chapter 7

FX Options: Structured Solutions

LEARNING OBJECTIVES

This chapter aims to make readers understand different types of structures which could be used for hedging foreign exchange exposures originating from export and import or for expressing directional/volatility view on market. It also takes readers deep into the technicalities and complexities of the market explained in a simple yet effective manner with practical examples. Execution of various kinds of structures depends on prevailing regulations and laws of land and their suitability for various investors from risk-return perspective. The contents of this chapter are organized in the following order:

VANILLA OPTION

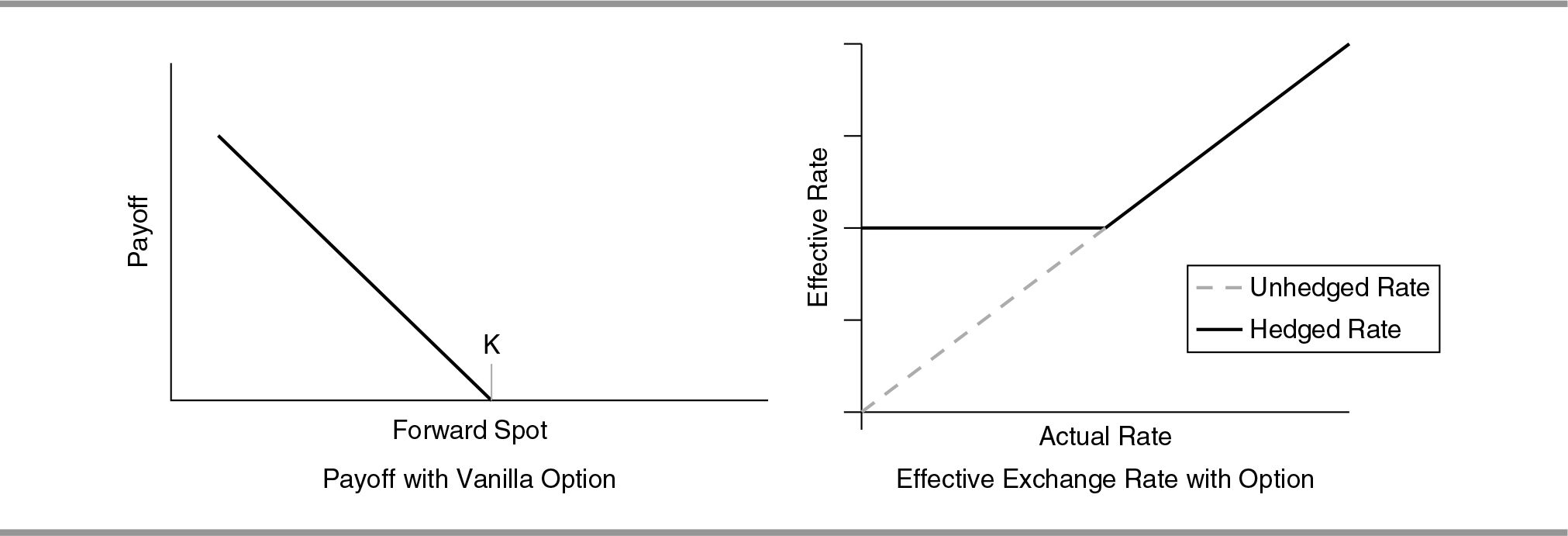

Vanilla Option (European)

Strategy Term: Vanilla Option (European)

Strategy Description: Vanilla option gives the option buyer, the right but not the obligation, to buy/sell the currency at a pre-determined exchange rate. Option seller has the obligation only, to buy/sell the currency at a pre-determined exchange rate in case the buyer exercises the option.

Protection from unfavourable currency movement and full upward participation is available to the option buyer. He has to pay premium to option seller to get an unlimited participation in the gain.

Strategy Application: In Vanilla option (call/put), the option buyer has the right to buy/sell currency at a predetermined exchange rate.

Example

An option buyer buys a GBP put at strike K = 1.5800. Though in this deal, at maturity, the option buyer will have an option to sell GBP at K, and will receive a fixed amount of dollars (dollar amount = GBP amount × 1.5800).

In case the GBP appreciates, the option buyer can choose not to exercise the option and can rather sell GBP at the prevailing spot rate which is higher than the strike of option and avail the benefit of GBP appreciation.

In case GBP depreciates, the option buyer can sell the GBP at option strike. The premium can be reduced by worsening the strike, i.e., buying further ‘out of money’ (OTM) put.

The premium of an option is determined on the following basis:

- Intrinsic value: The level of strike relative to the outright forward.

- Volatility: Higher the volatility, higher the premium.

- Tenor: Higher the tenor, higher the premium.

Payoff: Option with strike K.

At maturity:

| Month end rate | Option buyer sells GBP at |

|---|---|

| = < 1.5800 (K) | 1.5800 |

| > 1.5800 (K) | Market Rate |

Graph 7.1

Pros

- Worst-case rate is known, Therefore in this example, option buyer can sell GBP at 1.5800 even if GBP depreciates below 1.5800.

- Option buyer can participate in the upside as well and can avail the complete benefit of GBP appreciation above 1.5800.

Risks Involved

- The risk is limited to the option buyer to the extent of premium paid, in case the option is not exercised but the seller of option is open to the currency movement and has unlimited risk.

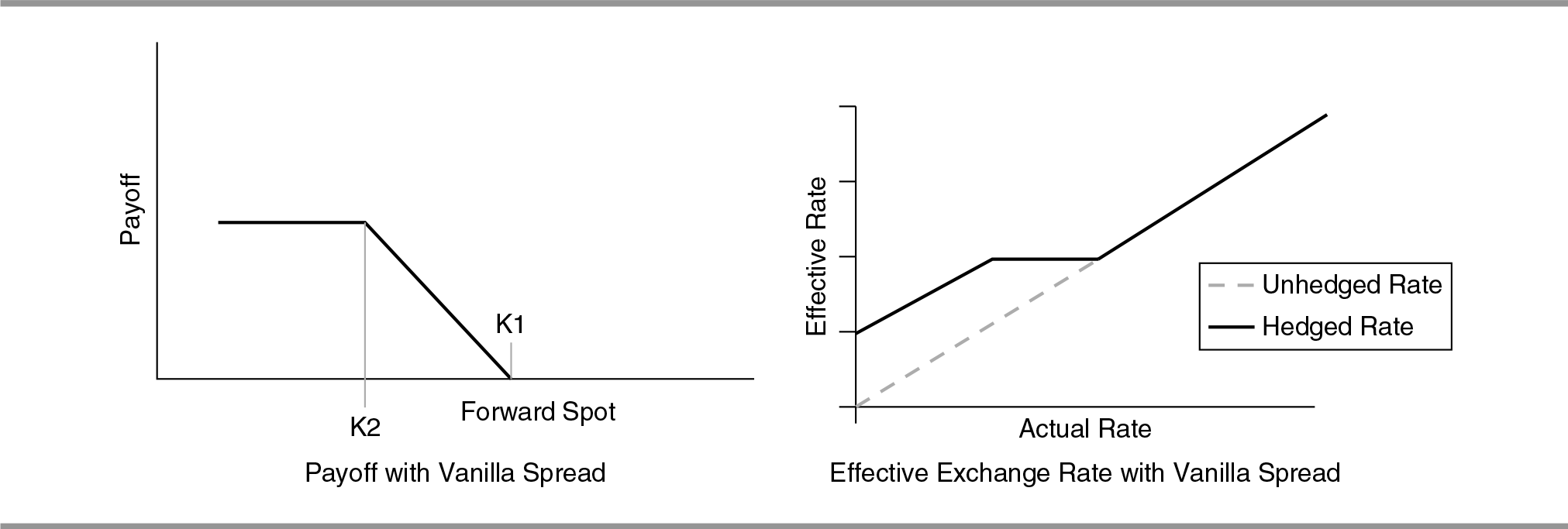

Vanilla Spread (European)

Strategy Term: Vanilla Spread (European)

Strategy Description: It is a cost reduction structure that caps the payoff. It involves simultaneous purchase and sale of put/call option at different strikes, to lock in future exchange rate with limited upward participation.

Strategy Application: There can be two structures:

- Put spread

- Call spread

Example

Structures are explained further taking an example of ‘put spread’.

In vanilla put spread,

- The option buyer will buy GBP put option at pre-determined GBP/USD exchange rate (K1, 1.5650 here).

- Also sell GBP put at a pre-determined GBP/USD exchange rate (K2, 1.5150 here).

- K2 will be lower than K1 in this case.

- At maturity, the option buyer will have an option to sell GBP at K1.

- The option buyer will have an obligation to buy GBP at K2.

In case GBP appreciates, the option buyer can choose not to exercise the option and can sell GBP at the prevailing spot rate and avail of the benefit s of GBP appreciation.

However, as GBP depreciates further and goes below strike K2, the sell GBP put will lead to negative payoff, which will be offset by the positive payoff from buy GBP put.

Like Vanilla option, the premium is affected by the following:

- Implied volatility

- Intrinsic value

- Tenor

Payoff: Option with Strike K1 and K2.

At maturity:

| ■ If Spot < K2, | then pay off is (K1 – Spot) + (Spot – K2). |

| ■ If K2 = < Spot = < K1, | then pay off is (K1 – Spot). |

| ■ If Spot > K1, | then payoff is 0. |

Building Blocks

- Spot 1.5633; Forward 1.56328.

- Buy 1 M GBP put/USD call @ 1.5650 (K1).

- Sell 1 M GBP put/USD call @ 1.5150 (K2).

| Month end rate | Option buyer sells GBP at |

|---|---|

| < 1.5150 (K2) | Market Rate + 0.05 |

| > = 1.5150 (K2) & = < 1.5650 (K1) | 1.5650 |

| > 1.5650 (K1) | Market Rate |

Graph 7.2

Pros

- Option buyer has a capped gain, in case, GBP depreciates. In this example, option buyer has the right to sell GBP at rate 0.05 higher than exchange rate prevailing at maturity if GBP depreciates below 1.5150.

- Option buyer can also participate in upside movement of currency and can avail complete benefit of GBP appreciation above 1.5650.

- Lower cost than Vanilla option.

Risks Involved

- Payoff is capped when GBP depreciates below the sell put strike, i.e., 1.5150 in the given example.

Range Forward/Risk Reversal

Strategy Term: Range Forward/Risk Reversal

Strategy Description: It involves simultaneous purchase of a put/call option and sale of a call/put option at different strikes, to lock in future exchange rate within a range. It is locked between a ‘worst case forward rate’ and a ‘best case forward rate’.

Strategy Application: There can be two structures:

- Importer range forward

- Exporter range forward

Example

These structures have been explained as follows, taking the example of an exporter range forward

In GBP exporter range forward,

- The option buyer will buy GBP put option at a pre-determined GBP/USD exchange rate (K1, 1.5650 here).

- Also sell GBP call at a pre-determined GBP/USD exchange rate (K2, 1.5850 here).

- In this case, K2 will be higher than K1.

- Through this deal the option buyer will have an option to sell GBP at K1.

- Also an obligation to sell GBP at K2, depending on spot GBP rate on maturity.

In case GBP appreciates but, it is at, or below, K2; then the option buyer can choose not to exercise the option and can sell the GBP at the prevailing spot rate to avail the benefit of GBP appreciation.

However, in case the GBP appreciates beyond K2, the option buyer will have a negative payoff. Thus, cost reduction comes at the increased risk of negative payoff.

Payoff: Option with Strike K1 and K2.

At maturity:

| ■ If Spot < K1, | then payoff is (K1 – Spot). |

| ■ If K1 = < Spot = < K2, | then payoff is 0. |

| ■ If Spot > K2, | then payoff is (K2 – Spot) (Negative). |

Building Blocks

- Spot 1.5659 forward 1.566.

- Buy 1 M GBP/USD put @ 1.5650 (K1).

- Sell 1 M GBP/USD call @ 1.5850 (K2).

This can either be zero cost or premium paid option structure.

| Month end rate | Option buyer sells GBP at |

|---|---|

| < 1.5650 (K1) | 1.5650 |

| >= 1.5650 (K1) & = < 1.5850 (K2) | Market Rate |

| > 1.5850 (K2) | 1.5850 |

Graph 7.3

Pros

- Worst-case scenario is known; therefore, the option buyer has the right to buy/sell the currency at a favourable rate. In this example, option buyer has the right to sell GBP at 1.5650, if GBP depreciates below 1.5650.

- The option buyer can avail limited benefit of GBP appreciation above 1.5650 upto 1.5850.

- Lower cost than vanilla option.

Risks Involved

- There is risk of negative payoff, in case, the GBP appreciates above 1.5850 because the buyer has an obligation to sell GBP at 1.5850 if it appreciates above 1.5850.

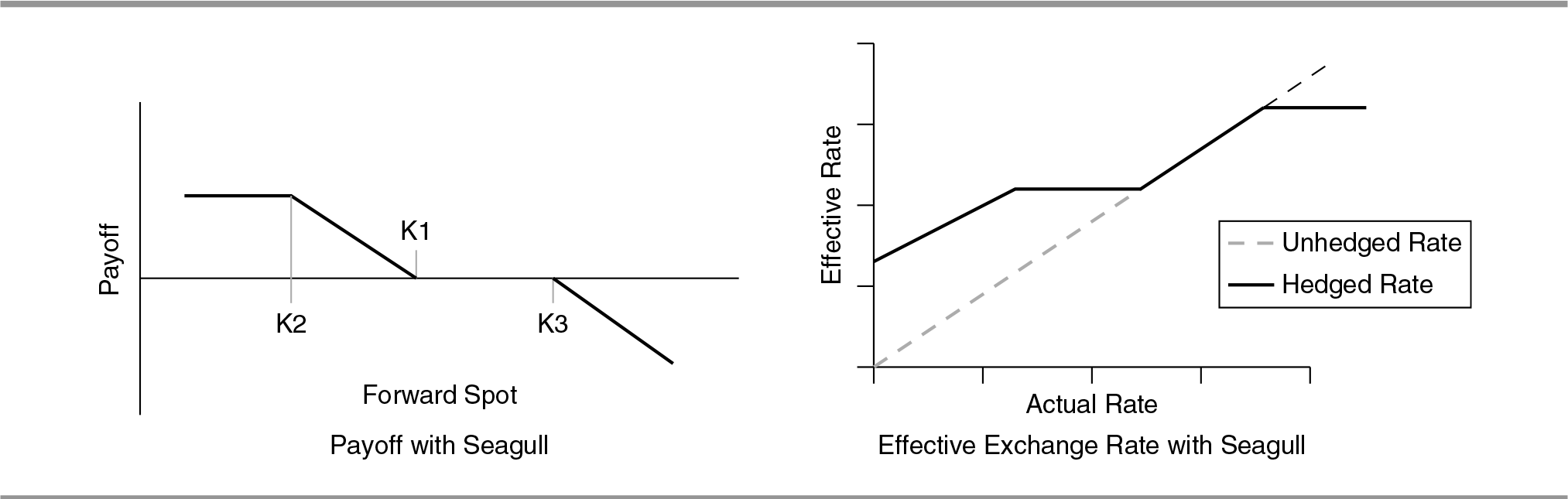

Seagull

Strategy Term: Seagull

Strategy Description: Seagull involves execution of the strategy using three options at a time, i.e., purchase of put/ call, sale of put/call and sale of call/put option at different strikes, to lock in the future exchange rate with limited upward participation and capped payoff.

Strategy Application: There can be two structures:

- Importer seagull

- Exporter seagull

Example

Structures are explained as follows taking the example of an exporter seagull.

In the exporter seagull,

- The option buyer will buy GBP put option at a pre-determined GBP/USD exchange rate (K1, 1.5650 here).

- Sell GBP put option at a pre-determined GBP/USD exchange rate (K2, 1.5450 here).

- Also sell a GBP call at a pre-determined GBP/USD exchange rate (K3, 1.5800 here).

- K1 will be higher than K2 and K3 will be higher than K1 in this case.

Through this deal, at maturity, the option buyer will have an option to sell the following:

- GBP at market rate + (K1- K2), if spot market rate is below K2.

- GBP at K1 if market rate is between K2 and K1.

- GBP at spot market rate if market rate is between K1 and K3.

- GBP at K3 if market rate is above K3.

In case GBP appreciates up to or below K3, the option buyer can choose not to exercise the option and can sell GBP at the prevailing spot rate and avail of the benefit due to GBP appreciation.

However, this benefit is limited as GBP appreciates further above K3. The sell GBP call will lead to a negative payoff.

In case, GBP depreciates beyond K2, the sell GBP put will lead to negative payoff, which will be offset by positive payoff from buy GBP put resulting in a capped payoff.

Payoff: Option with strike K1 and K2 and K3.

