CHAPTER 13

Financials

________________

The global financial sector serves as the engine that drives the world economy. From everyday banking transactions to financing the ongoing operations of businesses and world trade, these businesses serve a crucial role in the global economy. While basic financial services like banking and wealth management are a key part of our everyday lives, some of the services these companies provide are dependent on economic conditions, and demand for them can fluctuate significantly. Although relatively predictable, earnings for many businesses in the financial sector are cyclical in nature and vary significantly in different stages of the economic cycle.

Data source: Bloomberg, as of March 18, 2022.

Despite below-average sales growth over the past several years, the financial sector has generated strong profitability, profit growth, and dividend growth. Many of the companies in the sector are interest rate–sensitive, which means that their business prospects can be heavily affected by changes in the level of interest rates. The relationship between interest rates and financial sector earnings is complex, due to crosscurrents that affect industries differently within the sector. For banks, higher interest rates reduce demand for loans, but serve to disproportionally increase lending rates, thus boosting net interest margin (profitability). Conversely, lower interest rates increase demand for loans, but serve to lower net interest margin. We are primarily concerned with the net (combined) effect of a change in interest rates on these businesses. The performance of the equity markets can also impact the financial sector. Relative performance for the financial sector is usually best during the repair phase of the market cycle and poorest in the mid-cycle phase of a bull market. There are nine main industry groups: (1) asset management, (2) banks, (3) capital markets, (4) consumer finance, (5) financial conglomerates, (6) financial data and analytics, (7) life and health insurance, (8) property and casualty insurance, and (9) securities exchanges.

Asset Management

Data source: Bloomberg, as of March 18, 2022.

Businesses in the asset management industry provide wealth management solutions for individuals, as well as investment management and custody services for institutions. Revenues are principally earned by charging a percentage fee based on the dollar amount of assets under management (AUM) or administration (AUA). Traditional asset managers (those who actively manage stock and bond portfolios) have been losing market share to alternative asset managers, passive index funds, and exchange-traded funds (ETFs) in recent years. However, this trend usually reverses following bear markets during which active managers often outperform passive strategies. Other industry trends include customized investment solutions, lower fees, increasing allocations from high-net-worth clients, and the consolidation of relationships among institutional clients. The asset management industry is heavily regulated, and investors must keep themselves apprised of any upcoming or potential regulatory changes. Any economic or political factors that influence public markets can impact net asset values (NAVs) on which asset managers earn a fee. For private equity firms, any factors that move public markets can influence timing and realized value from exits, as well as the deployment of cash. Growth in sales and profitability is thereby determined largely by general changes in overall wealth. A rising stock market, for example, is good news for these businesses since it grows their AUM or AUA on which they earn a fee. Despite intense competition, the industry has generated strong sales and profit growth combined with strong profit margins and has delivered above-average dividend yields. Important metrics for investors to monitor include AUM by segment or product type, changes in AUM (distinguishing between fund flows and market-driven growth), net interest income, revenue and EPS growth, operating expense ratios, operating margins, and management fee margins. For alternative asset managers, net flows, fee-related earnings margin, and distributable earnings are important metrics to track. Standard valuation metrics such as P/E can be used for comparing valuations, while the slightly modified price to fee-related earnings (P/FRE) may provide additional insights for companies that are heavily dependent on fee income as a source of revenue.

