chapter 3

OTC FX Concepts

LEARNING OBJECTIVES

This chapter introduces readers to concepts around the system of quoting in foreign exchange markets with special reference to over-the-counter (OTC) market which refers to the market in which transactions are entered into by counterparties on bilateral basis without involvement of any settlement agencies like exchange. The contents of this chapter are organized in the following order:

1. Concept of Base Currency and Home Currency

4. Concept of Hedging in Over-the-counter Market

5. Introduction to Forex Rates Determination

6. Interest Rate Parity Theory

CONCEPT OF BASE CURRENCY AND HOME CURRENCY

In India, INR against USD is quoted as USD/INR. The left-side currency is known as base currency and the right-side currency is known as home currency.

Table 3.1 Quoting Convention

DIRECT AND INDIRECT QUOTES

- Direct quotes: Under this system, the exchange rate for foreign currency is expressed in the form of local currency equal to one unit of foreign currency. For example, USD 1.00 = INR 48.50 will be a direct exchange rate for the US dollar in India against Indian rupees.

- Indirect quotes: Under this system, the exchange rate is quoted in terms of the number of units of the foreign currency equal to one unit of local currency. For example, USD 2.0619 = INR 100 will be corresponding indirect quotation in India for the US dollar.

Until August 1993, USD/INR exchange rate was quoted under the system of indirect quote. The quotes used to be in terms of foreign currency units equal to INR 100. Subsequently, the system of direct quotes was adopted and consequently now the quotes are in terms of INR equal to a unit of foreign exchange.

CURRENCY REGIMES

There are three types of currency regimes, classified on the basis of the following:

- When (time issue)

- Where (place issue)

- How much (amount of currency you can trade, convert in the market)

The three currency regimes are as follows:

- Fully convertible

- Partially convertible

- Pegged

Fully Convertible

The currencies which are convertible at any place, any time and any amount are called fully convertible currencies. The currencies of countries like Europe, the United States, Australia, Japan, the United Kingdom, New Zealand, Switzerland and Canada are fully convertible currencies. The fully convertible currencies can be freely traded in any economy, in any amount and at any time in different parts of the world.

Partially Convertible

These currencies are partially convertible and cannot be freely traded in, or in unlimited amount or at all times, in different parts of the world. The currencies of emerging markets like India, Pakistan, Thailand and Latin American countries like Brazil, Mexico and Chile are partially convertible currencies. In these economies, the central banks frequently intervene to regulate their conversion rates versus other currencies for their economy’s benefit.

For example, in India

- USD/INR trades in the market only between 09:00 a.m. and 05:00 p.m.

- There are restrictions on both current and capital account transactions.

- There is a detailed set of rules and regulations for hedging of exposures which needs to be complied by market participants.

Pegged

In this type of market, the central bank fixes the upper and lower limit/band of its currency with another currency where it has major exposure. Hence, it can be said that the central bank fixes the percentage of volatility against a currency or basket of currencies depending upon the economy’s exposure and interest. Such percentage may vary from country to country. Whenever the currency market rate breaches such volatility ranges, the central bank of that country intervenes and brings the same within the desired range. For example, Chinese Yuan is pegged against the USD.

CONCEPT OF HEDGING IN OVER-THE-COUNTER MARKETS

Fluctuation in the exchange rates, i.e., either appreciation or depreciation can have favourable or unfavourable cash flow impact on an exporter or an importer, and this can be potentially detrimental to his financial position. To prevent/insure himself against such uncertainty of cash flows, the exporter/importer hedges his exposures through forward/options/swaps by entering into contract with counterparties like banks/financial institutions which are authorized to deal and make markets in these products.

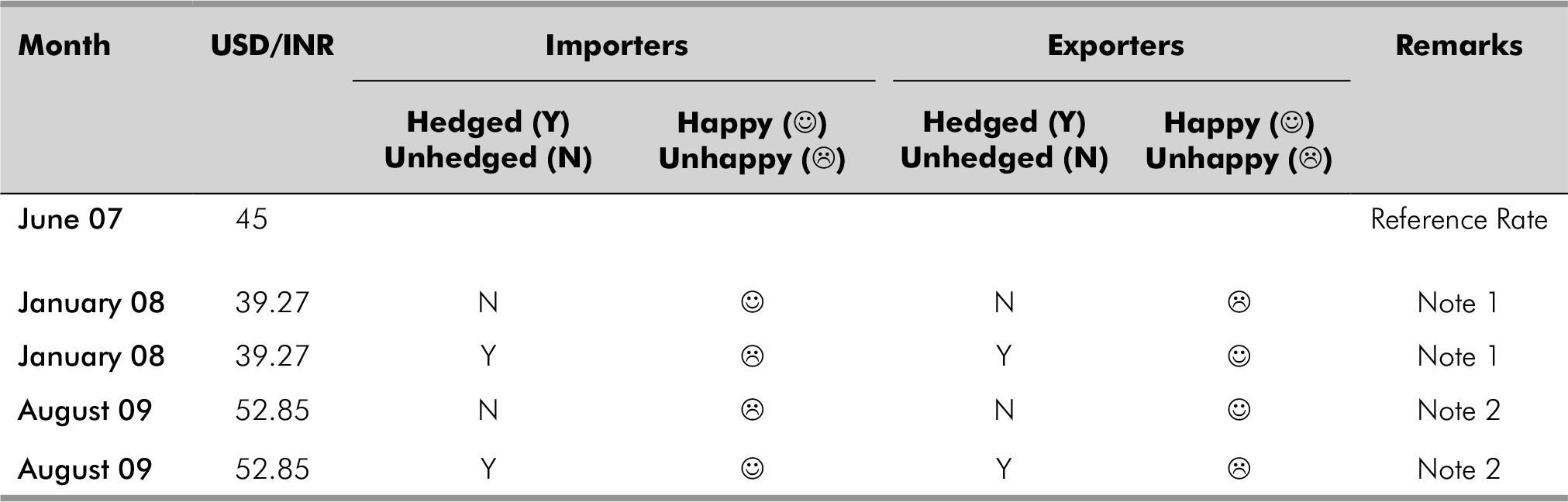

Hedging in simple terms is like ‘securing a rate or freezing a certain rate for foreign currency receivable/payable’. Fluctuations in exchange rates, post hedging, do not affect the hedged party, as his cash flows are crystallized. However, there might be notional opportunity gain/loss. Table 3.2 illustrates the same with an example.

Table 3.2 Exposure of Importer and Exporter

In the above example, the exposure, i.e., import/export, arose when the prevailing USD/INR exchange rate was 45. Hence, this is termed as the reference rate. Assuming that the exposure was unhedged at that point of time, there could have been two scenarios which are mentioned as follows:

- Scenario/Note 1: In case exposure was unhedged, the importer would have been happy since his INR outgo would have reduced per unit of USD, and the exporter would have been unhappy since his INR realization would have reduced per unit of USD and it would have been vice versa in case the exposures were hedged at inception.

- Scenario/Note 2: In case exposure was unhedged, the importer would have been unhappy since his INR outgo would have increased per USD, and the exporter would have been happy since his INR realization would have increased per unit of USD and it would have been vice versa in case the exposures were hedged at inception.

Table 3.3 Important Understanding

INTRODUCTION TO FOREX RATES DETERMINATION

Depending on the time and day on which foreign currency is exchanged between two counterparties, foreign exchange rates can be classified as follows:

Cash Rate

This is the rate which is quoted for buying/selling of currency where the inward/outward remittance of the respective foreign currency (FCY) takes place on the same day. This rate can be less or more than the spot rate depending on the interest rate and the demand/supply of currency.

Tom Rate (i.e. Rate for Tomorrow)

This is the rate which is quoted for buying/selling of currency where the inward/outward remittance of the respective FCY, takes place on the next working day. This rate can be less or more than the spot rate depending on the interest rate and demand and supply of currency.

Spot Rate

This is the rate which is quoted for buying/selling of currency where the inward/outward remittance of the respective FCY happens on the spot date. The spot date for the majority of currencies is T (i.e. today) + two working days. However, in case of certain currencies like Russian Ruble (RUB) and Canadian Dollar (CAD), it is T+1, i.e., in these cases ‘tom rate’ and ‘spot rate’ would be the same.

Spot rates of fully convertible currency are determined through the economics of demand and supply but in case of partially convertible currency and pegged currency, they are determined through a combination of market demand and supply and central bank action.

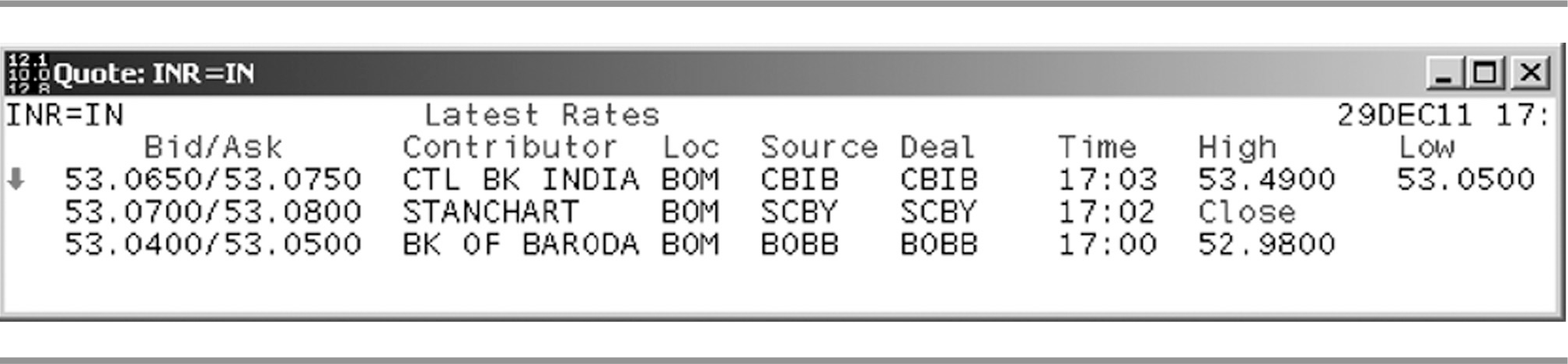

The screenshots of actual screen where USD/INR exchange rates are displayed in real-time are shown below:

Screenshot 3.1 Spot Rate

Forward Rate

This is the rate which is quoted for buying/selling of currency where the inward/outward remittance of the respective FCY happens beyond spot date, i.e., rate quoted for exchange beyond T + two days for the majority of FCY and rate quoted for few currencies like RUB and CAD for value beyond T + one day would be termed as forward rate. These rates are calculated based on the demand/supply dynamics and the interest rate parity theory.

