chapter 4

ETC FX Concepts

LEARNING OBJECTIVES

This chapter aims to provide readers with an in-depth knowledge on ETC markets with major emphasis on currency futures which have been recently launched in India, and are traded on various exchanges, viz., NSE, MCX and USE. ETC refers to ‘exchange traded contracts’ whereby each counterparty deals with exchange. Exchange acts as an intermediary and guarantees the settlement and performance of obligations by counterparties. The contents of this chapter are organized in the following order:

1. Currency Futures: Introduction

2. Market Participants in Currency Futures Segment

3. Currency Futures: Technical Aspects

4. Concept of Margin in ETC Markets

5. Advantages of Currency Futures Market

6. NSE and Thomson Reuters Screenshots

7. Summary Statement and Ledger Formats

8. Difference Between ETC and OTC

INTRODUCTION

- OTC market: OTC is an abbreviation for ‘over-the-counter’. It has no central market place and is linked to a network of dealers/traders who do not physically meet but instead communicate through a network of phones and computers. OTC contracts are typically customized based on negotiations between counter parties. The counter party default risk depends on the counterparty credit worthiness and other factors. The forwards which were discussed in the previous chapters are traded in OTC market.

- ETC market: ETC is an abbreviation for ‘exchange traded contracts’. The ETCs as compared to OTC forwards, serve the same economic purpose yet differ in fundamental ways. ETCs are standardized. In an exchange traded scenario, where the market lot is fixed at a much smaller in size than the OTC market, equitable opportunity is provided to all classes of investors, whether large or small, to participate in futures market. The other advantages of ETCs include greater transparency, efficiency and accessibility.

CURRENCY FUTURES: INTRODUCTION

A currency futures contract is a standardized version of a forward contract which is traded on a regulated exchange. It is an agreement to buy or sell a specified quantity of an underlying currency on a specified date in future at a specified rate (e.g. USD 1 = INR 44.00) (Note: USD is abbreviation for US dollar and INR for Indian rupees). The counter-party risk (credit risk) in a futures contract is eliminated by the presence of clearing house/corporation, which guarantees all settlements, and thus eliminates the default risk.

Thus, introduction of ETC futures has helped in overall development of foreign exchange market in the country. Any ‘Resident Indian’ or company, including banks and financial institutions, can participate in futures market. However, at present, foreign institutional investors (FIIs) and non-resident Indians (NRIs) are not permitted to participate in currency futures market.

RBI has allowed banks to participate in currency futures market. AD category I banks which fulfil stipulated prudential requirements are eligible to become a clearing member and/or trading member of currency derivatives segment of various exchanges. All other banks including urban and state co-operative banks can participate in currency futures market only as clients.

Currency futures can also help small traders as the minimum size of USD/INR futures contract is USD 1,000. This is within the reach of small traders. All transactions on the exchange are anonymous and executed on a price-time priority ensuring that best price is available to all categories of market participants irrespective of their size. Also since the profits or losses in the futures market are collected or paid on a daily basis, the scope of accumulation of losses for participants gets limited.

An individual with no exposure to foreign exchange risks can invest purely as an investor and benefit from exchange rate fluctuations just as one benefits by investing in equities market on exchange. However, like stock market, currency futures exchange is also risky and one can incur loss, in case the view taken goes wrong.

Exchange traded currency futures also enables hedging against currency risks. On a currency exchange platform, one can buy or sell currency futures. An importer can buy futures to ‘lock in’ a price for purchase of actual foreign currency at a future date, and similarly, an exporter can sell currency futures on the exchange platform and lock in price for sales of foreign exchange at a future date.

Risks in currency futures pertain to movements in the currency exchange rate. There is no rule of thumb to determine whether a currency rate will rise or fall or remain unchanged. A judgement on this aspect is a domain of experts with deep knowledge and understanding of variables that affect currency rates.

Internationally, exchanges such as Chicago Mercantile Exchange (CME), Johannesburg Stock Exchange (JSE), Euronext, Liffe, and Tokyo Financial Exchange (TFX), trade in currency futures.

MARKET PARTICIPANTS IN CURRENCY FUTURES SEGMENT

Hedgers

This includes large, medium and SME enterprises which wish to hedge their export- or import-related foreign exchange exposures.

Investors

This includes those who do not have any underlying currency exposure but they seek to profit from these markets by taking directional or volatility views.

Arbitrageurs

This includes those who want to benefit from price differentials between OTC and futures market.