Banks

Banks around the world provide people and businesses with a place to keep their savings and borrow funds to invest, buy a home, or fund a new business project. Traditional banks are facing increased competition from online lenders, and there is also a strong trend whereby consumers are conducting more of their banking through online platforms, forcing banks to build out their online presence and improve customer service. Consumer banking tends to be local, while trading and investment banking businesses (considered separately as part of the capital markets industry, although several of the businesses listed here operate in both industries) tend to be more global in nature. GDP growth, employment levels, and changes in interest rates are among the most important economic factors that affect bank sales and profit growth as well as their profitability. The difference between the rate at which banks pay interest on savings and the rate at which they loan money is referred to as the net interest margin (NIM) and is the primary driver of a bank's earnings. Changes in interest rates (which can be viewed through changes in the yield curve) therefore play a critical role in revenue and earnings growth of banks. As interest rates rise, banks can increase loan rates faster than the rate they pay on savings accounts, generating incremental profits in the process. In recent years, these businesses have traded at attractive valuations despite generating relatively high profit margins and attractive dividends yields, most likely due to below-average sales and profit growth. Return on equity (ROE), return on tangible common equity (ROTCE), net interest margin, total deposits, net interest income, fee growth, total revenue growth, loan growth, loan credit quality, changes in loan loss provisions, actual loan losses, the net charge-off (NCO) ratio, nonperforming loan (NPL) ratios, operating leverage, expense ratio, and net payout ratio are all important metrics for investors to monitor. The common equity tier 1 (CET 1) ratio, which compares the capital a bank holds against its risk-weighted assets, provides investors with a measure of the bank's ability to withstand financial crises. All else being equal, a higher CET 1 ratio is preferable. P/E is usually an appropriate measure of valuation for the banking industry, although a sum of the parts or DCF analysis may be required for large, diversified banks that operate in multiple segments of the financial sector.

Data source: Bloomberg, as of March 18, 2022.

Capital Markets

Data source: Bloomberg, as of March 18, 2022.

The capital markets industry plays a key role in executing security transactions around the world, including the trading of debt and equity securities, underwriting (facilitating) the sale of debt and equity securities by companies to investors. The performance of recent IPOs can be tracked using an ETF such as the Renaissance IPO ETF. Recent IPO performance provides an indication of current market conditions and has a bearing on whether companies decide to go public or delay until market conditions improve, thus affecting earnings for the industry. Robust performance of newly traded issues (and the stock market as a whole) can therefore be an indicator for new issuances, which drives earnings for underwriting businesses. Business structure can vary by country due to different regulatory environments that may prevent payment for certain services. Any economic factors that affect public equity and bond markets flow through into the capital markets industry by influencing AUM and AUA levels on which most companies earn a management fee. In addition, some economic factors like monetary policy could influence trading volumes, which affect commissions earned on security trades. Industry revenue and earnings are heavily affected by trading volumes of debt, equity, and derivative securities. These businesses have traded at attractive valuations in recent years, most likely due to below-average profitability, above-average debt levels, and below-average sales and profit growth. Important measures for investors to track include AUM, market share gains and losses by business segment, dollar value of interest-earning assets, net interest margin, net payout ratio, return on equity and return on tangible common shareholder equity (ROTCE), operating leverage, expense and compensation ratios, tax rates, trading revenue growth, and investment banking volumes. Standard valuation metrics such as P/E can be used for comparing valuations.

Consumer Finance

Data source: Bloomberg, as of March 18, 2022.

Consumer finance companies are engaged in extending credit to consumers primarily through credit cards and student, auto, and personal loans. Unlike banks, consumer finance companies are not deposit-taking institutions. They earn fees from interest charged on outstanding credit balances and they may also charge a fee on a per-transaction basis, usually a percentage of the transaction value. While most of these companies extend credit and therefore benefit from lower default rates, some businesses are focused on receivables collection and management and therefore benefit from higher default rates. Consumer finance businesses tend to be local and focused on a specific segment of consumer lending. Investors should note that not all credit card companies are the same. The credit card companies listed here (such as American Express) directly issue credit cards to consumers and, as a result, extend credit to their customers. Visa and Mastercard, in contrast, issue credit cards on behalf of third-party institutions without extending credit to consumers (they simply process transactions). Accordingly, Visa and Mastercard are considered separately in the fintech industry within the technology sector. Economic factors with the biggest influence on firm earnings/sales include GDP growth, interest rates, the level of unemployment, wage growth, and loan default rates. Due to their exposure to consumer spending, they earn higher profits when the economy is strong, and see their profits fall more than the market as economic conditions deteriorate and default rates begin to increase. A substantial portion of revenues are derived from discretionary purchases by consumers, so changes in the health of the economy are an important driver for the industry. These businesses have been trading at attractive valuations despite paying attractive dividends yields and generating above-average sales and profit growth. Important metrics for investors to track include trends in credit losses, loan (or net credit card) growth, consumer spending trends (including travel), and net interest margin. Important financial and operational metrics include ROE/ROTCE, net interest margin, revenue growth, operating leverage, expense ratio, and net payout ratio. Standard valuation metrics such as P/E can be used for valuation purposes.

Financial Conglomerates

Data source: Bloomberg, as of March 18, 2022.

Financial conglomerates are essentially holding companies with a significant portion of revenue generated from the financial sector. However, many of these companies also have investments in other sectors of the market. Economic factors that impact businesses in this industry are therefore dependent on the underlying businesses. Since these companies tend to be very broad-based and operate in several industries, revenue and earnings are not only influenced by economic growth but may also be impacted by many other factors, including changes in interest rates, commodity prices, and employment growth. Despite strong sales and profit growth in recent years, ample reinvestment opportunities have prevented these businesses from paying out higher dividends. As a result, dividend yields and dividend growth rates for the industry have been below the market average. P/E may provide an approximate measure of valuation for the industry. However, these businesses are best analyzed by evaluating the individual business divisions and using a sum of the parts approach to valuing the company. This is especially true in cases where the business operates in several, very distinct, end markets. Berkshire Hathaway (listed above) is an example of a financial conglomerate, with direct ownership of both insurance (Geico) and reinsurance (General Re) companies, a railroad (Burlington Northern Santa Fe), a carpet manufacturer (Shaw Industries), specialty chemicals, a battery maker (Duracell), and utility companies, among others. Financial conglomerates may also hold large investments in nonoperating companies that it does not control, such as Apple, American Express, and Coca-Cola. These investments may be valued simply by using the current share price of the underlying company. Financial conglomerates often trade at a discount to what a sum of the parts analysis would suggest.

Financial Data and Analytics

Financial data and analytics is big business. These businesses provide data and analytics to the financial sector and include credit ratings for consumers, ratings on debt (issued by both corporations and governmental bodies), risk assessment, and proxy voting services, among others. Data service providers in Europe have historically experienced slower growth rates and traded at lower valuation multiples compared to their North American peers. Notable industry trends include increasing adoption and budgets for data and analytics, embedding solutions and analytics within traditional data to create stickier products, and investing in technology to improve product development cycles. Economic factors that have a significant impact on sales growth and profitability relating to the bond rating segment of these businesses include changes in interest rates, mortgage rates, debt/GDP, and GDP growth. Other business segments would be affected by a variety of factors including GDP growth and business sentiment, along with uptake of ESG ratings. Over the past few years businesses in this industry have traded at above-average valuations, driven by strong relative profitability and strong profit growth. Low payout ratios have allowed these businesses to grow their dividends at an above-average rate. ESG is a new area of growth for the industry, and some of the companies listed are adding ESG analysis services to their businesses. Important metrics for investors to track include organic revenue growth by product line (index subscriptions, analytics, ESG, debt ratings, etc.), customer retention and cancellation rates, and adjusted EBITDA margin. Standard valuation measures such as P/E and EV/EBITDA are often used to assess valuations in this industry.

Data source: Bloomberg, as of March 18, 2022.