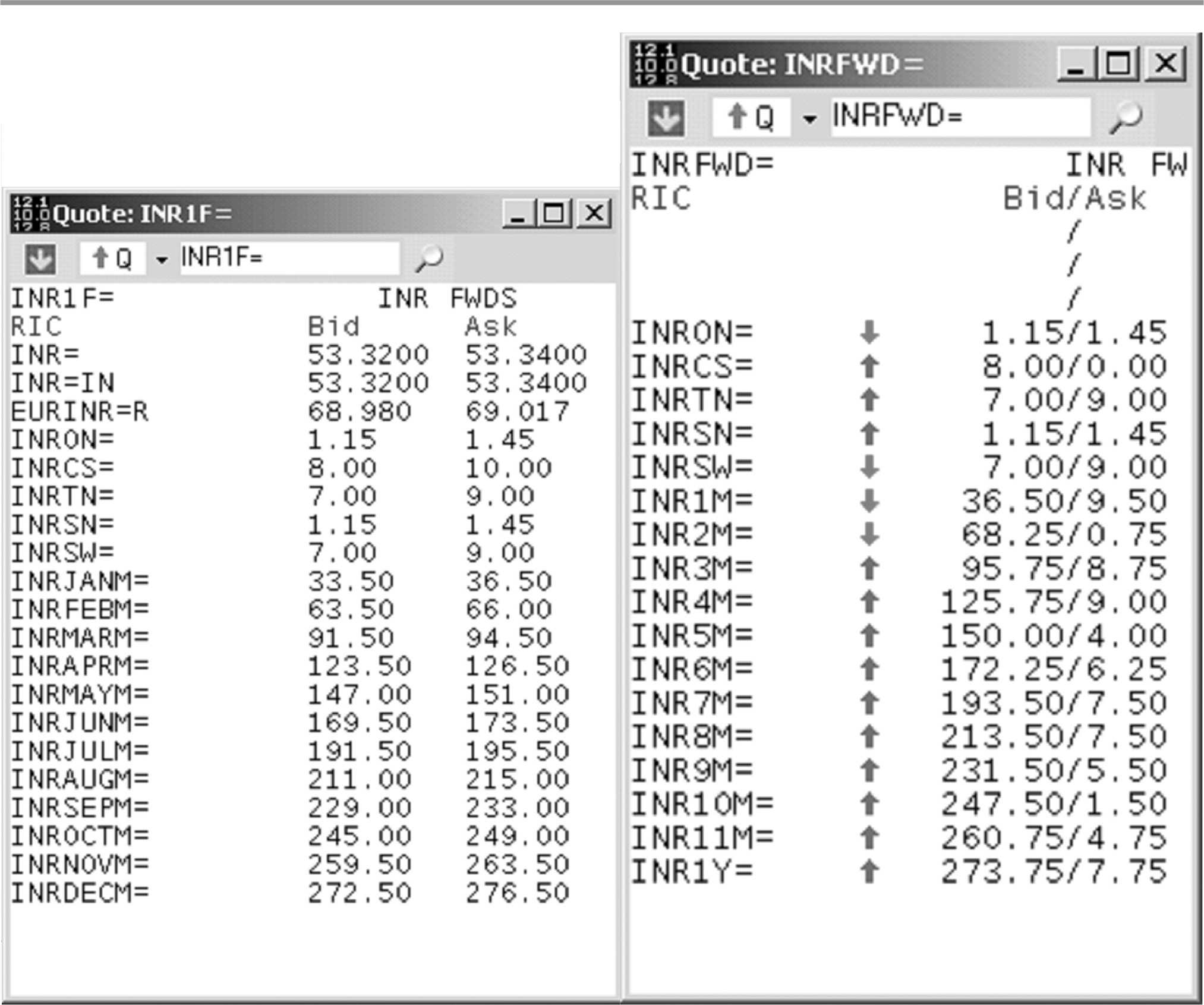

The below screenshot shows the forward points in USD/INR currency pair. These forward points are to be added to spot USD/INR rate to arrive at the final outright forward rate. There are two screens below. First screen provides one with forward swap points for every month end for next one year and another screen provides one with forward swap points for every rolling month, i.e., one month, two months……one year from the spot date (i.e. Today + two days). In the real world, market participants add or subtract the relevant forward points to spot rate to determine outright forward rates.

Screenshot 3.2 Forward Rate

Important Related Notes

Note 1: By default rate is spot rate The default rate quoted and traded in the market by various market participants for any currency is spot rate. All the other rates are derived by making adjustments to the spot rate. Although there are various theoretical formulas and models to determine the rate, the market has its own unique way of determining these adjustments based on demand and supply. The same is discussed in-depth later in this chapter.

Example

On 10 July 2011 at 10.00 a.m., an exporter requested his bank for providing him with FCY/LCY rate for conversion of his USD deposit to INR. The transaction was concluded at the rate of 45. By default, this would mean that the actual currency exchange between the exporter and bank would happen on spot date, i.e., 12 July 2011.

Note 2: Cash rate, tom rate and forward rate concept

Continuing the given example

In case on 10 July 2011 at 10.00 a.m., the exporter conveys to the bank that he wants INR to be credited to his account on the same day, i.e., 10 July 2011 itself, then the bank shall provide him with cash rate which would normally be different from the spot rate. It might be as follows:

- Less than 45

- More than 45

- Even equal to 45

In case on 10 July 2011 at 10.00 a.m., the exporter conveys to the bank that he wants INR to be credited to his account the next day, i.e., 11 July 2011, then the bank shall provide him with tom rate which would also normally be different from cash rate and spot rate. It might be as follows:

- Less than 45

- More than 45

- Even equal to 45

In case on 10 July 2011 at 10.00 a.m., the exporter conveys that he wants INR to be credited to his account at any date beyond spot date (12 July 2011), then the bank shall provide him with forward rate which would also normally be different from cash/tom/spot rate. Forward is ideally a tool of hedging and the simplest form of derivative.

Note 3: Foreign exchange rates keep on fluctuating unless they are pegged Foreign exchange rates normally keep on fluctuating provided they are not pegged by the central bank of a particular country. Foreign exchange rates are dynamic and are subject to continuous change, i.e., the rates available at 10 a.m. on 10 July 2010 shall be different from the rates available later during the same day or even the same hour.

Note 4: Interbank rates and client rates are different There is always a difference between prevailing interbank rates and client rates due to margin/ spread being charged by the bank. The client rates are communicated and transactions are concluded in forex markets via voice mode or electronic platforms like Reuters/Bloomberg dealing terminals or the bank’s own electronic platform.

Note 5: There’s a difference between the offer rate and the bid rate In the interbank market, market making institutions provide two way quotes, i.e., a rate to buy as well as sell FCY.

Example

A USD/INR quote of bid rate 45/offer rate 45.01 by the market making institution (Bank A) means Bank A is willing to buy USD against INR at 45 and sell USD against INR at 45.01.

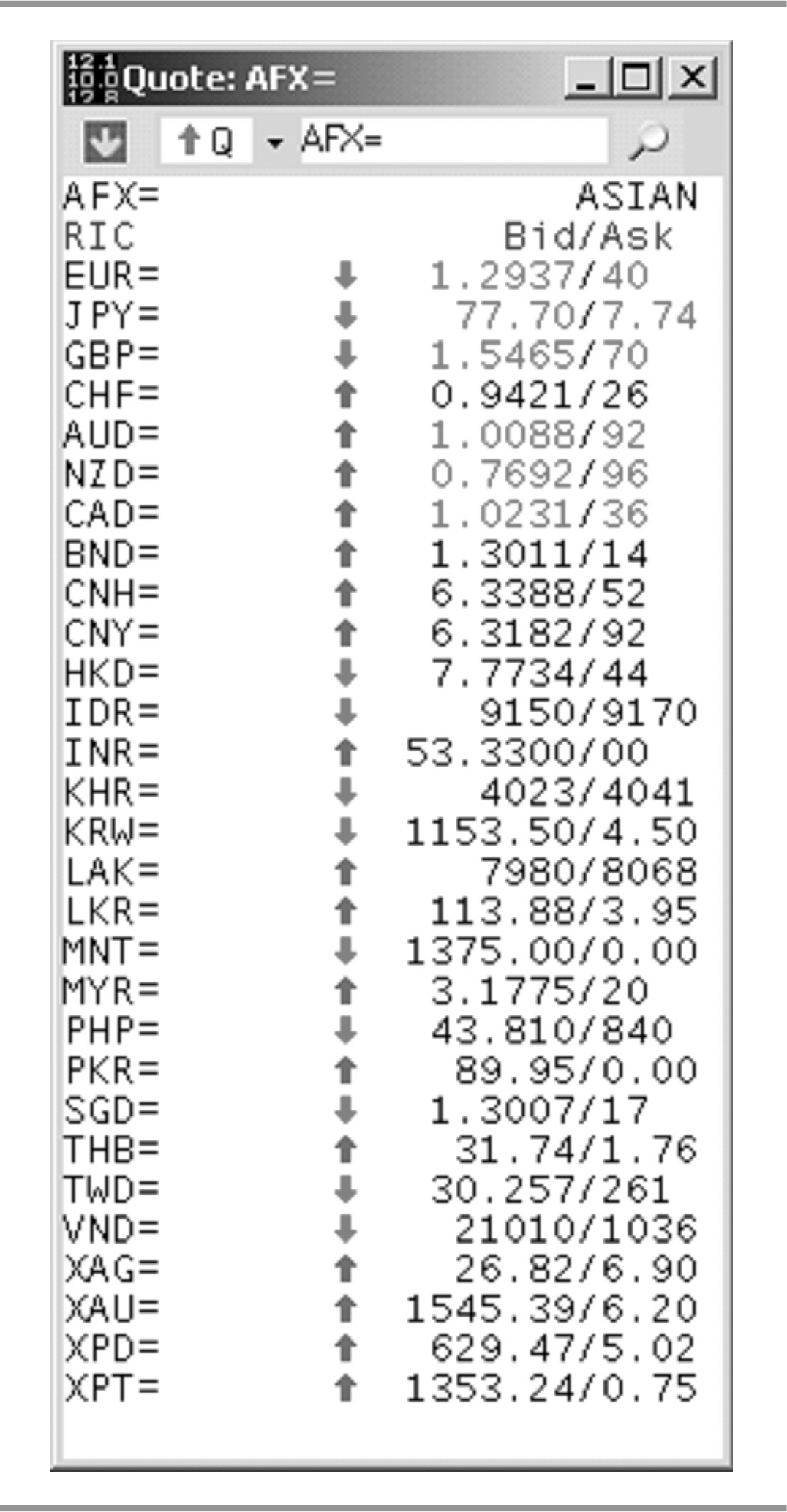

Screenshot 3.3 Major Currency Quotes Traded in Asian Time Zone

Note 6: Display of such interbank rates There are certain large companies which provide services in making the interbank rates available to all constituents, namely, Reuters, Newswire and Bloomberg, for a fee. The majority of the market participants, irrespective of how small or big they are, use these screens as they relay live streaming prices. Refer to screenshot 3.3 from Thomson Reuters 3000Xtra as an example to display live market rates for major currencies traded in Asian Time-zone.

Background to Bretton Woods

The foundation of the International Monetary system was laid in a conference held at Bretton Woods, New Hampshire, United States, in July 1944, post Second World War. Representatives of 45 governments participated in the Bretton Woods conference and settled the articles of agreements of a new international organization. The International Monetary Fund came into being in December 1945 after 44 countries (other than the erstwhile Soviet Union) signed the articles of agreement. The International Bank for Reconstruction and Development (‘World Bank’) was also formed as part of the deliberations at Bretton Woods. The Bretton Woods conference took place while the war was still going on but the allied powers were by then sure of winning it. As a result of the war, most of the European economies had been devastated. So was the case with Japan. The only major industrial power whose economy was relatively unaffected by the war was the United States. It was against this background that the two Bretton Woods institutions, namely, the International Monetary Fund and the World Bank, were formed. Apart from the damage done to the world economy by the war, the experience of pre-war decades emphasized the need for international monetary cooperation. The gold standard, under which a currency’s value was fixed in terms of gold (and money in circulation was limited to the availability of the gold with the country’s treasury), had worked reasonably well from the nineteenth century to the First World War. During that period, the United Kingdom was the world’s premier trading and lender country. After the war, the United Kingdom could no longer play that role. By then, the United States had become the largest economy and had accumulated huge stocks of gold. In the late 1920s, as the stock market crash pushed the United States into a recession, American imports fell and the consequent trade deficits in European countries had to be financed by export of gold. That, in turn, meant a drop in domestic money supply and deflation. To counter domestic unemployment, many countries resorted to competitive devaluations, multiple exchange rates and other measures to protect domestic economies. In 1931, the United Kingdom quit the gold standard and 25 other countries followed suit. Overall, the gold standard came to be identified with the 1930s deflation and unemployment. The worldwide depression really ended only with the beginning of the Second World War. But the experience of the 1930s underlined the importance of international monetary co-operation. Thus, the state of the world economy towards the end of the Second World War and the experience of the previous decades, both cried out for a greater degree of international monetary co-operation than had been the case until then. It was no wonder, therefore, the Bretton Woods conference succeeded in giving birth to a new International Monetary system.