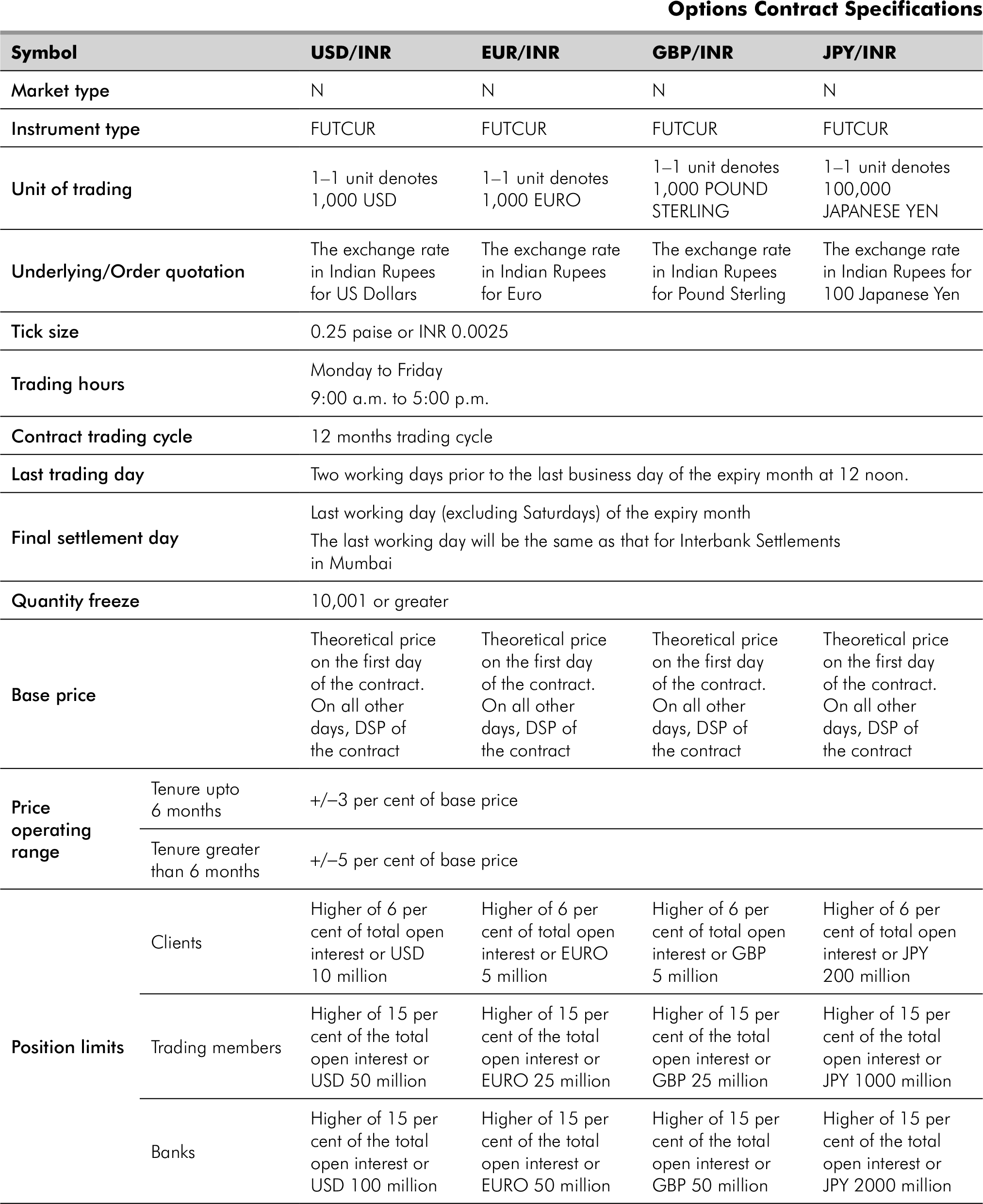

CURRENCY FUTURES: TECHNICAL ASPECTS

- All trades on MCX-SX or NSE take place on electronic trading platform and can be accessed with Internet connection.

- To buy/sell future contracts, clients have to participate only through a trading member. Clients have to open a trading account by submitting required documents and depositing stipulated margin.

- The counterparty has to be the exchange always. Hence, there would be no possibility of default.

- Contracts can be squared-off anytime during the exchange’s working hours and during the life of the contract; squaring-off can be done by entering into an opposite trade position in the same underlying contract before its maturity.

- All contracts which are open on maturity will be settled in Indian rupees in cash at the reference rate specified by RBI.

- After Market Orders (AMO) can be placed by the client after market hours. The trades will get executed when the exchange opens. These AMOs can be modified by the client till market opens.

- The minimum contract size of USD/INR futures contract is USD 1,000.

- The contract shall have a maximum maturity of 12 months. All monthly maturities ranging from one to 12 months are available.

- The settlement price is the reserve bank’s reference rate on the last trading day. Currency in which USD/INR contracts are settled is Indian rupees.

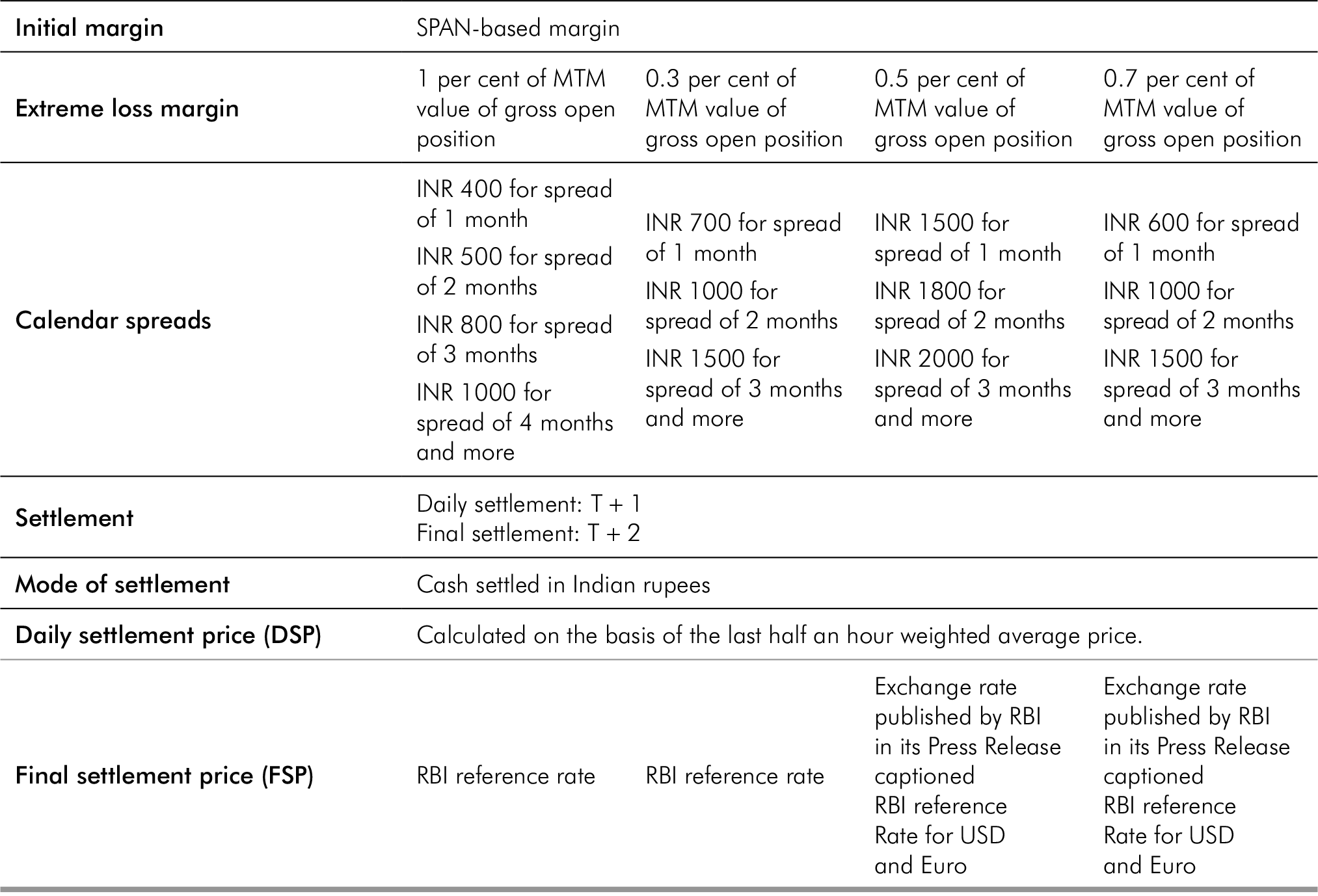

- Trading of currency futures is subject to maintenance of initial, extreme loss and calendar spread margin with the clearing house corporation. The initial margin is subject to a minimum of 1.75 per cent on the first day of currency futures and 1 per cent thereafter. The margins shall be deducted from the liquid net worth of the clearing member on an online and real-time basis. The amount that must be deposited in the margin account at the time a futures contract is first entered into is known as initial margin. In the futures market, at the end of each trading day, the margin account is adjusted to reflect the investor’s gain or loss depending upon the futures closing price. This is called marking-to-market.