Life and Health Insurance

Life and health insurance companies offer a wide variety of insurance policies and services to support the needs of individuals, groups, and businesses. Product offerings include life insurance, annuities, disability insurance, critical illness, long-term care insurance, health insurance, critical illness, and annuities. The breadth and complexity of product and service offerings can vary significantly by insurer. Premiums are based on the probability of contingent events (such as mortality rates), policyholder behavior, and expected investment earnings. Individual insurance policies are often long-term in nature with premiums that are set at the time of sale. Group insurance contracts are typically shorter in duration but can include coverages, such as disability insurance, that include long-term obligations. The industry is heavily regulated to ensure that companies retain enough capital to meet their obligations (liabilities) under a variety of adverse scenarios. Fixed income securities comprise the majority of the insurer's asset portfolio supporting its liabilities. These securities provide a steady stream of cash flows to support the liability cash flows. The inability of insurers to match long-term liability cash flows (typically 60 to 80 years into the future) with assets exposes them to reinvestment risk. As interest rates decrease, the insurer may not be able to reinvest at the rates assumed when the premiums were determined. A good time to own life insurance companies is when you think interest rates will rise. Equities are held within the insurer's asset portfolio to support longer-term-liability cash flows and to provide greater yield in both liability and surplus funds, and therefore equity market volatility can significantly impact profitability. Important industry themes include the move to digitization, expense reductions, and improved capital management. Potential changes in accounting standards are important to monitor as they can trigger increased volatility in an insurer's earnings before it can effectively adjust its strategies. Over the past few years, valuations have been below the market, while sales and profit growth have lagged. Important financial and operational metrics to monitor include return on equity, dividend payout ratios, premium growth, net income, accumulated other comprehensive income (AOCI), capital adequacy (solvency ratios), reserve levels and changes, and loss ratios. Given the regulatory pressures on life and health insurers it is important to be aware of potential regulatory changes that could impact the products and services offered. Valuation metrics commonly used include P/E and P/B (AOCI).

Data source: Bloomberg, as of March 18, 2022.

