Testing a trading strategy involves backtesting against historical data to fine-tune alpha factor parameters, as well as forward-testing against new market data to validate that the strategy performs well out of sample or if the parameters are too closely tailored to specific historical circumstances.

Pyfolio allows for the designation of an out-of-sample period to simulate walk-forward testing. There are numerous aspects to take into account when testing a strategy to obtain statistically reliable results, which we will address here.

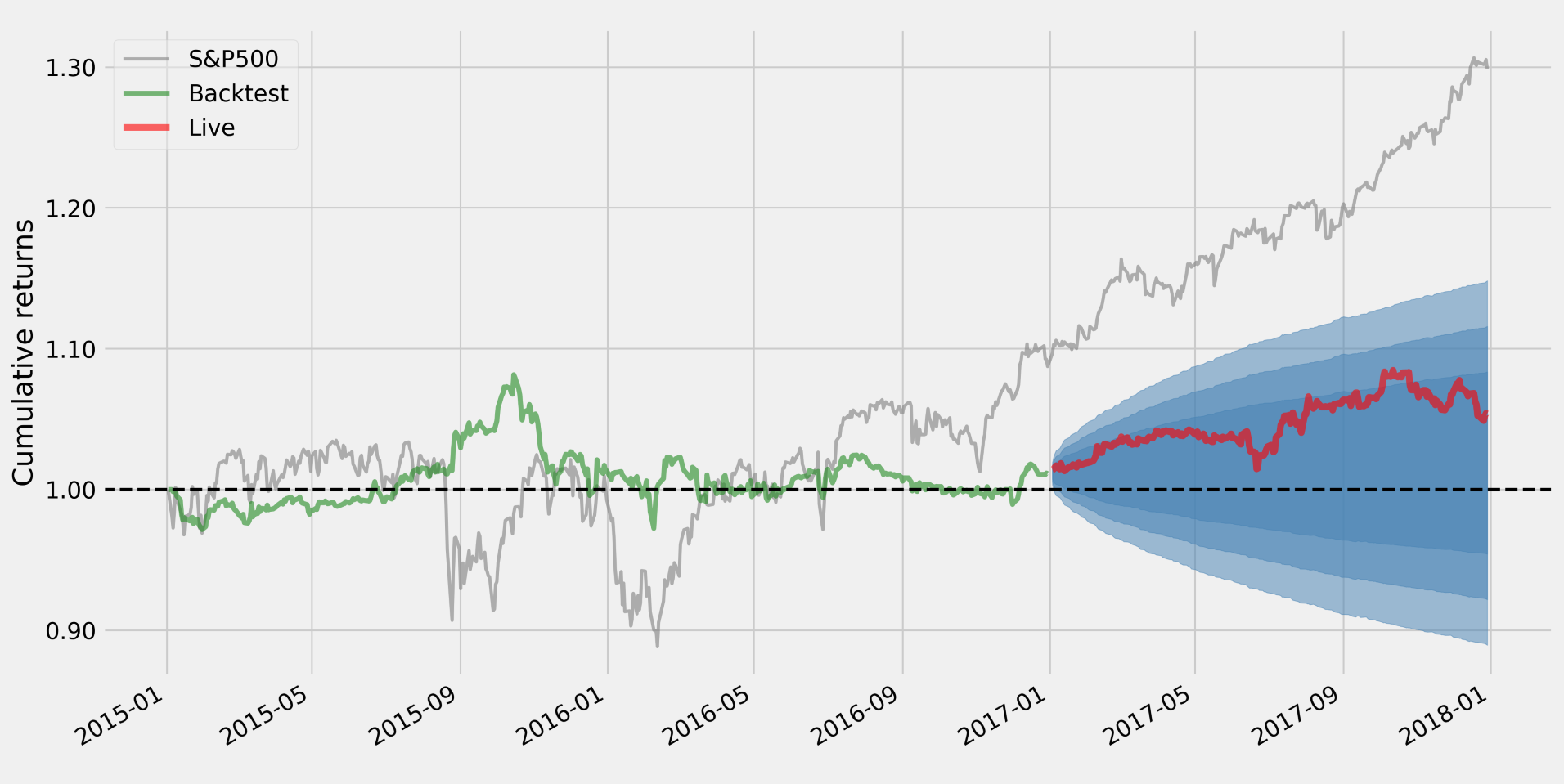

The plot_rolling_returns function displays cumulative in and out-of-sample returns against a user-defined benchmark (we are using the S&P 500):

from pyfolio.plotting import plot_rolling_returns

plot_rolling_returns(returns=returns,

factor_returns=benchmark_rets,

live_start_date='2017-01-01',

cone_std=(1.0, 1.5, 2.0))

The plot includes a cone that shows expanding confidence intervals to indicate when out-of-sample returns appear unlikely given random-walk assumptions. Here, our strategy did not perform well against the benchmark during the simulated 2017 out-of-sample period: