Chapter 10

Sector Investing: ETFs According to Industry

IN THIS CHAPTER

![]() Getting acquainted with major industry sectors

Getting acquainted with major industry sectors

![]() Weighing the pros and cons of sector and style investing

Weighing the pros and cons of sector and style investing

![]() Listing the ETFs that work best for sector investing

Listing the ETFs that work best for sector investing

![]() Choosing the best options for your portfolio

Choosing the best options for your portfolio

![]() Knowing which sector funds to avoid

Knowing which sector funds to avoid

Any Star Trek fan (yeah, beam me up) knows that matter and antimatter, should they ever meet, would result in an explosion so violent as to possibly destroy the entire universe or, at the very least, mess up Don Draper’s hair. Despite the firm convictions of zealots on both sides, style investing (large/small/growth/value) and sector investing (technology/utilities/healthcare/energy) are not matter and antimatter. They can, and sometimes do, exist very peacefully side-by-side.

In this chapter, I present the nuts and bolts of sector investing: how it can function alone, or in conjunction with style investing, to provide diversity both on the domestic and international sides of your portfolio (or overlapping the two). However you decide to slice the pie (whether by style or sector, or both), using ETFs as building blocks makes for an excellent strategy.

Selecting Stocks by Sector, not Style

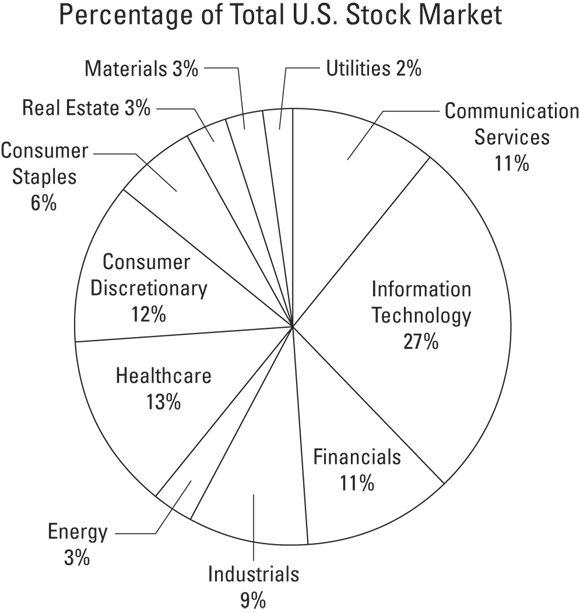

As of this writing, there are 471 industry-sector ETFs, per Morningstar Direct. You can find a fund to mirror each of the major industry sectors of both the U.S. and foreign economies: energy, basic materials, financial services, consumer goods, and so on. See Figure 10-1 for a bird’s-eye view of the U.S. economy split into its major industry sectors, each accorded its proper allotment.

FIGURE 10-1: The industry sector map for the United States.

Based on the breakdown of the MSCI U.S. Broad Market Index, this chart reveals the size of 11 major industry sectors of the U.S. economy. What you’re seeing is the total capitalization (value of stock) of all public companies within each industry group. Note: No standard methodology exists for breaking up the U.S. industry into sectors; MSCI does it one way, and FTSE Russell does it a slightly different way.

Some ETFs mirror subsections of the economy, such as semiconductors (a subset of information technology) and biotechnology (a subset of healthcare). In some cases, subsectors of the economy you may not even know exist — such as nanotech, cloud computing, and water resources — are represented with ETFs. And in other instances, you can find ETFs that represent sub-sub- and sub-sub-subsections of the economy, such as cybersecurity, telemedicine, video games, and, of course, the latest darling of Johnny-come-lately ETFs, cannabis. Many cannabis ETFs have sprung up lately. I know of at least a dozen, such as Cambria’s Cannabis ETF, with the ticker TOKE. Cute, eh?