- Trading in the currency futures takes place on all working days from Monday to Friday between 9 a.m. to 5 p.m.

- Tick values differ for different currency pairs and different underlying. For example, in the case of the USD/INR currency futures contract the tick size shall be 0.25 paisa or INR 0.0025.

- The last business day of the month will be termed the value date/final settlement date of each contract. The last business day would be taken to the same as that for interbank settlements in Mumbai. The rules for interbank settlements, including those for ‘known holidays’ and ‘subsequently declared holiday’ would be those as laid down by Foreign Exchange Dealers’ Association of India (FEDAI).

- Basis: In the context of financial futures, basis can be defined as the futures price minus the spot price. There will be a different basis for each delivery month for each contract. In a normal market, basis will be positive. This reflects that futures prices normally exceed spot prices.

- Cost of carry: The relationship between futures prices and spot prices can be summarized in terms of what is known as the cost of carry. This measures (in commodity markets) the storage cost plus the interest which is paid to finance or ‘carry’ the asset till delivery less the income earned on the asset. For equity derivatives, carry cost is the rate of interest.

- Types of orders

- Pro: Pro means that the orders are entered on the trading member’s own account.

- Cli: Cli means that the trading member enters the orders on behalf of a client.

- Limit price: An order to buy at or below a specified level or to sell at or above a specified price (called the price) which is favourable than the prevailing levels.

- Stop-loss: This facility allows the user to release an order into the system, after the market price of the security reaches or crosses a threshold price. For example, if for stop-loss buy order, the trigger is INR 48.0025, the limit price is INR 48.2575, then this order is released into the system once the market price reaches or exceeds INR 48.0025. This order is added to the regular lot book with time of triggering as the time stamp, as a limit order of INR 42.2575. Thus, for the stop-loss buy order, the trigger price has to be less than the limit price and for the stop-loss sell order, the trigger price has to be greater than the limit price.

- Immediate or cancel (IOC): An IOC order allows the user to buy or sell a contract as soon as the order is released into the system, failing which the order is cancelled from the system. Partial match is possible for the order and the unmatched portion of the order is cancelled immediately.

CONCEPT OF MARGIN IN ETC MARKETS

Initial Margin

- Initial margin is the minimum amount which the buyer and the seller have to maintain if they want to enter into a future contract.

- Initial margin is only a security provided by the client to the exchange. It can be withdrawn in full after the position is closed, i.e., after the contract expires and after the settlement of all losses, if any.

- Initial margin deposited is not an expense it is just like security deposit.

Mark-to-Market Margin

- It is like a profit and loss account which is to be settled on a daily basis. Futures follow pay as you go system. Any difference, resulting in gain/loss to the investor, is settled immediately.

- MTM has to be maintained by both buyer and seller in case of future contract.

- The margin account changes with the change in daily prices.

Maintenance Margin

- Maintenance margin is not any account which is to be maintained. It is just a limit or deadline below which balance should not drop.

- This is lower than the initial margin. This is to ensure that if balance in the margin account falls below the maintenance margin, the investor receives a margin call and is expected to top up the margin account to the initial margin level before trading commences on the next day. In other words, whenever balance falls below maintenance margin, we have to bring back the balance to the initial margin. The extra fund which is deposited is known as variation margin or margin call.

Note: It is because of strict provisions of margin requirement, the risk of default in such type of future contract is nil. Profit and losses are to be settled on a daily basis; hence, risk is nil. Investor can withdraw any amount during the period of contract from his account over and above the initial margin amount. Drawing must be done only if specific instruction is given in question.

ADVANTAGES OF CURRENCY FUTURES MARKET

Transparency

- Transactions are carried out through a state-of-the-art electronic trading infrastructure of recognized exchanges.

- Possible to verify trade details on exchange Web site.

Accessibility

- Investors get an easy access to currency futures trading on the popular exchanges through brokers.

- No underlying to be provided unlike OTC market.

Cost

- Competitive bid offer spreads for small amounts.

- Small amount of brokerage fees, statutory duties and taxes.

Efficient Price Discovery

- Internationally established that currency future is an efficient mechanism for price discovery.

- Automated electronic trading system where orders are executed on the basis of price-time priority.

Credit Risk

- All trades done on exchanges are guaranteed by the clearing corporations.

Standardized Contracts

- Lot size (USD 1,000) and maturity (12 monthly contracts).

- Small and medium investors with limited resources would find it tremendously beneficial to take positions in standardized USD/INR futures contracts.

Clients can also monitor the rates/contracts quoted in the exchange. They can check the contracts and quotes on the NSE or MCX-SX Web sites. The rates available with the dealer through the exchange terminal would be the same.

Clients can also verify the contracts entered by the dealers on their behalf. Dealers would be sending a contract note to the client within 24 hours of trade. They can then verify trades from the NSE or MCX-SX Web site from ‘Trade Verification’ link to see whether the deals entered into by dealers on his behalf have actually been entered or not.