At maturity:

| ■ If Spot < K2, | then payoff is (K1 – Spot) + (Spot – K2). |

| ■ If K2 = < Spot = < K1, | then payoff is (K1 – Spot). |

| ■ If K1 < Spot = < K3, | then payoff is 0. |

| ■ If Spot > K3, | then payoff is (K3 – Spot) (Negative). |

Building Blocks

- Spot 1.5650 Forward 1.56493.

- Buy 1 M GBP/USD put @ 1.5650 (K1).

- Sell 1 M GBP/USD put @ 1.5450 (K2).

- Sell 1 M GBP/USD call @ 1.5800 (K3).

| Month end rate | Option buyer sells GBP at |

|---|---|

| < 1.5450 (K2) | Market Rate + 0.20 |

| => 1.5450 (K2) & =< 1.5650 (K1) | 1.5650 |

| > 1.5650 (K1) and =< 1.5800 (K3) | Market Rate |

| > 1.5800 (K3) | 1.5800 |

Graph 7.4

Pros

- It gives a better strike to buy/sell currency than range forward due of capped upside.

- Option buyer gets better rate to buy/sell currency in case of unfavourable movement. In this example, he can sell GBP at market rate + 0.20.

- Option buyer can avail of limited benefit of GBP appreciation also.

Risks Involved

- Payoff is capped when GBP depreciates below the sell put strike.

- Negative payoff, in case the GBP appreciates above sell call price.

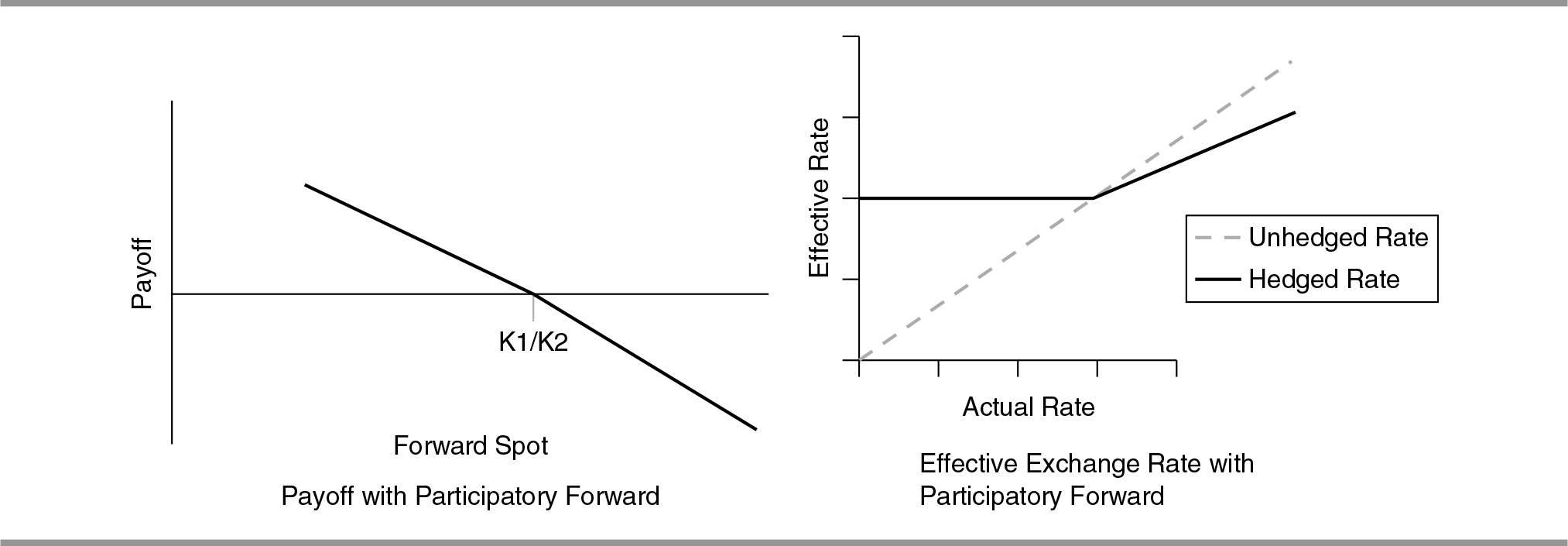

Participatory Forward

Strategy Term: Participatory Forward

Strategy Description: Participatory forward has limited participation in favourable market movement as compared to forward which does not allow any participation. This strategy involves execution of two options.

Example

Purchase of a put/call and sale of 0.5 call/put options at the same strike, to lock in future exchange rate, with limited upward participation. The ratio in which options are bought and sold can vary, for example, one can purchase a put/call for ‘x’ notional and sell call/put option for x/2, x/3, x/4 notional.

Strategy Application

- In participatory forward, the option buyer has benefit of participating in favourable movement.

- In this example, option buyer will buy GBP put option at a pre-determined GBP/USD exchange rate (K1, 1.5850 here).

- Sell 0.5 GBP call option at a pre-determined GBP/USD exchange rate (K2, 1.5850 here).

- K1 and K2 are same in this case.

- Through this deal, at maturity, the option buyer will have an option/obligation to sell GBP at K1/K2, and will receive a fixed amount of dollars.

In case the GBP appreciates, i.e., > K1/K2, the option buyer will have a flatter negative payoff than forward. Thus, worse lock in strike comes at the benefit of a flatter negative payoff than forward, i.e., participation in GBP appreciation.

Payoff: Option with Strike K1 and K2.

At maturity:

| ■ If Spot = < K1/K2, | then payoff is (K1/K2 – Spot). |

| ■ If Spot > K1/K2, | then payoff is (K1/K2 – Spot) (Negative) for half the notional. |

Building Blocks

- Spot 1.5713 Forward 1.57125.

- Buy 1 M GBP/USD put @ 1.5850 (K1).

- Sell 1 M GBP/USD call @ 1.5850 (K2) (0.5 the original notional).

| Month end rate | Option buyer sells GBP at |

|---|---|

| =< 1.5850 (K1/K2) | 1.5850 |

| > 1.5850 (K1/K2) | 1.5850 + 0.5 X (Market Rate − 1.5850) |

Graph 7.5

Pros

- Option buyer is protected from any unfavourable currency movement. In the given example, the worst case is a known rate of 1.5850 to sell GBP.

- Option buyer can avail of limited benefit of favourable currency movement also.

Risks Involved: In the given example, risk would be limited to half the notional in case of GBP appreciation.

- In case the structure was ‘zero cost’ then the strike would be worse than forward.

- In case the structure was premium paid then the risk would be limited to the extent of premium paid.

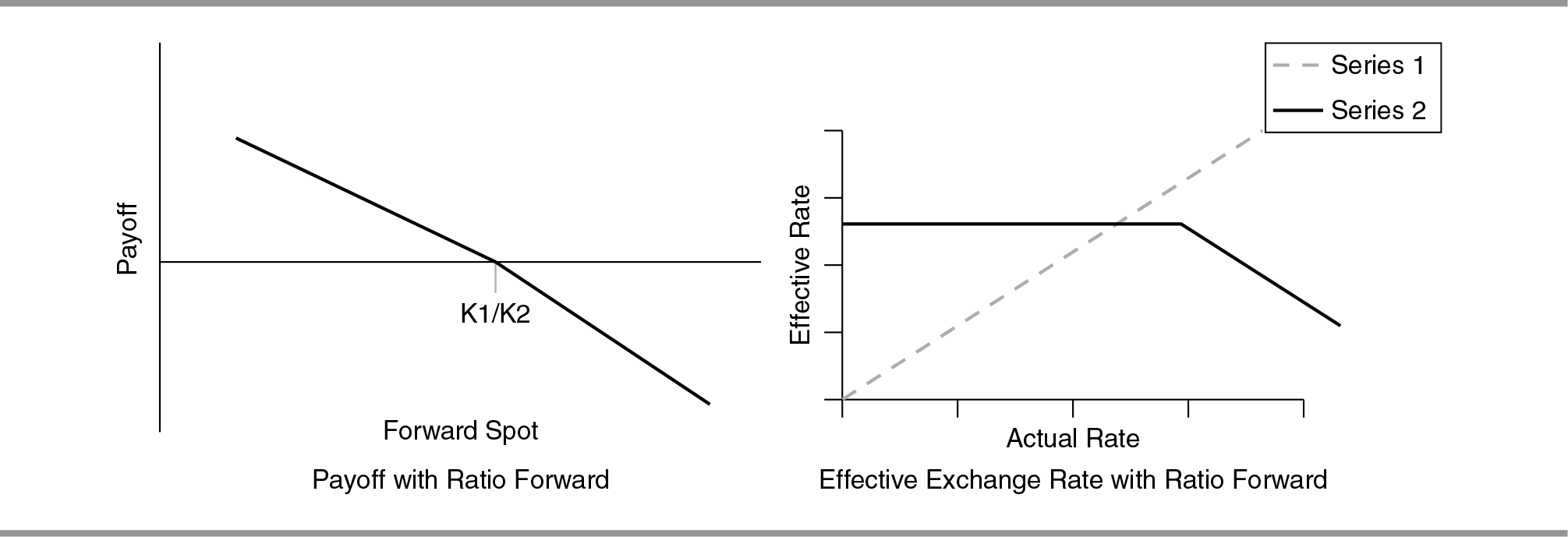

Ratio Forward

Strategy Term: Ratio forward

Strategy Description: A ratio forward is a ‘leveraged structure’ and it provides better strike than forward. The benefit comes at the increased risk of steeper negative payoff. It involves executing three options at a time. They are as follows:

- Simultaneous purchase of a put/call.

- Sale of two or more call/put options at the same strike to lock in future exchange rate with no upward participation and steeper downward risk.

- The option buyer gets better strike than a plain forward because of leverage.

Strategy Application:

- The option buyer will buy GBP put option at a pre-determined GBP/USD exchange rate (K1, 1.5846 here).

- Sell two GBP call options at a pre-determined GBP/USD exchange rate (K2, 1.5846 here).

- K1 and K2 are same in this case.

- Through this deal, at maturity, the option buyer will have an option/obligation to sell GBP at K1/K2, and will receive a fixed amount of dollars.

In case the GBP appreciates, i.e., GBP is > K1/K2, the option buyer will have steeper negative payoff. Thus, better lock in strike comes at increased risk of steeper negative payoff, than forward.

Payoff: Option with Strike K1 and K2.

At maturity:

| ■ If Spot = < K1/K2, | then payoff (K1/K2 – Spot). |

| ■ If Spot > K1/K2, | then payoff (K1/K2 – Spot) (Negative) for double the notional. |

Building Blocks

- Spot 1.5715 Forward 1.57130.

- Buy 1 M GBP/USD put @ 1.5846 (K1).

- Sell 1 M GBP/USD call @ 1.5846 (K2) (Double the notional).

| Month end rate | Option buyer sells GBP at |

|---|---|

| =< 1.5846 (K1/K2) | 1.58460 |

| > 1.5846 (K1/K2) | 1.5846 − (Market Rate − 1.5846) |

Graph 7.6

- Option buyer can get better strike to sell/buy currency than forward.

Risks Involved

- There is an increased risk of steeper negative payoff in case of unfavourable currency movement.

- In the example, if GBP appreciates above 1.5846, option buyer will have steeper negative payoff.

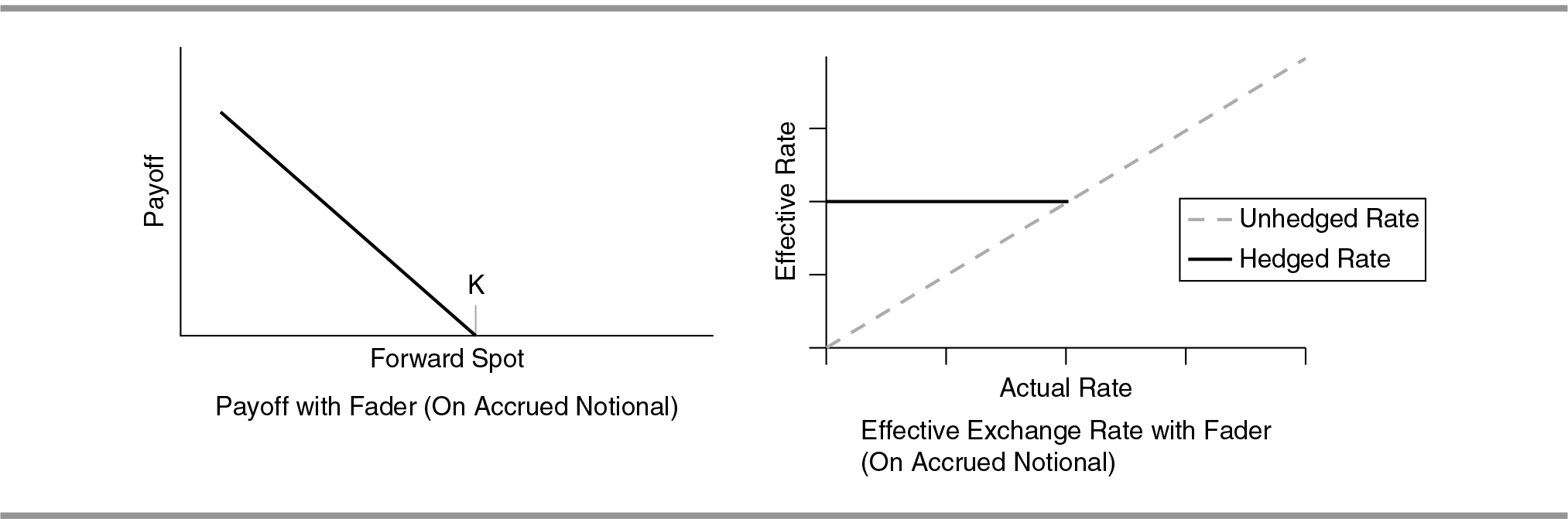

Fader

Strategy Term: Fader

Strategy Description: It is an accrual-based Vanilla option in which a notional value is accrued when the fixing settles above/below a particular level. Accrued notional = Notional × (fixing above/below a particular level)/N, where N is total number of fixings. The structure is cheaper than a Vanilla option.

Fixing refers to an exchange rate determined by an external agent or dealer being an exchange rate prevailing at a pre-determined time of the day, for example, Reuters TKFE 1500 fixing is determined by Reuters and refers to the rate prevailing for various currencies at 15:00 Tokyo time.

The fixing being observed for accrual could be daily, weekly and monthly.

Strategy Application: In Fader, the option buyer will buy GBP put Fader Option at a pre-determined GBP/USD exchange rate (K, 1.5722 here). The notional value will accrue when the fixing is below a particular level (K1, 1.5512 here). Through this deal, at maturity, the option buyer will have an option to sell accrued GBP notional at K, and will receive a fixed amount of dollars.

Payoff: Option with Strike K.

At maturity:

For accrued notional

| ■ If Spot = < K, | then (K – Spot). |

| ■ If Spot > K, | then 0. |

Building Blocks

- Spot 1.5719 Forward 1.57185.

- Buy 1 M GBP/USD put @ 1.5722 (K).

- Notional accumulation if GBP/USD fixing < 1.5512 (K1).

| Month end rate | Option buyer sells GBP at |

|---|---|

| =< 1.5722 (K) | 1.5722 |

| > 1.5722 (K) | Market Rate |

Graph 7.7

Pros

- The option buyer has the right to buy/sell a currency at strike even if currency moves in unfavourable direction. In this example, the worst case known rate is 1.5722.

- It is cheaper than Vanilla option due to partial accrual of notional.

Risks Involved

- The exposure is not fully hedged in case of partial accrual.

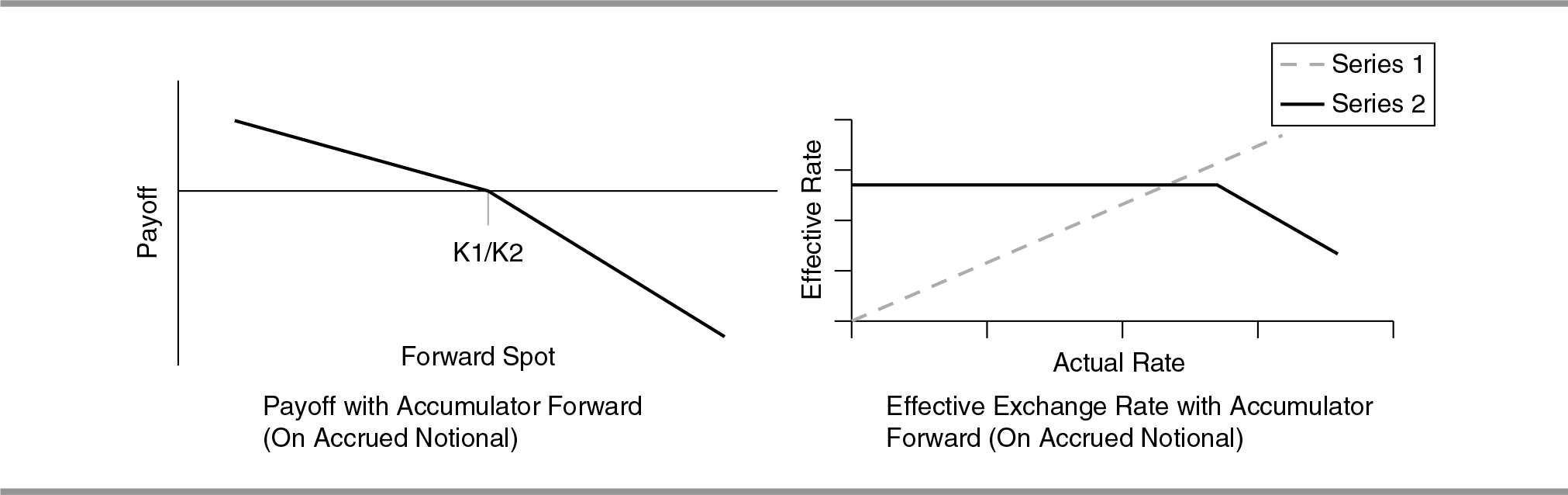

Accumulator Ratio Forward

Strategy Term: Accumulator Ratio Forward

Strategy Description: The structure provides better strike than ratio forward as the notional is not set on a single trade date but accrued based on the fixing.

where, N is the total number of fixings.