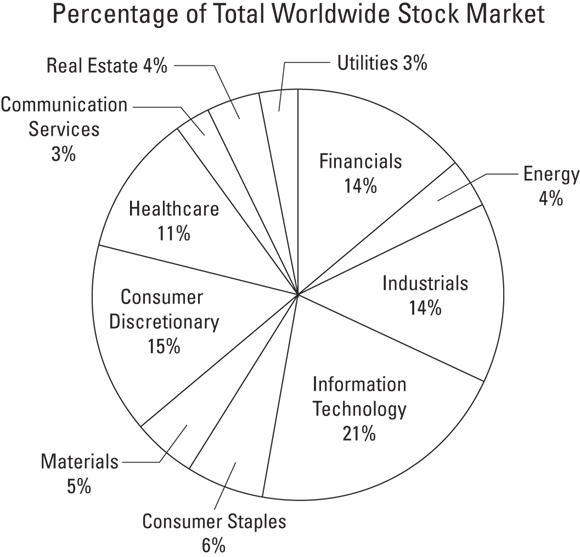

A good number of newer ETFs allow you to invest in industry sectors in foreign countries (which are not represented in Figure 10-1) or in global industries (which is to say U.S. and foreign countries together; see Figure 10-2).

FIGURE 10-2: The industry sector map for the entire world.

Looking at Figures 10-1 and 10-2, you can see that information technology is number one on the global chart, as it is on the U.S. chart. But healthcare moves from the number two spot on the U.S. chart down to number five on the global chart. (Only in the United States does a trip to the dermatologist boost the national economy!)

Looking at Figures 10-1 and 10-2, you can see that information technology is number one on the global chart, as it is on the U.S. chart. But healthcare moves from the number two spot on the U.S. chart down to number five on the global chart. (Only in the United States does a trip to the dermatologist boost the national economy!)

Here is living proof that you can, if you so wish, slice and dice a portfolio to ultimate death: You can actually find some ETFs that allow you to buy into a particular industry within a particular country, such as the KraneShares CSI China Internet ETF (KWEB). These are similar to the sub-sub-subsector ETFs I discuss earlier. Betting on slivers of the economy is almost as risky as betting on individual stocks. And day traders these days are just as likely to use ETFs (often the sub-sub-sub sectors) as they are individual stocks. Sadly, most day traders, whether they favor ETFs or stocks, are going broke, even as I’m typing these words. Please, invest broadly and trade infrequently. You’ll be glad you did.

Here is living proof that you can, if you so wish, slice and dice a portfolio to ultimate death: You can actually find some ETFs that allow you to buy into a particular industry within a particular country, such as the KraneShares CSI China Internet ETF (KWEB). These are similar to the sub-sub-subsector ETFs I discuss earlier. Betting on slivers of the economy is almost as risky as betting on individual stocks. And day traders these days are just as likely to use ETFs (often the sub-sub-sub sectors) as they are individual stocks. Sadly, most day traders, whether they favor ETFs or stocks, are going broke, even as I’m typing these words. Please, invest broadly and trade infrequently. You’ll be glad you did.

Speculating on the Next Hot Industry

Is there a God? Does he have a long, white beard? Is “he” possibly a “she”? Why do sector investors tend to be speculators, while style investors tend to be buy-and-hold kinds of people? These are questions that sometimes keep me awake at night. I won’t attempt to address the first three here. As for the fourth…heck, I have no idea. But there’s little question that people who divide their portfolios into large/small/value/growth are much more likely to be long-term investors with long-term strategies than are people who buy into sectors (often through ETFs). That’s just the way it is.

Sizzling and sinking

Sector funds are often purchased by investors who think they know which sectors (or sectors within specific countries, such as financials in Brazil) are going to shine, and gosh darnit, they’re going to profit by it. Unfortunately, they are often wrong.

I’m old enough to recall a time when environmental service companies, by dint of the realization that pollution was becoming a serious problem, were going to be a sure bet. But then, lo and behold, environmental service companies seriously lagged behind the overall market for years. Then it was information technology that couldn’t possibly fail, yet for three brutal years (2000–2002), the technology sector fell like hail. At the time of this writing, tech is hot once again (especially hydrogen/clean energy/electric vehicles), but not as hot as cryptocurrencies or marijuana. By the time this book comes out, who knows what everyone will be panting after?

Momentum riders and bottom feeders

Interestingly, while most investors are momentum investors — they tend to buy what’s hot — other investors look for what’s not, on the theory that everything reverts to the mean. The two camps are forever trading sector funds back and forth. Right now, the momentum investors are buying tech; the bottom feeders (who prefer to see themselves as value investors) are buying energy. Fortunately (or unfortunately), there is no dearth of ETFs to please both crowds.

(Note: I’m not saying that neither momentum investing nor buying up down-and-out industries has value. Both strategies have been known to make money. But such strategies can’t be done helter-skelter. Like any other kind of investing, they require careful thought and study. Many rapid sector traders are not such deep thinkers.)

You can tell from my tone, no doubt, that I’m no big fan of sector speculation — or speculation of any sort. But what about using sector ETFs as buy-and-hold instruments? Even though few people do it, can a buy-and-hold portfolio be just as easily and effectively divided up by industry sector as it can by investment style? Keep reading.

Doing Sector Investing Right

An in-depth study on industry-sector investing, done by Chicago-based Ibbotson Associates (now part of Morningstar), came to the very favorable conclusion that sector investing — because times have apparently changed — is potentially a superior diversifier to grid (style) investing. (I discuss the style grid in Chapters 4 and 5.) Globalization has led to a rise in correlation between domestic and international stocks; large-, mid-, and small-cap stocks have a high correlation to each other. A company’s performance is tied more to its industry than to the country where it’s based or its market capitalization, concluded Ibbotson.

The Ibbotson report didn’t end there. It also ballyhooed sector investing as a superior instrument for fine-tuning a portfolio to match an individual investor’s risk tolerance. A conservative investor might overweight utilities (a less volatile sector); a more aggressive investor might tilt toward technology (whooeee).

That sounds like a good plan, although the lead author of that study once confided to me that he still has the bulk of his personal portfolio broken up into value, growth, large cap, and small cap — as do I. However, we both have some industry-sector ETFs (for fine-tuning), as well.

Calculating your optimal sector mix

If you are going to go the sector route and build your entire stock portfolio, or a good part of it, out of industry-sector ETFs, I suggest that before you do anything, you take a look at Figures 10-1 and 10-2. Make sure you are able to have allocations to all or most major sectors of the economy.

Some advisors would tell you to keep your allocations roughly proportionate to each sector’s share of the broad market. I think that’s decent advice, with just a bit of caution: Had you taken that approach in 1999, your portfolio would have been chocked to the top with technology, given the gross overpricing of the sector at that point. (And you would have taken a bath the following year.) I’d suggest that no matter what sectors are hot at the moment, no single sector should ever make up more than 20 percent of your stock portfolio.

(If you’ve read Chapter 9, you may recall that I noted that single-country and especially small single-country ETFs are not something I go out of my way to own. One reason is that a smaller country’s economy can be dominated by one or two industries, making its markets especially volatile.)

Perhaps start by roughly allocating your sector-based portfolio according to the market cap of each sector and then tweak from there — based not on crystal-ball predictions of the future but on the unique characteristics of each sector. What do I mean? Read on.

Seeking risk adjustment with high- and low-volatility sectors

Some industry sectors have historically evidenced greater return and greater risk. (Return and risk tend to go hand in hand, as I discuss in Chapter 4.) The same rules that apply to style investing apply to sector investing. Know how much volatility you can stomach, and then — and only then — build your portfolio in tune with your risk tolerance.

As for historical risk and return, Figure 10-3 shows an approximation of how the major sectors rank. Keep in mind that any single sector — even utilities, the least volatile of all — will tend to be more volatile than the entire market because there is little diversification. Don’t overindulge!

Finally, keep in mind that your allocation between bonds and stocks will almost certainly have much more bearing on your overall level of risk and return than will your mix of stocks. In Part 3 of this book, I introduce bonds and discuss how an ETF investor should hold them.

FIGURE 10-3: Industry sectors, from most to least volatile.

Knowing where the style grid comes through

There is nothing wrong with dividing a stock portfolio into industry sectors, but please don’t be hasty in scrapping style investing. I really believe that if you’re going to pick one strategy over the other, the edge goes to style investing. For one thing, I know that it works. Style investing helps to diffuse (but certainly not eliminate) risk. Scads of data show that.

There is nothing wrong with dividing a stock portfolio into industry sectors, but please don’t be hasty in scrapping style investing. I really believe that if you’re going to pick one strategy over the other, the edge goes to style investing. For one thing, I know that it works. Style investing helps to diffuse (but certainly not eliminate) risk. Scads of data show that.