INTEREST RATE PARITY THEORY

In markets where exchange rates and interest rates are determined by demand and supply, and banks are free to deposit/ borrow foreign currencies (full convertible currency economy), the forward premium/discount (i.e. difference between spot and forward foreign exchange rates) are governed by the interest parity principle. In effect, in an efficient market, the forward margin on an exchange rate will be equal to the interest differential between the two currencies. However, in economies which are not fully convertible on current and capital account, demand/supply plays a major role in determining forward premium/discount.

Example

| Assumption | ||

| Prevailing USD/INR spot rate | = | 45 |

| India Rate of Interest | = | 8 per cent per annum |

| US Rate of Interest | = | 3 per cent per annum |

One method of arriving at one year forward rate of USD/INR can be to make reasonable estimate based on information available currently and expectations built for future. However, this is a risky proposition as there is no precise method to predict the exchange rate, and the estimates might go wrong.

Another conservative method is to calculate forward based on cost of borrowing and investing. For example, Person A borrows USD today at 3 per cent p.a. rate of interest from the US market and converts the same to INR at the prevailing USD/ INR exchange rate of 45. Subsequently, Person A deposits the same in bank for a tenor of one year and receives 8 per cent p.a. Thus, he would earn 5 per cent p.a. on account of interest rate differential. However, at the end of one year he would have to convert his INR proceeds into USD at the then prevailing exchange rate to repay USD borrowings. However, prevailing exchange rate can be more or less or equal to 45. The three potential scenarios and their impact are explained as follows:

- Scenario 1: In case the prevailing exchange rate post one year is less than 45, the Person A would earn interest rate differential as well as exchange rate differential.

- Scenario 2: In case the prevailing exchange rate post one year is 45, the Person A would earn interest rate differential only.

- Scenario 3: In case the prevailing exchange rate post one year is greater than 45, the Person A would earn interest rate differential but lose on account of exchange rate differential.

Thus, in order to hedge his exposure from currency fluctuations, Person A can enter into forward contract agreement on the day when he borrowed USD. Ideally, bank would provide him rate after adding 5 per cent premium to prevailing spot rate. This transction would earn him no profit. In case due to demand/supply situation bank charges him premium lower than 5 per cent, then he would profit from this transaction and this is termed as arbitrage.

- Important Note 1: Since Indian rupee is partially convertible currency, forward premium do not necessarily reflect interest rate differential.

- Important Note 2: In case of EUR/USD and such other fully convertible currencies, the interest rate parity theory normally holds good. In these currencies, ideally interest rate differential between them would be exactly equal to the forward discount/premium for the currency pair. However, in times of crisis, the interest rate parity theory does not work due to lack of availability of currency which is USD in today’s environment.

- Important Note 3: The forward premium is referred to as the premium on the currency of which forward rate is costlier than the spot rate, and the forward discount is on the currency of which forward rate is cheaper than the spot rate. In the cited interest rate scenario, the USD is at premium and INR is at a discount in the forward market.

When it is mentioned in the context of left hand side currency, it is always mentioned in the context of USD and it is to be quoted that the forward market is in premium. This means when USD is in premium against USD/INR, then it is going to appreciate in forward market.

In general, a currency will be at a premium vis-à-vis a higher interest currency and at a discount vis-à-vis a lower interest currency. Forward premium/discount is quoted using the same market convention as is used for spot. Normal market convention has been explained in earlier part of this chapter. For example, if the exchange rate is quoted as INR 45 per dollar, the forward margin will be quoted in paisa per dollar which means the forward premium for one year shall be quoted as 200 paise.

The relationship between interest differential and forward margins is a stable one. If it is disturbed, it will throw open arbitrage opportunities and arbitrage transactions will restore interest parity.

The pricing of a foreign exchange forward is equivalent to determining the forward foreign exchange rate. Since the expected net present value of forward foreign exchange contract must be zero at inception, the easiest way to obtain the forward exchange rate is to determine the exchange rate that ensures that the net present value of the contract is zero. This relation is called as interest rate parity.

The forward foreign exchange rate at contract inception, Ft, can be calculated with either of the following two general formulas:

| Formula 1: Simple Method: | Ft = S0 × [(1 + R)/(1 + L)] |

| Formula 2: Continuous Compounding: | Ft = S0 × e(R − L) × T |

where

Ft = forward foreign exchange rate at time period T

S0 = today’s spot foreign exchange rate

R = rate of interest for currency on right hand side for time period T

L = rate of interest for currency on left hand side for time period T

(Refer to Table 3.1: Quoting Convention.)

CALCULATION OF RATES

How Do Banks Calculate Value Cash/Value Today Foreign Exchange Rate?

Value cash/value today rate is calculated as follows:

Case 1: If cash/spot points are in premium, then the value cash rate is calculated as follows:

Case 2: If cash/spot points are in discount, then the value cash rate is calculated as follows:

Value tom rate is calculated in a similar manner. The only difference in the above formula is the replacement of cash/ spot points with tom/spot points.

Indicative spot rate, cash/tom points, tom/spot points, forward points are available for viewing on Reuters, Bloomberg, Newswire, etc. In screenshot 3.2, ‘INRCS =’ refers to cash/spot points and ‘INRTN =’ refers to tom/spot points.

MISCELLANEOUS ILLUSTRATIONS

ILLUSTRATION 1

If interbank spot rate is 48.60/48.62 and cash spot rate is 2/3, then calculate

- Spot rate for an exporter

- Spot rate for an importer

- Value cash rate for exporter

- Value cash rate for importer

Solution

Cash spot rate of 2/3 implies that market is in premium. When market is in premium, the rates are as follows:

- Spot rate for an exporter is 48.60

- Spot rate for an importer is 48.62

- Value cash rate for exporter is calculated as follows:

Value cash rate = bid side spot rate − offer side of cash/spot points= 48.60 − 0.03= 48.57

- Value cash rate for importer is calculated as follows:

| Exporter | Importer | |

|---|---|---|

| Interbank spot rate | 48.60 | 48.62 |

| Interbank cash rate | 48.57 | 48.60 |

ILLUSTRATION 2

In the above example, what is the cash rate for the exporter and the importer, if the bank has to keep the margin of one paise?