NSE AND THOMSON REUTERS SCREENSHOTS

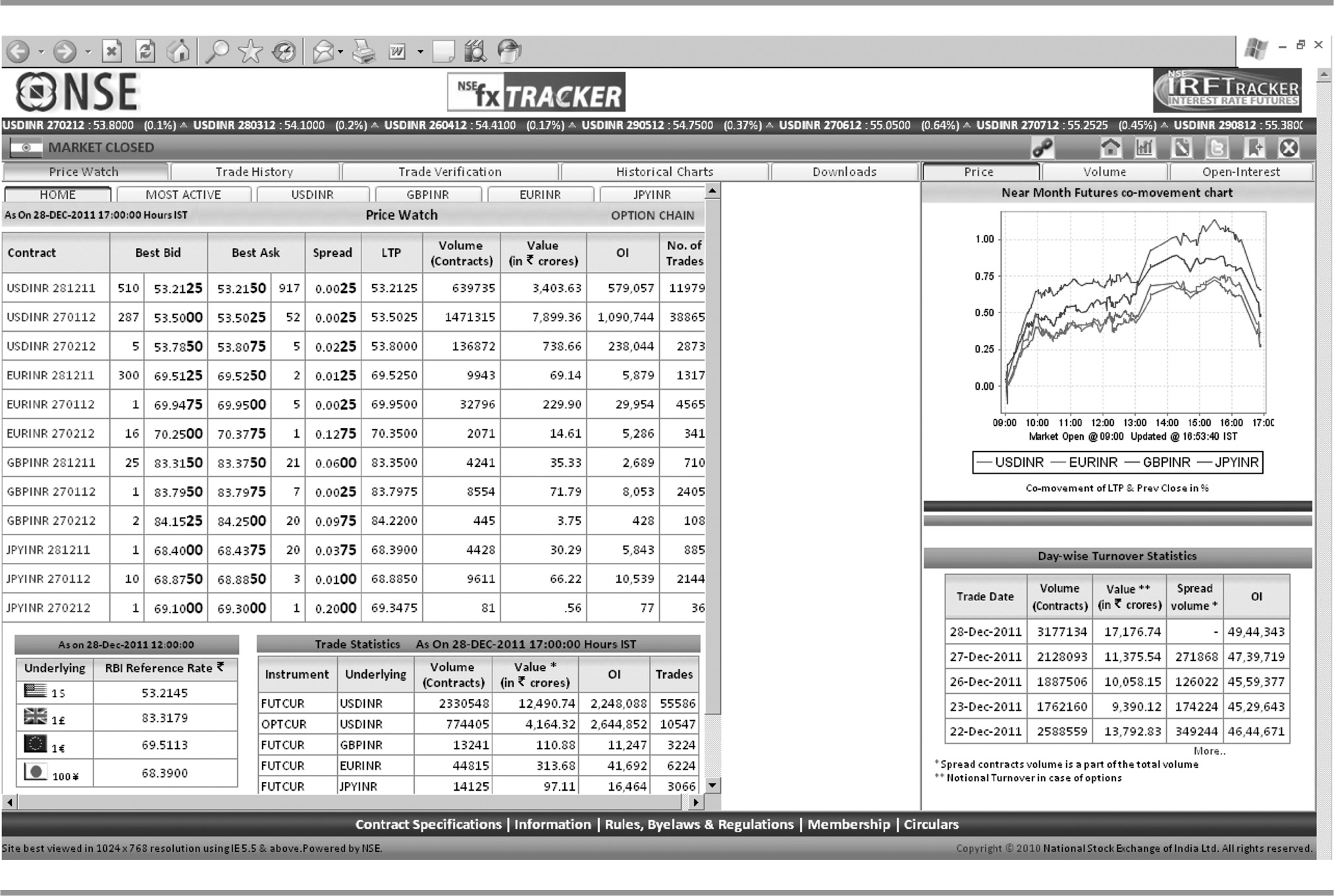

The following NSE screenshot has been taken from ‘NSE FX Tracker’ screen. This contains information on prevailing price, volume, open interest and other relevant trade statistics for the benefit of market participants.

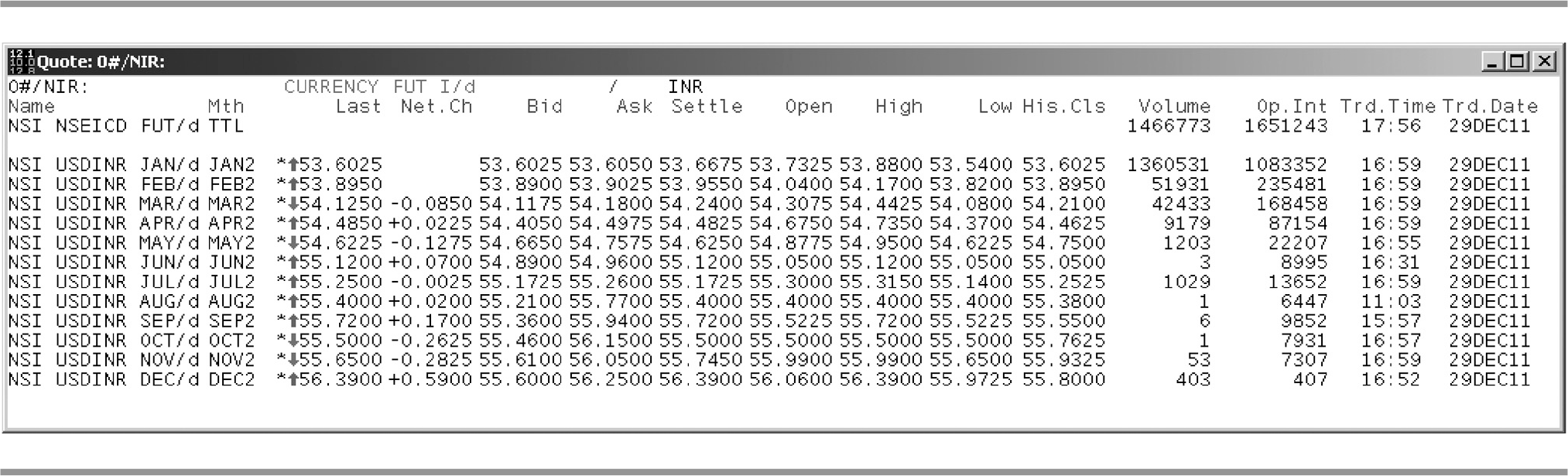

The following screenshot from Thomson Reuters provides information on live prices, today’s open, high, low, close, volume and open interest.