It involves execution of the following three options at a time:

- Simultaneous purchase of a put.

- Sale of two call options at the same strike to lock in future exchange rate with no upward participation.

- The notional is set as per the above formula.

Strategy Application: In an accumulator ratio forward, the option buyer will:

- Buy GBP put option at a pre-determined GBP/USD exchange rate (K1, 1.5734 here).

- Sell two GBP call options at a pre-determined GBP/USD exchange rate (K2, 1.5734 here).

- K1 and K2 are the same in this case.

- Through this deal, on every fixing, notional will get accrued if GBP/USD settles below a particular level (K3, 1.5612 here).

- In case, the GBP appreciates beyond K3, no notional will accrue to the contract holder.

- At the expiry, the option buyer will have an option/obligation to sell the accrued GBP notional at K1/K2, and will receive a fixed amount of dollars.

Payoff: Option with Strike K1 and K2.

At expiry:

On accrued notional

| ■ If Spot = < K1/K2, | then payoff is (K1/K2 – Spot). |

| ■ If Spot > K1/K2, | then payoff is (K1/K2 – Spot) (Negative). |

Building Blocks

- Spot 1.5719 Forward 1.57185.

- Buy 1 M GBP/USD put @ 1.5734 (K1).

- Sell 1 M GBP/USD call @ 1.5734 (K2). (Double the notional)

- Notional accumulation if GBP/USD fixing < 1.5612 (K3).

| Month end rate | Option buyer sells GBP at |

|---|---|

| > 1.5734 (K1/K2) | 1.5734 |

| =< 1.5734 (K1/K2) | 1.5734 − (Market Rate − 1.5734) |

Graph 7.8

Pros: Option buyer can get better strike than ratio forward.

Risks Involved

- It does not hedge the entire exposure in case of partial accrual.

- There is an increased risk of steeper negative payoff in case of GBP appreciation above 1.5734.

Variations: Accumulator ratio forward can be entered into at daily/weekly/monthly/yearly fixings.

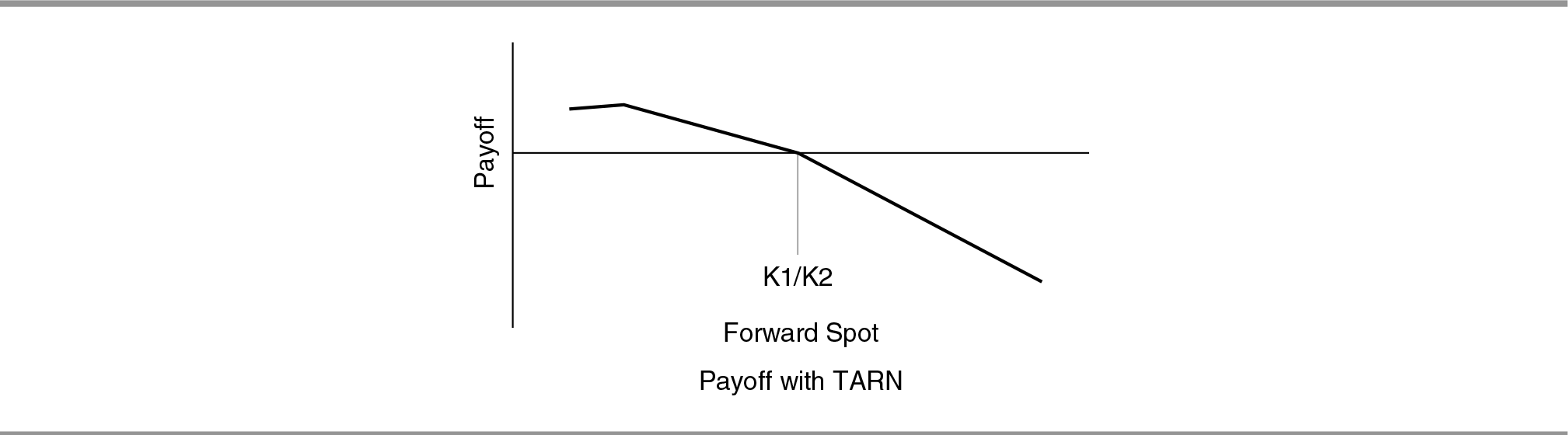

Target Redemption Notes (TARN)

Strategy Term: Target Redemption Notes (TARN)

Strategy Description: The structure provides a better strike than ratio forward, as the payoff is capped. It involves execution of the following three options at a time:

- Simultaneous purchase of a put (call).

- Sale of one or more call (put) options at same strike to lock in future exchange rate with limited upward participation.

- At a pre-determined payoff (gain) level the structure knocks out.

Strategy Application:

- The option buyer will buy GBP put option at a pre-determined GBP/USD exchange rate (K1, 1.5813 here).

- Sell two GBP call options at a pre-determined GBP/USD exchange rate (K2, 1.5813 here).

- K1 and K2 are same in this case.

- Through this deal, each month, the option buyer will have an option/obligation to sell GBP at K1/K2, and will receive a fixed amount of dollars.

- In case, the GBP appreciates beyond K1/K2, the option buyer will have a steeper negative payoff.

- Thus, better lock in strike comes at an increased risk of steeper negative payoff.

- In case the GBP depreciates and the pre-determined payoff level is touched, the structure will knock out.

Payoff: Option with Strike K1 and K2.

At maturity:

| ■ If Spot < K1/K2, | then payoff is (K1/K2 – Spot). |

| ■ If Spot > K1/K2, | then payoff is (K1/K2 – Spot) (Negative). |

Structure knocks out as pre-determined level of payoff is reached.

Building Blocks

- Spot 1.5720; Forward 1.5760.

- Buy 1 mio GBP/USD put @ 1.5813 (K1).

- Sell 1 mio GBP/USD call @ 1.5813 (K2). (Double the notional)

- Payoff level is capped @ 10,000 USD.

| Month end rate | Option buyer sells GBP at |

|---|---|

| = < 1.5813 (K1/K2) | 1.5813 |

| > 1.5813 (K1/K2) | 1.5813 − (Market Rate − 1.5813) |

Structure knocks out as pre-determined level of payoff is reached.

Graph 7.9

Pros: Option buyer can get better strike than ratio forward.

Risks Involved

- There is an increased risk of steeper negative payoff.

- The payoff is capped.

BARRIER OPTION

Barrier options are similar to the Vanilla option but with added set of ‘barriers’. Some of the barriers are given below.

- Knock-In (KI): The option comes into existence when KI level is touched.

- Knock-Out (KO): The option ceases to exist when KO level is touched.

- Knock-In Knock-Out (KIKO): Combination of both.

Barriers can increase/reduce the risk in a zero cost option and also reduce the cost of buying an option.

The barriers can be ‘In the money’, ‘Out of the money’ or both.

The barriers can be:

- American barriers: A barrier which is continuously observed.

- European barriers: A barrier which is observed only at expiry.

- Partial/Window barriers: A barrier which is observed during a particular period in the life of the option, i.e., it has a beginning date and time and ending date and time.

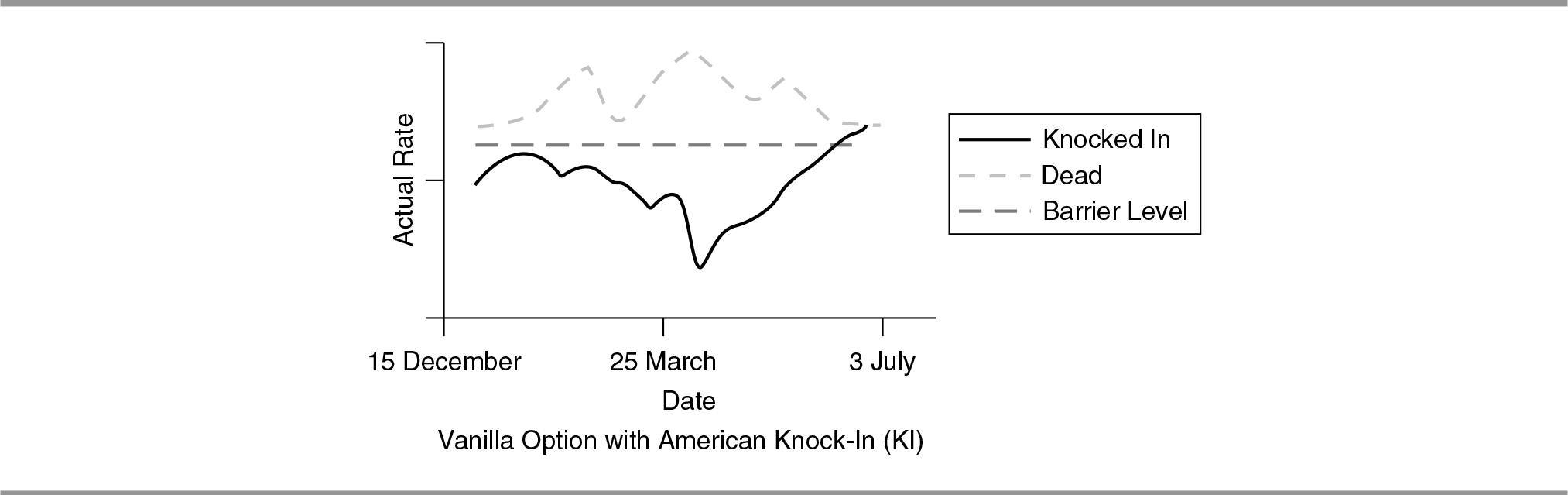

Vanilla Option with Knock-In (KI) (American)

Strategy Term: Vanilla option with Knock-In (KI) (American)

Strategy Description: It is similar to the Vanilla option in which the option holder locks in future exchange rate. The difference is that the option comes into existence only if the KI level is touched during the tenure of the option. KI level could be either ‘in the money’ or ‘out of the money’.

Strategy Application: In Vanilla option with KI, the option buyer buys/sells an option at a pre-determined exchange rate K (1.5650 in the example). The option will come into existence only if KI (1.5800 in the example) level is touched during the tenure of the option.

Premium of the option depends on the following:

- Probability of the KI event which in turn depends on:

- Volatility

- The difference between current spot and KI trigger

- The strike of the option, which comes into force if KI happens.

Payoff: Option with Strike K.

If KI level is touched:

At maturity:

| If Spot = < K, | then payoff is (K – Spot). |

| If Spot > K, | then payoff is 0. |

If KI level is not touched, option does not exist.

Building Blocks

- Spot 1.5650.

- Buy 1 M GBP/USD put @ 1.5650 (K) AKI 1.5800.

Graph 7.10

- If the KI level is touched, the worst-case rate for option buyer is known as strike of the option (1.5650 here).

- If the KI level is touched, the option buyer is protected in case of adverse movements in the underlying currency, i.e., option buyer is protected against the following:

- Depreciation in case he has bought put option

- Appreciation in case he has bought call option (if GBP depreciates below 1.5650 here).

- If the KI level is touched, the option buyer can avail of complete benefit of the favourable movement of underlying (appreciation of the GBP here).

- Lower cost than Vanilla option of the same strike.

Risks Involved

- If the KI level is not touched, the exposure is un-hedged.

- If KI level is not touched, the option premium paid goes waste as the option is not in force for the option buyer.

Variations

- European KI can be entered, which will be ‘Up and In’ on the expiry, i.e., If GBP/USD level crosses the KI trigger at the expiry, the option comes into existence.

- Partial KI can be entered, which will be observed for a particular period which is during the life of the option, i.e., if GBP/USD level crosses the KI trigger during the window, the option comes into existence.

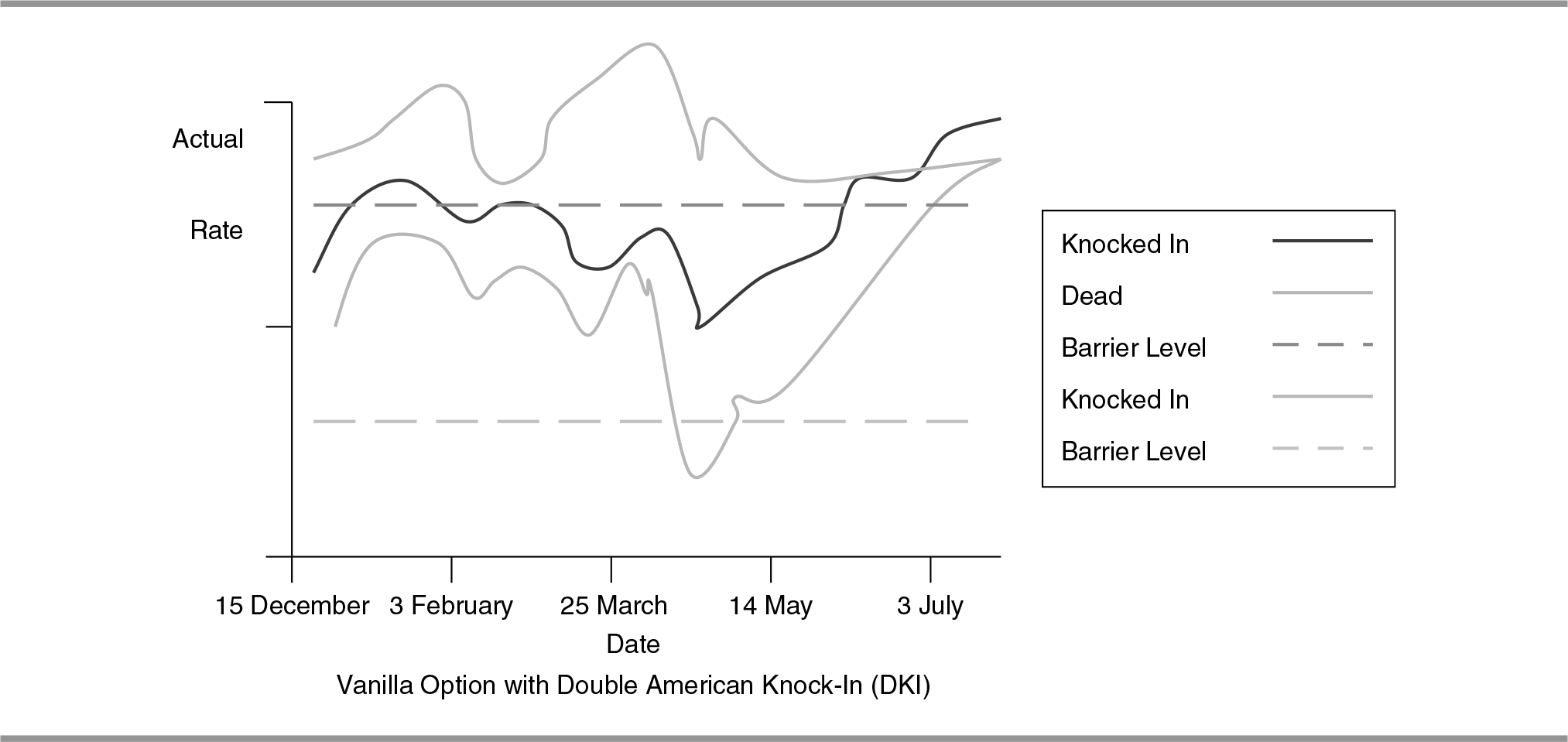

Vanilla Option with Double Knock-In (DKI) (American)

Strategy Term: Vanilla Option with Double Knock-In (DKI) (American)

Strategy Description: It is similar to the Vanilla option in which the option buyer locks in future exchange rate. The option comes into existence only if either of the two KI levels is touched during the tenure of the option. One KI level is above the underlying spot and the other is below.

Strategy Application: In vanilla option with double KI, the option buyer buys/sells an option at a pre-determined exchange rate (K, 1.5650 in the example). The option will come into existence only if either of the two KI (1.5450, 1.5850 in the example) level is traded during the tenure of the option.

Premium of the option depends on the following:

- Probability of the KI event which in turn depends on the following:

- Volatility

- The difference between current spot and KI trigger

- The strike of the option, which will come into force if KI happens.

If either of the two KI levels is touched:

At maturity:

| If Spot = < K, | then payoff is (K – Spot). |

| If Spot > K, | then payoff is 0. |

If either of the two KI levels is not touched:

Option does not exist.

Building Blocks

- Spot 1.52.

- Buy 1 M GBP/USD put @ 1.5650 (K) DKI levels at 1.5850 and 1.5450.

Graph 7.11

Pros

- If either of the two KI levels is touched, the worst-case rate for option buyer is the strike of the option (1.5650 here).

- If either of the two KI levels is touched, the option buyer is saved in case of adverse movements in the underlying currency, i.e., option buyer is protected against depreciation in case he has bought put option and appreciation in case he has bought call option (if GBP depreciates below 1.5650 here).

- If either of the two KI levels is touched, the option buyer can avail of complete benefit of the favourable movement of the underlying (appreciation of the GBP here).

- Lower cost than Vanilla option of the same strike.

Risks Involved

- If neither of the two KI levels is touched, the exposure is un-hedged.

- If neither of the two KI levels is touched, the option premium paid is waste as the option is not in force for the option buyer.

Variations

- European KI can be entered, which will be ‘Up and In’ or ‘Down and In’ on the expiry, i.e., If GBP/USD level crosses either of the two KI triggers at the expiry, the option comes into existence.

- Partial KI can be entered into which will be observed during a particular period during the life of the option, i.e., if GBP/USD level crosses either of the two KI triggers during the window, the option comes into existence.

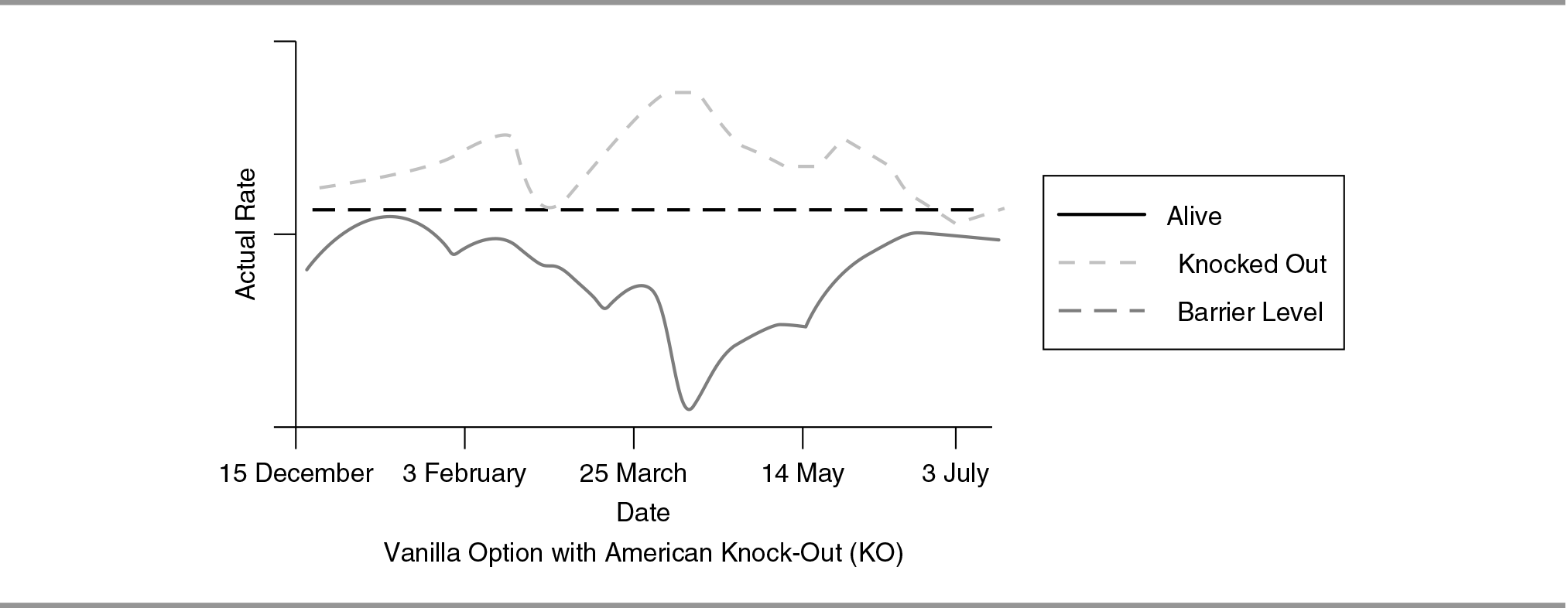

Vanilla Option with Knock-Out (KO) (American)

Strategy Term: Vanilla option with Knock-Out (KO) (American)

Strategy Description: It is similar to the Vanilla option in which the option buyer locks in future exchange rate. The difference is that the option ceases to exist if the KO level is touched during the tenure of the option. KO level could be either ‘Out of the money’ level or ‘In the money’ level.

Strategy Application: In Vanilla option with KO, the option buyer buys/sells GBP at a pre-determined exchange rate (K, 1.5650 in the example). The option will cease to exist if KO level (1.5850 in the example) is touched during the tenure of the option.

Premium of the option depends on the following:

- Probability of the KO event which in turn depends on:

- Volatility

- The difference between current spot and KO trigger

- The strike of the option, which will come into force if KI happens.

Payoff: Option with Strike K.

If KO level is not touched:

At maturity:

| If Spot = < K, | hen payoff is (K – Spot). |

| t If Spot > K, | then payoff is 0. |

If KO level is touched:

Option does not exist.

Building Blocks

- Spot 1.52.

- Buy 1 M GBP/USD put @ 1.5650 (K).

- American KO trigger: 1.5850.

Graph 7.12

Pros

- If the KO level is not touched, the worst-case rate for option buyer is strike of the option (1.5650 here).

- If the KO level is not touched, the option buyer is saved in case of adverse movements in the underlying currency, i.e., option buyer is protected against the following:

- If the KO level is not touched, the option buyer can avail of complete benefit of the favourable movement of the underlying (appreciation of the GBP here).

- Lower cost than Vanilla option of the same strike.

Risks Involved

- If the KO level is touched, the exposure is un-hedged.

- If KO level is touched, the option premium paid goes waste since the option cannot be exercised by the CH.

Variations

- European KO can be entered into which will be ‘Up and Out’ on the expiry, i.e., if GBP/USD level crosses the KO trigger at the expiry, the option ceases to exist.

- Partial KO can be entered into which will be observed during a particular period during the life of the option, i.e., If GBP/USD level crosses the KO trigger during the window, the option ceases to exist.

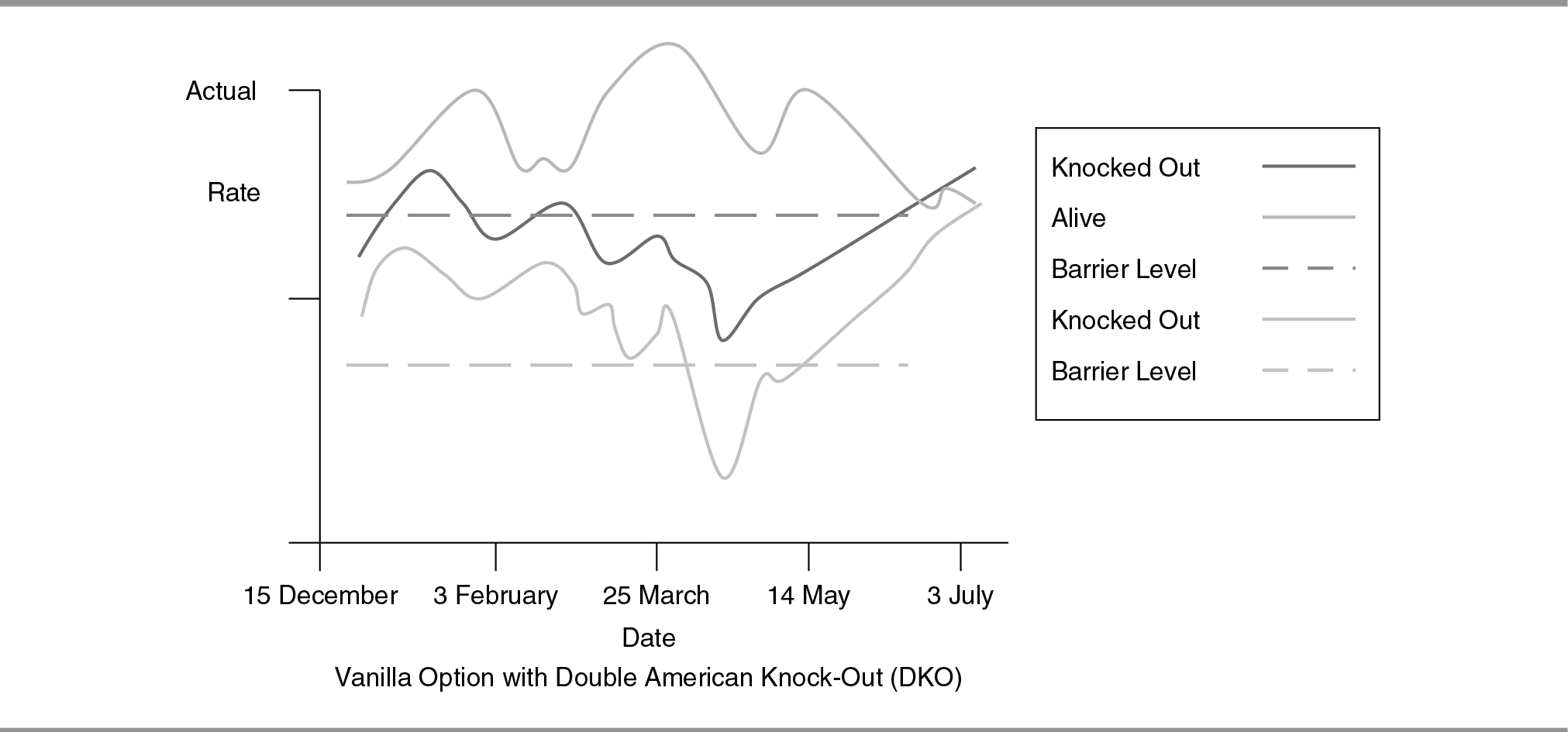

Vanilla Option with Double Knock-Out (DKO) (American)

Strategy Term: Vanilla Option with Double Knock-Out (DKO) (American)

Strategy Description: It is similar to the Vanilla option in which the option buyer locks in future exchange rate. The option ceases to exist if either of the two KO levels is touched during the tenure of the option. One KO level is above the underlying spot and the other is below.

Strategy Application: In vanilla option with double KO, the option buyer buys/sells GBP at a pre-determined exchange rate (K, 1.5650 in the example). The option will cease to exist if either of the two KO (1.5450, 1.5850 in the example) levels is touched during the tenure of the option.

Premium of the option depends on the following:

- Probability of the KO event which in turn depends on the following:

- Volatility

- The difference between current spot and KO triggers

- The strike of the option, which will come into force if KO takes place.

Payoff: Option with Strike K.

If neither of the two KO levels is not touched:

At maturity:

| If Spot = < K, | then payoff is (K – Spot). |

| If Spot > K, | then payoff is 0. |

If either of the two KO levels is touched:

Option does not exist.

Building Blocks

- Spot 1.5650.

- Buy 1 M GBP/USD put @ 1.5650 (K).

- DKO 1.5850 and 1.5450.

Graph 7.13

- If either of the two KO levels is not touched, the worst-case rate for option buyer is known at strike of the option (1.5650 here).

- If either of the two KO levels is not touched, the option buyer is saved in case of adverse movements in the underlying currency, i.e., option buyer is protected against depreciation in case he has bought put option and appreciation in case he has bought call option (if GBP depreciates below 1.5650 here).

- If either of the two KO levels is not touched, the option buyer can avail of complete benefit of the favourable movement of the underlying (appreciation of the GBP here).

- Lower cost than Vanilla option of the same strike.

Risks Involved

- If either of the KO levels is touched, the exposure is un-hedged.

- If either of the KO levels is touched, the option premium paid goes waste as the option cannot be exercised by the option buyer.

Variations

- European KO can be entered into which will be ‘Up and Out’ or ‘Down and Out’, on the expiry, i.e., if GBP/USD level crosses either of the two KO triggers at the expiry, the option ceases to exist.

- Partial KO can be entered into, which will be observed during a particular period, during the life of the option, i.e., if GBP/USD level crosses either of the two KO triggers during the window, the option ceases to exist.

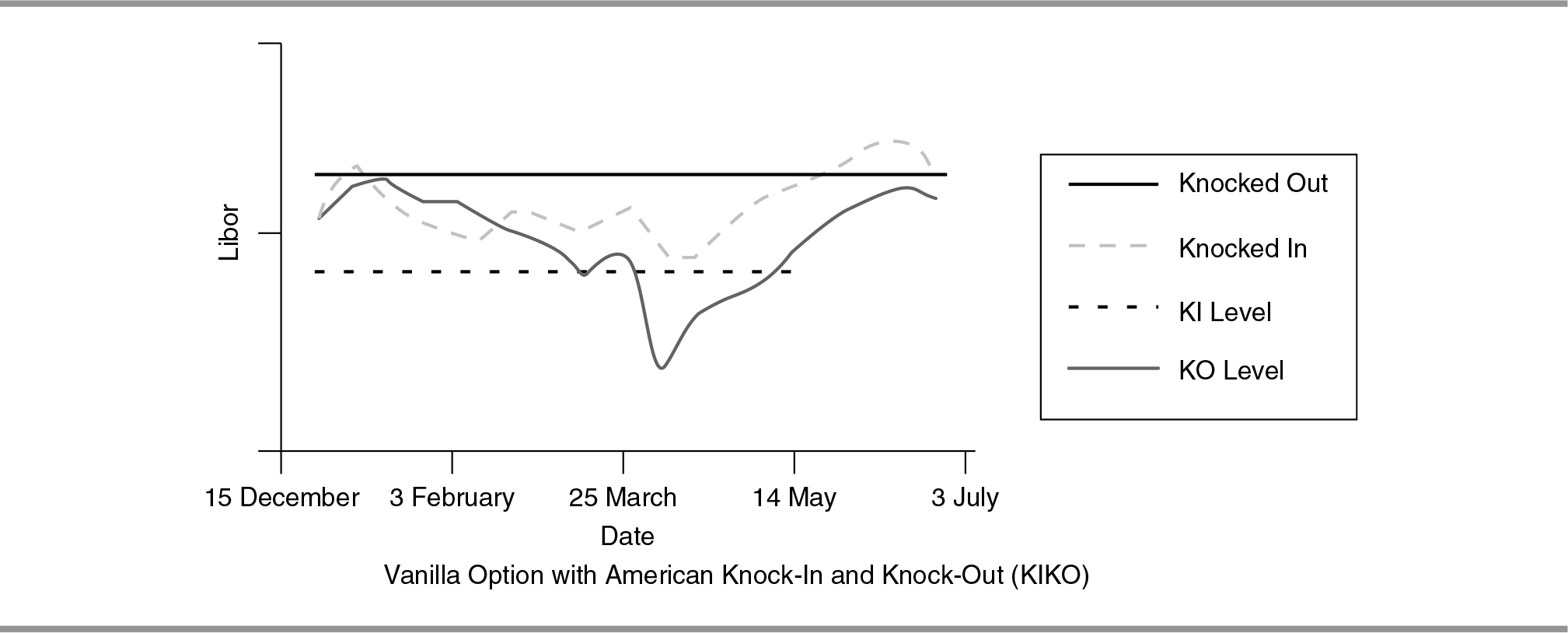

Vanilla Option with Knock-In and Knock-Out (KIKO) (American)

Strategy Term: Vanilla Option with Knock-In and Knock-Out (KIKO) (American)

Strategy Description: It is similar to Vanilla option to lock in future exchange rate. The option comes into existence only if the KI level is touched during the tenure of the option. The option ceases to exist if the KO level is touched during the tenure of the option. KI precedes KO. The two levels can be ‘above spot’ or ‘below spot’ or one above and the other below spot.

Strategy Application: In vanilla option with KIKO, the Option buyer buys/sells GBP at a pre-determined exchange rate (K, 1.5650 in the example).

- The option comes into force if KI level (1.5450 here) is touched.

- It will cease to exist if KO (1.5850 here) level is touched during the tenure of the option.

- Once the KO levels are touched, the option ceases to exist irrespective of the fact whether the KI levels are touched or not.