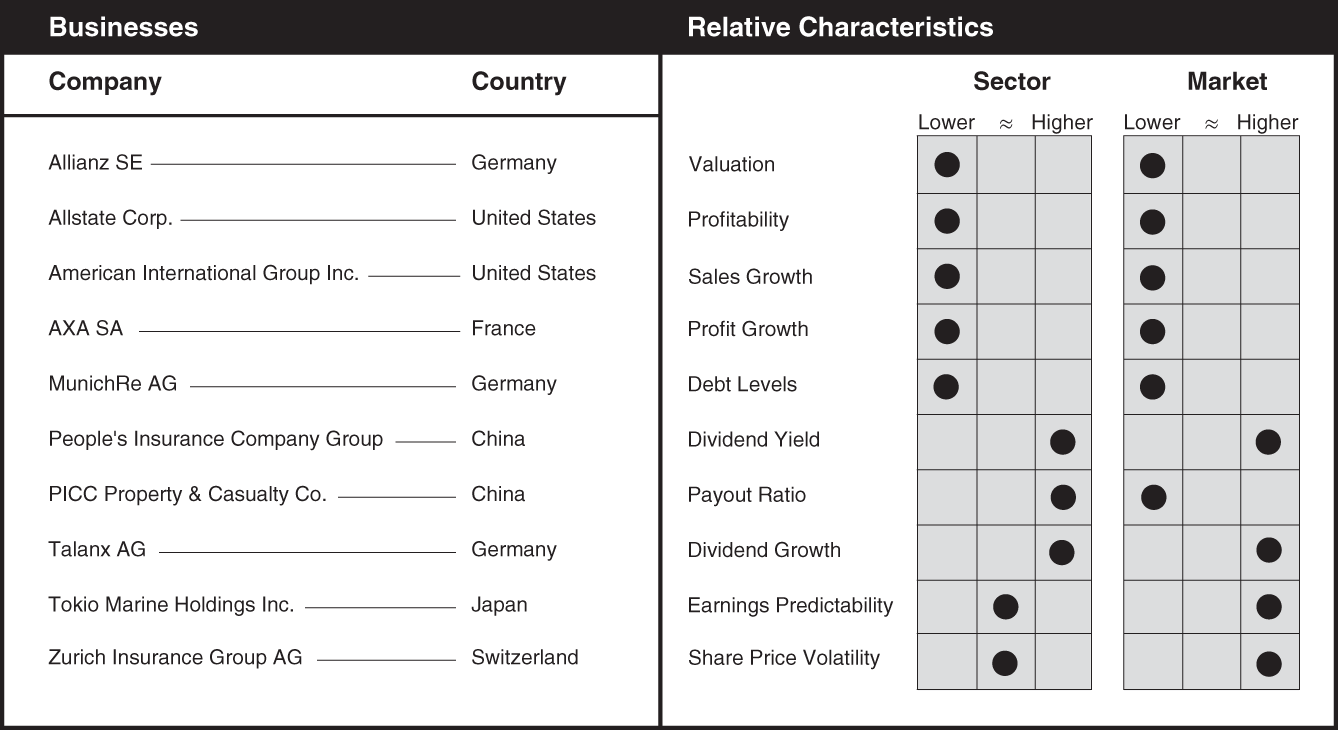

Property and Casualty Insurance

Data source: Bloomberg, as of March 18, 2022.

Property and casualty (P&C) insurers, often referred to as general insurers, provide property and auto insurance coverages to individuals and businesses (including farm). Reinsurance companies, which are used by both P&C and life insurance companies to help manage risk, have also been included in this group since most generate a greater portion of their revenue from the P&C part of their business. To illustrate, if a P&C insurer believes it has too much exposure to one risk factor or geography (such as hurricane insurance in Florida), they can pay a reinsurer to assume some of those liabilities. Natural catastrophes pose the biggest risk to the P&C industry. Hurricane Katrina, for example, is estimated to have cost almost $150 billion, much of which was absorbed by the P&C industry. P&C insurance policies are usually short-term in nature (one year), while life insurance policies could last decades. Solvency ratio calculations (available capital over required capital) differ by geography but, in all cases, indicate the ability of the company to withstand adverse scenarios. A low solvency ratio puts the company in danger of insolvency while a high solvency ratio suggests capital is being underutilized. Both liabilities and investments tend to be shorter in duration for P&C insurers when compared to life and health insurers. The best time to own P&C insurers is when industry pricing is “hard,” where the combined ratio is strong (below 100). The combined ratio is a measure of underwriting performance and indicates whether the premiums collected are enough to pay claims. A company's combined ratio should ideally be less than 100 since a higher number means they need to make up for the shortfall through investment income. Expected catastrophe losses are priced into earnings estimates via “reserves.” However, an unexpectedly large event or number of events in a condensed period may cause P&C firms to incur losses that exceed reserves, which lowers earnings. Potential changes in accounting standards are important to monitor as they can trigger increased volatility in an insurer's earnings before it can adjust its strategies. Important metrics for investors to follow include operating ROE, growth in gross written premium (GWP) and net premiums earned (NPE), combined ratio, solvency ratios, core loss ratios, and prior year claims development (PYD), representing the change in total claims liabilities net of reinsurance from the prior year. PYD is often expressed as a percentage of NPE. The requirement for rate approvals by regulators (where applicable) can have a significant impact on profitability. Regulatory challenges to increasing premium rates may result in the required premium increases lagging claim cost inflation and lead to an erosion of the combined ratio. Standard valuation measures such as P/E and EV/EBITDA are often used to assess valuations in the industry.