Screenshot 4.2 Thomson Reuters

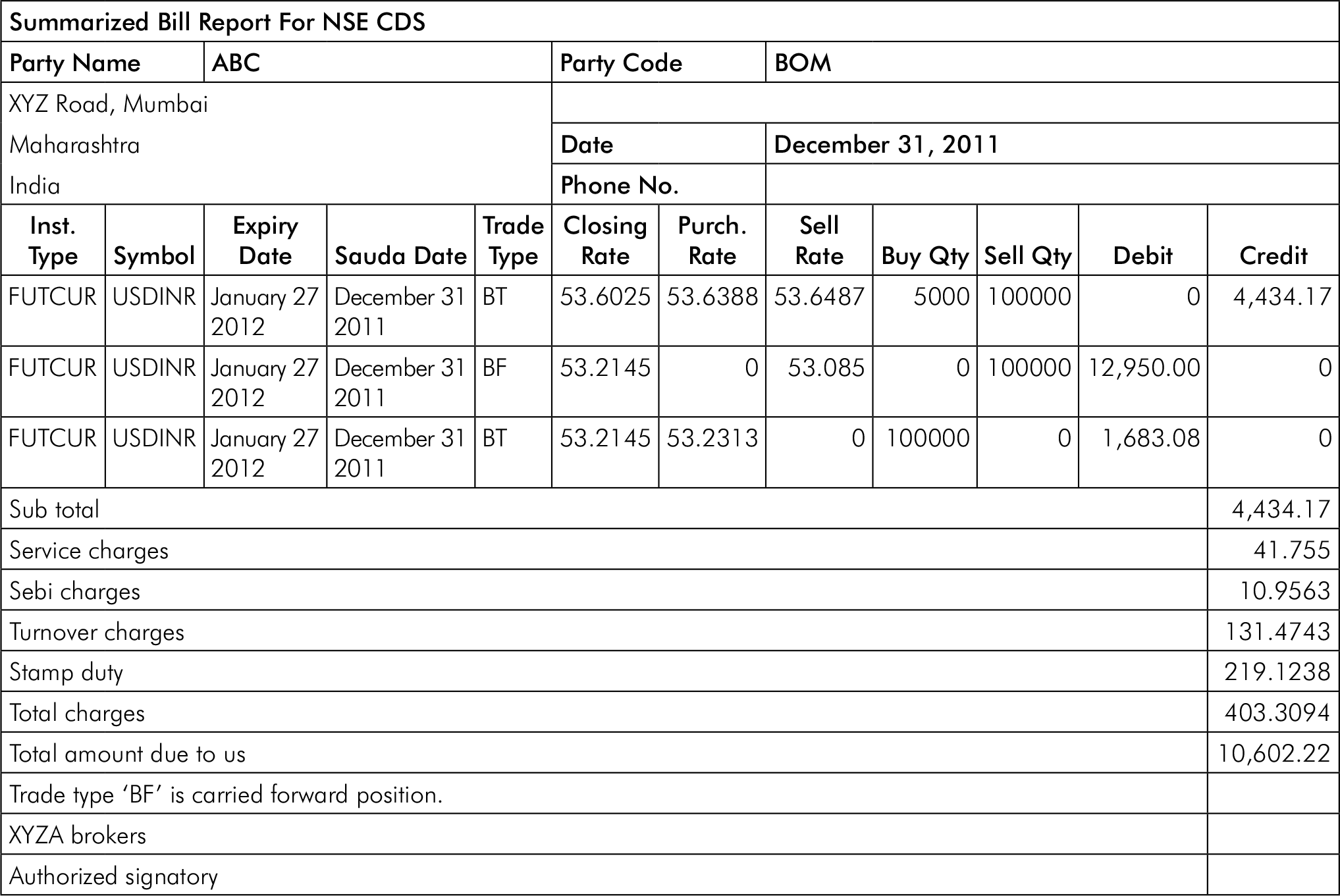

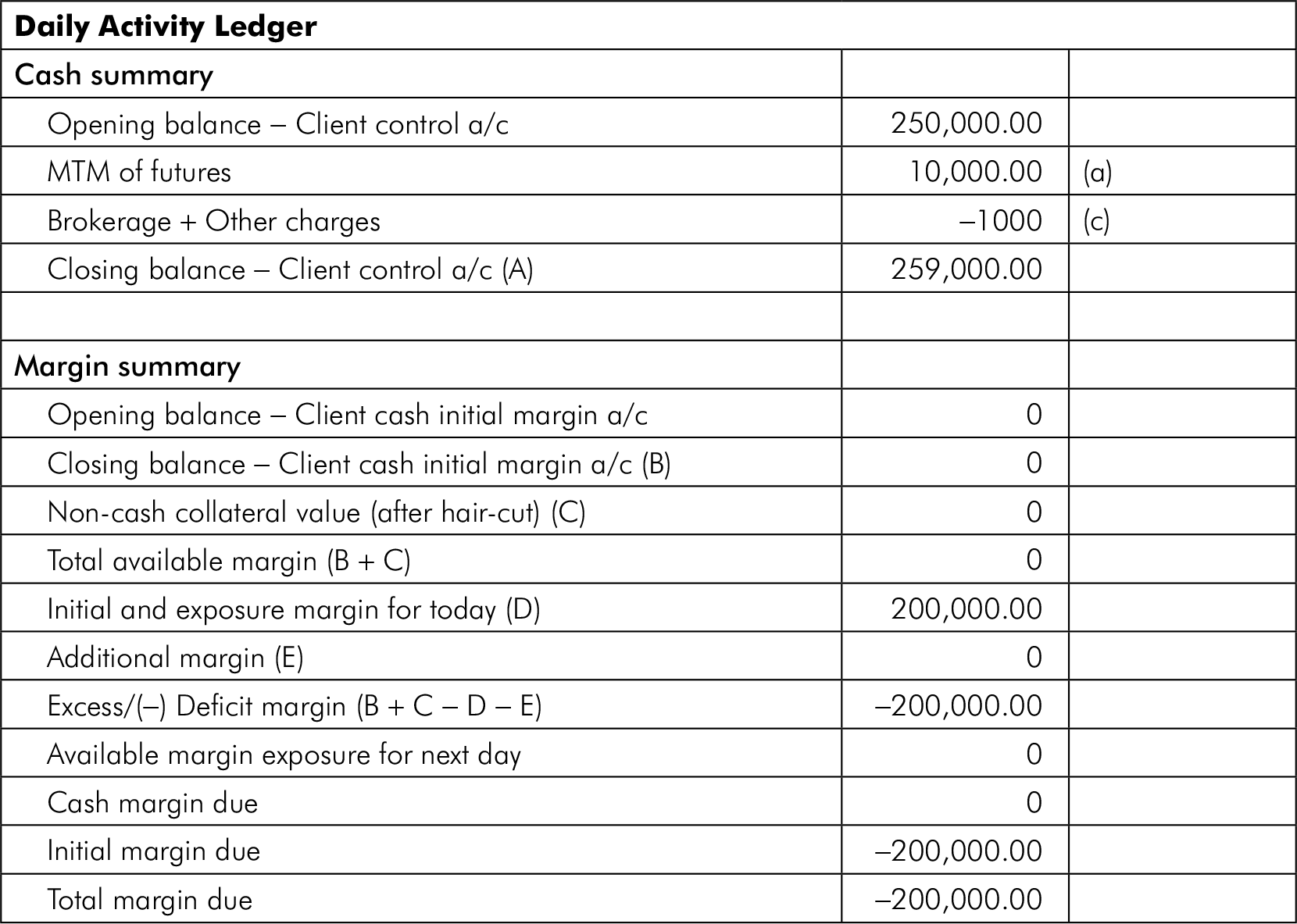

SUMMARY STATEMENT AND LEDGER FORMATS

As a part of dealing system on exchange, broker at the end of every day provides its clients with a summary of transactions done, brokerage charged and ledger. An illustrative summarized bill and ledger summary is mentioned further. The actual format of each broker may vary.

DIFFERENCE BETWEEN ETC AND OTC

STOCK FUTURES IN BRIEF

There is a spot market (cash market) where the transaction for purchase–sale item is against cash for immediate delivery. There is another market called ‘future market’ where the same item is traded for future dated delivery, but the contract will be entered today. The rate, quantity and delivery date will be decided today but actual transaction will be at future date. The item transacted is to be carried for future date. Hence, normally prices in the future market are more than the spot price.

- If there is no dividend on a share then

Fair future price = Cash price + Cost of carrying (interest cost)

- If the stock provides dividend then:

Fair future price = Cash price + Cost of carrying − Intermediate receipt (dividends)

The actual price for future may be different from fair future price:

It provides an opportunity for arbitrage.

- If actual future price is less than the fair future price:

- If actual price in future market is more than the fair future price, he should sell future and buy the spot.

- He will sell the item in future market.

- He will raise loan and buy the item in spot market.

- On the due date, he will sell the item at committed future price and repays loan with interest (i.e. arbitrage gain).

MISCELLANEOUS ILLUSTRATIONS

ILLUSTRATION 1

The futures contract in GBP/INR for value three months is quoted at 96.50. Prevailing spot rate for GBP/INR is 92. Calculate continuously compounded risk-free rate of interest implied in this contract.

Solution

Fair future price = Spot price × er × t = 96.50 = 92 × er × t × 0.25 = 1.04891

er0.25 = 0.04, r = 16 per cent (approx.) therefore, continuously compounded risk-free rate is 16 per cent p.a.

ILLUSTRATION 2

The spot rate of USD/INR is 40. The risk-free rate for the investor is 5 per cent. The three months futures rate is 42. Should an Indian exporter sell USD using three months futures contract?

Solution

Fair future price = Spot price × er × t = 40 × e0.05 × 3/12 = 40 × (1.0125) = 40.50

Decision

Actual future price = 42 and Equilibrium or Fair price = 40.50

Since actual future price (INR 42) > Fair future price (INR 40.50)

Future price is overvalued. Under such conditions, he should enter into a contract of selling future at INR 42.

ILLUSTRATION 3

An exporter has hedged USD 1 against INR at 45 for value 30 September 2011. Initial margin money taken by the broker is INR 1 and the exchange follows marked to market policy strictly. Calculate margin requirement for each of the dates below.

Solution

| Date | Market rate | ITM/ATM/OTM | Amount in INR charged from/passed to the client |

|---|---|---|---|

| 1 August | 44.00 | ITM | – |

| 3 August | 44.50 | ITM | – |

| 5 August | 43.00 | ITM | – |

| 7 August | 45.00 | ATM | – |

| 9 August | 47.00 | OTM | −1 |

| 11 August | 48.00 | OTM | −1 |

| 13 August | 47.00 | OTM | +1 |

| 15 August | 46.00 | OTM | +1 |

| 17 August | 44.00 | ITM | – |

| 19 August | 42.00 | ITM | – |

| 21 August | 41.00 | ITM | – |

| 23 August | 43.00 | ITM | – |

| 25 August | 45.00 | ATM | – |

| 27 August | 47.00 | OTM | −1 |

| 29 August | 49.00 | OTM | −2 |

| 31 August | 42.00 | ITM | +3 |

| 3 September | 46.00 | OTM | – |

| 6 September | 47.00 | OTM | −1 |

| 9 September | 42.00 | ITM | +1 |

| 12 September | 41.00 | ITM | – |

| 15 September | 40.00 | ITM | – |

| 18 September | 42.00 | ITM | – |

| 21 September | 48.00 | OTM | −2 |

| 24 September | 42.00 | ITM | +2 |

| 27 September | 44.00 | ITM | – |

| 30 September | 43.00 | ITM | – |

ILLUSTRATION 4

An importer has hedged USD 1 payable against INR at 45 for value 30 September 2011. Initial margin taken by the broker is INR 1 and the exchange follows marked to market policy strictly. Calculate margin requirement for each of the following dates.

| Date | Market rate | ITM/ATM/OTM | Amount in INR charged from/passed to the client |

|---|---|---|---|

| 1 August | 44.00 | OTM | – |

| 3 August | 44.50 | OTM | – |

| 5 August | 43.00 | OTM | −1 |

| 7 August | 45.00 | ATM | +1 |

| 9 August | 47.00 | ITM | – |

| 11 August | 48.00 | ITM | – |

| 13 August | 47.00 | ITM | – |

| 15 August | 46.00 | ITM | – |

| 17 August | 44.00 | OTM | – |

| 19 August | 42.00 | OTM | −2 |

| 21 August | 41.00 | OTM | −1 |

| 23 August | 43.00 | OTM | +2 |

| 25 August | 45.00 | ATM | +1 |

| 27 August | 47.00 | ITM | – |

| 29 August | 49.00 | ITM | – |

| 31 August | 42.00 | OTM | −2 |

| 3 September | 46.00 | ITM | +2 |

| 6 September | 47.00 | ITM | – |

| 9 September | 42.00 | OTM | −2 |

| 12 September | 41.00 | OTM | −1 |

| 15 September | 40.00 | OTM | −1 |

| 18 September | 42.00 | OTM | +2 |

| 21 September | 48.00 | ITM | +2 |

| 24 September | 42.00 | OTM | −2 |

| 27 September | 44.00 | OTM | +2 |

| 30 September | 43.00 | OTM | −1 |

ILLUSTRATION 5

The following data relates to the calculated Ltd.’s share price:

| Current price per share | INR 180 |

| Price per share in future market–six months | INR 195 |

It is possible to borrow money in the market for securities transactions at 12 per cent p.a.

Required:

- Calculate the theoretical minimum price of a six months forward contract.

- Explain if any arbitraging opportunities exist.

Solution

- Price in cash market today = INR 180

Fair price of future = Cash price + Cost to carry interest cost

= 180 + {180 × 12 per cent × 6/12}= 180 + 10.80 = INR 190.80 - Fair price for six months future transaction = INR 190.80

Actual price for six months future transaction = INR 195

(Today’s quotation in future market)

Actual price is not equal to fair price, hence arbitrage is possible.

Actual price is more, hence arbitrager will sell future.

He will buy spot by raising loan.