Premium of the option depends on the following:

- Probability of the KI/KO event which in turn depends on the following:

- Volatility

- The difference between current spot and KI/KO triggers

Payoff: Option with Strike K.

If KI level is touched and KO is not touched:

At maturity:

| If Spot < K, | then payoff is (K – Spot). |

| If Spot >= K, | then payoff is 0. |

If KI level is not touched:

Option does not exist.

If KI level is touched and KO is also touched:

Option ceases and does not exist.

Building Blocks

- Spot 1.5650.

- Buy 1 M GBP/USD put @ 1.5650 (K).

- KI 1.5450, KO 1.5850.

Graph 7.14

Pros

- If KI level is touched and KO level is not touched, the worst case rate for the option buyer is the strike of the option (1.5650 here).

- If KI level is touched and KO level is not touched, the option buyer is hedged against adverse movements of the underlying (GBP depreciates below 1.5650 here).

- IF KI level is touched and KO level is not touched, the option buyer can avail of the complete benefit of favourable underlying movement (GBP appreciation here).

- IF KI level is touched and KO level is not touched, the option buyer can avail of the complete benefit of favourable underlying movement (GBP appreciation here).

Risks Involved: If KI level is not touched, the exposure is un-hedged

Variations

- European KIKO can be entered into which will be ‘Down and In’ and ‘Up and Out’ on the expiry, i.e., if the GBP/ USD level crosses the KI trigger at the expiry, the option comes into existence and if GBP/USD level crosses the KO trigger at the expiry, the option ceases to exist.

- Partial KIKO can be entered into which will be observed during a particular period during the life of the option, i.e., if GBP/USD level crosses the KI trigger during the window, the option comes into existence and if GBP/USD level crosses the KO trigger during the window, the option ceases to exist.

DIGITALS

The option buyer receives a certain amount if the underlying asset crosses a pre-defined trigger else he does not receive anything.

- These structures are speculative in nature.

- They are added to other structures in case of KO or ‘Negative Payoff’ in order to give relief to the option buyer in the worst-case scenario.

Some variations of digitals are as follows:

- One touch (OT) digital leading to a certain payment if a level is touched.

- Double touch (DT) digital leading to lump sum payment if one of two levels is touched.

- Double must touch (DMT) digital leading to lump sum payment if both the levels are touched.

- No touch (NT) digital leading to lump sum payment if a level is not touched.

- Double no touch (DNT) digital leading to lump sum payment if both the levels are not touched.

Digitals can be as follows:

- American Digitals: A trigger which is continuously observed.

- European Digitals: A trigger which is observed only at expiry.

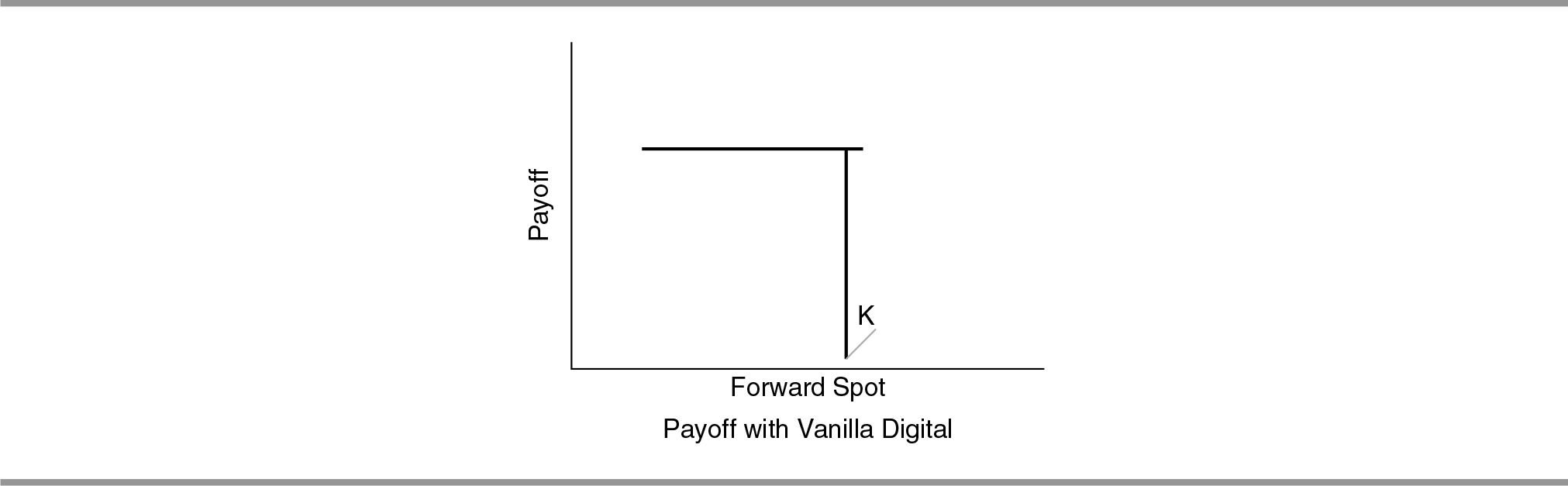

Vanilla Digital (European)

Strategy Term: Vanilla Digital (European)

Strategy Description: There is a certain payoff in case the future exchange rate breaks a particular level at expiry.

Strategy Application: In Vanilla digital, the option buyer will buy a Vanilla digital option at a pre-determined GBP/ USD exchange rate (K, 1.5800 here). Through this deal at expiry, the option buyer will receive a fixed amount of dollars, if GBP depreciates beyond the pre-determined GBP/USD exchange rate.

In case, the GBP appreciates, the option buyer does not receive anything. However, he will get more USDs for his GBP receivables. The premium depends on the forward fixing at, above or below the strike and volatility of the underlying product. Premium can also be approximated from delta of the Vanilla option at the same strike.

Payoff: One Touch with Strike K.

At maturity:

| If Spot < K, | then USD 10,000. |

| If K is not touched | then 0 |

Building Blocks

- Spot 1.5650.

- Buy 1 M GBP/USD digital @ 1.5800 (K).

Graph 7.15

Pros: Option buyer gets benefits in terms of certain payment, if the GBP depreciates below 1.5800.

Risks Involved: If the level is not touched, the premium is lost.

One Touch (OT) (American)

Strategy Term: One Touch (OT) (American)

Strategy Description: There is a certain payoff in case the future exchange rate touches a particular level at any time since inception of the option to expiry date of the option. The level can be above or below the spot.

Strategy Application: In OT, the option buyer will buy OT at pre-determined GBP/USD exchange rate (K, 1.5650 here). Through this deal, the option buyer will receive a fixed amount of payout such as USD if GBP/USD touches the pre-determined GBP/USD exchange rate.

The premium depends on the forward fixing

- At

- Above

- Below the strike and the volatility of the underlying.

Payoff: One Touch with Strike.

At maturity:

| If K is touched, | then USD 10,000. |

| If K is not touched, | then 0. |

Building Blocks

- Spot 1.5720.

- Buy 1 M GBP/USD OT @ 1.5650 (K).

Pros: Option buyer gets benefit in terms of certain payment, if the GBP depreciates below 1.5650.

Risks Involved: If the level is not touched, the premium is lost.

Double One Touch (DOT) (American)

Strategy Term: Double One Touch (DOT) (American)

Strategy Description: There is a lump sum payoff in case the future exchange rate touches one of the two pre-determined levels at any time since inception of the option to expiry date of the option. The levels can be above the spot or below the spot or one above and one below the spot.

Strategy Application: In DOT, the option buyer will buy DOT at pre-determined GBP/USD exchange rates. (Here K1 is 1.5500 and K2 is 1.5850). The option buyer will receive a fixed payout, for example, USD if GBP/USD exchange rate touches either of the two pre-determined GBP/USD exchange rates.

The premium depends on the forward fixing

- At

- Above

- Below the strikes and volatility of the underlying

Payoff: One Touch with Strike K.

At maturity:

| If K1 or K2 is touched, | then USD 10,000. |

| If K1 and K2 is not touched, | then 0. |

Building Blocks

- Spot 1.5720.

- Buy 1 M GBP/USD DOT @ 1.5500 (K1) and 1.5850 (K2).

Pros: The option buyer has benefit in terms of certain payment, if GBP depreciates beyond 1.5500 levels or appreciates above 1.5850.

Risks Involved: If one of the levels is not touched, the premium is lost.

Double Must Touch (DMT) (American)

Strategy Term: Double Must Touch (DMT) (American)

Strategy Description: There is a lump sum payoff, in case the future exchange rate touches both the two pre-determined levels at any time since inception of the option to expiry date of the option. The levels can be above the spot or below the spot or one above the spot and the other below the spot.

Strategy Application: In DMT, the option buyer will buy DMT at pre-determined GBP/USD exchange rates (K1, 1.5500 here and K2, 1.5950 here). Through this deal, the option buyer will receive a fixed amount of payout, for example, USD if GBP/USD touches both the pre-determined GBP/USD exchange rates.

The premium depends on the forward fixing

- At

- Above

- Below the strikes and the volatility of the underlying

Payoff: One Touch with Strike K.

At maturity:

| If K1 and K2 is touched, | then USD 10,000. |

| If K1 or K2 is not touched,, | then 0. |

Building Blocks

- Spot 1.5720.

- Buy 1 M GBP/USD DMT @ 1.5500 (K1) and 1.5950 (K2).

Pros: The option buyer gets benefit in terms of a certain payment, if the GBP rises to 1.5500 and subsequently falls to 1.5930.

Risks Involved: If both the levels are not touched, the premium is lost.

No Touch (NT) (American)

Strategy Term: No Touch (NT) (American)

Strategy Description: There is a lump sum payoff in case the future exchange rate does not touch a particular level till maturity. The level can be above or below the spot.

Strategy Application: In NT, the option buyer will buy NT at a pre-determined GBP/USD exchange rate (K, 1.50 here). Through this deal the option buyer will receive a fixed amount of payout, for example, USD GBP/USD does not touch the pre-determined GBP/USD exchange rate.

The premium depends on the forward fixing

- At

- Above

- Below the strike and volatility of the underlying

Payoff: One Touch with Strike K.

At maturity:

| If K is not touched, | then USD 1,000. |

| If K is touched, | then 0. |

Building Blocks

- Spot 1.5725.

- Buy 1 M GBP/USD NT @ 1.50 (K).

Pros: The option buyer gets benefit in terms of a certain payment, if the GBP does not appreciate to 1.50.

Risks Involved: If the level is touched, the premium is lost.

Double No Touch (DNT) (American)

Strategy Term: Double No Touch (DNT) (American)

Strategy Description: There is a lump sum payoff in case the future exchange rate does not touch both the two pre-determined levels till maturity. The levels can be above the spot or below the spot or one above the spot and the other below the spot.

Strategy Application: In DNT, the option buyer will buy DNT at pre-determined GBP/USD exchange rates (K1, 1.5850 and K2, 1.5950 here). Through this deal, every month, the option buyer will receive a fixed payout, for example, USD if GBP/USD does not touch both the pre-determined GBP/USD exchange rates.

The premium depends on the forward fixing

- At

- Above

- Below the strikes and volatility of the underlying

Payoff: One Touch with Strike K.

At maturity:

| If K1 and K2 are not touched, | then USD 10,000. |

| If K1 or K2 is touched, | then 0. |

Building Blocks

- Spot 1.5720.

- Buy 1 M GBP/USD DNT @ 1.5850 (K1) and 1.5950 (K2).

Pros: Option buyer gets benefit in terms of certain payment, if the GBP does not appreciate to 1.5850 and 1.5950.

Risks Involved: If one of the levels is touched, the premium is lost.

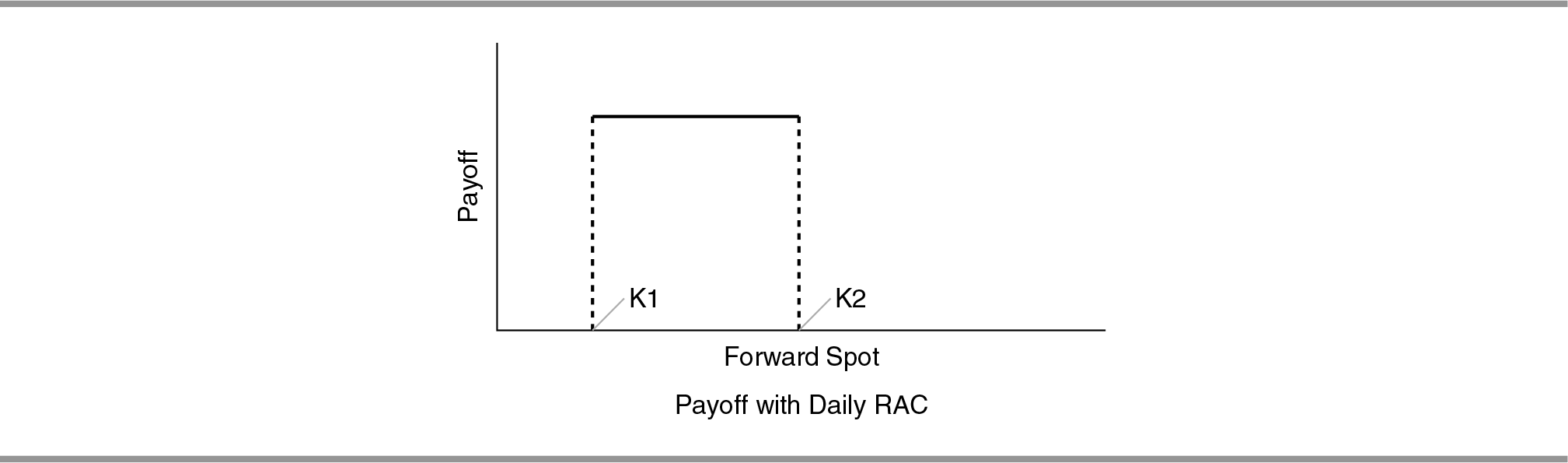

Daily Range Accrual (RAC)

Strategy Term: Daily Range Accrual (RAC)

Strategy Description: There is a lump sum payoff in case the daily exchange rate fixes within a particular range. It is a set of digital options.

Strategy Application: In daily RAC, the option buyer will buy daily RAC at pre-determined GBP/USD exchange rate range (Between K1, 1.5400 and K2, 1.5600 here). Through this deal, every day, the contract holder will receive a fixed amount of USD, if GBP/USD exchange rate fixes between the pre-defined ranges.

- In case, the GBP appreciates beyond the range, the option buyer does not receive anything; however, he will get more USD for his GBP receivables.

- In case, the GBP depreciates beyond the range, the option buyer does not receive anything, and the exposure is not hedged.

Payoff: Daily RAC with range between K1 and K2.

Each day:

| If K1= < Spot = < K2, | then USD 1,000. |

| If Spot < K1 and Spot > K2, | then 0. |

Building Blocks

- Spot 1.5725.

- Buy 1 M GBP/USD RAC @ 1.5400 (K1) and 1.5600 (K2).

Graph 7.16

Pros: The option buyer gets benefits in terms of certain payment, if the GBP depreciation is within 1.5400 and 1.5600.

Risks Involved: If GBP depreciates beyond the range, the option buyer does not get anything.

Variations

- Weekly/Monthly range accrual can be entered into.

- Partial range accrual can be entered into, in which, there is no more accrual once the range is broken.