In addition, style investing allows you to take advantage of years of other data that indicate you can goose returns without raising your risk, or raising it by much, by leaning your portfolio toward value and small cap (see Chapters 5, 6, 7, and 8). When you invest in industry sectors through ETFs, you are most often investing the vast majority of your funds in large caps, and you’re usually splitting growth and value evenly. That approach may limit your investment success.

Another reason ETF investors shouldn’t scrap style investing: Style ETFs are the cheaper choice. For whatever reason — yes, another one of those eternal mysteries that keeps me awake at night — style ETFs tend to cost much less than industry-sector ETFs. According to Morningstar Direct, the average sector equity fund will cost you 0.52 percent in management fees. Style funds are generally much less.

And one final reason to prefer style to sector for the core of your portfolio: You will require fewer funds. With large growth, large value, small growth, and small value, you can pretty much capture the entire stock market. With sector funds, you need nearly a dozen funds to achieve the same effect. Each sector fund offers minimal diversification because the price movements of companies in the same industry sector tend to be closely correlated.

Combining strategies to optimize your portfolio

There’s no point to having dozens of ETFs in your portfolio if they are only going to duplicate each other’s holdings. So if you already own the entire market through diversified ETFs in all corner quadrants of the style grid — large, small, value, and growth — then why add any industry sectors that are obviously already represented?

It would make sense to add a peppering of semiconductor stocks or utility stocks if you knew that semiconductors or utilities were going to blast off. (Of course, a rational investor would never say they knew anything about the future, other than that the sun will probably rise tomorrow.) And yet, taking on an added dose of semiconductors or utilities may still make sense if that added dose of either industry sector somehow were to raise your performance potential without raising risk. That could happen only if you chose an industry sector that is not closely correlated to the broader market.

Seeking low correlations for added diversification

Some sectors, or industry subsectors, even though they are part of the stock market, tend to move out of lockstep with the rest of the market. By way of example, consider REITs: real estate investment trusts. (If you look for REITs in Figure 10-1, you will find them buried under “Financials.”) I devote Chapter 11 almost entirely to REITs, and especially REIT ETFs.

Another sector that fits the bill is energy. For example, consider that in 2002, when the total U.S. stock market tanked by almost 11 percent, REITs were up 31 percent. The year 2005 was pretty lackluster for the total stock market, yet energy stocks were up 31 percent. In the past three years, all U.S. sectors have done very well, except for energy, with a return of –28 percent annually.

If you decide to build your portfolio around industry-sector funds, I urge you at the very least to dip into the style funds to give yourself the value- or small-cap tilt that I discuss in Chapters 5, 6, 7, and 8. That’s especially true if you use SPDRs to build your sector portfolio. This fund group is especially weighted toward large cap. In Chapter 21, I offer a few sample portfolios to illustrate workable allocations.

Sector Choices by the Dozen

After you decide which industry sectors you want to invest in, you need to choose among ETFs. BlackRock’s iShares, Vanguard, Fidelity, State Street Global Advisors SPDRs, and other fund managers all offer good-sized menus of sector funds, both domestic and international.

Begin your sector selection here:

- Do you want representation in large industry sectors (healthcare, technology, utilities)? Your options include Vanguard ETFs, BlackRock’s iShares, State Street Global Advisors SPDRs, and Fidelity, as well as some slightly innovative funds from Invesco.

- Do you want to zero in on narrower industry niches (insurance, oil service, nanotech, autonomous technology, and robotics)? Consider Invesco, iShares, VanEck, ARK Invest, and Global X. You can also choose State Street Global Advisors (non-Select Sector) SPDRs.

- Are you looking for sometimes ridiculously narrow industry niches (aluminum) or sectors within sectors within individual foreign countries? You should look at Global X, KraneShares, and Direxion ETFs. Ark Invest has one, too…if Israeli tech is your thing.

- Do you want to keep your expense ratios to a minimum? Fidelity and Vanguard are the cheapest.

In the following sections, I give you a more in-depth view of the sector offerings available to you.

Vanguard ETFs

The Vanguard industry sector offerings include the following:

U.S. Sector Fund Name | Ticker |

|---|---|

Vanguard Consumer Discretionary ETF | VCR |

Vanguard Consumer Staples ETF | VDC |

Vanguard Energy ETF | VDE |

Vanguard Financials ETF | VFH |

Vanguard Health Care ETF | VHT |

Vanguard Industrials ETF | VIS |

Vanguard Information Technology ETF | VGT |

Vanguard Materials ETF | VAW |

Vanguard Real Estate ETF | VNQ |

Vanguard Telecommunications Services ETF | VOX |

Vanguard Utilities ETF | VPU |

Vanguard’s International sector fund is the Global ex-U.S. Real Estate ETF (VNQI).