He will raise a loan of INR 180 and purchase that share in cash market. He sells that share in future market at INR 195 (delivery at six months)

At six months time:

The loan repayment = 180 + 10.80 = 190.80

Sale realization under future sale = INR 195

Net gain = Sale realization − Loan paid = 195 − 190.80 = INR 4.20

ILLUSTRATION 6

The price of XYZ Ltd. stock on 31 December 2010 was INR 220 and the future price of the same stock on the same date, i.e., 31 December 2010 for March 2011 was INR 230. Other features of the contract and related features are as follows:

| Time to expiration | Three months (0.25 years) |

| Borrowing rate | 15 per cent p.a. |

| Annual dividend on the stock | 25 per cent payable before 21 March 2011 |

Calculate theoretical value (fair value) of a future, assuming paid-up value per share is INR 10.

Solution

Fair future price = Cash price + Cost to carry − Dividend

Actual future price = 230

Actual future price is more than the fair future price. The person will sell the future by raising loan.

At three months,

| Sale value under future | 230 |

| Dividend redeemed | 2.50 |

| 232.50 | |

| Less: Loan repayment | 228.25 |

| Gain | 4.25 |

ILLUSTRATION 7

Current NIFTY is 1800 and minimum lot is 100. Risk-free rate is 8 per cent p.a. c.c [per annum continuously compounded] and the futures period is three months. What is the fair future value of three months NIFTY futures?

Solution

Fair future value = spot price × ert = 1800 × e0.08 × (3/12) = INR 1,836.36

Therefore, fair future value for 100 lots will be 100 × 1,836.36 = 183,636

ILLUSTRATION 8

The shares of Brown and Pages Ltd. are being traded at INR 250 on the BSE. Its futures for one month, two months and three months are also available on the BSE. If the risk-free rate is 12 per cent p.a. and no dividends are expected during this period, what should be the equilibrium price of these futures?

Solution

The equilibrium for different futures would be:

One month futures: F = Spot Price × ert = INR 250 × e0.12 × 0.83 = INR 252.50

Two months futures: F = Spot Price × ert = INR 250 × e0.12 × 0.167 = INR 255.05

Three months futures: F = Spot Price × ert = INR 250 × e0.12 × 0.25 = INR 257.61

Working Note: the time period (t) of these futures is one month, two months and three months, i.e. 0.083 years, 0.167 yrs, and 0.25 yrs. The spot price(s) is INR 250 and risk free rate (r) is 12 per cent p.a. c.c.

ILLUSTRATION 9

Determine value of six months future on Y Ltd. Shares from following data:

Current price = INR 80 Dividend (after three months) = INR 3 R = 10 per cent p.a. c.c

Solution

Fair future value = (Spot price − Present value of dividend) × ert

Where spot price = 80;

Present value of expected dividend

= Dividend × e–rt = 3 × e0.10 × 6/12 = 3 × 0.975325 = 2.93

Therefore, fair future value

= (80 − 2.93) × e(0.10 × 6/12) = 77.07 × 1.05127 = 81.02

ILLUSTRATION 10

Calculate the price of a six months futures contract on a share which is currently priced at INR 75. The share is expected to pay a INR 2 dividend four months from today. The continuously compounded risk-free rate is 12 per cent per annum. The contract size is 100. If the contract value is INR 7,400 what steps (action) would follow. In case it is INR 7,800 what would you do?

Solution

Fair future price = (Spot price − Present value of dividend income) × ert

Working notes: Present value of dividend income

Decision: Actual future price fair future price

| AFP | FFP | Valuation | Future market | Spot market |

|---|---|---|---|---|

| 7400 | 7760 | Under | Buy | Sell |

| 7800 | 7760 | Over | Sell | Buy |

Or decision:

When actual value is INR 7400:

Since actual future value < fair future value, stock is undervalued in the future market.

For arbitrage gain, sell the stock in the spot market, buy it in the future market.

When actual value is INR 7,800:

Since actual future value > fair future value, stock is overvalued in the future market.

For arbitrage gain: buy the stock in the spot market, sell the stock in the future market.

Additional analysis: gain or loss: on expiration, i.e., at the end of six months

- When the contract value is INR 7,400

Sell the stock in the spot market at INR 7,500 and invest the proceed at risk free

Rate of interest @ 12 per cent c.c for six months and collect at the end of six months

INR 7500 × e0.12 × 6/12 or 7500 × 1.0618, i.e.

Loss on dividend income to be received otherwise

(200 × e2/12 × 0.12 or 200 × e0.02 or 200 × 1.02020)

Purchase stock in the future market as contracted

Gain 359.76

(Here we have assumed that arbitrageur holds 100 shares of the given stock initially)

- When the contract value is INR 7,800

Repayment including interest @ 12 per cent c.c for borrowing and buying stock in the spot market

(7500 × e0.12 × 6/12 or 7500 × 1.06189)

Dividend to be received on stock purchased

(200 × e2/12 × 0.12 or 200 × e0.02 or 200 × 1.02020)

Sell the stock in the future market as contracted

Gain 40.24

ILLUSTRATION 11

The following data relate to Anant Ltd.’s share:

| Current price share | INR 1,800 |

| Six months future’s price/share | INR 1,950 |

Assuming it is possible to borrow money in the market for transactions in securities at 12 per cent per annum, you are required to calculate the theoretical minimum price of a six months forward purchase.

Solution

Calculation of theoretical minimum price of a six months forward contract.

Theoretical minimum price = INR 1,800 + (INR 1,800 × 12/100 × 6/12) = INR 1,908

ILLUSTRATION 12

The settlement price of December Nifty futures contract has been provided below. The broker requires initial margin of 8 per cent and maintenance margin of 6 per cent on the deal. The index closed at the following levels on the next five days.

| Days | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Closing price | 1,340 | 1,360 | 1,300 | 1,280 | 130 |

- Calculate the mark-to-market cash flows and daily closing balance in the account of (i) an investor who has gone long at 1310, and (ii) and investor who has gone short at 1310.

- Calculate the net profit or loss on each of the contracts.

Solution

Initial Margin (IM) = INR 10,480 (1310 × 100 × 0.08)

Maintenance Margin (MM) = INR 7,860 (1310 × 100 × 0.06)

Note: Initial margin and maintenance margin are same for both long and short positions

- Status of investor who has gone long:

Day Settlement price Opening balance Mark-to-market C/F Deposit Closing balance 1 1340 10480 +3000 13480 2 1360 13480 +2000 15480 3 1300 15480 −6000 9480 4 1280 9480 −2000 3000 10480 5 1305 10480 +2500 12980 Net profit on the contract = 3000 + 2000 − 6000 − 2000 + 2500

= (500) or simply (1305 − 1310) × 100= −500Additional analysis:

Why has margin call of INR 3,000 been made at the end of Day 4?

At the end of day 4, the balance falls below maintenance margin of INR 7860, i.e., it falls to

9480 − 2000 = 7480.Whatever balance falls below maintenance margin, one has to maintain the balance up to the initial margin.