MISCELLANEOUS ILLUSTRATIONS

Range Forward Strategy

QUESTION 1

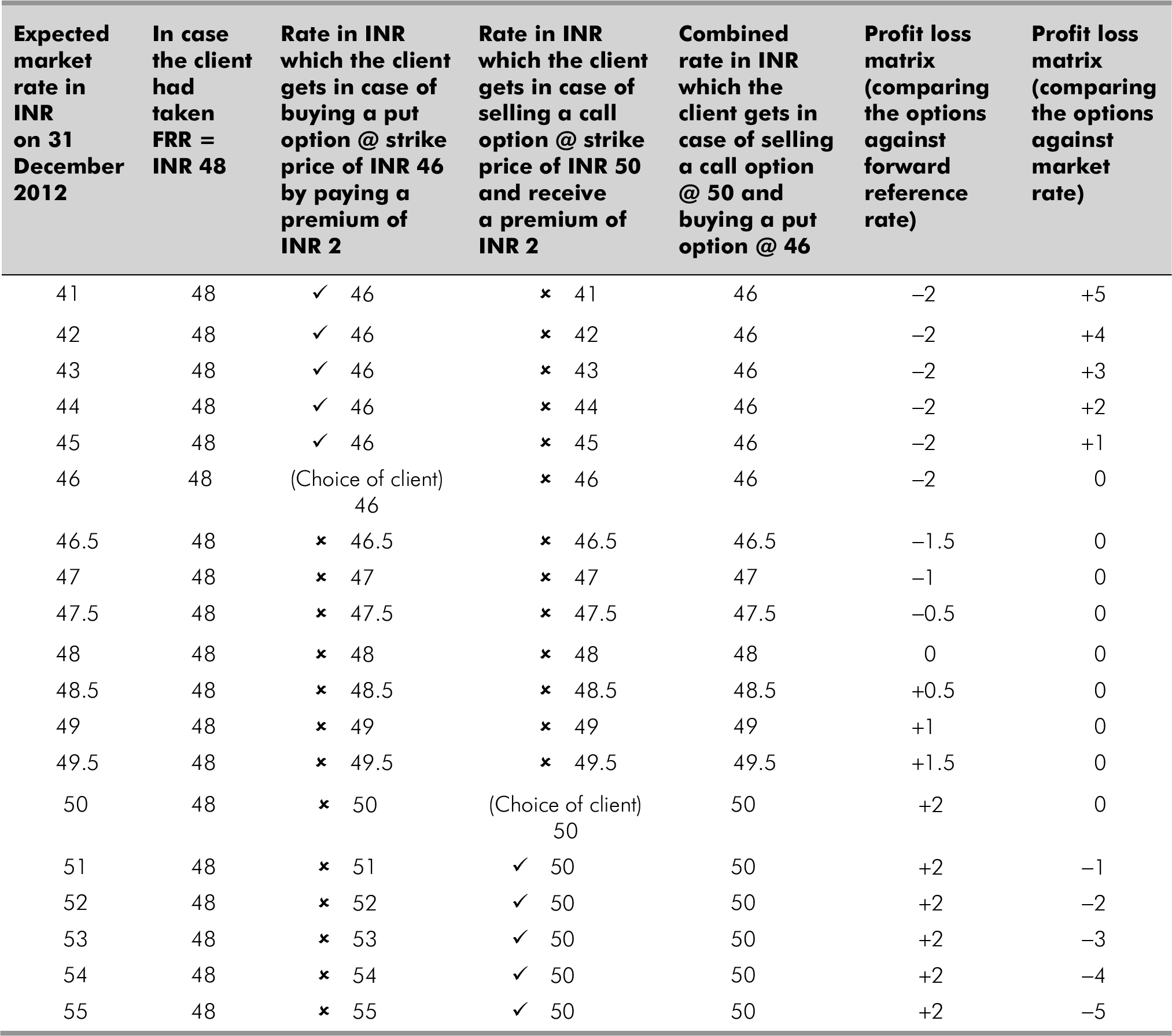

A client takes an option of Buy USD Put INR Call @ 46 by paying a premium of INR 2 and a Sell USD Call INR Put @ 50 by receiving a premium of INR 2 with FRR of INR 48 for maturity 31 December 2012. Answer the questions that follow.

- Who is the client?

Answer: The client is an exporter. Being an exporter he has to sell the underlying, buy put option is the right to sell and at the same time sell call option is the obligation to sell. Since, both the options are on sell side, the client is an Exporter.

- Is the strategy genuine?

Answer: Yes, the strategy seems to be a genuine strategy. Both the options taken by the client (i.e. Exporter) are on sell front, he seems to be a Genuine Exporter, so strategy taken is a genuine one.

- Is the option ATM/ITM/OTM?

Answer: The put option, whose strike price is 46, which is less than F RR, i.e., 48 is termed as OTM option at the time of taking/buying/holding/writing/selling the option.

The call option @ strike price of 50, which is more than FRR, i.e., 48 is termed as OTM option at the time of taking/ buying/holding/writing/selling the option.

Hence, both options are OTM.

- Develop the payoff matrix by comparing the strategy with (i) FRR and (ii) Market rate

Answer:

- Is the strategy zero cost?

Answer: Yes, the strategy is a zero cost strategy.

- What is the view of the client?

Answer: Since the client is a genuine player, his view would be considered looking at the pay off compared with FRR. Looking at this payoff we can conclude that, he has a range bound view of market to stay between 46 and 50. Also, he believes that USD/INR exchange rate could lie between 48 and 50 (beyond 50, the sell call option has limited his profit to INR 2). However, he is also apprehensive, that rupee might move in range of 46–48. Hence, he has taken this strategy to restrict his profit and loss without paying any premium on structure.

QUESTION 2

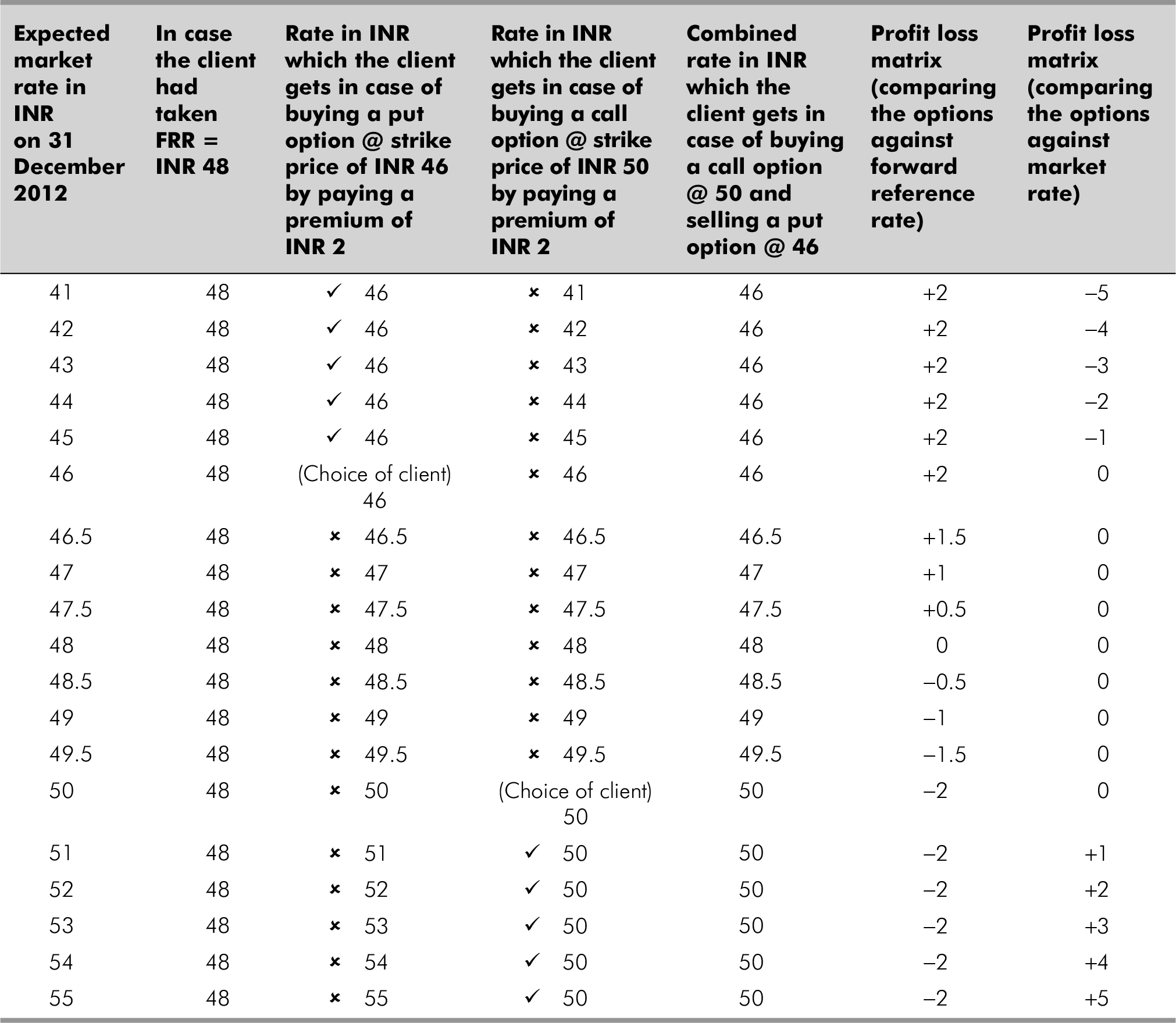

A client takes an option of Buy Call @ 50 by paying a premium of INR 2 and a Sell Put @ 46 by receiving a premium of INR 2 with FRR of INR 48 for maturity 31 December 2012. Answer the questions that follow.

- Who is the client?

Answer: The client is an importer. Being an importer, he has to buy the underlying, buy call option is the right to buy and at the same time sell put option is the obligation to buy. Since, both the options are on buy front, so the client is an Importer.

- Is the strategy genuine?

Answer: Yes, the strategy seems to be a genuine strategy. Both the options taken by the client (i.e. Importer) are on buy front, he seems to be a Genuine Importer, so the strategy taken is a genuine one.

- Is the option ATM/ITM/OTM?

Answer: For selling the put option @ strike price of 46 which is less than FRR, i.e., 48, such option is termed as OTM option at the time of taking/buying/holding/writing/selling the option.

For call option whose strike price is 50 which is more than FRR, i.e., 48, such option is termed as OTM option at the time of taking/buying/holding/writing/selling the option.

Hence, both options are OTM.

- Is the strategy zero cost?

Answer: Yes, the strategy is a zero cost strategy.

- What is the view of the client?

Answer: Since the client is a genuine player his view would be considered looking at the payoff compared with FRR. Looking at this payoff we can formulate, he has a range bound view between 46 and 50. He is more bearish on market fluctuating between 48 and 50 (beyond 46 the sell put option has limited his profit to INR 2) but is also apprehensive that rupee might move in the range of 46–48. Hence, he has taken this strategy to restrict his profit and loss without paying any premium on structure.

- Develop the payoff matrix by comparing the strategy with (i) FRR and (ii) Market rate

Answer:

- Is the view for short term or long term?

Answer: The strategy taken by the importer here indicates that he has opted for this option for a short term.

Range Extra Strategy

QUESTION 1

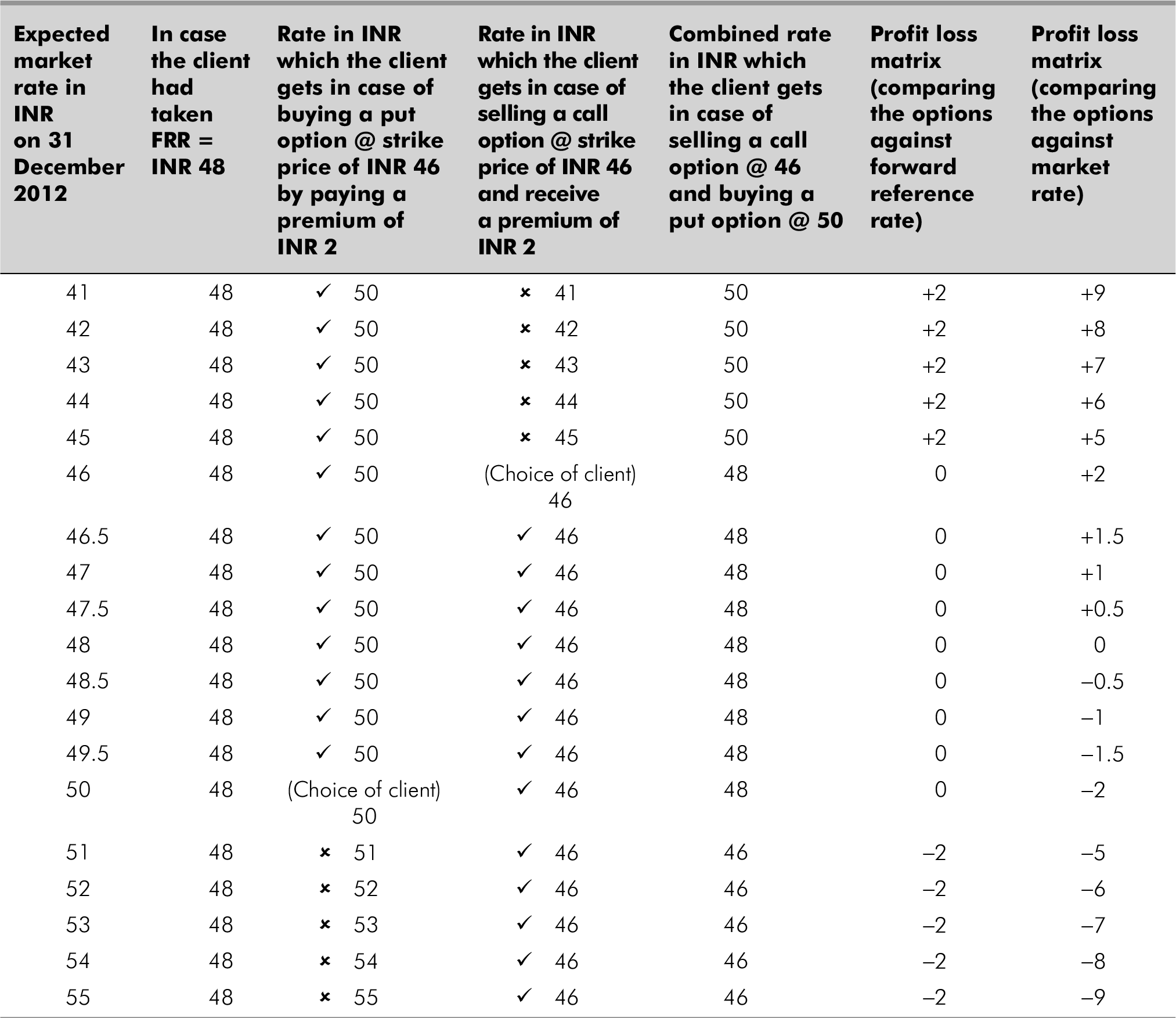

A client takes an option of buy put @ 50 by paying a premium of INR 2 and a sell call @ 46 by receiving a premium of INR 2 with FRR of INR 48 for maturity 31 December 2012. Answer the questions that follow.

- Who is the client?

Answer: The client is an exporter. Being an exporter he has to sell the underlying, buy put option is the right to sell and at the same time sell call option is the obligation to sell. Since, both the options are on sell front, so the client is an Exporter.

- Is the strategy genuine?

Answer: Yes, the strategy seems to be a genuine strategy. Both the options taken by the client (i.e. Exporter) are on sell front, he seems to be a Genuine Exporter. So the strategy taken is a genuine one.

- Is the option ATM/ITM/OTM?

Answer: For the put option whose strike price is 50 is more than FRR, i.e., 48, such option is termed as ITM option at the time of taking/buying/holding/writing/selling the option.

For selling the call option @ strike price of 46 which is less than FRR, such option is termed as ITM option at the time of taking/buying/holding/writing/selling the option.

Hence, both options are ITM.

- Develop the payoff matrix by comparing the strategy with (i) FRR and (ii) Market rate

Answer:

- Is the strategy zero cost?

Answer: Yes, the strategy is a zero cost strategy.

- What is the view of the client?

Answer: Since the client is a genuine player his view would be considered looking at the payoff compared with FRR. Looking at this payoff, we can formulate that the client is very much sure that INR will appreciate for which he wants to earn extra profit against forward. He is also aware that he might suffer extra loss for this strategy. Hence, it is known as range extra for an exporter.

- Is the view for short term or long term?

Answer: The strategy taken by the exporter here indicates that he has opted for this option for short term.

QUESTION 2

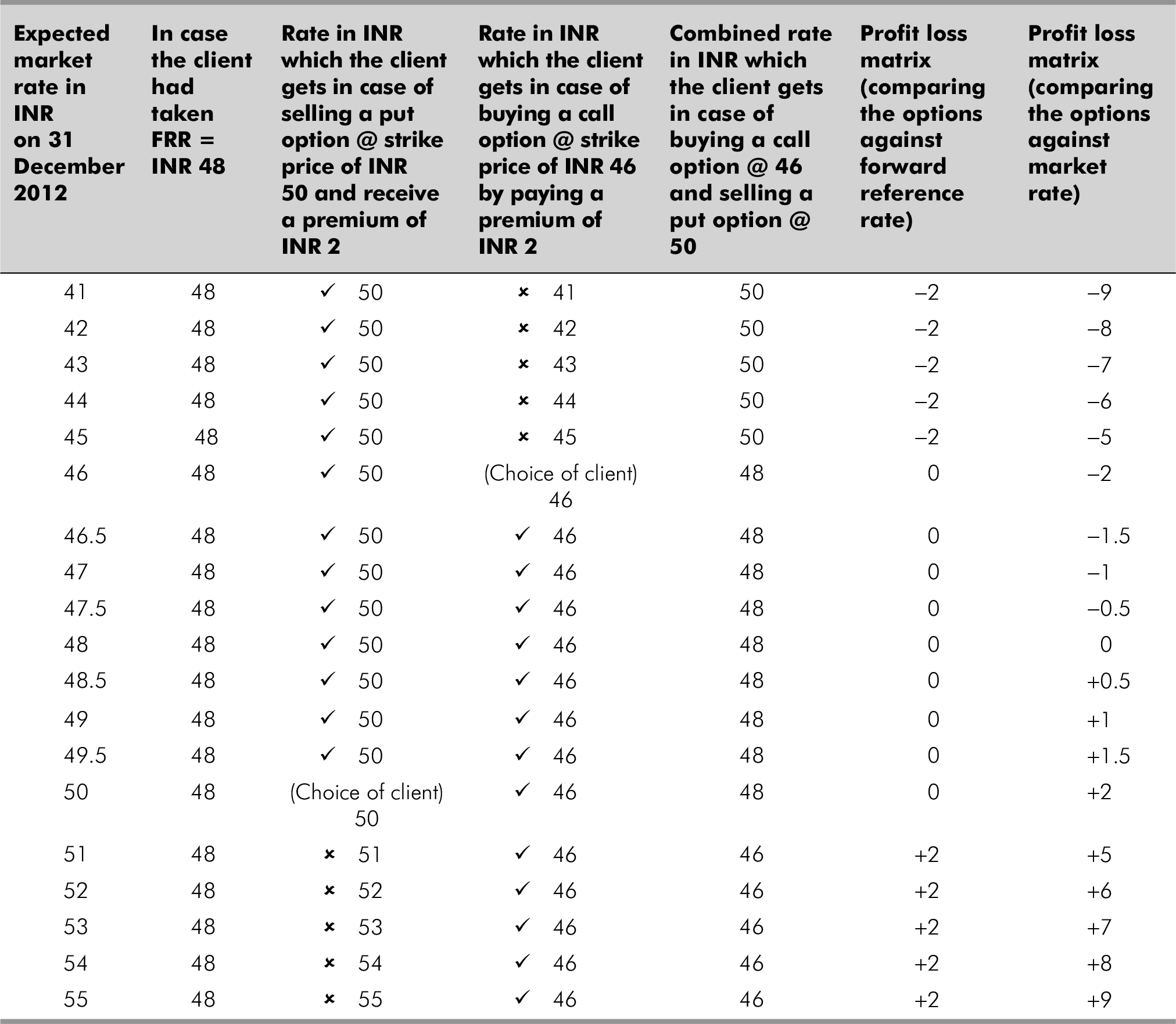

A client takes an option of Buy Call @ 46 by paying a premium of INR 2 and a Sell Put @ 50 by receiving a premium of INR 2 with FRR of INR 48 for maturity on 31 December 2012. Answer the questions that follow.

- Who is the client?

Answer: The client is an importer. Being an importer he has to buy the underlying, buy call option is the right to buy and at the same time sell put option is the obligation to buy. Since, both the options are on buy front, so the client is an Importer.

- Is the strategy genuine?

Answer: Yes, the strategy seems to be a genuine strategy. Both the options taken by the client (i.e. Importer) are on buy front, he seems to be a Genuine Importer. So the strategy taken is a genuine one.

- Is the strategy zero cost?

Answer: Yes, the strategy is a zero cost strategy.

- Develop the payoff matrix by comparing the strategy with (i) FRR and (ii) Market rate

Answer:

- Is the option ATM/ITM/OTM?

Answer: For selling the put option @ strike price of 50 which is more than a FRR, such option is termed as ITM Option at the time of taking/buying/holding/writing/selling the option.

For the call option whose strike price is 46 is less than FRR, such option is termed as ITM option at the time of taking/buying/holding/writing/selling the option.

Hence, both options are ITM.

- What is the view of the client?

Answer: Since the client is a genuine player, his view would be considered looking at the payoff compared with FRR. Looking at this payoff we can formulate that the client is very much sure that INR will depreciate for which he wants to earn extra profit against forward. He is also aware that he might suffer extra loss for this strategy. Hence, it is known as range extra for an importer.

- Is the view for short term or long term?

Answer: The strategy taken by importer here indicates that he has opted for this option for short term.

Straddle Strategy

Straddle is a combination of buy put and buy call at the same strike price and for the same maturity period.

QUESTION 1

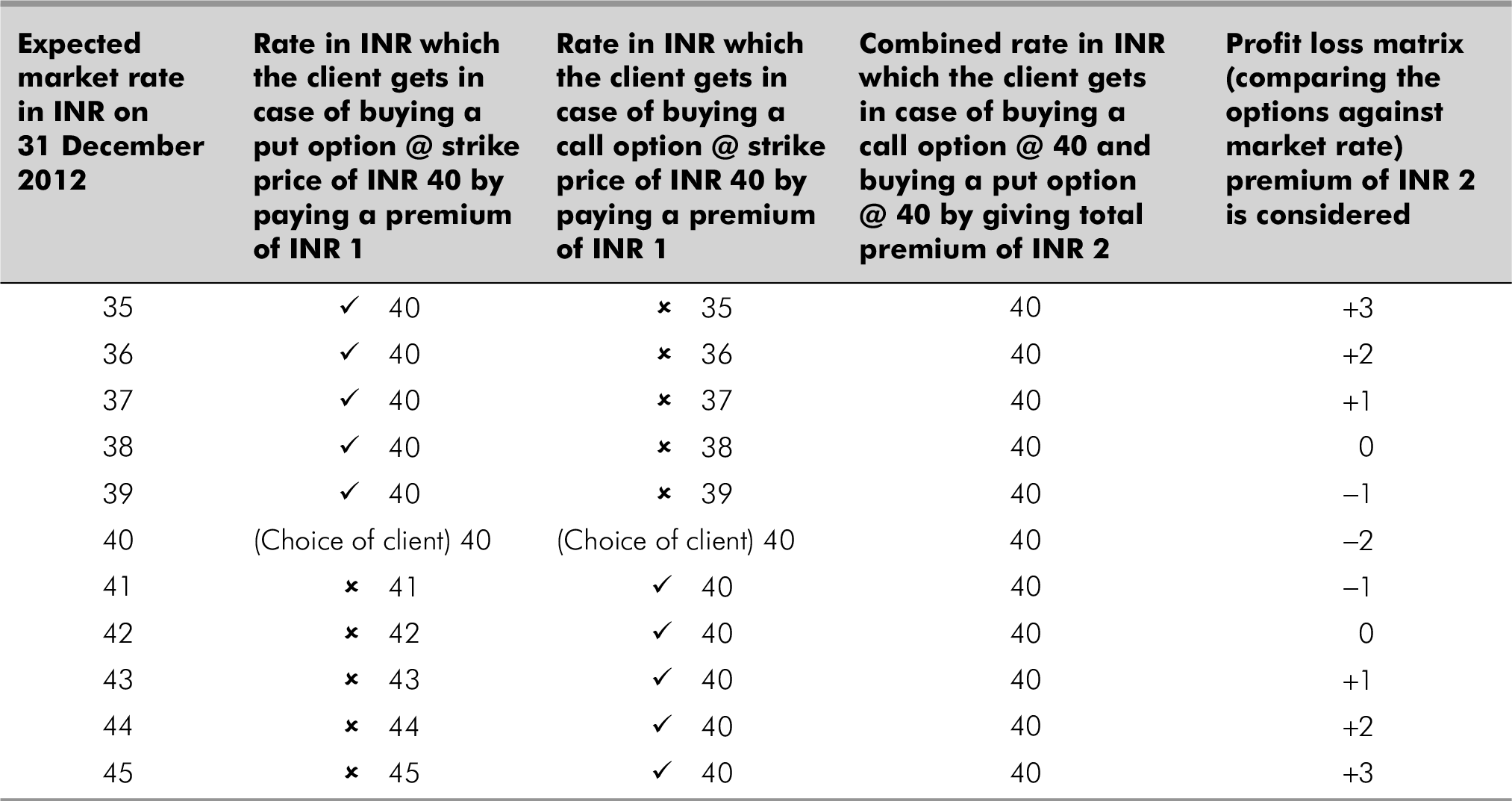

A client takes an option of buy put @ 40 strike price by paying a premium of INR 1 and a buy call @ 40 strike price by paying a premium of INR 1 with FRR of INR 40 for same maturity period of 31 December 2011. Answer the following questions.

- Who is the client?

Answer: The client is neither an importer nor an exporter because he has bought both options: Call and Put. He has the right to buy as well as the right to sell. Therefore, he is a speculator.

- Is the strategy zero cost?

Answer: No, the strategy is not a zero cost strategy because the client is buying the options for which he is paying the premium amount.

- Is the option ATM/ITM/OTM?

Answer: For the call option whose strike price is 40 is equal to the FRR, such option is termed as ATM option at the time of taking/buying/holding/writing/selling the option.

For the put option whose strike price is 40 is equal to the FRR, such option is termed as ATM option at the time of taking/buying/holding/writing/selling the option.

Hence, both options are ATM (At the Money).

- Develop the payoff matrix by comparing the strategy with (i) FRR and (ii) Market rate

Answer:

- What is the view of the client?

Answer: Since the client is not a genuine player his view would be considered looking at the payoff compared with the market rate. Looking at this payoff one can formulate, that the client is thinking that market is very volatile. The market will either go above INR 42 or below INR 38.

Straddle Strategy

Strangle is a strategy which is combination of buy put and buy call having different strike prices for equal maturity period.

Point to be noted is that the strike price of call option is higher than the strike price of the put option.

QUESTION 1

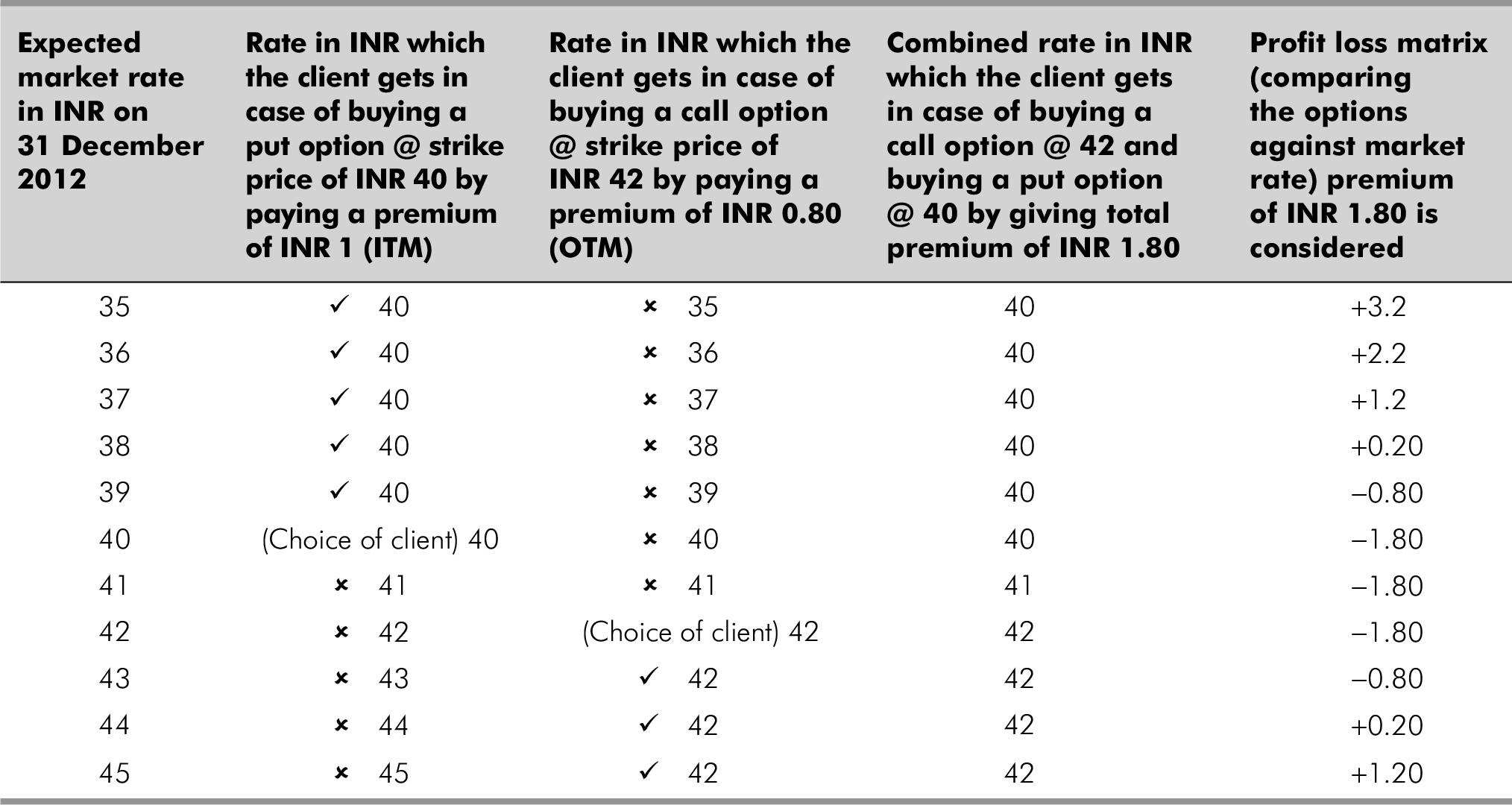

A client takes an option of buy put @ 40 strike price by paying a premium of INR 1 and a buy call @ 42 strike price by paying a premium of INR 0.80 with FRR of INR 41 for the same maturity period of 31 December 2011. Answer the following questions.

- Who is the client?

Answer: The client is neither an importer nor an exporter because he has bought both options—Call and Put. He has the right to buy as well as the right to sell. Therefore, he is a speculator.

- Is the strategy zero cost?

Answer: No, the strategy is not a zero cost strategy because the client is buying the options for which he is paying the premium amount.

- Is the option ATM/ITM/OTM?

Answer: For the call option whose strike price is 42 is more than the FRR, i.e., 41, such option is termed as OTM option at the time of taking/buying/holding/writing/selling the option.

For the put option whose strike price is 40 is less than the FRR, i.e., 41, such option is termed as ITM option at the time of taking/buying/holding/writing/selling the option.

- Develop the payoff matrix by comparing the strategy with (i) FRR and (ii) Market rate

Answer:

- What is the view of the client?

Answer: Since the client is not a genuine player his view would be considered looking at the payoff compared with the market rate. Looking at this payoff, one can formulate that the client is thinking that the market is very volatile. The market will either go above INR 43 or below INR 39.

Strangle strategy is similar to straddle strategy because the view of the client is almost the same. The view of client is that market is very volatile. The only difference between both strategies is that amount of premium paid in strangle is less than the amount of premium paid in the straddle strategy.

Butterfly Strategy

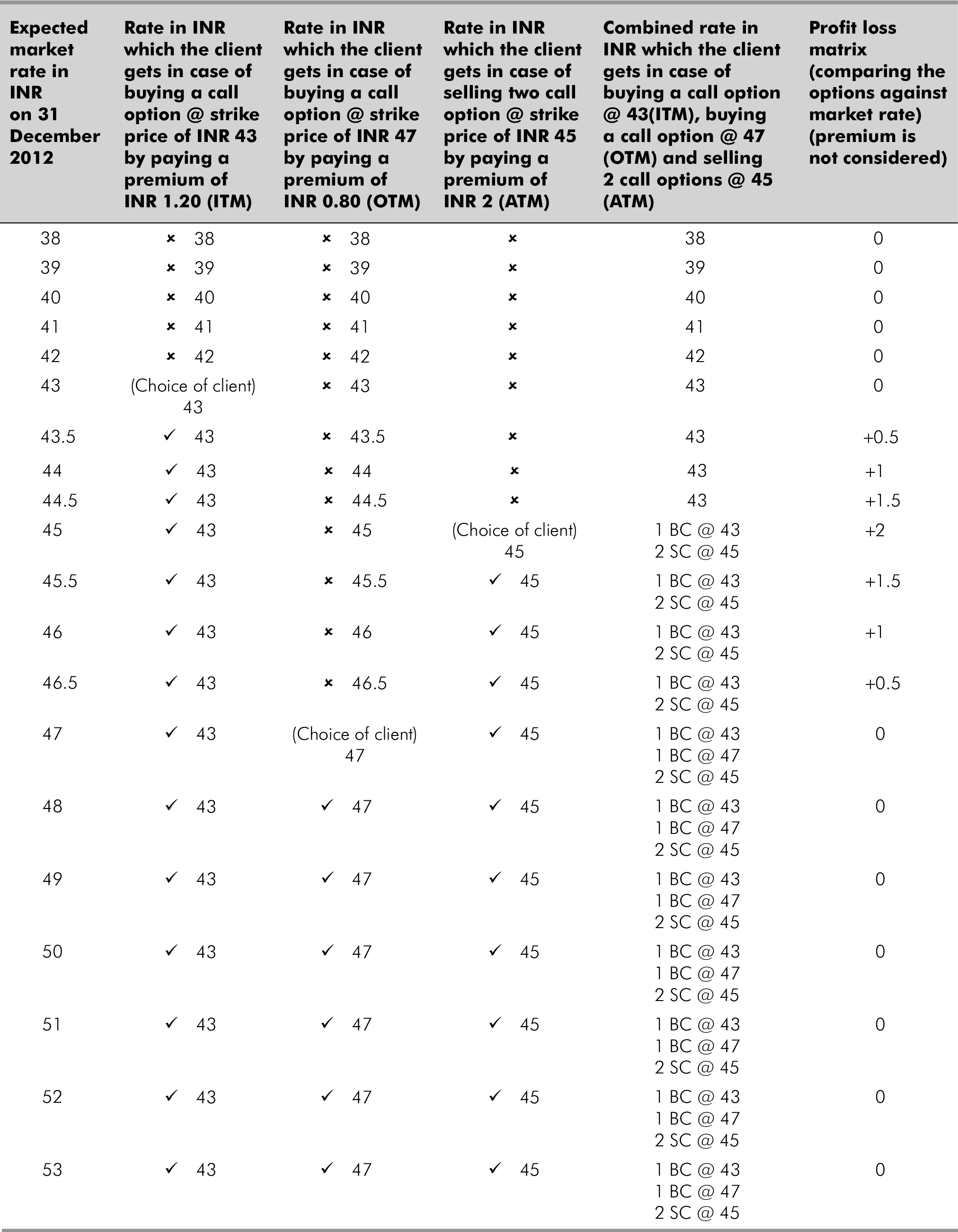

Butterfly Strategy is a combination of one OTM Buy Call, one another ITM Buy Call and two ATM Sell Call.