Fill your domestic stock portfolio with Vanguard’s 11 U.S. industry-sector ETFs, and presto! You’ve captured just about the entire universe of Yankee stocks. Granted, that universe will be weighted in such a manner that you’ll have only token representation of mid and small caps (although you’ll have more small-cap exposure than you would with SPDRs).

The one exception is the Vanguard REIT Index ETF (VNQ). Principally a mid-cap fund, VNQ is a prince among ETFs. It is well diversified within its own real estate universe, and if you’re going to own a U.S. REIT ETF, Vanguard’s selection is an excellent choice. (See Chapter 11 for more on REITs.) This fund carries an expense ratio of 0.12 percent, as does Vanguard’s international counterpart VNQI. The other Vanguard U.S. sector ETFs carry an expense ratio of 0.10 percent — a real bargain among sector funds.

In general, Vanguard ETFs (based on MSCI indexes) and the Select Sector SPDRs (based on S&P indexes) are your best building blocks for a U.S. stock portfolio that is sliced and diced by industry sectors. They are also excellent options for peppering a style grid–based portfolio with sector funds.

If you want a more globally based sector approach, then the more expensive iShares options may be your best bet. In Part 4, where I build sample portfolios, you see how some of these funds can be incorporated into an optimally diversified investment strategy.

Select Sector SPDRs: State Street Global Advisors (Part 1)

In this section, I focus on Select Sector SPDRs. In the next section, I introduce just plain old SPDRs representing industry sectors. What’s the difference? Keep reading because I explain in the next section. First, let me acquaint you with some fund names.

Select Sector SPDR offerings include the following.

U.S. Sector Fund Name | Ticker |

|---|---|

Communication Services Select Sector SPDR | XLC |

Consumer Discretionary Select Sector SPDR | XLY |

Consumer Staples Select Sector SPDR | XLP |

Energy Select Sector SPDR | XLE |

Financial Select Sector SPDR | XLF |

Health Care Select Sector SPDR | XLV |

Industrial Select Sector SPDR | XLI |

Materials Select Sector SPDR | XLB |

Technology Select Sector SPDR | XLK |

Utilities Select Sector SPDR | XLU |

Real Estate Select Sector SPDR | XLRE |

Overall, I put the Select Sector SPDRs on a par with the Vanguard sector ETFs. Like the Vanguard funds, they represent large U.S. industry groupings. They follow reasonable indexes, and they will cost you only a tad more than the Vanguard and Fidelity ETFs — 0.12 percent for Select Sector compared to 0.10 and 0.084 percent a year in management fees for Vanguard and Fidelity, respectively. (The exception is real estate funds; both SPDRs and Vanguard charge 0.12 percent, whereas Fidelity charges 0.085 percent.)

Because the S&P indexes upon which the Select Sector SPDRs are built tend to represent mostly large-cap companies, I urge anyone building a Select Sector SPDR portfolio to tap into small caps through some other means, such as buying into one of the small-cap ETFs discussed in Chapters 7 and 8.

SPDRs: State Street Global Advisors (Part 2)

Regular SPDRs industry-sector offerings include the following.

U.S. Sector Fund Name | Ticker |

|---|---|

SPDR S&P Bank ETF | KBE |

SPDR S&P Regional Banking ETF | KRE |

SPDR S&P Insurance | KIE |

SPDR S&P Oil & Gas Exploration & Production ETF | XOP |

SPDR S&P Oil & Gas Equipment & Services | XES |

SPDR S&P Health Care Equipment | XHE |

International Sector Fund Name | Ticker |

|---|---|

SPDR Dow Jones International Real Estate ETF | RWX |

Global Sector Fund Name | Ticker |

|---|---|

SPDR Dow Jones Global Real Estate ETF | RWO |

SDPR S&P Global Natural Resources ETF | GNR |

Ready to find out what distinguishes a Select Sector SPDR from a plain old industry-sector SPDR? Both are industry-sector funds. Both are owned and run by megabank State Street Global Advisors. But the two ETF lineups are somewhat different. Retailers and car manufacturers call the differentiation product-line extension. So just as Honda has its Acura line of cars as well as plain old Hondas, and Toyota has its Lexus line in addition to the plain old Toyotas, State Street has both SPDRs and Select Sector SPDRs.