Hence, margin call of INR 3,000 (10,480 − 7,480) has been made.

- Status of the investor who has gone short:

Day Settlement price Opening balance Mark-to-market C/F Deposit Closing balance 1 1340 10480 +3000 3000 10480 2 1360 10480 −2000 8480 3 1300 8480 +6000 14480 4 1280 14480 +2000 16480 5 1305 16480 −2500 13980 Net profit (loss) on the contract: −3000 − 2000 + 6000 + 2000 − 2500 = 500

Or simply (1310 − 1305) × 100 = 500

TEST YOUR UNDERSTANDING

- Consider a three months maturity future contract on a USD/INR having a spot rate of 46 with compounded continuously risk-free rate of return of 10 per cent p.a. Find the price of the future contract.

- The spot of GBP/INR on 31 December 2010 was 75 and the future price on the same date, i.e., 31 December 2010, for 31 March 2011 was INR 80. Related information of the contract are as follows:

Time to expiration Three months (0.25 years) Borrowing rate 15 per cent p.a. Calculate theoretical value (fair value) of the future of the currency pair.

- Jai Exports Ltd. has long USD 1 million on 1 June 2011 for maturity 30 June 2011 at 44.50 USD/INR with exchange. The client has hired you as his financial consultant to let him know about his daily MTM position and the margin money which he shall pay or receive to the bank on account of such MTM.

Date Market rate In the money/Out of money/At the money Remarks 5 June 44.75 8 June 45.00 14 June 45.15 17 June 44.55 21 June 44.65 23 June 44.35 25 June 44 27 June 44.15 30 June 44.50 Answer the following questions:

(Assume no initial margin being taken for calculation purposes)

- Fill in the two vacant columns above. In remarks you have to tell the amount of money which the client shall pay or receive.

- What do you understand by initial margin and maintenance margin?

- Mittal Imports Ltd. has an import payment of USD 1 million for maturity 30 June 2011, for which he hedges at 45.50 USD/INR with the exchange. The client has hired you as his financial consultant to let him know about his daily MTM position and the margin money which he shall pay to or receive from the bank on account of such MTM.

Date Market rate In the money/Out of money/At the money Remarks 5 June 44.75 8 June 46.00 14 June 46.15 17 June 45.55 21 June 45.65 23 June 45.35 25 June 45 27 June 45.15 30 June 45.50 Answer the following questions:

(Assume no initial margin being taken for calculation purposes)

- Fill in the two vacant columns above. In remarks column, state the amount of money payable or receivable by the client.

- What are the above market rates known as in foreign exchange parlance?

- A client is an exporter and hedges USD 1 million at INR 45 for maturity 30 September 2011. Initial margin money taken by the broker is INR 1 on each USD and the exchange follows marked to market policy strictly. Fill the rest of the table provided as follows.

Date Market rate ITM/ATM/OTM Amount in INR charged from/passed to the client 1 August 44.00 3 August 44.50 5 August 43.00 7 August 45.00 9 August 47.00 11 August 48.00 13 August 47.00 15 August 46.00 17 August 44.00 19 August 42.00 21 August 41.00 23 August 43.00 25 August 45.00 27 August 47.00 29 August 49.00 31 August 42.00 3 September 46.00 6 September 47.00 9 September 42.00 12 September 41.00 15 September 40.00 18 September 42.00 21 September 48.00 24 September 42.00 27 September 44.00 30 September 43.00 - A client is an importer and hedges USD 1 million at INR 45 for maturity 30 September 2011. Initial margin money taken by the broker is INR 1 on each USD and the exchange follows marked to market policy strictly. Fill the rest of the table provided as follows.

Date Market rate ITM/ATM/OTM Amount in INR charged from/passed to the client 1 August 44.00 3 August 44.50 5 August 43.00 7 August 45.00 9 August 47.00 11 August 48.00 13 August 47.00 15 August 46.00 17 August 44.00 19 August 42.00 21 August 41.00 23 August 43.00 25 August 45.00 27 August 47.00 29 August 49.00 31 August 42.00 3 September 46.00 6 September 47.00 9 September 42.00 12 September 41.00 15 September 40.00 18 September 42.00 21 September 48.00 24 September 42.00 27 September 44.00 30 September 43.00 - If Study Point Ltd. provided a dividend yield of 6 per cent p.a., the current value of the stock is INR 500 and the continuously compounded risk-free rate of return is 8 per cent p.a. What would be the value of a six months future contract? If the future rate is INR 550 what action would follow? Will the position change if the rate is INR 350?

- Azhar Ltd. quoted in the market at INR 40. A six months future contract on 100 shares of it can be bought. The risk-free rate of interest is 12 per cent p.a. continuously compounded. Azhar Ltd. is certain to pay a dividend of INR 2.5 per share three months from now. What should be the value of future contract? If the future contract is priced at INR 4,500 what action would follow? If it is priced at INR 3,500 what would you do?

- Consider a three months future contract on 500 shares with each share priced at INR 75. Dividend @ INR 2.50 per share is expected to accrue to the share in a period of three months. The continuous compounded risk-free rate of return is 15 per cent p.a. Find the value of the future contract.

- Following is the data of Mamta Ltd. share prices:

Current price per share INR 160 Price per share in the future market—six months INR 168 Dividend per share at six months time INR 2.50 It is possible to borrow money in the market for securities transactions @ 12 per cent p.a.

- Calculate the theoretical minimum price of a six months forward contract.

- Explain if any arbitraging opportunities exist.

- If price per share in the future market for six months is INR 162. Is there any arbitrage opportunity?

- Consider a six months gold future contract of 100 gm. If the spot price is INR 600 per gram and it costs INR 3 per gram for the six months period to store gold and that the cost is incurred at the end of two months. If the risk-free rate of interest is 12 per cent p.a. continuously compounded, compute the future rate. If the futures are available at INR 620, what action would you follow? Would the position changes if the future were available at INR 660?

- Calculate the theoretical value (fair value) of a future BSE Sensex 30.

Date : Spot Cash BSE Sensex 30 : INR 5, 750 Interest rate : 6 per cent p.a. (not compounded continuously) Dividend yield : 4 per cent p.a. (not compounded continuously) Days till expiry : 91 - A three months futures contract on NIFTY is available at a time when the NIFTY is quoting 4800 points. Continuously compounded risk-free rate is 10 per cent. Continuously compounded yield on the Nifty stock is 2 per cent p.a. One future contract equals 200 Nifty. How much will you pay for Nifty futures, if the Nifty future trades at 4825? What action would you take?