Solution

For exporter, margin is subtracted from the value cash rate.

Therefore, cash rate is 48.57 − 0.01 = 48.56

For importer, margin is added to the value cash rate

Therefore, cash rate is 48.60 + 0.01 = 48.61

ILLUSTRATION 3

If interbank spot rate is 48.60/48.62 and cash spot rate is 3/2, what is

- Spot rate for an exporter

- Spot rate for an importer

- Value cash rate for an exporter

- Value cash rate for an importer

Solution

Cash spot rate of 3/2 implies that market is in discount. When market is in discount, the rates are as follows:

- Spot rate for an exporter is 48.60

- Spot rate for an importer is 48.62

- Value cash rate for an exporter is calculated as follows:

Value cash rate = bid side spot rate + offer side of cash/spot points= 48.60 + 0.02= 48.62

- Value cash rate for an importer is calculated as follows:

Value cash rate = offer side spot rate + bid side of cash/spot points= 48.62 + 0.03= 48.65

Exporter Importer Interbank spot rate 48.60 48.62 Interbank cash rate 48.62 48.65

ILLUSTRATION 4

In the same example, what is the cash rate for the exporter and for the importer if the bank has to keep a margin of 0.01 paise?

Solution

For exporter, margin is subtracted from the interbank cash rate Therefore, cash rate is 48.62 − 0.01 = 48.61

For importer, margin is added to the interbank cash rate

Therefore, cash rate is 48.65 + 0.01 = 48.66

Important Concept: Cross Currency

An Indian exporter exporting goods to Japan would need to convert JPY inward remittance to INR and reverse would be true for an importer importing goods from Japan.

In order to convert JPY into INR or INR into JPY, you have to first convert the same into USD and subsequently into another currency. Hence, USD is also known as vehicle currency.

ILLUSTRATION 5

If interbank spot rate is USD/JPY 110.24/110.26 and cash spot rate is 20/30 and USD/INR 48.50/48.52 and cash/ spot is 3/4. What is:

- Spot rate for an exporter?

- Spot rate for an importer?

- Value cash rate for an exporter?

- Value cash rate for an importer?

Assume that all exports are made to Japan and similarly imports are from Japan.

Solution

Cash spot rate of 20/30 and 3/4 imply market is in premium for both the currencies.

- Interbank spot rate USD/JPY for exporter is 110.26 and USD/INR is 48.50.

- Interbank spot rate USD/JPY for importer is 110.24 and USD/INR is 48.52.

- Interbank cash rate for exporter is calculated as follows:

For Exporter

Exporter receives inward remittance in JPY which has to be converted into INR. There are two steps involved in this process:

Step 1: Convert JPY into USD, i.e., buy USD/JPY currency pair

Step 2: Convert USD into INR, i.e., sell USD/INR currency pair

Cash rate for buying USD/JPY = Offer side of USD/JPY − Bid side of Cash/Spot premium

Cash rate for selling USD/INR = Bid side of USD/INR − Offer side of Cash/Spot premium

JPY/INR rate is calculated as USD/INR ÷ USD/JPY = JPY/INR

i.e. 48.46/110.06 = 0.4403

Hence, value cash rate for an exporter is JPY/INR = 0.4403

For Importer

Importer has to pay for outward remittance in JPY which needs to be generated from INR. There are two steps involved in this process:

Step 1: Convert INR into USD, i.e., buy USD/INR currency pair

Step 2: Convert USD into JPY, i.e., sell USD/JPY currency pair

Cash rate for buying USD/INR = Offer side of USD/INR − Bid side of Cash/Spot premium

Cash rate for selling USD/JPY = Bid side of USD/JPY − Offer side of Cash/Spot premium

JPY/INR rate is calculated as USD/INR ÷ USD/JPY = JPY/INR,

i.e., 48.49/109.94 = 0.4411

ILLUSTRATION 6

If interbank spot rate of EUR/USD = 1.4050 (Euro Libor = 3 per cent and USD Libor = 1 per cent), what is three months and 12 months forward rate and premium/discount using interest rate parity theory?

Solution

Forward Rate = 1.4050 × (1.01/1.03) = 1.3777

Discount = 1.4050 − 1.3777 = 0.0273

Three months Forward Rate = 1.4050 × [(1 + (0.01 × 3/12))/(1 + (0.03 × 3/12))] = 1.3980

Discount = 1.4050 − 1.3980 = 0.007

ILLUSTRATION 7

If interbank spot rate of GBP/AUD = 1.4365 (GBP Libor = 3 per cent and AUD Libor = 4 per cent), answer

- Is the forward rate of this currency pair in premium or discount?

- Calculate six months forward.

- Calculate annual premium/discount in pips or percentage.

- If annual premium is 3 per cent on spot, what would be the eight months forward rate?

Solution

- Forward Rate = 1.4365 × [1.04/1.03] = 1.4504

Premium = 1.4504 − 1.4365 = 0.0139. Hence, forward rate is in premium.

- Six months Forward Rate = 1.4365 × [(1 + (0.04 × 6/12))/(1 + (0.03 × 6/12))] = 1.4435

Premium = 1.4435 − 1.4365 = 0.0070

- Annual percentage = (0.0139/1.4365) × 100 = 0.9676 per cent

- Eight months Forward Premium = 1.4365 × 0.03 × (8/12) = 0.02873

Eight months Forward Rate = 1.4365 + 0.02873 = 1.4652

ILLUSTRATION 8

If interest rate is 5 per cent for USD and 8 per cent for INR, calculate premium or discount. Assume spot rate of USD/INR = 48.60.