A big difference between the two lineups (just as with Hondas and Acuras, and Toyotas and Lexuses) is price, but if you assume that the “Select” names will cost you more, surprise! Whereas the Select Sector SPDRs charge 0.10 percent in management fees, the non-Select Sector SPDRs charge 0.35 percent for the domestic options, 0.59 percent for the one international, and 0.50 (RWO) and 0.40 percent (GNR) for the two global ETFs.

Another difference is the exposure. Select Sector SPDRs track large sectors of the economy, such as healthcare and energy. The plain old SPDRs, which happen to be darlings among day traders, track narrower segments of the market. Instead of energy, you’re looking at Oil & Gas Exploration & Production or Oil & Gas Equipment & Services, for example. Instead of healthcare, you’re looking at just healthcare equipment. Because I prefer larger segments of the market, and I certainly prefer lower prices, I tend to prefer the Select Sector SPDRs over the SPDRs for any kind of domestic stock exposure.

As for the international side of things, State Street had a bunch of international sector ETFs, which they’ve retired. All that’s left is the International Real Estate ETF (RWX), which at 0.59 percent, is way, way more than Vanguard’s Global ex-U.S. Real Estate ETF. Vanguard charges 0.12 percent, making it a far preferable option.

However, State Street has a handful of (non-select) global sector funds, and in this handful are two funds that I like quite a bit: The SPDR Dow Jones Global Real Estate ETF (RWO) and, even more impressive, the SDPR S&P Global Natural Resources ETF (GNR). These global selections offer reasonable management fees of 0.50 and 0.40, respectively.

The SPDRs website — www.sectorspdr.com — is full of fabulous tools. Check out especially the Correlation Tracker, SPDR Map of the Market, and Sector Tracker. (You don’t have to be a SPDRs investor to use these tools.)

BlackRock’s iShares

The iShares industry-sector offerings include the following.

U.S. Sector Fund Name | Ticker |

|---|---|

iShares U.S. Basic Materials Index | IYM |

iShares U.S. Consumer Goods Index | IYK |

iShares U.S. Consumer Services | IYC |

iShares U.S. Energy Index | IYE |

iShares U.S. Financial Sector Index | IYF |

iShares U.S. Financial Services | IYG |

iShares U.S. Healthcare | IYH |

iShares U.S. Industrials | IYJ |

iShares U.S. Real Estate | IYR |

iShares U.S. Technology | IYW |

iShares U.S. Telecommunications | IYZ |

iShares Transportation Average | IYT |

iShares U.S. Utilities | IDU |

International Sector Fund Name | Ticker |

|---|---|

iShares MSCI Europe Financials | EUFN |

iShares Emerging Markets Infrastructure | EMIF |

Global Sector Fund Name | Ticker |

|---|---|

iShares Global Energy | IXC |

iShares Global Materials | MXI |

iShares Global Consumer Staples | KXI |

iShares Global Timber & Forestry | WOOD |

iShares Global Utilities | JXI |

As you may be aware by now, I like iShares just fine. I like their style funds, and, as I discuss in Chapter 9, I like many of their international funds. As for domestic industry-sector funds, however, BlackRock, Inc. (sponsor of iShares) simply charges too much. Most of their sector ETFs charge 0.42 to 0.43 percent. A few, mysteriously, charge as little as 0.18. In the aggregate, the Vanguard ETFs or Select Sector SPDRs are a much more economical way to get domestic sector exposure.

On the international and global front, however, the iShares ETFs are competitive with SPDRs: Most charge 0.46 percent in management fees. And the iShares lineup offers more global sector funds than any other ETF provider. (The ones I list here are just a representative sampling.) If you want to divide your portfolio into global sectors, iShares is the place to go.

Invesco

Invesco industry-sector offerings include the following.

