribution costs.

Net Realisable Value = Estimated selling price – (Estimated costs of completion + Estimated costs to make the sale)

Cost Formulae: This standard envisages that the formula used should be the fairest possible approximation to cost (incurred in bringing the items of inventory to their present level and condition). AS–2 (Revised) emphasises the following formulae to determine the cost.

- Specific Identification Cost.

- FIFO.

- WAC.

- AS–2 Revised cost does not permit the use of LIFO basis for determining the cost.

Net realisable value: For inventories in case:

- They are damaged.

- They have become obsolete (partial or full).

- The price is declined.

Net realisable value method has to be applied. Estimates must be based on the most reliable evidence at the time of estimate and they should not be marked below cost.

Disclosure: AS–2 (Revised) stipulates that the financial statements should disclose:

- The accounting policies adopted in valuing inventories,

- The cost formula used,

- The total carrying amount of inventories,

- Classification of inventories such as raw materials, work-in progress, finished goods and the like.

Not applicable:

This standard is not applicable for the following:

- Work-in-progress arising under construction contracts as AS–7 sets provisions for construction contracts,

- Work-in-progress in the business of service providers,

- Shares, debentures etc., held as stock-in-trade,

- Producers’ inventories of live-stock, agriculture and forest products,

- Natural resources – mineral ores, oil wells, gases, quarries.

Summary

- Inventory means an exhaustive list of assets – goods that a company is holding from the stage of purchase till the stage they are sold off.

- Inventories vary according to the nature of the business – trading concern, manufacturing concern.

- Significance: “Inventory” is a major asset to assess the liquidity of entity, to determine true income and to ascertain true financial position.

- Inventory records systems – Periodic Inventory System is a method to ascertain inventory by taking actual physical count at a particular date and Perpetual Inventory System is a method of recording inventory balances after each purchase and sales takes place.

- Valuation of inventories: As per AS–2 (Revised), inventories should be valued at the lower of the cost and net realisable value.

- Cost of inventories comprises of cost of purchase, cost of conversion and other costs incurred in bringing the inventories to their present location and condition.

- Cost formulae: 1. Specific identification of costs, means that specific costs are attributed to identified items of inventory. Two steps, (i) to keep track of the purchase price of each specific unit and (ii) to know which specific units were sold. 2. FIFO Method – under this method, stock ledger is prepared as the units which are received first, will be sold first. Flow of costs is presumed to be the same as flow of goods. 3. LIFO Method – under this method, goods which are purchased last are sold first. 4. Weighted Average Method – this method is based on the assumption that each sale of goods consists of a due proportion of the earlier lots and such a sale is valued at Weighted Average Price.

- Weighted Average Price

[whereas Total Cost = Quantity × Cost per Unit]

- Choice of inventory valuation methods: Choice of a method depends on the price level changes, stock turnover company’s policy on profit and accounting policy and procedure.

- Valuation of inventory as on the Balance Sheet: To ascertain the valuation of inventory as on the Balance Sheet, adjustments have to be made on Purchases and Sales Returns – computation of valuation of inventory prior to and after the Balance Sheet refer to Illustration Nos. 7, 8, 9, 10, 11, 12, 13, 14, 15, 16 and 17.

- Salient features of AS–2 (Revised) – Refer the text.

Key Terms

Accounting Standard: AS–2: It is issued by ICAI. It mainly deals with “Inventories.”

Cost Formulae: AS–2 has stipulated certain ground rules and methods for valuation of inventories. The methods of inventory valuation recommended by ICAI are termed as cost formulas.

Cost of Goods Sold: It mainly includes cost of materials, labour and factory overheads but excludes selling and distribution expenses.

FIFO Method: This is a method of inventory valuation where computation of cost of items sold or consumed in the order of their acquisition. Goods purchased first are sold first.

Inventories: Assets held (i) for sale in the ordinary course of business (ii) in the process of production for such sale or (iii) in the form of materials or supplies to be consumed in the production process or in the rendering of services are inventories.