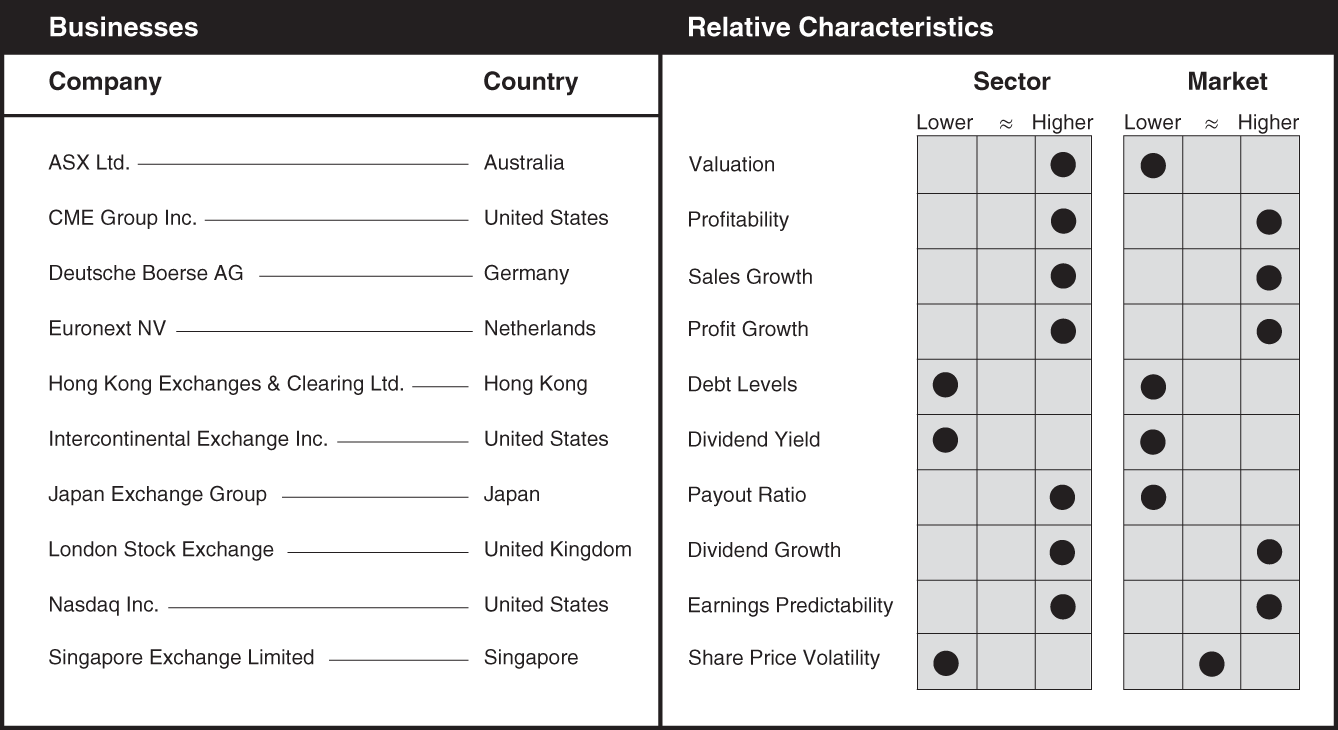

Securities Exchanges

Data source: Bloomberg, as of March 18, 2022.

Security exchanges provide platforms for the trading of financial securities, including stocks, bonds, options, commodities, futures, and, more recently, cryptocurrency. This once was conducted exclusively in a physical location (exchange floor), but now most trading takes place electronically. Industry earnings are most susceptible to overall trading volumes, which makes them a good indicator for assessing investor sentiment and the overall health of the industry. Investor sentiment is an important economic factor for the exchange industry, as is the pace of new company listings. As with most industries within the financial sector, security exchanges are tightly regulated and have built-in safeguards to protect investors and ensure the integrity of the financial market. A well-functioning exchange is key to the success of a country's long-term economic development. Securities exchanges generate revenue primarily from listing fees, and by selling real-time pricing, trade, and index data generated through the exchange. Sales and profit growth for the industry have also benefited from an abundance of new company listings and new financial products. Companies in this industry have been trading at higher valuations compared to the financial sector largely due to their above-average growth rates and profitability. Although their dividend yields have been below the market, they have grown their dividends at an above-average rate. Important metrics for investors to track include total revenue, trading volumes (dollar value or number of securities/contracts), rates per security/contract, number of new listings, newly listed product types, total expense ratios, adjusted EBITDA, and adjusted EBITDA margin. Standard valuation metrics such as P/E, P/CF, and EV/EBITDA can be used to compare valuations between companies in this industry.