U.S. Sector Fund Name | Ticker |

|---|---|

Invesco Dynamic Building & Construction | PKB |

Invesco Dynamic Energy & Exploration | PXE |

Invesco Dynamic Food & Beverage | PBJ |

Invesco Dynamic Leisure & Entertainment | PEJ |

Invesco Dynamic Media | PBS |

Invesco Dynamic Networking | PXQ |

Invesco Dynamic Pharmaceuticals | PJP |

Invesco Dynamic Software | PSJ |

Invesco Solar | TAN |

Invesco Aerospace & Defense | PPA |

Invesco WilderHill Clean Energy | PBW |

Invesco Water Resources | PHO |

Global Sector Fund Name | Ticker |

|---|---|

Invesco Global Water Index | CGW |

Invesco Global Clean Energy ETF | PBD |

On the down side, Invesco charges about 0.60 percent for its domestic offerings (each differs slightly) and 0.75 percent for its global funds: That’s a whole lot more than most of the competition is charging or would dare charge. The funds are also “dynamic,” which means that the indexes they track are actively managed (in a sense, the index is tooled in a way that allows the creators to stock pick, indirectly). Many investors would see that as a plus; I don’t. It means added expense (both up front and behind the scenes) and a possible loss of tax efficiency. On the upside, however, Invesco’s selection of industry groupings, in both their U.S. and global offerings, has been innovative, to say the least.

Although I wouldn’t suggest building an entire portfolio of Invesco sector ETFs, if you’re looking to sprinkle some noncorrelating holdings into an otherwise well-diversified portfolio, Invesco may have something to offer. I’m especially intrigued with the Invesco Global Clean Energy ETF and the Invesco Global Water Index ETF. Investing in companies that provide alternative fuels and the filtration and delivery of drinking water respectively, these two ETFs, so far, seem to have sweetly low correlations to the broad market. I’m keeping an eye on them. If Invesco were to lower the expense ratios, I might keep two eyes on them.

Before I leave Invesco, I want to introduce some of the company’s innovative equal-weight sector funds.

Equal-Weight Sector Fund Name | Ticker |

|---|---|

Invesco S&P 500 Equal Weight Consumer Staples ETF | RHS |

Invesco S&P 500 Equal Weight Health Care ETF | RYH |

Invesco S&P 500 Equal Weight Energy ETF | RYF |

Invesco S&P 500 Equal Weight Technology ETF | RYT |

Invesco S&P 500 Equal Weight Utilities ETF | RYU |

Invesco S&P 500 Equal Weight Real Estate ETF | EWRE |

Equal weight means that the ETFs are not “market weighted,” as are the vast majority of ETFs (and mutual funds). So if you look at, for example, the S&P 500 Equal Weight Technology ETF (RYT), you find a portfolio of about 70 company stocks, and very much unlike the typical technology fund, Apple and Microsoft do not dominate the portfolio. Those two tech giants are each given approximately 1.45 percent of the entire portfolio, so that Apple has no greater a position than say, Adobe, Inc., Paycom software, or Skyworks Solutions.

Invesco’s equal weight ETFs charge 0.40 percent — less than most of its other sector funds. Unlike almost all other sector funds, you are going to get exposure to portfolios that are not dominated by large caps, but have roughly equal exposure to large, mid, and small caps. Over the long haul, small caps should outperform large caps, but with some added volatility. I would say that if you are going to build an entire portfolio with sector funds, you might want to consider this Invesco lineup. Or, if you are a style investor but want to overweight one particular sector, then an equal-weighted Invesco ETF wouldn’t be a bad choice.

Fidelity

Brokerage giant Fidelity got into the ETF business a little later than most, and so they figure that they must cut costs to get market share. They offer 11 sector funds, and the cost for most is 0.084 percent. (In case you’re wondering, 0.084 percent versus Vanguard’s 0.10 percent would mean that you’d be saving $1.60 a year on a $10,000 investment.)

Here is a sampling of Fidelity’s sector offerings:

Fidelity Sector Fund Name | Ticker |

|---|---|

Fidelity MSCI Information Technology Index ETF | FTEC |

Fidelity MSCI Health Care Index ETF | FHLC |

Fidelity MSCI Financials Index ETF | FNCL |

Fidelity MSCI Consumer Discretionary Index ETF | FDIS |

Fidelity MSCI Utilities Index ETF | FUTY |

Fidelity MSCI Energy Index ETF | FENY |

There’s nothing not to like about the Fidelity sector funds. They use solid, plain-vanilla MSCI indexes, and the price is more than competitive.