LIFO Method: This is another method of inventory valuation, whereby goods purchased last are issued first. Goods purchased last are sold first.

Periodic Inventory System: A system of determining the physical quantities and rupee value of inventories sold and in hand. It is done at a time whenever inventory information is needed. It is also called system of records.

Perpetual Inventory System: Another system of determining physical quantities and rupee value of inventories whereby continuous recording each purchase or sale transaction. It is also described as a system of records.

Weighted Average Method: Under this method, no particular flow of goods (either first or last) is recognised. Costs are to be assigned to cost of goods sold as well as goods in hand. The weighted average unit is calculated by dividing the total cost of similar units in a period by the related number of units.

References

Bhabatosh Banerjee, Cost Accounting, The World Press Pvt. Ltd., Calcutta, 1978.

Charles T. Horngreen, Srikant M. Datar, and George Foster, Cost Accounting – A Managerial Emphasis, Pearson Education, New Delhi, 2008.

Mansh Dutta, Cost Accounting, Pearson Education, New Delhi, 2005.

A Objective-type Questions

I. State whether the following statements are True or False

- Inventories consist of goods purchased and held for resale.

- Inventories include machinery spares.

- For inventory valuation, cost may mean historical.

- Abnormal amounts of wasted materials, labour or other production costs are included in the cost of inventories.

- Selling and distribution costs are excluded from the cost of inventories.

- Periodic Inventory System is a method of ascertaining inventory by taking an actual physical count.

- The Closing Inventory is calculated as a residual figure under Perpetual Inventory System.

- The Cost of Goods Sold is calculated as a residual figure under Perpetual Inventory System.

- Perpetual Inventory System is a method of ascertaining inventory on the basis of records.

- 10. The method of valuation (FIFO, LIFO, etc) is applied only once at the end of the accounting period under Periodic Inventory System to ascertain the cost of Closing Inventory.

- The AS–2 (Revised) is mandatory in nature.

- The FIFO Method is based on the assumption that the goods which are received recently are issued first.

- The FIFO Method is in conformity with the physical flow of goods.

- The LIFO Method is based on the assumption that the goods which are received first are issued first.

- The LIFO Method does not conform to the physical flow of goods.

- The Specific Identification Method is used specially for the goods produced and segregated for specific projects.

- Net realisable value is the actual cost of selling price without any adjustments.

- The inventory of finished goods is valued at cost or net realisable value whichever is lower.

- The inventory of materials and other suppliers is valued at cost if the finished goods are expected to be sold below the historical cost.

- Inventory of non-realisable waste should be valued at cost or net realisable value whichever is higher.

Answers

1. True |

2. False |

3. True |

4. False |

5. True |

6. True |

7. False |

8. False |

9. True |

10. True |

11. True |

12. False |

13. True |

14. False |

15. True |

16. True |

17. False |

18. True |

19. False |

20. False |

II Fill in the blanks with suitable words

- Inventories are only __________.

- For inventory valuation, cost may mean historical, current or __________.

- Historical cost represents the cost actually incurred at the date of __________.

- Current replacement cost represents the replacement price on the date of __________.

- Standard cost represents the __________ cost.

- Storage costs are __________ while determining cost of inventories.

- Opening Inventory + Purchases – Closing Inventory = __________.

- Opening Inventory + Purchases – Cost of Goods Sold = __________.

- Under Periodic System, inventory is ascertained by taking an actual __________.

- Under Perpetual Inventory System, inventory is ascertained on the basis of __________.

- Cost of goods sold includes cost of __________ goods, if any.

- Under Perpetual Inventory System, the method of valuation is applied __________ during an accounting period to ascertain the Cost of Goods Sold.

- Under Periodic Inventory System, the method of valuation is applied __________ at the end of the accounting period to ascertain the cost of Closing Stock.