Solution

Forward = 48.60 × (1 + 0.08/1 + 0.05) = 49.9886, hence premium = 49.99 − 48.60 = 1.39

ILLUSTRATION 9

If interest rate is 3 per cent for EUR and 6 per cent for USD and spot rate is EUR/USD = 1.4020, calculate three months premium in percentage.

Solution

Forward = 1.4020 × (1 + 0.06/1 + 0.03) = 1.4428 and Premium = 1.4428 − 1.4020 = 0.0408

So, three months premium = 0.0102 [0.0408/4]

In percentage = 0.0102/1.4020 × 100 = 0.72 per cent

ILLUSTRATION 10

If interest rate is 3 per cent for USD and 8 per cent for INR and spot USD/INR = 48.60 and forwards are one month – 10 paisa, two months 20 paisa and three months 30 paisa. Find out whether there is any arbitrage opportunity in three months tenor.

Solution

Forward = 48.60(1 + 0.08/1 + 0.03) = 50.96

Three months premium = (50.96 − 48.60)/4 =0.59

So, forward = 48.60 + 0.59 = 49.19

Now as per given rate, forward = 48.60 +.30 = 48.90. Hence, there is a possibility of arbitrage.

ILLUSTRATION 11

If interest rate is 2 per cent for EUR, 3 per cent for USD and 8 per cent for INR and spot EUR/USD = 1.4020 and spot USD/INR = 48.50, calculate the rate at which exporter of EUR in India can hedge for one year.

Solution

EUR→USD→INR→

EUR/INR = 1.4020 × 48.50 = 67.997

Forward rate = 67.997(1 + 0.08/1 + 0.02) = 71.9968

ILLUSTRATION 12

Spot on interbank treasury screen: EUR/USD = 1.4020/40

- Calculate the interbank spot rate for an exporter of EUR in US.

- Calculate the interbank spot rate for an importer of EUR in US.

- Calculate the interbank spot rate for an importer of USD in Europe.

- Calculate the interbank spot rate for an exporter of USD in Europe.

Solution

- Interbank spot rate = 1.4020

- Interbank spot rate = 1.4040

- Interbank spot rate = 1.4020

- Interbank spot rate = 1.4040

ILLUSTRATION 13

Spot on interbank treasury screen: AUD/USD = 0.9650/70

- Calculate the spot rate for an exporter of USD in Australia and margin 20 pips.

- Calculate the spot rate for an importer of AUD in US and margin 20 pips.

Solution

- Spot rate = 0.9690

- Spot rate = 0.9690

ILLUSTRATION 14

Spot on interbank treasury screen:

EUR/CAD = 1.0640/60

EUR/USD = 1.4020/40

USD/JPY = 124.80/00

CAD/NZD = 0.9835/40

Calculate cross currency spot rate for converting JPY to NZD.

Solution

Step 1: What is required?

NZD/JPY or JPY/NZD

Step 2: Identify the path of conversion

JPY-USD-EUR-CAD-NZD

Step 3: Identify the rates on each leg

USD/JPY = 125 EUR/USD = 1.4040 EUR/CAD = 1.0640 CAD/NZD = 0.9835

Step 4: To get the required rate (as in step-1) we need to multiply/divide the currency pairs

(USD/JPY) × (EUR/USD) × (1/(EUR/CAD)) × (1/(CAD/NZD))

Step 5: Fill in the rates as identified in step-3

125 × 1.4040 × 1/1.0640 × 1/0.9835

Hence, NZD/JPY = 167.71

ILLUSTRATION 15

Spot on interbank treasury screen:

USD/INR = 45.30/40

EUR/USD = 1.4535/45

GBP/CHF = 1.6510/20

CHF/AUD = 1.0120/30

Calculate the cross currency rate for an importer invoicing in Australian dollar in India for value spot taking into account margin of 20 paisa on the rate finally arrived.

Solution

Step 1: What is required?

INR/AUD or AUD/INR

Step 2: Identify the path of conversion

INR-USD-EUR-GBP-CHF-AUD

Step 3: Identify the rates on each leg

USD/INR = 45.40 EUR/USD = 1.4545 EUR/GBP = 0.8750 GBP/CHF = 1.6510 CHF/AUD = 1.0120

Step 4: To get the required rate (as in step-1) we need to multiply/divide the currency pairs

(USD/INR) × (EUR/USD) × (1/(EUR/GBP)) × (1/(GBP/CHF)) × (1/(CHF/AUD))

Step 5: Fill in the rates as identified in step 3

45.40 × 1.4545 × 1/0.8750 × 1/1.6510 × 1/1.0120

Hence, AUD/INR after levying margin of 20 pips on end = 45.16 + 0.20 = 45.36

ILLUSTRATION 16

Spot on interbank treasury screen on 1 July 2011:

USD/INR = 48.60/80

C/S = 5/4

One month = 10/12 (31 July 2011)

Two months = 14/16 (31 August 2011)

Three months = 18/20 (30 September 2011)

- Calculate cash rate for an exporter of USD for value today with margin of 20 paisa.

- Calculate forward rate for an exporter who would receive USD on 30 September 2011 with margin of 20 paisa.

- Calculate forward rate an importer who has to remit USD outward on 31 August 2011 with margin of 20 paisa.

Solution

- Cash Rate = 48.60 + 0.04 − 0.20 = 48.44

- Rate = 48.60 + 0.18 − 0.20 = 48.58

- Rate = 48.80 + 0.16 + 0.20 = 49.16

ILLUSTRATION 17

Spot on interbank treasury screen on 30 June 2011:

EUR/USD = 1.4020/40

C/S = 10/20

One month = 40/30

Two months = 30/25

Three months = 25/20

Four months = 20/15

An importer of Euro in the United States has to make payment on 30 September 2011. Calculate forward rate to hedge his exposure for 30 September 2011 assuming margin is 20 pips.