QUESTION 1

If the strike price of sell call is INR 45 and ITM & OTM calls have a strike price of INR 2 (ITM), INR 2 (OTM). The premiums are 80 paisa, INR 1 and INR 1.20. Answer the following questions.

- Construct the Butterfly Strategy?

Answer: Butterfly strategy consists of the three following things:

- Two ATM sell call

- One OTM buy call

- One ITM buy call

So, there will be two ATM sell calls @ strike price of INR 45 by receiving INR 1 as premium which means that FRR is 45 because ATM option means strike price is equal to FRR.

One OTM buy call will be @ strike price of INR 47 by paying premium of INR 0.80 because OTM buy call means strike price of the option is more than FRR and OTM option premium is the cheapest.

One ITM buy call will be @ strike price of INR 43 by paying premium of INR 1.20 because ITM buy call means strike price of the option is less than FRR and ITM option premium is the largest.

- Who is the client?

Answer: The client is neither an importer nor an exporter because he has bought both the options—Call and Put. He has the right to buy as well as the right to sell. Therefore, he is a speculator.

- Is the strategy zero cost?

Answer: Yes, the strategy is a zero cost strategy because client is buying two call options at different strike price by paying INR 2 as premium in total and at the same time he is selling two call options by receiving INR 2. Therefore, in net he is not paying any premium amount.

- Develop the payoff matrix by comparing the strategy with

- FRR and

- Market rate

Answer:

- What is the view of the client?

Answer: Since the client is not a genuine player, his view would be considered looking at the payoff compared with market rate. Looking at this payoff, one can formulate that the client is thinking that market will remain between 43 and 47.

Bull Spread/Call Spread Strategy

Bull Spread/Call Spread strategy is a combination of buy call and sell call wherein the buy call is ITM and the sell call is OTM.

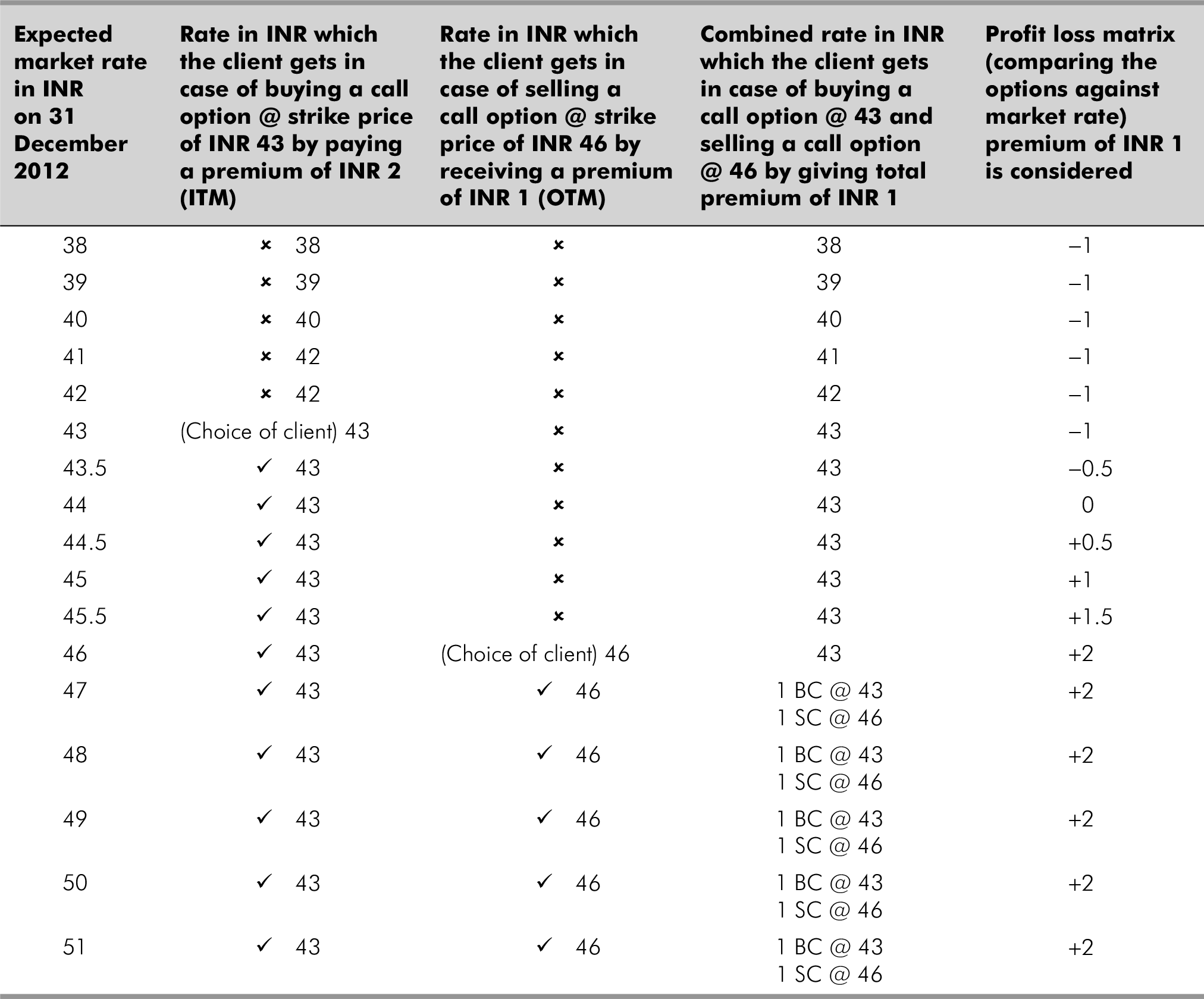

QUESTION 1

A client takes an option of buy call @ 43 strike price by paying a premium of INR 2 and a sell call @ 46 strike price by receiving a premium of INR 1 with FRR of INR 45 for same maturity period of 31 December 2011. Answer the following questions.

- Is the option ATM/ITM/OTM?

Answer: For buying the call option whose strike price is 43 which is less than the FRR, i.e., 45, such an option is termed as ITM option at the time of taking/buying/holding/writing/selling the option.

For selling the call option whose strike price is 46 which is more than the FRR, i.e., 45, such option is termed as OTM option at the time of taking/buying/holding/writing/selling the option.

- What is the view of the client?

Answer: Since the client is not a genuine player his view would be considered looking at the payoff compared with the market rate. Looking at this payoff, one can formulate that the client is thinking that market is bullish but at the same time he restricts his loss by INR 1 if market falls below INR 44.

- Develop the payoff matrix by comparing the strategy with (i) FRR and (ii) Market rate

Answer:

Bear Spread/Put Spread Strategy

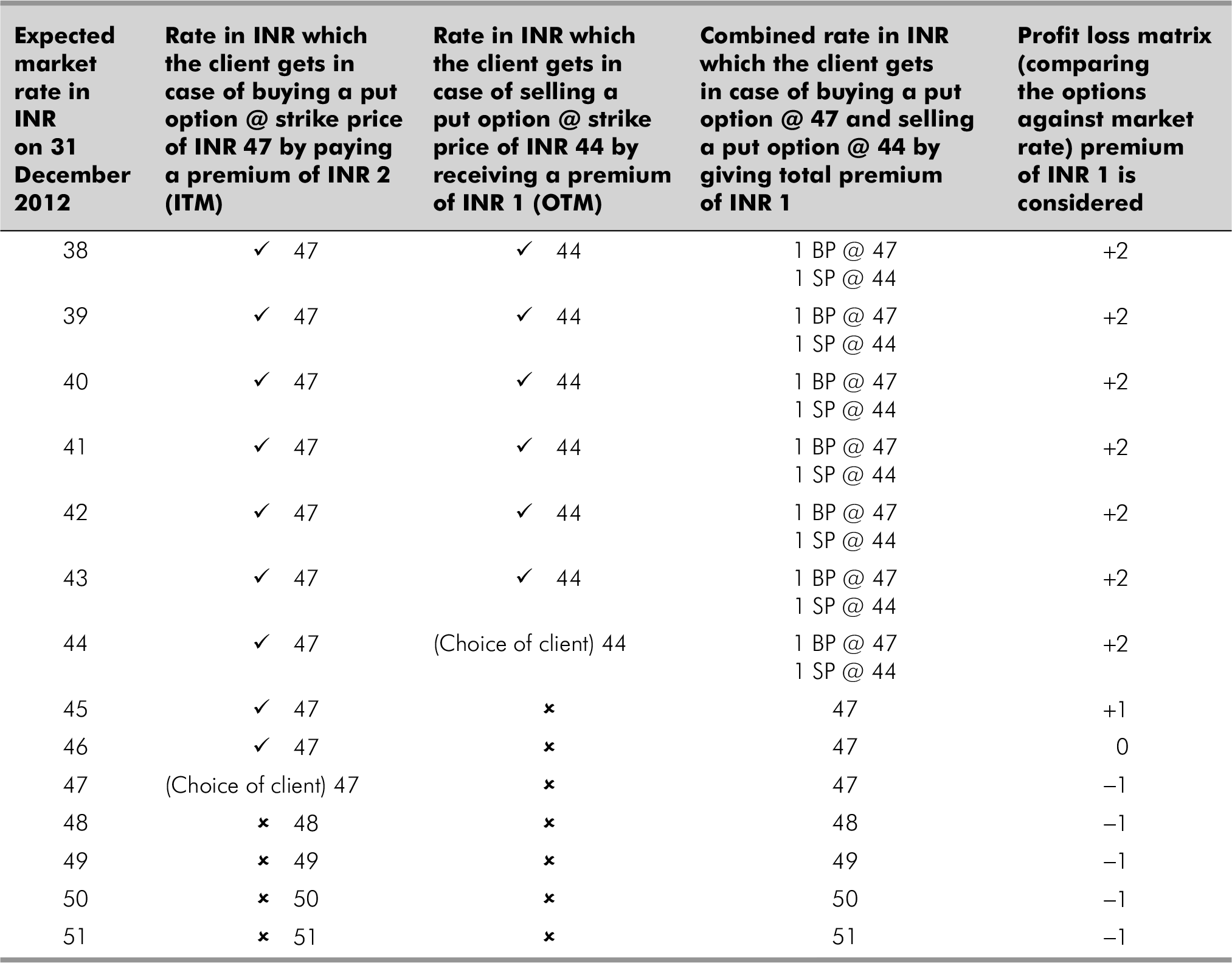

Bear Spread/Put Spread strategy is a combination of Buy Put and Sell Put wherein Buy Put is ITM and Sell Put is OTM.

QUESTION 1

A client takes an option of Buy Put @ 47 strike price by paying a premium of INR 2 and a Sell Put @ 44 strike price by receiving a premium of INR 1 with FRR of INR 45 for the same maturity period of 31 December 2011. Answer the following questions.

- Is the option ATM/ITM/OTM?

Answer: For buying put option whose strike price which is 47 is more than the FRR, i.e., 45, such option is termed as ITM option at the time of taking/buying/holding/writing/selling the option.

For selling the call option whose strike price is 44 which is less than the FRR, i.e., 45, such option is termed as OTM option at the time of taking/buying/holding/writing/selling the option.

- What is the view of the client?

Answer: Since the client is not a genuine player, his view would be considered looking at the payoff compared with the market rate. Looking at this payoff, one can formulate that the client is thinking that market is bearish but at the same time he restricts his loss by INR 1, if market goes above INR 46.

- Develop the payoff matrix by comparing the strategy with (i) FRR and (ii) Market rate

Answer:

TEST YOUR UNDERSTANDING

- What do you understand by a seagull structure? Construct a seagull exporter structure with a combination of EUR put at 1.4650 and at 1.4450 along with EUR call at 1.5000 on EUR/USD currency pair.

- Construct the payoff.

- What shall be the risks involved and the pros in the same?

- What do you mean by a ‘leveraged structure’? Is ratio forward a leveraged one? Construct a ratio forward on AUD/ USD currency pair for 31 December maturity.

- What do you understand by TARN? How is it different from Fader?

- What do you understand by barrier option? What do you understand by partial/window barriers? Is range extra structure a barrier option structure?

- A Client has bought USD call/CHF put at a strike price of 1.2275 with RKO at 1.2350 for USD 2000,000 and sold USD put/CHF Call at the same strike price with KI at 1.1130 and RKO at 1.2350 for the same notional. Additionally the client has bought a one touch option with KI at 1.2350 and payout of 10,000 USD.

- Is the above structure barrier options strategy?

- What do you understand with KI and KO?

- Construct the payoff of the client.

- Make some analysis on the strategy.

- Construct the structure, if the client has bought USD put at 45 on USD/INR currency pair for notional one million USD and sold a Call at 50 for equal maturities, the premiums also getting offset on the same.

- Is the strategy zero cost?

- What is the structure known as?

- A client has bought one buy put option at INR 46 and one buy call option at INR 46. The premium for both buy call and buy put options is INR 1. Find the following:

- Final rate

- Profit and loss

What is the strategy known as?

- A client has bought one buy put option at INR 43 having a premium of INR 1 and one buy call option at INR 44 having a premium of INR 0.50. Find the following:

- Final rate

- Profit and loss

What is the strategy known as?

- A client has taken out one in the money (ITM) buy call at INR 42 having a premium of INR 1 and one OTM buy call at INR 48 having a premium of INR 0.50 and sells two at the money (ATM) buy call at INR 45 having a premium of INR 1.5. Find the following:

- Final rate

- Profit and loss

What is the strategy known as?

- A client has bought a sell call option at INR 1,200 and a buy call option at INR 1,000. Find the following:

- Final rate

- Profit and loss

What is the strategy known as?

- A client has bought one buy call at INR 40 having a premium of INR 1 and one sell call at INR 42 having a premium of INR 2. Find the following:

- Final rate

- Profit and loss

What is the strategy known as?

- A client has bought one buy call at INR 40 having a premium of INR 2 and one sell call at INR 42 having a premium of INR 1. Find the following:

- Final rate

- Profit and loss

What is the strategy known as?

- A client has buy put option at INR 53 by paying a premium of INR 3 and sell call option at INR 58 by paying a premium of INR 2. The forward rate given is INR 56. Answer the following:

- Is the strategy genuine or not?

- Is it taken by an exporter or an importer?

- Is this a zero cost strategy?

- What if premium on buy put was INR 2 and sell call was INR 3 Elaborate.

- What is the view of the client?

- Is the above view for short term or long term?

- What is the name of the strategy?

- Classify the option legs as ATM, ITM or OTM?

- A client has bought call option at INR 30 and sold put option at INR 34. The forward rate given is INR 32. Answer the following:

- Is the strategy genuine or not?

- Is it taken by an exporter or an importer?

- Is this a zero cost strategy?

- What is the view of the client?

- Is the above view for short term or long term?

- What is the name of the strategy?

- Classify the option legs as ATM, ITM or OTM?

- A client has buy call option at INR 26 by paying a premium of INR 1 and buy call option at INR 0.50 by paying a premium of INR 2. The forward rate given is INR 0.75. Answer the following:

- Is the strategy genuine or not?

- Is it taken by an exporter or an importer?

- Is this a zero cost strategy?

- Plot the pro?t and loss.

- What is the strike price of buy call?

- What is the name of the strategy?

- Classify the option legs as ATM, ITM or OTM?

- A client has bought call option at INR 30 by paying a premium of INR 1 and bought call option at INR 34 by paying a premium of INR 0.50. The forward rate given is INR 32. Answer the following:

- Is the strategy genuine or not?

- Is it taken by an exporter or an importer?

- Is this a zero cost strategy?

- Plot the pro?t and loss.

- What is the name of the strategy?