- The residual factor under Periodic Inventory System is __________.

- The residual factor under Perpetual Inventory System is __________.

- Under FIFO Method, the goods which are received __________ are to be issued first.

- Under LIFO, the goods which are received __________ are to be issued first.

- Weighted Average Price Method is used in __________ industries, advantageously.

- Goods are sold at a profit of 25% on cost is equal to __________ % on sales.

- All inventories should be valued at __________ of historical cost or net realisable value subject to certain conditions.

Answers

- Assets

- Standard Cost

- Acquisition

- Consumption

- Predetermined

- Excluded

- Cost of Goods Sold

- Closing Inventory

- Physical count

- Records

- Lost

- Continuous

- Only once

- Cost of Goods Sold

- Closing Inventory

- First

- Last

- Process

- 20%

- Lower

B Short Answer-type Questions

- What do you mean by “inventories”?

- Explain the significance of valuation of inventory.

- What are the components of historical cost?

- Explain: “cost of purchase.”

- Explain: “cost of conversion.”

- What do you mean by “other costs”?

- Mention the items that are excluded from the cost of inventories.

- Mention the types of inventory systems.

- What is meant by Periodic Inventory System?

- Explain: Perpetual Inventory System.

- What are the methods of valuation of inventories recognised by AS–2 (Revised)?

- What is FIFO Method?

- Mention any four advantages of FIFO Method?

- Mention any four limitations of FIFO Method?

- In case of rising prices, what will be the implication of the use of FIFO Method?

- What is LIFO Method?

- Mention any four advantages of this method.

- Mention any four disadvantages of LIFO Method.

- What is Weighted Average Price Method?

- What are the merits of the Weighted Average Price Method?

- What are the disadvantages of the Weighted Average Price Method?

- What do you mean by Specific Identification Method?

- What do you mean by Standard Cost Method?

- What are the advantages of Standard Cost Method?

- What are the reasons for the difference for the value of stock as per books and as per physical verification?

- What is Net Realisable Value?

- Mention the disclosure requirements (relating to inventories in financial statements according to AS–2 – Revised.

- How should the inventory of consumable stores be valued?

- How should inventory of reusable waste be valued?

- How should the inventory of non-reusable waste be valued?

C Essay-type Questions

- Explain the term “inventories.” Discuss the meaning of “cost of inventory valuation” with suitable illustrations.

- Explain the inventory systems – distinguish between Periodic Inventory System and Perpetual Inventory System.

- Explain the procedure to be followed in inventory valuation under FIFO and Weighted Average Price methods.

- While computing the value of inventory in case:

- If an inventory is taken on a date after the Balance Sheet date.

- If an inventory is taken on a date prior to the date of the Balance Sheet, explain the adjustments to be carried out with illustration.

D Exercises

Model: Perpetual System (Q.1 to Q.7)

1. Calculate by FIFO Method of inventory valuation, the Cost of Goods Sold and value of Ending Inventory from the following data:

Answer: Cost of Goods Sold: Rs 1,46,400; Cost of Ending Inventory: Rs 7,500

2. From the following particulars for the months of Dec 2009, find out the cost of inventory on Dec 31, 2009 under Perpetual Inventory System using FIFO Method of pricing issue of materials:

[C.S. (Foundation) – Modified]

Answer: Cost of inventory on 31.12.2009 is Rs 3,71,400

3. A trader has the following transactions in a certain product in the month of May 2009. Calculate the Cost of Goods Sold and the Closing Inventory using FIFO, LIFO and WAP methods.

Cost of Goods Sold: FIFO = Rs 2,430; LIFO = Rs 2,536; WAP = Rs 2,460

Cost of Closing Inventory: FIFO = Rs 1,030; LIFO = Rs 924; WAP = Rs 1,000

4. A trader has the following transactions in a certain product for three months from Feb 2009:

| Date | Transaction | |

|---|---|---|

Feb 3 |

Purchases |

300 items at Rs 20 each |

Feb 20 |

Purchases |

100 items at Rs 24 each |

Mar 1 |

Sells |

100 items at Rs 30 each |

Mar 20 |

Purchases |

150 items at Rs 30 each |

Mar 30 |

Sells |

200 items at Rs 40 each |

Apr 2 |

Purchases |

150 items at Rs 40 each |

Apr 15 |

Sells |

175 items at Rs 50 each |

Required

- Compute the Gross Profit earned during the period,

- Compute the value of the Closing Stock at Apr 30, 2009 using each of the following alternative bases of 2009 valuation: (a) FIFO, (b) LIFO, (c) WAP methods.

Answer

5. With the help of the following particulars, prepare Stores Account, showing issue of materials on the basis of LIFO Method:

|

Purchases |

|

|

June 1 |

(250 kg @ Rs 2.00 per kg) |

|

June 8 |

(175 kg @ Rs 2.10 per kg) |

|

June 18 |

(300 kg @ Rs 2.20 per kg) |

|

June 25 |

(250 kg @ Rs 2.30 per kg) |

|

Issues |

|

|

June 9 |

(300 kg on requisition No. 1) |

|

June 19 |

(225 kg on requisition No. 2) |

|

June 28 |

(255 kg on requisition No. 3) |

|

June 30 |

(75 kg on requisition No. 4) |

|

Assume that there was no opening stock |

|

[C.S. (Foundation) – Modified]

Answer: Balance 120 kg @ Rs 2 = Rs 240

6. From the following data compute the Cost of Goods Sold and Closing Inventory under FIFO, LIFO and WAC methods of inventory valuation:

Nov 1: Stock in hand 250 units @ Rs9 each

|

Purchases |

|

|

Nov 2 |

(250 units @ Rs 11 each) |

|

Nov 9 |

(500 units @ Rs 12 each) |

|

(300 units @ Rs 10 each) |

|

|

Nov 22 |

(250 units @ Rs 12 each) |

|

Nov 29 |

(200 units @ Rs 13 each) |

|

Issues |

|

|

Nov 4 |

(200 units) |

|

Nov 7 |

(250 units) |

|

Nov 15 |

(450 units) |

|

Nov 20 |

(250 units) |

|

Nov 30 |

(300 units) |

Answer

7. Green Ltd was following LIFO Method of valuation of stock. Due to promulgation of revised accounting standard they want to switch over to FIFO Method. From the following

- Draw up stock ledgers under FIFO and LIFO Methods of valuation of stocks,

- Find out the Closing Stock and cost of materials consumed under each of the above two methods.

Opening Stock 2,500 metric tonnes @ Rs 22 per MT = Rs 55,000

|

Purchases |

|

|

1.9.2009 |

(500 MT @ Rs 30 per MT) |

|

6.9.2009 |

(1,000 MT @ Rs 35 per MT) |

|

10.9.2009 |

(750 MT @ Rs 38 per MT) |

|

16.9.2009 |

(750 MT @ Rs 35 per MT) |

|

21.9.2009 |

(1,000 MT @ Rs 32 per MT) |

|

27.9.2009 |

(1,000 MT @ Rs 35 per MT) |

|

30.9.2009 |

(750 MT @ Rs 30 per MT) |

|

Issues |

|

|

1.9 to 6.9.2009 |

(1,000 MT) |

|

7.9 to 10.9.2009 |

(1,500 MT) |

|

11.9 to 21.9.2009 |

(2,000 MT) |

|

22.9 to 26.9.2009 |

(1,500 MT) |

|

27.9 to 30.9.2009 |

(1,500 MT) |

[C.A. (Foundation) – Modified]

Answer:

| FIFO Rs | LIFO Rs | |

|---|---|---|

| (1) Value of Closing Stock | 750 MT @ Rs 30 = Rs 22,500 | (i) 250 MT @ Rs 35 = Rs 19,750 |