Solution

Rate = 1.4040 − 0.0020 + 0.0020 = 1.4040

TEST YOUR UNDERSTANDING

- Spot on interbank treasury screen:

EUR/USD = 1.2430/40 and C/S = 30/20

USD/JPY = 124.60/70 and C/S = 20/30

EUR/GBP = 0.9850/60 and C/S = 30/10

GBP/CHF = 1.6430/40 and C/S = 20/15

AUD/CHF = 0.9630/40 and C/S = 20/30

Calculate cash rate with margin 20 pips on each for an exporter of JPY in Australia.

- Calculate cross currency spot rate assuming margin of 20 pips on each leg for a person who has to travel from Europe to Japan.

Spot on interbank treasury screen:

GBP/EUR → 1.2460/80

GBP/CHF → 1.4060/70

CHF/AUD → 0.9650/70

AUD/USD → 0.09830/40

AUD/JPY → 130.60/80

- EUR/USD = 1.4020/40 and C/S = 10/20 GBP/USD = 1.6430/40 and C/S = 20/10

1 month = 40/30 (31 July 2011) 1 month = 30/40 (31 July 2011) 2 months = 30/25 2 months = 50/60 3 months = 25/20 3 months = 70/80 4 months = 20/15 4 months = 90/100 - As a consultant to the importer of GBP in eurozone, and having a view that EUR would appreciate against USD, and USD would appreciate against GBP, three months down the line when the remittance has to be made, what should one advise?

- One has to travel from the United Kingdom to Europe on 31 August 2011. However, one is certainly of the view that market would move against him. Calculate forward rate assuming a margin of 20 pips.

-

AUD/GBP = 0.9650/70 and C/S = 30/20 EUR/GBP = 0.8580/00 and C/S = 10/20 GBP/JPY = 136.20/80 and C/S = 20/40 1 month = 100/90 (31 July 2011) 1 month = 90/80 (31 July 2011) 1 month = 30/40 (31 July 2011) 2 months = 90/80 2 months = 80/70 2 months = 40/50 3 months = 80/70 3 months = 70/60 3 months = 50/60 4 months = 70/60 4 months = 60/50 4 months = 60/70 - One has to go to airport of Australia to pick his friend who is coming from JAPAN. His friend does not know the rate of conversion and has only JPY in his pocket when he arrived at airport. Calculate appropriate rate for him assuming margin of 20 pips.

- His friend has to travel to Europe at the end of three months post his stay in Australia. Calculate the advance rate for him assuming margin of 20 pips.

- Based in Australia, in October end, one is planning to go on a trip to Europe. Calculate the rate at which one can lock-in forward rate for that date as of today.

- Answer the questions below taking into account the following currency rates.

USD/INR EUR/USD USD/JPY Spot Rate 48.40/42 1.4042/44 124.80/90 C/S 3/4 10/7 10/12 1 month 15/17 100/90 80/70 2 months 19/21 90/80 60/50 3 months 30/32 80/70 40/30 4 months 36/38 70/60 20/10 - An importer of JPY in India is expecting USD and JPY to appreciate against INR due to which he is looking to hedge his JPY payable for value two months. Assume there is no margin, what should one suggest him to do?

- Exporter of Euro in India is expecting EUR inwards in August end and has a view that USD would appreciate against INR and EUR would depreciate against USD. What should one suggest him to do?

- Calculate forward rate for an importer of EURO in Japan for value two months assuming margin of 20 pips on both legs.

- One has to make immediate value today payment in JPY from India. Calculate value today rate.

- Calculate forward rate for an exporter of JPY in India for value three months.

- In the interbank market, the DM is quoting INR 21.50. If the bank charges 0.125 per cent commission for TT selling and 0.15 per cent for TT buying, what rate should one quote to customer two way?

- A customer wants to sell a bill worth USD 1,000,000 to a bank. The bill might mature any time during the second month. If the bank charges a margin of 0.5 per cent and exchange rates are as given as follows, calculate the rate which the bank is likely to quote.

USD/INR Spot 35.50/35.55 One month forward 15/10 Two months forward 20/15 - Hindustan Ltd. an Indian company has an export of 10 million (100 lacs) JPY, value September end. JPY is not directly quoted against INR. The current spot rates are USD/INR = 41.79 and USD/JPY = 129.75. It is estimated that JPY will depreciate to 144 level and INR to depreciate against USD to 43. Forward rate for September, 2011 USD/JPY = 137.35 and USD/INR = 42.89

- Calculate the expected loss without doing any hedges. How would the position alter with company taking forward cover?

- If the spot on 30 September, 2011 was eventually USD/JPY = 137.85 and USD/INR = 42.78. Was the decision to take forward cover proved right?

- In 2010, a transistor cost USD 22.84 in New York, SGD 69 in Singapore and 14.56 Euros in Europe. The exchange rates in 2010 were USD/SGD = 1.3685 and EUR/USD = 1.4020. Where would one prefer to buy a transistor?

- On January 28 2010, an importer customer requested his bank to remit Singapore Dollar (SGD) 2,500,000 under an irrevocable LC. However, due to bank strikes, the interbank market rates were as follows:

January 28 February 4 USD/INR INR 45.85/45.90 45.91/45.97 GBP/USD USD 1.7840/1.7850 1.7765/1.7775 GBP/SGD SGD 3.1575/3.1590 3.1380/3.1390 The bank wishes to retain an exchange margin of 0.125 per cent. How much does the customer stand to gain or lose due to the delay? (Calculate rate in multiples of 0.0001)

- S and T Ltd operating in a country having USD as its unit of currency has today invoiced sales to an Indian company with credit period of three months from the date of invoice.

The invoice amount is USD 13,750 and at today’s spot rate of USD 0.0275 per INR 1, is Equivalent to INR 5,00,000. The three months forward rate is quoted as USD 0.0273 per INR 1. Calculate the gain/loss to S and T Ltd by entering into a forward contract, if on maturity the exchange rate is USD 0.03.

- The US dollar is selling in India at INR 45.5. If the interest rate for a six months borrowing in India is 8 per cent per annum and the corresponding rate in the United States is 2 per cent.

- Is USD at a premium or discount in Indian forward market?

- Calculate expected six months forward rate for USD in India.

- Calculate forward premium or discount.