Another application of PCA involves the covariance matrix of the normalized returns. The principal components of the correlation matrix capture most of the covariation among assets in descending order and are mutually uncorrelated. Moreover, we can use standardized principal components as portfolio weights.

Let's use the 30 largest stocks with data for the 2010-2018 period to facilitate the exposition:

idx = pd.IndexSlice

with pd.HDFStore('../../data/assets.h5') as store:

stocks = store['us_equities/stocks'].marketcap.nlargest(30)

returns = (store['quandl/wiki/prices']

.loc[idx['2010': '2018', stocks.index], 'adj_close']

.unstack('ticker')

.pct_change())

We again winsorize and also normalize the returns:

normed_returns = scale(returns

.clip(lower=returns.quantile(q=.025),

upper=returns.quantile(q=.975),

axis=1)

.apply(lambda x: x.sub(x.mean()).div(x.std())))

After dropping assets and trading days as in the previous example, we are left with 23 assets and over 2,000 trading days. We estimate all principal components, and find that the two largest explain 55.9% and 15.5% of the covariation, respectively:

pca.fit(cov)

pd.Series(pca.explained_variance_ratio_).head()

0 55.91%

1 15.52%

2 5.36%

3 4.85%

4 3.32%

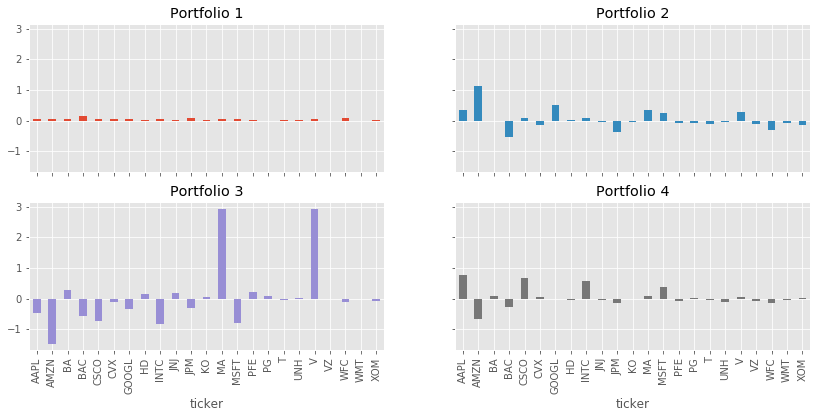

Next, we select and normalize the four largest components so that they sum to 1 and we can use them as weights for portfolios that we can compare to an equal-weighted portfolio formed from all stocks:

top4 = pd.DataFrame(pca.components_[:4], columns=cov.columns)

eigen_portfolios = top4.div(top4.sum(1), axis=0)

eigen_portfolios.index = [f'Portfolio {i}' for i in range(1, 5)]

The weights show distinct emphasis—for example, Portfolio 3 puts large weights on Mastercard and Visa, the two payment processors in the sample, whereas Portfolio 2 has more exposure to technology companies:

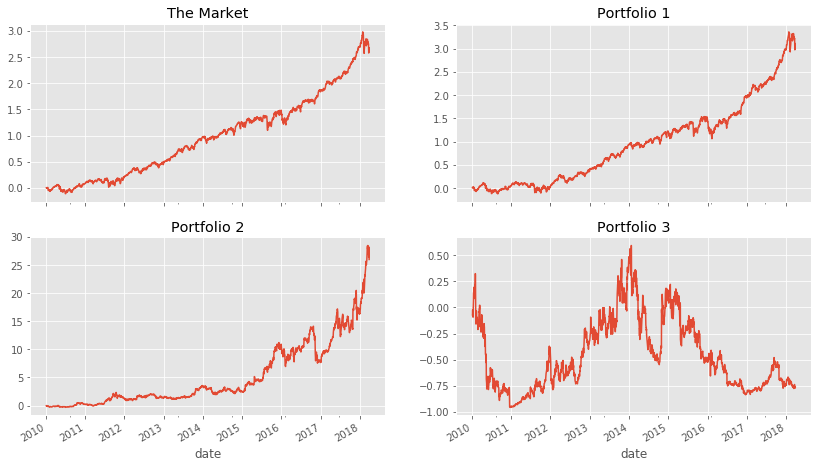

When comparing the performance of each portfolio over the sample period to The Market consisting of our small sample, we find that portfolio 1 performs very similarly, whereas the other portfolios capture different return patterns: